Tympanostomy Products Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

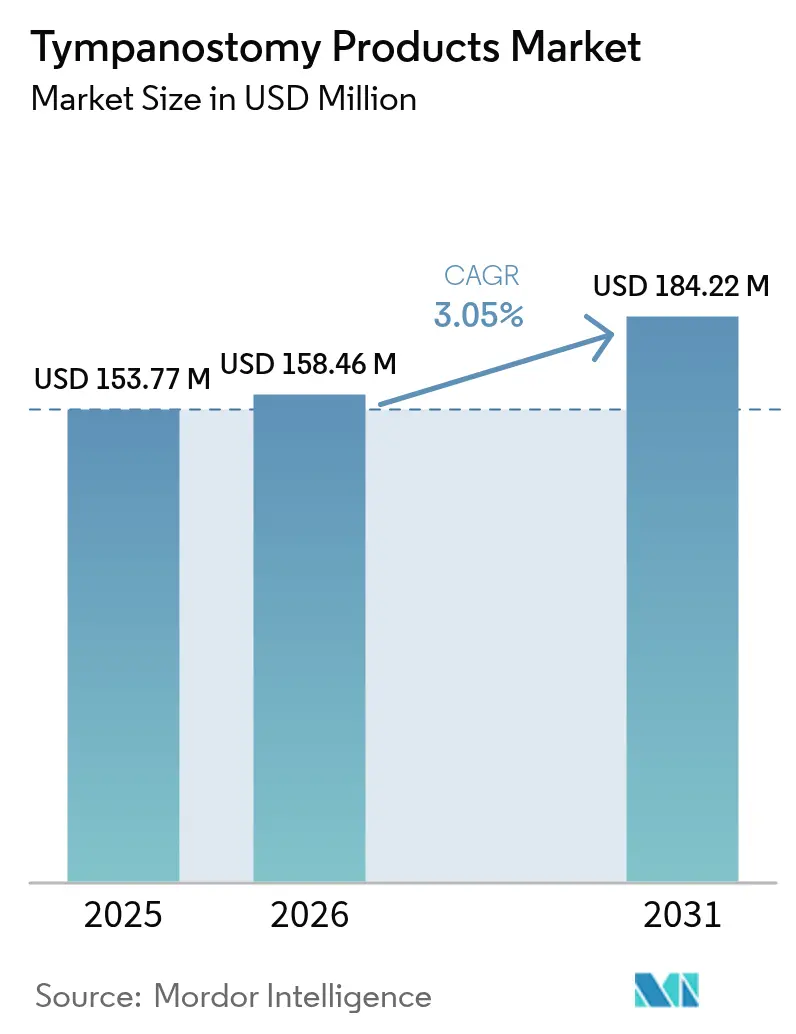

| Market Size (2026) | USD 158.46 Million |

| Market Size (2031) | USD 184.22 Million |

| Growth Rate (2026 - 2031) | 3.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tympanostomy Products Market Analysis by Mordor Intelligence

tympanostomy products market size in 2026 is estimated at USD 158.46 million, growing from 2025 value of USD 153.77 million with 2031 projections showing USD 184.22 million, growing at 3.05% CAGR over 2026-2031. Ongoing migration of ear-tube placement from hospital operating rooms to office-based suites reshapes competitive priorities as suppliers shift from volume-driven catalogs toward higher-value systems that streamline procedure time, lower anesthesia exposure and reduce payer outlay. Demand is reinforced by pediatric otitis-media prevalence—with more than 80% of children experiencing at least one episode before age 3—and by antimicrobial-stewardship policies that increasingly favor surgical solutions over repeated antibiotic cycles. North America remains the largest regional buyer on the strength of mature reimbursement, while Asia-Pacific generates the fastest incremental revenue as surgical capacity and disposable incomes expand. Product leadership is maintained by tympanostomy tubes, yet growth momentum is most visible in accessories and single-use insertion kits aligned with same-day care models.

Key Report Takeaways

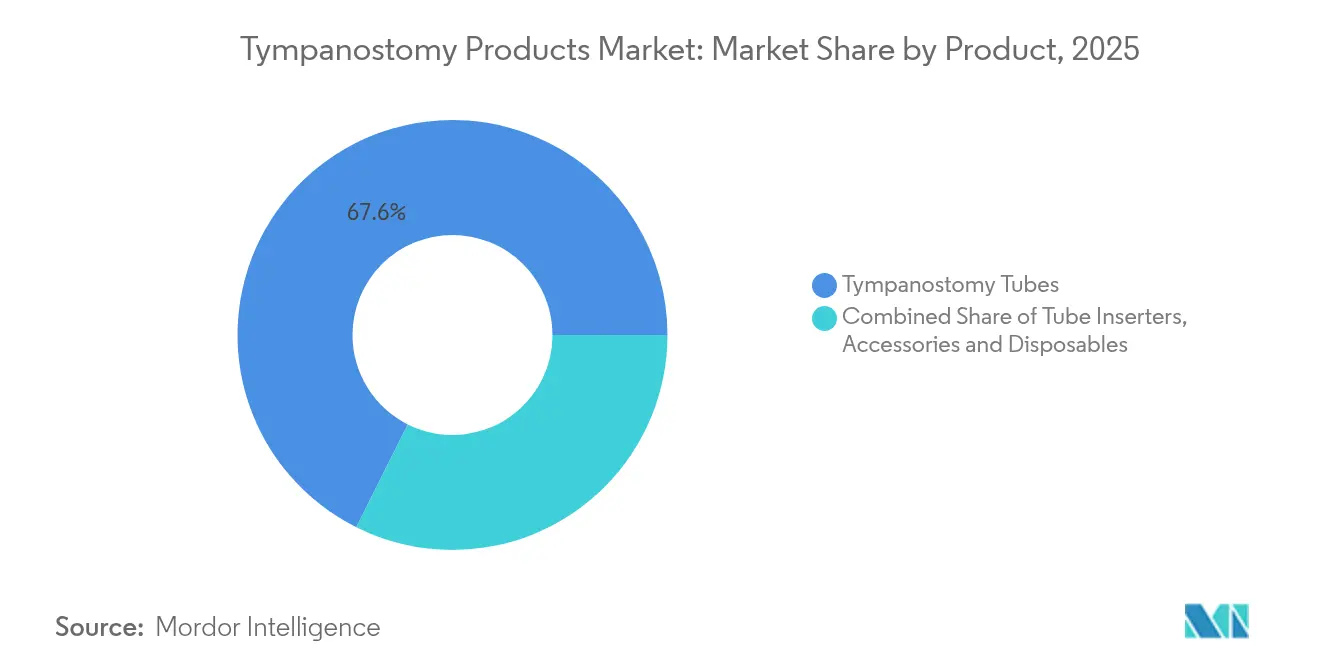

- By product category – Tympanostomy tubes captured 67.62% of tympanostomy products market share in 2025; accessories and disposables are projected to grow at a 4.05% CAGR through 2031.

- By material – Silicone held 45.15% share of the tympanostomy products market size in 2025, while fluoroplastic materials are expected to register a 3.95% CAGR to 2031.

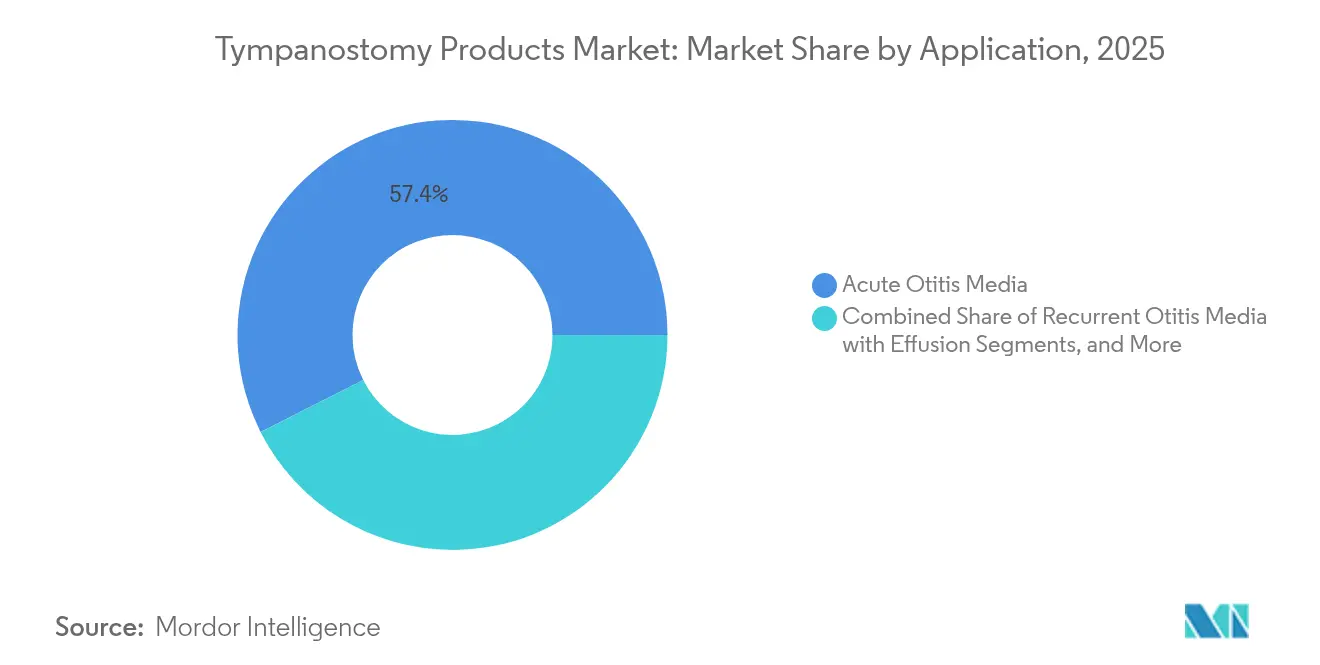

- By application – Acute otitis media accounted for 57.44% of demand in 2025; recurrent otitis media with effusion is advancing at a 3.66% CAGR through 2031.

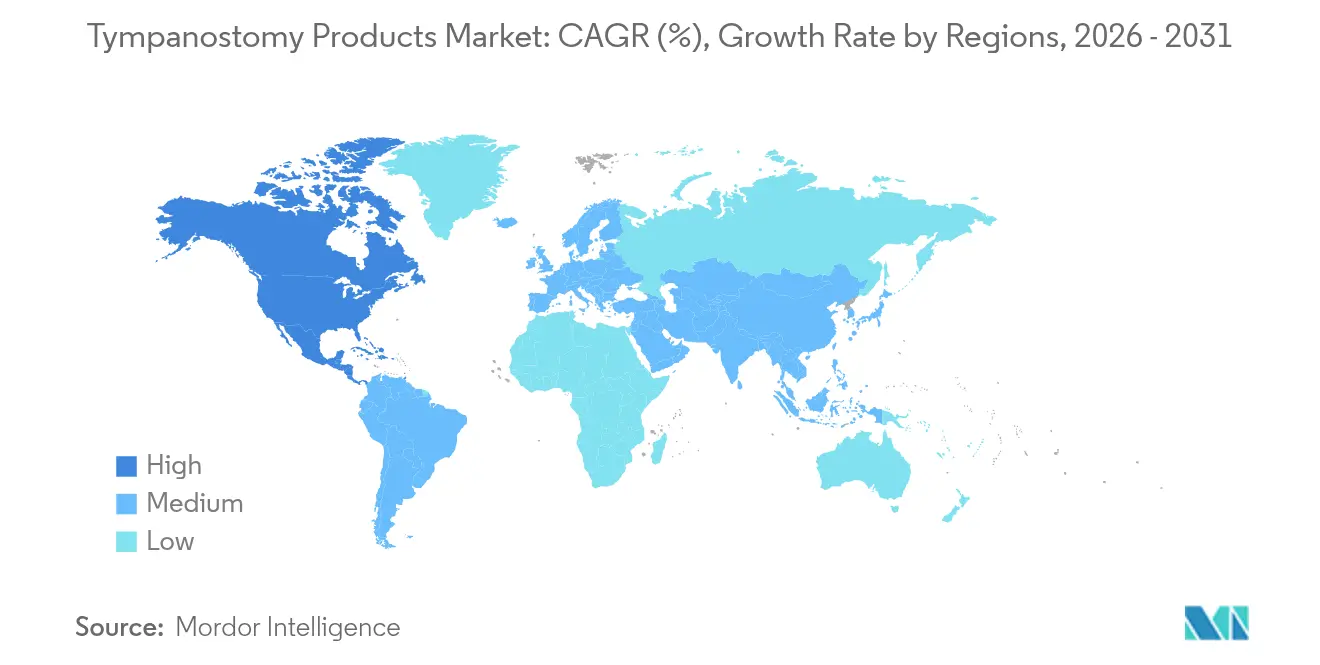

- By geography – North America led with 45.30% revenue share in 2025, whereas Asia-Pacific is forecast to expand at a 4.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tympanostomy Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High pediatric otitis-media incidence | +1.2% | Global; higher in developing regions | Long term (≥ 4 years) |

| Advances in minimally invasive inserters | +0.8% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Emergence of bioresorbable / drug-eluting tubes | +0.6% | Global; led by developed markets | Long term (≥ 4 years) |

| Expanding ENT surgical capacity in emerging markets | +0.9% | APAC core; spill-over to MEA and Latin America | Medium term (2-4 years) |

| Tele-monitoring of postoperative patients | +0.3% | North America & Europe | Short term (≤ 2 years) |

| Office-based reimbursement incentives | +0.7% | North America, expanding to Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Pediatric Otitis-Media Incidence

Persistent global cases sustain volume in the tympanostomy products market. Vaccination lowered some serotypes, yet non-vaccine strains keep surgical demand elevated. Clinical focus on minimizing systemic antibiotics positions ear-tube insertion as the preferred alternative. Drug-eluting designs that locally release antimicrobials further align with stewardship objectives. Emerging-economy middle-class growth magnifies the long-term driver by increasing access to pediatric ENT surgery.

Advances in Minimally Invasive Inserters

Office-based systems reduce anesthesia use and trim total procedure cost by nearly 60%. The FDA-cleared Hummingbird TTS combines myringotomy and tube placement in a single pass and has proven safe in more than 225 pediatric cases. Such devices fit same-day consult-and-treat pathways, accelerating adoption in regions with robust ambulatory reimbursement and contributing additional lift to the tympanostomy products market.

Emergence of Bioresorbable / Drug-Eluting Tubes

Silk-protein or polylactide tubes that dissolve once function is complete eliminate secondary removal procedures. Simultaneous release of ciprofloxacin or similar agents maintains therapeutic middle-ear concentrations without caregiver compliance issues. Although regulatory timelines temper near-term revenue, these platforms enable premium pricing strategies while addressing unmet needs, fortifying the long-range expansion of the tympanostomy products market [1]Sarah A. Bradner, “Silk Protein Bioresorbable, Drug-Eluting Ear Tubes: Proof-of-Concept,” Advanced Healthcare Materials, onlinelibrary.wiley.com.

Expanding ENT Surgical Capacity in Emerging Markets

Planned addition of 34,000 private-hospital beds in India and continued Chinese investment grow operating-suite availability and open referral pipelines. Local ENT residency programs and technology-transfer ventures spread competence beyond tier-1 cities. The resulting procedure-volume uplift positions Asia-Pacific as the principal engine of future gains within the tympanostomy products market.

Tele-Monitoring of Postoperative Patients

Remote otoscopy and mobile-app symptom tracking allow clinicians to detect complications early, driving confidence in office placements. Insurers increasingly reimburse brief digital check-ins, which close follow-up gaps and support wider uptake of minimally invasive tubes, particularly in rural North America and Europe where travel distance once discouraged surgery.

Office-Based Reimbursement Incentives

CPT code 69433 and comparable European tariffs reimburse ear-tube insertion under local anesthesia at favorable rates, making in-clinic procedures financially attractive for providers. This shift diverts volume from hospital ORs, elevating demand for integrated kits and reinforcing the tympanostomy products market’s orientation toward value-driven devices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of pharmacologic / watch-and-wait therapies | -0.4% | Global, stronger in regions with conservative treatment approaches | Medium term (2-4 years) |

| Risk of post-operative infections & complications | -0.3% | Global, with higher impact in resource-limited settings | Long term (≥ 4 years) |

| Stringent sterility & regulatory requirements | -0.5% | Global, with highest impact in emerging markets | Medium term (2-4 years) |

| Antimicrobial-stewardship limiting tube placements | -0.2% | North America & Europe, expanding globally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Pharmacologic / Watch-and-Wait Therapies

Guidelines from the American Academy of Otolaryngology advise conservative observation for single effusion episodes under three months, and Italian consensus protocols support narrow-spectrum antibiotics for mild cases. These recommendations temper procedure growth, especially in cost-contained systems. However, improved diagnostics that flag non-resolving fluid and antimicrobial-resistance pressures may ultimately refine rather than suppress surgical demand.

Risk of Post-Operative Infections & Complications

Otorrhea episodes affect roughly half of pediatric tube recipients, and premature extrusion or persistent perforation creates additional follow-up burden. Such events prompt parental hesitancy and payer scrutiny. Device makers counter with antimicrobial coatings, hydrophobic lumens and predictable resorption times to curtail complication incidence, which, if successful, should buffer the longer-term restraint on the tympanostomy products market [2]Laura L. Neff, “Ear Infections in Children: What You Can Do and When It’s Time for Ear Tubes,” Children’s Mercy, childrensmercy.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Tubes Dominate Despite Accessory Growth

Tympanostomy tubes commanded 67.62% of tympanostomy products market share in 2025 on the back of their central therapeutic role. The category remains the cornerstone of the tympanostomy products market, yet unit volumes plateau in mature regions. In parallel, the accessories and disposables segment records a 4.05% CAGR, reflecting a move toward bundled procedural kits that guarantee sterility and shorten chair time.

Single-pass inserters, preloaded blade-and-tube cartridges and suction-assisted visualization devices underpin this surge. Providers prefer turnkey packs that align with office workflow, which in turn lifts the tympanostomy products market size associated with consumables and instrumentation. Digital otoscopes and smartphone-based endoscopy further augment accessory purchasing patterns by allowing instant image capture for documentation and audit compliance.

By Material: Silicone Leadership Challenged by Fluoroplastic Innovation

Silicone tubes retained a 45.15% slice of the tympanostomy products market size in 2025 owing to surgeon familiarity, softness and ease of insertion. Nonetheless, fluoroplastic designs are pacing the field with a 3.95% CAGR through 2031. Their low surface energy reduces biofilm build-up and lumen obstruction, extending functional dwell time and lowering repeat procedure rates.

Titanium and emerging bioresorbable polymers cater to niche but clinically significant subpopulations such as patients needing multi-year ventilation or those at elevated anesthesia risk. Bioresorbable variants remove the need for extraction, a feature highly valued by parents and pediatricians alike. Drug-eluting versions under review align material science with pharmacology, providing an attractive value proposition and sustaining competitive churn within the tympanostomy products market.

By Application: Acute Cases Drive Volume, Recurrent Conditions Show Promise

Acute otitis media drove 57.44% of 2025 procedures, cementing its status as the primary volume contributor to the tympanostomy products market. Rapid symptom relief and prevention of conductive hearing loss underpin its clinical appeal.

Recurrent otitis media with effusion, although currently a smaller slice, accelerates at a 3.66% CAGR. Surgeons increasingly advocate pre-emptive tube placement after successive fluid episodes to mitigate speech-development delays and to reduce systemic-antibiotic exposure. Parallel interest in treating chronic eustachian-tube dysfunction with balloon dilation or stent systems broadens the procedural toolkit but does not materially displace tube demand; instead, it introduces combination therapy opportunities that keep the tympanostomy products market dynamic.

Geography Analysis

North America generated 45.30% of global revenue in 2025, benefitting from entrenched pediatric ENT pathways, comprehensive insurance coverage and swift uptake of in-office technologies such as the Hummingbird TTS. Nearly 700,000 procedures are performed annually in the United States, and payer policies that reimburse local-anesthesia placements sustain high throughput. However, utilization reviews that flag potential overuse in certain metropolitan areas temper incremental growth. Continued FDA clearances for adjunct devices, including acoustic therapy systems, reinforce the technology pipeline and maintain regional leadership .

Asia-Pacific is the most buoyant zone with a projected 4.29% CAGR, lifted by rapid hospital build-outs and a widening middle-class denominator. Indian private chains plan USD 6 billion of capacity additions by 2029, while Chinese industrial policy encourages domestic manufacturing and foreign technology partnerships. Disparities in ENT specialist distribution persist, yet tele-mentoring and mobile clinics are narrowing the gap, translating into broader regional penetration of the tympanostomy products market.

Europe maintains steady climb amid universal healthcare systems that reimburse evidence-based interventions. Budgetary caps in some nations curb premium pricing, but clinical-data-driven procurement favors suppliers with robust safety and efficacy dossiers. Latin America and Middle East Africa remain emerging frontiers: expanding medical-school outputs and improving insurance coverage create a pipeline for future procedure growth even as macroeconomic volatility moderates near-term expansion. Collectively, these dynamics ensure geographic diversification of the tympanostomy products market over the forecast horizon.

Regulatory Landscape

In the United States tympanostomy devices are regulated as Class II otolaryngology devices under 21 CFR Part 874 with related 21 CFR 874.3930 classifications for semipermeable membranes. Clearance pathways predominantly rely on predicate-based 510(k) submissions, with labeling, sterilization validation, and performance testing central to approvals, and ISO 10993-1:2018 biocompatibility requirements anchoring material and coating choices for pediatric use. Notable anchors include AventaMed's Solo+ Tympanostomy Tube Device clearance (K232702, May 2024) and Tusker Medical's Tula Tympanostomy Tube Delivery Device clearance (K252436, April 2026), alongside a PMA supplement for a manufacturing process change (P190016/S010, October 2025).

Value Chain Analysis

The tympanostomy value chain starts with specialty materials such as silicone elastomers and PTFE, moving through precision component fabrication and assembly into ventilation tubes, preloaded delivery devices, and single-use procedural kits. Ethylene oxide sterilization remains a gating step for many components, shaping lead times and batch-release planning for office-based workflows. Downstream, products move via OEM sales teams and regional distributors into hospitals, ambulatory surgery centers, and ENT office-based suites where integrated systems and reliable consumables are increasingly valued. FDA-reviewed manufacturing changes can alter release workflows and supply cadence, and 2025 component tariffs plus broader supply-chain scrutiny have pushed suppliers toward tighter qualification, dual-sourcing, and inventory buffering for high-volume accounts.

Competitive Landscape

Market structure is moderately fragmented, with diversified multinationals such as Medtronic, Olympus and Smith & Nephew contending alongside focused ENT specialists and start-ups. No single company exceeds a one-third revenue stake, leaving room for differentiated platforms to gain traction. Leading suppliers bundle tubes, blades, suction tips and visualization aids into unified kits aimed at office workflows, reinforcing the pricing power of integrated solutions.

Acquisitions target capability gaps: Integra LifeSciences’ USD 1 billion purchase of Acclarent in April 2024 expanded its ENT presence and added balloon-dilation assets that complement tube portfolios. Partnerships also flourish; regional distributors in Asia-Pacific secure exclusive rights to U.S. innovations in exchange for regulatory navigation and hospital access.

Competitive advantage increasingly hinges on demonstrable clinical-economic value. Studies validating reduced anesthesia risk, shorter chair time or lower revision rates translate into tender wins. Digital-health add-ons—ranging from postoperative tele-monitoring dashboards to machine-learning algorithms that flag fluid recurrence—enhance differentiation and sustain the competitive churn propelling the tympanostomy products market.

Tympanostomy Products Industry Leaders

Adept Medical Ltd

Atos Medical

Grace Medical

Integra LifeSciences Corporation

Olympus Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The market is advancing as ear-tube placement shifts from hospital operating rooms to in-office settings, expanding demand for integrated, single-use delivery systems that streamline procedures in ENT clinics and ambulatory sites. Evidence from 510(k) clearances for office-based platforms, including Solo+ (May 2024) and Tula (April 2026), anchors this shift and supports workflow-fit packaging and standardized sterile kits. In parallel, a January 2026 study on Tympanostomy U-Tube reports a 2.08 percent permanent perforation rate in the evaluated cohort, underscoring ongoing interest in designs that optimize dwell time and removal. January 2026 also highlights 3D printing and machine-learning optimization of tube geometry, signaling faster iteration while preserving compatibility with Class II regulatory pathways for tympanostomy devices.

Recent Industry Developments

- April 2026: Tusker Medical received FDA 510(k) clearance (K252436) for the Tula Tympanostomy Tube Delivery Device. The clearance enables broader in-office deployment and integrated workflow for ENT procedures.

- June 2025: AventaMed (a KARL STORZ company) announced an expanded FDA indication for the Solo+ Tympanostomy Tube Device to include pediatric patients aged 6 months and older. The update broadens the addressable pediatric segment for in-office, single-use placement systems.

- April 2024: Integra LifeSciences completed its approximately USD 1 billion acquisition of Acclarent, expanding its ENT device portfolio and commercial footprint.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as revenues generated from tympanostomy tubes and related insertion tools used to create a temporary ventilation pathway through the tympanic membrane during ENT procedures, along with commonly bundled accessories and disposables.

Scope exclusions: Hearing-aid components, diagnostic otoscopes, and implantable middle-ear devices are not counted in this sizing.

Segmentation Overview

- By Product

- Tube Inserters

- Tympanostomy Tubes

- Accessories & Disposables

- By Material

- Silicone

- Fluoroplastic (Teflon)

- Others

- By Application

- Acute Otitis Media

- Recurrent Otitis Media with Effusion

- Eustachian Tube Dysfunction

- Chronic Tympanic-Membrane Perforation

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Rest of World

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for ear infection and ear tube procedures, and then mapping it back to product usage and pricing. We refer to public health and statistical sources such as CDC materials on otitis media, WHO health statistics where relevant, and OECD health data for procedure trends and care access signals.

To keep assumptions grounded, we also review product and regulatory context using sources such as the US FDA device databases and safety communications, along with published clinical guidelines and peer-reviewed ENT literature that describe tube selection, revision rates, and typical care pathways. We scan company filings, investor presentations, reputable press, and public tender notices when they help validate mix shifts and distribution patterns. We selectively use paid subscriptions for company financials and patent databases to clarify portfolios and timeline shifts. The sources listed here are illustrative, and many other public and paid references were also used to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure-test procedure volumes, typical kit contents, and price movement by channel before our final totals are locked. We speak with a mix of manufacturers, distributors, ENT clinicians, and procurement or materials teams across APAC, EMEA, and the Americas, so gaps from desk inputs can be filled and assumptions can be triangulated.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 44% |

| Mid tier: 53% | Functional/Unit leaders: 33% | EMEA: 32% |

| Smaller Players: 16% | Managers: 53% | Americas: 24% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where procedure and treated-patient signals are reconstructed by region, and then converted into product demand using usage rates per case. Those totals are then checked with selective bottom-up approximations, such as sampled ASP times volume by channel and a supplier and distributor roll-up on a limited set of countries, so the final number stays realistic.

Key inputs that move the model include ear infection burden and recurrence patterns, tympanostomy procedure volumes by care setting, tube replacement and revision frequency, average tubes used per procedure, and observed shifts between hospitals and ambulatory surgery centers. Pricing is handled through a simple ASP logic that separates tubes from inserters and from accessories and disposables, and then applies region-specific mix and inflation assumptions that were validated in interviews.

For forecasting, scenario analysis is used around a central case, since procedure recovery cycles and pricing tend to change in steps rather than in a smooth line. Assumptions are carried forward with checks on clinical practice patterns and reimbursement pressure. Where country data is thin, nearby market proxies are applied and then corrected using expert feedback before it is accepted.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including procedure activity direction, pricing movement, and expected mix splits by setting of care. When a variance shows up, we recheck the underlying driver first, and then re-contact sources if the gap is still not explainable by seasonality or one-time ordering.

Before sign-off, the model goes through multi-step analyst review, including reasonableness checks at regional and country levels, and a final sweep for currency conversion consistency. Reports are refreshed annually, and interim updates are triggered when there are material events such as meaningful price changes, regulatory shifts, or noticeable procedure disruptions. A final pre-delivery pass is then completed so clients receive the latest view.

Mordor Intelligence's Tympanostomy Products Market Size Measured Against Other Published Estimates

Published market sizes for tympanostomy products can differ even when the product names look the same, because the counted items and timing choices are not always aligned. The year used for currency conversion, the way average selling prices are stepped forward, and how procedure volumes are validated across care settings are usually the biggest contributors to the spread.

In this study, refresh cadence and currency timing are treated as active inputs, and ASPs are updated using channel feedback and mix checks rather than being held flat. That is one reason the total lands higher than some conservative snapshots, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 158.46 M (2026) | |

| Healthcare Analytics A | USD 90.08 M (2024) | Uses an earlier base year and a narrower price build, and the growth profile suggests limited adjustment for care-setting mix shifts and post-period ASP movement. |

| Trade Publisher B | USD 95.80 M (2024) | Anchors the market to a single-year snapshot and a shorter forecast window, which can understate later-year price and mix effects if the update cycle is not aligned to recent procedure normalization. |

Overall, the spread is mainly explained by timing choices and by how pricing and procedure signals are refreshed. By keeping the scope tied to tubes, inserters, and commonly bundled disposables, and then validating volumes and ASP movement with repeat checks, our estimate stays traceable to clear demand and pricing drivers.

Key Questions Answered in the Report

What is the current Tympanostomy Products Market size?

The tympanostomy products market size stands at USD 158.46 million in 2026 and is set to grow to USD 184.22 million by 2031.

Who are the key players in Tympanostomy Products Market?

Adept Medical Ltd, Atos Medical, Grace Medical, Integra LifeSciences Corporation and Olympus Corporation are the major companies operating in the Tympanostomy Products Market.

Which is the fastest growing region in Tympanostomy Products Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Tympanostomy Products Market?

North America commands 45.30% of global revenue owing to mature reimbursement structures and high procedure volumes.

What product category is growing fastest?

Accessories and disposables, including single-pass inserters and procedural kits, are projected to expand at a 4.05% CAGR through 2031.

Page last updated on: