Hydrocortisone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 4.28% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hydrocortisone Market Analysis by Mordor Intelligence

The Hydrocortisone Market size is projected to expand from USD 1.76 billion in 2025 and USD 1.82 billion in 2026 to USD 2.25 billion by 2031, registering a CAGR of 4.28% between 2026 to 2031.

Demand remains anchored by its essential-medicine status, established use in adrenocortical insufficiency, and widespread reliance in dermatology for low-potency topical care, which together preserve baseline volumes across public and private channels. Competitive pressure persists as steroid-sparing options gain traction in moderate-to-severe inflammatory diseases and as regulators intensify topical steroid withdrawal safety actions, which together temper long-run upside even as acute care protocols sustain parenteral use. Manufacturers focus on differentiated delivery and emergency-readiness tools in order to protect margins in selected niches within the otherwise commoditized hydrocortisone market.[1]Addison’s Disease Self-Help Group, “Hydrocortisone Injection Supply Notification,” ADSHG

Key Report Takeaways

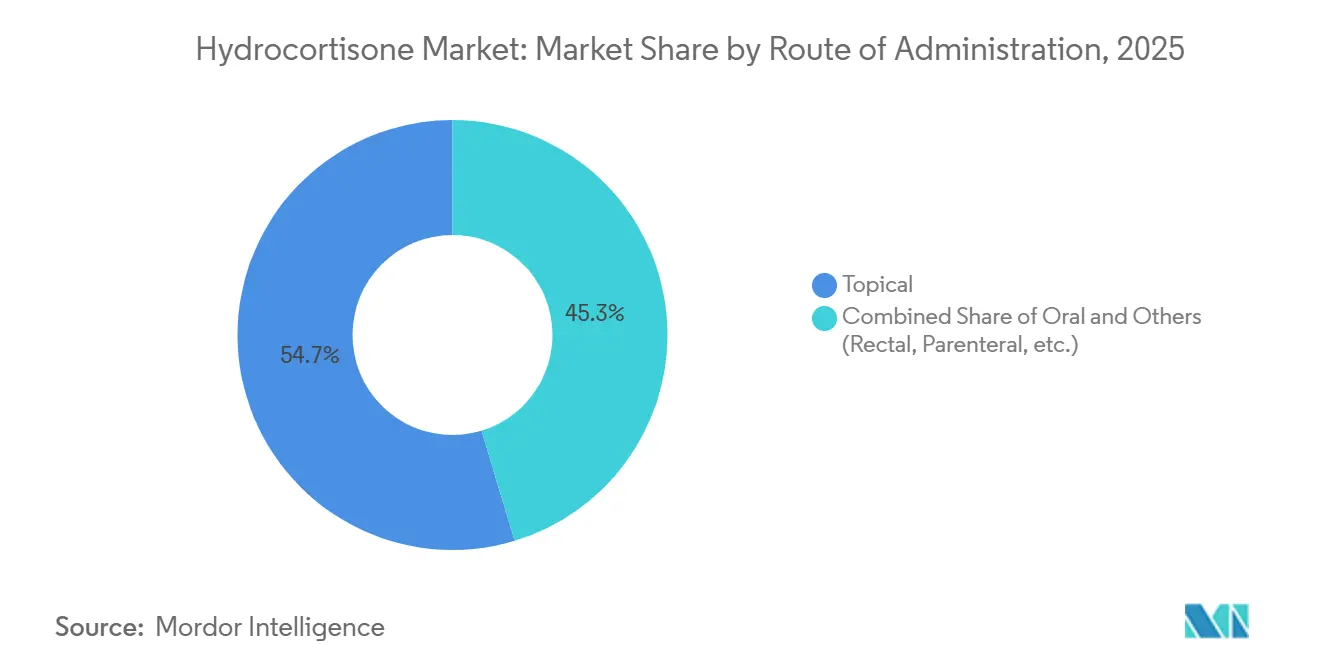

By route of administration, topical delivery led with 54.68% revenue share in 2025, while oral formulations are projected to record the fastest growth at 5.98% CAGR through 2031.

By prescription type, OTC availability held 57.88% share in 2025, and prescription pathways are forecast to grow at 6.34% CAGR through 2031.

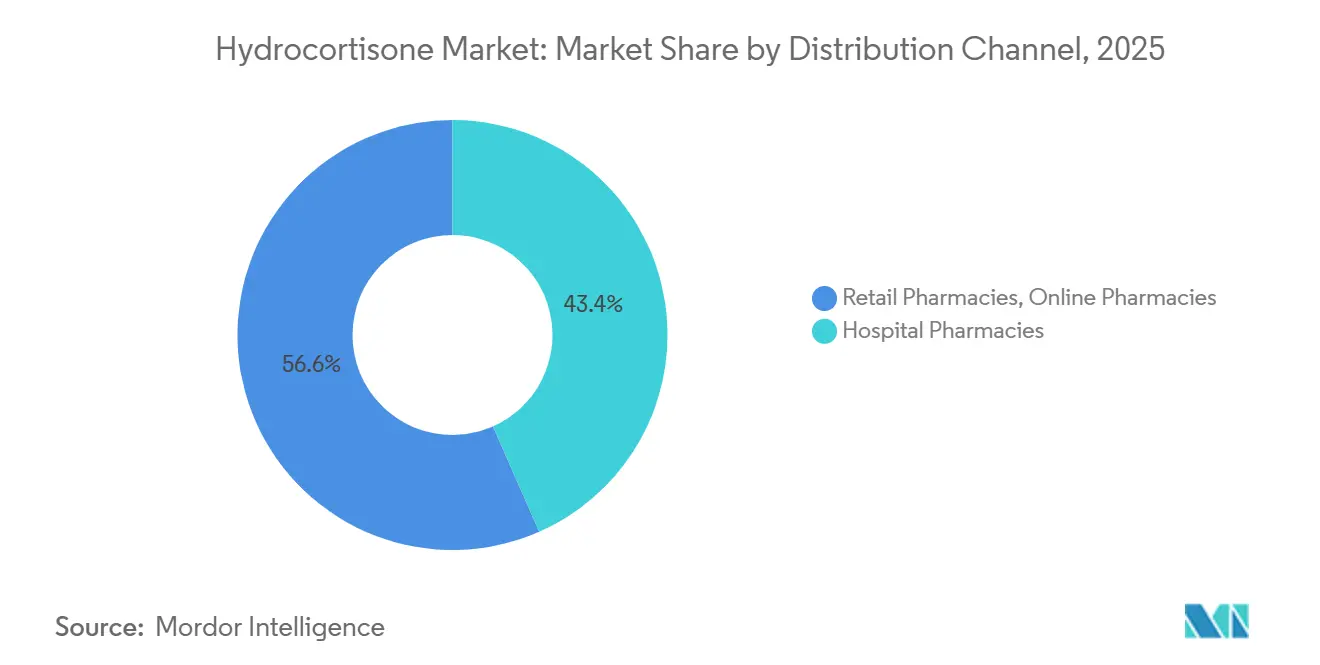

By distribution channel, hospital pharmacies accounted for 43.38% of revenue in 2025, while online pharmacies are expected to grow at 7.67% CAGR through 2031.

By indication, dermatology captured 32.34% of 2025 revenue and is projected to advance at a 5.87% CAGR through 2031.

By geography, North America held 38.34% of the 2025 revenue base, while Asia Pacific is expected to post the fastest regional CAGR at 5.21% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Hydrocortisone Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| WHO Essential Medicines status ensures baseline demand and formulary inclusion | +0.8% | Global | Long term (≥ 4 years) |

| OTC availability (0.5–1%) enables self-care and retail/e-pharmacy access expansion | +1.2% | Global, with early gains in North America, Asia Pacific | Medium term (2-4 years) |

| Guideline-backed use in vasopressor-refractory septic shock (parenteral demand) | +0.5% | Global, stronger in Europe & North America due to protocol adoption | Medium term (2-4 years) |

| Emergency adrenal crisis protocols mandate hydrocortisone kits and rapid dosing | +0.6% | Global, highest in advanced healthcare systems | Long term (≥ 4 years) |

| Pediatric-specific approvals (oral granules/solution) for adrenal insufficiency | +0.9% | North America & Europe, spillover to Asia Pacific | Short term (≤ 2 years) |

| Endocrine tapering/stress-dose guidance favors hydrocortisone in GIAI management | +0.4% | Global, with concentrated impact in North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

WHO Essential Medicines Status Ensures Baseline Demand and Formulary Inclusion

Hydrocortisone’s presence on the 24th WHO Model List of Essential Medicines, reaffirmed in September 2025, secures priority in national procurement and public formularies across income levels, which stabilizes the hydrocortisone market against abrupt displacement in tender-driven settings. The 10th WHO Model List of Essential Medicines for Children in 2025 codified broader pediatric coverage, including oral liquid 1 mg/mL, oral granules, and injectables, aligning supply with pediatric replacement needs and mitigating dosing workarounds that previously eroded adherence. Country lists in Africa and other regions mirror these inclusions, anchoring availability from primary care posts to tertiary hospitals and reinforcing sustained baseline volumes for both oral and parenteral formats. Ongoing WHO Expert Committee reviews in 2026 keep the competitive bar active for overlapping therapies. Yet, hydrocortisone’s physiologic replacement role and emergency-use relevance make removal risk low in the near term. This status enhances access while constraining pricing power in public channels, which shapes a predictable but cost-sensitive foundation for the hydrocortisone market.

OTC Availability Enables Self-Care and Retail/E-Pharmacy Access Expansion

OTC hydrocortisone at 0.5–1% strength enables routine self-management of minor dermatoses without physician visits, supporting the largest 2025 prescription-type share and aligning with consumer preference for low-friction access, which together reinforce volume resilience across retail and digital channels. The United States FDA’s Additional Conditions for Nonprescription Use framework, effective in January 2025, allows technology-enabled self-selection for certain OTC medicines, which supports safe self-care journeys and can lift conversion among consumers who otherwise defer treatment. Growth is moderated by rising consumer awareness of topical steroid withdrawal risks, which encourages some users to prefer non-steroidal options, but convenient OTC access still anchors front-line care for mild inflammation.

Guideline-Backed Use in Vasopressor-Refractory Septic Shock Sustains Parenteral Demand

The 2026 Surviving Sepsis Campaign[2]Society of Critical Care Medicine, “Surviving Sepsis Campaign International Guidelines, 2026,” Society of Critical Care Medicine suggests intravenous corticosteroids, typically hydrocortisone 200–300 mg per day, for adults with vasopressor-refractory septic shock, which sustains a reliable base of parenteral demand in critical care workflows. Pediatric guidance remains more conservative, which concentrates parenteral hydrocortisone use in adult ICUs while pediatric populations rely more on oral replacement and stress dosing. As protocols are embedded across hospitals and emergency departments, the hydrocortisone market benefits from recurrent institutional purchasing that is less sensitive to consumer sentiment.

Pediatric-Specific Approvals Enhance Access and Drive Oral Segment Growth

The United States FDA approved Eton Pharmaceuticals’ KHINDIVI hydrocortisone 1 mg/mL oral solution in May 2025 for patients aged 5 and older with adrenocortical insufficiency, addressing the long-standing need for precise, liquid dosing and reducing variability from tablet splitting or crushing. Eton projects combined peak sales for KHINDIVI and ALKINDI SPRINKLE pediatric granules to exceed USD 50 million annually, supported by specialty pharmacy distribution and patient-assistance programs that together lift adherence and continuity of care in school-age and adolescent cohorts. The KHINDIVI label excludes use under age 5 due to excipient-related toxicity risks in very young children, which focuses uptake on older pediatric patients while reinforcing the need for tailored formulations across age groups.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse effects and steroid-phobia/TSW reduce adherence and appropriate use | -0.7% | Global, acute regulatory action in United Kingdom & Europe; heightened awareness in North America | Short term (≤ 2 years) |

| Generic price pressure and intense competition compress margins | -0.9% | Global, most pronounced in Asia Pacific & Latin America | Medium term (2-4 years) |

| Steroid-sparing biologics/JAK inhibitors displace use in select indications | -0.6% | North America & Europe lead; Asia Pacific following | Medium term (2-4 years) |

| Pediatric sepsis guidance limits routine hydrocortisone; retail curbs on misuse | -0.3% | Pediatric protocols global; retail curbs concentrated in India, Middle East, parts of Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Generic Price Pressure and Intense Competition Compress Margins

Hydrocortisone is widely produced across oral, topical, and parenteral forms by many manufacturers, which intensifies price competition and narrows transaction margins across channels without significantly lifting unit volumes in mature indications. Supply-chain events underscore fragility in certain presentations, as the United Kingdom signaled shortages of pre-mixed hydrocortisone injection in 2025[3]Drug shortage alert: injectable hydrocortisone." Addison's Disease Self-Help Group. Updated March 26, 2026and advised substitution with sodium succinate powder for injection that is suitable for kit assembly, which preserved emergency-kit readiness but highlighted single-supplier risk. In this environment, the hydrocortisone market remains volume-stable but price-sensitive, and manufacturers increasingly prioritize niche, margin-protected formulations to defend profitability.

Adverse Effects and Steroid-Phobia/TSW Reduce Adherence and Appropriate Use

Topical steroid withdrawal was formally recognized by the United States National Institutes of Health in March 2025, elevating clinical attention to a syndrome characterized by burning, flushing, dysautonomia-like symptoms, and widespread exfoliation after discontinuation of moderate-to-high potency topical corticosteroids. Health authorities and medical societies in multiple countries strengthened labeling and advisories between 2022 and 2025, and New Zealand’s Medsafe undertook safety assessments that included specific reporting on withdrawal phenotypes, which reinforced real-world surveillance and counseling needs at the point of care. The United Kingdom's professional and patient organizations jointly acknowledged TSW while emphasizing appropriate topical steroid use where clinically indicated, a balance that influences both safety monitoring and continued first-line use in mild disease. This evolving safety discourse redirects a subset of patients toward non-steroidal topicals and biologics, which trims repeat OTC hydrocortisone demand in dermatology-heavy segments of the hydrocortisone market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Route of Administration: Oral Formulations Ascend Through Pediatric Innovation

Topical administration accounted for 54.68% of 2025 revenue on the strength of OTC and prescription use in dermatology, while oral formulations are projected to grow fastest at 5.98% CAGR through 2031 as pediatric-specific products enable precise dosing and reduce caregiver variability, a dynamic that supports the hydrocortisone market size outlook through the forecast period. Eton’s KHINDIVI oral solution for patients aged 5 and older received FDA approval in May 2025 and launched with specialty pharmacy support, complementing ALKINDI SPRINKLE granules and improving dosing accuracy in a population where precision is clinically important. The KHINDIVI label excludes children under 5 due to excipient risks, which narrows its on-label reach but reinforces the clinical rationale for age-tailored formulations within the hydrocortisone market. WHO EMLc[4]World Health Organization, “The WHO Model List of Essential Medicines, 24th List, 2025,” World Health Organization 2025 includes oral liquids and granules alongside tablets, providing a policy foundation for broader pediatric access in markets where essential medicines lists steer procurement.

Topical hydrocortisone continues to dominate front-line management of mild inflammatory dermatoses, supported by OTC access, patient familiarity, and clinician comfort with lowest-potency regimens in sensitive areas where risk-benefit profiles are favorable for limited durations. Rectal delivery is positioned for targeted gastrointestinal use, where Cristcot’s next-generation 90 mg hydrocortisone acetate suppository progressed to an FDA decision and reported remission benefits in Phase 3 results disclosed at NDA acceptance, expanding options for distal ulcerative colitis. Across modalities, the hydrocortisone industry is concentrating investment in delivery improvements that minimize systemic exposure while preserving efficacy for localized indications, a strategy aimed at creating durable niches inside a generics-heavy field. Emergency-focused delivery tools, including efforts to simplify rapid dosing outside clinical settings, reflect parallel emphasis on safety and readiness for adrenal crisis. This mix of entrenched topical leadership and rising oral precision dosing strengthens the hydrocortisone market’s footing across hospital and home settings as clinical needs diversify

By Prescription Type: Rx Pathways Gain Through Emerging Indications Despite OTC Dominance

OTC products accounted for a 57.88% of 2025 revenue by enabling rapid, low-friction access for mild symptoms. Still, prescription pathways are projected to grow faster at 6.34% CAGR through 2031 as specialized formulations expand care in pediatrics, ulcerative colitis, and critical care, which together diversify the hydrocortisone market. Specialty distribution and copay programs around pediatric solutions help reduce barriers to adherence and position Rx hydrocortisone as a precision tool rather than a commodity choice, which underpins the growth gap with OTC. Rx-only parenteral presentations are insulated from OTC substitution because they are procedure-based in ICUs and emergency departments, where protocol adherence prioritizes on-formulary availability and consistency. OTC hydrocortisone remains a cornerstone in self-managed dermatology due to convenience, cost access, and widespread product familiarity, features that reinforce volume leadership even as clinical vigilance around topical steroid withdrawal rises. In parallel, Rx channels capture value through formulations and indications that require physician supervision or precise dosing that cannot be replicated in over-the-counter formats, which balances the hydrocortisone market across price tiers and care settings. Over the forecast, differentiated Rx products and hospital-driven uses maintain faster growth as they address clinical niches that are less exposed to consumer sentiment swings. At the same time, OTC continues to absorb the broad base of minor inflammatory presentations.

By Distribution Channel: Online Pharmacies Accelerate as Hospital Formularies Remain Anchor

Hospital pharmacies held 43.38% of 2025 revenue due to widespread accessibility, over-the-counter availability of low-dose formulations, and strong consumer reliance on community pharmacists, while online pharmacies are projected to grow at 7.67% CAGR through 2031 as digital access expands chronic-disease refills and same-day fulfillment, strengthening multichannel dynamics in the hydrocortisone market size trajectory. Online fulfillment grows as platforms add telepharmacy consults and easier refill journeys for families managing pediatric dosing, which increases the share of recurring oral prescriptions online and expands delivery convenience for OTC hydrocortisone. Major chains invest in digital-first care models, and logistics reach that compress last-mile timing for refills and flare-driven orders, reshaping channel mix across urban and suburban settings. Retail pharmacies remain indispensable due to their accessibility and immediate over-the-counter availability for common conditions, and their trusted role in frontline patient guidance, while online growth reflects consumer migration toward convenient, tech-enabled care.

By Indication: Dermatology Dominates Yet Faces Steroid-Sparing Headwinds

Dermatology led with 32.34% of 2025 revenue and is forecast to grow at a 5.87% CAGR through 2031, reflecting OTC-fueled self-care for mild eczema, contact dermatitis, and insect bites, as well as prescription use for controlled courses, which together secure a large and steady demand pool for the hydrocortisone market. Safety discourse around topical steroid withdrawal broadened through 2025, with NIH recognition and academic reports informing risk stratification that encourages the lowest-potency choice, the shortest effective duration, and close follow-up where risk factors exist. Non-steroidal topical therapies, including JAK inhibitors, have expanded treatment options for mild-to-moderate dermatologic conditions and are supported by clinical trial evidence for symptom relief. However, low-potency corticosteroids such as hydrocortisone remain first-line therapy in many mild cases due to their established efficacy, safety, and cost accessibility.

Geography Analysis

North America held 38.34% of revenue in 2025 as pediatric precision dosing matured and hospital protocols remained firmly embedded, while Asia Pacific is projected to deliver the fastest CAGR at 5.21% through 2031, a two-speed pattern that shapes the hydrocortisone market across reimbursement, access, and channel maturity. The United States and Canadian healthcare systems maintain injectable hydrocortisone in hospital formularies for emergency use in adrenal crisis and shock management. Pediatric adrenal insufficiency is managed with chronic hydrocortisone replacement, including liquid and compounded formulations when needed, supported through standard pharmacy and compounding channels, resulting in ongoing prescription requirements in affected patients. Digital pharmacy expansion and same-day logistics widen convenient access for patients and caregivers, while clinical groups and regulators continue to update safety communications to ensure appropriate topical steroid use. The North American hydrocortisone market is being shaped by ongoing innovation in corticosteroid formulations for inflammatory bowel diseases, particularly ulcerative colitis. For instance, as per the article published in MJH Life Sciences[5]MJH Life Sciences, "FDA Accepts NDA For Next-Generation Hydrocortisone Acetate in Ulcerative Colitis of the Rectum: in April 2026, the FDA’s acceptance of an NDA for a next-generation hydrocortisone acetate suppository for ulcerative colitis of the rectum highlights a key driver rising demand for targeted, locally acting therapies that improve efficacy while reducing systemic side effects in chronic GI conditions. Overall, increasing regulatory support for advanced rectal corticosteroid delivery systems and the unmet need for effective localized ulcerative colitis treatments are expected to be major growth drivers for the North America hydrocortisone market.

Asia Pacific’s growth reflects rising urbanization, penetration of generic hydrocortisone across retail and hospital settings, and rapid adoption of pharmacy e-commerce and telepharmacy services that together strengthen continuity of care for chronic needs like adrenal replacement.

Competitive Landscape

The hydrocortisone market combines multi-sourced generics with targeted innovation in delivery and indication-specific formulations, creating a competitive field where price-sensitive products coexist with niche, margin-protected offerings that aim to reduce systemic exposure and improve adherence. Large generic manufacturers operate across oral tablets, topical forms, and injectables, while brand-oriented players focus on hospital channels and emergency care continuity supported by protocolized use in shock and adrenal crisis.

Pediatric precision dosing represents a clear example of value-oriented specialization, where Eton Pharmaceuticals built a focused franchise with KHINDIVI oral solution and ALKINDI SPRINKLE granules targeted to age-specific requirements, specialty distribution, and copay support, which carved a durable position and underpinned the projected growth of oral routes.

Strategic moves in distribution continue to influence competitive positioning, as major pharmacy groups accelerate digital transformation and same-day logistics that lift refill convenience for both OTC and Rx hydrocortisone, while serialization and quality controls address authenticity and handling requirements across channels. Manufacturers and specialty firms invest in patient education around safe topical use, stress dosing, and tapering to reinforce appropriate utilization as safety awareness broadens, which supports sustained engagement even where steroid-sparing alternatives grow. Overall, the hydrocortisone market remains moderately fragmented, with leadership distributed across generics, pediatric dosing specialists, and hospital-focused suppliers, while innovation and service integration determine durable share capture in margin-protected lanes

Hydrocortisone Industry Leaders

-

Amneal Pharmaceuticals, Inc.

-

Hikma Pharmaceuticals PLC

-

Pfizer Inc.

-

Sanofi

-

Teva Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cristcot announced FDA acceptance of its NDA for a next-generation 90 mg hydrocortisone acetate suppository for ulcerative colitis of the rectum, with a PDUFA target date in October 2026 and Phase 3 trial disclosure at NDA acceptance indicating remission benefits

- May 2025: Eton Pharmaceuticals received United States FDA approval for KHINDIVI, the first FDA-approved hydrocortisone oral solution for pediatric patients aged 5 years and older with adrenocortical insufficiency, with commercial launch supported by specialty distribution and copay assistance.

Global Hydrocortisone Market Report Scope

As per the scope of the report, hydrocortisone is a corticosteroid medication, specifically a synthetic version of the natural hormone cortisol, used to reduce inflammation, suppress the immune system, and treat conditions like skin irritation (eczema, rashes), allergies, arthritis, and adrenal insufficiency.

The hydrocortisone market is segmented by route of administration, prescription type, distribution channel, indication, and geography. Based on route of administration, the market is segmented into topical, oral, and others. By prescription type, the market is segmented into over-the-counter (OTC) and prescription (Rx). By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. By indication, the market is segmented into dermatology, gastrointestinal, and others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Topical |

| Oral |

| Others (Rectal, Parenteral, etc.) |

| Over-the-Counter (OTC) |

| Prescription (Rx) |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Dermatology |

| Gastrointestinal |

| Others (Ophthalmic, Allergic reacttions, etc.) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Route of Administration | Topical | |

| Oral | ||

| Others (Rectal, Parenteral, etc.) | ||

| By Prescription Type | Over-the-Counter (OTC) | |

| Prescription (Rx) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Indication | Dermatology | |

| Gastrointestinal | ||

| Others (Ophthalmic, Allergic reacttions, etc.) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the hydrocortisone market size and growth outlook to 2031?

The hydrocortisone market size is projected to rise from USD 1.82 billion in 2026 to USD 2.25 billion by 2031 at a 4.28% CAGR, supported by essential-medicine status and protocolized emergency uses while moderated by steroid-sparing options.

Which segments are leading and which are growing fastest within the hydrocortisone market?

Topical delivery and OTC products lead by revenue, while oral formulations, prescription pathways, and online pharmacies are growing fastest due to pediatric precision dosing and digital access.

How are clinical guidelines shaping demand in the hydrocortisone market?

Adult sepsis protocols sustain parenteral demand and emergency dosing mandates maintain kit readiness, while pediatric dosing approvals and endocrine stress-dose guidance support growth in oral formulations.

Which regions are most important for future growth in the hydrocortisone market?

North America leads current revenue on protocol and reimbursement strength, and Asia Pacific is forecast to grow fastest on rising access, formulary alignment with WHO lists, and accelerating e-pharmacy adoption.

Page last updated on: