Spain Endoscopy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

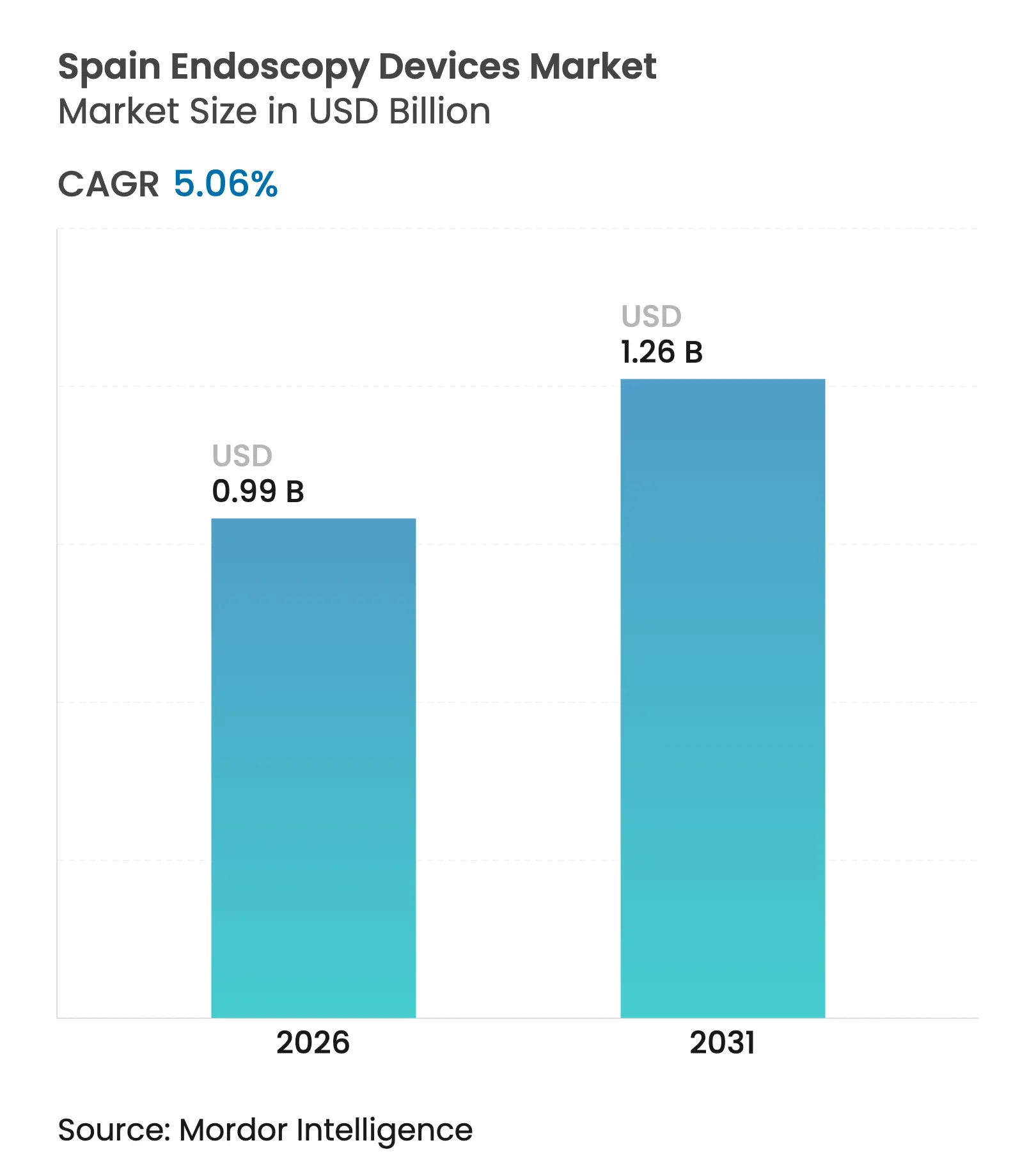

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.26 Billion |

| Growth Rate (2026 - 2031) | 5.06 % CAGR |

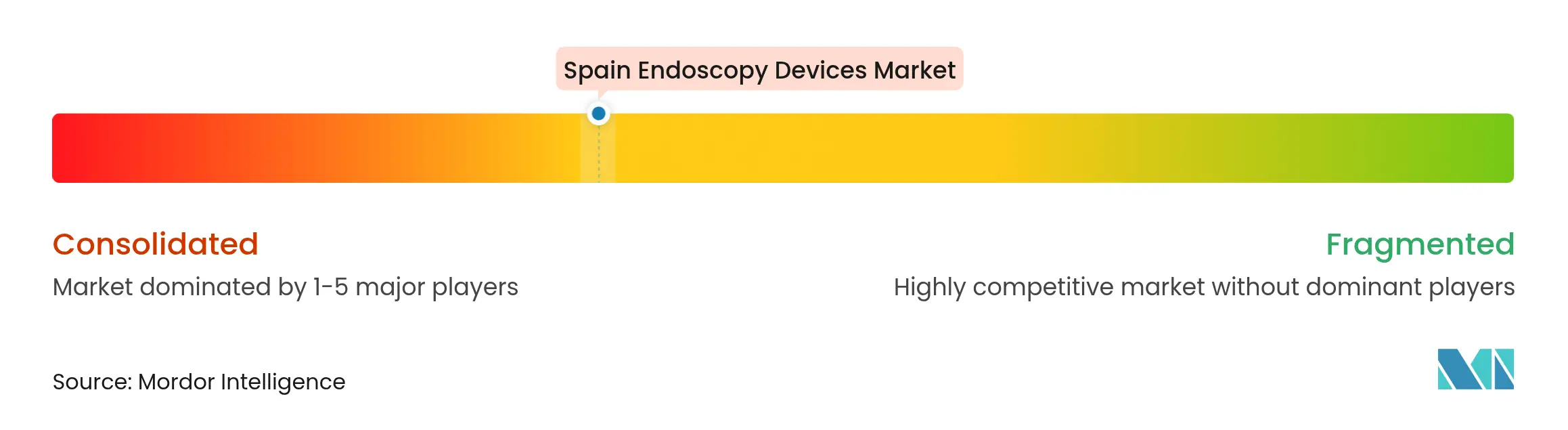

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Spain Endoscopy Devices Market Analysis by Mordor Intelligence

The Spain endoscopy devices market size was valued at USD 940 million in 2025 and estimated to grow from USD 987.56 million in 2026 to reach USD 1.26 billion by 2031, at a CAGR of 5.06% during the forecast period (2026-2031). Growing demand for minimally invasive procedures, higher diagnostic volumes from colorectal-cancer screening, and rapid upgrades to HD and AI-ready platforms are accelerating equipment refresh cycles. Procedure throughput is also rising as Spain’s private insurance enrollment climbs, lifting device demand in ambulatory surgery centers. At the same time, the aging population is pushing up gastrointestinal disease prevalence, reinforcing the need for advanced visualization systems that shorten hospital stays and cut overall treatment costs. Leading manufacturers are responding with single-use scopes that address infection-control gaps and with software updates that embed real-time lesion-recognition algorithms.

Key Report Takeaways

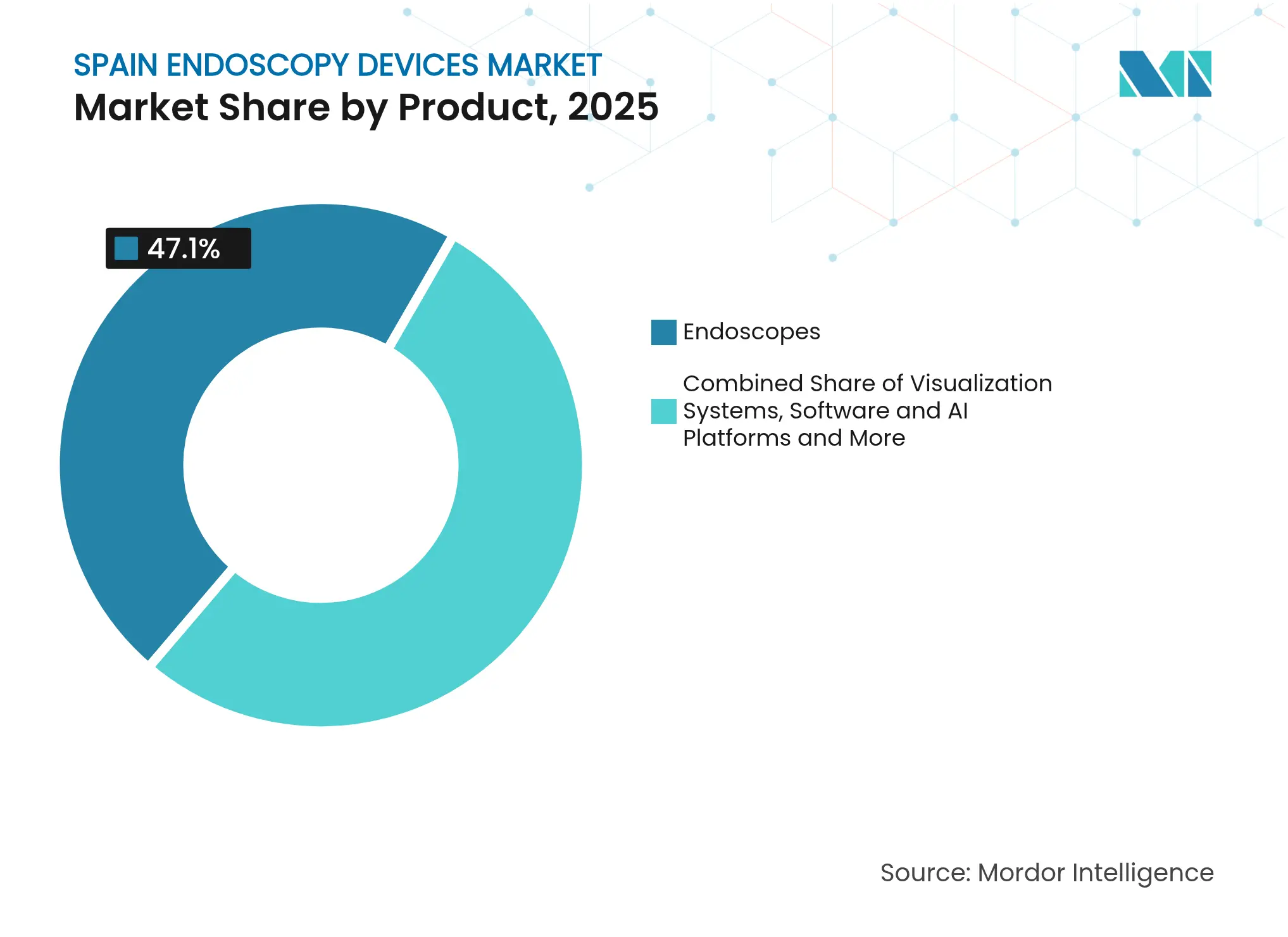

- By product category, endoscopes led with 47.10% of Spain endoscopy devices market share in 2025, while disposable scopes are advancing at a 11.4% CAGR through 2031.

- By application, gastroenterology accounted for a 56.60% share of the Spain endoscopy devices market size in 2025 and pulmonology is growing fastest at 8.7% CAGR to 2031.

- By end user, public hospitals held 51.20% of Spain endoscopy devices market share in 2025; ambulatory surgery centers are projected to expand at an 8.2% CAGR through 2031.

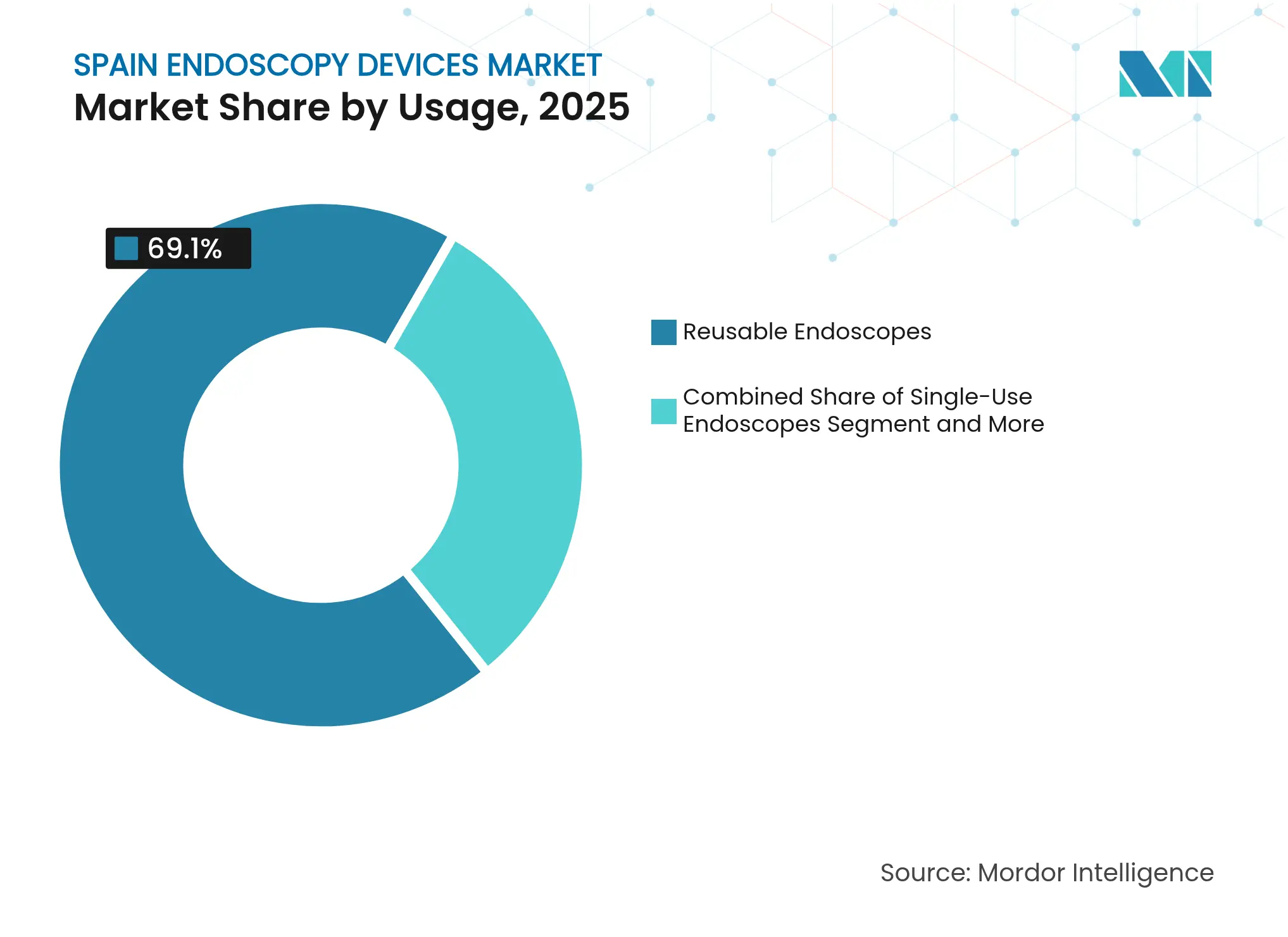

- By usage type, reusable systems dominated with 69.10% share in 2025, whereas disposable scopes are forecast to post a 11.4% CAGR between 2026 and 2031.

- By technology, 2D HD platforms captured 63.00% share of the Spain endoscopy devices market size in 2025 and AI-assisted systems are set to rise at a 14.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Endoscopy Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising prevalence of

GI disorders & cancer in aging population

Rising prevalence of

GI disorders & cancer in aging population

| +1.8% | Asturias, Castilla y León, Galicia | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+1.8%

| Geographic Relevance:

Asturias, Castilla y

León, Galicia

| Impact Timeline:

Medium term (2-4

years)

|

Shift toward

minimally invasive procedures

Shift toward

minimally invasive procedures

| +1.2% | Madrid, Barcelona, Valencia | Short term (≤ 2 years) | |||

Technological

advances in HD/4K imaging & AI

Technological

advances in HD/4K imaging & AI

| +1.5% | Major public and private hospitals | Medium term (2-4 years) | |||

Growing penetration

of private health insurance

Growing penetration

of private health insurance

| +0.9% | Madrid, Barcelona, Basque Country | Long term (≥ 5 years) | |||

Replacement cycle

for robotic & digital platforms

Replacement cycle

for robotic & digital platforms

| +0.7% | Teaching and specialty centers | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Prevalence of GI Disorders & Cancer in an Aging Spanish Population

Colorectal cancer is now Spain’s second-most common malignancy, and 20.5% of Spaniards are already over 65 years old. National screening expansion is boosting colonoscopy volumes, and the TEOGIC cohort anticipates a 15%-20% procedure jump by 2027. Providers therefore prioritize high-definition wide-field scopes and AI computer-aided detection (CADe) modules to spot flat lesions early. Hospitals in Galicia and Asturias have accelerated equipment replacement schedules, citing higher regional incidence of early-onset GI cancers. Manufacturers benefit because tender specifications now require image-enhancement modes such as narrow-band-imaging plus cloud-based analytics.

Shift Toward Minimally Invasive Procedures Reducing Hospital Stay & Costs

Public hospitals use these gains to shrink waiting lists, while private groups market same-day discharge packages. Insurers now reimburse laparoscopic or endoscopic approaches at parity with traditional surgery, reinforcing uptake. Device vendors increasingly bundle energy sources, insufflators, and imaging towers, offering cost-per-procedure contracts that fit constrained SNS budgets.

Rapid Technological Advances in HD/4K Imaging and AI Integration

AI-assisted colonoscopy improves adenoma detection by 26% and polyp detection by 30% over standard practice[1]Anson Mwango et al., “Artificial Intelligence-Aided Colonoscopy,” ijgii.org. Olympus secured CE approval for cloud-based CADe devices that slash reading time to under four minutes. Early adopters include large Madrid hospitals, which report shorter list backlogs and improved training for junior endoscopists. Integrating 4K chip-on-tip cameras with AI software also lowers biopsy rates, saving about EUR 320 per colonoscopy.

Growing Penetration of Private Health Insurance Driving Procedure Volumes

Private insurance in Spain reached 12 million policies in 2024, equal to 25.8% of the population. Private hospitals, owning 32% of national beds, rapidly refresh their fleets with disposable bronchoscopes and premium video towers to differentiate service quality. Ambulatory surgery centers cluster in Madrid and Catalonia, where coverage tops 30%, and collectively log double-digit growth in screening colonoscopy. Suppliers often pilot innovations in these centers before rolling nationwide.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

High capital &

maintenance costs

High capital &

maintenance costs

| -1.2% | Regional public hospitals | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:

-1.2%

| Geographic Relevance:

Regional public

hospitals

| Impact Timeline:

Short term (≤ 2

years)

|

Complex reprocessing

requirements

Complex reprocessing

requirements

| -0.9% | Older facilities nationwide | Medium term (2-4 years) | |||

Shortage of trained

nurses & technicians

Shortage of trained

nurses & technicians

| -1.4% | Rural areas, small cities | Long term (≥ 5 years) | |||

| Source: Mordor Intelligence | ||||||

High Capital and Lifecycle Maintenance Costs Limiting Adoption

Premium video systems cost EUR 80,000-150,000, while annual service fees reach 8-12% of purchase price. Spain’s NHS allocates only 7.9% of its health budget to medical technologies, below the EU mean of 8.3%. Smaller regional hospitals therefore stretch equipment beyond recommended years of use, widening the technology gap with tertiary centers. Cost-effectiveness thresholds hover at EUR 22,000-25,000 per QALY, restricting approval for premium upgrades unless they clearly displace follow-up procedures.

Complex Reprocessing Requirements Raising Total Cost of Ownership

Only 30% of Spanish units employ automated washer-disinfectors and merely half renew cleaning fluid after each cycle, fueling 8.69% scope contamination in bronchoscopes. The labor, consumables, and downtime tied to reprocessing inflate per-procedure costs. Hospitals that trial single-use scopes eliminate these steps yet must balance higher device prices against reduced nosocomial-infection risk.

Segment Analysis

By Product: Endoscopes Lead While Disposables Surge

Endoscopes commanded 47.10% of Spain endoscopy devices market size in 2025, underpinned by entrenched use across gastroenterology and pulmonology suites. Investment priorities remain centered on high-definition video gastroscopes and colonoscopes that support virtual-chromoscopy modes. Disposable scopes, however, are accelerating at a 11.4% CAGR as infection-control audits expose reprocessing gaps; AI-capable processors that pair seamlessly with single-use models are easing the transition.

Visualization towers rank second by revenue, driven by progressive rollouts of 4K and near-infrared systems that improve lesion contrast and facilitate fluorescence imaging. Endotherapy instruments trail but enjoy robust uptake in therapeutic ESD and POEM procedures. Software platforms embedding computer-aided detection illustrate how Spain endoscopy devices market fosters a shift from hardware-centric procurement toward integrated digital ecosystems.

Note: Segment shares of all individual segments available upon report purchase

By Application: Gastroenterology Dominates While Pulmonology Accelerates

Gastroenterology represented 56.60% of Spain endoscopy devices market share in 2025, tied to nationwide colorectal-cancer screening that targets full eligibility coverage by 2026. Capsule endoscopy and bariatric endoluminal therapies broaden procedural mix, supporting repeat purchases of slim scopes and disposable overtubes. Pulmonology usage is expanding at a 8.7% CAGR as chronic respiratory diseases and post-COVID sequelae raise bronchoscopic volumes.

AI staging modules for lung-nodule assessment and single-use bronchoscopes combine to shorten ICU turnover times. ENT and gynecology segments remain smaller yet benefit from 3-chip rigid camera heads that migrate down the cost curve. Spain endoscopy devices industry players also note rising intraoperative visualization demand in hybrid ORs, pressuring suppliers to integrate scopes with surgical navigation systems.

By End User: Public Hospitals Lead While ASCs Grow Rapidly

Public hospitals held 51.20% of Spain endoscopy devices market size in 2025, leveraging centralized procurement to negotiate bundled pricing that spans processors, light sources, and service. Even so, multi-year austerity measures prolong replacement cycles, prompting some facilities to refurbish existing equipment rather than buy new. Ambulatory surgery centers are registering an 8.2% CAGR, powered by private insurance volumes and a push toward same-day colonoscopy and ERCP.

Private hospitals prioritize premium experience; 57% actively promote endoscopy suites in marketing campaigns. Specialty clinics carve out niches in bariatric and fertility procedures, sourcing compact video systems that fit smaller footprints. The decentralized uptake of AI cloud analytics further levels technical capabilities between tertiary and community settings.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Usage: Reusable Dominates While Disposables Gain Momentum

Reusable systems accounted for 69.10% of Spain endoscopy devices market share in 2025, justified by lower amortized cost over hundreds of procedures. Yet contamination studies revealing 22.31% gastroscope positivity have spurred procurement of single-use devices, especially for high-risk patients. Hospitals evaluate hybrid models combining reusable imaging cores with disposable distal ends that cap infection risk without forfeiting advanced optics.

Third-party reprocessed scopes linger in niche roles where budget pressures trump performance. However, SNS guidance now spotlights sterility over capital outlay, likely redirecting funds toward disposables in ICU bronchoscopy and infectious-disease wards. Spain endoscopy devices market size thus reflects a dual track where reusable fleets coexist with fast-growing disposable lines.

Note: Segment shares of all individual segments available upon report purchase

By Technology: 2D HD Leads While AI-Assisted Grows Fastest

2D HD captured 63.00% of Spain endoscopy devices market size in 2025, valued for affordability and established workflows. 4K/UHD gains momentum in oncology centers, delivering crisper mucosal patterns that aid Barrett’s surveillance. Robotic and 3D systems occupy specialist niches for complex gastrointestinal dissections. AI-assisted platforms, posting a 14.6% CAGR, integrate cloud connectivity so updates deploy simultaneously across national fleets.

Leading teaching hospitals report AI modules boosting adenoma detection rates while trimming pathologist referrals. Manufacturers pair CADe algorithms with scope tracking sensors that map withdrawal speed, standardizing quality across operators. Spain endoscopy devices industry innovation now emphasizes software feature releases alongside optical upgrades, mirroring trends in broader digital surgery.

Geography Analysis

Regional spending patterns strongly shape Spain endoscopy devices market. Madrid, Catalonia, and the Basque Country, where per-capita health budgets run 20% above the national average, pioneer AI-ready 4K towers and single-use bronchoscopes. Penetration of AI colonoscopy exceeds 35% in teaching hospitals in these hubs, versus under 10% in Castilla-La Mancha. Rural provinces such as Extremadura endure average wait times of 76 days for elective endoscopy, double that of urban peers, reflecting both staffing gaps and scarce capital allocations.

Northern regions with older populations—Asturias, Castilla y León, and Galicia—see higher colorectal-cancer incidence, prompting accelerated replacement of legacy colonoscopes with wide-angle 330° viewing models. Hospitals there also engage in multicenter trials of capsule-based screening to offset personnel shortages. Meanwhile, coastal tourist destinations invest in ambulatory units to serve both residents and medical travelers, lifting procedure counts during summer months.

Private-sector dominance varies sharply: private facilities provide 42% of endoscopy capacity in Madrid but under 20% in Andalusia. Consequently, suppliers tailor commercial strategies by region, bundling service contracts in the south while promoting AI subscriptions in the capital. Spain endoscopy devices market size therefore maps closely to localized wealth, demographic risk, and the interplay between SNS and private insurers.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Spain endoscopy devices market demonstrates moderate concentration: Olympus, Cook Medical, Boston Scientific Corporation, and Medtronic together hold a significant share. Olympus leads at around 30% due to its breadth of gastroenterology platforms and strong service infrastructure. KARL STORZ broadened its reach into robotic visualization after acquiring Asensus Surgical and the LUNA system, signaling strategic commitment to digital surgery[3]KARL STORZ, “Acquisition of Asensus Surgical,” karlstorz.com. Fujifilm leverages the ELUXEO 8000 processor’s 4-LED light source to court hospitals upgrading to linked-color imaging.

Medtronic positions its AI-powered GI Genius module as a vendor-neutral add-on, partnering with both Fujifilm and Olympus to widen platform reach. Ambu disrupts with sterile single-use scopes, winning tenders in ICUs where cross-contamination penalties are severe. Niche Spanish firms supply specialty accessories—pediatric forceps, bariatric suturing kits—that global majors incorporate through OEM deals.

Competitive tactics revolve around financing schemes such as pay-per-use and managed-equipment-services that transfer capital risk off public hospitals’ balance sheets. Vendors also embed cloud dashboards that benchmark site-level adenoma detection rates, nurturing long-term subscriptions. Emerging competition comes from imaging-AI startups offering SaaS plugins that retrofit legacy HD towers, undercutting hardware replacement cycles.

Spain Endoscopy Devices Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Fujifilm introduced the ELUXEO 800 Series endoscopes and ELUXEO 8000 processor in Spain, adding multi-light LED technology and enhanced color algorithms.

- September 2024: KARL STORZ finalized its purchase of Asensus Surgical, reinforcing robotic and digital visualization capabilities for future Spanish rollouts.

Table of Contents for Spain Endoscopy Devices Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising Prevalence of GI Disorders & Cancer in Ageing Spanish Population Boosting Diagnostic Endoscopy Demand

- 4.2.2Shift Toward Minimally-Invasive Procedures Reducing Hospital Stay & Costs across Spanish Healthcare

- 4.2.3Rapid Technological Advances in HD/4K Imaging and AI Integration Enhancing Clinical Accuracy & Adoption

- 4.2.4Growing Penetration of Private Health Insurance Driving Procedure Volumes in Private Hospitals & ASCs

- 4.2.5Replacement Cycle Driven by Robotic & Digital Endoscopy Platforms Elevating Capital Spend

- 4.3Market Restraints

- 4.3.1High Capital & Lifecycle Maintenance Costs Limiting Adoption in Budget-Constrained Public Hospitals

- 4.3.2Complex Reprocessing Requirements Raising Total Cost of Ownership and Infection-Control Challenges

- 4.3.3Shortage of Trained Endoscopy Nurses & Technicians Curtailing Throughput Capacity

- 4.4Regulatory Outlook

- 4.5Technological Outlook

- 4.6Porter's Five Forces

- 4.6.1Threat of New Entrants

- 4.6.2Bargaining Power of Buyers

- 4.6.3Bargaining Power of Suppliers

- 4.6.4Threat of Substitutes

- 4.6.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Product

- 5.1.1Endoscopes

- 5.1.1.1Flexible Endoscopes

- 5.1.1.2Rigid Endoscopes

- 5.1.1.3Capsule Endoscopes

- 5.1.1.4Robot-Assisted Endoscopes

- 5.1.1.5Disposable / Single-Use Endoscopes

- 5.1.2Visualization Systems

- 5.1.2.1Video Processors & Light Sources

- 5.1.2.2Camera Heads & Monitors

- 5.1.3Operative Devices & Accessories

- 5.1.3.1Endotherapy & Energy Devices

- 5.1.3.2Insufflation & Irrigation Systems

- 5.1.4Software & AI Platforms

- 5.2By Application

- 5.2.1Gastroenterology

- 5.2.2Pulmonology

- 5.2.3ENT Surgery

- 5.2.4Gynecology

- 5.2.5Urology

- 5.2.6Orthopedic & Arthroscopy

- 5.2.7Cardiology

- 5.2.8Neurology / Neuroendoscopy

- 5.2.9Intraoperative Visualization

- 5.3By End User

- 5.3.1Public Hospitals (SNS)

- 5.3.2Private Hospitals

- 5.3.3Ambulatory Surgery Centers

- 5.3.4Specialty Clinics

- 5.4By Usage

- 5.4.1Reusable Endoscopes

- 5.4.2Disposable / Single-Use Endoscopes

- 5.4.3Reprocessed (Third-Party) Endoscopes

- 5.5By Technology

- 5.5.12D HD Endoscopy

- 5.5.24K / UHD Endoscopy

- 5.5.33D & Robotic Endoscopy

- 5.5.4AI-Assisted Endoscopy

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1Olympus Corporation

- 6.3.2KARL STORZ SE & Co. KG

- 6.3.3Boston Scientific Corporation

- 6.3.4Johnson & Johnson (Ethicon Inc.)

- 6.3.5Fujifilm Holdings Corporation

- 6.3.6Hoya Corporation (Pentax Medical)

- 6.3.7Medtronic plc

- 6.3.8Stryker Corporation

- 6.3.9Richard Wolf GmbH

- 6.3.10Cook Medical LLC

- 6.3.11Ambu A/S

- 6.3.12ConMed Corporation

- 6.3.13Cantel Medical (Steris plc)

- 6.3.14Arthrex Inc.

- 6.3.15Mindray Medical International Ltd.

- 6.3.16SonoScape Medical Corp.

- 6.3.17Karl Kaps GmbH & Co. KG

- 6.3.18Optomic Spain

- 6.3.19Palex Medical SA

- 6.3.20VirtaMed AG

7. Market Opportunities & Future Outlook

- 7.1White-Space & Unmet-Need Assessment

Spain Endoscopy Devices Market Report Scope

As per the scope of the report, endoscopes are minimally-invasive devices and can be inserted into natural openings of the body, to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries.

The Spain endoscopy devices market is segmented by type of device (visualization equipment, endoscopes, endoscopic operative device, and other devices) and application (gastroenterology, pulmonology, orthopedic surgery, cardiology, ENT surgery, gynecology, neurology, and other applications).

The report offers the value (in USD) for the above segments.