Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

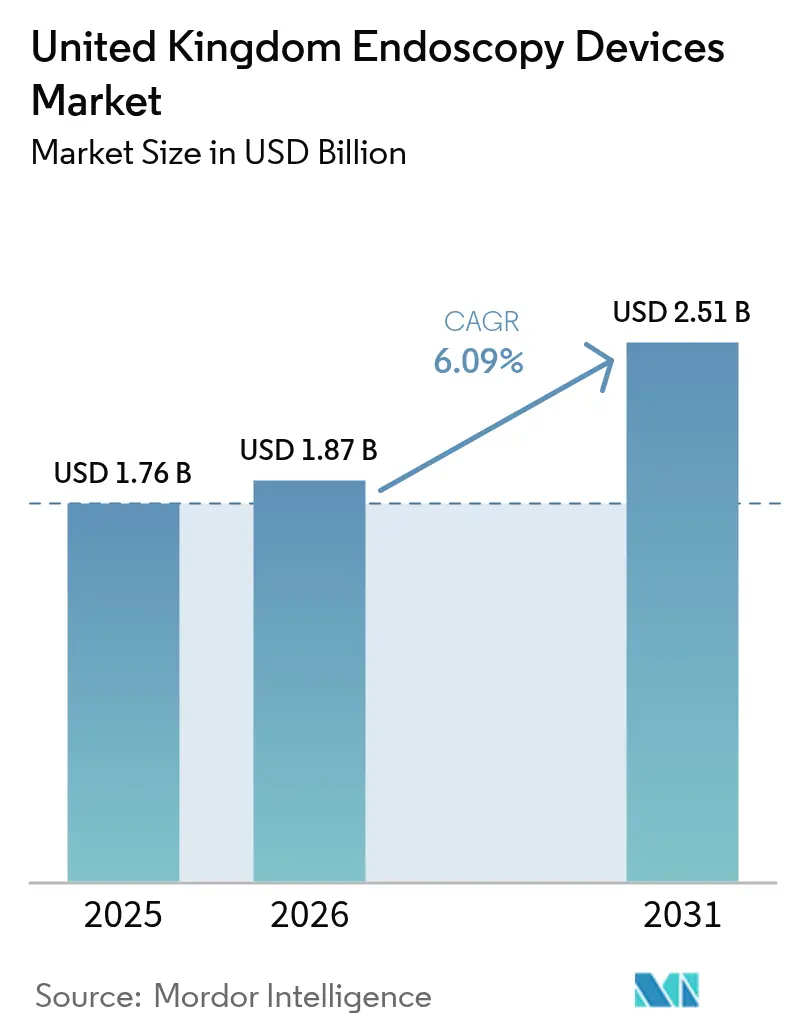

| Base Year Market Size (2025) | USD 1.76 Billion |

| Market Size (2026) | USD 1.87 Billion |

| Market Size (2031) | USD 2.51 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Endoscopy Devices Market Analysis by Mordor Intelligence

The United Kingdom endoscopy devices market size in 2026 is estimated at USD 1.87 billion, growing from 2025 value of USD 1.76 billion with 2031 projections showing USD 2.51 billion, growing at 6.09% CAGR over 2026-2031. Robust demand is anchored in the National Health Service’s (NHS) strategic swing toward preventive diagnostics, the independent sector’s sustained capacity expansion and the accelerated rollout of AI-enabled imaging that shortens procedure times while improving adenoma detection accuracy. Persistent public-sector capacity bottlenecks are pushing more bowel-cancer screening, bronchoscopy and day-case gastrointestinal procedures into private treatment centers, intensifying equipment refresh cycles across both public and private facilities. In addition, the temporary UKCA/CE convergence window shields vendors from regulatory uncertainty, encouraging timely product launches and easing procurement barriers. On the supply side, single-use platforms and AI-assisted visualization systems are gaining ground as hospitals look to mitigate infection litigation risk and curb sterile-services workload. Meanwhile, Brexit-linked component inflation and a chronic shortage of trained endoscopists provide a counterweight to otherwise healthy underlying demand.

Key Report Takeaways

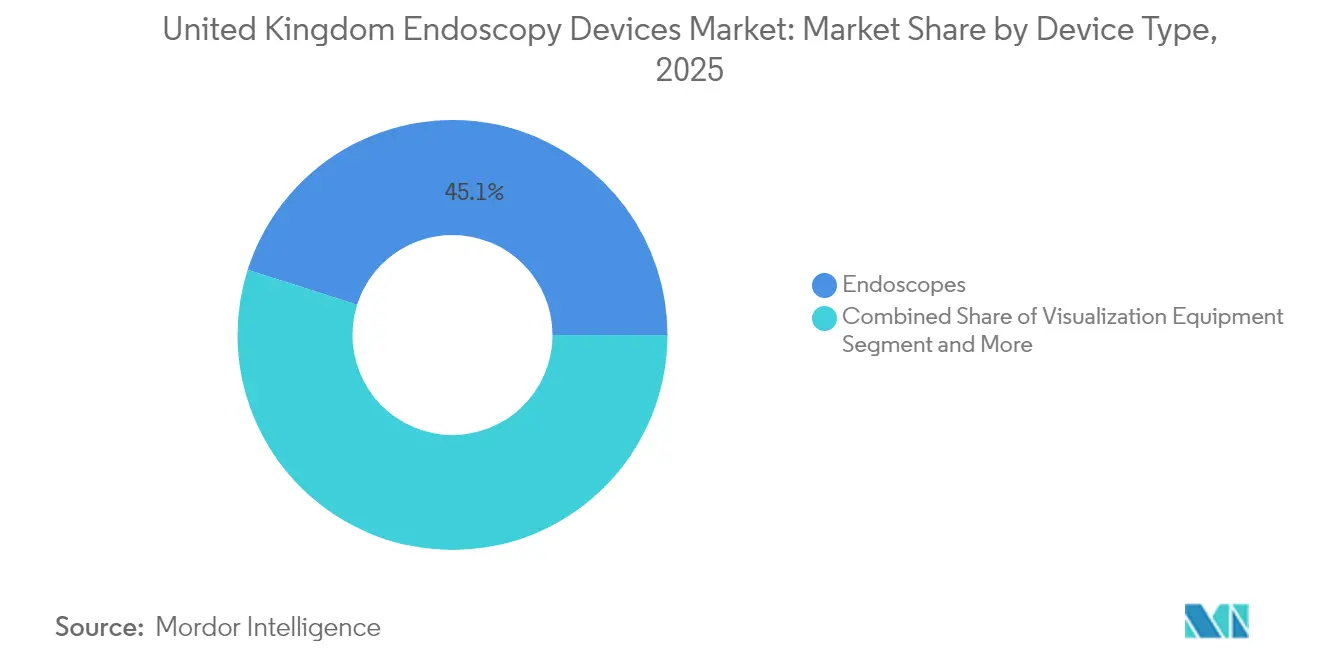

- By device type, endoscopes led with 45.10% of United Kingdom endoscopy devices market share in 2025, while visualization equipment is set to compound at an 10.78% CAGR through 2031.

- By application, gastroenterology accounted for 51.10% of the United Kingdom endoscopy devices market size in 2025 and urology is projected to record the fastest 9.42% CAGR between 2026-2031.

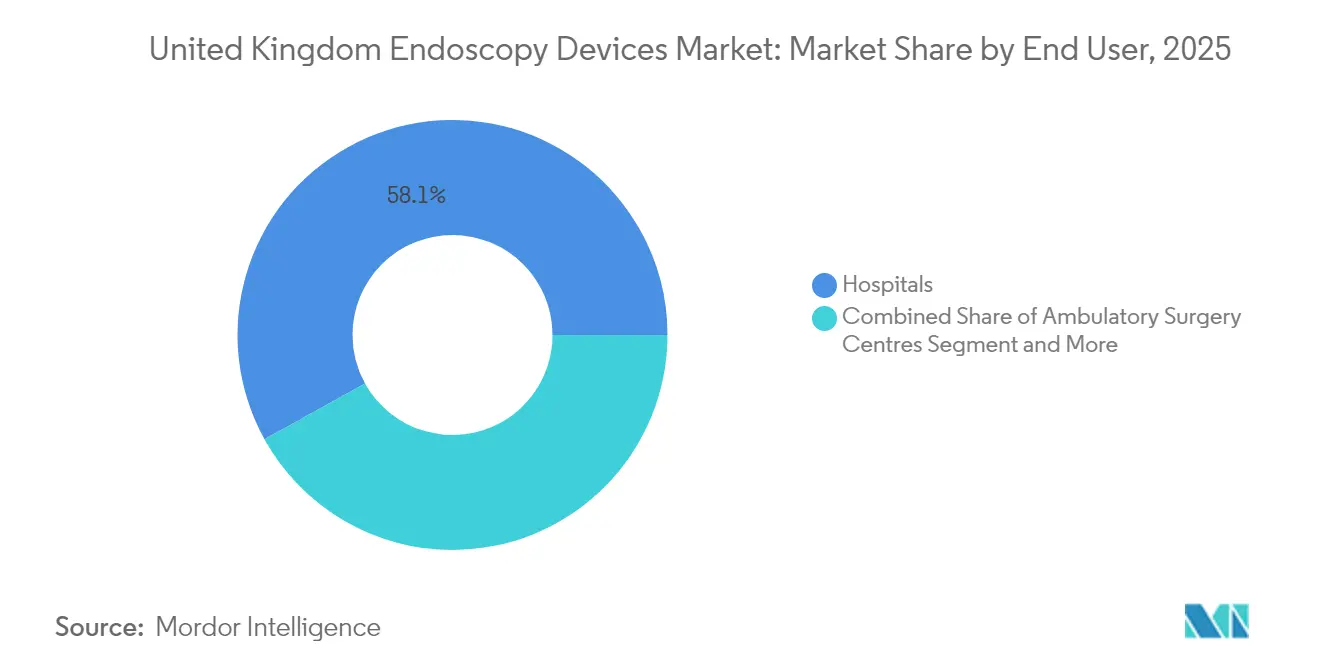

- By end user, hospitals captured 58.05% revenue in 2025; ambulatory surgery centers represent the quickest-growing channel with a 11.68% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NHS bowel-cancer screening expansions boost colonoscopy volumes | +1.2% | National, concentrated in England | Medium term (2-4 years) |

| AI-enhanced polyp-detection software accelerates diagnostic adoption | +0.8% | National, early adoption in major NHS trusts | Short term (≤ 2 years) |

| Disposable bronchoscopes mitigate cross-infection & reprocessing costs | +0.6% | National, NHS and independent sector | Medium term (2-4 years) |

| Surge in day-case GI procedures across UK independent sector treatment centres | +0.9% | National, concentrated in London and South-East | Short term (≤ 2 years) |

| UKCA/CE convergence period lowers regulatory uncertainty for vendors | +0.4% | National | Short term (≤ 2 years) |

| Sterile-services workforce shortages drive outsourcing of scope reprocessing | +0.5% | National, acute in NHS trusts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

NHS Bowel-Cancer Screening Expansions Boost Colonoscopy Volumes

NHS England’s GBP 6 million colon-capsule endoscopy pilot delivered 2,288 procedures across 51 trusts in 2024, underscoring a deliberate pivot toward less-invasive diagnostics that demand fewer clinical endoscopists[1]NHS England, “NHS England colon capsule endoscopy pilot programme,” england.nhs.uk. Early success has encouraged parallel rollouts in Scotland and Wales, signalling national scalability that will influence equipment procurement for both capsule systems and supporting visualization towers. Large-city teaching hospitals such as UCLH, Guy’s & St Thomas’ and Milton Keynes University Hospital are already reserving dedicated lists for capsule studies, building predictable throughput for vendors. As acceptance widens, traditional colonoscope fleets face slower replacement in favor of hybrid portfolios that include capsules for screening and conventional scopes for therapeutic follow-up. The resulting mixed-modality demand supports continued revenue growth even in the face of workforce scarcity.

AI-Enhanced Polyp-Detection Software Accelerates Diagnostic Adoption

Completion of the COLO-DETECT trial and NHS deployment of the GI Genius platform mark a watershed in UK gastroenterology, marrying 4K imaging with real-time lesion identification. Trusts adopting the software report higher adenoma detection and shorter withdrawal times, translating into higher list utilization and reduced overtime payments. Vendor-run training programs allow trainee endoscopists to achieve competency faster, partially offsetting attrition among experienced clinicians. Integration with existing picture-archiving systems has proven smooth under the MHRA’s digital-health pre-submission route, encouraging broader uptake before the UKCA deadline. As early adopters demonstrate measurable productivity gains, peer organisations face mounting pressure to budget for AI add-ons during the next capital cycle.

Disposable Bronchoscopes Mitigate Cross-Infection & Reprocessing Costs

High-profile litigation over duodenoscope-borne infections has heightened NHS risk perceptions, prompting many trusts to test single-use bronchoscopes in intensive-care and bronchoscopy suites. With mobile decontamination hubs processing up to 195 scopes per 12-hour shift, sterile-services staffing shortages remain acute, making disposable devices attractive despite unit-cost premiums. Insurance carriers are responding by offering lower premiums when trusts commit to single-use programs, effectively shifting total-cost equations in favor of disposables. Independent sector hospitals, less encumbered by pay-cap procurement rules, have moved even faster, aiming to differentiate on infection-control metrics for a private-payer audience. As volumes climb, manufacturers achieve scale economies that narrow the price gap versus reusable alternatives.

Surge in Day-Case GI Procedures Across UK Independent Treatment Centres

Private healthcare admissions hit a record 898,000 in 2023, propelled by 9% yearly growth in diagnostic upper-GI endoscopies and colonoscopies. Independent centres now host 54% of all JAG-accredited sites, a sharp contrast to the NHS’s 35% share. These providers are clustering in wealthier regions such as London and the South-East where insured patient numbers are greatest; consequently, equipment vendors are prioritising local service hubs to guarantee rapid technical support. The shift to same-day pathways aligns with payer interest in shorter lengths of stay, further entrenching independent facilities as procurement powerhouses for advanced visualization, AI modules and capsule systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-budget squeeze in NHS hospital trusts | -0.7% | National, acute in England | Medium term (2-4 years) |

| Reusable-scope infection lawsuits raise insurance premiums | -0.4% | National, concentrated in NHS trusts | Short term (≤ 2 years) |

| Endoscopist workforce gap limits throughput | -1.1% | National, severe in secondary care | Long term (≥ 4 years) |

| Brexit-linked supply-chain friction inflates component costs | -0.3% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Endoscopist Workforce Gap Limits Throughput

A 2023 pan-workforce survey recorded a 31.5% five-year intention-to-leave among clinical endoscopists, who already conduct 78% more sessions per capita than consultant gastroenterologists. Advanced ERCP capacity is even more fragile, with practitioners over 55 registering 76.6% exit intentions, jeopardising training pipelines. Just 9% of gastroenterology trainees are on track for ERCP competence at completion, while over a quarter plan to leave the NHS entirely. NHS England’s long-term workforce plan requires 40,000 additional doctors to meet OECD averages, but medical-school caps and limited registrar slots undermine the objective. Without enough operators, new imaging towers risk under-utilisation, placing a structural ceiling on the growth trajectory of the United Kingdom endoscopy devices market.

Capital-Budget Squeeze in NHS Hospital Trusts

Secondary-care medical vacancies amounted to 10,165 posts in England as of 2025, equal to 6.2% of all medical positions[2]British Medical Association, “Medical staffing in the NHS,” bma.org.uk. Staffing shortfalls compel trusts to divert scarce capital toward locum and waiting-list initiative payments, delaying upgrades to 4K towers, AI servers and robotic endoscopy consoles. Although NHS Supply Chain offers leasing frameworks, tightening Integrated Care Board budgets limit uptake. Consequently, visualization-equipment vendors increasingly market service-as-subscription models that convert capital expenditure into operating expense. The private sector, free from public-sector budget cycles, exploits the gap to modernise rapidly, intensifying competitive contrast.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Endoscopes Lead, Visualization Accelerates

Endoscopes accounted for 45.10% of United Kingdom endoscopy devices market share in 2025, confirming their centrality to both diagnostic and therapeutic workflows across public and private settings. Flexible scopes dominate because they serve high-volume gastroenterology and pulmonology lists, while rigid scopes remain essential for niche ENT and orthopedic procedures with higher per-case value. Capsule endoscope uptake jumped after the 51-trust NHS pilot, demonstrating patient preference for non-invasive screening and enabling hospitals to tackle growing bowel-cancer test backlogs without proportional staffing increases. In parallel, robotic-compatible scopes are gaining prominence as the NHS targets 500,000 robot-assisted operations annually by 2035, embedding endoscopy visualization within surgical arms.

Visualization equipment is the fastest-growing device cluster, projected at an 10.78% CAGR thanks to 4K procurement mandates and AI overlay requirements that transform legacy towers into decision-support hubs. Early adopters cite measurable improvement in adenoma detection, cut-through times and theatre utilisation, making investment justifiable even amid capital constraints. Endoscopic operative devices and single-use accessories also benefit: cross-contamination lawsuits and rising sterilisation premiums encourage hospitals to dedicate more of the United Kingdom endoscopy devices market size toward disposable snares, biopsy forceps and single-use bronchoscopes that reduce decontamination workload.

By Application: Gastroenterology Dominance, Urology Momentum

Gastroenterology commanded 51.10% of the United Kingdom endoscopy devices market size in 2025, reflecting sustained bowel-cancer screening expansions, rising Barrett’s oesophagus surveillance and the independent sector’s 9% surge in diagnostic upper-GI cases. Procedure breadth—from screening colonoscopy to advanced EMR—anchors demand for high-definition scopes and AI decision support. Capsules augment rather than cannibalise conventional scopes because therapeutic interventions still require traditional access.

Urology is forecast to expand at a 9.42% CAGR, the fastest among applications, fuelled by demographic ageing and widespread commissioning of robotic-assisted partial nephrectomy and prostatectomy services. NHS framework agreements covering integrated robot instrumentation bundles are stimulating separate procurement lines for dedicated flexible ureteroscopes and in-vivo imaging fibres. Pulmonology maintains solid mid-single-digit growth, underpinned by disposable bronchoscopes that mitigate infection risk in critical care. ENT, gynecology and neurology procedures post stable gains, benefitting indirectly from improved outpatient pathways that release theatre time for additional minimally invasive cases.

By End User: Hospitals Dominate, Ambulatory Centres Accelerate

Hospitals held 58.05% of revenue in 2025, consolidating the bulk of advanced ERCP, ESD and interventional pulmonology work. The channel benefits from NHS Supply Chain volume purchasing and embedded sterile-services infrastructure, yet faces attrition pressures as endoscopists seek better work-life balance in community settings. Ambulatory surgery centres, by contrast, are projected to chart a 11.68% CAGR, buoyed by day-case targets that incentivise shifting routine diagnostic lists out of acute sites. Private providers operate 106 JAG-accredited centres—equal to 54% of national accredited capacity—and often adopt the newest visualization stacks first to lure consultants and insured patients.

Outpatient clinics leverage capsule technology and AI triage to offer rapid turnaround with minimal infrastructure, appealing to self-pay consumers deterred by long NHS waits. Office-based procedures, including transnasal endoscopy, have started to flourish after BMJ-documented service-quality gains in 2025. Equipment vendors have responded by engineering portable towers and cloud-based software licences suited to small-footprint environments, broadening the reach of the United Kingdom endoscopy devices market.

Geography Analysis

England dominates consumption, hosting 87.2% of respondents in the latest workforce census and the lion’s share of private admissions growth, which rose by 23,800 insured cases in London alone during 2023. Large Integrated Care Systems such as North-West London and Greater Manchester pool capital budgets to acquire multipurpose towers that can be shared across trust networks, promoting standardisation and vendor lock-in. The South-East follows closely owing to dense private-insurance penetration; facilities in Surrey and Kent now operate extended evening lists to absorb spill-over demand from the capital.

Scotland contributes about 8.2% of the workforce yet punches above its weight in technology adoption, pioneering nationwide capsule rollouts that mirror England’s pilot but with stronger central funding guarantees. Wales exhibits the highest self-pay growth rate at 11%, driven by patients crossing the Severn Bridge for faster diagnostics when NHS timelines stretch. Northern Ireland, while smaller in absolute numbers, posted a dramatic 144% spike in self-funded admissions, creating fertile ground for distributors that can navigate its distinct Health and Social Care procurement.

The Brexit-induced customs regime affects all regions but is felt acutely in Celtic nations where ports are less diversified; supply-chain buffers are now standard contract clauses, incentivising vendors to warehouse in Birmingham or Liverpool. Although the UKCA/CE convergence grace period runs until 2028, devolved regulators have aligned documentation to avoid intra-UK barriers, smoothing national rollouts even for smaller suppliers.

Competitive Landscape

Olympus, Boston Scientific and Medtronic remain the anchor tenants of NHS Supply Chain catalogues, together accounting for a majority of tenders for high-definition towers, flexible scopes and therapeutic accessories. Their entrenched service footprints, including field engineers stationed within major teaching hospitals, create formidable switching costs. Mid-tier challengers such as Pentax and Fujifilm are elevating share through HD chips and ergonomics upgrades; Fujifilm’s 2025 acquisition of Aquilant’s endoscopy assets is expected to streamline after-sales service routes, increasing competitiveness in replacement cycles.

AI-native entrants leverage algorithmic intellectual property rather than hardware alone, partnering with trusts to embed software licences into existing towers; the COLO-DETECT consortium exemplifies this hybrid model. Single-use specialists operate on unit economics that become favourable as litigation-driven premium hikes bite into reusable margins, particularly for bronchoscopes and duodenoscopes. Mobile decontamination providers offer interim capacity, forging tri-party agreements with hospitals and scope makers that lock in consumable supply, further reshaping channel power. Overall, competition centres on demonstrable efficiency gains—faster turnaround, higher detection, lower infection risk—rather than pure capital cost, aligning with the operational objectives of cash-constrained yet performance-driven hospital boards.

United Kingdom Endoscopy Devices Industry Leaders

Boston Scientific Corporation

Cook Medical

Richard Wolf GmbH

Medtronic PLC

Fujifilm Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: FUJIFILM Healthcare UK completed an asset purchase agreement for Aquilant Endoscopy’s Fujifilm business, adding capital equipment plus proprietary therapeutic accessories to its domestic portfolio.

- May 2025: Creo Medical launched SpydrBlade Flex, a multimodal endoscopic device engineered for precision cancer resection, with the first customer site live in the United Kingdom and the European Union.

United Kingdom Endoscopy Devices Market Report Scope

As per the scope of this report, endoscopy devices are minimally invasive and can be inserted into natural openings of the human body, in order to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries. The UK endoscopy devices market is segmented by type of device (endoscopes, endoscopic operative devices, and visualization equipment) and application (gastroenterology, pulmonology, ENT surgery, gynecology, neurology, urology, and other applications). The report offers the value (in USD million) for the above segments.

By Device Type

| Endoscopes | Rigid Endoscope |

| Flexible Endoscope | |

| Capsule Endoscope | |

| Robot-assisted Endoscope | |

| Endoscopic Operative Devices | Irrigation / Suction Systems |

| Access Devices | |

| Operative Manual Instruments | |

| Single-use Accessories | |

| Visualization Equipment |

By Application

| Gastroenterology |

| Pulmonology |

| ENT Surgery |

| Gynecology |

| Neurology |

| Urology |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgery Centres |

| Office-based / Out-patient Clinics |

| By Device Type | Endoscopes | Rigid Endoscope |

| Flexible Endoscope | ||

| Capsule Endoscope | ||

| Robot-assisted Endoscope | ||

| Endoscopic Operative Devices | Irrigation / Suction Systems | |

| Access Devices | ||

| Operative Manual Instruments | ||

| Single-use Accessories | ||

| Visualization Equipment | ||

| By Application | Gastroenterology | |

| Pulmonology | ||

| ENT Surgery | ||

| Gynecology | ||

| Neurology | ||

| Urology | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centres | ||

| Office-based / Out-patient Clinics | ||

Key Questions Answered in the Report

How large is the United Kingdom endoscopy devices market in 2026?

The market is valued at USD 1.87 billion in 2026 and is projected to reach USD 2.51 billion by 2031.

What is the forecast CAGR for United Kingdom endoscopy device sales?

The overall market is expected to expand at a 6.09% CAGR between 2026 and 2031.

Which device category generates the most revenue?

Endoscopes remain the largest device class, accounting for 45.10% of sales in 2025.

Which application area is growing the fastest?

Urology shows the quickest trajectory, with a projected 9.42% CAGR through 2031.

Why are single-use endoscopes gaining traction in the UK?

Rising infection-control litigation, escalating reprocessing costs and shortages in sterile-services staffing are driving hospitals toward disposable scopes.

How is AI technology influencing the market?

AI-assisted polyp-detection platforms are boosting adenoma detection and lowering procedure times, prompting many NHS trusts to integrate AI modules into new visualization towers.

Page last updated on: