Medical Foam Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 35.18 Billion |

| Market Size (2031) | USD 49.51 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Foam Market Analysis by Mordor Intelligence

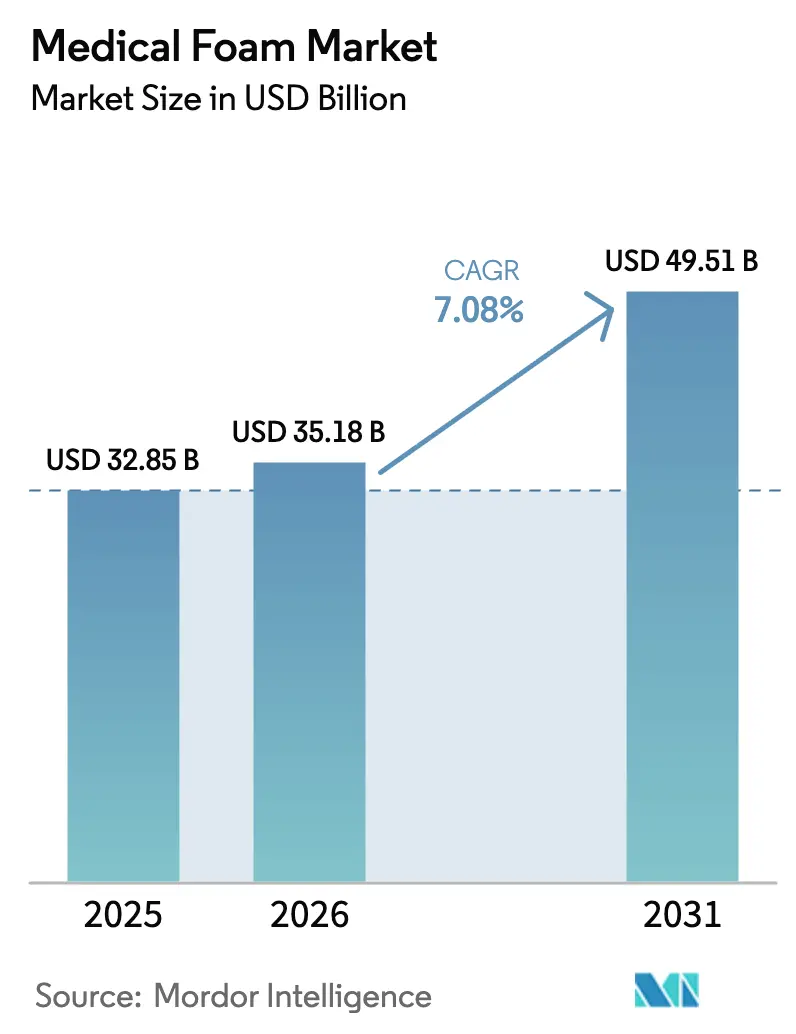

The Medical Foam Market size was valued at USD 32.85 billion in 2025 and estimated to grow from USD 35.18 billion in 2026 to reach USD 49.51 billion by 2031, at a CAGR of 7.08% during the forecast period (2026-2031).

A resilient demand pattern underpins this trajectory, led by polyurethane grades that accounted for 59.66% of 2024 revenue, while polyolefin grades are expanding at a 10.12% CAGR on the back of circular-economy initiatives. Demographic aging continues to widen the user base for pressure-relief bedding, advanced wound dressings and cushioning systems that rely on high-performance foams. Flexible formulations dominate day-to-day hospital and long-term-care needs, whereas spray technologies have opened custom-fit opportunities in prosthetics and orthotics. Regulatory incentives for infection control, coupled with temperature-controlled pharmaceutical distribution, keep demand for sterile and insulated packaging foams elevated.

Key Report Takeaways

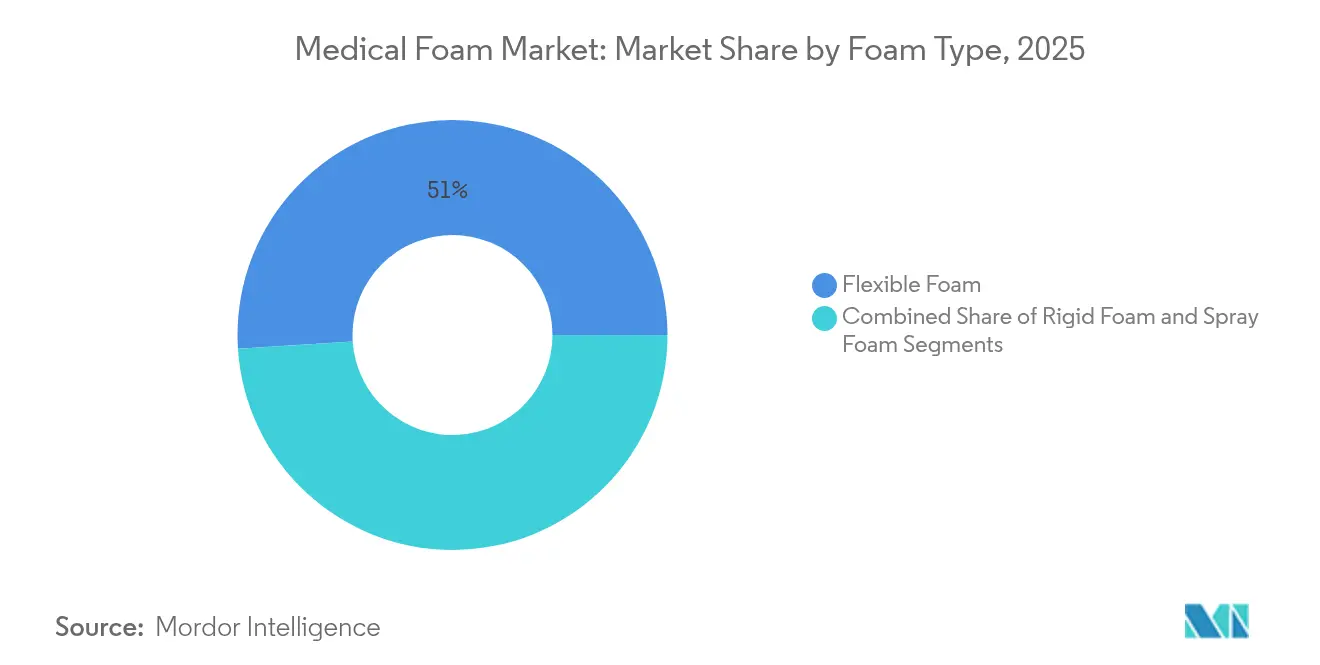

- By foam type, flexible foams led with 51.02% of medical foam market share in 2025 while spray foams are projected to register a 8.62% CAGR to 2031.

- By product, polyurethane captured 59.05% of the medical foam market size in 2025; polyolefin grades are forecast to grow at a 9.71% CAGR between 2026-2031.

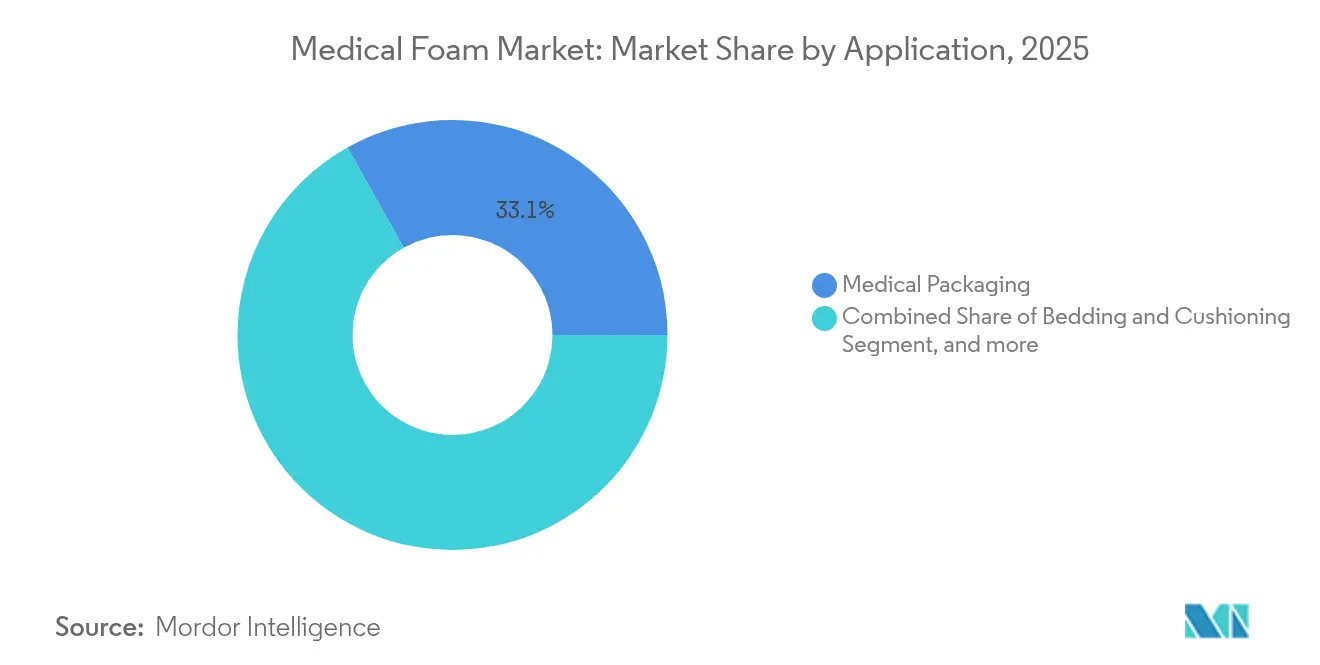

- By application, medical packaging held 33.12% revenue share in 2025 and prosthetics & wound care is advancing at a 11.74% CAGR through 2031.

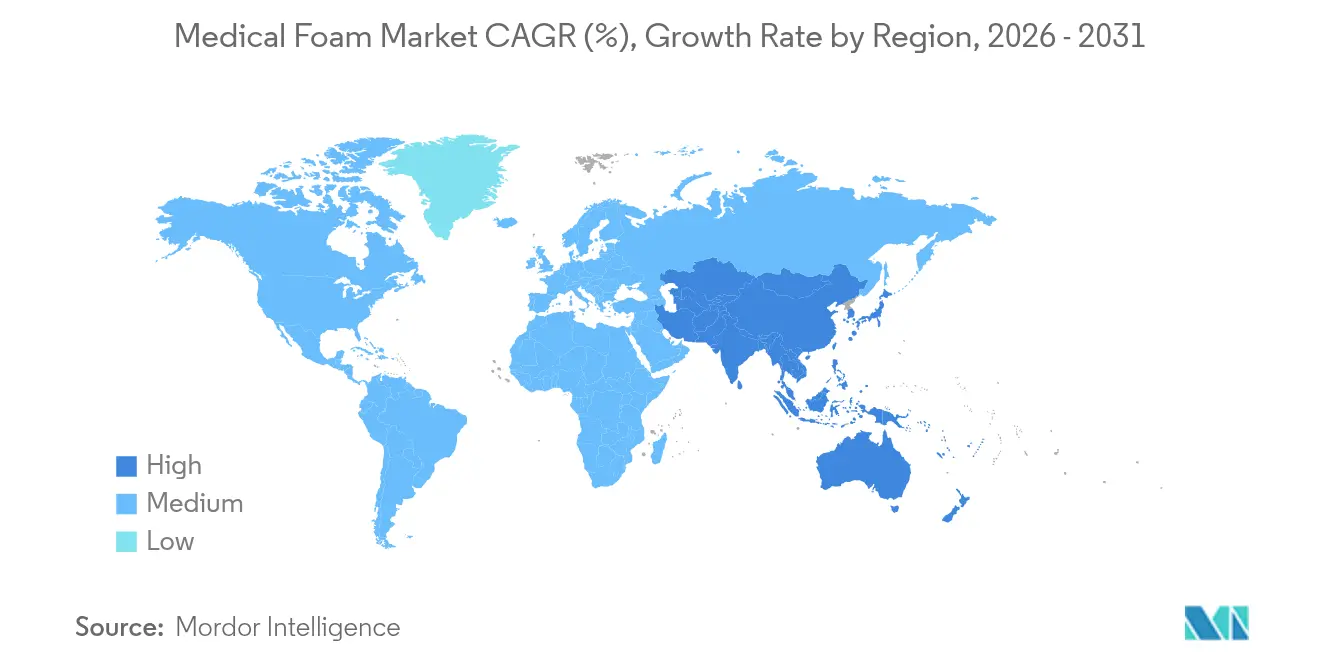

- By geography, North America commanded 33.21% of 2025 revenue, whereas Asia-Pacific is tracking the fastest pace at a 9.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Medical Foam Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Geriatric Population and Chronic Disease Prevalence | +1.8% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapid Adoption of Medical-grade Foams in Sterile Packaging | +1.2% | Global, led by North America & Asia-Pacific | Medium term (2-4 years) |

| Home-Health Boom Driving Demand for Pressure-Relief Bedding | +1.5% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Government Incentives for Advanced Wound-Care Materials | +0.9% | North America & Europe | Short term (≤ 2 years) |

| AI-guided Design of Foam Micro-Cell Structures for Personalised Prosthetics | +0.7% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Pharmaceutical Cold-Chain Mandates for Reusable Cryogenic Foam Shippers | +0.6% | Global, with emphasis on developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population and Chronic Disease Prevalence

Polyurethane dressings cut pressure-ulcer incidence by 35% compared with conventional gauze, lowering hospitalization length and after-care costs. Elderly patients experience pressure-ulcer rates of 10-25%, prompting hospitals and home-health operators to prioritise mattresses that redistribute load effectively. Medicare coverage determinations L38902 and L37166 reimburse advanced foam dressings, reinforcing adoption in long-term-care and outpatient settings.[1]Centers for Medicare & Medicaid Services, “Surgical Dressings Local Coverage Determination L38902,” cms.gov Demographic ageing therefore creates a multi-year volume runway for vendors supplying bed, seat and heel-protection products across care environments.

Rapid Adoption of Medical-grade Foams in Sterile Packaging

ISO 11607-1:2019 prescribes that materials must safeguard terminally sterilised devices until point of use, favouring closed-cell foams with repeatable microbial-barrier performance.[2]ISO, “ISO 11607-1:2019 Packaging for Terminally Sterilized Medical Devices,” iso.org Pharmaceutical cold-chain networks simultaneously need insulation that maintains 2-8 °C profiles. DS Smith’s TailorTemp solution keeps temperature ranges intact for 36 hours while cutting CO₂ emissions 40% versus expanded polystyrene, demonstrating how design can converge performance and sustainability dssmith.com. Demand spans orthopaedic implants to cardiology kits where vibration dampening, puncture resistance and ease of sterilisation matter.

Home-Health Boom Driving Demand for Pressure-Relief Bedding

Cost-containment policies favour shifting recovery to the home, where durable medical equipment must match hospital-grade safety standards. Memory-foam multilayer cores relieve interface pressure while breathable top layers maintain micro-climate comfort. Sensor-embedded foams allow real-time pressure mapping; research shows adaptive prosthetic sockets that auto-adjust via smartphone apps improve daily-wear tolerance.[3]Yun Lee et al., “Adaptive Socket Pressure Systems for Lower-Limb Prosthetics,” Nature Publishing, nature.com Reimbursement frameworks classify such surfaces as medically necessary when risk factors meet threshold scores, sustaining a purchasing cycle among home-health agencies.

Government Incentives for Advanced Wound-Care Materials

Local Coverage Determinations and the Physician Fee Schedule reimburse surgical dressings that demonstrate clinical efficacy, incentivising procurement of modern polyurethane composites. FDA device-review pathways remain clear: EXEM FOAM recently secured regulatory-review-period determination, illustrating predictable market-entry routes. Hospital quality programmes that target lower infection rates now emphasise single-use, non-adherent foam dressings that manage exudate and minimise dressing changes.

Restraints Impact Analysis of Medical Foam Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Isocyanate and Polyol Prices | -1.1% | Global, with highest impact in manufacturing regions | Short term (≤ 2 years) |

| Stringent VOC and Phthalate Emission Regulations | -0.8% | North America & Europe, expanding globally | Medium term (2-4 years) |

| PFAS "forever-chemical" Scrutiny on Fluorinated Foam Additives | -0.6% | North America & Europe, with global regulatory spillover | Medium term (2-4 years) |

| Recycling Bottlenecks for Multi-Material Medical Foams | -0.4% | Global, with emphasis on developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Isocyanate and Polyol Prices

Toluene diisocyanate and methylene diphenyl diisocyanate underpin most polyurethane medical foams and track petroleum price swings, squeezing margins when contract prices lag feedstock inflation. Manufacturers hedge risk through dual-supplier strategies and bio-content initiatives that diversify feedstocks away from fossil-derived inputs.

Stringent VOC and Phthalate Emission Regulations

The Danish Environmental Protection Agency found dimethylformamide and related compounds in consumer foams at levels warranting tighter limits. California’s Consumer Products Regulations impose VOC caps and phase out toxic additives, pushing formulators toward water-blown or CO₂-blown systems. ASTM D8142-17e1 chemical-emission testing adds laboratory costs and lengthens product-development cycles. Collectively, these rules elevate compliance expenditure but promote safer end-use conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Medical Foam Market Segment Analysis

By Foam Type:

Flexible Domination and Spray-Segment MomentumFlexible grades held 51.02% of 2025 revenue, reflecting widespread use in hospital mattresses, OR table pads and wound dressings where contour conformity is paramount. Rising home-health demand anchors stable volumes, while incremental gains stem from the sensor-integration trend in next-generation cushions. Spray technologies accounted for a smaller baseline but are forecast to post a 8.62% CAGR as portable applicators and two-component chemistries allow clinicians to cast in-situ liners and bespoke limb sockets. Growing practitioner familiarity, faster curing and lower volatile-emission variants accelerate their penetration in orthotics laboratories and point-of-care fittings.

Innovation cycles favour spray foams containing blocked isocyanate systems that eliminate occupational hazards and enable room-temperature skin contact. Investment by raw-material suppliers in equipment training broadens the installer base, supporting market entry in ambulatory centres. Meanwhile, rigid foams remain indispensable where dimensional stability outranks flexibility, for instance within imaging-equipment housings or cold-chain pallet shippers. Volume growth, however, parallels overall device-manufacturing output rather than showing breakout expansion.

By Product:

Polyurethane Supremacy with Polyolefin Sustainability UpsidePolyurethane retained 59.05% revenue control in 2025, confirming its role as the staple polymer matrix for both flexible and rigid healthcare foams. Covestro’s Baymedix range illustrates how tailored isocyanate chemistry delivers both breathable backing films and hydrophilic pad cores that speed exudate uptake. High regulatory familiarity, ready sterilisation and fine-tuned hardness grades lock in formulation preference among OEMs.

Polyolefin foams, however, are expanding at a 9.71% CAGR. Their absence of plasticisers, intrinsic recyclability and density-reduction potential align with hospital sustainability charters. Emerging batch-foam processes can now achieve medical-grade cleanliness without post-foaming laminates, paving the way for adoption in sterile packaging inserts and paediatric positioning aids. Polystyrene and PVC retain niche roles where rigidity or clarity is indispensable, though volume prospects remain modest in view of environmental scrutiny.

By Application:

Packaging Scale and Prosthetic AccelerationSterile and temperature-controlled logistics maintained packaging’s 33.12% share in 2025. Stringent barrier, particulate and thermal-shock benchmarks lock in repeat demand for die-cut inserts, vial separators and vaccine shippers. Growth moderates in line with overall pharmaceutical output, yet product iterations that combine recyclability with drop-test resilience keep value realisation intact.

Conversely, prosthetics and wound care lead expansion at a 11.74% CAGR as patient-specific solutions gain traction. Multi-zone foams let prosthetists modulate durometer across sockets, improving residual-limb comfort. In wound management, open-cell polyurethane with ionic-silver impregnation controls bioburden while maintaining moisture vapor transmission, enabling extended wear intervals that lower nursing labor. These outcomes reinforce clinician switch from legacy gauze to advanced foams, feeding a robust replacement cycle.

Geography Analysis

North America Medical Foam Market

North America holds a 33.21% revenue lead on the strength of integrated chemical supply chains, device-manufacturing clusters and reimbursement mechanisms that reward clinical efficacy. Medicare coverage for advanced dressings and therapeutic mattresses underpins predictable purchasing budgets. Multinationals operate manufacturing footprints across the United States and Canada, ensuring rapid fulfilment and regulatory alignment.

Europe Medical Foam Market

Europe mirrors North America in technical standards but surpasses it in environmental policy intensity. The forthcoming Packaging and Packaging Waste Regulation obliges medical-device makers to engineer recyclability into product lifecycles, a shift that expands opportunities for low-density polyolefin solutions. Regional health systems favour cost-effectiveness studies, hence vendors that document reduced dressing-change frequency or shorter rehabilitation turnarounds gain bidding advantages.

APAC, MEA and South America Medical Foam Market

Asia-Pacific is advancing at a 9.28% CAGR, powered by capacity expansions at regional polyurethane plants which shorten lead times and reduce import costs. Public-hospital modernisation programmes in China and India direct investments toward pressure-relief bedding and negative-pressure wound-therapy kits, both foam-intensive categories. Governments simultaneously encourage localised sourcing to build supply-chain resilience, prompting raw-material suppliers to establish propylene-glycol and polyol plants within the region dow.com. Middle East & Africa and South America remain nascent yet promising, with hospital-construction pipelines and regulatory reforms laying groundwork for faster uptake of advanced care materials over the coming decade.

Competitive Landscape

The sector shows moderate fragmentation, with the top five suppliers controlling significant share of global revenue. BASF, Dow and Covestro command backward-integrated feedstock chains that deliver cost stability, while specialised converters such as UFP Technologies capture value in high-complexity assemblies. 3M separated its healthcare assets into Solventum in 2024, allowing a sharper focus on wound-care and sterilisation technologies. DuPont’s 2024 agreement to acquire Donatelle Plastics broadened its contract-manufacturing reach in drug-delivery devices.

Technology leadership hinges on coupling foam science with sensing and digital-design competencies. Academic collaboration has produced grid-based piezoresistive sensors delivering sensitivities of 2.24 kPa⁻¹, enabling mattresses that alert caregivers to shear-force build-up. Covestro and Huntsman advance bio-content pathways that cut greenhouse-gas footprints without compromising tensile or compression set.

Price competition characterises commodity bedding and packaging segments, yet OEM qualification costs and sterility-validation hurdles shelter margins in medical-device components. Suppliers that provide turnkey material, design and clean-room conversion services enjoy stickier customer relationships and higher switching barriers.

Medical Foam Industry Leaders

American Excelsior Company

American Foam Products

Heubach Corporation

UFP Technologies, Inc.

Rogers Corporation

- *Disclaimer: Major Players sorted in no particular order

Medical Foam Market Companies Covered in this Report

- American Excelsior Company

- American Foam Products

- Heubach Corporation

- General Plastics Manufacturing Company Inc.

- UFP Technologies Inc.

- FXI

- Rogers Corporation

- Dow

- Huntsman International LLC

- 3M

- Rempac Foam LLC

- VPC Group

- Recticel NV

- Sekisui Chemical Co. Ltd.

- BASF

- Covestro

- Carpenter Co.

- Armacell International

- Foamtec Medical

- ConvaTec Group plc

- Smiths Group

Recent Industry Developments in Medical Foam Market

- May 2025: UFP Technologies reported record Q1 2025 results with 50.4% increase in medical market sales reaching USD 135.4 million, driven by strong demand in safe patient handling applications and securing exclusive manufacturing rights through 2030 with a major customer.

- March 2025: Researchers developed a bio-based method for producing aromatic diisocyanates from D-galactose, enabling creation of 100% bio-based polyurethane foams without toxic chemicals like phosgene, potentially transforming sustainable medical foam manufacturing.

- January 2025: DS Smith launched TailorTemp recyclable temperature-controlled packaging solution at PharmaPack Europe 2025, offering pharmaceutical industry a sustainable alternative to EPS that maintains cool temperatures for up to 36 hours with 40% CO2 emission reduction.

- May 2024: Consortium developed an evolutionary concept, Foam Recycling Ecosystem Evolution (FREE), for recycling end-of-life polyurethane mattress foams.

Medical Foam Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the medical foam market as revenues generated from polymer-based foams, chiefly polyurethane, polystyrene, polyolefin, and PVC, engineered for bedding and cushioning, sterile packaging, device components, and prosthetics or wound-care applications across hospitals, home-care, and ambulatory settings.

Scope exclusion: Foams sold for general furniture, automotive, or industrial insulation are not considered.

Segments Covered in This Report

- By Foam Type

- Flexible Foam

- Rigid Foam

- Spray Foam

- By Product

- Polyurethane (PU)

- Polystyrene (PS)

- Polyolefin

- Polyvinyl Chloride (PVC)

- Other Products

- By Application

- Bedding & Cushioning

- Medical Packaging

- Medical Devices & Components

- Prosthetics & Wound Care

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Analysts conducted structured interviews with polymer formulators, wound-care clinicians, packaging converters, and supply-chain managers in North America, Europe, and Asia-Pacific. The conversations clarified average selling prices, density standards, and substitution trends, helping us validate model assumptions.

Desk Research

We collated trade volumes, price trajectories, and usage norms from open datasets issued by organizations such as the UN Comtrade, the U.S. International Trade Commission, Eurostat, and the American Chemistry Council. Health-system indicators, including inpatient surgical volumes and chronic-wound prevalence, were gathered from WHO, OECD Health Data, and national ministries. Company 10-Ks, investor decks, key patent families (Questel), and curated news via Dow Jones Factiva rounded out the secondary stack. This list is illustrative; many other public and paid sources supported data checks.

Market-Sizing and Forecasting

A top-down demand pool was built from surgical procedure counts, bed additions, and device production; it was translated into foam demand using penetration ratios and average material weights, then priced via regional ASP curves. Supplier roll-ups and channel checks served as selective bottom-up tests before totals were finalized. Key variables like polyol feedstock prices, hospital admission growth, chronic-ulcer incidence, medical device output, and polyurethane density shifts feed a multivariate regression that drives the 2025-2030 forecast. Gap areas in bottom-up samples were bridged using regional proxy ratios agreed upon with expert respondents.

Data Validation and Update Cycle

Outputs pass a two-step peer review, variance screens versus external trade and capacity signals, and senior analyst sign-off. Mordor refreshes every twelve months and issues mid-cycle updates for material events; before publication, we rerun key formulas so clients receive the latest view.

How Mordor Intelligence's Medical Foam Market Size Compares to Other Published Estimates

Published estimates often differ because firms pick distinct foam families, care settings, or price assumptions. We anchor on healthcare-only demand, current ASPs, and yearly refreshes, which keeps our 2025 value of USD 32.85 billion grounded.

Key gap drivers include whether packaging for non-sterile consumer kits is counted, if recycled content premiums are added, and the cadence at which ASP ladders are re-benchmarked. Our model, updated annually and cross-checked with both capacity reports and clinical demand signals, mitigates these disparities.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 32.85 bn (2025) | Mordor Intelligence | - |

| USD 40.79 bn (2025) | Global Consultancy A | Includes home and beauty foam packaging, uses five-year-old ASP set. |

| USD 30.77 bn (2025) | Industry Association B | Excludes spray foam, applies uniform global price. |

| USD 33.05 bn (2025) | Trade Journal C | Counts veterinary applications, forecasts off constant currency. |

In sum, the disciplined scoping, dual-track validation, and annual refresh cycle practiced by Mordor Intelligence deliver a balanced, transparent baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current value of the medical foam market?

The medical foam market is valued at USD 35.18 billion in 2026 and is projected to reach USD 49.51 billion by 2031.

How are regulations influencing product development?

ISO 11607 and VOC-emission rules require materials to offer sterile barriers and low volatile output, pushing manufacturers toward cleaner chemistries and bio-content formulations.

Which foam type dominates hospital and long-term-care applications?

Flexible polyurethane foams lead with 51.02% revenue share owing to their pressure-redistribution and conformability features.

Why are polyolefin foams gaining traction in healthcare packaging?

Polyolefin grades combine recyclability and low density, aligning with new packaging regulations that prioritise circular-economy performance.

Which application segment is expanding the fastest?

Prosthetics and wound care are growing at a 11.74% CAGR due to personalised-medicine trends and advanced wound-dressing adoption.

Which region is expected to be the fastest-growing market through 2031?

Asia-Pacific is forecast to progress at a 9.28% CAGR, supported by healthcare infrastructure investments and expanded local polyurethane capacity.

Page last updated on: