Endoscopy Operative Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.87 Billion |

| Market Size (2031) | USD 20.62 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

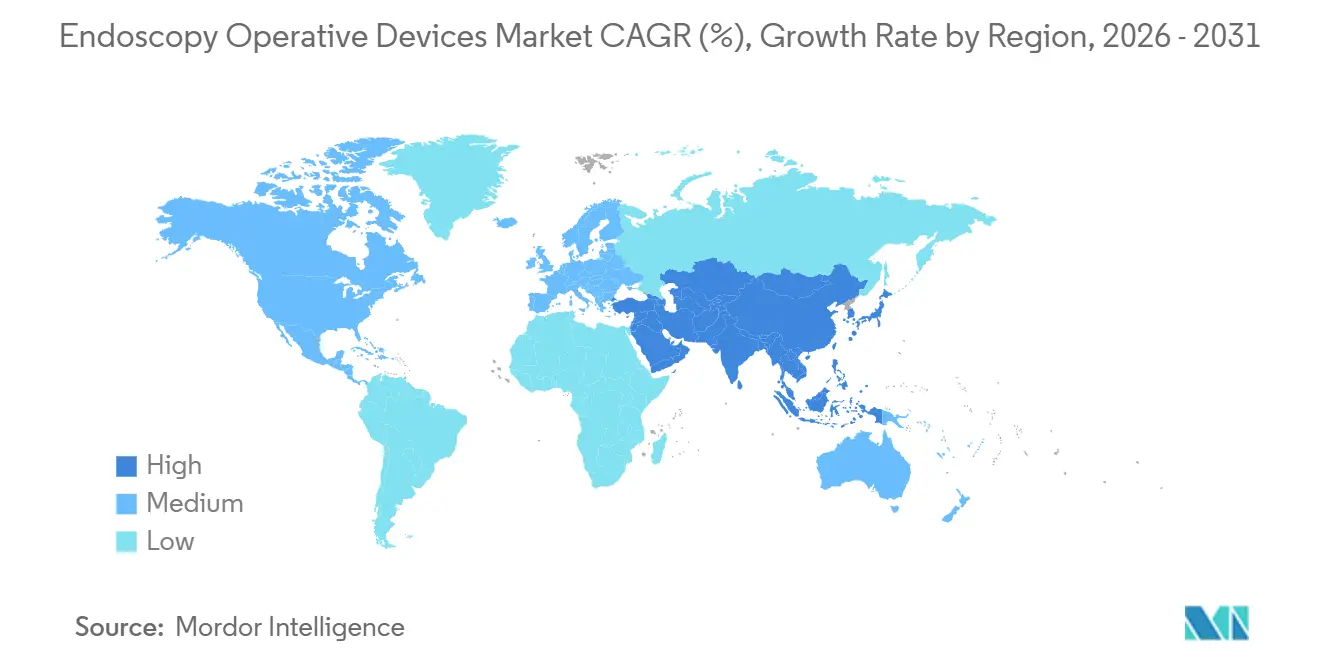

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

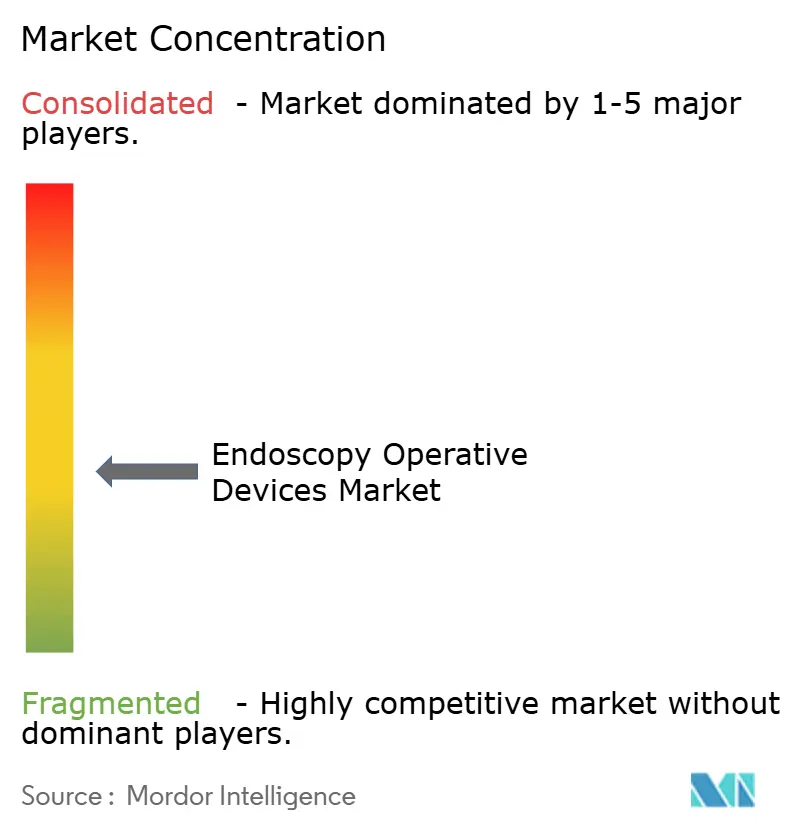

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Endoscopy Operative Devices Market Analysis by Mordor Intelligence

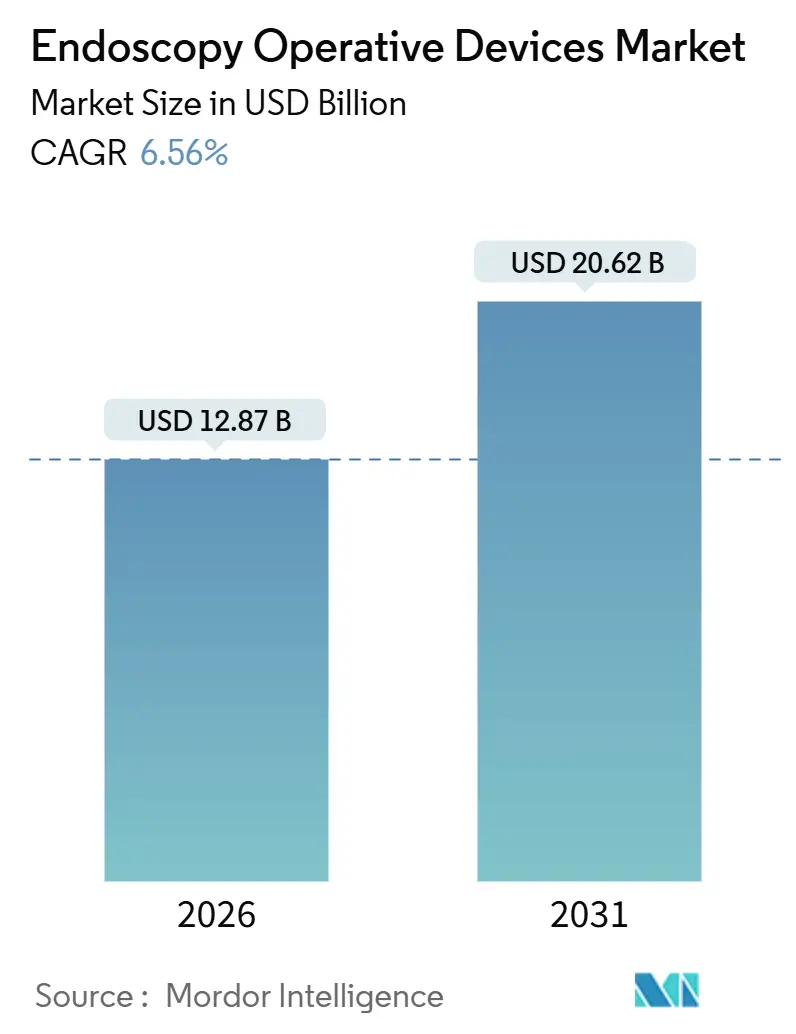

The Endoscopy Operative Devices Market size is estimated at USD 12.87 billion in 2026, and is expected to reach USD 20.62 billion by 2031, at a CAGR of 6.56% during the forecast period (2026-2031).

Demand growth is being shaped less by procedure volumes and more by a structural realignment of where and how endoscopic care is delivered. Hospitals and ambulatory surgical centers are shifting routine diagnostic and therapeutic work from inpatient floors to outpatient suites, compressing capital replacement cycles and accelerating the unbundling of towers, accessories, and software. At the same time, device makers are adjusting portfolios to favor single-use scopes, plasma and ultrasonic energy systems, and AI software licenses that fit subscription budgets. These features are resonating because Medicare payment parity for ambulatory surgeries has removed historical facility-fee advantages, while Scope 3 emissions mandates are pressuring health systems to adopt lower-energy platforms. Competitive headroom remains wide open as single-use entrants and AI developers press incumbents on both price and functionality, keeping the endoscopy operative devices market dynamic and innovation-driven.

Key Report Takeaways

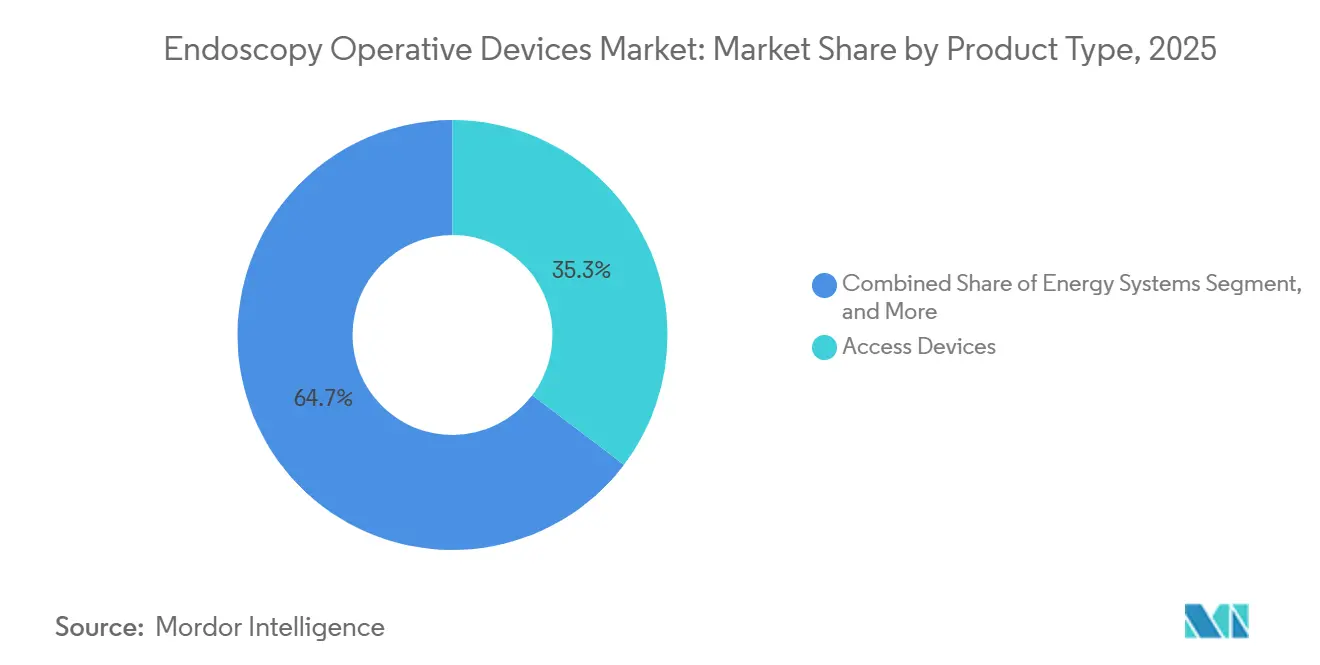

- By product type, access devices captured 35.31% of the endoscopy operative devices market share in 2025, while energy systems are forecast to expand at a 6.98% CAGR to 2031.

- By application, gastrointestinal endoscopy led with 49.57% revenue share in 2025; laparoscopy is advancing at a 7.72% CAGR through 2031.

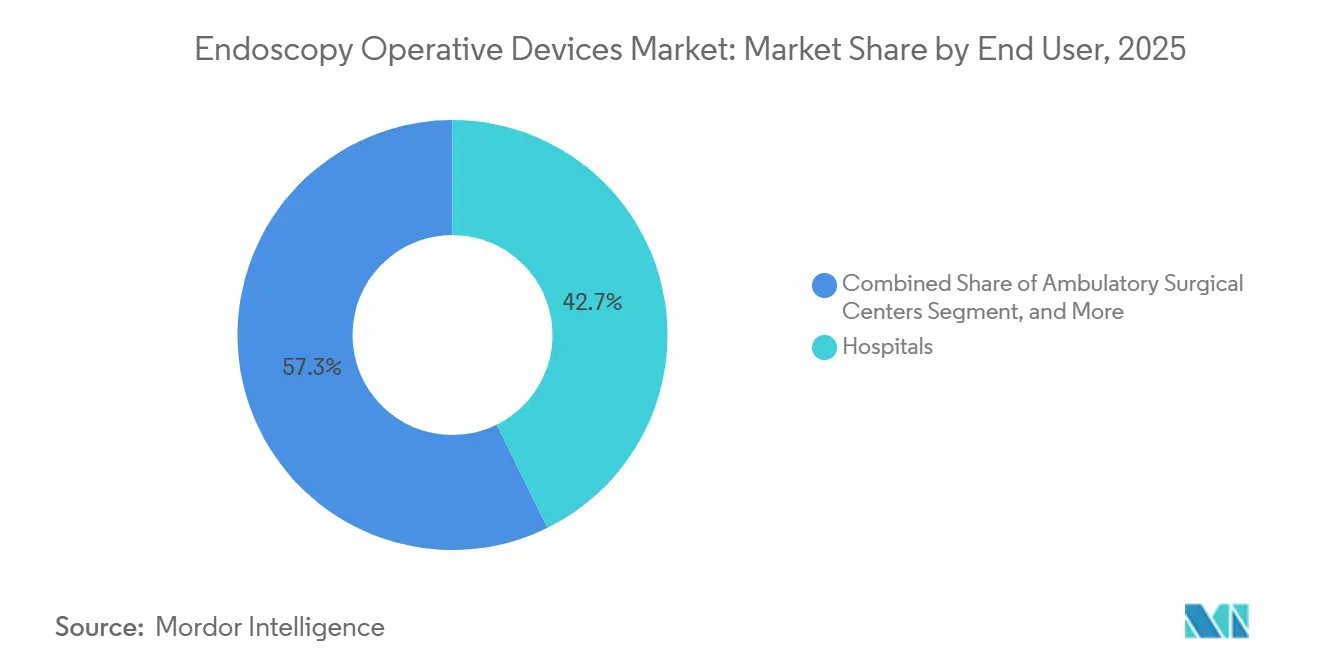

- By end user, hospitals accounted for 42.72% of revenue in 2025, whereas ambulatory surgical centers hold the highest projected CAGR at 8.07% for 2026-2031.

- By geography, North America secured a 39.83% share in 2025, while Asia-Pacific is set to grow at a 9.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Endoscopy Operative Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Minimally-Invasive GI & Bariatric Procedures | +1.2% | Global, with concentration in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Accelerated Shift of Routine Endoscopy to Outpatient & ASC Settings | +1.4% | North America and Western Europe, early adoption in GCC | Short term (≤ 2 years) |

| Rapid Adoption of Single-Use Endoscopes for Infection Control | +0.9% | Global, with regulatory mandates strongest in North America and EU | Medium term (2-4 years) |

| Integration of AI-Assisted Real-Time Lesion Detection | +0.8% | North America, EU, Japan, and China; limited penetration in emerging markets | Medium term (2-4 years) |

| Tariff-Driven Near-Shoring of Endoscope Component Supply Chains | +0.6% | North America and EU manufacturing hubs, with spillover to Mexico, India, Vietnam | Long term (≥ 4 years) |

| Hospital ESG Targets Favouring Low-Energy Plasma/Ultrasonic Energy Systems | +0.7% | EU and North America, with early adoption in Australia and select GCC hospitals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Minimally-Invasive GI and Bariatric Procedures

Endoscopic sleeve gastroplasty and intragastric balloon placements exceeded 15,000 combined cases in the United States during 2024 after joint clinical guidelines positioned these interventions as first-line therapy for patients with a body mass index between 30 and 40.[1]American Society for Gastrointestinal Endoscopy, “Joint Guidelines on Endoscopic Bariatric Procedures,” asge.org Device makers responded with pre-loaded suturing patterns that reduce procedure time to less than one hour, enabling ambulatory centers to schedule more bariatric cases per day. European payers followed Germany’s decision to reimburse duodenal-jejunal bypass liners at EUR 3,200 (USD 3,456), giving hospitals a clear commercial path for metabolic endoscopy. These changes bolster procedure volumes, stimulate accessory demand, and reinforce the positive outlook for the endoscopy operative devices market. Manufacturers, therefore, prioritize platforms that streamline sleeve geometry and liner deployment to maintain clinical momentum.

Accelerated Shift of Routine Endoscopy to Outpatient and ASC Settings

Full Medicare payment parity for colonoscopy in ambulatory surgical centers took effect in 2024, and commercial insurers quickly mirrored the policy to steer patients toward lower-cost venues.[2]U.S. Centers for Medicare & Medicaid Services, “Medicare-Certified Ambulatory Surgical Centers,” cms.gov The result was a double-digit rise in ASC-based upper-endoscopies and a move to three-year equipment leases that bundle hardware, software, and disposables into a single monthly invoice. Parallel initiatives are emerging elsewhere: the United Kingdom has earmarked GBP 240 million (USD 312 million) to expand community diagnostic centers, aiming to reduce hospital procedures by 20% by 2027. As a consequence, tower upgrades and accessory sales now hinge on flexible financing and service contracts, keeping the endoscopy operative devices market centered on subscription economics.

Rapid Adoption of Single-Use Endoscopes for Infection Control

The U.S. Food and Drug Administration advised providers in 2024 to transition to disposable duodenoscopes after detecting consistent contamination in reusable models despite proper reprocessing. Boston Scientific and Ambu each launched scopes that replicate the maneuverability of reusable devices while avoiding the need for high-level disinfection. Randomized trials covering more than 4,000 patients reported no difference in procedural success between single-use and reusable colonoscopes, closing the last primary clinical objection to disposables. Hospitals have begun factoring avoided reprocessing labor and capital outlays into procurement decisions, strengthening the cost case for disposables and adding further momentum to the endoscopy operative devices market.

Integration of AI-Assisted Real-Time Lesion Detection

Medtronic’s GI Genius received approval in Japan in 2024 and in China in 2025, opening markets that collectively perform more than 40 million colonoscopies a year.[3]Medtronic, “GI Genius AI Platform Approvals,” medtronic.com Real-time bounding boxes increased adenoma detection rates by double digits in European registries, while Olympus and Fujifilm expanded CE Mark indications to include vascular pattern recognition and histology prediction. Providers are adopting pay-per-use licenses that integrate seamlessly with existing towers, boosting the software’s share of device revenue and prompting incumbents to embed AI updates into long-term service agreements. These dynamics sustain innovation and reinforce strategic stickiness within the endoscopy operative devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Endoscopists & Reprocessing Technicians | -0.8% | Global, with acute shortages in rural North America, Southern Europe, and sub-Saharan Africa | Medium term (2-4 years) |

| High Capital & Maintenance Cost of Advanced Visualization Platforms | -0.6% | Emerging markets in Asia-Pacific, Latin America, and Middle East & Africa | Long term (≥ 4 years) |

| Stringent Post-Market Surveillance For AI-Enabled Devices | -0.4% | EU under MDR, with spillover compliance burden in APAC and Latin America | Medium term (2-4 years) |

| Reimbursement Uncertainty for Outpatient Therapeutic Endoscopy in Emerging Markets | -0.5% | India, Southeast Asia, Middle East (excluding GCC), and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Endoscopists and Reprocessing Technicians

The American Gastroenterological Association projects a 14,000-provider shortfall by 2030 because retirements are outpacing fellowship graduations. Rural communities already face six-month waits for screening colonoscopy, while high turnover among reprocessing staff forces urban centers to cancel lucrative therapeutic cases. These staffing shortages constrain capacity even as advances in equipment accelerate, tempering the otherwise strong growth prospects of the endoscopy operative devices market. Health systems are experimenting with virtual pre-procedure teaching and robotic scope steering to mitigate the gap, yet the near-term impact on installed-base utilization remains negative.

High Capital and Maintenance Cost of Advanced Visualization Platforms

Upgrading to 4K towers with AI software and multi-spectral imaging can require USD 180,000-250,000 upfront plus 12-15% annually for service, a hurdle many community hospitals and independent ASCs cannot clear. Return-on-investment models often assume procedure growth that smaller centers rarely achieve. In emerging economies where per-capita spend is below USD 200, older high-definition systems remain in use, delaying replacement cycles and moderating expansion of the endoscopy operative devices market. Vendor financing and pay-per-scan structures are gaining traction, yet price sensitivity continues to curb penetration of top-tier platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Energy Platforms Gain on Surgical Precision Mandates

Energy systems recorded the fastest forecast growth at 6.98% from 2026 to 2031 as providers swap monopolar devices for plasma and ultrasonic platforms that cut thermal spread without smoking the field. Olympus Thunderbeat added thoracic clearance in 2024, and Ethicon’s updated Harmonic introduced adaptive tissue sensing in 2025, underscoring a steady flow of iterative improvements. Access devices maintained a 35.31% share in 2025, anchored by legacy trocar fleets and a gradual move toward single-incision ports. GelPOINT now appears in 18% of U.S. laparoscopic colorectal cases, illustrating how disposable seals can reshape workflows. The endoscopy operative devices market for energy systems is projected to grow steadily as hospitals adopt ESG directives that reward low-power alternatives.

Suction and irrigation devices add filtration to capture aerosolized fragments, while hand instruments face price pressure from bundled purchasing. Insufflators have shifted from stand-alone boxes to algorithm-based tower modules that auto-adjust intra-abdominal pressure. Niche categories such as wound retractors and snares ride the wave of natural-orifice surgery, pointing toward incremental yet diversified revenue across the endoscopy operative devices market.

By Application: Laparoscopy Builds Momentum on Robotic Integration

Gastrointestinal procedures retained 49.57% revenue share in 2025, supported by high screening volumes, but laparoscopy is advancing at a 7.72% CAGR as robotic-assisted colorectal and bariatric cases proliferate. The da Vinci 5 system, launched in 2024, widened access to complex minimally invasive surgery by adding instrument tracking and force feedback that shorten learning curves. Hospitals report 18% year-over-year growth in robotic general surgery, boosting the accessory pull-through vital to the endoscopy operative devices market. Meanwhile, single-use cystoscopes expand office urology, and robotic bronchoscopy extends the reach into peripheral lung nodules, underscoring how diversification of applications sustains demand.

Obstetrics and gynecology endoscopy maintains stable procedure counts, while arthroscopy and other specialties focus on imaging fidelity rather than volume growth. The endoscopy operative devices market share for laparoscopy is expected to climb steadily as reimbursement aligns with improved patient recovery metrics.

By End User: ASC Adoption Accelerates Under Cost-Containment Pressures

Hospitals generated 42.72% of 2025 revenue but face growing competition from ambulatory surgical centers, which are forecast to post an 8.07% CAGR through 2031. Payment parity and tiered insurance benefits make ASCs the preferred venue for screening colonoscopy, routine upper GI scopes, and straightforward laparoscopic procedures. Leasing and per-procedure payment schemes align with ASC capital constraints, prompting vendors to bundle visualization towers with AI updates and disposables into flat monthly fees. This arrangement anchors predictable cash flows while boosting utilization across the endoscopy operative devices market.

Hospitals retain complex therapeutic cases that require ICU backup, anesthesia depth, or overnight monitoring. Specialty clinics, though smaller, deliver high throughput and negotiate direct contracts at favorable discounts, illustrating how varied purchasing behavior across end users influences price realization and competitive positioning within the endoscopy operative devices market.

Geography Analysis

North America commanded a 39.83% share in 2025, aided by Medicare parity, rapid AI clearances, and infrastructure grants for outpatient diagnostic hubs. Bariatric endoscopy grew 28% after new reimbursement codes equalized payments with laparoscopic alternatives, pulling accessory demand into fast-growth territory. Canada and Mexico reinforce regional supply chains as manufacturers reroute assembly from tariff-exposed Chinese plants to North American facilities. These developments underpin a resilient revenue base for the endoscopy operative devices market.

Asia-Pacific is on track for a 9.29% CAGR, the fastest worldwide, as China approved 47 Class III devices in 2024 and India extended national insurance to hundreds of millions more citizens. Domestic Chinese suppliers undercut Japanese incumbents by 40% while still meeting ISO 13485 standards, compressing price bands across flexible scopes. Japan spurred a replacement wave by adding reimbursement for narrow-band imaging, while India’s incentive program lured Fujifilm to Bangalore for camera-head assembly. Medical tourism in South Korea drives premium demand, keeping the endoscopy equipment market diverse and vibrant across the region.

Europe advances steadily despite regulatory drag from the Medical Device Regulation, which lengthens AI approvals by up to 1 year. Germany, the United Kingdom, and France remain the volume anchors, with the U.K. investing USD 312 million to migrate 20% of endoscopies to community diagnostic centers by 2027. The Gulf Cooperation Council fuels Middle East expansion through large hospital projects, while Brazil adds public endoscopy suites, yet struggles with under-reimbursed therapeutic codes. Collectively, these shifts maintain long-term growth prospects for the global endoscopy operative devices market, even as regional hurdles persist.

Competitive Landscape

The top five vendors, Olympus, Boston Scientific, Medtronic, Karl Storz, and Stryker, held a significant global revenue in 2025, a level that signals moderate concentration. Each firm defends installed bases by bundling AI lesion detection with tower upgrades, locking customers into multi-year contracts that combine software updates, analytics dashboards, and cloud storage for captured images. Olympus filed 14 patents in 2024 for real-time histology routines that run on legacy processors, illustrating a pivot toward software-defined differentiation. Boston Scientific extended its single-use portfolio while expanding U.S. silicone extrusion to meet nearshoring goals, and Medtronic leveraged GI Genius approvals to cross-sell energy devices.

Challenger brands such as Ambu and Aohua crack open specific niches—ICU bronchoscopy and price-sensitive flexible scopes—by emphasizing low total cost of ownership. Intuitive Surgical leverages robotic customer relationships to cross-sell the Ion bronchoscopy platform, snagging 12% of global lung biopsy procedures within three years of launch. Contract manufacturers in Vietnam and India now achieve ISO 13485 at scale, enabling rapid product cycles that pressure incumbent pricing. Overall, pricing power is migrating toward service bundles and AI subscriptions, shaping future competition in the endoscopy operative devices market.

Endoscopy Operative Devices Industry Leaders

Asensus Surgical Inc.

Boston Scientific Corporation

CONMED Corporation

Cook Medical Inc.

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Aspen Surgical acquired Ruhof Healthcare, adding enzymatic detergents and cleaning verification to its perioperative portfolio.

- September 2025: Outlook Surgical secured FDA clearance for the Inova 1 towerless endoscope platform, blending rigid and flexible capabilities.

- September 2025: Intuitive Surgical rolled out the da Vinci 5 with force feedback and tracking, surpassing 1,200 global installs by year-end.

- November 2024: Medtronic received Chinese approval for GI Genius, unlocking an additional 40 million colonoscopies per year.

Global Endoscopy Operative Devices Market Report Scope

The Endoscopy Operative Devices Market Report is Segmented by Product Type (Energy Systems, Access Devices, Suction & Irrigation Systems, Hand Instruments, Insufflation Devices, Other Product Types), Application (Gastrointestinal Endoscopy, Laparoscopy, Obstetrics & Gynecology Endoscopy, Urology/Cystoscopy, Bronchoscopy, Arthroscopy, Other Applications), End User (Hospitals, Ambulatory Surgical Centers, Specialty Clinics & Others), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Energy Systems |

| Access Devices |

| Suction & Irrigation Systems |

| Hand Instruments |

| Insufflation Devices |

| Other Product Types (Wound Retractors, Snares, etc.) |

| Gastrointestinal Endoscopy |

| Laparoscopy |

| Obstetrics & Gynecology Endoscopy |

| Urology / Cystoscopy |

| Bronchoscopy |

| Arthroscopy |

| Other Applications (Mediastinoscopy, Otoscopy, etc.) |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Energy Systems | |

| Access Devices | ||

| Suction & Irrigation Systems | ||

| Hand Instruments | ||

| Insufflation Devices | ||

| Other Product Types (Wound Retractors, Snares, etc.) | ||

| By Application | Gastrointestinal Endoscopy | |

| Laparoscopy | ||

| Obstetrics & Gynecology Endoscopy | ||

| Urology / Cystoscopy | ||

| Bronchoscopy | ||

| Arthroscopy | ||

| Other Applications (Mediastinoscopy, Otoscopy, etc.) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the endoscopy operative devices market?

The endoscopy operative devices market size reached USD 12.87 billion in 2026.

How fast is the market expected to grow over the next five years?

It is forecast to register a 6.56% CAGR, driving value to USD 20.62 billion by 2031.

Which product segment is expanding the fastest?

Energy systems are projected to grow at 6.98% annually as hospitals favor plasma and ultrasonic platforms.

Why are ambulatory surgical centers gaining share?

Medicare payment parity and insurer benefit designs steer routine endoscopy to ASCs, supporting an 8.07% CAGR for the segment.

Which region offers the highest growth potential?

Asia-Pacific shows the fastest regional CAGR at 9.29%, supported by Chinese approvals and expanded insurance coverage in India.

Page last updated on: