Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

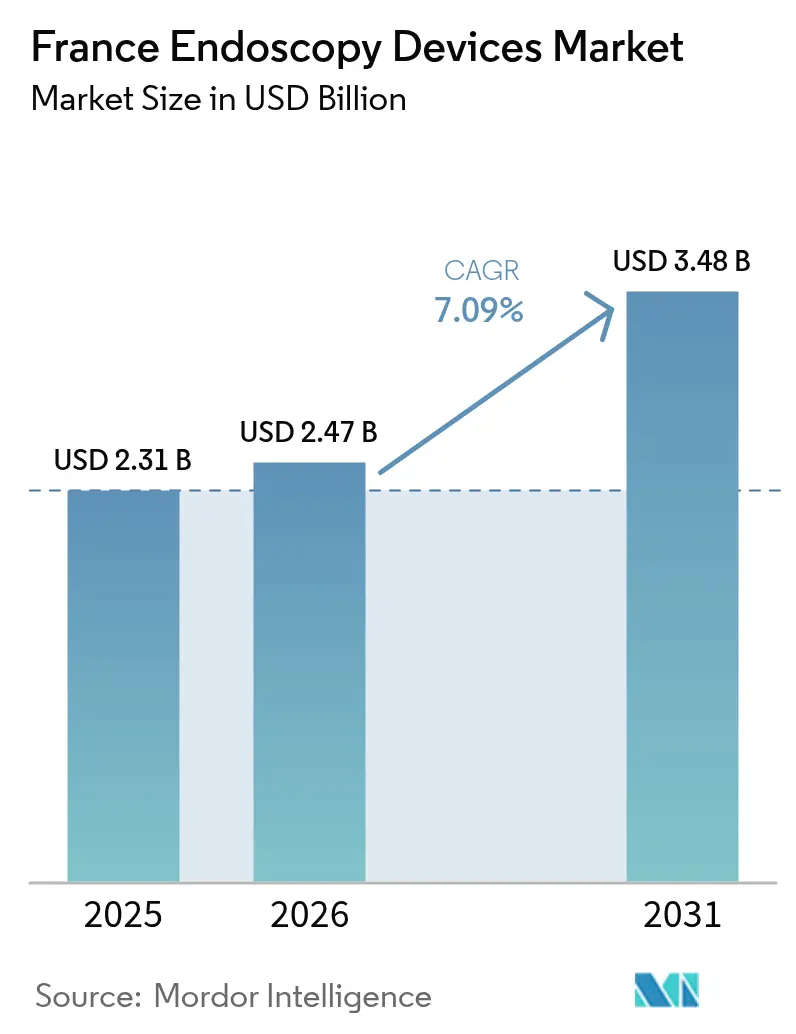

| Base Year Market Size (2025) | USD 2.31 Billion |

| Market Size (2026) | USD 2.47 Billion |

| Market Size (2031) | USD 3.48 Billion |

| Growth Rate (2026 - 2031) | 7.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Endoscopy Devices Market Analysis by Mordor Intelligence

The France endoscopy devices market size was valued at USD 2.31 billion in 2025 and estimated to grow from USD 2.47 billion in 2026 to reach USD 3.48 billion by 2031, at a CAGR of 7.09% during the forecast period (2026-2031). The growth outlook is powered by government-led cancer screening mandates, rapid adoption of AI-assisted imaging, and a structural pivot toward single-use platforms that heighten infection control efficiency. Heightened private insurance coverage and the migration of elective procedures to ambulatory centers are reinforcing premium-device demand, while the EU-MDR recertification backlog is constraining near-term product launches. Competitive intensity is rising as incumbents pursue targeted M&A to secure share in the high-growth disposable subsegment, and smaller innovators differentiate through cloud-based analytics designed for gastroenterology and pulmonology workflows. Across France, hospitals face budget ceilings that stretch replacement cycles, yet ambulatory sites continue to invest in rapid-turnover systems that minimize reprocessing downtime, underpinning the next phase of the France endoscopy devices market expansion.

Key Report Takeaways

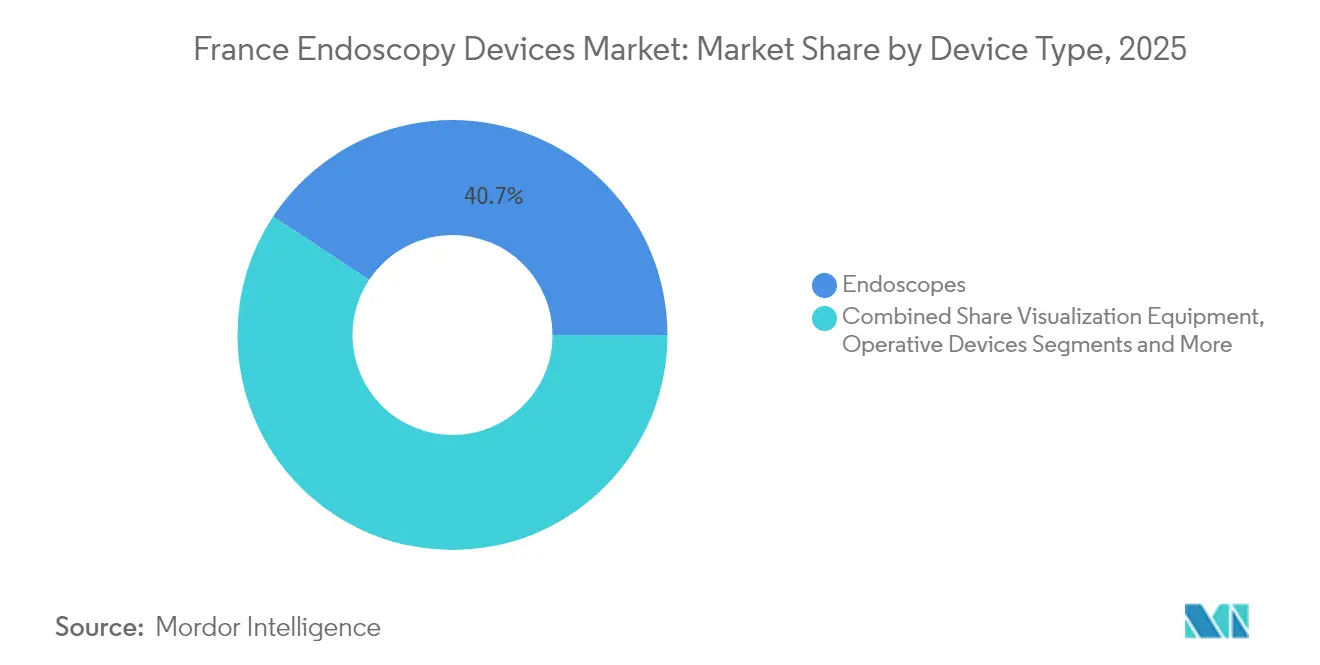

- By device type, single-use disposable endoscopes captured 17.8% growth and are expanding at a 17.2% CAGR, the fastest pace within the France endoscopy devices market.

- By application, gastroenterology led with a 54.12% share of the France endoscopy devices market size in 2025, while pulmonology is accelerating at a 8.72% CAGR through 2031.

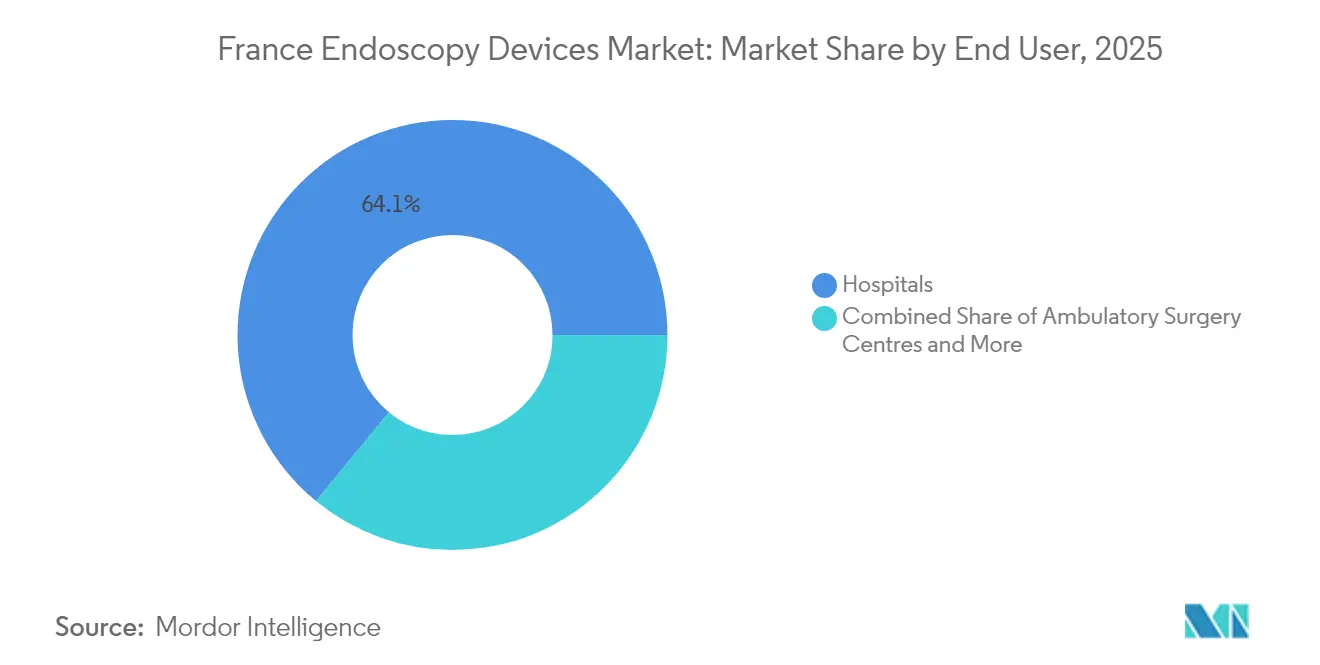

- By end user, hospitals commanded 64.05% of the France endoscopy devices market share in 2025; ambulatory surgery centers are advancing at an 8.06% CAGR to 2031.

- By usage, reusable platforms held 71.34% share of the France endoscopy devices market size in 2025, yet single-use systems are scaling at an 17.2% CAGR despite environmental trade-offs.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government cancer-prevention strategy elevating demand for diagnostic endoscopy | +2.1% | National, urban centers | Medium term (2-4 years) |

| Rising private health-insurance penetration fuelling premium device purchases | +1.4% | National, metropolitan | Medium term (2-4 years) |

| Migration of elective procedures to outpatient and day-surgery settings | +1.8% | National, Paris-Lyon-Marseille | Short term (≤ 2 years) |

| Technological convergence of HD imaging, robotics and AI elevating clinical outcomes | +1.9% | National, academic centers | Medium term (2-4 years) |

| Ageing demographics and chronic GI and respiratory disease burden | +1.2% | National, older regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Cancer-Prevention Strategy Elevating Demand for Diagnostic Endoscopy

France’s 2025-2030 cancer plan prioritizes early detection, prompting hospitals to upgrade visualization platforms and expand small-bowel capsule programs. More than 24,000 capsule procedures are now performed annually, underscoring a preference for diagnostic accuracy over therapeutic versatility. Value-based procurement criteria reward systems that shorten detection-to-treatment intervals, redirecting budgets toward AI-assisted colonoscopy that cuts missed-lesion rates. Vendors that align portfolios with screening protocols gain faster tender approvals, reinforcing the nationwide rollout of high-definition imaging. Urban oncology hubs report equipment renewal cycles two years shorter than rural peers, reflecting targeted financing that supports the France endoscopy devices market in prevention-led pathways.

Rising Private Health-Insurance Penetration Fuelling Premium Device Purchases

Complementary insurance now covers 14% of national health spending, enabling private facilities to prioritize 4K endoscopy towers and cloud-based analytics suites. Acquisition rates for AI-enhanced systems in private centers outpace the public sector by 2.3:1, creating a two-speed market where manufacturers segment offerings by funding model. Patient preference surveys show a growing willingness to travel for AI-guided diagnostics, reinforcing private investment momentum. Public purchasers respond by negotiating risk-sharing contracts that tie payments to diagnostic yield, gradually narrowing the technology gap. The virtuous cycle between reimbursement incentives and facility differentiation anchors premium growth across the France endoscopy devices market.

Migration of Elective Procedures to Outpatient & Day-Surgery Settings

Endoscopic ultrasound volume climbed 63% and pancreaticobiliary interventions rose 70.2% as hospitals shifted low-acuity cases to ambulatory units. Single-use endoscopes thrive in these sites by eliminating reprocessing queues that erode turnover metrics. Seven percent of inpatient beds closed during the past four years, tilting procedure flow toward centers optimized for same-day discharge. Procurement committees now evaluate device value through downtime savings rather than unit price, a metric that favors disposable models. Early-adopter regions demonstrate 18-month payback windows on single-use bronchoscopy, catalyzing national scale-up that sustains the France endoscopy devices market momentum.

Technological Convergence of HD Imaging, Robotics & AI Elevating Clinical Outcomes

AI algorithms embedded in endoscopy platforms achieve polyp-detection sensitivity on par with expert endoscopists while reducing inter-operator variance[1]Olympus, “CE Approval for Cloud-Based AI Devices,” olympus.fr. Olympus secured CE clearance for cloud tools addressing colorectal lesions, Barrett’s esophagus and ulcerative colitis, with French roll-out slated for Q1 2025. Academic centers in Paris already document 15% workflow-time reductions using algorithmic annotation, supporting faster list closures. Robotics adds precision in submucosal dissection, while HD optics sharpen depth perception, jointly lifting resection completeness rates. Vendors bundling software subscriptions with capital hardware increase recurring revenue streams, embedding themselves deeper within the France endoscopy devices market digital ecosystem.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operating costs under national budget pressure | -0.9% | National, public hospitals | Medium term (2-4 years) |

| Lengthy EU-MDR regulatory pathway slowing market entry | -1.2% | National, all facilities | Short term (≤ 2 years) |

| Preference for refurbished equipment in secondary hospitals | -0.6% | Regional, smaller cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Operating Costs Under National Budget Pressure

The 2025 Diagnosis Related Group tariff update trailed device inflation, forcing public hospitals to prolong equipment life cycles by 2.3 years. Forty-one percent of facilities responded by tightening procedural appropriateness thresholds to stretch resources. This prolongs installed-base aging and slows uptake of AI-ready platforms, creating a technology gap against privately funded peers. Suppliers counter by offering modular upgrades and usage-based financing that spread cost over procedure volume. Sustained fiscal pressure nevertheless caps near-term upside for capital-intensive towers within the France endoscopy devices market.

Lengthy EU-MDR Regulatory Pathway Slowing Market Entry

Manufacturers face approval timelines that have doubled under EU-MDR, with more than 500,000 devices awaiting recertification[2]Regulatory Affairs Professionals Society, “European Commission Consultation on Electronic MDR Amendments,” raps.org. Smaller innovators struggle to resource documentation demands, delaying commercialization of niche single-use scopes. Established brands prioritize high-revenue models, leaving portfolio gaps in emerging subsegments. Hospitals consequently defer procurement until recertified versions ship, compressing short-term sales. Policy proposals to streamline conformity assessments could unlock pent-up pipeline value, yet uncertainty persists, moderating growth in the France endoscopy devices market during the transition window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Single-Use Revolution Reshapes Market

The endoscopes category accounted for 40.72% of the France endoscopy devices market in 2025, anchored by widespread use in digestive and respiratory procedures. Disposable scopes now record a 17.2% CAGR, well ahead of reusable models, as infection-control priorities outweigh unit-price premiums. Studies revealed residual bioburden on 30% of reprocessed scopes despite guideline adherence, intensifying calls for sterile-packed alternatives. Visualization equipment ranks second in revenue, buoyed by AI overlay modules that automate lesion characterization and feed data lakes powering continuous-learning algorithms. Operative devices enjoy momentum after Micro-Tech’s purchase of Creo Medical assets, which broadened its energy-based resection tools. Accessories and consumables provide stable recurring streams, with public tenders allocating EUR 2.73 million for digestive endoscopy disposables in 2024, equal to USD 2.95 million using the 2024 average EUR-USD rate. Capsule platforms complete the mix with roughly 24,000 annual procedures, underscoring niche yet steady adoption. The France endoscopy devices market size for endoscopes is projected to widen as single-use uptake accelerates, narrowing cost differentials via economies of scale.

Demand acceleration favors manufacturers that control both reusable and disposable lines, enabling hospitals to tailor fleets by service mix. Olympus and Fujifilm focus on high-end towers linked to AI clouds, whereas Ambu and Pentax expand single-use catalogs paired with recycling initiatives. Sustainability concerns prompt life-cycle analyses comparing carbon footprints; recent findings note single-use gastroscopes emit 2.5 times more CO₂ than reusable counterparts, mainly in the production phase. Market leaders therefore pilot bio-based handles and closed-loop recycling that could offset environmental criticism. Cumulatively, these shifts underscore how infection prevention, data integration and eco-design will jointly steer the next chapter of the France endoscopy devices market.

By Application: Gastroenterology Dominates While Pulmonology Accelerates

Gastroenterology controlled 54.12% of the France endoscopy devices market size in 2025, reflecting high colorectal cancer screening volumes and expanded therapeutic interventions. Early adoption of AI polyp-detection modules increased adenoma-find rates, reinforcing hospital investment in high-resolution colonoscopes. Bariatric and metabolic endoscopy gains traction under April 2024 ASGE-ESGE guidelines that widened eligibility to patients with BMI ≥ 30 kg/m², fueling incremental tower utilization. Pulmonology applications record the fastest trajectory at a 8.72% CAGR as advanced bronchoscopic navigation, cryobiopsy and robotic platforms target peripheral lesions. An international survey showed 58% of interventional pulmonologists intend to acquire new bronchoscopic technology within two years, highlighting a robust pipeline.

Colorectal cancer screening benefits from national campaigns that push fecal immunochemical test positives to colonoscopy within thirty days, hiking procedural throughput at ambulatory units. Urology broadens as Ambu launches single-use ureteroscopes and cystoscopes that simplify sterile workflow. ENT and gynecology remain smaller but stable, supported by compact video chips that deliver superior image resolution in office settings. The France endoscopy devices market share held by gastroenterology will gradually erode as pulmonology and bariatric indications expand, yet absolute volume in digestive endoscopy continues to rise.

By End User: Hospitals Lead While Ambulatory Centers Surge

Hospitals retained 64.05% command of the France endoscopy devices market in 2025, leveraging complex-case capabilities, centralized reprocessing and academic research. Private hospitals differentiate through premium AI-enabled towers financed via supplemental insurance, while public institutions prioritize cost-containment through modular upgrades. Ambulatory surgery centers post an 8.06% CAGR, buoyed by regulatory support for day-case reimbursement and patient preference for shorter stays. A nationwide longitudinal study reported that 76.9% of hospital endoscopy admissions transitioned to day-case pathways, compressing inpatient volumes.

Outpatient diagnostic clinics base purchasing on throughput benchmarks that reward single-use scopes free from decontamination bottlenecks. Mobile endoscopy units emerge in underserved rural regions, offering scheduled visits that shrink waiting lists by up to 30 days. Training institutions remain pivotal end users, as 92.3% of ESGE survey respondents operated within public or university hospitals, underscoring reliance on teaching centers for skill dissemination. Manufacturers support these hubs through simulation scholarships and bundled service packages, cultivating brand loyalty that sustains the France endoscopy devices market pipeline.

By Usage: Single-Use Adoption Accelerates Despite Environmental Concerns

Reusable endoscopes dominate at 71.34% share yet face infection-control scrutiny after studies documented persistent contamination even post-reprocessing. Disposable scopes answer sterility demands and unlock efficiencies by removing washer-disinfector queues, giving them an 17.2% CAGR to 2031. Hospital sustainability committees weigh carbon emissions data that spotlight higher production footprints for single-use devices, yet lifecycle analyses including water and energy used in reprocessing narrow the gap. Pentax Medical’s acquisition of cold-plasma drying specialist Plasmabiotics highlights innovation in enhanced reprocessing to sustain reusable relevance. Ambu pledges to launch bio-polymer handles and eliminate PVC in 95% of new products by 2025, positioning disposables within decarbonization roadmaps.

Policy makers encourage procurement that balances infection control, cost and ecology, catalyzing pilots in which reusable towers coexist with single-use scopes for high-risk patients. Investment in traceability software ensures auditable scanning of scope serial numbers and patient IDs, helping hospitals select optimal modality on a case-by-case basis. The resulting hybrid ecosystem underpins diversified revenue streams across the France endoscopy devices market.

Geography Analysis

Paris, Lyon and Marseille anchor premium adoption, supported by academic centers with greater capital budgets and concentrated specialist talent. These metropolitan hubs spearhead AI-enhanced colonoscopy and robotic bronchoscopic pilots, resulting in waiting times 20% shorter than national averages. Northern and eastern regions exhibit faster single-use scope uptake, driven by higher private facility density and infection-control mandates. Conversely, southern coastal zones prioritize advanced imaging and ultrasound integration for hepatobiliary workloads, reflecting the prevalence of specialized gastroenterology institutes. Rural departments face specialist scarcity, with appointment delays reaching 52% above urban benchmarks, prompting mobile units that transport portable towers on weekly circuits.

Over the past four years, more than 260,000 endoscopy appointments were canceled nationwide, highlighting capacity constraints most acute outside major cities. Manufacturers collaborate with tele-endoscopy providers to deliver real-time remote visualization, enabling specialists in Paris to supervise procedures in underserved areas. Regional disparities in fellowship training compound service gaps; only 6% of fourth-year trainees completed the recommended portfolio of procedures, with lower exposure in non-academic centers. Vendors run regional cadaver labs to expand hands-on experience, supporting uniform clinical outcomes that reinforce the broader France endoscopy devices market.

Infrastructure modernization grants channeled through Plan France Relance fund upgrades to rural hospitals include earmarks for endoscopy suites, although capital disbursement lags announced timelines. These projects nonetheless signal potential long-term catch-up, especially if paired with performance-based procurement that rewards high-utilization equipment. Such policy alignment is projected to narrow geographic inequities, sustaining consistent demand across the France endoscopy devices market through 2030.

Regulatory Landscape

Endoscopy devices marketed in France must comply with the EU Medical Device Regulation (EU) 2017/745 (EU MDR). Oversight for vigilance, post-market surveillance, and market surveillance actions is led at the national level by ANSM. In April 2026, Decree No. 2026-299 (published April 21, 2026, effective April 22, 2026) completed further alignment of the French Public Health Code with EU MDR requirements. The update reinforces obligations around vigilance, traceability, and documentation for devices supplied in France, including clear French-language requirements for labeling and instructions for use.

Market access and funding dynamics run alongside EU compliance through France-specific reimbursement and pricing processes. HAS evaluates medical devices for clinical value, including through CNEDiMTS assessments where applicable, while CEPS negotiates prices and tariffs for products listed on the LPPR. That makes evidence generation and dossier quality central to commercial traction. On the registration side, EUDAMED obligations intensified in 2026, with mandatory EUDAMED registration applying to new economic operators and new MDR devices from May 28, 2026, and legacy device registration required by November 28, 2026, increasing near-term operational workload for manufacturers and authorized representatives supplying endoscopy portfolios into France.

Competitive Landscape

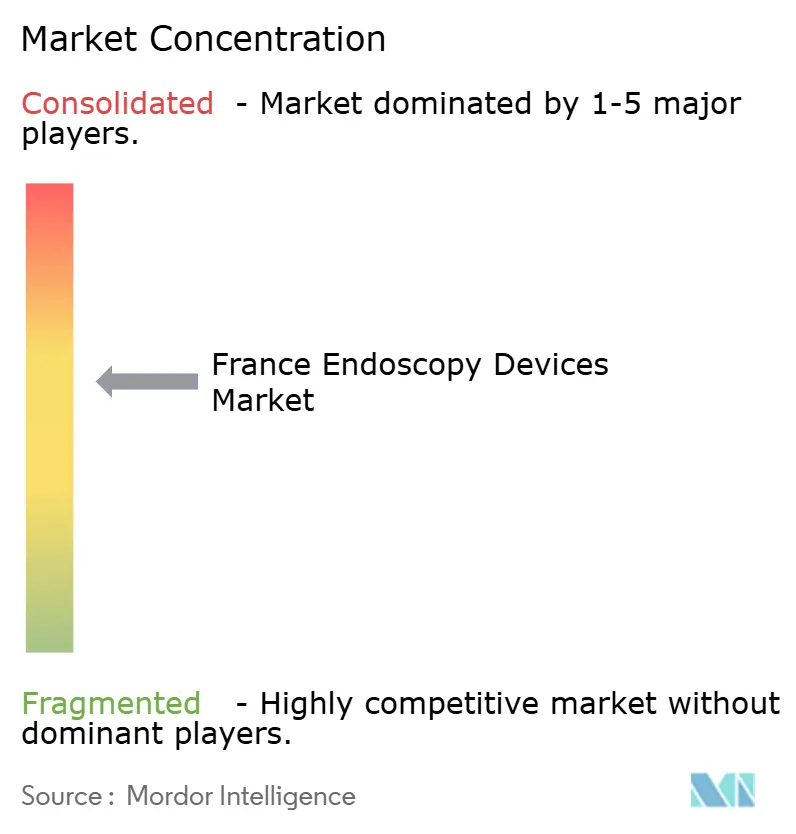

The France endoscopy devices market shows moderate concentration. Olympus leads with about 30% GI endoscope share, capitalizing on a 70% global footprint and early AI commercialization. Karl Storz, Boston Scientific, Fujifilm and Medtronic round out the top tier, collectively controlling a majority of revenue. Ambu, dominant in single-use scopes, posted 19.7% segment growth and now derives 59% of sales from endoscopy solutions, challenging reusable incumbents[3]Ambu A/S, “Ambu Annual Report 2023/24,” ambu.com. Micro-Tech’s 51% acquisition of Creo Medical S.L.U. fortifies its energy-based surgery offering and signals rising M&A aimed at Western European expansion.

Technological arms races focus on AI cloud ecosystems, where proprietary datasets create defensible moats. Olympus gained CE approval for CADDIE, CADU and SMARTIBD and plans a connected workflow platform by 2025. Fujifilm introduced Detective Flow Imaging for endoscopic ultrasound to improve vascular visualization. Medtronic signed a distribution partnership for Dragonfly Endoscopy accessories, expanding its pancreaticobiliary reach.

Competitive differentiation also spans sustainability pledges. Pentax promotes plasma drying cabinets that curb microbial growth without heat, whereas Ambu commits to PVC-free portfolios. Pricing pressure from refurbished channels shapes defensive strategies such as factory-certified preowned programs by Olympus. Overall, innovation cadence, sustainability positioning and regulatory execution will define winner profiles within the France endoscopy devices market.

France Endoscopy Devices Industry Leaders

Boston Scientific Corporation

Conmed Corporation

Medtronic PLC

Cook Medical LLC

Johnson & Johnson (Ethicon)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hospital modernization programs and reconfiguration of endoscopy infrastructure provide a practical equipment and workflow opportunity beyond routine replacement cycles. The most relevant pull comes when capacity expansion is tied to same-day pathways and centralized reprocessing. In March 2026, CHU de Nimes reported that its 4,530 m2 Centre dEndoscopie Diagnostique et Interventionnelle (CEDI) project reached final interior finishing, backed by the Fonds de modernisation et dinvestissement en sante (FMIS). Centre Hospitalier dAvignon launched procurement in February 2026 to centralize endoscope disinfection services. Together, these moves support demand for integrated towers, reprocessing equipment, traceability solutions, and service contracts designed to reduce downtime in high-throughput units.

Therapeutic endoscopy specialization also widens the addressable opportunity within premium procedure sets, as training concentration and clinical adoption at academic hubs drive pull-through for specialized devices and accessories. In June 2026, first commercial EndoZip Automated Suturing System cases for Endoscopic Sleeve Gastroplasty (ESG) were performed at IHU Strasbourg, pointing to expanding use of endoscopic suturing platforms in bariatric pathways between medical management and surgery. Reprocessing service ecosystems remain another lever for both reusable fleets and hybrid models. Ecolab operates an endoscopy reprocessing research and service center in Aubagne serving about 2,000 installed hospital equipment units in France, supporting opportunities in process standardization, maintenance, and consumables as single-use scopes gain traction in settings where turnaround time and infection control are prioritized.

Recent Industry Developments

- June 2026: Boston Scientific ran an interventional endoscopy training workshop at Hopital prive Jean Mermoz in Lyon, covering procedures such as ERCP and endoscopic ultrasound. The program builds procedural adoption and standardization for advanced GI interventions, supporting pull-through demand for therapeutic devices and accessories used in complex cases.

- March 2026: HAS (CNEDiMTS) issued an opinion on Boston Scientifics SpyScope DS II single-operator cholangiopancreatoscopy accessory for managing indeterminate biliary stenoses and complex biliary or pancreatic stones. A named HAS assessment provides a visible market access milestone in France and supports procurement discussions where clinical value documentation is a gating item for adoption.

- December 2024: Medtronic France secured public contracts (notified December 10-11, 2024) for supply and maintenance of endoscopic equipment, including mechanical resection or aspiration systems and specialized instruments used in neuro-endoscopy and fluorescence video-surgery. These awards highlight continued multi-year tendering activity for both capital equipment and service coverage, reinforcing competitive pressure in hospital accounts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of endoscopy devices used in France for diagnostic and therapeutic procedures, including endoscopes, visualization systems, operative tools, and related accessories and consumables that support an endoscopic procedure.

Scope exclusions: Standalone surgical systems that are not used for endoscopic visualization or intervention, as well as general hospital consumables not specific to endoscopy workflows, are not counted.

Segmentation Overview

- By Device Type

- Endoscopes

- Rigid Endoscopes

- Flexible Endoscopes

- Capsule Endoscopes

- Disposable / Single-Use Endoscopes

- Robot-Assisted Endoscopes

- Visualization Equipment

- Endoscopy Cameras

- Image Processors & Light Sources

- 3-D / 4-K Display & Recording Systems

- Operative Devices

- Endotherapy & Energy Systems

- Insufflators & Irrigation Pumps

- Accessories & Consumables

- Endoscopes

- By Application

- Gastroenterology

- Pulmonology

- Orthopedic (Arthroscopy)

- Cardiology

- ENT Surgery

- Gynecology

- Neurology

- Urology

- Bariatric & Colorectal Cancer Screening

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgery Centres

- Out-Patient Diagnostic Facilities

- By Usage

- Reusable / Reprocessable Endoscopes

- Single-Use / Disposable Endoscopes

- Reprocessing Equipment & Consumables

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the base structure of the market model and to anchor assumptions that can be checked independently. We start with public health statistics and care delivery indicators, such as national health accounts and procedure-related publications from sources such as France's Ministry of Health and related public agencies, Eurostat health data, the OECD health statistics series, and the World Health Organization databases.

After that, we review device and procedure signals that help explain demand and pricing, including reimbursement and coding references, hospital activity publications, and safety and vigilance updates. Supporting inputs are also taken from company annual reports, investor presentations, reputable press, and peer-reviewed clinical journals that track adoption of minimally invasive procedures and imaging performance. In a few places, we use a paid subscription for company financials and a patent database to confirm product mix direction and innovation intensity. The desk sources listed here are illustrative only, and many other public references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure test the model and close gaps that desk sources cannot resolve, especially around product mix, replacement cycles, and price progression for reusable versus single-use components. We speak with a mix of hospital procurement and sterilization stakeholders, clinicians and department managers, distributors, and local industry participants across France, so our assumptions align with actual purchasing behavior and the specific care settings where these devices are used.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 15% | |

| Mid tier: 54% | Functional/Unit leaders: 34% | |

| Smaller Players: 15% | Managers: 51% |

Market-Sizing & Forecasting

Sizing starts from a top-down build, where procedure volumes and the care setting mix are used to reconstruct the addressable demand pool for endoscopy equipment in France, and then the spend is allocated across endoscopes, visualization, operative devices, and accessories and consumables. Once this spine is set, we add selective bottom-up checks using sampled price bands and volume proxies from channel feedback, along with supplier and hospital purchasing patterns, so totals can be adjusted when the first pass looks stretched.

Inputs that matter in this market include endoscopy procedure intensity by specialty, the shift toward minimally invasive pathways, the split between reprocessable and single-use items (and the resulting reprocessing burden), replacement and upgrade cycles for endoscopes and visualization towers, and public versus private hospital purchasing cadence. When data is thin for a subcategory, it is bridged using adjacent procedure groups and validated with interview feedback, so the missing blocks do not distort the total.

For forecasting, scenario analysis is used, since growth is shaped by a few clear demand drivers that can move faster or slower depending on budgets and adoption. The forward view is built from expected procedure growth, product mix changes, and gradual price movement, and then reviewed with experts so the final curve fits what decision makers are seeing in the field.

Data Validation & Update Cycle

Validation happens in multiple steps so obvious gaps and hidden inconsistencies can be caught early. We compare model outputs against independent signals like procedure activity direction, public spending trends, and category-level adoption patterns, and then large variances are traced back to the specific assumption that caused the swing.

Before sign-off, the numbers go through analyst review checks for year-over-year continuity, mix logic, and outlier pricing assumptions, followed by targeted re-contact when a key input looks uncertain. Reports are refreshed annually, and interim updates are made when material events occur that can change demand or pricing. Just before delivery, a fresh pass is completed so clients receive the most current view that can be supported with clear steps and explainable inputs.

Mordor Intelligence's France Endoscopy Devices Market Estimate Compared With Other Published Estimates

Published market values can differ even when the topic sounds identical, because counted products, the base year, and the pricing logic are not always aligned. Differences also come from how each publisher treats reprocessing related spend, accessories and consumables, and whether growth is modeled from procedure activity or from supplier-side revenue assumptions.

Procedure mix signals and the reprocessable versus single-use shift are the evidence checks that tie Mordor Intelligence's estimate to what hospitals actually buy for endoscopic workflows, and this often leads to a wider device scope than studies that only track endoscopes. Some external figures also start from an earlier base year and then apply a flatter growth path, which can understate the near-term impact of upgrades in imaging and operative tools. Currency timing and the refresh cadence of assumptions can further widen the spread when price changes are occurring in parallel with volume growth.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.31 B (2025) | |

| Industry Data Publisher A | USD 2.03 B (2023) | Uses an earlier base year and a slower growth path, and the category structure leans toward core device systems, which can dampen the value contribution from accessories and consumables over time. |

| Sector Analytics Group B | USD 0.92 B (2023) | Tracks endoscopes only rather than the broader endoscopy devices basket, which removes visualization equipment, operative devices, and a large share of procedure driven consumables from the counted total. |

Taken together, the spread is mainly explained by scope boundaries and starting year choices, rather than a disagreement that demand exists. By keeping the math traceable to procedure activity, care setting mix, and realistic replacement cycles, our view stays explainable and can be reproduced as new signals emerge.

Key Questions Answered in the Report

What is the current value of the France endoscopy devices market?

The France endoscopy devices market size is USD 2.47 billion in 2026, with a forecast value of USD 3.48 billion by 2031.

Which segment is growing fastest within French endoscopy?

Single-use disposable endoscopes are expanding at an 17.2% CAGR between 2026 and 2031 as infection-control priorities intensify.

Why are ambulatory surgery centers important to endoscopy growth in France?

They support 8.06% annual growth by focusing on same-day procedures that favor rapid-turnover equipment, including disposable scopes.

How is AI influencing endoscopy adoption in France?

AI-assisted imaging boosts detection accuracy and workflow efficiency, prompting hospitals to upgrade to cloud-connected towers.

What regulatory challenge is affecting device launch timelines?

EU-MDR recertification requirements have doubled approval times, delaying the commercial availability of newer endoscopic platforms.

Which companies lead the French market for endoscopy equipment?

Olympus, Karl Storz, Boston Scientific, Fujifilm and Medtronic form the top tier, with Olympus alone holding roughly 30% share.

Page last updated on: