Embolotherapy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

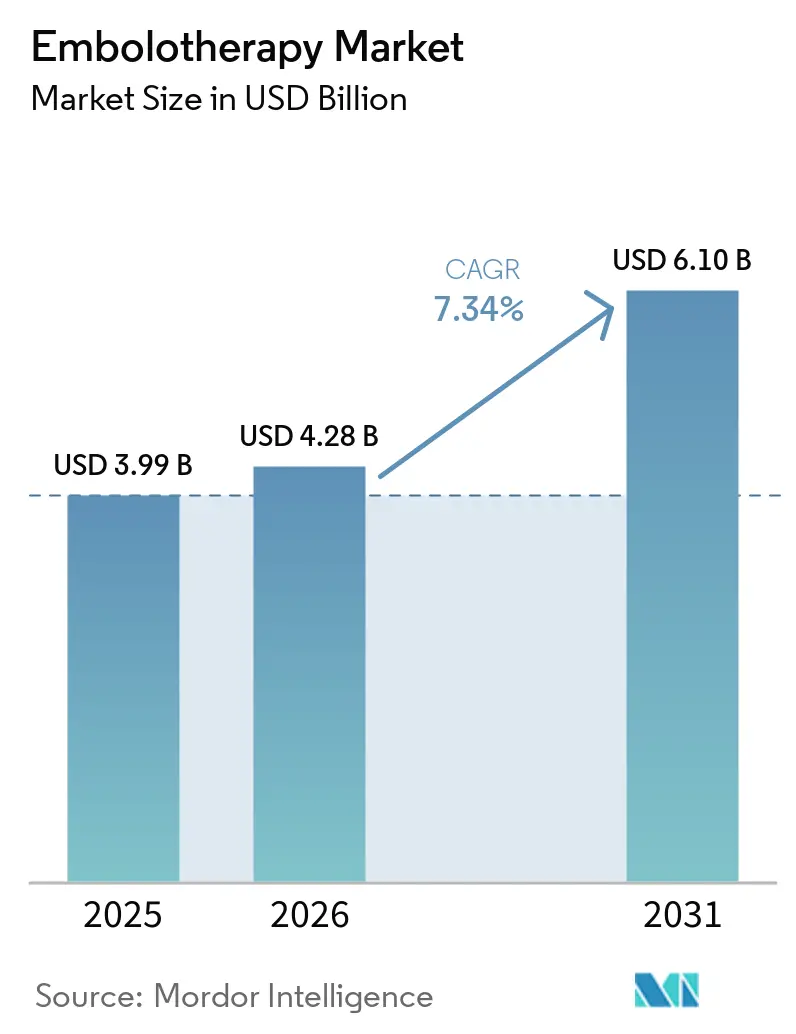

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 6.10 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embolotherapy Market Analysis by Mordor Intelligence

The Embolotherapy Market size is expected to increase from USD 3.99 billion in 2025 to USD 4.28 billion in 2026 and reach USD 6.10 billion by 2031, growing at a CAGR of 7.34% over 2026-2031.

The embolotherapy market is experiencing growth driven by the increasing oncology burden, particularly in liver, kidney, and bone cancers, where hypervascular tumor patterns support the use of transcatheter embolization. Additionally, the market benefits from a shift in care delivery as catheter-based procedures move from inpatient settings to shorter-stay environments, improving procedural access and efficiency. Product innovations, such as liquid and resorbable embolic materials, are expanding the clinical applications of embolotherapy and supporting repeat-treatment planning in cancer care. Emerging neurovascular applications, like middle meningeal artery embolization, are also creating new treatment opportunities, challenging previous demand assumptions. Competition is intensifying as companies focus on indication-specific approvals, delivery-system integration, and scalable material platforms.

Key Report Takeaways

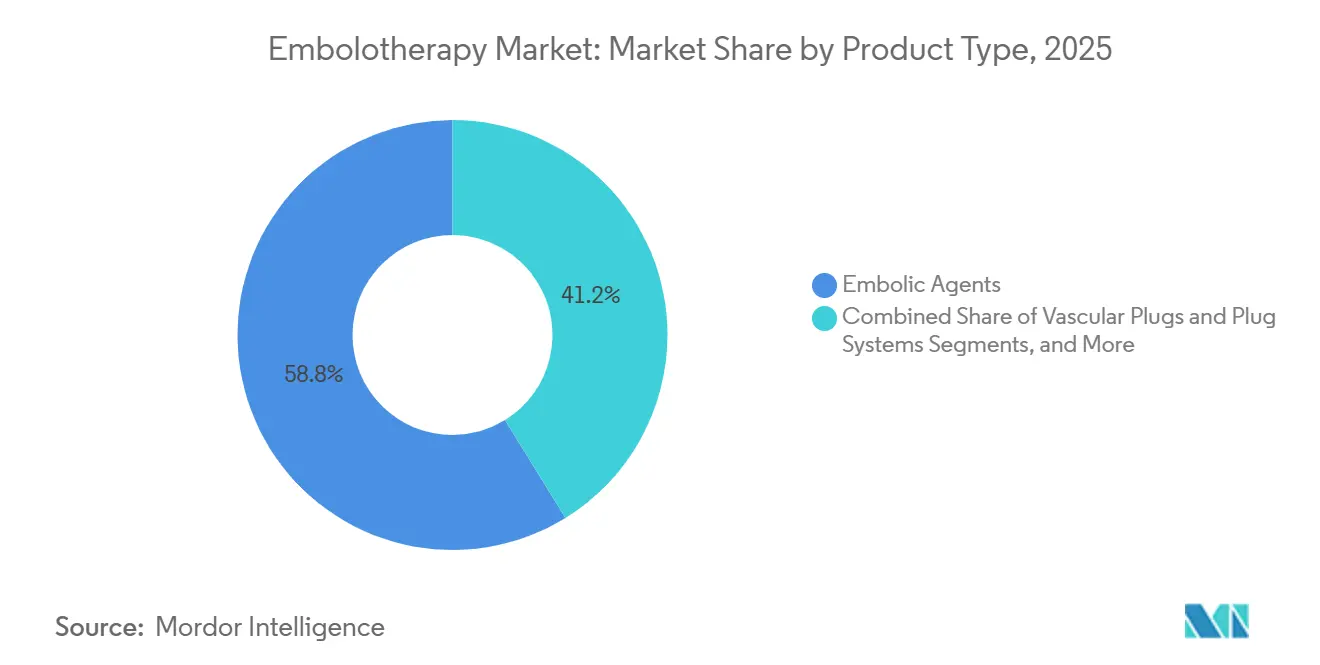

- By product type, embolic agents led with 58.77% revenue share in 2025, while vascular plugs and plug systems are forecast to expand at a 7.99% CAGR through 2031.

- By procedure, TACE held 34.40% of revenue in 2025, while TARE is projected record a CAGR at 8.25% through 2031.

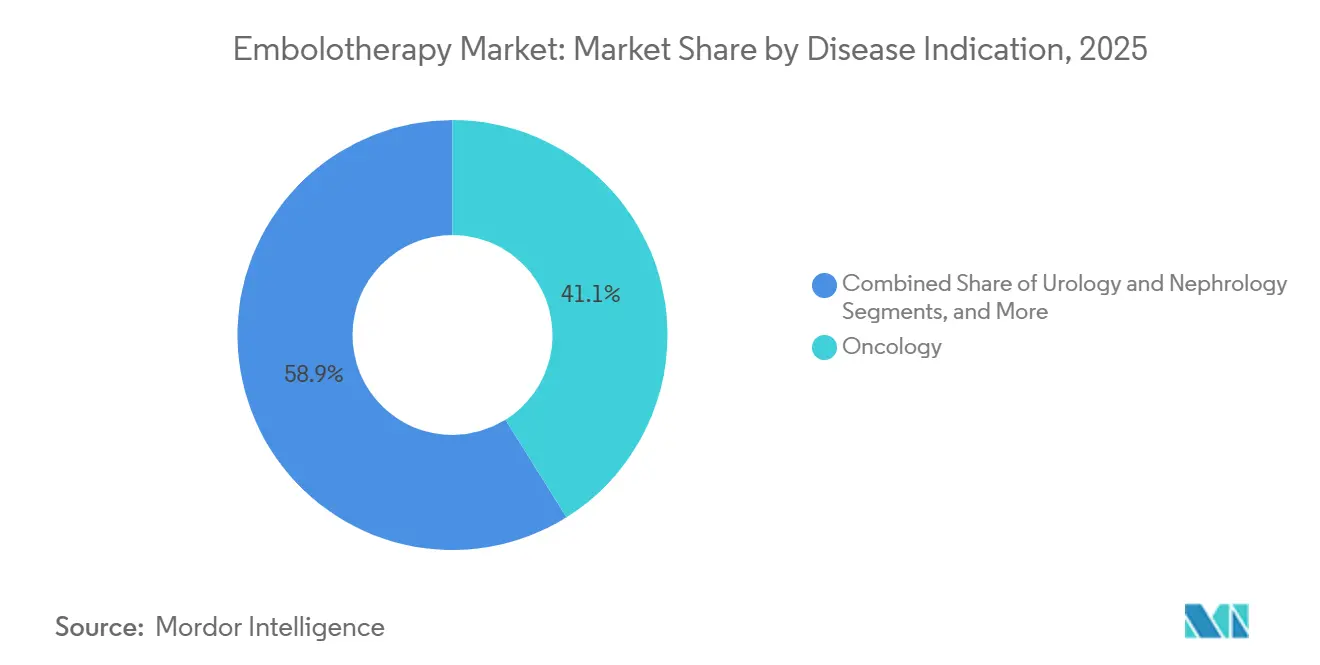

- By disease indication, oncology accounted for 41.11% of revenue in 2025, while urology and nephrology is projected to grow at a 7.55% CAGR through 2031.

- By end user, hospitals captured 82.45% of revenue in 2025, while ambulatory surgical centers are projected to grow at an 8.76% CAGR through 2031.

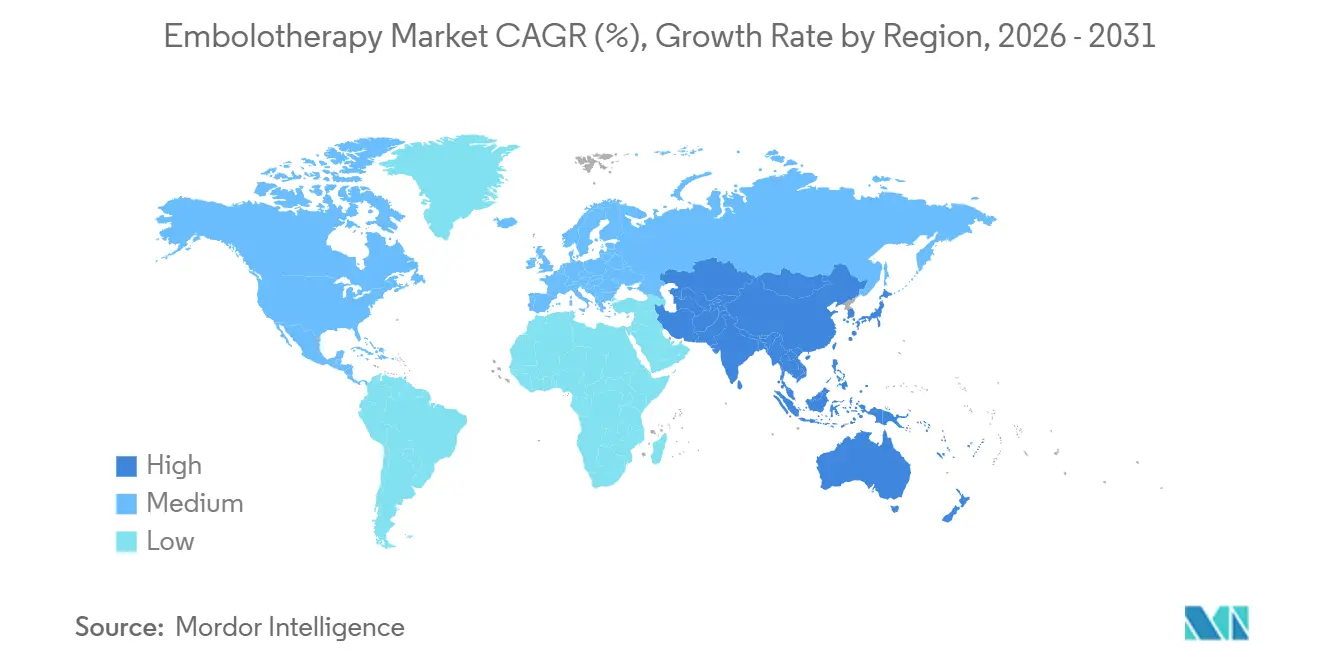

- By geography, North America held 38.79% share in 2025, while the Asia-Pacific is projected to advance at 8.45% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Embolotherapy Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising burden of cancer and hypervascular tumors | +2.1% | Global, concentrated in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Expanding use of minimally invasive image-guided procedures | +1.5% | Global, with North America and Europe leading and Asia-Pacific widening | Medium term (2-4 years) |

| Broader adoption of liquid and resorbable embolic agents | +1.2% | North America leading, followed by Europe and Asia-Pacific | Short term (≤ 2 years) |

| Shift of suitable cases toward ambulatory and short-stay settings | +0.8% | North America first, followed by Europe and Australia | Short term (≤ 2 years) |

| Device innovation in microcatheters, delivery systems, and visibility | +0.7% | Global | Medium term (2-4 years) |

| Evidence generation for new indications such as middle meningeal artery embolization | +1.0% | North America and Europe, with Japan and South Korea emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Cancer and Hypervascular Tumors

The embolotherapy market is closely tied to the global cancer burden, as embolization is critical for treating diseases with high vascular activity. Global cancer cases are projected to reach 20 million in 2025, with a significant rise expected by 2050, ensuring a growing patient base for embolic procedures.[1]American Association for Cancer Research, “AACR Cancer Progress Report 2025, Cancer in 2025,” AACR Cancer Progress Report, aacr.org This trend is particularly evident in liver cancer, renal tumors, and bone lesions, where managing tumor blood supply is vital for both curative and palliative treatments. Demand is also shifting geographically, with Asia-Pacific and parts of Africa experiencing a rise in HBV- and HCV-related liver cancer cases, driving the need for TACE and similar procedures. Manufacturers are adapting product designs, pricing, and training to cater to a broader range of hospitals.

Expanding Use of Minimally Invasive Image-Guided Procedures

The embolotherapy market is benefiting from a shift toward catheter-based treatments in oncology, trauma, and vascular care. Enhanced imaging techniques, such as cone-beam CT and advanced fluoroscopic guidance, are improving distal vessel access and reducing procedural uncertainties. This shift enables more precise treatments and lowers technical barriers, allowing community hospitals and mid-sized centers to handle complex embolic cases. Newer coil systems are being designed to enhance workflow efficiency and reduce device burdens during large-vessel embolizations. As a result, the market is expanding through both rising disease incidences and broader procedural adoption across care settings.

Broader Adoption of Liquid and Resorbable Embolic Agents

Innovations in embolic materials are reshaping the embolotherapy market. Instylla’s Embrace Hydrogel Embolic System, approved by the FDA in August 2025, entered commercial use in January 2026, offering a liquid embolic platform for hypervascular tumor embolization. Boston Scientific’s OBSIDIO Conformable Embolic, cleared by the FDA in October 2025, simplifies delivery across diverse vessel anatomies with its premixed, adaptable design. These advancements address limitations of permanent occlusion, enabling physicians to consider repeat interventions and extended treatment sequences. The market is evolving toward a structure where material properties significantly influence clinical decisions.

Evidence Generation for New Indications: Middle Meningeal Artery Embolization

The embolotherapy market is witnessing rapid growth in middle meningeal artery embolization for chronic subdural hematoma. Procedure volumes surged from 4,014 in 2019 to 20,836 in 2025, with projections indicating nearly 79,000 annual procedures by 2029.[2]Ansaar T. Rai, Paul S. Link, and Dhairya A. Lakhani, “Rising Tide of Middle Meningeal Artery Embolization for Chronic Subdural Hematomas, Current Volumes and Future Growth Compared with Cerebral Aneurysm and Stroke Interventions,” Journal of NeuroInterventional Surgery, jnis.bmj.com Balt USA’s SQUID Liquid Embolic Agent has received FDA premarket approval for this application, providing a clear commercial pathway. A German study reported 718 procedures across 30 neurovascular centers with a 2.5% symptomatic complication rate. As more trial results and guidelines emerge, the neurovascular segment is expected to transition from a niche area to a stable volume driver, encouraging manufacturers to develop versatile platforms for both oncology and neurovascular applications.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Reimbursement variability across indications and care settings | -0.9% | Global, with stronger impact in fragmented payer systems and emerging markets | Medium term (2-4 years) |

| High per-case device cost and inventory complexity | -0.7% | Global, with stronger impact in public systems across Asia-Pacific and South America | Medium term (2-4 years) |

| Specialist dependency and procedural learning curve | -0.5% | Global, most acute in Sub-Saharan Africa, South Asia, and Latin America | Long term (≥ 4 years) |

| Limited access to interventional infrastructure in resource-constrained settings | -0.7% | Middle East and Africa, South America, South Asia, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reimbursement Variability Across Indications and Care Settings

The embolotherapy market faces reimbursement challenges as the expansion of medical indications often outpaces payer frameworks in many countries. While oncology applications have clearer billing pathways, newer uses in neurology and urology lack consistency. In the U.S., evolving payer policies for novel materials and applications delay hospital formulary adoption and broader market rollouts. In Europe, variations in health technology assessments and payer interpretations across countries result in uneven access, even with regulatory approvals. Premium-priced next-generation embolics are initially adopted in high-volume centers with coding expertise, specialized staff, and robust internal review processes, slowing the market's ability to achieve widespread commercial success.

High Per-Case Device Cost and Inventory Complexity

Cost remains a significant barrier in the embolotherapy market, especially for procedures requiring expensive kits, dosimetry tools, or specialized delivery systems. A 2025 Italian study reported that TARE with standard dosimetry cost EUR 32,381 (approximately USD 35,200), compared to EUR 27,735 (around USD 30,200) for DEB-TACE over a two-year care episode.[3] Instylla, Inc., “Instylla Initiates Commercial Launch with First Use of the Embrace Hydrogel Embolic System,” Instylla, instylla.com Even with favorable outcomes, procurement teams demand strong economic justifications for broader adoption. Additionally, interventional suites require diverse coil sizes, embolic formulations, and catheter configurations, complicating inventory management. Manufacturers that simplify packaging, reduce SKU burdens, and align product bundles with procedural workflows can better address these challenges in the embolotherapy market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Embolic Agents Anchor Revenue as Vascular Plugs Lead Velocity

In 2025, embolic agents held a dominant 58.77% share of the embolotherapy market, surpassing all other product categories. This leadership stems from the widespread use of microsphere-based TACE, particle embolization, and the expanding liquid embolic class, all integral to interventional oncology. Unlike other product types confined to specific procedures, this group thrives across diverse treatment settings. Drug-eluting microspheres enhance local chemotherapy delivery while minimizing systemic exposure, while newer liquid systems offer flexibility for repeat or staged cancer treatments. Even with increasing emphasis on pricing and clinical differentiation, embolic agents remain the cornerstone of the embolotherapy market's revenue.

The premium segment of this category is evolving rapidly. Resorbable and conformable liquid embolics are shifting the focus from vessel occlusion to treatment planning and follow-up flexibility. Embolization coils, especially valued in neurovascular and complex peripheral applications, emphasize repositionability and control. Vascular plugs and plug systems, projected to grow at a 7.99% CAGR through 2031, are increasingly utilized in prostate artery embolization, fibroid procedures, and trauma cases requiring controlled occlusion.

By Procedure: TACE Leads on Volume as TARE Builds Clinical Preference

TACE accounted for 34.40% of the embolotherapy market in 2025, making it the leading procedure by revenue. Its dominance is attributed to its established role in hepatocellular carcinoma, integration into treatment pathways, and widespread adoption in academic and community hospitals. TACE's procedural familiarity supports its repeated use in liver-directed oncology and extends its application to metastases, neuroendocrine tumors, and other hypervascular lesions. This versatility ensures TACE remains central to routine embolic practices, even as newer procedures gain attention.

TARE, projected to grow at an 8.25% CAGR through 2031, is gaining traction due to its clinical preference in specific patient demographics. A meta-analysis spanning 2024 to 2025 highlighted TARE's superior response, disease control, and one-year survival rates compared to TACE, alongside fewer common complications. A 2025 study showcased an 83% objective response rate and a median overall survival of 47.2 months for HCC patients with portal vein invasion undergoing Y-90 glass microsphere therapy.

By Disease Indication: Oncology Leads as Urology and Nephrology Gain Momentum

In 2025, oncology accounted for 41.11% of the embolotherapy market's revenue, solidifying its position as the dominant disease indication. This prominence stems from the established efficacy of embolization in treating hepatocellular carcinoma, metastatic liver disease, and renal cell carcinoma. These conditions, often presenting as strong vascular targets, benefit from catheter-based treatments. The oncology segment's significance lies in its high procedural frequency and diverse embolic approaches, spanning chemoembolization to radioembolization.

Urology and nephrology are set to witness the highest growth rate at 7.55% CAGR through 2031, signaling a broadening clinical base. Prostate artery embolization is gaining momentum for benign prostatic hyperplasia, varicocele embolization is being recognized in male fertility programs, and renal artery embolization is finding its place in organ-sparing and pre-surgical contexts. Each validated application introduces distinct treatment cohorts, enhancing the clinical landscape.

By End User: Hospital Dominance Intact, ASCs Redefine Site-of-Care Economics

In 2025, hospitals commanded 82.45% of end-user revenue, underscoring their pivotal role in the embolotherapy market. This dominance is attributed to the advanced imaging systems, specialized nursing support, and multidisciplinary coordination required for these procedures. Large tertiary hospitals and academic medical centers anchor complex oncology and neurovascular embolizations and play a crucial role in trial participation and early technology adoption, influencing broader practice patterns.

Ambulatory surgical centers (ASCs) are projected to grow at an impressive 8.76% CAGR through 2031. This growth reflects a strategic migration of lower-complexity procedures to settings favoring shorter stays and tighter workflow control. Such a transition benefits companies adept at simplifying setup, streamlining device selection, and endorsing single-session treatment models. Specialty clinics, especially in urology, oncology, and vascular care, are becoming increasingly prominent for elective and standardized procedures.

Geography Analysis

In 2025, North America accounted for 38.79% of the embolotherapy market, maintaining its position as the largest regional contributor. This dominance stems from a strong interventional radiology infrastructure, a wide procedural base in oncology and women’s health, and regulatory support for innovative product approvals. The U.S. serves as the primary launch platform for new embolic technologies, providing early market access. North America is also central to the growth of middle meningeal artery embolization, with procedure volumes expected to approach acute ischemic stroke treatment levels by 2029.

In 2025, Europe held a significant share of the embolotherapy market, supported by advanced hospital systems in Germany, France, and the U.K. These countries benefit from well-developed interventional radiology departments and centralized oncology networks, enabling procedures like TACE, TARE, fibroid embolization, and neurovascular treatments. A German study documented 718 middle meningeal artery embolization procedures across 30 neurovascular centers, reflecting specialist density and growing clinical acceptance. Italy and Spain contribute to liver-directed oncology volumes, partly due to historical hepatitis-related disease burdens. Europe plays a key role in protocol development, product validation, and specialist training, influencing the global embolotherapy market.

Asia-Pacific is projected to achieve the fastest regional CAGR of 8.45% through 2031, emerging as the strongest growth driver for the embolotherapy market. The region faces a rising burden of hepatocellular carcinoma, particularly in areas with high HBV prevalence. China and India are expanding interventional radiology capacity, increasing access to embolization procedures beyond major urban centers. Japan is advancing clinical and regulatory pathways for middle meningeal artery embolization, signaling a growing neurovascular focus.

Competitive Landscape

The embolotherapy market features a moderately consolidated top tier yet remains fragmented beyond the leading global device companies. Major players like Medtronic, Boston Scientific, Penumbra, Stryker, Terumo, MicroVention, and Sirtex leverage their established brands, extensive procedural coverage, and robust hospital ties. However, the market is not tightly dominated by a select few. Specialist and mid-tier companies are carving out niches in liquid embolics, delivery systems, and indication-specific platforms. This dynamic ensures enduring leadership at the top while leaving avenues for growth open to targeted challengers.

A key trend in the market is portfolio expansion through strategic acquisitions and product-line integration. For instance, in January 2025, Argon Medical strengthened its oncology portfolio by acquiring the SeQure and DraKon microcatheters, enhancing its position in therapeutic delivery. Another significant trend is innovation driven by specific indications, with companies seeking approvals that create dedicated commercial pathways. Balt USA’s SQUID approval for middle meningeal artery embolization ties the product to a growing neurovascular application. Similarly, Instylla’s launch of a bioresorbable hydrogel embolic addresses a gap overlooked by traditional permanent embolics. These strategies highlight a shift in competition, focusing on regulatory positioning and treatment adaptability over incremental device enhancements.

Competition in the embolotherapy market is increasingly centered on procedural efficiency and platform control. Penumbra’s 2025 launch of the Ruby XL System reflects efforts to reduce device usage and streamline workflows for large-vessel embolization. Boston Scientific’s OBSIDIO clearance aligns with this trend, enabling easier preparation and delivery to appeal to operators with varying experience levels. Additionally, in TARE, advancements in dosimetry and treatment-planning software are influencing product selection at institutions. Future competition in the embolotherapy market is expected to focus on mastering treatment workflows rather than solely on selling embolic devices.

Embolotherapy Industry Leaders

Boston Scientific Corporation

Medtronic plc

Stryker Corporation

Johnson and Johnson

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Guerbet received EU approval for a new Lipiodol Ultra Fluid indication, enabling its use in vascular embolization with cyanoacrylate-based surgical glues, enhancing its role in interventional radiology and oncology.

- April 2026: Embolization Inc.'s polymer-based NED coil achieved over 70 successful cases in 4 US institutions during its limited-market release, demonstrating effective vessel occlusion with reduced imaging artifacts.

- January 2026: Instylla began commercial procedures with its Embrace Hydrogel Embolic System, the only FDA-approved liquid embolic for hypervascular tumor embolization in peripheral arteries ≤5 mm.

- January 2026: Balt USA's SQUID Liquid Embolic Agent received FDA approval for embolizing the middle meningeal artery in patients with symptomatic chronic subdural hematoma.

- October 2025: Boston Scientific's OBSIDIO Conformable Embolic gained FDA clearance for its adaptable design, simplifying delivery across various microcatheter systems and operator expertise levels.

Global Embolotherapy Market Report Scope

As per the scope of the report, embolotherapy (or embolization) is a minimally invasive medical procedure. Doctors deliberately block specific blood vessels to stop bleeding, treat tumors, or fix abnormal vessels. An interventional radiologist guides a tiny tube (catheter) through your blood vessels and releases agents like tiny beads, coils, or glue to close them off.

The embolotherapy market is segmented by product type, procedure, disease indication, end-user, and geography. By product type, the market includes embolic agents (liquid embolic agents, microspheres, particles, sclerosants and adhesives), embolization coils (detachable coils, pushable coils), vascular plugs and plug systems, flow diverters, and support devices (microcatheters, guidewires). By procedure, the market is segmented into transarterial chemoembolization, transarterial radioembolization, transcatheter arterial embolization, stent-assisted coiling, particle embolization, sac packing, and the sandwich technique. By disease indication, the market is categorized into oncology, benign tumors, vascular abnormalities, hemorrhage and trauma, neurology, urology and nephrology, and peripheral vascular disease. By end-user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and academic and research institutes. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Embolic Agents | Liquid Embolic Agents |

| Microspheres | |

| Particles | |

| Sclerosants and Adhesives | |

| Embolization Coils | Detachable Coils |

| Pushable Coils | |

| Vascular Plugs and Plug Systems | |

| Flow Diverters | |

| Support Devices | Microcatheters |

| Guidewires |

| Transarterial Chemoembolization |

| Transarterial Radioembolization |

| Transcatheter Arterial Embolization |

| Stent-Assisted Coiling |

| Particle Embolization |

| Sac Packing |

| Sandwich Technique |

| Oncology |

| Benign Tumors |

| Vascular Abnormalities |

| Hemorrhage and Trauma |

| Neurology |

| Urology and Nephrology |

| Peripheral Vascular Disease |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Academic and Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Embolic Agents | Liquid Embolic Agents |

| Microspheres | ||

| Particles | ||

| Sclerosants and Adhesives | ||

| Embolization Coils | Detachable Coils | |

| Pushable Coils | ||

| Vascular Plugs and Plug Systems | ||

| Flow Diverters | ||

| Support Devices | Microcatheters | |

| Guidewires | ||

| By Procedure | Transarterial Chemoembolization | |

| Transarterial Radioembolization | ||

| Transcatheter Arterial Embolization | ||

| Stent-Assisted Coiling | ||

| Particle Embolization | ||

| Sac Packing | ||

| Sandwich Technique | ||

| By Disease Indication | Oncology | |

| Benign Tumors | ||

| Vascular Abnormalities | ||

| Hemorrhage and Trauma | ||

| Neurology | ||

| Urology and Nephrology | ||

| Peripheral Vascular Disease | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Academic and Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the embolotherapy market?

The embolotherapy market is valued at USD 4.28 billion in 2026 and is projected to reach USD 6.10 billion by 2031, with a 7.34% CAGR over the forecast period.

Which product category leads embolotherapy revenue?

Embolic agents led product revenue with 58.77% share in 2025, supported by strong use in microsphere-based TACE, particle embolization, and newer liquid embolic platforms.

Which procedure is growing fastest in embolotherapy?

TARE is the fastest-growing procedure, with a projected 8.25% CAGR through 2031, driven by stronger clinical preference in selected hepatocellular carcinoma settings.

Why is oncology the largest disease indication for embolotherapy?

Oncology held 41.11% of revenue in 2025 because embolization is already established in hepatocellular carcinoma, metastatic liver disease, renal tumors, and bone metastases with hypervascular profiles.

Which end-user group is expanding fastest?

Ambulatory surgical centers are projected to grow at an 8.76% CAGR through 2031, reflecting a gradual movement of suitable lower-complexity procedures into shorter-stay settings.

Which region is growing fastest in embolotherapy?

Asia-Pacific is expected to post the fastest regional growth at 8.45% CAGR through 2031, supported by rising hepatocellular carcinoma burden and expanding interventional radiology capacity.

Page last updated on: