Endoluminal Suturing Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 122.65 Million |

| Market Size (2031) | USD 207.88 Million |

| Growth Rate (2026 - 2031) | 11.13% CAGR |

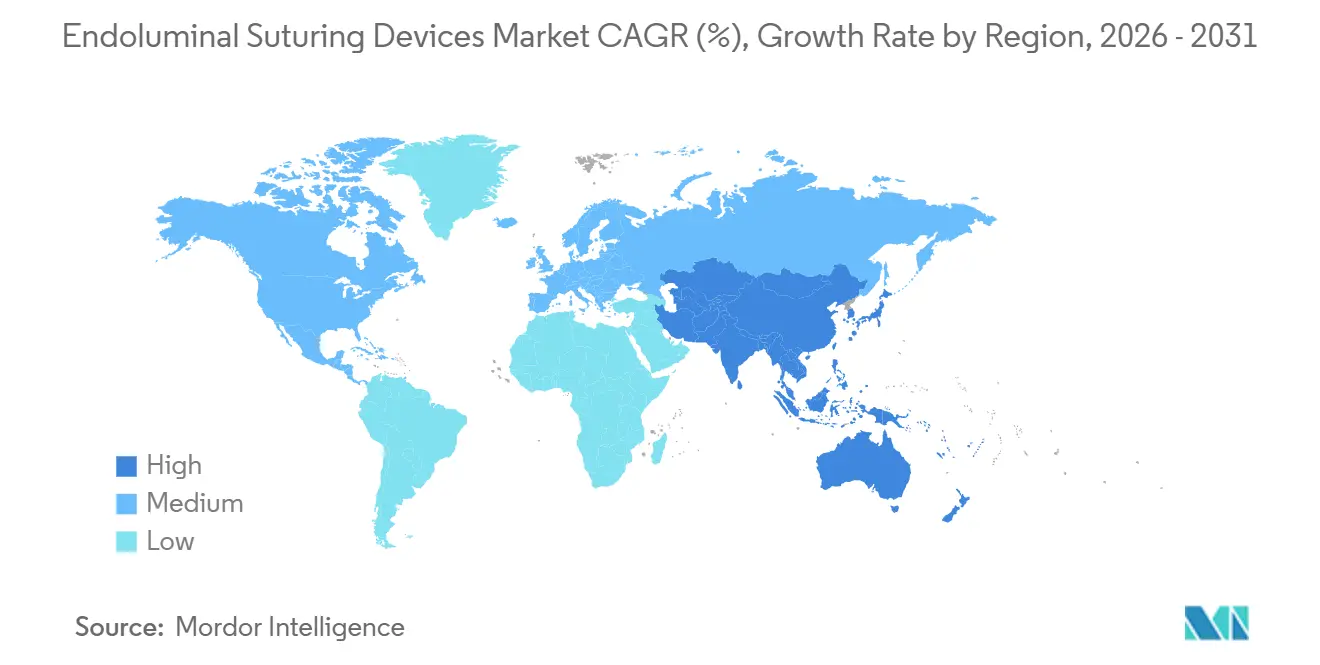

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

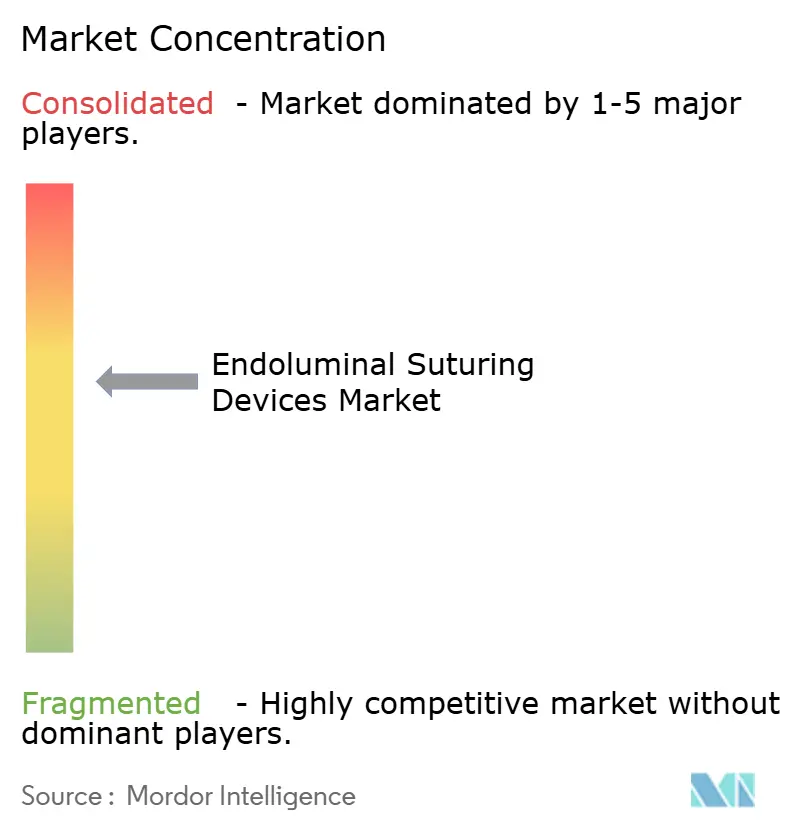

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoluminal Suturing Devices Market Analysis by Mordor Intelligence

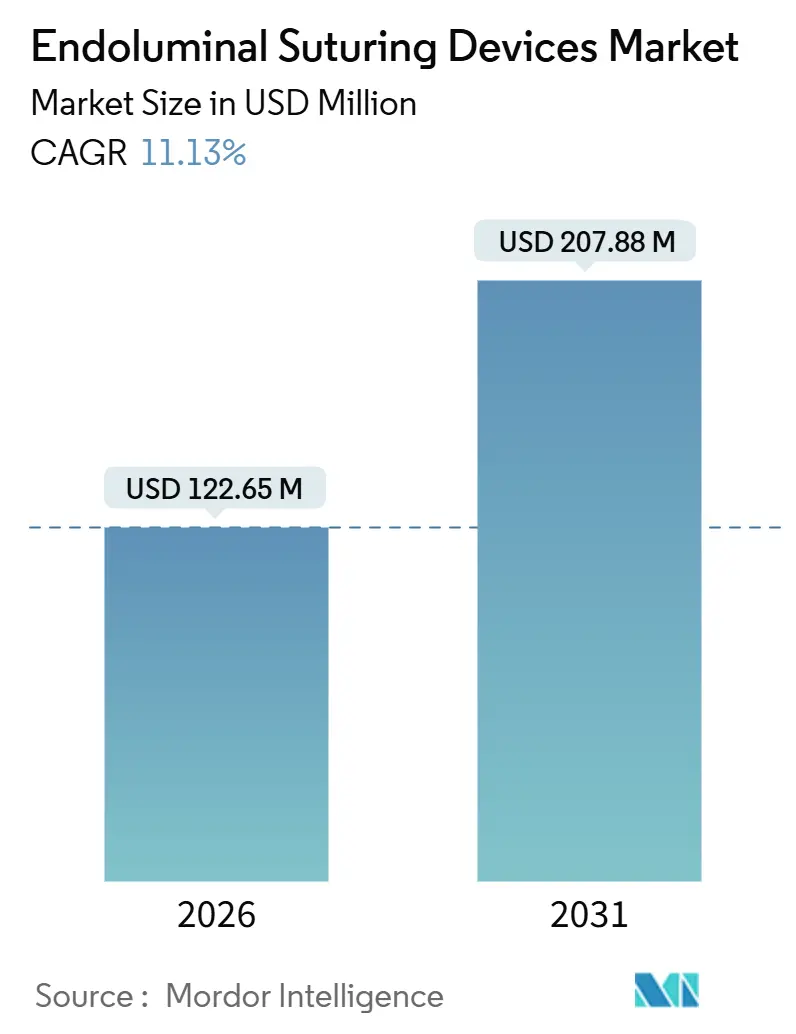

The Endoluminal Suturing Devices Market size is estimated at USD 122.65 million in 2026, and is expected to reach USD 207.88 million by 2031, at a CAGR of 11.13% during the forecast period (2026-2031).

Momentum stems from escalating obesity prevalence, health-system preference for incision-less care, and steady integration of robotic and artificial-intelligence guidance into suturing workflows. Disposable systems already dominate procedure rooms, automated platforms are rapidly scaling, and regulatory agencies have cleared multiple bariatric and anti-reflux indications in major regions, lowering adoption hurdles. Force-feedback robotics, cloud-based case logging, and AI-driven tissue recognition are compressing learning curves, while outpatient care models channel procedure volume from hospital operating suites to ambulatory centers. At the same time, reimbursement pathways remain patchy, pressure from GLP-1 pharmacotherapy looms, and bio-adhesive sealants introduce substitution risk, collectively shaping price discipline and margin strategy within the endoluminal suturing devices market.

Key Report Takeaways

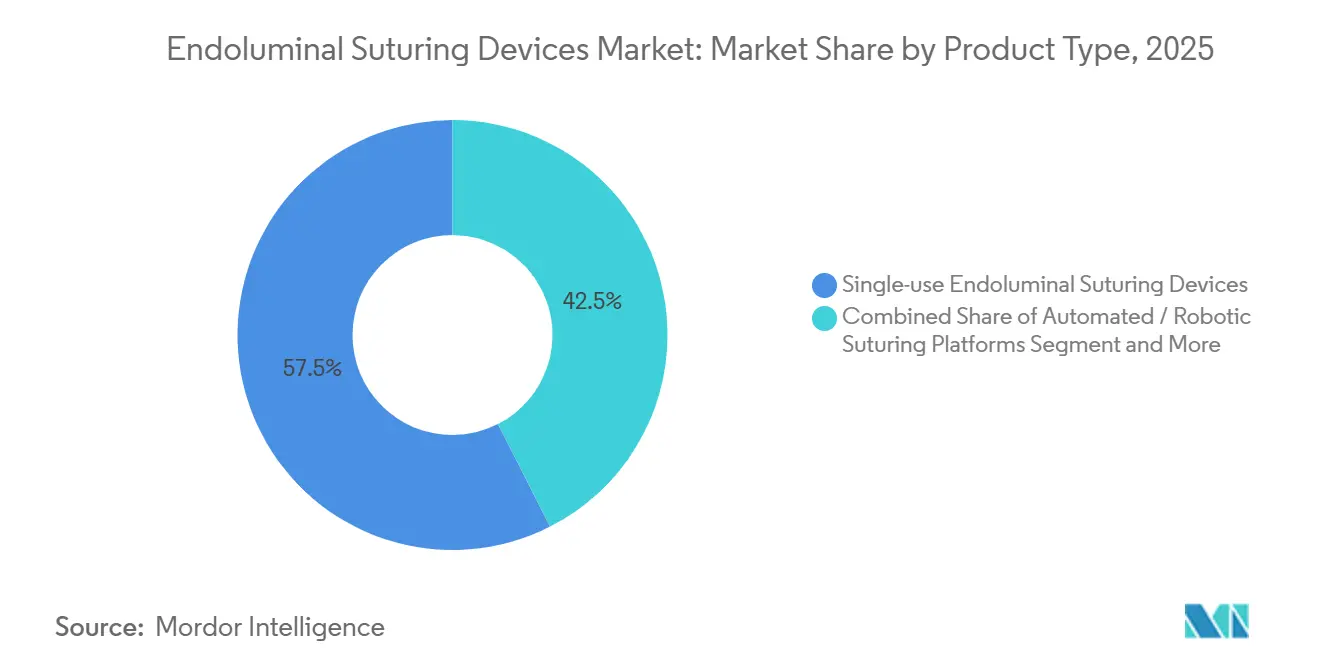

- By product category, single-use systems led with 57.55% of endoluminal suturing devices market share in 2025. Automated and robotic platforms are projected to expand at a 14.25% CAGR to 2031.

- By application, gastrointestinal surgery commanded a 44.53% share of the endoluminal suturing devices market size in 2025 and is advancing at an 11.13% CAGR through 2031. Gastroesophageal reflux disease procedures are forecast to grow at a 12.85% CAGR through 2031.

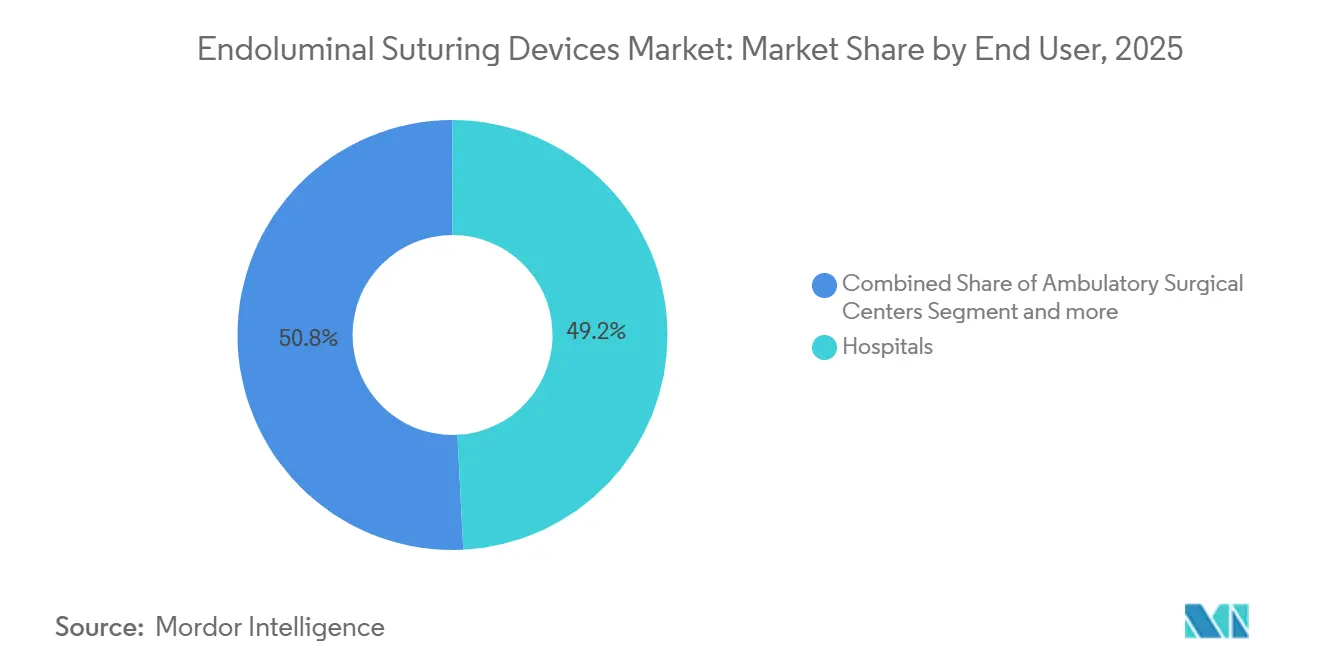

- By end user, hospitals held 49.23% revenue share in 2025, while ambulatory surgical centers recorded the highest projected CAGR at 12.55% through 2031.

- By geography, North America accounted for 41.25% of revenue in 2025; Asia-Pacific is poised for a 13.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endoluminal Suturing Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of obesity and GI disorders | +2.8% | Global, highest in North America, Middle East, Asia-Pacific cities | Medium term (2-4 years) |

| Growing adoption of minimally invasive endoscopy | +2.5% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Technological advances in robotics and AI | +2.2% | North America, Europe for R&D; Asia-Pacific for commercialization | Long term (≥ 4 years) |

| Favorable reimbursement for ESG and GERD endotherapy | +1.8% | North America, Europe | Medium term (2-4 years) |

| Surge in endoscopic revision of failed bariatric surgeries | +1.5% | North America, Europe, early Latin America | Medium term (2-4 years) |

| Outpatient ESG programs in retail health centers | +1.3% | North America, emerging Middle East, parts of Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Obesity and Gastrointestinal Disorders

Global obesity prevalence keeps climbing, producing a steady pipeline of candidates for endoscopic sleeve gastroplasty, transoral fundoplication, and defect-closure procedures. GERD affects roughly one in five adults in Western nations, and many patients seek alternatives to long-term proton-pump inhibitors, fueling procedure demand. In emerging regions, bariatric surgical capacity remains constrained, positioning the endoluminal suturing devices market as an essential bridge therapy. Coupled with chronic GI disorders such as bleeding ulcers and anastomotic leaks, the clinical addressable population is expanding faster than surgical workforce growth. Consequently, payers are studying five-year outcomes indicating durable weight loss and symptom resolution, tilting the benefit-risk calculus toward minimally invasive solutions.

Growing Adoption of Minimally Invasive Endoscopic Procedures

Endoscopic interventions are replacing open or laparoscopic bariatric operations for select patient groups because they shorten recovery, cut complication risk, and leave no external scars. The MERIT randomized trial reported a 13.1-percentage-point improvement in total body weight loss at 12 months with ESG compared to lifestyle therapy, while serious events remained near 2% and no surgical conversions occurred. Professional societies now back ESG for class I–II obesity, citing pooled analysis of more than 15,700 cases with only 1.25% serious events. Hospitals and ambulatory centers are retrofitting suites with dual-channel scopes, high-definition visualization, and advanced suturing systems. The American Society for Gastrointestinal Endoscopy’s STAR Fundamentals of Suturing course, launched in December 2025, is broadening the operator base[1]American Society for Gastrointestinal Endoscopy, “STAR Fundamentals of Suturing Course,” asge.org. Collectively, these trends accelerate procedure migration from operating rooms into flexible endoscopy units, lifting equipment utilization and strengthening the endoluminal suturing devices market.

Technological Advances in Robotics and AI-Guided Suturing

Robotic and AI-assisted platforms are turning technically demanding manual suturing into a digitally guided routine. The da Vinci 5 gained FDA clearance in March 2024, bringing force-feedback to end-effectors that could eventually improve full-thickness gastric plications[2]Intuitive Surgical, “Investor Relations and Product Updates,” intuitive.com. Olympus invested USD 65 million in Swan EndoSurgical in 2025 to develop a flexible robotic suite aiming at a USD 2 billion U.S. opportunity by 2040. KARL STORZ folded Asensus Surgical’s Senhance and LUNA assets into its program in 2024, accelerating performance-guided surgery capabilities. Boston Scientific followed with the OverStitch NXT, adding physician-controlled retractors and better articulation. Early data show these upgrades can shorten procedure times, lower the learning curve, and open new anatomical targets, reinforcing double-digit growth prospects for the endoluminal suturing devices market.

Favorable Reimbursement for ESG and GERD Endotherapy

Economic evidence is convincing payers that endoluminal approaches save money over medication in appropriate patients. A 2024 JAMA analysis found ESG saved USD 33,583 per patient over five years versus semaglutide if the drug stayed at listed prices. Medicare already reimburses transoral incisionless fundoplication under defined criteria, bolstering procedure economics. European health systems reimburse ESG within structured obesity pathways, pushing volumes across Germany, France, and the Nordics. Even so, payer heterogeneity persists; BCBS Rhode Island labeled transoral therapies “not medically necessary” in 2025, illustrating variability that can blunt momentum. Sustained publication of 10-year durability data and head-to-head comparisons with medical therapy will be decisive for long-term market expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and procedural cost | −1.2% | Global, most acute in emerging markets and low-volume centers | Short term (≤ 2 years) |

| Limited pool of skilled operators | −0.9% | Global, especially Asia-Pacific and Latin America | Medium term (2-4 years) |

| Metal-alloy tariff shocks | −0.6% | North America and Europe | Short term (≤ 2 years) |

| Shift toward bio-adhesive closure | −0.7% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Procedural Cost of Advanced Systems

An OverStitch console must be paired with specialized endoscopes, while each case typically consumes multiple disposable helixes, cinches, and sutures that can push per-procedure supply costs beyond USD 1,000. Emerging markets and low-volume ambulatory centers find such outlays prohibitive. Manufacturers face rising sterilization compliance fees as the U.S. Environmental Protection Agency tightens ethylene-oxide rules, potentially inflating costs for reprocessed accessories. Medtronic disclosed stapling category price pressure in fiscal 2025, highlighting intensifying competition that constrains pricing flexibility[3]Medtronic, “FY25 Earnings Presentation,” medtronic.com. To defend share, vendors negotiate bundled pricing and volume-based rebates, yet the capital hurdle still slows new program launches and tempers expansion of the endoluminal suturing devices market.

Limited Pool of Skilled Endoscopic Suturing Operators

Advanced suturing demands both cognitive and manual dexterity. Global training programs historically centered on diagnostic rather than therapeutic endoscopy, leaving many regions short of credentialed operators. ASGE’s STAR course addresses the gap in the United States, but Asia-Pacific and Latin America still lag in simulation centers and proctorships. Specialty fragmentation compounds the problem; gastroenterologists, not surgeons, perform most ESG cases, causing under-representation in surgical registries and limiting peer-to-peer diffusion. KARL STORZ’s acquisition of Asensus aims to embed haptic feedback and step-wise guidance into devices, lowering the learning threshold. Until those platforms achieve broad rollout, operator scarcity will cap procedure volumes in many hospitals, restraining the endoluminal suturing devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Single-Use Dominance Amid Robotic Platform Acceleration

Single-use devices captured 57.55% of 2025 revenue, reflecting hospital infection-control rules that discourage reprocessing and a manufacturer pivot toward predictable consumable streams. Disposable helixes, cinches, and cartridges often account for most per-case spend and underpin attractive gross margins within the endoluminal suturing devices market. Reusable consoles face sterilization bottlenecks as EPA rules tighten ethylene-oxide emissions, raising compliance costs and nudging buyers toward disposables or semi-automated kits.

Parallel to this consumable upswing, fully automated and robotic suites are charting the fastest growth, with a projected 14.25% CAGR through 2031, as Olympus-Swan and KARL STORZ-Asensus alliances funnel capital into force-feedback actuators and vision-guided stapling. Boston Scientific’s OverStitch NXT shows how incremental enhancements—an auxiliary irrigation channel and larger plication bites—extend the life of manual platforms while the market digests premium robotic options. Emerging through-the-scope devices such as EndoZip promise lower capital thresholds by eliminating external consoles, potentially expanding addressable sites among community hospitals and ambulatory centers. Over the forecast horizon, product segmentation is likely to stratify into premium robotics, mid-range semi-automated scopes, and cost-conscious single-use kits, each aiming at distinct volume bands and case-complexity tiers in the endoluminal suturing devices market.

By Application: Gastrointestinal Surgery Leads as GERD Procedures Accelerate

Gastrointestinal surgery procedures—including endoscopic sleeve gastroplasty, defect closure, and revisional outlet reduction—generated 44.53% of revenue in 2025 and continue to anchor the endoluminal suturing devices market size. Bariatric centers gravitate toward suturing because it enables durable gastric remodeling with fewer complications than stapling. Meanwhile, GERD interventions are on a steeper 12.85% CAGR trajectory, buoyed by five-year TEMPO data showing 86% regurgitation elimination and payer coverage expansions for transoral fundoplication.

Commercial payers remain mixed; BCBS Rhode Island’s 2025 denial contrasts with Medicare’s defined coverage, but growing registry evidence—94% clinical success and 72% acid-exposure normalization—strengthens the reimbursement case. Elsewhere, bleeding control, anastomotic leak repair, and post-ESD mucosal closure offer incremental growth pockets where sutures compete head-to-head with clips and sealants. Overall, the application mix is shifting toward GERD and revision heavy caseloads, yet bariatric sleeve applications will sustain leadership through 2031, supporting volume resilience across diverse care settings within the endoluminal suturing devices market.

By End User: Hospitals Retain Share as Ambulatory Centers Gain Momentum

Hospitals maintained 49.23% of global revenue in 2025 thanks to established bariatric programs, multidisciplinary teams, and capital budget cycles aligned with device acquisition. Nevertheless, ambulatory surgical centers (ASCs) are pacing at a 12.55% CAGR, fueled by site-neutral Medicare payments and patient preference for same-day discharge. ASCs leverage lower facility fees and simplified scheduling to attract ESG and fundoplication patients, amplifying device turnover.

Specialty clinics and retail health providers are layering concierge nutrition support and transparent bundle pricing onto ESG offerings, further decentralizing patient flow from tertiary centers. Research institutes, though small in revenue, remain vital for multicenter trials that validate next-gen robotics and AI guidance. Over the forecast window, hospitals will still lead complex revision and full-thickness cases, but ASCs will outpace them in volume growth, diversifying the customer base for the endoluminal suturing devices market.

Geography Analysis

North America generated 41.25% of 2025 revenue, benefiting from early FDA clearances, extensive bariatric-endoscopy training networks, and Medicare reimbursement for select anti-reflux and bariatric procedures. The region’s health systems have the infrastructure to integrate robotics rapidly, and strategic acquisitions—such as KARL STORZ-Asensus—bolster technology pipelines that will feed future adoption. Yet Asia-Pacific is on track for a 13.21% CAGR through 2031. China’s National Medical Products Administration cleared Intuitive’s Ion system in 2024, and Japanese regulators approved multiple suturing accessories in 2025, positioning regional endoscopy leaders to localize Western platforms.

Rising middle-class demand for metabolic surgery, combined with hospital partnerships that co-develop training curricula, accelerates uptake. Europe, while modest in headline growth, maintains a solid installed base, supported by unified technical guidance from ESGE and state-funded reimbursement across Germany, France, and the Nordics. Central and Eastern European markets add upside as they adopt ESG within national obesity strategies. Latin America and the Middle East present mixed pictures; private payers drive premium uptake in the Gulf Cooperation Council, whereas public budgets in Brazil and Mexico restrict volume to high-income urban areas. Overall, the geography mix will tilt gradually toward Asia-Pacific without dislodging North America from revenue leadership, ensuring a balanced demand profile for the endoluminal suturing devices market.

Competitive Landscape

The endoluminal suturing devices market is moderately concentrated. Boston Scientific’s OverStitch and Apollo Endosurgery’s suite still dominate routine caseloads, but share is eroding as multinationals deploy robotics to differentiate on ease of use. Olympus’s 2025 investment in Swan EndoSurgical wagers on capturing a projected USD 2 billion U.S. robotics niche by 2040, capitalizing on the company’s 70% global scope share to seed upgrades across its fleet. KARL STORZ integrated Senhance’s haptics with its visualization systems, creating a performance-guided stack targeting both surgical theaters and endoscopy rooms. Intuitive’s da Vinci 5 adds tactile sensing that could cross over to flexible endoscopy, while the firm’s Ion platform logged nearly 100,000 procedures globally in 2024, validating demand for robotic endoluminal workflows.

Disruptors such as EndoQuest and Nitinotes are testing automated suturing systems that promise shorter procedure times and flatter learning curves, though they must prove durability in multicenter IDE trials. Bio-adhesive entrants like Ethicon’s VISTASEAL nibble at low-complexity closure use cases, keeping incumbents vigilant. Strategic alliances—KARL STORZ with Fujifilm to co-market scopes and integration software—underscore the shift toward ecosystem selling rather than stand-alone devices. Over the next five years, incumbents will seek to lock in customers through multi-year fleet contracts, software subscriptions, and cloud data analytics, while new entrants leverage cost innovation or niche indications to wedge into the endoluminal suturing devices market.

Endoluminal Suturing Devices Industry Leaders

Boston Scientific Corporation

Medtronic plc

Apollo Endosurgery Inc.

Johnson & Johnson (Ethicon)

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Nitinotes treated the first U.S. patient in its IDE EASE Trial evaluating the EndoZip Automated Suturing System for ESG at Lenox Hill Hospital, New York.

- September 2025: EndoQuest Robotics completed the first gastroenterologist-led procedure in the PARADIGM Trial assessing its Endoluminal Surgical System for lower-GI applications.

Global Endoluminal Suturing Devices Market Report Scope

As per the scope of the report, endoluminal suturing devices are specialized medical tools designed to facilitate suturing (stitching) inside the lumen of tubular structures within the body, such as the gastrointestinal tract or blood vessels, using minimally invasive endoscopic techniques. These devices enable precise tissue approximation and closure during endoscopic procedures, reducing the need for open surgery.

The segmentation for the endoluminal suturing devices market is categorized by product type, application, end user, and geography. By product type, the market includes single-use endoluminal suturing devices, reusable endoluminal suturing devices, disposable components, and automated/robotic suturing platforms. By application, it covers bariatric surgery, gastrointestinal surgery, GERD procedures, and other therapeutic procedures. By end user, the segmentation includes hospitals, ambulatory surgical centers, specialty clinics, and research institutes. By geography, the market is divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The Market Forecasts are Provided in Terms of Value (USD).

| Single-use Endoluminal Suturing Devices |

| Reusable Endoluminal Suturing Devices |

| Disposable Components |

| Automated / Robotic Suturing Platforms |

| Bariatric Surgery |

| Gastrointestinal Surgery |

| GERD Procedures |

| Other Therapeutic Procedures |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Single-use Endoluminal Suturing Devices | |

| Reusable Endoluminal Suturing Devices | ||

| Disposable Components | ||

| Automated / Robotic Suturing Platforms | ||

| By Application | Bariatric Surgery | |

| Gastrointestinal Surgery | ||

| GERD Procedures | ||

| Other Therapeutic Procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the endoluminal suturing devices market in 2026?

The endoluminal suturing devices market size reached USD 122.65 million in 2026 and is forecast to grow at an 11.13% CAGR to 2031.

Which product type holds the largest share?

Single-use systems led with 57.55% revenue share in 2025, driven by hospital infection-control mandates.

What is the fastest growing application?

Gastroesophageal reflux disease procedures are projected to expand at a 12.85% CAGR between 2026 and 2031.

Why are ambulatory surgical centers gaining traction?

ASCs benefit from site-neutral reimbursement, same-day discharge models, and lower facility fees that attract ESG patients.

Which region will add the most incremental revenue by 2031?

Asia-Pacific, supported by double-digit growth in China and Japan, is expected to contribute the largest share of new revenue.

What technologies are shaping future growth?

Force-feedback robotics, AI-guided tissue capture, and cloud-based analytics are lowering skill barriers and expanding indications.

Page last updated on: