Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

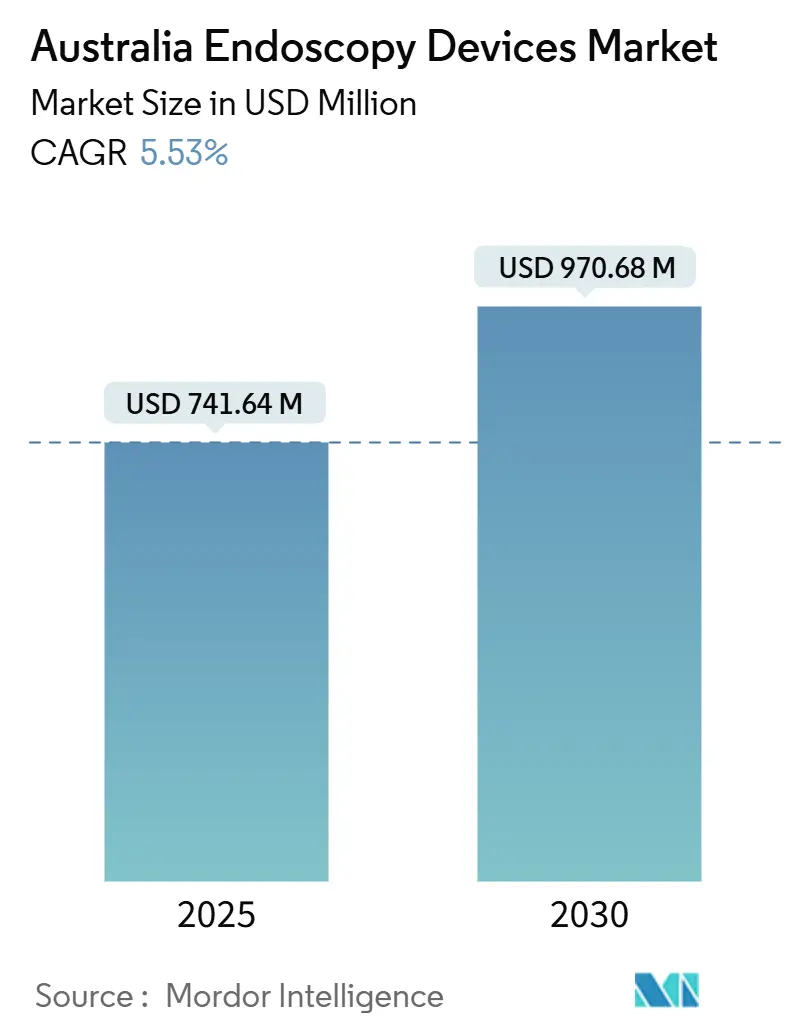

| Market Size (2025) | USD 741.64 Million |

| Market Size (2030) | USD 970.68 Million |

| Growth Rate (2025 - 2030) | 5.53% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Endoscopy Devices Market Analysis by Mordor Intelligence

Australia endoscopy devices market size is valued at USD 741.64 million in 2025 and is forecast to advance to USD 970.68 million by 2030, expanding at a 5.53% CAGR. The trajectory reflects a mature yet innovative field where reimbursement security, state capital spending, and private-sector competition intersect. Demand is anchored by the National Bowel Cancer Screening Program, which draws more than 2.5 million participants each year. Hospitals accelerate replacement cycles for high-definition endoscopes, while AI-ready visualization platforms gain traction as providers chase higher adenoma detection rates. Reprocessing cost inflation tilts some buyers toward single-use scopes, even as sustainability goals temper disposable adoption. Regulatory complexity rises after the Therapeutic Goods Administration (TGA) activated its Unique Device Identification (UDI) system in March 2025, elevating compliance hurdles for late entrants.

Key Report Takeaways

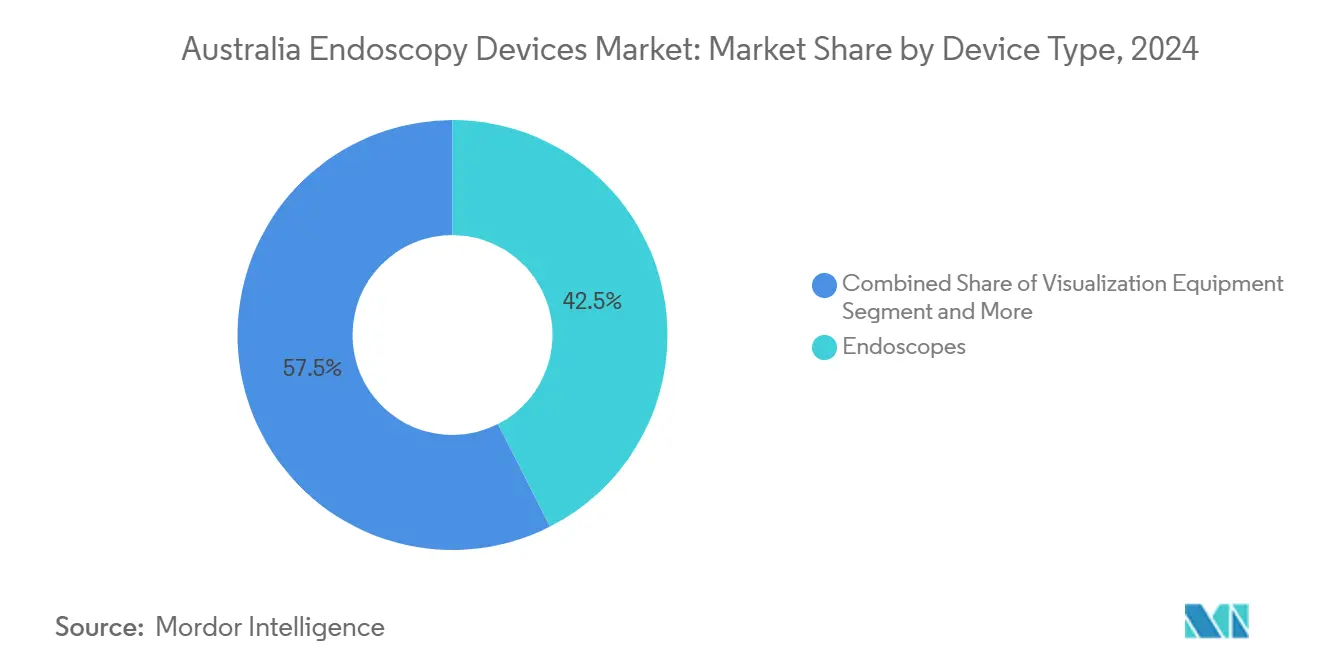

- By device type, endoscopes captured 42.55% of Australia endoscopy devices market share in 2024. Visualization equipment is projected to grow at a 9.25% CAGR through 2030.

- By application, gastroenterology commanded 49.53% share of the Australia endoscopy devices market size in 2024 and is poised for steady 5.1% growth through 2030. Pulmonology is forecast to expand at a 9.85% CAGR to 2030.

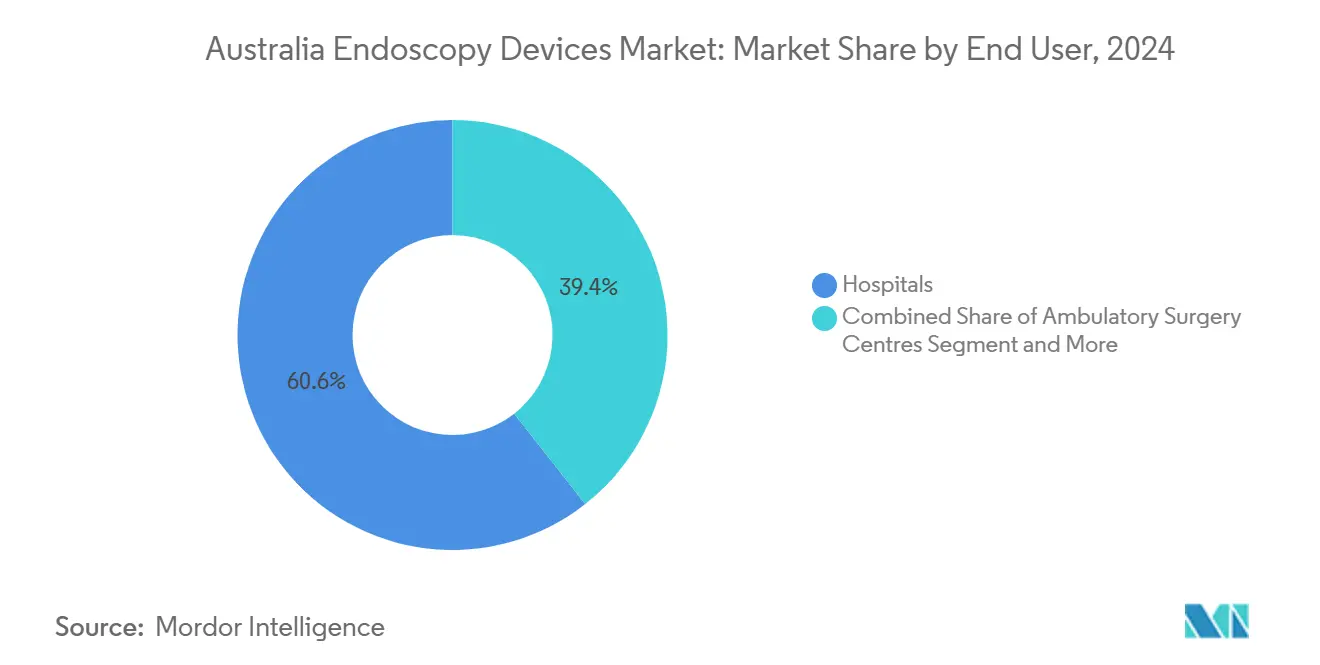

- By end user, hospitals held 60.63% revenue share in 2024, while ambulatory surgery centers are set to advance at a 10.17% CAGR through 2030.

Australia Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of minimally-invasive surgery | +1.2% | National, stronger in metropolitan areas | Medium term (2–4 years) |

| Growing GI-cancer screening programs | +0.8% | National, enhanced rural initiatives | Short term (≤2 years) |

| Shift to single-use endoscopes for infection control | +1.1% | National, prioritized in high-risk cases | Medium term (2–4 years) |

| AI-assisted real-time lesion detection | +0.9% | Metropolitan hospitals, expanding regionally | Long term (≥4 years) |

| Public–private funding for rural tele-endoscopy | +0.6% | Rural and remote regions | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Minimally-Invasive Surgery

Australian surgeons and advanced practice nurse endoscopists increasingly favor endoscopic approaches because patients recover faster and hospitals lower length-of-stay costs. Austin Health’s statewide nurse endoscopist training pipeline exemplifies capacity building that meets rising case volumes without diluting quality[1]Austin Health, “Advanced Practice Nursing,” austin.org.au. Private health insurers reimburse complex procedures—MBS item 30694 pays USD 481.35—so providers have a financial cushion to invest in next-generation platforms. Tasmania surpassed its 2023–24 endoscopy target by 3%, validating how systematic workforce expansion expands service availability. As more specialties embrace endoluminal techniques, procedure complexity escalates, raising demand for high-definition optics, operative accessories, and ergonomic scope designs that minimize operator fatigue.

Growing GI-Cancer Screening Programs

Lowering the bowel-cancer screening age to 45 years propelled a fresh cohort into the pathway and lifted annual kit distribution above 5 million. Participation hovers near 44% among invitees, but positive tests obligate follow-up colonoscopies, anchoring recurring demand for scopes and single-use accessories. Registry metrics track adenoma detection, prompting facilities to chase image-quality upgrades and AI-enabled detection overlays. Government support remains firm because bowel cancer still ranks second in national incidence, ensuring protected budgets even as other line items face austerity.

Shift to Single-Use Endoscopes for Infection Control

COVID-19 elevated awareness of cross-contamination risks, spotlighting duodenoscope-associated outbreaks. Single-use scopes remove reprocessing uncertainty; the TGA cleared VersaVue disposable cystoscopes in April 2024, sending a strong market signal. Yet hospitals weigh 24–47-fold higher greenhouse-gas output against infection-control gains, particularly because public facilities have carbon-neutral targets. Reprocessing costs—AUD 52–67 per cycle—and a 24-minute turnaround hurt productivity, making disposables economical in low-volume ambulatory surgery centers (ASCs). Procurement committees now run total-cost models that dilute sticker-price gaps and sometimes green-light single-use scopes for high-risk ERCP or cystoscopy cases.

AI-Assisted Real-Time Lesion Detection

Early adopters in Sydney and Melbourne integrated Medtronic GI Genius and Fujifilm CAD EYE modules, observing 13–29% jumps in adenoma detection. Optiscan’s collaboration with Monash University, backed by a AUD 3 million CRC-P grant, is building a confocal endomicroscope with embedded AI that distinguishes malignant from benign mucosa at the cellular level. The Royal Australian College of General Practitioners underscores that AI decisions still need physician oversight, which preserves clinician primacy but boosts demand for intuitive dashboards and explainable algorithms[2]Royal Australian College of General Practitioners, “Artificial Intelligence in General Practice Guidelines,” racgp.org.au. As the Australian Digital Health Agency pushes FHIR-based interoperability, integration barriers should ease, allowing AI image outputs to populate electronic medical records automatically.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & reprocessing costs | -0.7% | National, sharper in rural Australia | Short term (≤2 years) |

| Shortage of advanced-endoscopy specialists | -0.5% | National, acute in rural areas | Medium term (2–4 years) |

| Stringent TGA device-approval timelines | -0.4% | National | Medium term (2–4 years) |

| Sustainability push curbing single-use plastics | -0.3% | National, strong in public hospitals | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capital & Reprocessing Costs

Austin Health will replace a full fleet of flexible scopes in 2026, underscoring how five-year refresh cycles hit budgets cyclically. Updated AS 4187:2014 and Gastroenterological Society of Australia protocols drove per-cycle reprocessing expense to AUD 52–67 and lengthened turnover by nearly half an hour, reducing daily throughput[3]Gastroenterological Society of Australia, “Clinical Guidelines and Updates,” gesa.org.au. Rural hospitals with fewer than four scopes cannot justify automated washers and rely on manual cleaning, hiking error risk and insurance premiums. Private-equity owners, who injected AUD 4.5 billion into healthcare in 2022, prioritize EBITDA and often postpone capital projects, delaying technology modernization.

Shortage of Advanced-Endoscopy Specialists

RACP’s training pipeline outputs too few gastroenterologists; as of 2025, 22% of rural posts sit vacant. South West Healthcare has advertised specialist positions for more than a year with limited response, illustrating persistent geographic maldistribution. The CCRTGE’s REST recertification program ensures competence but soaks up faculty bandwidth and case lists, slowing new-fellow throughput. North Queensland’s remote capsule program cannot replace on-site therapeutic capability, so complex ERCP cases still migrate hundreds of kilometers, deflating local procedure volumes and equipment spending.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Endoscopes Hold the Line while Visualization Surges

Endoscopes generated 42.55% of Australia endoscopy devices market revenue in 2024, cementing their status as procedural bedrock across GI, respiratory, and urologic specialties. Flexible designs dominate because they serve multiple lumens, whereas rigid scopes retain value for ENT and orthopedic work. Hospitals refresh flagship models to gain 4K imaging chips and narrow-band filters that elevate mucosal detail. The Australia endoscopy devices market size for endoscopes is projected to reach USD 414 million by 2030, sustaining 4.7% growth. Capsule scopes gain momentum under remote-screening initiatives; Queensland shipped hundreds to remote patients in 2024, sidestepping the need for in-clinic staffing. Robot-assisted prototypes from Endogene tease future demand for self-advancing systems that shorten procedure time and lower patient discomfort.

Visualization equipment grows fastest at 9.25% CAGR because AI modules, big-data archiving, and streaming capability revolutionize image workflows. Hospitals link towers to PACS cloud archives, letting surgeons replay clips for morbidity meetings and insurance documentation. The Australia endoscopy devices market now values a console not merely as a video source but as a data node, which intensifies refresh cycles whenever new chipsets or AI licenses debut. Operative accessories such as irrigation pumps and insufflators remain stable earners because volume growth offsets price compression. The TGA’s UDI mandate from 2025 forces barcode scanners onto workstations, nudging hospitals to pick vendors that integrate tracking software natively.

By Application: Gastroenterology Rules but Pulmonology Accelerates

Gastroenterology accounted for 49.53% of Australia endoscopy devices market sales in 2024 on the back of compulsory bowel-cancer surveillance. Colonoscopy reimbursement at USD 285.70 per case safeguards margins, while therapeutic mucosal resection at USD 584.60 incentivizes advanced kit upgrades. The segment’s maturity invites premium pricing for AI-aided polyp detection, which providers market as quality differentiators. Tasmania processed 13,394 GI procedures in FY 2023–24, up 3% on plan, showing latent demand met by capacity expansion. The Australia endoscopy devices market share for gastroenterology is predicted to edge down slightly as other specialties grow faster, yet absolute spending climbs on equipment sophistication.

Pulmonology leads growth with a 9.85% CAGR because lung-cancer screening protocols widened eligibility after pandemic-linked respiratory awareness surged. Navigation bronchoscopy platforms fuse CT data with real-time scope tracking, raising diagnostic yield for small nodules. Public campaigns on COPD management encourage earlier bronchoscopic interventions such as valve placement, spurring demand for specialty catheters. ENT and orthopedic procedures hold modest shares but benefit from 3D rigid scopes that cut operating-theater time. Gynecology emerges as a suburban clinic service line where office hysteroscopy kits enable one-stop diagnosis and therapy, a model aligned with ASC expansion.

By End User: Hospitals Command yet ASCs Emerge

Hospitals controlled 60.63% of Australia endoscopy devices market turnover in 2024, supported by NSW’s AUD 12.4 billion capital program that funds tower replacements and sterile reprocessing rooms. Major systems such as Austin Health are constructing purpose-built suites within the Harold Stokes redevelopment, embedding unidirectional instrument flow to cut infection risk. Private hospitals dominate throughput—70% of national procedures—leveraging brand reputation and 24/7 ICU backup for complex cases. The Australia endoscopy devices market size for hospital end users will exceed USD 550 million by 2030, yet growth decelerates as outpatient models siphon routine volume.

Ambulatory surgery centers ride a 10.17% CAGR wave because insurers push site-neutral payments and patients value same-day discharge. Single-use scopes dovetail with ASC economics by removing sterilizer capital and staff, freeing floor space for revenue-producing rooms. The TGA’s classification framework ensures ASCs maintain compliance without the documentation burden hospitals shoulder. Office-based clinics take smaller slices, driven by capsule endoscopy and cystoscopy services that fit within primary-care workflows. As rural tele-endoscopy gains momentum, community hospitals may leapfrog to portable towers rather than mimicking metro megacenters, creating a niche for scaled-down consoles.

Geography Analysis

Sydney, Melbourne, and Brisbane host most high-volume endoscopy suites, generating more than 60% of Australia endoscopy devices market revenue. Urban density yields patient volumes that justify 4K towers, AI subscriptions, and in-house sterilization hubs. Olympus chose Melbourne for its “Sapphire” reprocessing facility, affirming the city’s biomedical cluster and matching hospitals’ infection-control focus. The plant complies with AS 5369 and ISO 13485, ensuring guaranteed sterility that public tenders increasingly demand.

Rural and remote regions grapple with specialist shortages. Queensland Health’s remote capsule pipeline illustrates a technology fix that sidesteps workforce scarcity, but advanced therapeutic cases still transfer to metro centers. Telehealth infrastructure—6,000+ videoconference endpoints—enables supervised procedures, yet bandwidth and medico-legal frameworks limit adoption for complex interventions. South West Healthcare’s protracted specialist vacancies signal persistent maldistribution despite incentive packages.

State funding disparities influence equipment cycles. NSW’s AUD 12.4 billion infrastructure outlay finances next-generation towers, whereas smaller states rely more on federal grants and private philanthropy. The National Clinical Quality Registry program injects AUD 40 million to collect outcome data, nudging rural hospitals to install scopes that integrate with registry APIs. Private-insurance penetration peaks in urban areas, fostering premium service adoption; public-reliant regions gravitate to cost-efficient, reusable devices with extended life spans.

Competitive Landscape

The Australia endoscopy devices market shows moderate concentration. Olympus, Fujifilm, and Stryker Corporation jointly hold significant revenue share, leveraging bundled scope-tower-service contracts and nationwide field engineering teams. Hospitals prefer one-stop procurement to minimize multi-vendor compatibility headaches, giving incumbents leverage. Olympus’ Sapphire center vertically integrates reprocessing, locking customers into long-term scope exchanges and reducing third-party washer reliance.

Challengers deploy AI and single-use narratives. Medtronic and Pentax Medical promote plug-and-play disposables for duodenoscopy, pitching infection-risk elimination. Optiscan positions its confocal endomicroscope as a leap toward optical biopsies, supported by CRC-P funding. TGA’s UDI rule raises registration overhead, squeezing startups that lack regulatory muscle, which could spark consolidation or OEM partnerships.

Strategic moves continue. Pentax Medical registered an automated flushing sink in June 2025, broadening its consumables ecosystem. Boston Scientific pilots subscription models bundling AI licenses with capital gear, easing hospitals’ cash-flow concerns. Rural service gaps attract tele-endoscopy platform vendors who integrate cloud PACS, satellite links, and ruggedized scopes, yet reimbursement ambiguity hinders scale.

Australia Endoscopy Devices Industry Leaders

Stryker Corporation

FUJIFILM Holdings Corporation

Olympus Corporation

Medtronic Plc.

Hoya Group (PENTAX Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Pentax Medical Singapore registered an endoscope flushing/rinsing sink system with the TGA, enhancing Australian reprocessing workflows.

- September 2024: Olympus Australia inaugurated “Sapphire,” its first flexible endoscope sterilization facility in Melbourne, offering turnkey sterile scope supply.

Australia Endoscopy Devices Market Report Scope

As per the scope of the report, endoscopic devices are minimally invasive that can be inserted into natural openings of the human body, to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries. The Australia endoscopy devices market is segmented by type of device (endoscopes (rigid endoscope, flexible endoscope, capsule endoscope, robot-assisted endoscope), endoscopic operative devices (irrigation/suction system, access device, wound protector, insufflation device, operative manual instrument, other endoscopic operative devices), and visualization equipment), and application (gastroenterology, pulmonology, orthopedic surgery, cardiology, ENT surgery, gynecology, and other applications). The report offers the value (in USD million) for the above segments.

By Device Type

| Endoscopes | Rigid Endoscopes |

| Flexible Endoscopes | |

| Capsule Endoscopes | |

| Robot-assisted Endoscopes | |

| Endoscopic Operative Devices | Irrigation / Suction Systems |

| Access Devices | |

| Wound Protectors | |

| Insufflation Devices | |

| Operative Manual Instruments | |

| Other Operative Devices | |

| Visualization Equipment |

By Application

| Gastroenterology |

| Pulmonology |

| Orthopedic Surgery |

| Cardiology |

| ENT Surgery |

| Gynecology |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgery Centres |

| Office-based / Out-patient Clinics |

| By Device Type | Endoscopes | Rigid Endoscopes |

| Flexible Endoscopes | ||

| Capsule Endoscopes | ||

| Robot-assisted Endoscopes | ||

| Endoscopic Operative Devices | Irrigation / Suction Systems | |

| Access Devices | ||

| Wound Protectors | ||

| Insufflation Devices | ||

| Operative Manual Instruments | ||

| Other Operative Devices | ||

| Visualization Equipment | ||

| By Application | Gastroenterology | |

| Pulmonology | ||

| Orthopedic Surgery | ||

| Cardiology | ||

| ENT Surgery | ||

| Gynecology | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centres | ||

| Office-based / Out-patient Clinics | ||

Key Questions Answered in the Report

What is the current value of the Australia endoscopy devices market?

The market stands at USD 741.64 million in 2025 and is on course to reach USD 970.68 million by 2030.

Which device category leads sales?

Endoscopes remain the top category, accounting for 42.55% of 2024 revenue.

Why are single-use endoscopes gaining interest?

They remove reprocessing-related infection risks and can be cost-competitive in low-volume or high-risk settings, although sustainability concerns persist.

How fast are ambulatory surgery centers expanding their endoscopy volumes?

Procedures performed in ASCs are projected to grow at a 10.17% CAGR through 2030.

Which application segment is growing the quickest?

Pulmonology shows the fastest rise, with a 9.85% CAGR expected through 2030, driven by lung-cancer screening and COPD management.

What impact does the TGA's UDI rule have on suppliers?

It raises compliance costs and documentation requirements, favoring manufacturers with established quality systems and potentially accelerating market consolidation.

Page last updated on: