Embolic Protection Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

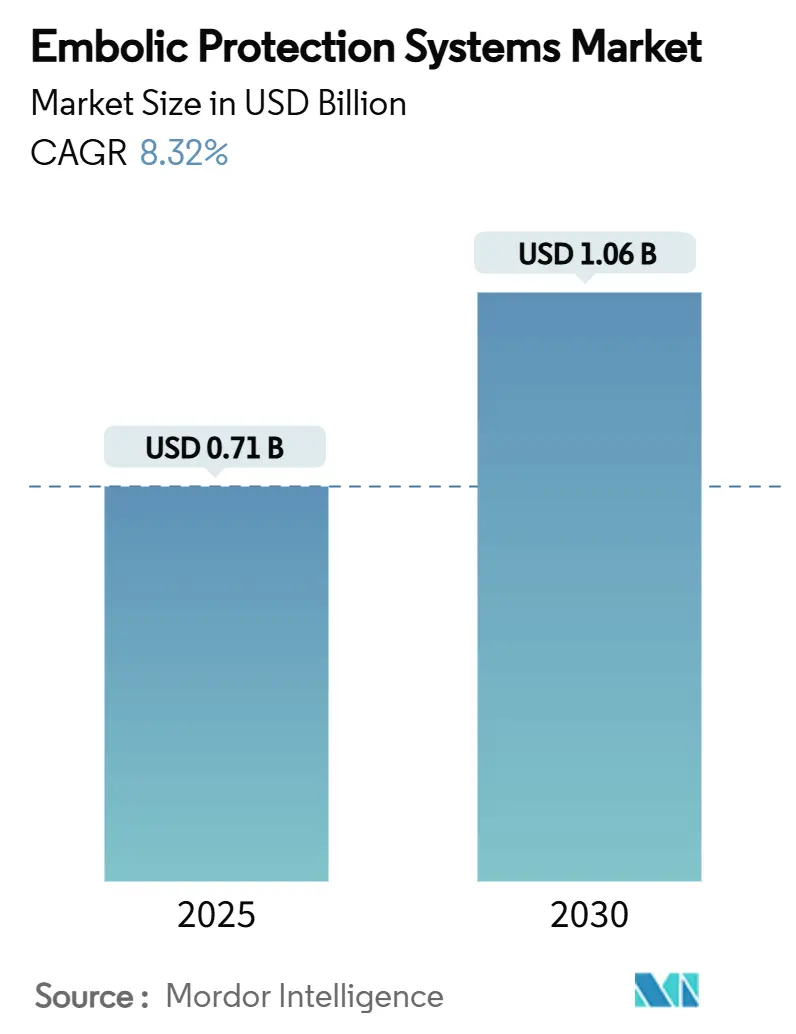

| Market Size (2025) | USD 0.71 Billion |

| Market Size (2030) | USD 1.06 Billion |

| Growth Rate (2025 - 2030) | 8.32% CAGR |

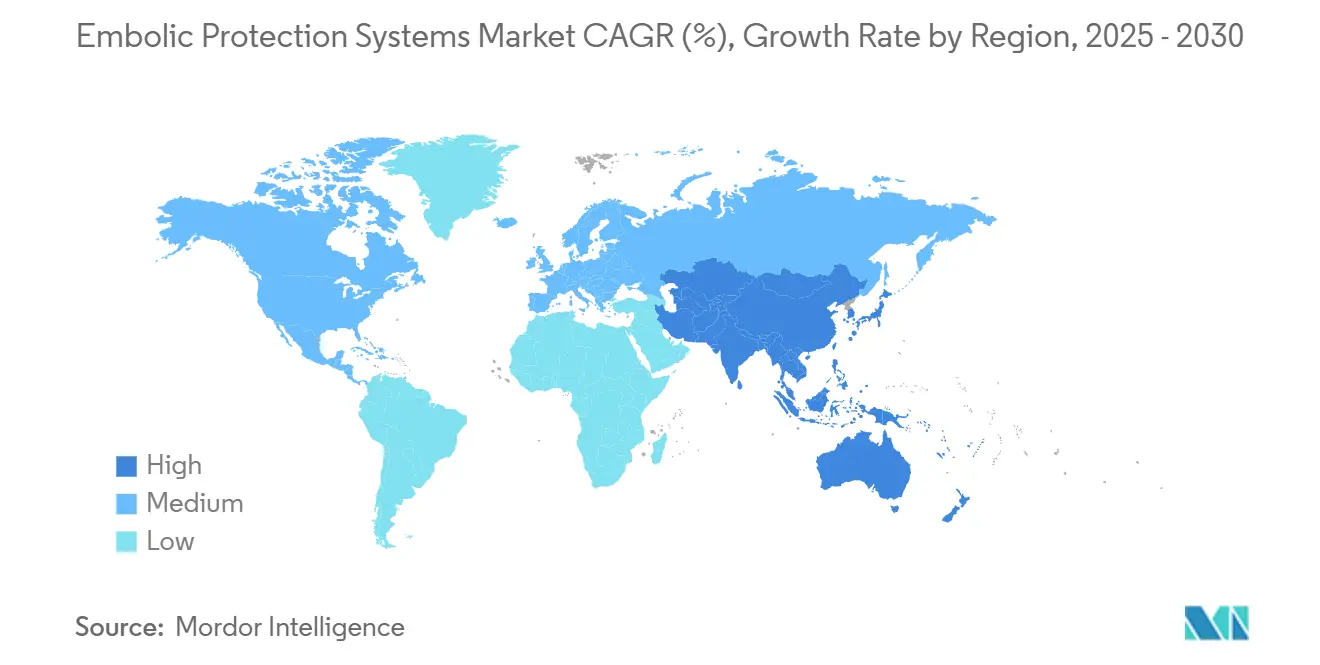

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embolic Protection Systems Market Analysis by Mordor Intelligence

The embolic protection systems market size reached USD 711.16 million in 2025 and is projected to hit USD 1,060.50 million by 2030, advancing at an 8.32% CAGR during the forecast period. The growth trajectory reflects the steady rise in cardiovascular and neurovascular procedures, broadening transcatheter indications, and material science advances that improve device performance. Heightened demand comes from transcatheter aortic valve replacement (TAVR) and large-bore peripheral interventions, where embolic debris management is now viewed as essential rather than optional. Consolidation among leading vendors and rapid regulatory approvals for next-generation integrated systems also accelerate global penetration, especially in high-volume centers across North America and Western Europe. Meanwhile, Asia-Pacific stands out as the fastest-growing region on the back of rising procedural volumes, supportive government initiatives, and local manufacturing investments.

Key Report Takeaways

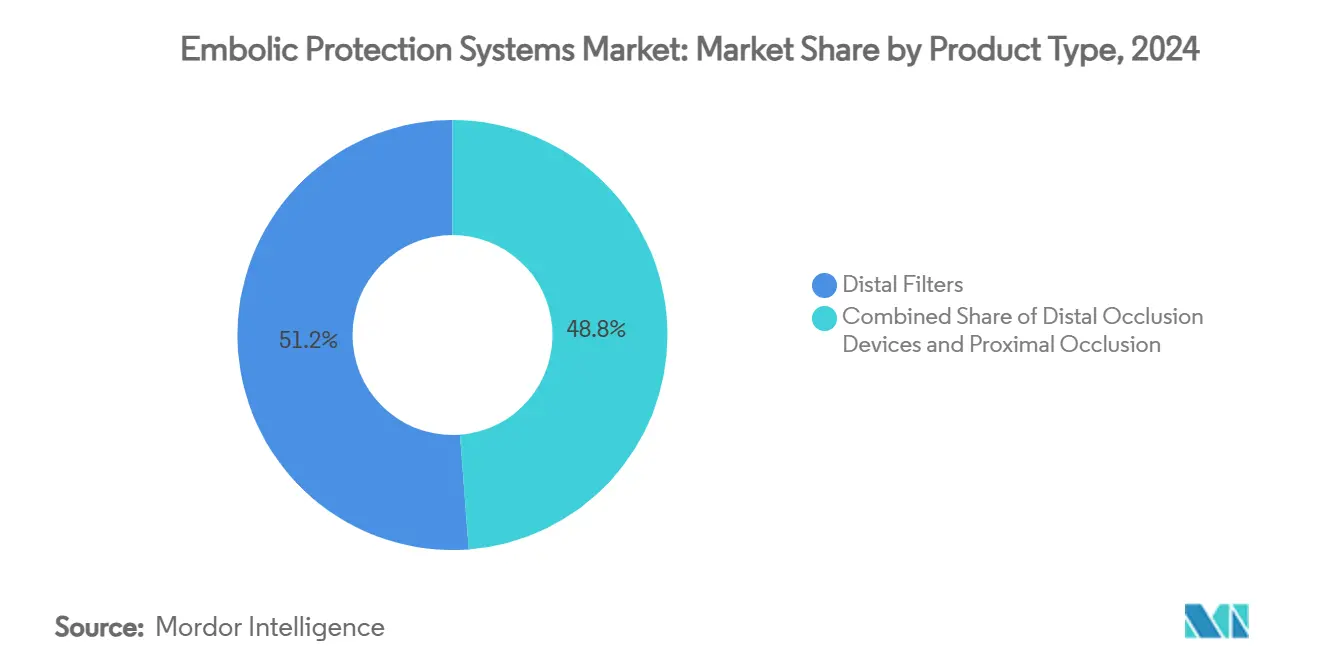

- By product technology, distal filters captured 51.25% of embolic protection systems market share in 2024; proximal occlusion/flow-reversal systems are forecast to expand at an 8.81% CAGR to 2030.

- By material, nitinol commanded 61.34% share of the embolic protection systems market size in 2024, while polyurethane is projected to register a 9.12% CAGR through 2030.

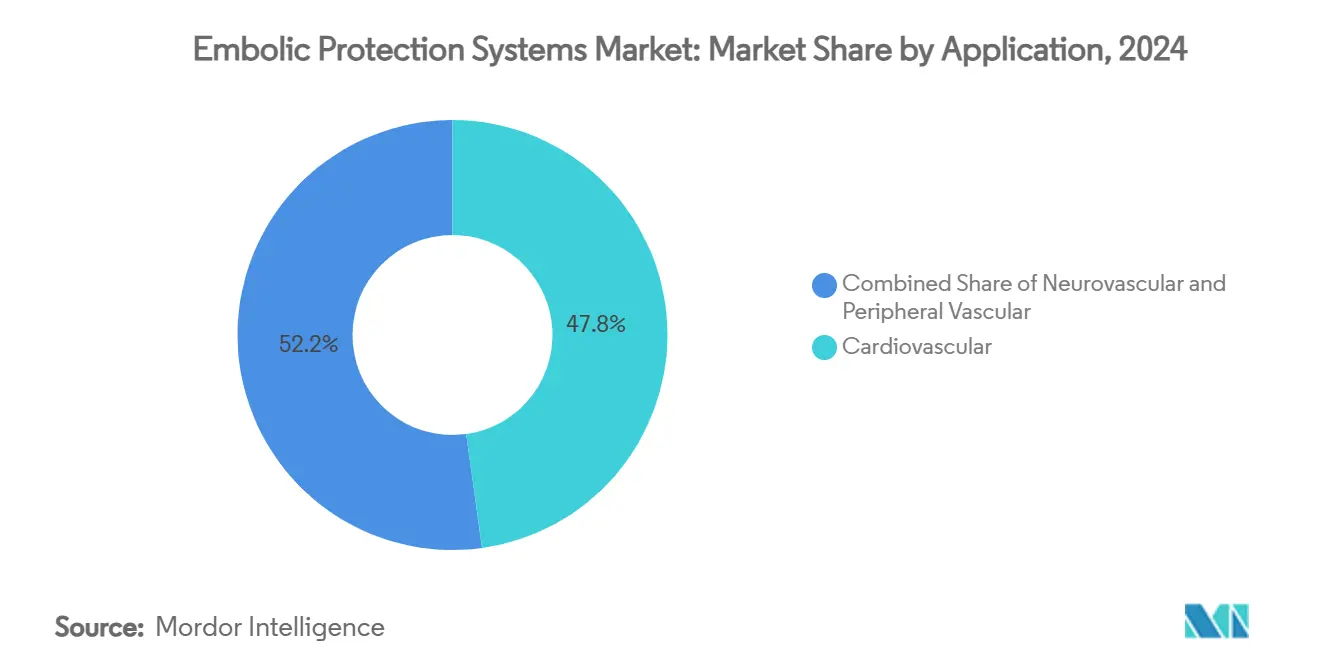

- By application, cardiovascular interventions accounted for 47.81% of the embolic protection systems market size in 2024, and neurovascular procedures are advancing at a 9.38% CAGR to 2030.

- By end user, hospitals led with 54.85% revenue share in 2024; ambulatory surgical centers are set to grow at a 9.61% CAGR during the forecast window.

- North America dominated with 42.87% of embolic protection systems market share in 2024; Asia-Pacific exhibits the fastest regional CAGR of 9.92% through 2030.

Global Embolic Protection Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in prevalence of cardiovascular & neurovascular diseases | +1.8% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Increasing demand for minimally invasive transcatheter procedures | +2.1% | Global, led by North America, expanding in APAC | Medium term (2-4 years) |

| Growing adoption of TAVR-linked cerebral protection | +1.5% | North America & EU core, emerging in APAC | Medium term (2-4 years) |

| Surge in large-bore peripheral interventions | +1.2% | North America & Europe, with APAC uptick | Short term (≤ 2 years) |

| Reimbursement expansions for cerebral EPDs | +0.9% | North America & Europe | Short term (≤ 2 years) |

| AI-driven real-time embolic detection & device optimization | +0.7% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Prevalence of Cardiovascular & Neurovascular Diseases

Ischemic stroke impacts nearly 900,000 U.S. residents yearly, fueling mechanical thrombectomy growth and, in turn, sustained demand for embolic protection devices [1]AngioDynamics, “AlphaVac F1885 System Clearance,” investors.angiodynamics.com. Aging populations increase procedural complexity, making debris capture vital for favorable outcomes. Real-world registry analyses indicate that cerebral protection lowers major stroke from 1.5% to 1.2% during TAVR, supporting wider adoption [2]American Heart Association, “Outcomes and Predictors of Stroke After TAVR,” ahajournals.org. Middle meningeal artery embolization volumes rose from 4,014 in 2019 to 20,836 in 2023 and could reach 79,483 by 2029, illustrating the multiplier effect on device demand. Hospitals and specialty centers consequently invest in newer filter and flow-reversal systems to address the higher disease burden, keeping the embolic protection systems market on a firm uptrend.

Increasing Demand for Minimally Invasive Transcatheter Procedures

TAVR procedures expanded to include asymptomatic severe aortic stenosis after FDA approval in 2025, widening the eligible cohort. Outpatient percutaneous coronary interventions remain a small but fast-growing slice, with safety profiles equivalent to inpatient care, signaling fresh opportunities for portable embolic protection solutions Cerebral angiography’s shift to outpatient endovascular centers mirrors earlier transitions in interventional radiology, heightening the need for quick-deploy protection systems capable of delivering hospital-grade safety in ambulatory settings.

Growing Adoption of TAVR-Linked Cerebral Protection

The PROTECT-TAVI trial with 7,635 patients showed no overall stroke reduction but did note fewer major strokes, prompting selective use in high-risk subgroups. Large-scale U.S. registries associate cerebral protection with lower mortality (0.7% vs 1.3%) and stroke (1.2% vs 1.5%), validating targeted deployment. Dedicated reimbursement codes (CPT +33370, HCPCS C1889) removed economic barriers, while next-generation systems such as TriGUARD 3 continue to improve filter coverage and procedural ease.

Surge in Large-Bore Peripheral Interventions

FDA-cleared AlphaVac F1885 allows pulmonary embolism thrombectomy through an 18 Fr system and is now CE-marked in Europe. Mechanical approaches from FlowTriever and ClotTriever have broadened venous-thromboembolism treatment and require robust debris capture to prevent distal embolization. Large-bore access management has therefore become integral to comprehensive embolic protection protocols.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent global regulatory evidence requirements | -1.4% | Global, most stringent in EU & US | Long term (≥ 4 years) |

| Limited clinical proof of stroke-reduction benefit | -0.8% | Global, impacting cost-sensitive markets | Medium term (2-4 years) |

| Cost constraints & shortage of trained operators | -0.6% | Global, highest in emerging markets | Medium term (2-4 years) |

| Patent cliffs & litigations slowing next-gen filters | -0.5% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Global Regulatory Evidence Requirements

The FDA’s post-market surveillance rules and the EU Medical Device Regulation demand large randomized trials plus real-world registries, lengthening development cycles for embolic protection devices. The AMPLATZER AMULET clocked a 1,846-day review timeline, exemplifying the hurdle for new entrants [3]Federal Register, “Regulatory Review Period—AMPLATZER AMULET,” federalregister.gov. Additional compliance with special controls under Class II classification adds cost, slowing next-generation filter commercialization.

Limited Clinical Proof of Stroke-Reduction Benefit

A meta-analysis of seven randomized controlled trials involving 4,016 patients found no significant difference in all-cause stroke or mortality between protected and unprotected groups, although filter-based devices hinted at disabling stroke reduction. This evidence gap fuels payer skepticism in low-margin markets, delaying wider uptake in community hospitals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Proximal Systems Gain Momentum

Distal filters retained a 51.25% share of the embolic protection systems market in 2024, supported by established workflows and ease of use. However, proximal occlusion/flow-reversal devices are projected to post an 8.81% CAGR, propelled by clinical data showing lower cerebral event rates during carotid stenting. The embolic protection systems market size for proximal technology could approach USD 480 million by 2030 if current adoption trajectories hold.

Proximal occlusion’s appeal lies in simultaneous capture of macro- and micro-emboli before they enter cerebral circulation. The Neuroguard IEP’s 40-μm filter integrated with self-expanding stent exemplifies the shift toward single-platform protection, recording zero major strokes and stent thrombosis in pivotal trials. Distal occlusion balloons remain pertinent in challenging anatomies but face slower growth as clinicians lean toward flow-reversal approaches for complex lesions.

By Material: Polyurethane Innovation Accelerates

Nitinol dominated 61.34% of the embolic protection systems market share in 2024 owing to shape-memory and fatigue-resistance properties vital for self-expanding frames. Yet polyurethane-based systems are forecast to register a 9.12% CAGR on advancements in shape-memory polymers that permit controlled expansion and improved biocompatibility. The embolic protection systems market size for polyurethane could exceed USD 150 million by 2030 if ongoing trials validate safety in intracranial settings.

Thin-film nitinol research demonstrates 70%-96% particle capture while fostering endothelial alignment, but concerns over nickel ion release spur interest in polymeric alternatives. Confluent Medical’s ultra-polyimide and novel hybrid composites further diversify materials, offering a path toward fully resorbable filter meshes in the long run.

By Application: Neurovascular Procedures Outpace

Cardiovascular interventions held 47.81% of embolic protection systems market size in 2024, anchored by mandatory use during saphenous vein graft PCI and growing penetration in TAVR. Neurovascular applications, however, are expected to climb at a 9.38% CAGR as carotid artery stenting volumes rebound and middle meningeal artery embolization becomes mainstream.

Artificial-intelligence-guided navigation boosts success rates during cerebral aneurysm coiling, reinforcing the value proposition of adjunctive protection. Peripheral vascular uses—such as pulmonary embolism removal—will continue their steady rise, but neurovascular procedures represent the fastest incremental revenue contributor to the embolic protection systems market.

By End User: Ambulatory Centers Gain Share

Hospitals represented 54.85% of revenues in 2024, benefiting from integrated stroke programs and cardiac catheter laboratories. Ambulatory surgical centers are set to capture a larger slice as they clock a 9.61% CAGR through 2030, driven by the migration of elective PCI and carotid stenting into lower-cost outpatient environments.

Specialty cardiac and neuro centers pilot AI-enabled protection platforms, recording 82% precision in carotid stenting device tracking. These early adopters often influence guideline updates, indirectly raising demand among community hospitals seeking to match outcomes.

Geography Analysis

North America accounted for 42.87% of embolic protection systems market share in 2024, supported by high procedure volumes, favorable reimbursement, and rapid rollout of next-generation systems such as the SENTINEL filter. Continuous TAVR indication broadening and major acquisitions—Stryker acquiring Inari Medical for USD 4.9 billion—further consolidate the regional landscape. A vibrant innovation ecosystem, exemplified by Stanford’s milli-spinner thrombectomy device with 90% tough-clot success, accelerates product refresh cycles.

Europe retains a sizeable slice of embolic protection systems market size through coordinated stroke networks and CE-Mark rapid-access pathways. The 33-center PROTECT-TAVI trial offers a clinical evidence backbone that could standardize cerebral protection usage across TAVR-experienced nations. European demand also benefits from the AlphaVac F1885’s CE approval for pulmonary embolism, catering to a region with elevated venous-thromboembolism incidence.

Asia-Pacific is projected to lead growth at 9.92% CAGR as China, Japan, and India scale up structural-heart programs and neurovascular capabilities. Venus Medtech’s P-valve posted 98.2% procedural success, pointing to strong domestic innovation addressing unique anatomical profiles. Government insurance expansions and medical-device localization policies add tailwinds, enabling local manufacturers to compete on price while maintaining performance standards.

Competitive Landscape

Market concentration sits in the middle range, with Boston Scientific, Abbott, and Medtronic anchoring more than half of global revenue. Boston Scientific’s SENTINEL system dictates cerebral protection standards, while Abbott’s Emboshield NAV6 remains entrenched in carotid interventions. Stryker’s USD 4.9 billion Inari Medical purchase and Boston Scientific’s USD 1.26 billion Silk Road Medical acquisition underline renewed focus on embolic protection technologies.

New entrants emphasize integrated or AI-assisted systems. Contego Medical secured FDA approval for its Neuroguard IEP, merging stent, balloon, and filter in one delivery platform. Teleflex’s 2025 buyout of BIOTRONIK’s vascular unit indicates broader diversification toward neuro- and peripheral-embolization solutions.

Intellectual-property disputes—such as Emboline versus AorticLab—reflect crowded patent portfolios, potentially delaying commercialization of niche innovations. Nonetheless, venture-backed start-ups including Jupiter Endovascular (USD 21 million funding) aim to penetrate pulmonary-embolism niches with novel aspiration systems.

Embolic Protection Systems Industry Leaders

Boston Scientific Corporation

Medtronic Plc

Abbott Laboratories

Cardinal Health

Hellman & Friedman LLC (Cordis)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Arsenal Medical initiated the EMBO-02 study evaluating NeoCast for chronic subdural hematoma treatment via middle meningeal artery embolization.

- October 2024: Transverse Medical appointed Professor Ian T. Meredith, MD, to its board to advance POINT-GUARD cerebral embolic protection.

- April 2024: Emboline acquired SWAT Medical’s intellectual-property portfolio to enhance TAVR stroke-mitigation technologies.

- March 2024: CERENOVUS released the TRUFILL n-BCA Liquid Embolic System Procedural Set, streamlining hemorrhagic-stroke workflows.

Global Embolic Protection Systems Market Report Scope

As per the scope of the report, embolic protection devices (EPDs) prevent or reduce plaque debris from reaching the distal bed and thereby have the potential to reduce adverse clinical events. The Embolic Protection Systems Market is Segmented by Product Technology Type (Distal Occlusion Devices, Distal Filters, Proximal Occlusion Devices), Material (Nitinol, Polyurethane), Application (Neurovascular Diseases, Cardiovascular diseases, Others), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Distal Occlusion Devices |

| Distal Filters |

| Proximal Occlusion / Flow-Reversal Devices |

| Nitinol |

| Polyurethane |

| Others (e.g., PET, Stainless Steel) |

| Cardiovascular | Coronary Interventions (SVG, native) |

| Structural Heart (TAVR, Mitral, LAAC) | |

| Neurovascular | Carotid Artery Stenting |

| Intracranial Interventions | |

| Peripheral Vascular | Lower-Limb PAD |

| Renal & Visceral Artery Interventions |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Cardiac & Neuro Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Distal Occlusion Devices | |

| Distal Filters | ||

| Proximal Occlusion / Flow-Reversal Devices | ||

| By Material | Nitinol | |

| Polyurethane | ||

| Others (e.g., PET, Stainless Steel) | ||

| By Application | Cardiovascular | Coronary Interventions (SVG, native) |

| Structural Heart (TAVR, Mitral, LAAC) | ||

| Neurovascular | Carotid Artery Stenting | |

| Intracranial Interventions | ||

| Peripheral Vascular | Lower-Limb PAD | |

| Renal & Visceral Artery Interventions | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Cardiac & Neuro Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Embolic Protection Systems Market size?

It stood at USD 711.16 million in 2025.

Who are the key players in Embolic Protection Systems Market?

Boston Scientific Corporation, Medtronic Plc, Abbott Laboratories, Cardinal Health and Hellman & Friedman LLC (Cordis) are the major companies operating in the Embolic Protection Systems Market.

Which is the fastest growing region in Embolic Protection Systems Market?

Asia-Pacific, forecast at a 9.92% CAGR through 2030, due to expanding structural-heart and neurovascular programs.

Why are ambulatory surgical centers gaining traction for embolic protection procedures?

The migration of elective PCI and carotid stenting to outpatient settings cuts costs while maintaining safety, spurring device demand.

Page last updated on: