Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

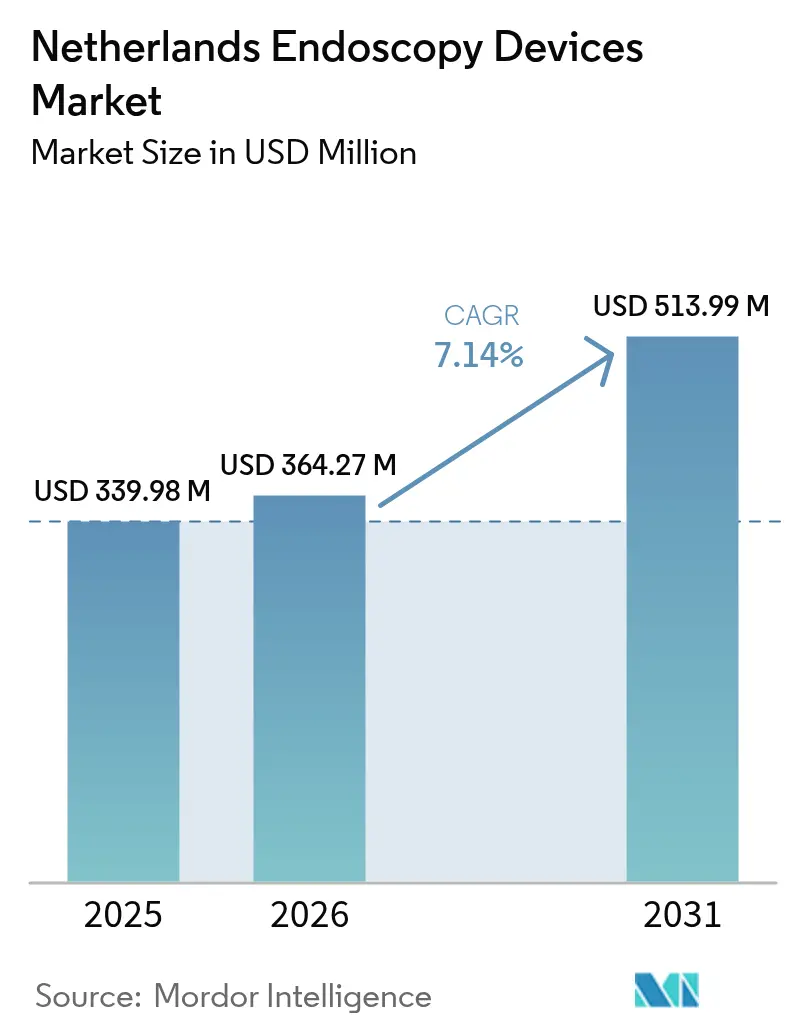

| Base Year Market Size (2025) | USD 339.98 Million |

| Market Size (2026) | USD 364.27 Million |

| Market Size (2031) | USD 513.99 Million |

| Growth Rate (2026 - 2031) | 7.14% CAGR |

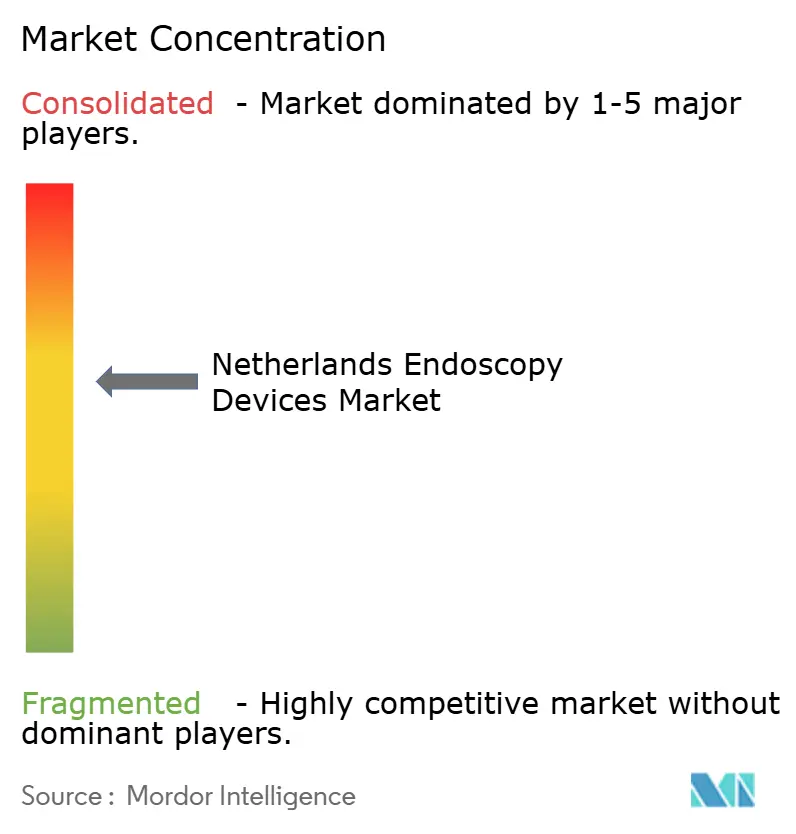

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Netherlands Endoscopy Devices Market Analysis by Mordor Intelligence

The Netherlands endoscopy devices market size in 2026 is estimated at USD 364.27 million, growing from 2025 value of USD 339.98 million with 2031 projections showing USD 513.99 million, growing at 7.14% CAGR over 2026-2031. Demand expands as hospitals and ambulatory centers accelerate the shift toward minimally invasive, day-case procedures, while national climate policy pushes every care provider to adopt lower-carbon technologies[1]Government of the Netherlands, “More sustainability in the health and care sector,” government.nl. Growing uptake of high-definition, AI-enabled imaging systems, together with robotic platforms, is strengthening procedural precision and diagnostic yield. At the same time, EU Medical Device Regulation (EU-MDR) infection-control clauses are steering facilities toward single-use scopes, creating tension between safety, cost, and sustainability objectives. Payers’ increasing use of value-based quality metrics is reinforcing the migration from fee-for-service to outcome-linked reimbursements, further reshaping supplier strategies within the Netherlands endoscopy devices market.

Key Report Takeaways

- By device type, endoscopes led with 61.83% of Netherlands endoscopy devices market share in 2025; visualization and imaging systems are projected to expand at an 8.24% CAGR through 2031.

- By application, gastroenterology captured 45.05% of Netherlands endoscopy devices market size in 2025, while ENT/otolaryngology is forecast to grow fastest at an 8.54% CAGR to 2031.

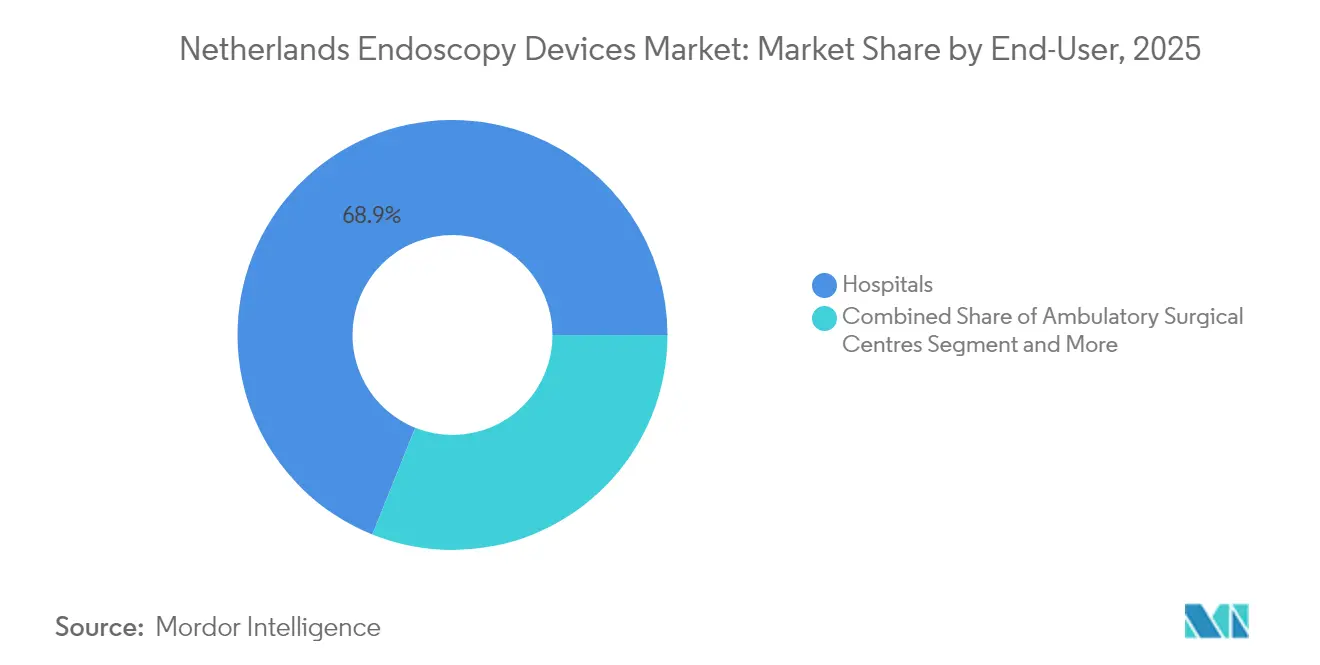

- By end user, hospitals held 68.92% revenue share in 2025; ambulatory surgical centers record the highest projected CAGR at 7.77% over 2026-2031.

- By usability, reusable scopes accounted for 84.95% of Netherlands endoscopy devices market size in 2025; single-use scopes are set to grow at a 8.96% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Netherlands Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population and chronic GI disease burden | +1.8% | National (urban hubs) | Long term (≥ 4 years) |

| Preference for minimally invasive day-case surgeries | +1.5% | National (university centers first) | Medium term (2-4 years) |

| Technological leaps in HD, AI and robotics | +1.2% | National with spill-over to Belgium and Germany | Medium term (2-4 years) |

| Shift to single-use scopes under EU-MDR infection rules | +0.9% | EU-wide, Netherlands early adopter | Short term (≤ 2 years) |

| Insurer-linked AI quality metrics | +0.7% | National (pilot hospitals) | Medium term (2-4 years) |

| Dutch Green Deal push for low-carbon devices | +0.6% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Chronic GI Disease Burden

Rising life expectancy and a parallel uptick in younger-onset colorectal cancer are boosting diagnostic colonoscopy volumes, stretching capacity across tertiary and peripheral hospitals. National screening programs already achieve 96.6% colonoscopy follow-up for FIT-positive participants through digital intake tools that streamline scheduling and reduce outpatient visits. Alongside malignancies, inflammatory bowel disease prevalence is climbing, reinforcing steady demand for repeat surveillance in the Netherlands endoscopy devices market. Providers thus prioritize high-definition imaging and AI-assisted polyp detection to manage growing caseloads without compromising quality.

Preference For Minimally-Invasive Day-Case Surgeries

The Dutch healthcare model records 96% laparoscopic cholecystectomy rates and fewer than 1% inpatient cataract stays, setting an international benchmark for same-day treatment. Financial incentives embedded in the DBC system reward throughput and low complication rates; consequently, endoscopy suites invest in next-generation visualization towers and ergonomic accessories that shorten turnover time. Evidence from the multicenter ESCAPE trial showed better outcomes with early minimally invasive surgery over an endoscopy-first approach in chronic pancreatitis, confirming procedural shifts that amplify equipment demand.

Technological Leaps (HD, AI, Robotics) In Endoscopy

Dutch academic centers partner with industry to validate AI software that lifts adenoma detection and standardizes quality scoring. GI specialists report 78.2% intent to integrate such tools within five years. 4K imaging stacks and robotic endoscopes enhance maneuverability inside convoluted anatomy, especially during complex ERCP or submucosal dissection. Continuous upgrades keep the Netherlands endoscopy devices market on par with leading US and Japanese centers, attracting cross-border referrals.

Shift To Single-Use Scopes Under EU-MDR Infection Rules

New surveillance requirements make post-procedural contamination events a high-profile liability. Hospitals therefore deploy disposable duodenoscopes for high-risk ERCP, protecting patients and avoiding service-line shutdowns. While lifecycle cost debates persist, clinical studies report comparable cannulation success and shortened turnaround under single-use protocols. This regulatory driver accelerates procurement cycles and widens the supplier base in the Netherlands endoscopy devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified endoscopy nurses/technicians | -1.1% | National (peripheral regions) | Short term (≤ 2 years) |

| High capital and lifecycle cost of advanced systems | -0.8% | National (smaller hospitals) | Medium term (2-4 years) |

| Reimbursement caps for outpatient GI procedures | -0.6% | National | Long term (≥ 4 years) |

| Stricter Dutch water-discharge rules for reprocessing | -0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shortage Of Certified Endoscopy Nurses/Technicians

Peripheral hospitals face prolonged vacancies that limit weekly lists, prompting referral overflow into university centers and lengthening wait times. Wage inflation compounds budget pressure, and the advanced competencies needed for AI-assisted or robotic procedures lengthen training pipelines[2]European Public Health Association, “EUPHA webinars,” epha.org. Skills deficits therefore temper procedure volume growth despite latent demand within the Netherlands endoscopy devices market.

High Capital & Lifecycle Cost Of Advanced Systems

Full 4K imaging suites, integrated AI licences and robotic platforms can exceed EUR 1 million per room, a threshold challenging for regional institutions operating under fixed-budget ceilings. Total ownership costs also now include carbon-footprint reporting and mandatory cybersecurity audits, adding pressure to procurement committees weighing upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Device: Endoscopes Lead Market Transformation

Endoscopes generated 61.83% of Netherlands endoscopy devices market revenue in 2025, anchored by versatile flexible systems deployed across GI, pulmonary and urology suites. Capsule platforms penetrate small-bowel diagnostics as reimbursement expands, while robot-assisted designs enter tertiary centers for suturing and EFTR. Improved optics and articulating tips sustain high clinician loyalty to established brands, yet lower-priced value lines from Asian suppliers intensify price negotiations.

Visualization and imaging units post an 8.24% CAGR because AI overlay modules and 4K CMOS sensors are now prerequisites for accreditation audits. Integrated recording and cloud analytics simplify peer review, and simulator-ready processors satisfy the ESGE’s call for competency-based training. Operative accessories, insufflators, irrigation pumps and tissue resection tools—ride the growth of therapeutic endoscopy, adding incremental revenue streams to the Netherlands endoscopy devices market.

By Application: Gastroenterology Dominance Faces ENT Disruption

Gastroenterology accounted for 45.05% of Netherlands endoscopy devices market size in 2025. Nationwide FIT screening and high IBD prevalence drive routine colonoscopy and chromoendoscopy volumes, ensuring continuous refresh cycles for colonoscopes and imaging stacks. Pulmonology demand remains steady as targeted lung cancer screening pilots launch.

ENT/otolaryngology shows the fastest 8.54% CAGR as office-based transnasal esophagoscopy and balloon sinuplasty gain acceptance, supported by ultra-slim scopes and portable towers. Cardiology, neurology and gynecology sub-segments grow modestly but collectively enrich aftermarket sales of specialty accessories that broaden supplier portfolios.

By End-User: Hospital Dominance Challenged by Ambulatory Growth

Hospitals retained 68.92% of Netherlands endoscopy devices market share in 2025 due to comprehensive infrastructure, 24 hour anaesthesia coverage and MDR-compliant reprocessing. University facilities pioneer AI pilots and sustainability scoring, shaping national purchasing standards that vendors must meet.

Ambulatory surgical centers expand at an 7.77% CAGR because day-case reimbursement aligns with patient preference for rapid discharge. These centers prioritize compact towers, mobile documentation carts and single-use scopes that bypass central sterilization, streamlining flow while meeting Green Deal targets. Diagnostic labs and specialized clinics complement hospital capacity, especially during national screening campaigns.

By Usability: Single-Use Revolution Challenges Reusable Tradition

Reusable platforms held 84.95% share in 2025, protected by amortized investments in washer-disinfectors and trained staff. Scope tracking software and new brush designs lower contamination risk, supporting continued use in low-risk case mix. Nonetheless, evidence that single-use gastroscopes produce 2.5 times the carbon emissions of reusables highlights the environmental calculus purchasers must weigh.

Single-use scopes accelerate at 8.96% CAGR as EU-MDR surveillance and FDA guidance trigger risk-mitigation policies. Manufacturers respond with biodegradable plastics and recycling take-back schemes, positioning disposables as a managed-service rather than a commodity sale within the Netherlands endoscopy devices market.

Geography Analysis

Urban academic hubs in Amsterdam, Rotterdam and Utrecht anchor technology diffusion, absorbing the earliest AI add-ons and robotic consoles. High procedure volumes justify rapid refresh cycles that sustain supplier pipelines. Regional hospitals in Friesland, Zeeland and Drenthe concentrate on scalable, cost-effective towers that comply with EU-MDR yet fit smaller budgets.

National transport density allows complex cases to centralize in university centers without compromising access, enabling peripheral units to focus on routine screenings. This hub-and-spoke distribution keeps overall Netherlands endoscopy devices market logistics efficient and aligns with workforce availability.

Cross-border collaborations through the Meuse-Rhine Euregion facilitate shared trials with Belgian and German sites, amplifying clinical data packages for CE marking. Participation in Horizon Europe robotics consortia gives Dutch buyers early insight into emerging platforms, reinforcing the country’s role as a proving ground for next-generation devices.

Regulatory Landscape

Endoscopy devices in the Netherlands are governed by the EU-wide market access requirements under the Medical Device Regulation (EU) 2017/745 (MDR), including CE marking, UDI obligations, and post-market surveillance/vigilance duties. National market surveillance and enforcement are led by the Health and Youth Care Inspectorate (Inspectie Gezondheidszorg en Jeugd, IGJ), which can intervene through administrative measures and impose administrative fines (up to EUR 450,000) for non-compliance under the Medical Devices Act framework. Specific categories (including some class I devices, custom-made devices, and systems/procedure packs) also require national notification in NOTIS.

In 2026, the regulatory focus tightened around traceability and supply transparency as the Wet van 4 februari 2026 (Staatsblad 2026, 23) amended the Medical Devices Act to implement Regulation (EU) 2024/1860, including EUDAMED rollout provisions and mandatory reporting of supply chain interruptions. From May 2026, key EUDAMED modules (Actors, Devices, Certificates) moved into mandatory use under the same regulation, raising the operational bar for manufacturers, authorized representatives, and importers to maintain accurate registrations and documentation for continued market access in the Netherlands.

Competitive Landscape

The Netherlands endoscopy devices market shows moderate concentration. Olympus positions its EVIS X1 platform around sustainability scorecards and a roadmap toward disposable colonoscopes. Ambu expands 100% single-use portfolios beyond bronchoscopy, capitalizing on procurement shifts in infection-prone specialties.

Boston Scientific pilots pay-per-procedure models that bundle capital, service, and consumables, easing hospital cash-flow barriers. Fujifilm promotes 4K/AI towers integrated with cloud dashboards that auto-populate quality registries, directly supporting insurer benchmarks. Domestic med-tech startups collaborate with TU Delft and Erasmus MC on steerable robotic catheters and low-carbon packaging, diversifying supplier options and injecting competitive dynamism into the Netherlands endoscopy devices market.

Strategic alliances center on simulation-based education, carbon-footprint auditing and lifecycle service. Vendors that quantify emission savings or document detection-rate uplifts secure multi-year framework agreements as hospitals align purchasing with Green Deal and value-based metrics.

Netherlands Endoscopy Devices Industry Leaders

Olympus Corporation

Cook Group Incorporated

Medtronic PLC

Johnson & Johnson (Ethicon Endo-Surgery)

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Hospital infrastructure renewal and consolidation into dedicated intervention and diagnostics centers are creating new tender cycles for endoscopy towers, imaging stacks, and procedure-enabling accessories across Dutch provider networks. In 2026, Franciscus Gasthuis opened a new facility building housing the Operatie & Interventie Centrum (Surgery and Intervention Center), and Elisabeth-TweeSteden Ziekenhuis (ETZ) advanced its new Center for Diagnosis and Treatment (Phase 2) by signing a design-phase contract (May 2026). These projects concentrate endoscopy and interventional activity into modernized footprints where vendors can compete on integrated room solutions (visualization, documentation, pumps/insufflation, and compatible single-use components) rather than point products.

Regulatory and quality-system changes also create room for suppliers that streamline compliance and strengthen reprocessing risk management. The 2026 mandatory use of key EUDAMED modules (under Regulation (EU) 2024/1860) increases demand for clean device master data, UDI readiness, and transparent supply continuity processes, supporting value propositions tied to traceability, service, and lifecycle documentation. At the same time, the IGJ infection-prevention supervision framework for flexible endoscopes, combined with ongoing oversight of MDR/IVDR duties, encourages hospitals and ambulatory centers to reassess their mix of reusable and single-use scopes, reprocessing equipment, and workflow tools (tracking, standardized cleaning/disinfection adherence, and compatible accessories) to maintain throughput while remaining audit-ready.

Recent Industry Developments

- April 2026: Fujifilm Healthcare Europe GmbH announced the European market introduction of the FlexCan Steerable Cannula for ERCP, positioned for use alongside its ELUXEO 8000 endoscopy solution. The release strengthens Fujifilm's therapeutic endoscopy accessory footprint and reinforces compatibility-focused selling around platform integration and procedural efficiency.

- March 2026: Olympus announced commercial availability in Europe of its OFP-3 and OFP-3 PLUS endoscopic flushing pump systems. Broader access to updated fluid-management hardware supports procedural standardization in high-throughput suites and gives Olympus another basis to bundle capital equipment with consumables and service in competitive tenders.

- October 2025: Olympus launched the first three applications of its OLYSENSE CAD AI portfolio in EMEA. The release extends the installed-base upgrade path from conventional visualization toward AI-enabled workflows, tying procurement discussions more directly to quality metrics and software-driven differentiation in colonoscopy.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers endoscopy devices sold in the Netherlands that are used to visualize, diagnose, or treat through natural openings or small incisions in clinical settings. It includes relevant capital equipment and core device kits that are purchased by hospitals, clinics, and ambulatory centers.

Scope exclusions: We do not count service and maintenance contracts, rental income, or broad imaging systems that are not specific to endoscopy procedures.

Segmentation Overview

- By Type of Device

- Endoscopes

- Rigid Endoscopes

- Flexible Endoscopes

- Capsule Endoscopes

- Robot-assisted Endoscopes

- Operative Devices

- Irrigation / Suction Systems

- Access Devices & Ports

- Wound Protectors

- Insufflation Devices

- Other Operative Devices

- Visualization & Imaging

- Endoscopic Cameras

- SD Visualization Systems

- HD & 4K Visualization Systems

- AI-assisted Image-Analysis Software

- Endoscopes

- By Application

- Gastroenterology

- Pulmonology / Bronchoscopy

- Orthopedic / Arthroscopy

- Cardiology

- Gynecology

- Neurology

- ENT / Otolaryngology

- By End-user

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics & Diagnostic Labs

- By Usability

- Re-usable Endoscopes

- Single-use Endoscopes

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the boundaries of what should be counted as endoscopy devices in the Netherlands and to build the basic demand picture behind procedures. We used public sources such as the Dutch National Institute for Public Health and the Environment (RIVM), Statistics Netherlands (CBS), European Commission documentation (including EU-MDR context), and OECD health statistics to understand demographics, care delivery patterns, and regulatory conditions that affect procurement.

To turn this into usable sizing inputs, we also reviewed sources such as hospital annual reports, procurement and tender announcements, clinical society and association publications, and peer reviewed medical journals on endoscopy utilization and infection control practices. Where company level signals were needed, paid company financials and news intelligence, plus a patent database and a contracts and tenders database, were used only to cross check launch timing, portfolio emphasis, and buyer behavior patterns. The sources named here are illustrative only, and many other public materials were also referenced for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased and replaced in Dutch care settings, and how pricing differs between reusable and single use setups for similar procedures. We spoke with hospital procurement and sterilization stakeholders, clinical users across high volume endoscopy departments, and local distribution and service specialists, so the key assumptions from desk research could be checked and corrected where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | |

| Mid tier: 55% | Functional/Unit leaders: 33% | |

| Smaller Players: 19% | Managers: 52% |

Market-Sizing & Forecasting

The sizing starts with a top-down demand pool build using Netherlands procedure activity and care delivery signals, which are then translated into device demand using practical replacement and utilization assumptions. In simple terms, we connected expected procedure volumes to device mix (reusable versus single use), then applied a realistic price level by product category to arrive at a value estimate.

While the model is mainly top-down and bottom-up is used as a cross check, we also corroborated totals with selective supplier side approximations, such as sampled price points for key device groups and a reasonableness check against channel activity and procurement patterns. When inputs were missing, assumptions were filled using ranges agreed in interviews and then narrowed through consistency checks, so the final total stays traceable.

Forecasts were produced using scenario analysis, where variables were adjusted based on how practitioners and buyers expect procurement to shift over the next few years. Inputs that matter most include minimally invasive and day case procedure momentum, reusable scope replacement timing, adoption of single use scopes in infection control sensitive pathways, capital cycle timing for visualization towers and light sources, and EU-MDR driven compliance and reprocessing requirements that can reshape purchasing choices.

Data Validation & Update Cycle

Before sign-off, outputs are triangulated against independent market signals such as procedure direction, capital purchase cycle logic, and the implied unit volumes required by the final value. If a sub-category shows an unusual jump or drop, the drivers are revisited, and follow-up calls are triggered with selected respondents to confirm whether it is a real shift or an input error.

A multi-step analyst review is followed so assumptions stay consistent across device types and use settings, and currency treatment and timing are checked for alignment. The report is refreshed annually, and interim updates are made when a material event occurs, such as a major regulatory change or a clear procurement shift. Right before delivery, we do a final pass to ensure the latest public signals are reflected.

Mordor Intelligence's Netherlands Endoscopy Devices Market Size Versus Other Published Estimates

It is common to see different market size values for the same topic because each publisher sets its own boundaries and uses its own mix of indicators. The selected year, what counts as an endoscopy device versus an adjacent item, and how pricing is treated can all move the final number.

Key gap drivers in this market tend to be whether estimates include service revenue and broad imaging equipment, whether single use items are treated as devices or as general consumables, and whether the model follows a hospital procurement view or a broader healthcare spending view. By tracking procurement-cycle timing and device replacement logic, Mordor Intelligence keeps the Netherlands estimate aligned with what care providers buy as endoscopy specific equipment, which can differ when wider categories are included.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.34 B (2025) | |

| Global Consultancy A | USD 9.42 B (2024) | This estimate appears to use a much broader value pool, where the device boundary likely expands into wider endoscopy related systems and spend categories, and the base year and pricing basis differ from equipment-only procurement modeling. |

| Industry Publisher B | USD 0.19 B (2026) | The lower value is consistent with a narrower counted set, such as focusing on selected endoscopy device groupings or excluding some capital equipment and accessories, which shifts the total even if procedure demand is similar. |

Looking across the three values, the spread is mainly explained by what is included in scope and how the purchase event is defined, rather than a disagreement on endoscopy usage itself. A model that clearly separates endoscopy specific equipment from adjacent healthcare spend, and that checks the result against replacement cycles and purchasing behavior, gives decision makers a cleaner number to plan against.

Key Questions Answered in the Report

What is the current size of the Netherlands endoscopy devices market?

The market is valued at USD 364.27 million in 2026 and is projected to reach USD 513.99 million by 2031.

Which device segment grows the fastest in the Netherlands?

Visualization and imaging systems expand at an 8.24% CAGR, driven by AI-enabled 4K processors and training simulators.

Why are single-use endoscopes gaining ground despite sustainability goals?

EU-MDR infection-control rules and risk-mitigation policies push hospitals to adopt disposables for high-risk ERCP and ICU cases.

How do Dutch reimbursement policies influence device adoption?

The DBC model rewards day-case efficiency and now pilots AI-linked quality bonuses, nudging providers toward advanced imaging and analytics.

Which end-user segment shows the highest growth to 2031?

Ambulatory surgical centers, supported by high national day-surgery rates, post an 7.77% CAGR through 2031.

Page last updated on: