Catheter-Directed Thrombolysis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

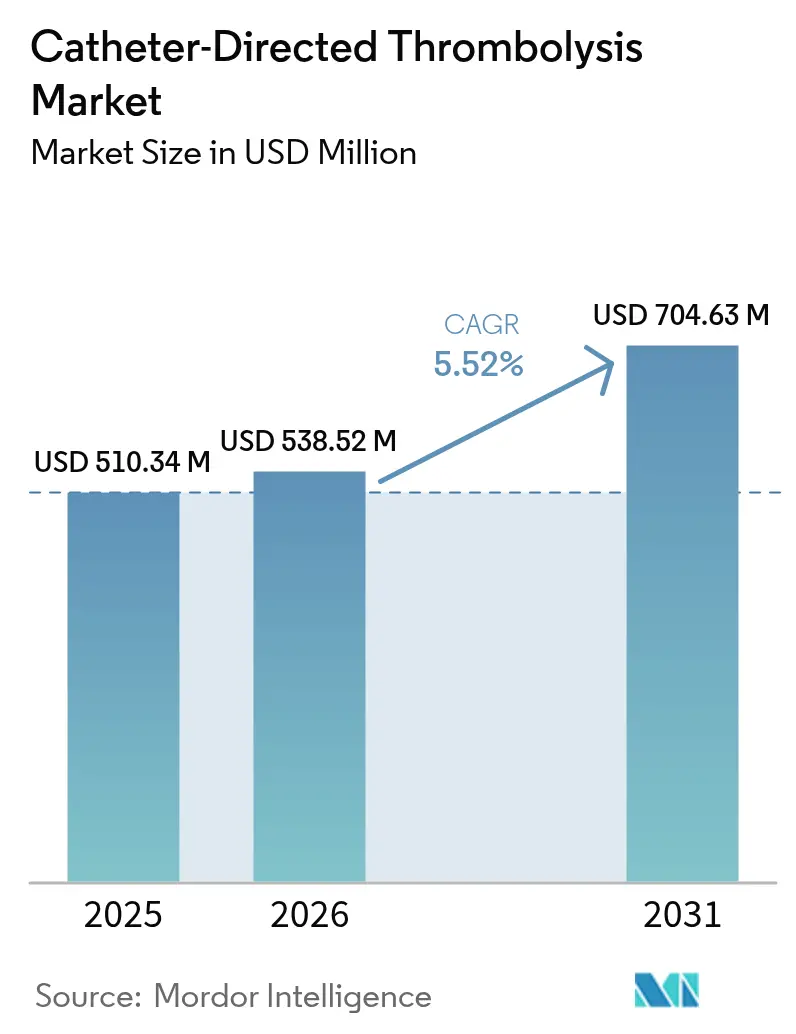

| Market Size (2026) | USD 538.52 Million |

| Market Size (2031) | USD 704.63 Million |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

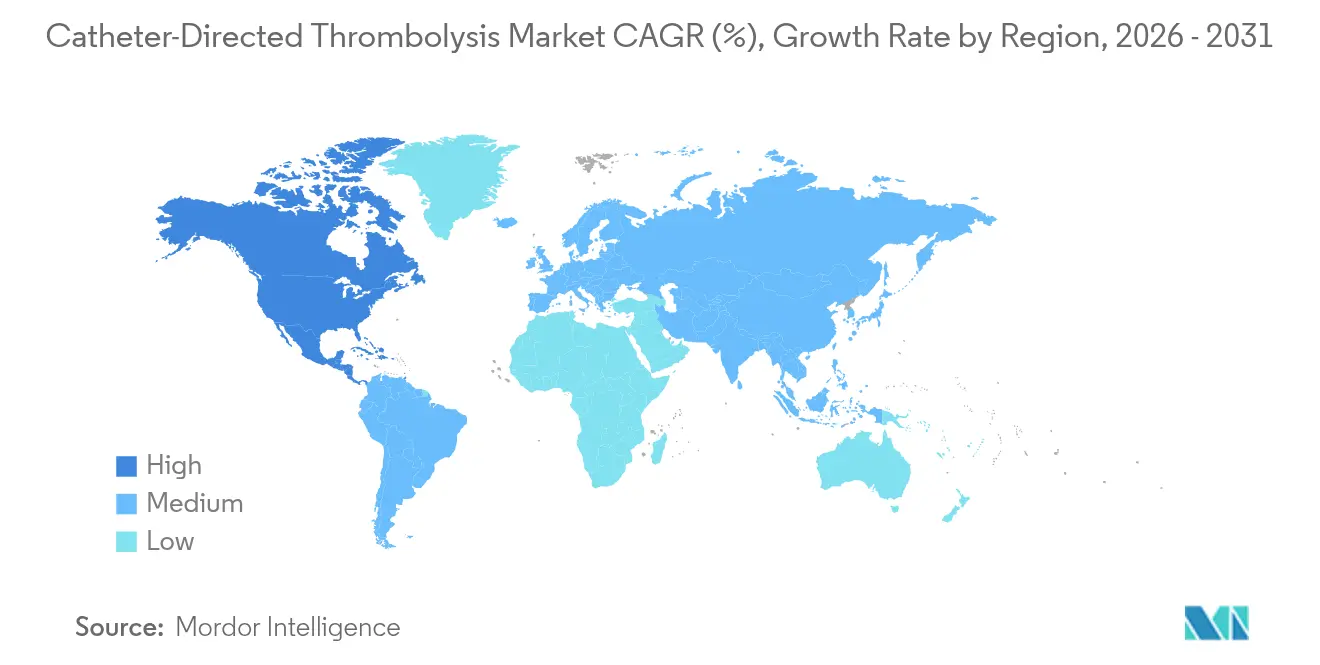

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Catheter-Directed Thrombolysis Market Analysis by Mordor Intelligence

catheter-directed thrombolysis market size in 2026 is estimated at USD 538.52 million, growing from 2025 value of USD 510.34 million with 2031 projections showing USD 704.63 million, growing at 5.52% CAGR over 2026-2031. The catheter-directed thrombolysis market is shifting from an experimental niche to a mainstream interventional option as mounting clinical evidence and broader reimbursement coverage encourage targeted thrombus dissolution over systemic lysis. Clinical urgency linked to venous thromboembolism (VTE) and peripheral artery disease (PAD), coupled with payer incentives that reward faster recovery and shorter intensive-care stays, keeps demand resilient. Vendors are widening portfolios to integrate ultrasound energy, aspiration modules, and AI-guided navigation, although procedure growth is tempered by interventional radiology (IR) workforce shortages and the ascent of mechanical thrombectomy-only systems. Capacity constraints outside tier-1 centers limit throughput, but technology convergence, outpatient migration, and favorable payment updates anchor a steady, mid-single-digit expansion path for the catheter-directed thrombolysis market.

Key Report Takeaways

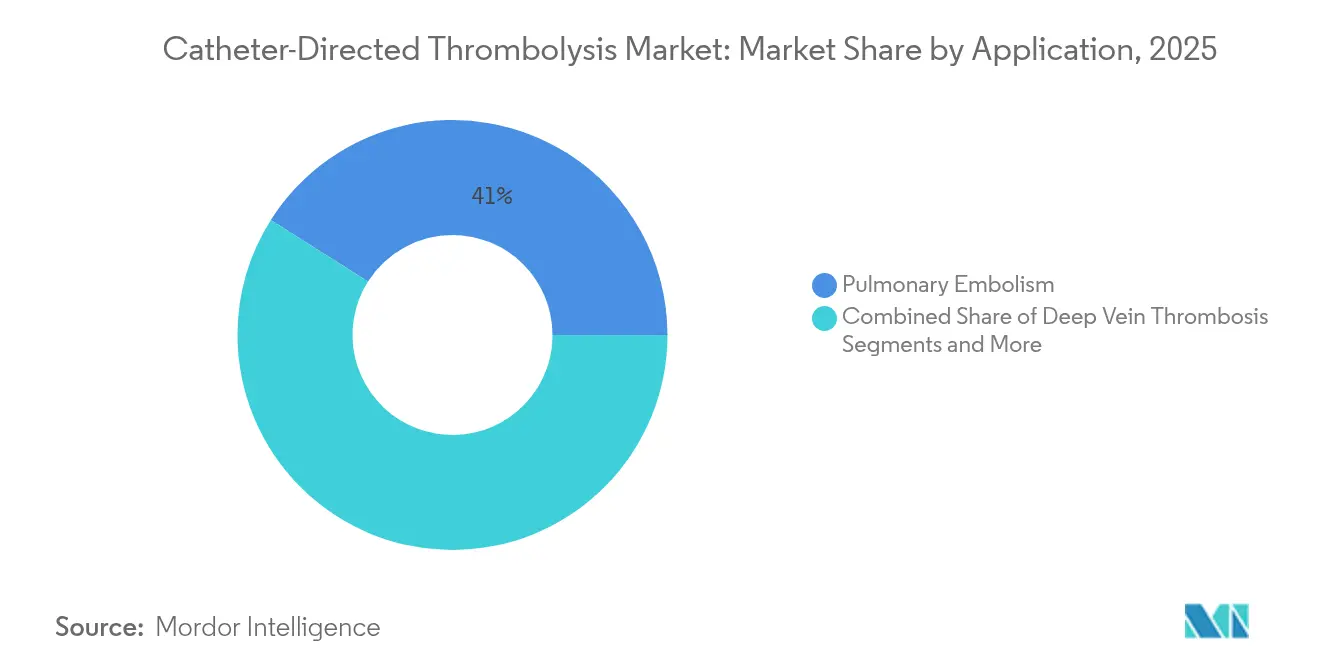

- By application, pulmonary embolism led with 41.02% of catheter-directed thrombolysis market share in 2025, while deep vein thrombosis is projected to grow at a 6.05% CAGR through 2031.

- By end user, hospitals held 62.64% of catheter-directed thrombolysis market size in 2025, whereas ambulatory surgical centers are expanding at a 6.43% CAGR to 2031.

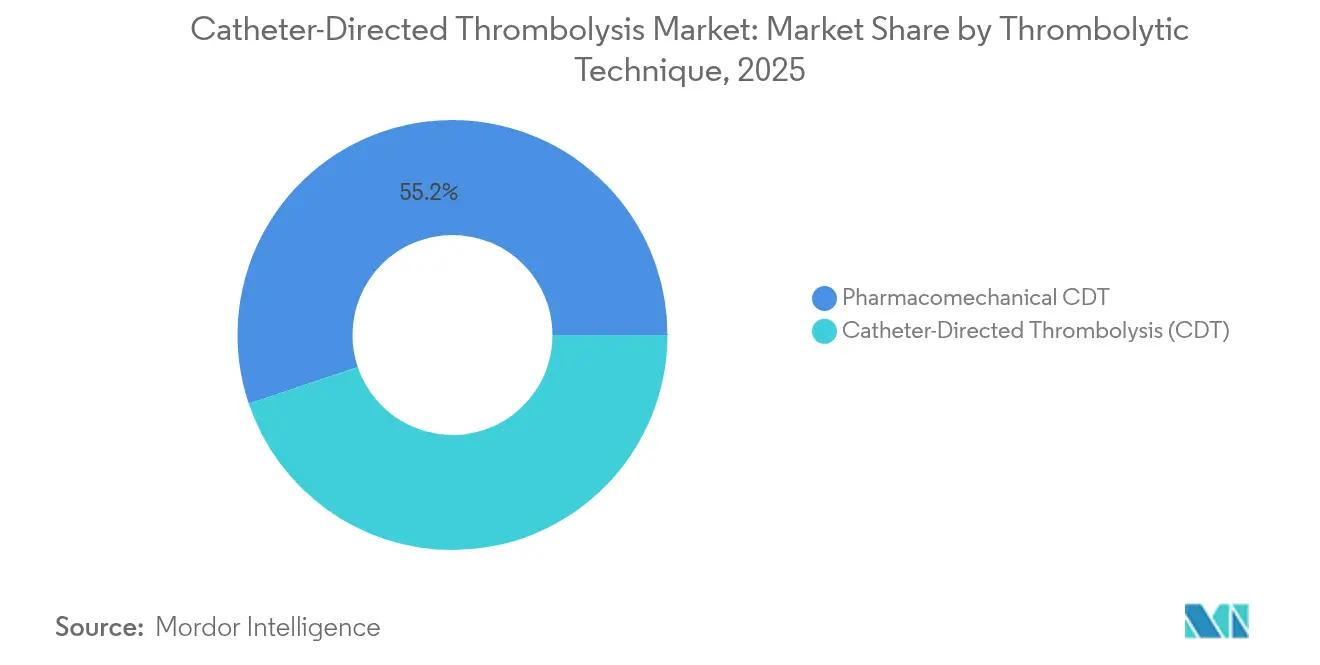

- By thrombolytic technique, pharmacomechanical systems accounted for 55.18% share of the catheter-directed thrombolysis market in 2025; traditional catheter-directed thrombolysis is forecast to advance at a 6.83% CAGR.

- By geography, North America commanded 41.95% share of the catheter-directed thrombolysis market in 2025, while Asia-Pacific is the fastest-growing region at a 7.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Catheter-Directed Thrombolysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Incidence of VTE & PAD | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapid Adoption of Pharmacomechanical CDT Systems | +0.9% | North America & EU core, expanding to APAC | Medium term (2-4 years) |

| Surge in Hospital Demand for Day-Case Minimally-Invasive PE Care | +0.7% | Global, led by North America & Western Europe | Short term (≤ 2 years) |

| AI-Guided Vascular Imaging Improving Procedural Success | +0.5% | North America, EU, Japan, with spillover to urban APAC | Medium term (2-4 years) |

| Value-Based Reimbursement Models Favoring Reduced ICU Stay | +0.8% | North America primary, EU secondary adoption | Short term (≤ 2 years) |

| Next-Gen Catheter Coatings Lowering Re-Intervention Rates | +0.6% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence of VTE & PAD

Escalating VTE prevalence—now the third-leading vascular killer worldwide—intensifies demand for catheter interventions that can remove clot burden without systemic bleeding risks. The aging demographic in developed markets and the lingering pro-thrombotic sequelae of COVID-19 amplify case volumes. Hospital audits place VTE incidence between 0.53% and 19.8% among acute stroke admissions, underscoring sizable procedural headroom. Because PAD often coexists with VTE, cross-indication use bolsters procedure growth, anchoring a recurring revenue base for the catheter-directed thrombolysis market.

Rapid Adoption of Pharmacomechanical CDT Systems

Pharmacomechanical platforms held 55.71% of 2024 catheter-directed thrombolysis market share by combining mechanical fragmentation with localized drug delivery, thereby lowering lytic dose and bleeding risk. Ultrasound-assisted catheters enhance penetration of thrombolytics, while aspiration channels evacuate debris in one pass, trimming procedure times. The technology serves as a bridge while purely mechanical thrombectomy devices finalize pivotal trials, sustaining mid-term momentum for the catheter-directed thrombolysis market.

Surge in Hospital Demand for Day-Case Minimally Invasive PE Care

Hospitals worldwide are revising care pathways to enable same-day discharge for selected pulmonary embolism cases, easing bed pressure and capturing outpatient reimbursements. Medicare spending on ASC services hit USD 6.1 billion in 2022, reflecting a pronounced outpatient shift [1]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy 2024,” medpac.gov. Catheter-based thrombolysis, with shorter recovery than systemic lysis, aligns with these efficiency goals and stimulates incremental growth, particularly in urban centers with integrated IR suites.

AI-Guided Vascular Imaging Improving Procedural Success

Machine-learning tools that overlay real-time fluoroscopy with predictive catheter paths shorten procedure duration and reduce radiation exposure. Early trials of robotic catheter controls report perfect navigation success and an 18.38% drop in operator control loops, signaling future productivity gains. Vendors embedding AI modules differentiate offerings and secure premium pricing inside the catheter-directed thrombolysis market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Device & Drug Costs in Low-Income Settings | -0.8% | Emerging markets in APAC, MEA, Latin America | Long term (≥ 4 years) |

| Limited Interventional Radiology Capacity Outside Tier-1 Centers | -1.1% | Global, most acute in rural North America & developing regions | Medium term (2-4 years) |

| Bleeding-Risk Concerns for Elderly with Polypharmacy | -0.6% | Developed markets with aging populations | Short term (≤ 2 years) |

| Growing Competition from Mechanical Thrombectomy-Only Devices | -0.9% | North America & EU primary, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Interventional Radiology Capacity Outside Tier-1 Centers

Only 58.5% of independent IR residency seats were filled in 2024 in the United States, revealing a pipeline gap that directly constrains procedure volume. Comparable shortages in France kept mechanical thrombectomy output at 7,500 cases against theoretical capacity of 20,500, a proxy for CDT bottlenecks. In rural hospitals and emerging markets, lack of specialists forces referrals or delayed therapy, dampening uptake across the catheter-directed thrombolysis market.

Growing Competition From Mechanical Thrombectomy-Only Devices

The PEERLESS trial showed large-bore mechanical thrombectomy lowered clinical deterioration to 1.8% versus 5.4% with catheter thrombolysis, cutting ICU use by more than half [2]American College of Cardiology, “PEERLESS Trial Results,” acc.org. Devices that omit thrombolytics attract centers wary of bleeding in elderly or polypharmacy patients. As registry data confirm safety, payers may favor faster, drug-free solutions, pressuring traditional revenue streams in the catheter-directed thrombolysis market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Pulmonary Embolism Drives Current Volumes

Pulmonary embolism accounted for 41.02% of 2025 catheter-directed thrombolysis market size, reflecting its life-threatening nature and the preference for targeted clot lysis when systemic options are contraindicated. High-risk cases treated with catheter regimes showed 43% mortality versus 57% with veno-arterial ECMO alone across 34 European centers. Growing clinical endorsement keeps procedure demand steady even as mechanical systems vie for share.

Deep vein thrombosis (DVT) is the fastest-growing application segment, expanding at 6.05% CAGR through 2031 as outpatient protocols and refined risk stratification prompt earlier intervention. Expanded reimbursement for lower-extremity DVT procedures, coupled with rising obesity and cancer prevalence, widens the patient base. Lower acuity allows ambulatory settings to capture incremental volume, aiding geographic penetration of the catheter-directed thrombolysis market.

By End User: Hospitals Dominate Despite ASC Growth

Hospitals retained 62.64% of catheter-directed thrombolysis market size in 2025 thanks to ICU access and multidisciplinary backup. Complex pulmonary embolism and combined arterial-venous cases remain hospital-centric. However, ambulatory surgical centers (ASCs) posted a 6.43% CAGR and are poised to absorb elective DVT cases, supported by CMS reimbursement hikes of 5-13% for cardiac procedures between 2020 and 2024.

ASC expansion forces device vendors to streamline workflows and shorten observation windows. Mechanical thrombectomy’s 41.6% ICU utilization in PEERLESS versus 98.6% for CDT suggests protocols that can accelerate the outpatient pivot circulationjournal.jp. Over time, volume migration could rebalance end-user mix within the catheter-directed thrombolysis market.

By Thrombolytic Technique: Pharmacomechanical Leads Innovation

Pharmacomechanical systems captured 55.18% of 2025 catheter-directed thrombolysis market share by combining fragmentation, ultrasound penetration, and drug delivery. Systems such as AngioJet pair pressurized saline jets with simultaneous aspiration and demonstrate efficacy comparable to pharmacological lysis alone while using lower drug doses.

Traditional catheter thrombolysis, although older, is accelerating at a 6.83% CAGR as ultra-hydrophilic coatings and heparin-network surfaces extend antithrombotic performance up to 30 days . Enhanced safety supports renewed uptake, especially in centers preferring simpler capital expenditure profiles. Technique diversity underpins healthy competition and broadens clinician choice across the catheter-directed thrombolysis market.

Geography Analysis

North America held 41.95% of 2025 catheter-directed thrombolysis market size, anchored by broad insurance coverage, mature IR networks, and constant clinical trial activity. CMS doubled payments for cardiovascular CT and lifted ASC cardiac reimbursements, structurally rewarding adoption. Yet, workforce shortages limit penetration into suburban and rural centers, prompting tele-mentoring initiatives and hub-and-spoke referral models to maximise installed capacity.

Europe represents a mature but cost-pressured territory. France’s mechanical thrombectomy plateau illustrates system bottlenecks that also hamper CDT. Regulatory tightening under the Medical Device Regulation raises compliance costs but ultimately favors well-capitalized manufacturers. CE-mark clearances for devices such as Penumbra’s CAVT platform confirm steady pipeline flow, though budget scrutiny could cap premium pricing across the catheter-directed thrombolysis market.

Asia-Pacific is the fastest-growing region at a 7.1% CAGR, fueled by infrastructure upgrades and rising VTE awareness in China, Japan, and India. Inari Medical’s distribution alliances and Penumbra’s acknowledgment of geopolitical headwinds signal both opportunity and complexity. Value-engineered systems and modular pricing tiers are gaining traction as hospitals balance innovation with affordability. Expanding private insurance coverage in India and universal health reforms in China position the region as a pivotal demand driver for the catheter-directed thrombolysis market.

Regulatory Landscape

In the United States, catheter-directed thrombolysis and related mechanical thrombolysis catheters are commonly regulated as Class II devices under 21 CFR 870.5150. This typically requires FDA 510(k) clearance and adherence to applicable FDA guidance for intravascular catheters and thrombectomy/thrombolysis device clinical and nonclinical evidence packages. As manufacturers add features such as infusion control, ultrasound energy, aspiration modules, or integrated hemodynamics sensing, requirements tighten around performance testing, labeling, and clinical evidence to support intended use in indications such as pulmonary embolism and deep vein thrombosis.

In Europe, devices are governed by the Medical Device Regulation (EU) 2017/745, which raises clinical evaluation expectations and post-market surveillance obligations. This can increase the time and cost of conformity assessment through Notified Bodies. Where systems incorporate medicinal substances or are used alongside thrombolytic drugs in ways that trigger combination considerations, MDR provisions (including consultation pathways with medicinal product authorities) add regulatory complexity. Standards such as ISO 10555-1:2023 for sterile, single-use intravascular catheters and ISO 11070:2014 for introducers/guidewires remain important anchors for global technical documentation and risk management across product lines.

Value Chain Analysis

The catheter-directed thrombolysis value chain begins with raw materials and components, including biocompatible polymers, braided or coiled metal reinforcement, radiopaque markers, and coatings that influence trackability and thrombogenicity. Specialized catheter manufacturers and contract partners supply shaft extrusion, braiding, tip forming, and sub-assembly. Device developers then integrate infusion architectures and, in some platforms, adjunct modalities such as ultrasound-assisted delivery or aspiration.

Quality systems, biocompatibility and performance verification, and validated sterilization and packaging are key, and capacity constraints can show up when complex assemblies require specialized processes and centralized manufacturing footprints. Downstream, commercialization is driven by direct sales and clinical support into hospital systems and integrated delivery networks, where purchasing committees increasingly prefer vendors that can bundle capital equipment (where applicable), consumables, and training across multiple sites. Logistics and service support align to interventional radiology and vascular teams performing CDT in acute care settings, while ambulatory surgical centers are becoming more relevant for selected lower-acuity venous interventions, increasing demand for streamlined kits, predictable lead times, and standardized protocols that reduce observation and staffing burden.

Competitive Landscape

The catheter-directed thrombolysis market is moderately fragmented, with diversified conglomerates and pure-play innovators jostling for share. Boston Scientific’s USD 1.26 billion takeover of Silk Road Medical and Teleflex’s €760 million purchase of BIOTRONIK’s vascular intervention assets illustrate an arms-race for technology scale. Portfolio breadth now ranges from drug-eluting balloons to AI-driven navigation consoles, giving integrated suppliers pull-through advantages in key accounts.

Clinical evidence is a prime differentiator. The PEERLESS and FLASH studies furnished mechanical thrombectomy vendors with compelling safety data, forcing CDT incumbents to underscore cost-effectiveness or dual-modality versatility. Patent filings in hydrophilic coatings and heparin-network surfaces show continued R&D to improve biocompatibility and curb re-intervention, particularly important where payers tie reimbursement to long-term outcomes.

Smaller entrants exploit focused innovations—such as aspiration catheters for distal venous segments—to carve niches the majors overlook. Yet many ultimately enter partnership or acquisition discussions once pivotal trials validate performance. Consolidation is therefore likely to continue, gradually increasing market concentration even as novel devices proliferate across the catheter-directed thrombolysis market.

Catheter-Directed Thrombolysis Industry Leaders

Boston Scientific Corporation

AngioDynamics, Inc.

Thrombolex

Medtronic Plc

Edwards Lifesciences Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Clinical and technology momentum is creating whitespace for workflow-efficient CDT and pharmacomechanical protocols that reduce infusion time and ICU utilization, particularly for intermediate-risk pulmonary embolism pathways. Evidence generation and guideline positioning are practical demand enablers: 2026 guidance from major societies including AHA, ACC, and SIR recognizes catheter-directed approaches for intermediate-high-risk and high-risk pulmonary embolism when systemic fibrinolysis is contraindicated or ineffective. The 2026 CIRSE Standards of Practice also validate catheter-directed thrombolysis and mechanical thrombectomy as established endovascular options. This enables hospital pathway redesign toward day-case and shorter-stay models, where device platforms compete on procedural speed, hemodynamic improvement, and reduced lytic dose.

Product-level innovation is also opening adoption opportunities in catheter configurations aimed at time and access constraints in busy interventional suites. FDA 510(k) clearances in early 2026 for devices such as Argon Medical Devices VariFuse Adjustable Infusion Catheter and Liquet Medicals Versus catheter configuration highlight ongoing platform refresh cycles, including dual-tip/telescoping concepts designed for bilateral pulmonary embolism treatment and configurations oriented to pulmonary artery pressure measurement. New and ongoing clinical studies, including Flow Medicals 2026 pilot study preparations (NCT07681154) in acute intermediate-risk pulmonary embolism, add to trial activity that can broaden evidence bases and refine patient selection. At the same time, these developments intensify competition with mechanical thrombectomy-only systems as payers and providers compare total resource utilization.

Recent Industry Developments

- April 2026: Thrombolex announced enrollment of the 100th patient in the RAPID-PE clinical study evaluating its BASHIR Endovascular Catheter using an On-The-Table protocol for intermediate-risk pulmonary embolism. The milestone advances prospective evidence around pharmacomechanical lysis workflows designed to avoid prolonged post-procedure infusion. It also supports the companys positioning with centers prioritizing reduced ICU use and faster throughput.

- June 2025: AngioDynamics reported the first patient enrolled in the RECOVER-AV clinical trial evaluating the AlphaVac F1885 System in intermediate-risk pulmonary embolism. Initiation of a dedicated trial program helps build indication-specific safety and effectiveness data that procurement committees increasingly require for broader adoption. The study also supports competitive differentiation as catheter-based options are compared against purely mechanical approaches.

- May 2024: AngioDynamics announced CE Mark approval in Europe for the AlphaVac F1885 System for non-surgical removal of thrombi or emboli from the pulmonary arteries. The authorization expanded the companys commercial footprint for pulmonary embolism interventions across EU markets operating under MDR-era evidence and surveillance expectations. It also increased competitive intensity for hospitals evaluating device-based clot removal and adjunct thrombolysis strategies.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers catheter-directed thrombolysis (CDT) procedures where a catheter is used to deliver thrombolytic drugs directly to a clot inside a blood vessel, including pharmacomechanical catheter-directed approaches used in clinical practice.

Scope exclusions: Systemic thrombolysis given without catheter guidance and standalone mechanical thrombectomy procedures that do not include local lytic drug infusion are excluded.

Segmentation Overview

- By Application

- Deep Vein Thrombosis

- Pulmonary Embolism

- Ischemic Stroke

- Other Applications

- By End User

- Hospitals

- Ambulatory Surgical Centers

- By Thrombolytic Technique

- Catheter-Directed Thrombolysis (CDT)

- Pharmacomechanical CDT

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with defining the real demand pool for CDT by mapping clot-burden conditions and the care settings that actually perform these procedures. We referenced public health and utilization signals from sources such as the CDC, NIH and PubMed-indexed clinical journals, the WHO, and payer and hospital reporting that indicates procedure growth patterns.

On the supply and pricing side, we reviewed public regulatory and labeling material (including FDA safety communications and device listings), plus company filings, investor decks, and credible press coverage to understand where adoption is rising and how the therapy mix is shifting. Select paid subscriptions for company financials and patent databases were used only to speed up cross-checks on revenue exposure and technology direction. The examples above are not exhaustive, and many other public and internal references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with interventional clinicians, cath lab administrators, distributors, and product managers who see procedure flow and purchasing behavior in their day-to-day roles. We aimed for coverage across major geographies so differences in treatment preference, reimbursement strength, and site-of-care capacity could be reflected, then used these inputs to fill gaps in adoption rates and typical pricing (including what is bundled versus billed separately).

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | APAC: 39% |

| Mid tier: 40% | Functional/Unit leaders: 31% | EMEA: 36% |

| Smaller Players: 22% | Managers: 54% | Americas: 25% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach where epidemiology and treated-case rates were translated into likely CDT procedure volumes by region, and then converted into value using a blended procedure cost and device and drug pricing logic. To keep the totals realistic, we corroborated the outputs using selective bottom-up approximations, including supplier revenue exposure checks, sampled average selling price ranges, and channel feedback on annual unit movement, then adjusted where the two views did not line up.

Key inputs used in the model included VTE and PE and DVT case trends, the share of patients eligible for interventional management, hospital and ambulatory center procedure capacity, adoption of ultrasound-assisted and pharmacomechanical techniques, and the typical number of catheters and adjunct disposables used per case. Pricing was treated carefully because real-world quotes change with tender timing and bundled contracting, so we used ranges and converted them into an annual blended ASP by region before applying volumes.

Forecasts were produced using scenario analysis. Procedure growth, reimbursement tone, and interventional staffing constraints were varied within realistic bounds and then aligned with what experts described as plausible over the next five years. Where bottom-up signals were missing for smaller countries, we used proxy penetration rates from comparable markets with similar care access and payer dynamics, then rechecked the implied spend per treated patient for reasonableness.

Data Validation & Update Cycle

Validation was done through multiple checks so results stayed consistent with real-world clinical activity and purchasing behavior. We compared modeled outputs with independent signals such as procedure mix shifts discussed in clinical literature, country-level health spending direction, and publicly visible regulatory and labeling milestones, and flagged anomalies for review.

Before sign-off, the model and assumptions go through a stepwise analyst review. Any large variance by region triggers re-contact with select primary sources to confirm whether the gap is driven by pricing, adoption, or definition boundaries. Reports are refreshed annually, and interim updates are made when material events occur, such as major guideline changes, reimbursement updates, or notable product approvals. Right before delivery, a final pass is completed so clients receive the most current view available.

Mordor Intelligence's Catheter Directed Thrombolysis Market Sizing Compared With Other Published Estimates

Published market sizes for catheter-directed thrombolysis often do not match because groups make different calls on what is counted as CDT value and how they translate procedure activity into dollars. Differences usually come from scope boundaries, pricing treatment, and the timing of the base year used for currency and inflation handling.

A big gap driver here is how frequently ASP assumptions are refreshed, and whether exchange rates are taken from a consistent annual average. Since catheters and adjunct disposables are priced unevenly across regions and contracts, older price points can carry forward incorrectly. By updating pricing inputs and FX timing to a consistent yearly window, then rechecking the implied spend per procedure against interview feedback, Mordor Intelligence reduces drift that can show up when older price points are carried forward without a fresh validation pass.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 538.52 M (2026) | |

| Global Consultancy A | USD 565.94 M (2025) | Uses a different base year and may apply a broader spend boundary around CDT care, which can shift totals when currency timing and bundled pricing are not normalized the same way. |

| Industry Publisher B | USD 540.09 M (2026) | Appears to include a wider set of system elements and delivery modes in some definitions, so the included device and adjunct scope can be slightly different even when the base year matches. |

Overall, the spread is explained by a mix of timing and what gets counted inside the CDT spend basket, plus how prices are carried through the forecast. Our approach keeps the estimate traceable to treated-case volumes and a clearly stated ASP build, and then checks the result against clinical adoption and purchasing signals so the final number stays practical to use.

Key Questions Answered in the Report

What is the current Catheter-Directed Thrombolysis Market size?

The catheter-directed thrombolysis market is estimated at USD 538.52 million in 2026 and is forecast to reach USD 704.63 million by 2031 at a 5.52% CAGR.

Who are the key players in Catheter-Directed Thrombolysis Market?

Boston Scientific Corporation, AngioDynamics, Inc., Thrombolex, Medtronic Plc and Edwards Lifesciences Corporation are the major companies operating in the Catheter-Directed Thrombolysis Market.

Which is the fastest growing region in Catheter-Directed Thrombolysis Market?

Asia-Pacific leads with a projected 7.1% CAGR as China, Japan, and India boost procedure volumes and expand interventional capacity.

Which application area currently generates the highest revenue?

Pulmonary embolism holds the top spot, accounting for 41.02% of 2025 revenue within the catheter-directed thrombolysis market.

Page last updated on: