Blood Lancet Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

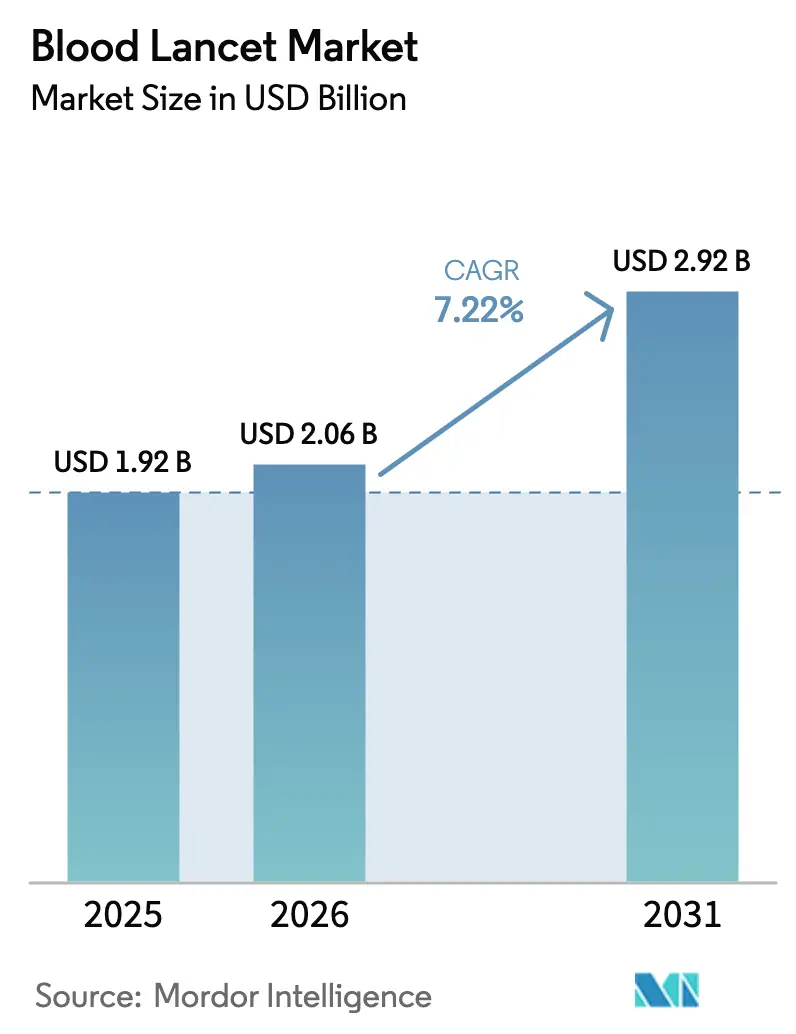

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 7.22% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blood Lancet Market Analysis by Mordor Intelligence

The Blood lancet market size was valued at USD 1.92 billion in 2025 and estimated to grow from USD 2.06 billion in 2026 to reach USD 2.92 billion by 2031, at a CAGR of 7.22% during the forecast period (2026-2031). Growth stems from surging diabetes prevalence, broader insurance coverage for self-monitoring supplies, and accelerating adoption of point-of-care diagnostics in hospitals, retail clinics, and homes [1]World Health Organization, “WHO Compendium of Innovative Health Technologies for Low-Resource Settings 2024,” who.int . Safety-engineered devices gain traction as regulators mandate sharps-injury prevention, while painless microneedle concepts shape long-term innovation pipelines. Sustainability priorities, raw-material cost swings, and emerging non-invasive glucose sensors collectively define the competitive playbook for the Blood lancet market through 2030.

Key Report Takeaways

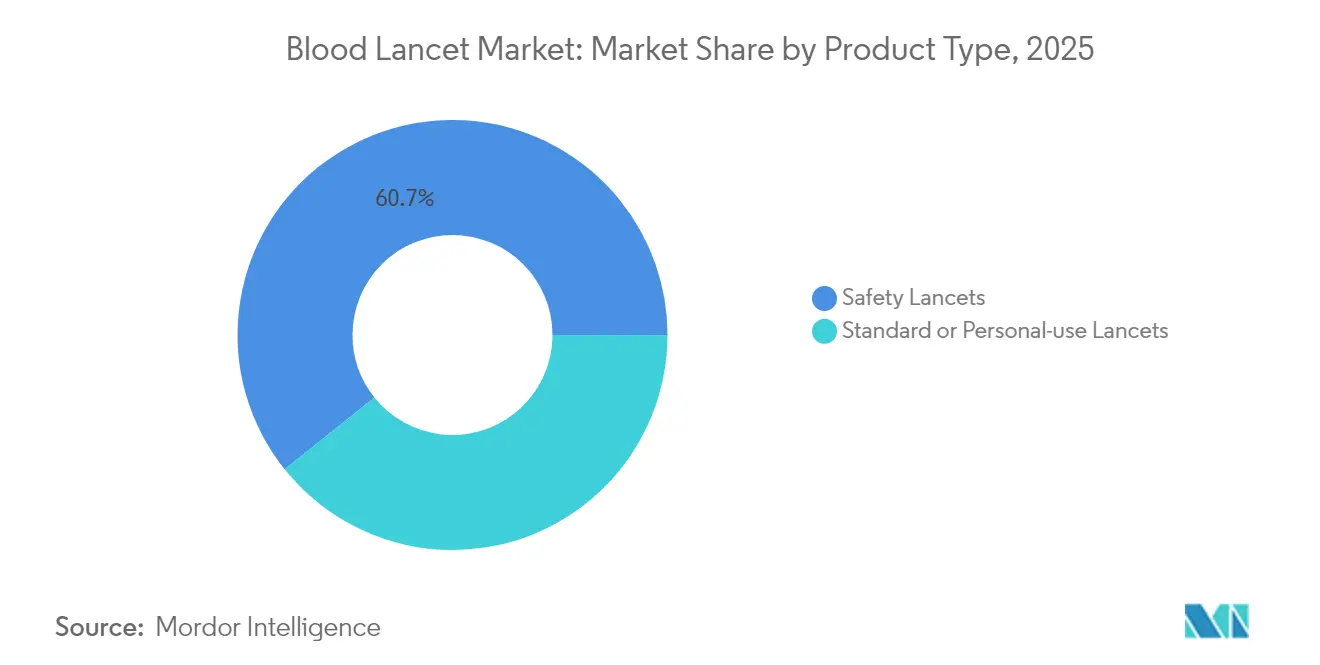

- By product type, Safety lancets led with 60.74% revenue share in 2025; Standard/Personal-use lancets are projected to expand at an 8.05% CAGR to 2031.

- By end user, hospitals accounted for 50.98% of the Blood lancet market size in 2025, while diagnostic laboratories record the highest projected CAGR at 8.12% through 2031.

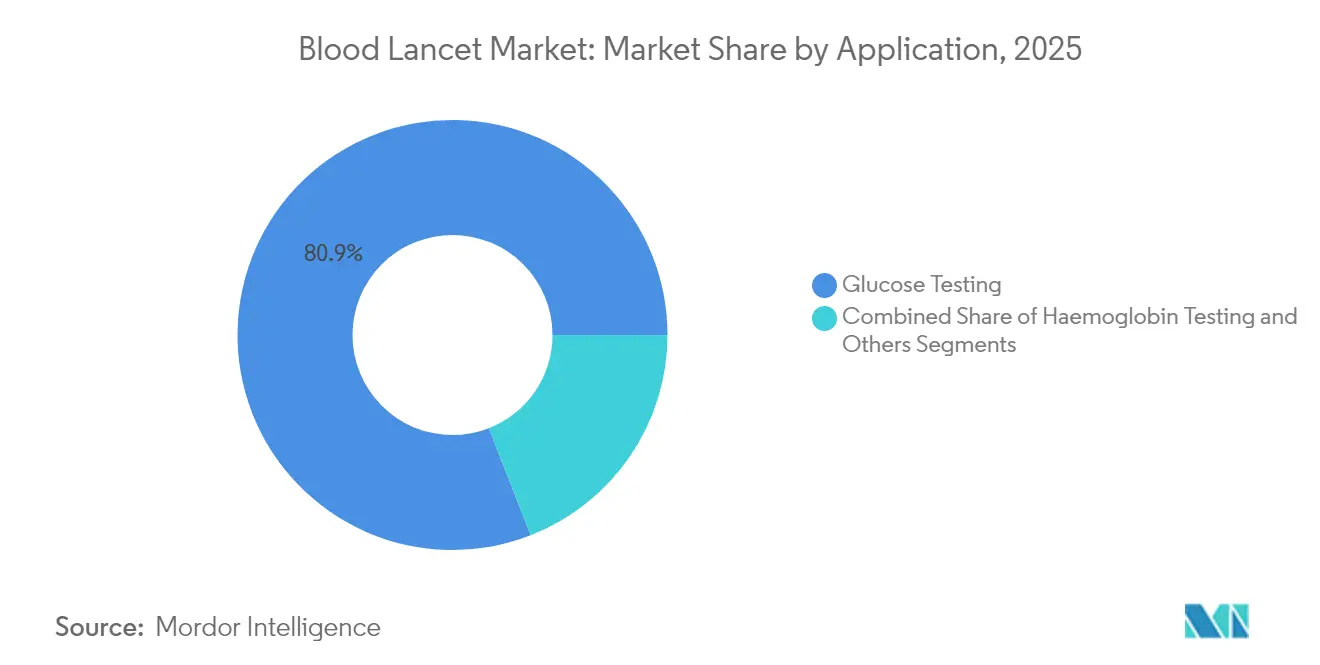

- By application, glucose testing captured 80.92% of Blood lancet market share in 2025 and haemoglobin testing is advancing at an 8.21% CAGR through 2031.

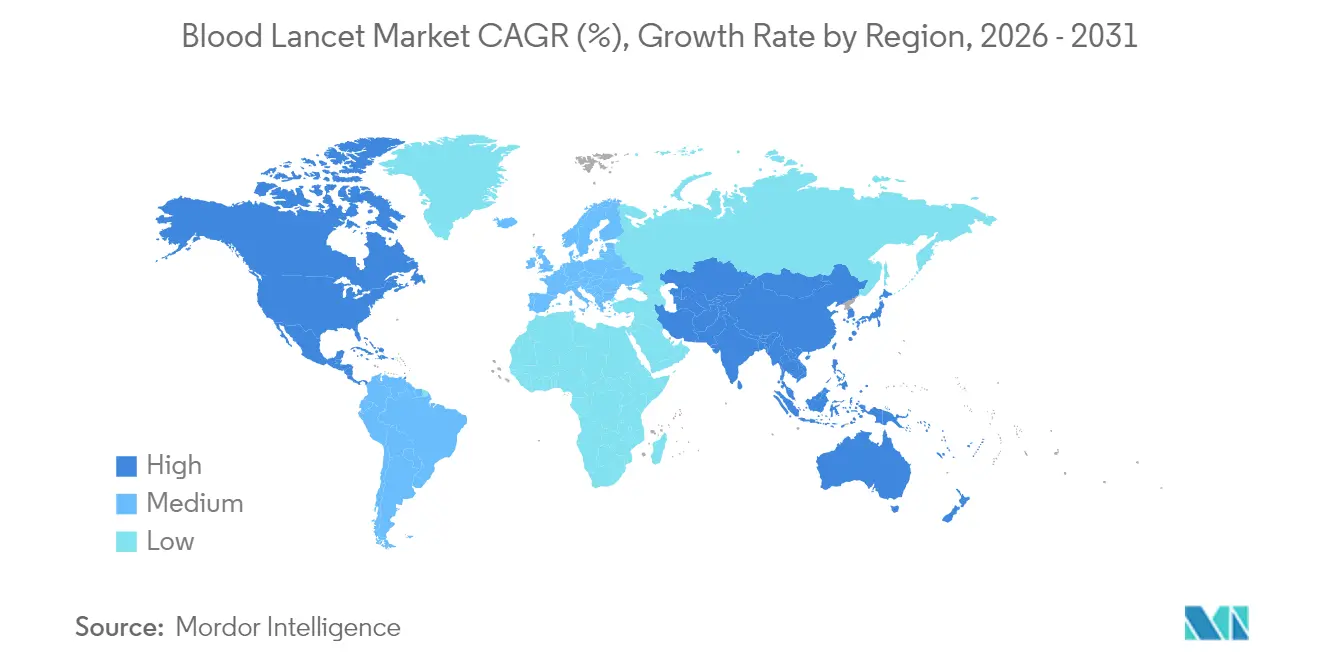

- By geography, North America held 41.88% Blood lancet market share in 2025; Asia-Pacific is set to grow at an 8.25% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Blood Lancet Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising diabetes & other chronic disease incidence | +1.8% | Global, with highest impact in APAC and MEA | Long term (≥ 4 years) |

| Growing adoption of point-of-care diagnostics | +1.5% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Favourable reimbursement policies in OECD nations | +1.2% | North America, Europe, Australia | Medium term (2-4 years) |

| Expansion of blood-donation & screening programs | +0.9% | Global, with emphasis on developing regions | Long term (≥ 4 years) |

| Painless microneedle innovations boosting paediatric compliance | +0.7% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Home-based genetic / tele-health finger-prick kits surge | +1.0% | North America & EU, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes and Other Chronic Disease Incidence

More than 588.7 million adults were living with diabetes in 2024, a number projected to hit 852.5 million by 2050. Untreated populations in emerging regions open a sizable addressable pool for capillary-blood monitoring, while aging demographics in developed economies multiply per-patient lancet use as comorbidities rise. Routine screening embedded in primary care pathways across OECD countries secures baseline demand, and national drive programs in India and China lift unit shipments sharply through 2030. Elevated chronic kidney and cardiovascular disease prevalence further widens the Blood lancet market as multiparameter finger-prick panels become standard follow-up diagnostics.

Growing Adoption of Point-of-Care Diagnostics

Decentralized testing models shorten turnaround times and improve therapeutic decision-making, prompting emergency rooms, ambulatory centers, and rural clinics to bulk-purchase disposable lancets. Portable analyzers that fit into backpack kits enable outreach in underserved zones, multiplying test frequency over a single patient episode. FDA fast-track pathways for at-home glucose and haemoglobin devices legitimize consumer self-testing, and private insurers increasingly reimburse home-based kits, stimulating retail-pharmacy demand. Integrated workflow benefits—fewer venipunctures, lower lab courier costs, immediate drug titration—cement the Blood lancet market as a foundational supply line for bedside diagnostics.

Favorable Reimbursement Policies in OECD Nations

Medicare Advantage and European national health schemes reimburse routine lancets under bundled diabetes management programs. Monthly allotments of testing supplies remove out-of-pocket barriers, encouraging regular self-monitoring. Occupational-safety clauses in these policies also absorb premium pricing for safety lancets, since reduced needlestick injuries lower workers’ compensation payouts. Reimbursement parity between in-clinic and self-administered tests sustains balanced demand across institutional and consumer channels, anchoring the Blood lancet market against short-term volume shocks.

Expansion of Blood-Donation & Screening Programs

WHO blood-management guidelines stipulate multiple sample draws during donor sessions, pushing per-donation lancet counts higher [2]World Health Organization, “WHO Compendium of Injection Safety,” who.int . Mobile collection units rely solely on single-use lancets due to sterilization limits, intensifying demand in populous countries such as Nigeria and Indonesia. International aid flows earmarked for blood-safety infrastructure routinely include lancet provisioning, stabilizing baseline volumes in resource-constrained regions and creating fresh tender opportunities for mid-tier manufacturers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection risk from lancet reuse & poor disposal | -0.8% | Global, particularly in resource-constrained settings | Medium term (2-4 years) |

| Emergence of non-invasive glucose-monitoring devices | -1.2% | North America & EU initially, expanding globally | Long term (≥ 4 years) |

| Sharps-waste environmental regulations raising costs | -0.6% | Europe & North America, expanding to APAC | Medium term (2-4 years) |

| Medical-grade stainless-steel supply bottlenecks | -0.4% | Global, with highest impact in Asia manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infection Risk from Lancet Reuse and Poor Disposal

WHO injection-safety campaigns spotlight improper sharps disposal as a leading vector for blood-borne pathogen transmission. Compliance costs rise as clinics must provide puncture-proof bins and certified incineration agreements, eroding discretionary budgets in low-income regions. Litigation linked to healthcare-worker injuries heightens institutional risk aversion, pushing procurement toward costlier retractable models and compressing margins for basic metal-blade lines.

Emergence of Non-Invasive Glucose-Monitoring Devices

Continuous glucose monitors achieve lab-grade accuracy without routine finger-stick calibration, eliminating up to 85% of daily lancet use among insulin-dependent patients in pilot programs across Germany and Japan. Wearable optical sensors tethered to smartphone dashboards amplify user preference for painless measurement, raising a long-term substitution threat to the Blood lancet industry. Device prices remain high in 2025, but scaling economies and insurer coverage could tip adoption curves within five years.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Safety Features Underpin Premium Adoption

Safety lancets captured 60.74% of Blood lancet market size in 2025, reflecting mandatory sharps-injury prevention protocols in hospital supply chains. Institutional buyers accept higher unit prices because retractable designs lower liability exposures and workers’ compensation claims. Standard or personal-use lancets, while priced 35% lower on average, deliver the fastest volume growth at an 8.05% CAGR as tele-health consults and over-the-counter diabetes packages normalize home testing routines.

Hospitals in the United States and Western Europe lock three-year supply contracts that favor ISO-certified safety models, safeguarding predictable revenue streams for market leaders. Meanwhile, e-commerce channels in Asia promote vivid color variants, ergonomic grips, and bulk refill packs that appeal to self-managing consumers. Hybrid SKUs merging protective sleeves with economical spring systems target low-to-mid income clinics, signaling future convergence within the Blood lancet market .

By End User: Hospital Scale Meets Laboratory Agility

Hospitals accounted for 50.98% share of Blood lancet market size in 2025, thanks to high-volume draws from emergency wards, oncology units, and critical-care pathways requiring serial testing. Central purchasing departments negotiate bundled deals covering lancets, alcohol swabs, and vacutainers, bolstering supplier leverage. Diagnostic laboratories, however, post the highest 8.12% CAGR to 2031 as personalized medicine panels and genomic workflows boost sample throughput.

Commercial labs invest in auto-loading workstation trays that standardize depth settings, cutting error rates and lowering wastage. Blood banks keep a steady base load, driven by WHO-aligned donor safety protocols. Fast-growing home-care agencies equip visiting nurses with pre-sterilized lancet kits, diversifying order patterns and expanding the Blood lancet market beyond brick-and-mortar health facilities.

By Application: Glucose Dominance Faces Early Diversification

Glucose testing commanded 80.92% Blood lancet market share in 2025, a testament to entrenched diabetes management guidelines. Each insulin-treated patient averages three to five finger-sticks per day, translating into resilient recurrent revenue. Yet haemoglobin testing advances at an 8.21% CAGR through 2031 as anemia-screening mandates enter prenatal and geriatric care bundles worldwide, creating tailwinds for higher-gauge blade formats optimized for lower-volume draws.

Emerging applications in lipid profiling, rapid infectious-disease screens, and platelet-rich plasma procedures progressively diversify consumption. These new use cases rely on capillary micro-samples rather than venous draws, ensuring the Blood lancet market retains relevance even as non-invasive glucose monitoring gains share.

Geography Analysis

North America’s Blood lancet market size leads with a 41.88% revenue share in 2025, anchored by Medicare reimbursement for safety consumables and widespread insurance coverage for at-home diabetes supplies. Hospitals in the United States routinely adopt pain-minimized lancets to bolster patient satisfaction metrics and avert worker-safety litigation. Canadian provincial health plans deploy community-pharmacy collection hubs that distribute subsidized lancet starter kits, sustaining baseline demand.

Asia-Pacific is the fastest-growing region, projecting an 8.25% CAGR through 2031 as India’s national non-communicable disease (NCD) program scales rural screening and China’s urban clinics adopt tele-monitoring platforms. Public-private partnerships supply low-cost safety lancets in Indonesia’s provincial health posts, while Japan’s aging society pushes daily capillary testing volumes upward in long-term-care homes. Currency-hedged contract structures and local blade machining investments protect multinational suppliers from raw-material price shocks in the region.

Europe maintains stable share through robust procurement consortia such as NHS Supply Chain, which reserve tender slabs for environmentally compliant devices. Sharps-waste directives incentivize biodegradable components, opening niche opportunities for polymer innovators. South America’s growth revolves around Brazilian Unified Health System upgrades and Argentina’s import-substitution incentives, whereas Gulf Cooperation Council states procure premium microneedle kits aimed at medical tourists. Overall, region-specific reimbursement and regulation patterns collectively broaden the Blood lancet market while tempering one-size-fits-all product strategies.

Competitive Landscape

The Blood lancet industry is moderately concentrated. Becton Dickinson, Roche, and Abbott leverage global distribution infrastructure, proprietary blade-coating chemistries, and high-throughput molding lines to guard share. Mid-tier players such as Owen Mumford differentiate via customizable depth settings and pediatric-friendly designs, while Asian OEMs pursue cost leadership on standard lancets. Vertical integration into needle-wire drawing and automated assembly grants incumbents scale economies that buffer commodity steel price swings.

R&D pipelines focus on pain reduction, workflow automation, and eco-friendly materials. BD’s UltraTouch set uses thinner pen-point tips that cut penetration force by up to 32%. Owen Mumford’s Unistik 3 received multi-gauge FDA clearance in 2025, widening clinical versatility. Start-ups prototype laser-based micro-perforation to sidestep disposable blades, posing a medium-term disruption threat.

Strategic moves include MTD Group’s acquisition of Ypsomed’s consumable unit, boosting annual capacity past 2.5 billion pieces and strengthening negotiating power with raw-material suppliers. Terumo invests in donor-focused devices linked to its plasma-collection systems, creating cross-selling synergies. Meanwhile, Medline’s recall of swabsticks underscores that quality-assurance lapses can ripple across adjacent single-use categories, prompting buyers to favor vendors with spotless compliance histories. Collectively, innovation cadence, supply-chain resilience, and regulatory alignment will dictate competitive outcomes within the Blood lancet market through 2030.

Blood Lancet Industry Leaders

Becton, Dickinson and Company

F. Hoffmann-La Roche Ltd

B. Braun Melsungen AG

Abbott

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: MTD Group acquired Ypsomed’s pen needle and blood glucose-monitoring units, expanding annual output to 2.5 billion pieces and lowering per-unit costs through vertical integration.

- April 2024: BD India launched the BD Vacutainer UltraTouch Push Button Blood Collection Set featuring RightGauge and PentaPoint technologies, claiming an 88% reduction in needle-injury risk.

- March 2024: NHS Supply Chain issued a GBP 288 million tender for blood-collection devices with a GBP 20 million allocation for safety lancets, cementing strict sustainability and injury-prevention criteria.

- February 2024: Medline initiated a Class 2 recall of alcohol swabsticks due to weak seals that might compromise sterility, spotlighting supply-chain vigilance across single-use devices.

Global Blood Lancet Market Report Scope

As per the scope, a blood lancet is the blood sampling device used in capillary blood sampling. The instrument has a double-edged blade that punctures the skin, and then the blood sample can be collected, which is further used for various monitoring and diagnosing purposes. The Blood Lancet Market is Segmented by Product Type (Safety Lancet, Homecare Lancet), End User (Hospitals, Blood Banks, Home Care, Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). ). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (USD million) for the above segments.

| Safety Lancets |

| Standard / Personal-use Lancets |

| Hospitals |

| Blood Banks |

| Diagnostic Laboratories |

| Home Care |

| Others |

| Glucose Testing |

| Haemoglobin Testing |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Safety Lancets | |

| Standard / Personal-use Lancets | ||

| By End User | Hospitals | |

| Blood Banks | ||

| Diagnostic Laboratories | ||

| Home Care | ||

| Others | ||

| By Application | Glucose Testing | |

| Haemoglobin Testing | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the Blood lancet market in 2031?

The Blood lancet market is expected to be worth USD 2.92 billion by 2031.

Which product type currently leads sales?

Safety lancets led with 60.74% revenue share in 2025 due to mandatory sharps-injury prevention rules.

Which region is growing fastest?

Asia-Pacific posts the highest growth, advancing at an 8.25% CAGR through 2031.

Why are diagnostic laboratories gaining momentum?

Personalized medicine panels and direct-to-consumer testing push diagnostic laboratories to an 8.12% CAGR, the fastest among end-user groups.

How is technology changing lancet demand?

Painless microneedle innovation and the rise of continuous glucose monitors improve user experience but also create a longer-term substitution threat for conventional lancets.

Page last updated on: