Wound Debridement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.54 Billion |

| Market Size (2031) | USD 7.29 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wound Debridement Market Analysis by Mordor Intelligence

wound debridement market size in 2026 is estimated at USD 5.54 billion, growing from 2025 value of USD 5.25 billion with 2031 projections showing USD 7.29 billion, growing at 5.62% CAGR over 2026-2031. Demand is propelled by population ageing, the rising burden of diabetes, and the fast uptake of AI-guided diagnostic tools that shorten time to treatment. Health systems also show growing preference for ultrasonic and hydrosurgical technologies that remove necrotic tissue without harming viable structures. Better clinical outcomes, shorter hospital stays, and mounting pressure to curb long-term care costs further support adoption. Meanwhile, sustainability concerns about single-use disposables and tighter regulatory oversight steer innovators toward greener materials and higher-quality evidence.

Key Report Takeaways

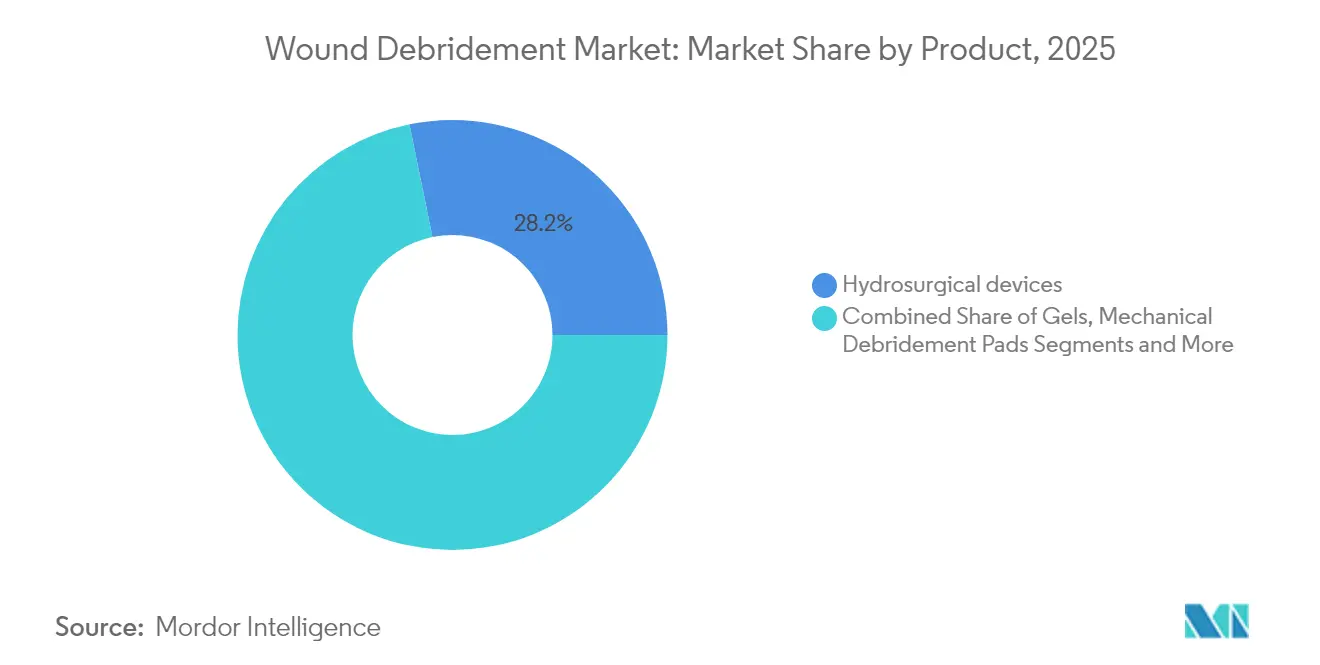

- By product type, hydrosurgical devices led with 28.21% of wound debridement market share in 2025, while ultrasonic devices post the fastest 9.28% CAGR to 2031.

- By method, surgical debridement held 39.05% of the wound debridement market size in 2025; ultrasonic methods are advancing at an 8.44% CAGR through 2031.

- By wound type, surgical and traumatic wounds accounted for 35.93% of the overall market in 2025, yet burns will rise at a 9.31% CAGR.

- By end user, hospitals dominated with 52.34% share in 2025, whereas home-care settings are growing 8.05% each year.

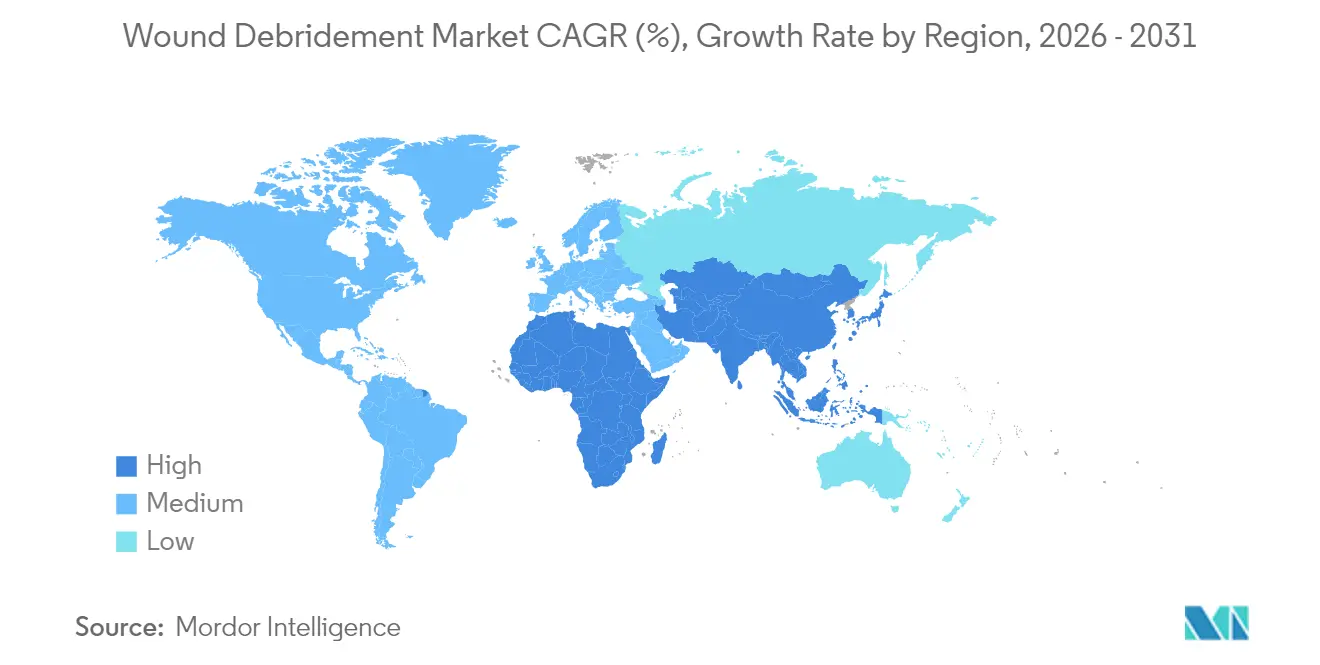

- By geography, North America commanded 37.02% revenue in 2025; Asia-Pacific is forecast to expand at a 6.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Wound Debridement Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence Of Diabetic Foot & Venous Leg Ulcers | +1.2% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Growing Volume Of Complex Surgical Procedures | +0.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rapid Adoption Of Advanced Hydrosurgical & Ultrasonic Systems | +1.5% | North America & Europe, early APAC adoption | Short term (≤ 2 years) |

| Ageing Population With Impaired Wound Healing | +0.9% | Global, acute in developed economies | Long term (≥ 4 years) |

| AI-Enabled Wound-Assessment Platforms Accelerating Debridement Decisions | +0.7% | North America & Europe, pilot programs in APAC | Medium term (2-4 years) |

| Biofilm-Targeting Topical Enzymes Improving Debridement Efficiency | +0.6% | Global, regulatory approval dependent | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising incidence of diabetic foot and venous leg ulcers

Diabetic foot ulcers affect 15–25% of people living with diabetes, and 85% of diabetes-related amputations are preceded by such ulcers. Evidence now shows that early, aggressive debridement reaching beyond wound edges removes biofilm and hyperproliferative tissue and markedly lowers amputation risk. This clinical shift increases demand for enzymatic and ultrasonic platforms that deliver tissue-selective removal without collateral damage, while preventive tools such as pressure-altering insoles further elevate upstream intervention needs.[1]American Heart Association, “Current Status and Principles for the Treatment and Prevention of Diabetic Foot Ulcers,” ahajournals.org

Rapid adoption of advanced hydrosurgical and ultrasonic systems

Saline-jet hydrosurgery, exemplified by the VERSAJET platform, streamlines procedures and preserves healthy tissue. Ultrasonic devices such as SonicOne remove devitalized tissue through low-frequency vibration, are painless, and foster granulation. Hospitals and outpatient centres quickly adopt these modalities as studies report faster closure rates and shorter admissions, accelerating the wound debridement market transition toward non-contact, precision-guided care.

Growing volume of complex surgical procedures

Higher surgical complexity, including necrotizing soft tissue infections that require debridement within 72 hours, fuels demand for precise devices that minimise blood loss and reduce operating time. Integrating debridement with negative-pressure wound therapy leads providers to favour multi-modal platforms. Case series using biodegradable temporising matrices in Asian patients achieved 94.6% healing, highlighting the importance of region-specific solutions.[2]Mei-Ling Wong, “A Bioelectrically Enabled Smart Bandage for Accelerated Wound Healing,” mdpi.com

Ageing population with impaired wound healing

Chronic wounds now affect close to 2% of the global population, heavily weighted toward older adults with diabetes, vascular disease, or malnutrition. Smart bandages delivering electric stimulation and real-time data accelerate closure, while gentler hydrosurgical and enzymatic methods respect fragile skin. These demographic dynamics secure long-run growth for the wound debridement market.[3]Harlan A. Fischer, “Advanced Wound Care Strategies in Patients with Necrotizing Soft Tissue Infections,” Medicina, mdpi.com

Restraints Impact Analysis of Wound Debridement Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Overall Treatment & Device Costs | -0.8% | Global, acute in emerging economies | Short term (≤ 2 years) |

| Shortage Of Certified Wound-Care Specialists In Emerging Economies | -0.6% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Tightening FDA/EMA Scrutiny On Collagenase & Enzymatic Agents | -0.4% | North America & Europe | Medium term (2-4 years) |

| Sustainability Push Against Single-Use NPWT Canisters & Disposables | -0.3% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High overall treatment and device costs

Average diabetic foot ulcer episodes cost EUR 4,888 per patient, with most spending tied to lengthier inpatient stays rather than devices. Payers therefore insist on robust evidence showing that premium platforms shorten time to closure or reduce complications before reimbursing higher prices. Providers respond by focusing on total cost-of-care analyses instead of front-end device costs.

Shortage of certified wound-care specialists

Specialist nurses and physicians remain concentrated in high-income markets, while chronic wounds rise fastest in emerging regions. Staffing gaps constrain adoption of advanced protocols and prompt interest in AI-enabled decision support and tele-mentoring that extend expertise across distance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Wound Debridement Market Segment Analysis

By Product:

Hydrosurgical devices maintain lead yet ultrasonic units gain groundHydrosurgical systems secured 28.21% of wound debridement market share in 2025 through their ability to excise devitalised tissue with minimal collateral trauma. Their popularity in operating rooms stems from faster set-up, better visibility, and lower infection risk. Despite this lead, ultrasonic devices are expanding at a 9.28% CAGR, aided by non-contact operation that eases patient discomfort and lowers cross-contamination. Enzymatic gels retain a place in chronic ulcer care, whereas mechanical pads find limited use when only superficial slough must be removed.

Ultrasonic technology builds momentum because adjustable amplitude lets clinicians fine-tune depth of action, which is invaluable for irregular burn beds and fragile diabetic ulcers. These advantages, together with shrinking capital costs, underpin ultrasonic disruption of the wound debridement market. By contrast, biologic methods such as maggot therapy, though clinically effective, confront cultural resistance. Regulatory scrutiny of antimicrobial dressings also pushes innovators toward mechanical options that sidestep resistance issues.

By Method:

Surgical dominance meets ultrasonic innovationSurgical debridement represented 39.05% of the wound debridement market size in 2025 on account of its role in emergency departments and trauma theatres. Its capacity to remove necrosis and biofilm in one session cements its status among vascular and orthopaedic surgeons. Enzymatic debridement follows, offering a chemical route for patients who cannot tolerate surgery.

Ultrasonic approaches, growing 8.44% yearly, combine precision with patient comfort and can be repeated in outpatient clinics, therefore lowering bed occupancy. Mechanical and autolytic routes continue to serve frail patients, while biologic strategies await clearer regulatory pathways after the FDA transferred oversight of medicinal maggots to CBER in late 2024.

By Wound Type:

Burns emerge as fastest climberSurgical and traumatic wounds contributed 35.93% of revenue in 2025, driven by high procedure volumes and reimbursement frameworks that reward rapid tissue clearance. Chronic ulcers, including diabetic, pressure, and venous leg ulcers, consume considerable resources because they demand weekly debridement plus infection control.

Burns create the sharpest growth at a 9.31% CAGR as early debridement within 72 hours improves graft take rates. Advanced antimicrobial dressings using silver, zinc, and bioactive compounds and the pipeline of cell-based therapies increase procedural complexity, calling for devices that adapt to evolving burn protocols.

By End User:

Home care sparks treatment decentralisationHospitals owned 52.34% of revenue in 2025 owing to operating-room infrastructure and multidisciplinary teams. Ambulatory centres occupy a middle ground, handling less complex wounds while delivering cost savings.

The shift to community settings is clear: home-care volumes are rising 8.05% each year. Remote monitoring bandages now transmit pH, temperature, and exudate data, allowing clinicians to direct care plans virtually. Compact ultrasonic handpieces and pre-filled enzymatic kits are under development to serve domiciliary markets, thereby growing the wound debridement market in non-hospital channels.

Geography Analysis

North America Wound Debridement Market

North America generated 37.02% of 2025 sales, anchored by high diabetes prevalence, generous reimbursement, and early uptake of AI-enabled assessment software. Smith+Nephew reported 3.8% underlying growth in its Advanced Wound Management franchise for Q1 2025, underscoring sustained regional demand. Regulations remain supportive, yet recent FDA warning letters emphasise manufacturing quality and favour well-capitalised firms.

Europe Wound Debridement Market

Europe remains an innovation hub, with start-ups progressing enzymatic and photonic devices and regulators tightening evidence requirements for antimicrobial agents. Environmental legislation that discourages single-use plastic canisters prompts suppliers to redesign negative-pressure wound therapy consumables.

APAC Wound Debridement Market

Asia-Pacific is the growth engine, forecast to deliver a 6.86% CAGR through 2031. Ageing populations, rising surgical volumes, and government investment in tertiary hospitals underpin expansion. ConvaTec has noted regulatory delays in China, yet local trials of biodegradable temporising matrices yielding 94.6% healing rates spotlight domestic appetite for advanced therapy. South-East Asian and South Asian nations invest in tele-mentoring networks to compensate for limited specialist density, a move that stimulates demand for AI-guided tools.

LATAM and MEA Wound Debridement Market

Latin America and the Middle East & Africa show slower uptake because of budget limits and workforce shortages, though incidence of chronic wounds is climbing. Multilateral aid programmes that sponsor diabetic foot clinics are expected to open new pockets of demand beyond 2027.

Competitive Landscape

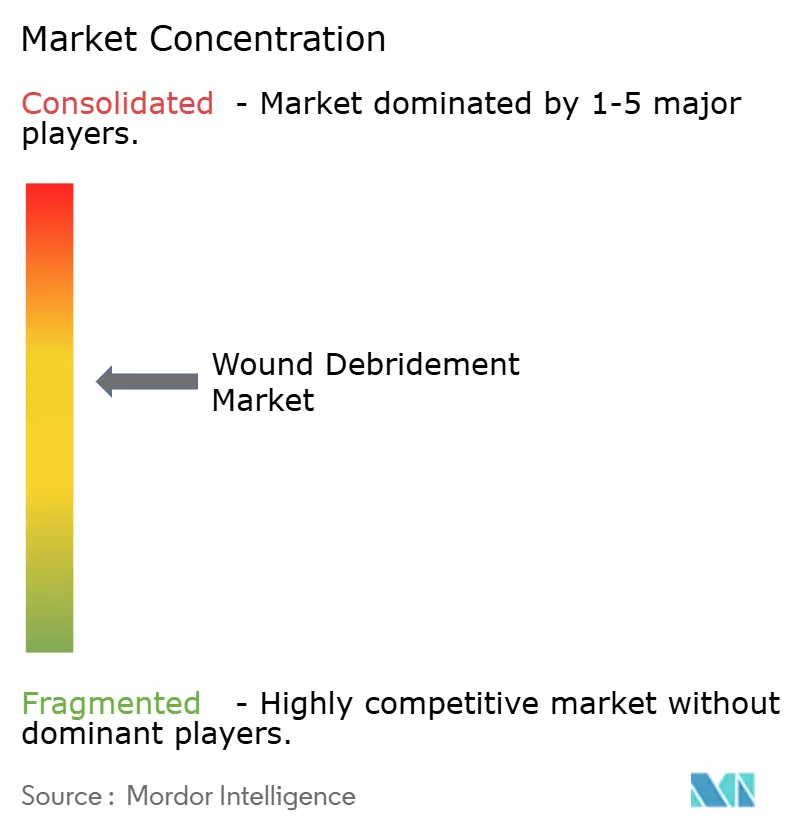

The wound debridement market remains moderately fragmented. Smith+Nephew integrates hydrosurgery, robotics, and negative-pressure systems, delivering 12.2% underlying Advanced Wound Management growth in Q4 2024. ConvaTec recorded 6.7% organic expansion in the same period, buoyed by Aquacel Ag+ and InnovaMatrix. Mölnlycke and 3M leverage broad wound portfolios to retain hospital contracts, while Zimmer Biomet explores intra-operative debridement add-ons to orthopaedic toolkits.

Disruptors target niche gaps. SolasCure gained FDA Fast Track status for Aurase Wound Gel in June 2025, positioning enzymatic therapy for calciphylaxis ulcers. SANUWAVE promotes MIST Therapy®, a portable ultrasonic system suited to outpatient and home settings. Biologic-based players anticipate faster approvals after the FDA shifted oversight of medicinal maggots to CBER, potentially lowering regulatory barriers.

Competition increasingly centres on biofilm eradication and sustainability. Firms test biodegradable dressings and recyclable canisters to satisfy Europe’s single-use plastics rules. AI-powered image analysis that quantifies slough and granulation in seconds also differentiates offerings, allowing clinical teams to document progress objectively.

Wound Debridement Industry Leaders

B. Braun SE

Smith+Nephew

PAUL HARTMANN AG

ConvaTec Group PLC

Mölnlycke Health Care AB

- *Disclaimer: Major Players sorted in no particular order

Wound Debridement Market Companies Covered in this Report

- Smiths Group

- Convatec

- Molnlycke Health Care

- B. Braun

- Hartmann Group

- Bioventus (Misonix)

- Lohmann & Rauscher

- Solventum

- Coloplast

- DeRoyal Industries

- Arobella Medical

- Histologics LLC

- Medaxis AG

- Söring GmbH

- Zimmer Biomet (Pulsavac)

- RLS Global AB

- PulseCare Medical

- Integra LifeSciences

- Medtronic

- Stryker

Recent Industry Developments in Wound Debridement Market

- June 2025: SolasCure received FDA Fast Track Designation for Aurase Wound Gel to treat calciphylaxis ulcers, broadening its potential indications.

- March 2025: FDA cleared the SkinDisc Wound System that prepares autologous platelet-rich plasma for topical management of chronic ulcers

- March 2025: SolasCure dosed the first patient in the Phase II CLEANVLU2 study of Aurase Wound Gel at higher Tarumase strength for venous leg ulcers.

Wound Debridement Market Report Scope and Research Methodology

Market Definition and Coverage

Our study counts global revenue from products that actively remove devitalized tissue, including gels, ointments, creams, hydrosurgical and ultrasonic consoles, single-use mechanical pads, biologic larvae kits, and sharp instruments, supplied to hospitals, ambulatory centers, and clinically supervised home care across seventeen tracked nations.

Scope exclusion: Moisture dressings and negative-pressure pumps used mainly for closure sit outside this review.

Segments Covered in This Report

- By Product

- Gels

- Ointments & Creams

- Surgical Debridement Devices

- Hydrosurgical Devices

- Ultrasound-Assisted Debridement Devices

- Mechanical Debridement Pads

- Biologic Debridement (Maggot Therapy)

- Other Products

- By Method

- Surgical

- Enzymatic

- Mechanical

- Autolytic

- Biologic

- Ultrasonic

- By Wound Type

- Chronic Ulcers

- Diabetic Foot Ulcers

- Pressure Ulcers

- Venous Leg Ulcers

- Surgical & Traumatic Wounds

- Burns

- Chronic Ulcers

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Home-Care Settings

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed wound-care nurses, vascular surgeons, procurement heads, and device managers across North America, Europe, Asia-Pacific, and the Gulf. These conversations clarified therapy mix shifts, ultrasonic uptake, and live ASP drift that public filings often miss.

Desk Research

We began with open datasets from the International Diabetes Federation, WHO Global Burn Registry, OECD hospital-procedure files, UN age projections, and Comtrade codes, then verified guidance issued by the European Wound Management Association. Public company 10-Ks, investor calls, and tariff schedules from CMS and the NHS revealed price and volume clues. Paid intelligence drawn through D&B Hoovers and Dow Jones Factiva refined revenue bands. The sources named are illustrative; many others supported data capture, validation, and clarification.

A second pass reconciled reported unit shipments with import-export tallies and checked prevalence figures against peer-reviewed journals, letting us flag any outliers before model build.

Market-Sizing & Forecasting

We employ a top-down prevalence-to-treated-pool model, converting diabetic foot, pressure-ulcer, burn, and surgical case counts into annual debridement events, then multiplying by blended ASPs. Select supplier roll-ups and sampled clinic invoices bottom-up validate totals. Core variables, including diabetic population growth, elective surgeries, hydrosurgical penetration, reimbursement moves, ASP deflation, and home-care share, feed a multivariate regression with ARIMA smoothing to 2030.

Data Validation & Update Cycle

Outputs face variance checks against manufacturer revenue, ratio tests versus procedure norms, and senior peer review before sign-off. Reports refresh each year, with interim updates when major regulatory or pricing events occur.

How Mordor Intelligence's Wound Debridement Market Size Compares to Other Published Estimates

Published estimates often diverge because publishers choose distinct product baskets, price curves, and refresh intervals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.25 B | Mordor Intelligence | - |

| USD 5.31 B | Global Consultancy A | Excludes biologics plus home-care spend |

| USD 5.35 B | Trade Journal B | Frozen five-year ASPs, no FX harmonization |

| USD 1.16 B | Industry Association C | Counts only capital ultrasonic systems |

When scope aligns, gaps stay narrow; when core inputs diverge, numbers swing widely. By aligning scope, sampling prices quarterly, and normalizing every currency at IMF rates, we at Mordor Intelligence give decision-makers a balanced, transparent baseline they can depend on.

Key Questions Answered in the Report

What is the current size of the wound debridement market?

The market is valued at USD 5.54 billion in 2026 and is projected to reach USD 7.29 billion by 2031.

Which segment is growing fastest within the wound debridement market?

Ultrasonic devices are expanding at a 9.28% CAGR through 2031 owing to non-contact, tissue-selective action.

Why is Asia-Pacific seen as the key growth region?

Healthcare infrastructure upgrades, ageing demographics, and increasing surgery volumes push Asia-Pacific to a 6.86% CAGR, ahead of all other regions.

What are the main restraints to market expansion?

High treatment costs and a shortage of certified wound-care specialists, especially in emerging economies, slow wider adoption of advanced solutions.

How are sustainability concerns shaping product development?

Manufacturers are shifting toward biodegradable dressings and recyclable NPWT components to meet stricter environmental regulations in Europe and North America.

Page last updated on: