Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 42.73 Billion |

| Market Size (2031) | USD 58.71 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

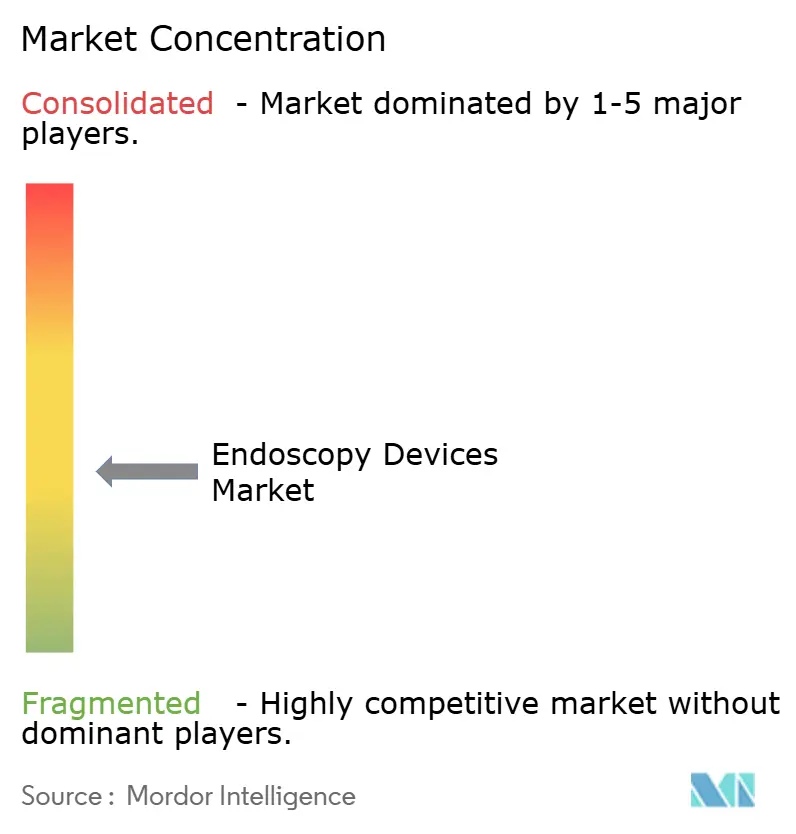

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoscopy Devices Market Analysis by Mordor Intelligence

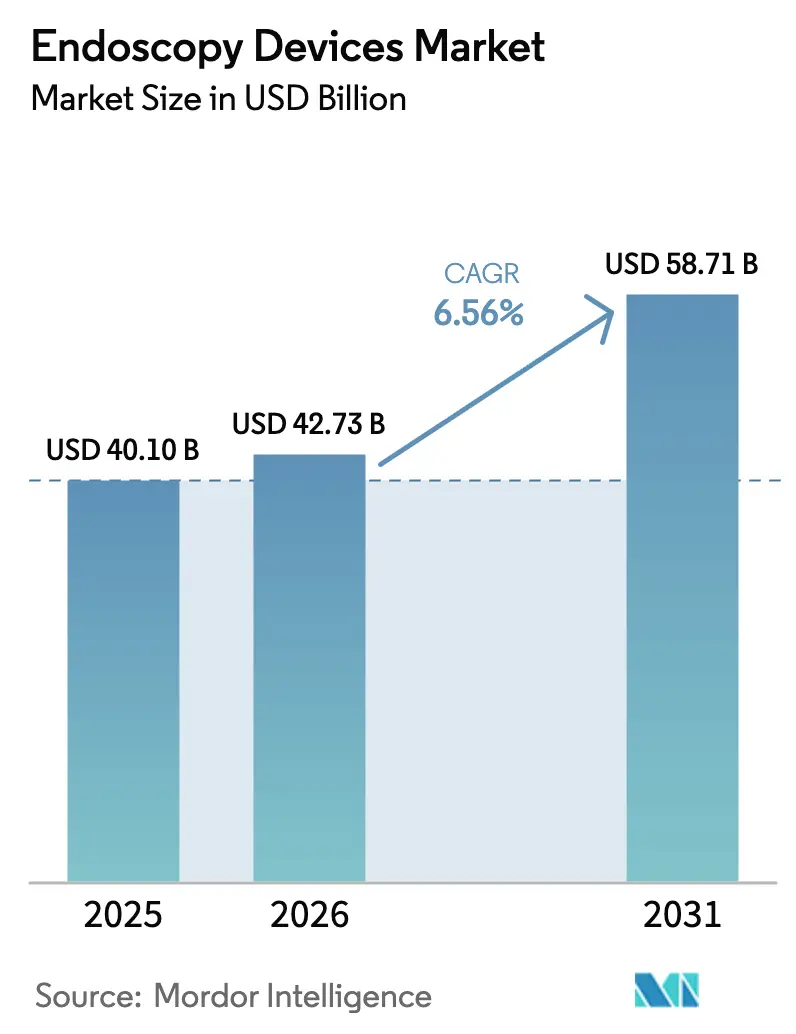

The Endoscopy Devices Market size is projected to expand from USD 40.10 billion in 2025 and USD 42.73 billion in 2026 to USD 58.71 billion by 2031, registering a CAGR of 6.56% between 2026 to 2031.

Growth stems from Medicare’s 2024 decision to remove cost-sharing for screening colonoscopies, rapid upgrades to 4K visualization towers, and faster adoption of artificial-intelligence guidance that boosts adenoma detection rates. Hospitals are shortening replacement cycles for aging platforms, while ambulatory surgical centers (ASCs) scale purchases of compact integrated systems that fit single-specialty footprints. Tight infection-control standards, especially after 12 separate U.S. Food and Drug Administration (FDA) safety communications between 2024 and 2026, are tilting procurement toward single-use scopes despite higher per-procedure costs. Meanwhile, emerging reimbursement schemes in China, India, and Japan are expanding the addressable patient base, cementing long-term volume visibility across both diagnostic and therapeutic procedures.

Key Report Takeaways

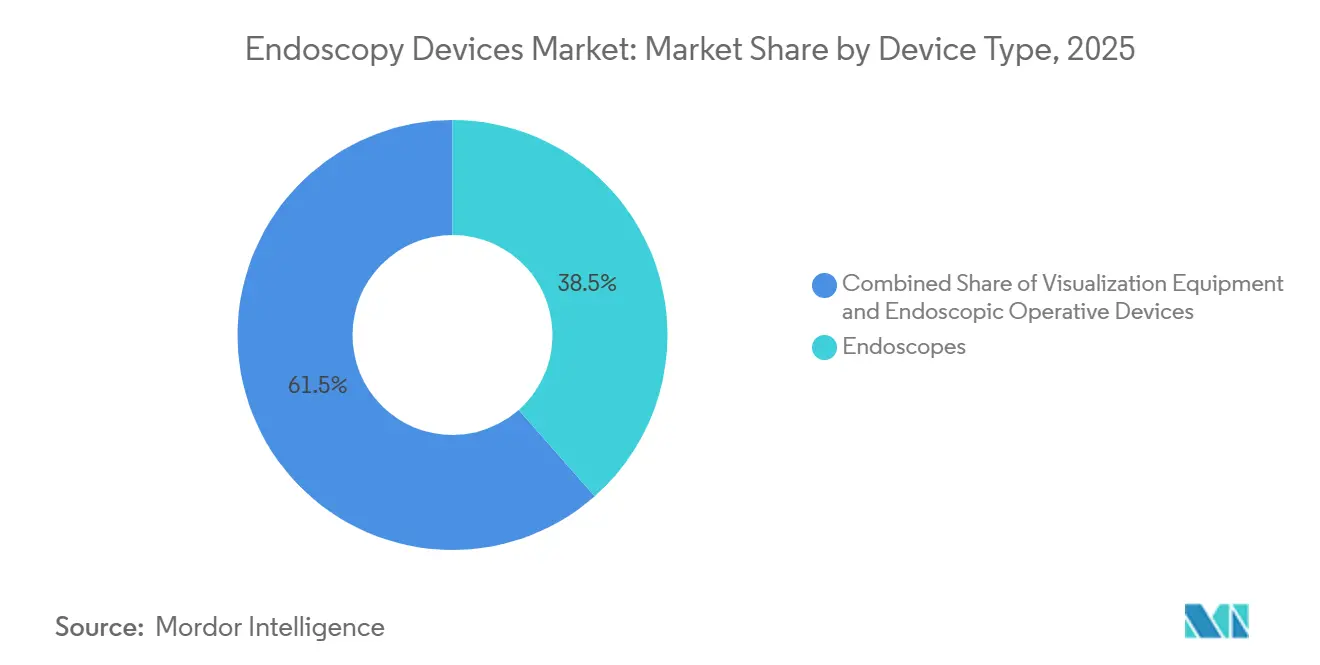

- By device type, visualization equipment accounted for the fastest growth, advancing at an 8.25% CAGR through 2031 as hospitals and ASCs swapped standard-definition platforms for AI-ready 4K systems.

- By application, gastrointestinal endoscopy led with 55.53% of 2025 revenue, while laparoscopy registered the steepest expansion, rising at an 8.85% CAGR on the back of robotic-assisted oncologic procedures.

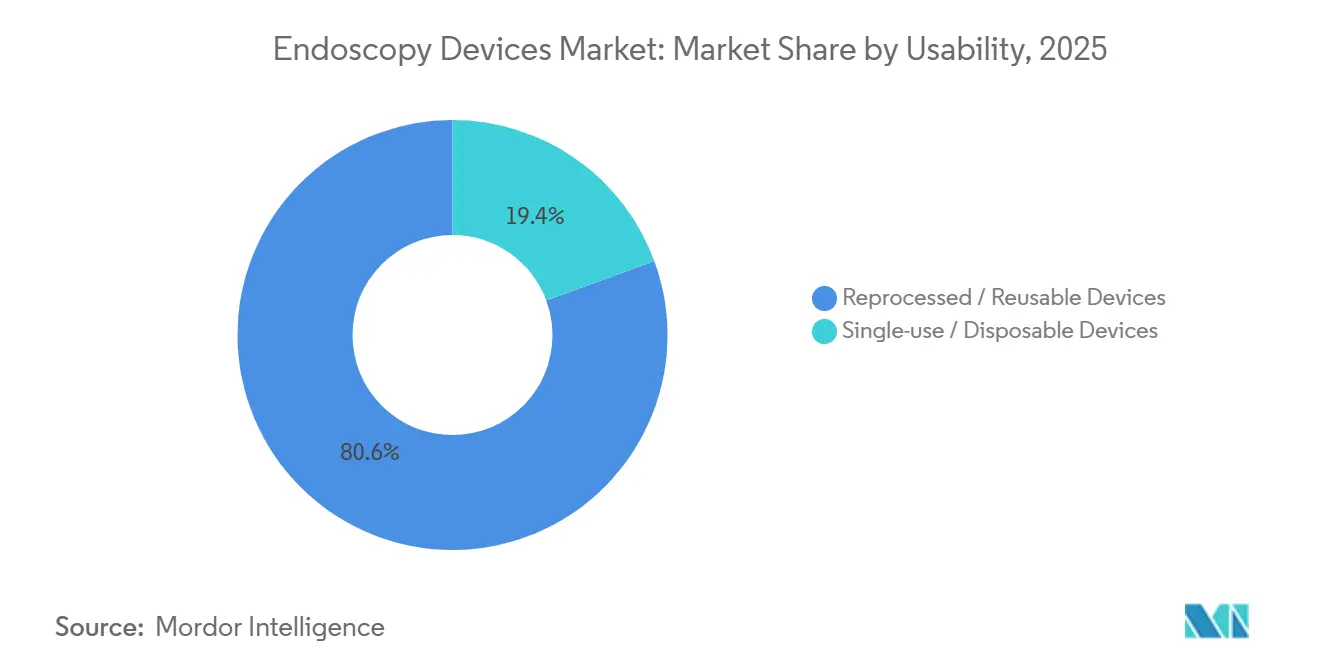

- By usability, reprocessed products retained 80.63% share in 2025, yet single-use scopes are on track for a 10.87% CAGR, propelled by infection-control mandates that followed repeated contamination alerts.

- By end-user, ASCs captured the highest growth, recording a 9.7% CAGR through 2031 as site-neutral payment reforms shifted procedure volumes out of hospitals.

- By geography, North America accounted for 41.13% of 2025 revenue, while Asia-Pacific is projected to advance at an 8.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Incidence of Gastrointestinal & Colorectal Cancers | +1.2% | Global, peak in North America & Europe | Medium term (2-4 years) |

| Widespread Shift Toward Minimally Invasive Procedures | +1.1% | Global, led by North America & Asia-Pacific | Long term (≥ 4 years) |

| Continuous Innovation in Endoscopy Visualization | +0.9% | North America, Europe, Japan | Short term (≤ 2 years) |

| Expansion of Ambulatory Surgical Centers | +0.8% | North America, spillover to Europe | Medium term (2-4 years) |

| Favorable Reimbursement & Public-Health Programs | +0.7% | North America, Europe, China, India | Medium term (2-4 years) |

| Aging Population with Chronic Conditions | +0.6% | Global, concentrated in North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence of Gastrointestinal & Colorectal Cancers Driving Screening Demand

Colorectal cancer cases among U.S. adults aged 20-49 increased 9% between 2020 and 2024, prompting payers to broaden screening eligibility to younger cohorts[1]American Cancer Society, “Colorectal Cancer Statistics 2024,” cancer.org. Endoscopy fleets therefore require faster refresh cycles, with high-volume centers acquiring high-definition (HD) colonoscopes that better visualize flat or depressed lesions responsible for 30% of interval cancers. Japan and South Korea illustrate the effect of mandatory screening: per-capita endoscope utilization runs three to four times higher than in Western systems, demonstrating the procedure volume that emerging Chinese and Indian programs could unleash. The World Health Organization’s 2024 cancer outlook projects a 47% rise in global cancer incidence by 2040, spotlighting gastrointestinal malignancies as the largest absolute increase. Regulators are also tightening quality standards; updated ISO 13485 audits link device performance directly to documented cancer-detection rates, raising the entry hurdle for new vendors.

Widespread Shift Toward Minimally Invasive Procedures Across Surgical Specialties

Minimally invasive techniques now represent 72% of elective abdominal surgeries in the United States, up from 64% in 2020[2]Agency for Healthcare Research and Quality, “HCUP Trends 2024,” ahrq.gov. Bariatric endoscopic sleeve gastroplasty volumes jumped 38% in 2024 as shortages of GLP-1 agonists steered patients from pharmacotherapy to procedural weight management. Orthopedic arthroscopy follows a similar trajectory, with 85% of U.S. meniscus repairs completed arthroscopically in 2024. Robotic bronchoscopy platforms such as Intuitive Surgical’s Ion, cleared in 2024, reached an 89% diagnostic yield for sub-2 cm lung nodules, underscoring how flexible-scope technology increasingly merges with robotics. This broad procedural pivot expands the endoscopy devices market well beyond gastroenterology, opening white-space opportunities for hybrid visualization systems that blend rigid-scope precision with flexible-scope reach.

Continuous Innovation in Endoscopy Visualization Enhancing Clinical Outcomes

Between 2024 and 2026, the FDA cleared 14 artificial-intelligence (AI) colonoscopy systems, each embedding real-time polyp-detection software that lifts adenoma detection rates by 8-12 percentage points. Fujifilm’s CAD EYE, integrated into the ELUXEO 8000 platform, uses linked-color imaging to highlight vascular patterns linked to neoplasia. Olympus’s EVIS X1 achieved 97% sensitivity for Barrett’s esophagus dysplasia in a 2024 multicenter trial, outperforming white-light endoscopy by 14 percentage points. Karl Storz’s IMAGE1 S 4K system provides 8.3-megapixel resolution that helps surgeons identify nerve bundles during laparoscopic prostatectomy, reducing incontinence by 18%. Capsule solutions are also advancing; Medtronic’s PillCam, cleared in 2024 for Crohn’s disease monitoring, offers a non-invasive alternative to repeat ileocolonoscopy. These innovations shorten average colonoscopy time from 28 minutes to 22 minutes, allowing centers to raise daily throughput without extra staff.

Expansion of Ambulatory Surgical Centers Boosting Outpatient Endoscopy Volumes

ASCs completed 9.2 million U.S. GI endoscopies in 2024, a 14% jump since 2020, after Medicare’s 2024 site-neutral payment rule equalized reimbursement with hospital outpatient departments. Removing colonoscopy from the inpatient-only list opened another 2.3 million annual procedures to ASCs. Colonoscopy now costs Medicare USD 1,068 in an ASC versus USD 1,783 in a hospital outpatient department, a 40% savings that commercial plans replicate through preferred ASC networks. Twelve states scrapped certificate-of-need barriers between 2024 and 2026, with Florida, Texas, and Arizona hosting 38% of new centers. Compact integrated towers such as Olympus’s EVIS X1 Compact meet the footprint and budget constraints of these facilities. Similar outpatient growth is emerging in Japan and Germany after payers in both countries approved stand-alone ambulatory endoscopy clinics in 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Lifecycle Maintenance Costs | -0.9% | Global, acute in emerging markets | Medium term (2-4 years) |

| Persistent Infection-Control Challenges | -0.7% | Global, focused in North America & Europe | Short term (≤ 2 years) |

| Global Shortage of Trained Endoscopists | -0.5% | Global, severe in North America & Asia-Pacific | Long term (≥ 4 years) |

| Lengthy, Stringent Regulatory Approvals | -0.4% | North America, Europe, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Lifecycle Maintenance Costs of Advanced Endoscopic Systems

A fully integrated 4K tower with AI software lists between USD 180,000 and USD 250,000, about 60% higher than standard-definition rigs—a hurdle for community hospitals and ASCs with thin margins. Automated endoscope reprocessors (AERs), mandated by FDA and CDC protocols, cost USD 40,000-75,000 apiece, while high-level disinfectants add USD 12-18 per scope cycle[3]Centers for Disease Control and Prevention, “HAI Outbreaks Linked to Endoscopes 2024,” cdc.gov. Total annual ownership of a reusable colonoscope averages USD 2,800 when maintenance, servicing, and reprocessing are included. Disposable scopes eliminate reprocessing costs but introduce a USD 200-400 per-case expense, limiting viability to low-volume or high-infection-risk settings. Emerging-market budgets remain tight; typical Indian public hospitals earmark USD 25,000 per year for endoscopy equipment, adequate for only a single mid-tier flexible scope. Leasing models that bundle capital, maintenance, and consumables into per-procedure fees are growing in Europe but still cover less than 5% of installed systems.

Persistent Infection-Control Challenges and Heightened Regulatory Scrutiny

The FDA issued 12 separate flexible-scope contamination alerts from 2024 to 2026, including a Class I recall of Olympus’s TJF-Q190V duodenoscope after 18 confirmed carbapenem-resistant Enterobacteriaceae infections. The Centers for Disease Control and Prevention (CDC) connected 47 healthcare-associated outbreaks in 2024 to improper endoscope reprocessing, with duodenoscopes and echoendoscopes implicated in 68% of cases. New FDA rules obligate manufacturers to conduct post-market surveillance on all flexible scopes with reusable components. Europe’s Medical Device Regulation (MDR) upgraded flexible endoscopes from Class IIa to Class IIb in 2024, requiring clinical proof of reprocessing efficacy plus third-party audits. Compliance costs are rising: Olympus disclosed USD 120 million in incremental regulatory spending for 2024, while smaller firms are exiting the reusable-scope market entirely. Single-use adoption spiked after the FDA recommended disposable duodenoscopes for high-risk ERCP cases, pushing penetration to 22% of such procedures by late 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Visualization Leads Innovation Race

Visualization equipment expanded at an 8.25% CAGR between 2026 and 2031, the fastest among all device categories. The segment’s momentum reflects hospital demand for 4K and AI-ready towers like Olympus’s EVIS X1 and Fujifilm’s ELUXEO 8000, both cleared in 2024, which cut adenoma miss rates by up to 14 percentage points. Endoscopes retained 38.55% of 2025 revenue, with flexible variants dominating gastroenterology and pulmonology. Capsule endoscopes, led by Medtronic’s PillCam, carved a niche in small-bowel imaging and Crohn’s disease surveillance. Robotic-compatible visualization, exemplified by Intuitive’s Ion bronchoscope, blends flexible reach with robotic precision, underpinning 89% diagnostic yields in peripheral lung biopsies.

Manual instruments such as snares and forceps are commoditizing as Asian suppliers exert price pressure, yet high-margin digital visualization suites offset the squeeze. Karl Storz’s IMAGE1 S 4K system supports nerve-sparing prostatectomy, demonstrating the clinical lift associated with ultra-high resolution. As a result, visualization commanded the largest slice of incremental revenue in the endoscopy devices market. Hybrid 4K/HD portfolios cater to budget-sensitive geographies where reimbursement remains inadequate for premium hardware, extending the replacement opportunity curve.

By Application: Laparoscopy Surges on Robotic Adoption

Gastrointestinal endoscopy held a commanding 55.53% share in 2025, driven by more than 19 million annual colonoscopies in the United States alone. Yet laparoscopy clocked the swiftest growth at an 8.85% CAGR through 2031 as robotic platforms reduced surgeon fatigue and enabled single-port appendectomies and cholecystectomies. Intuitive Surgical’s da Vinci SP, cleared for transoral applications in 2024, illustrates the convergence of rigid and flexible modalities under a robotic umbrella. Pulmonology accelerates too: the U.S. Preventive Services Task Force’s 2024 guidelines expanded lung-cancer screening eligibility, adding 6.4 million candidates and fueling adoption of robotic bronchoscopy systems.

ENT, urology, and gynecology procedures continue to benefit from HD imaging upgrades, while neurology endoscopy gains attention for hydrocephalus management via single-burr-hole techniques. Orthopedics remains mature but innovates through augmented-reality overlays that guide ligament reconstruction, a feature Smith & Nephew commercialized in its 4K arthroscopy suite in 2024. The breadth of clinical indications ultimately broadens the total addressable endoscopy devices market, insulating revenue streams from single-specialty slowdowns.

By Usability: Single-Use Gains Despite Cost Premium

Single-use and disposable scopes are set to grow at a 10.87% CAGR, outpacing reusable platforms as infection-control mandates intensify. Ambu’s disposable bronchoscopes and duodenoscopes, cleared in 2024 and 2025, remove reprocessing workflows and slash turnaround time from 45 minutes to zero. Boston Scientific priced its EXALT Model D duodenoscope at USD 1,850, about 40% above reusable per-procedure costs but attractive for low-volume centers.

Reusable systems still dominate because Olympus’s EVIS X1 delivers 1.25 million-pixel resolution that disposable rivals cannot yet match. Hybrid models such as Pentax’s single-use forceps paired with reusable scopes offer a middle path that contains infection risk without forfeiting image quality. Environmental pressure is the main counterweight, as disposable scopes generate 3.2 times more plastic waste per case.

By End-User: ASCs Capture Outpatient Migration

ASCs registered a 9.7% CAGR through 2031, the fastest among end-users, after Medicare’s 2024 reforms removed site-of-service payment gaps. Hospital and academic centers still accounted for 42.13% of 2025 revenue, retaining complex ERCP and endoscopic submucosal dissection cases that demand surgical backup. Specialty clinics proliferate in Japan and Germany, where 2024 reimbursement updates recognized standalone endoscopy centers. Private-equity consolidation among U.S. ASCs continues, with platforms like Surgery Partners acquiring 47 GI-focused centers in 2024 to negotiate 15-20% capital equipment discounts. In emerging markets, reimbursement hurdles still tether procedure volumes to hospital settings, slowing the outpatient shift.

Geographical Analysis

North America held 41.13% of 2025 revenue due to Medicare’s elimination of cost-sharing for screening colonoscopies in 2024, which expanded the screening pool by 19 million people. ASCs performed 9.2 million GI endoscopies in 2024, consolidating their role as the primary outpatient site. Canada’s pilot of AI-assisted colonoscopy in Ontario and British Columbia improved adenoma detection by 11%, a catalyst for countrywide rollout. Mexico broadened coverage to an additional 8.2 million beneficiaries through the Instituto Mexicano del Seguro Social in 2024.

Asia-Pacific will post the fastest regional expansion with an 8.51% CAGR through 2031. China’s National Healthcare Security Administration extended endoscopy reimbursements to 95% of urban residents in 2025, while India’s Ayushman Bharat added upper-GI screening for high-risk groups. Japan’s 2024 decision to pay for AI-assisted colonoscopy accelerated the domestic shift to CAD EYE-enabled platforms. Australia started reimbursing capsule endoscopy for Crohn’s disease and suspected small-bowel bleeding in 2024, enlarging its advanced imaging base.

Europe experienced steady uptake after the MDR took full effect in 2024, compelling hospitals to modernize to compliant platforms. Germany allowed screening colonoscopies in certified ambulatory centers, easing hospital bottlenecks. G-BA.DE. France reimbursed single-use duodenoscopes for high-risk ERCP in 2024. The United Kingdom’s National Health Service is piloting AI colonoscopy across 12 trusts, aiming to cut interval cancer by 15% by 2027.

The Middle East is scaling capacity under Saudi Arabia’s Vision 2030, which earmarked USD 1.2 billion for endoscopy infrastructure. Brazil’s public system added diagnostic endoscopy to its primary-care benefits in 2024, covering 140 million citizens. Argentina’s private insurers embraced therapeutic endoscopy coverage the same year, widening access to advanced procedures.

Competitive Landscape

Olympus, Fujifilm, and Karl Storz dominate flexible and rigid scopes, yet Ambu’s single-use lineup is fragmenting share, especially in high-infection-risk segments. Olympus’s 2024 acquisition of Veran Medical Technologies for USD 340 million added electromagnetic navigation bronchoscopy, while Boston Scientific’s USD 615 million purchase of Apollo Endosurgery consolidated bariatric and metabolic portfolios. Intuitive Surgical’s Ion platform captured 12% of U.S. bronchoscopy revenue within 18 months of its 2024 launch, underscoring robotics as a disruptive axis.

Patent filings underline strategy: Olympus lodged 47 endoscopy patents in 2024, with 38% targeting AI image-processing and 26% aimed at disposable components. Regulatory compliance costs are rising; Fujifilm spent an extra USD 85 million on MDR alignment in 2024. Smaller innovators such as Outlook Surgical gain traction with towerless scopes that blend rigid and flexible features, accelerating cost-effective adoption for ASCs.

Single-use devices are a wedge for new entrants. Ambu leveraged the FDA’s 510(k) pathway to obtain 2024 and 2025 clearances, compressing development cycles to 18 months and bypassing premarket approval costs. Medtronic’s PillCam Crohn’s capsule seized 8% of small-bowel imaging within a year of its 2024 approval. As AI, robotics, and disposal economics collide, competitive intensity in the endoscopy devices market escalates, encouraging incumbents to hedge with dual reusable and single-use portfolios.

Endoscopy Devices Industry Leaders

Olympus Corporation

Boston Scientific Corporation

Medtronic PLC

Fujifilm Holdings Corporation

Karl Storz SE & Co. KG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Olympus launched the Vathin E-SteriScope single-use flexible rhinolaryngoscope for diagnostic and therapeutic ENT procedures.

- September 2025: Outlook Surgical received FDA clearance for its Inova 1 Towerless Endoscope System, integrating rigid and flexible capabilities in a portable form factor.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the endoscopy devices market as all visualization towers, endoscopes (rigid, flexible, capsule, robot-assisted), operative hand instruments, and single- or multi-use accessory sets that providers buy for diagnostic or therapeutic endoscopy. Values are expressed at manufacturer invoice level in constant 2025 US dollars.

Scope exclusions: We intentionally leave out reprocessing chemicals, large capital imaging systems, and over-the-counter camera pills that lack medical clearance.

Segmentation Overview

- By Device Type

- Endoscopes

- Rigid Endoscopes

- Flexible Endoscopes

- Capsule Endoscopes

- Robotic-assisted Endoscopes

- Endoscopic Operative Devices

- Irrigation / Suction Systems

- Access Devices

- Wound Protectors

- Insufflation Devices

- Manual Instruments

- Visualization Equipment

- Endoscopic Cameras

- SD Visualization Systems

- HD / 4K Visualization Systems

- Endoscopes

- By Application

- Gastrointestinal Endoscopy

- Laparoscopy

- Pulmonology / Bronchoscopy

- ENT / Otolaryngology

- Urology

- Gynecology

- Cardiology

- Neurology

- Orthopedics / Arthroscopy

- By Usability

- Reprocessed / Reusable Devices

- Single-use / Disposable Devices

- By End-User

- Hospitals & Academic Medical Centers

- Ambulatory Surgical Centers

- Specialty Clinics

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview GI surgeons, hospital procurement heads, ASC managers, channel distributors, and component suppliers across North America, Europe, Asia-Pacific, and Latin America. These discussions test preliminary findings, surface transaction-level prices, and let us fine-tune utilization curves before locking the model.

Desk Research

We build the evidence stack by pooling procedure counts from OECD Health Data, WHO GI-Cancer Registry, CMS Hospital Cost Reports, and device approvals captured in FDA and EMA databases. Trade bodies such as the American Society for Gastrointestinal Endoscopy and the Japan Gastroenterological Endoscopy Society supply annual adoption audits, while customs records illuminate cross-border flows of scope sub-assemblies. Paid repositories, notably D&B Hoovers and Dow Jones Factiva, help our team trace corporate revenue trails and track new launches. This list is illustrative; many additional sources support every figure we publish.

Market-Sizing & Forecasting

We begin with a top-down reconstruction that scales national procedure volumes, expected device life cycles, and average selling prices. We then run bottom-up cross-checks using sampled supplier shipments and channel margin audits. Key fingerprints, including colonoscopy volume growth, single-use scope penetration, hospital capital-spend indices, regulatory clearance counts, and ASP deflation rates, feed a multivariate regression that generates the 2025-2030 trajectory. Country gaps are bridged by region-specific procedure proxies validated during expert calls.

Data Validation & Update Cycle

Outputs pass variance checks against prior-year ratios and adjacent device markets, after which a senior analyst signs off. We refresh models annually and issue interim tweaks for major recalls, guideline shifts, or currency shocks so clients receive the latest view.

Why Mordor's Endoscopy Devices Baseline Commands Reliability

Published estimates often diverge because firms select different device baskets, update cadences, and currency normalizations. Our disciplined scope and yearly refresh keep totals aligned with what buyers actually spend.

Key gap drivers: several publishers blend maintenance services and disinfectants into revenue, while others strip out operative instruments or robot-assisted scopes. Exchange-rate choices and discounting assumptions widen spreads further.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.10 Bn (2025) | Mordor Intelligence | |

| USD 61.06 Bn (2024) | Global Consultancy A | Adds service contracts and cleaning consumables |

| USD 34.83 Bn (2024) | Global Consultancy B | Excludes operative devices and robot-assisted scopes |

These contrasts show why clients lean on our balanced, transparent baseline. It sits between optimistic add-ons and narrow equipment-only counts and can be traced to openly stated variables and repeatable steps.

Key Questions Answered in the Report

What is the projected value of the endoscopy devices market in 2031?

The endoscopy devices market is forecast to reach USD 58.71 billion by 2031.

Which device category is expanding the fastest?

Visualization equipment is growing quickest, registering an 8.25% CAGR through 2031 thanks to 4K and AI integration.

Why are ambulatory surgical centers important for future demand?

ASCs benefit from site-neutral payment reforms that lower procedure costs, propelling a 9.7% CAGR through 2031 in equipment purchases.

How fast are single-use scopes growing?

Disposable endoscopes are advancing at a 10.87% CAGR as infection-control mandates intensify.

Which region will record the swiftest growth?

Asia-Pacific leads with an 8.51% CAGR, driven by expanded reimbursement in China, India, and Japan.

What is the main regulatory hurdle facing manufacturers?

Compliance with stricter FDA post-market surveillance and Europe's MDR raises development costs and lengthens approval timelines.

Page last updated on: