Market Overview

| Study Period | 2020 - 2031 |

|---|---|

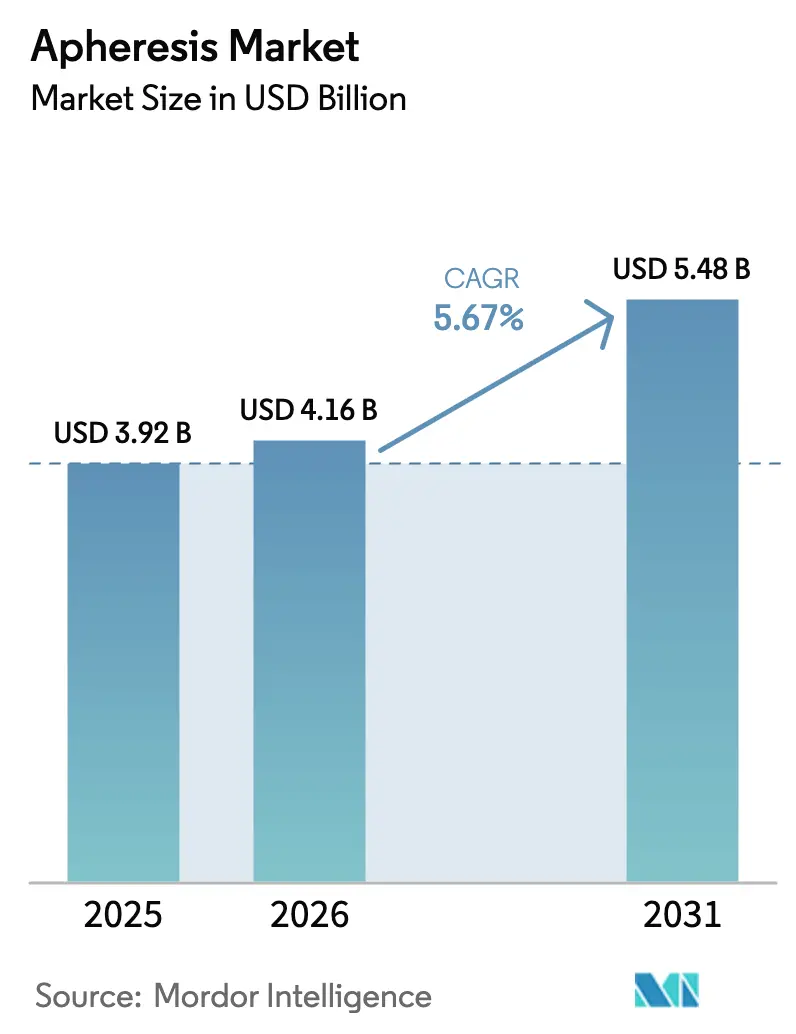

| Market Size (2026) | USD 4.16 Billion |

| Market Size (2031) | USD 5.48 Billion |

| Growth Rate (2026 - 2031) | 5.67% CAGR |

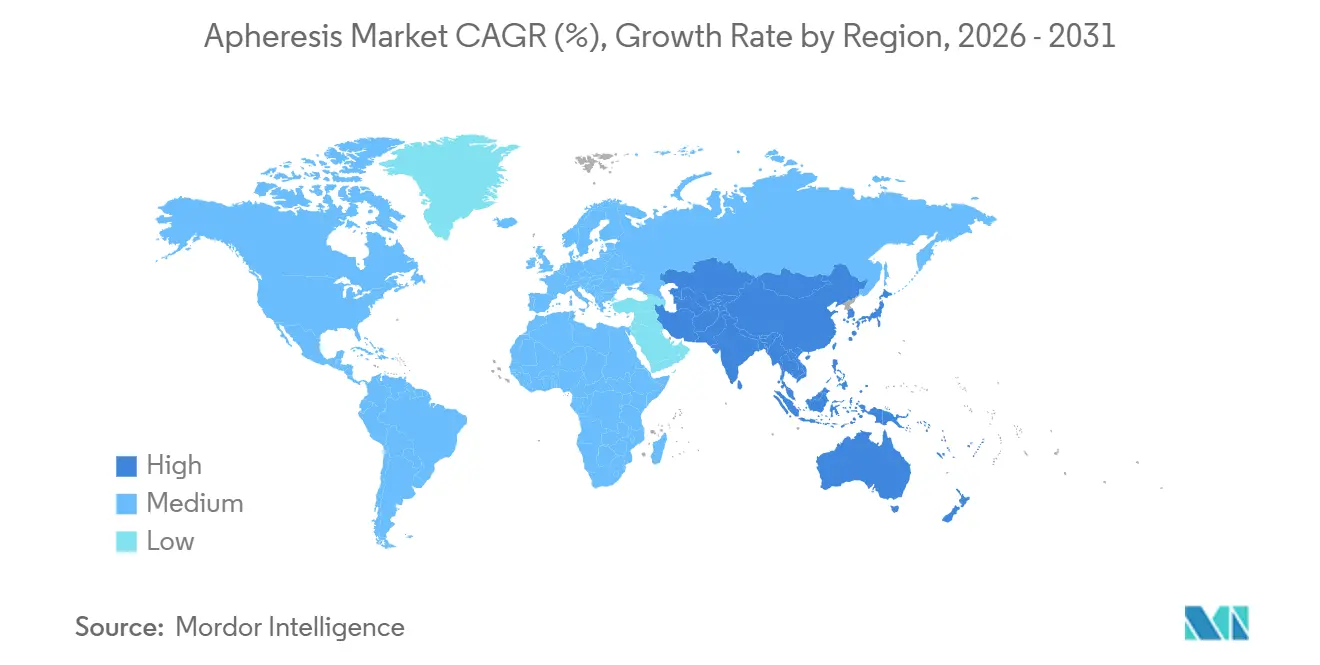

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Apheresis Market Analysis by Mordor Intelligence

The Apheresis Market size is expected to increase from USD 3.92 billion in 2025 to USD 4.16 billion in 2026 and reach USD 5.48 billion by 2031, growing at a CAGR of 5.67% over 2026-2031.

Demand now extends beyond transfusion medicine because every FDA-approved CAR-T product depends on standardized leukapheresis, transforming the procedure into a recurring pharmaceutical input and encouraging hospitals to treat apheresis suites as core oncology infrastructure. Single-use kits that cut water and energy consumption have become procurement priorities despite raising per-procedure costs, while automated membrane systems are shortening run times and improving cell yields. Plasma-derived immunoglobulin shortages in North America and Europe are sustaining high plasmapheresis volumes, and regulatory fast-tracks in China and Japan are accelerating device approvals that support regional self-sufficiency programs. Competitive intensity remains moderate because proprietary disposables lock buyers into established vendor ecosystems even as mid-tier Chinese entrants undercut capital-equipment prices.

Key Report Takeaways

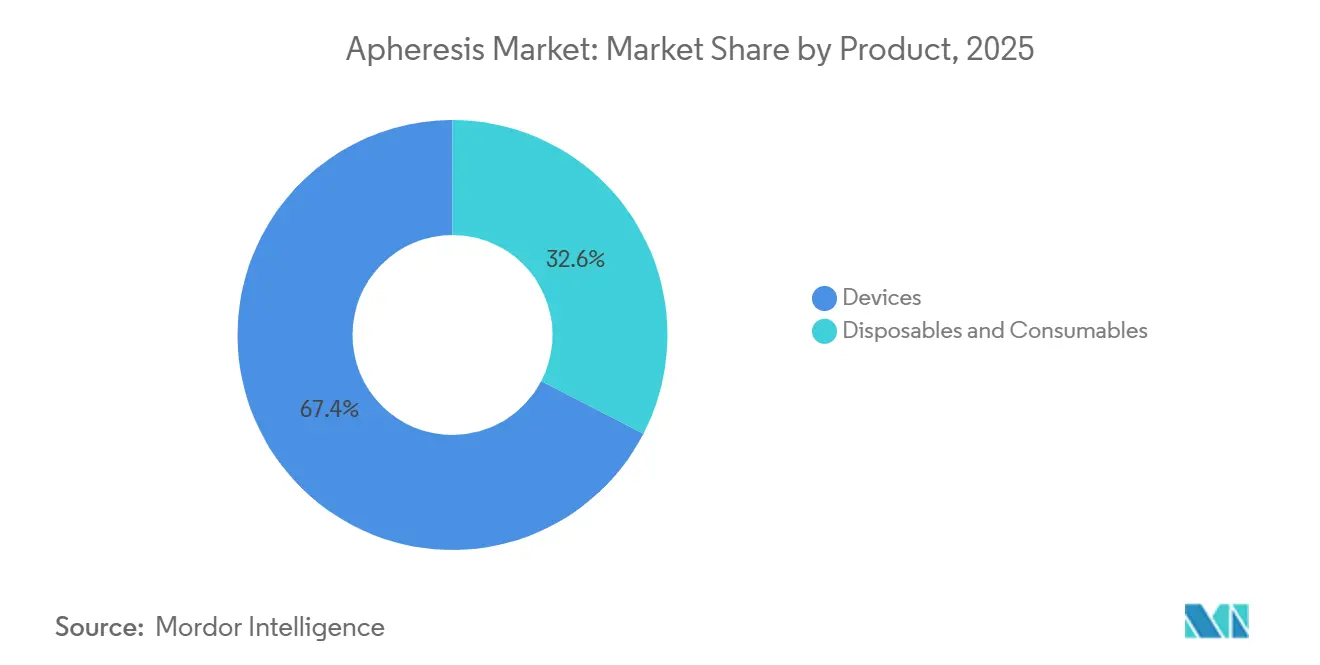

- By product, devices captured 67.43% of the apheresis market share in 2025, while disposables and consumables are forecast to grow at a 7.24% CAGR through 2031.

- By procedure, plasmapheresis accounted for 41.62% of 2025 volume, whereas photopheresis is advancing at an 8.35% CAGR to 2031.

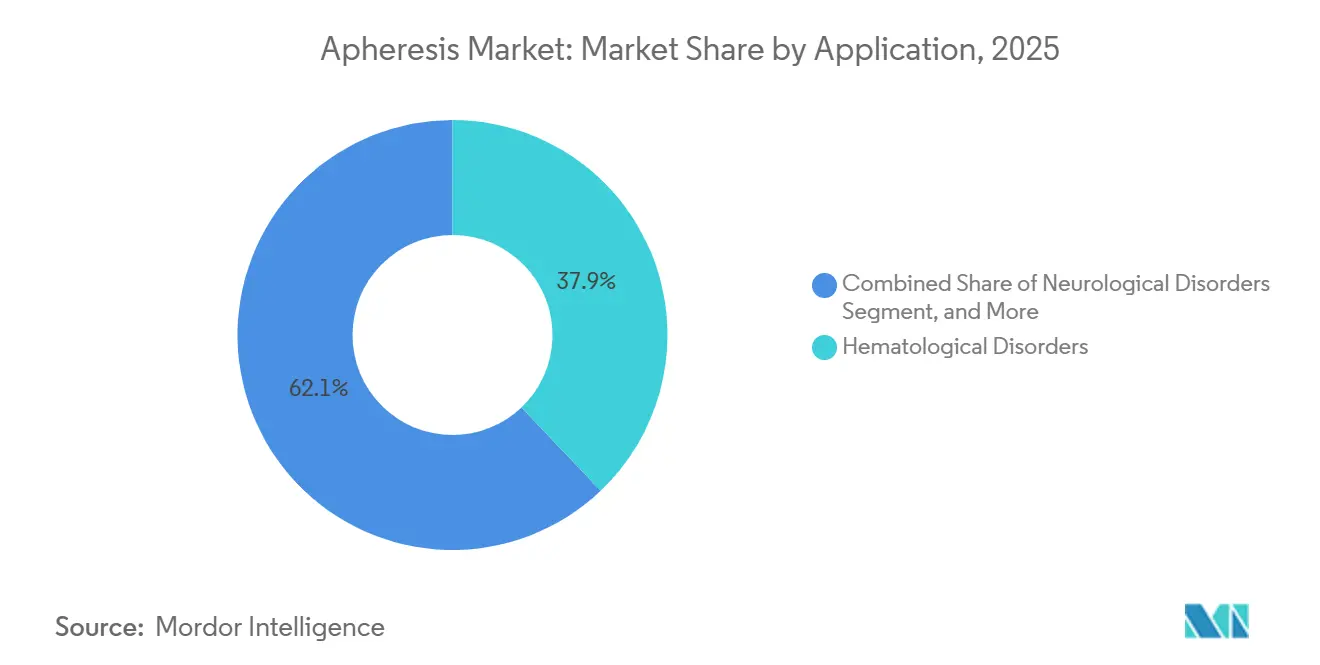

- By application, hematological disorders accounted for 37.88% of the apheresis market in 2025, and neurological disorders are projected to expand at a 6.85% CAGR through 2031.

- By end user, hospitals and transfusion centers led with a 47.74% revenue share in 2025; blood banks and component providers are projected to record the highest CAGR of 8.68% from 2026 to 2031.

- By geography, North America retained a 43.35% market share in 2025, while the Asia-Pacific region is set to grow at an 8.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Apheresis Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Hematologic & Autoimmune Disorders | +1.2% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Growing Demand for Plasma-Derived Therapeutics & Blood Components | +0.8% | Global, acute in North America, Europe, and emerging APAC markets | Long term (≥ 4 years) |

| Technological Advances in Automation & Membrane Filtration | +1.5% | Global, early adoption in North America, EU, Japan | Medium term (2-4 years) |

| Expansion of Cell & Gene Therapies Needing Leukapheresis | +1.8% | North America & EU core, spillover to APAC | Medium term (2-4 years) |

| Emergence of Portable Point-of-Care Apheresis Systems | +0.5% | APAC rural regions, sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| ESG-Driven Investment in Low-Waste Single-Use Kits | +0.9% | North America & EU, regulatory push in California, Germany | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hematologic & Autoimmune Disorders

Registry data from the American Society of Hematology and the European Hematology Association revealed an 18% increase in apheresis-eligible cases between 2024 and 2025, primarily driven by multiple myeloma and plasma cell dyscrasias. Myasthenia gravis and chronic inflammatory demyelinating polyneuropathy diagnoses rose 22%, reinforcing guideline upgrades that position therapeutic plasma exchange as first-line care. Japan added 14,000 reimbursable systemic lupus erythematosus patients after approving immunoadsorption apheresis in April 2025.[1]Ministry of Health, Labour and Welfare Japan, “Health Expenditure Statistics 2025,” mhlw.go.jp An aging OECD population continues to raise baseline monoclonal-gammopathy rates, ensuring that procedure volumes remain resilient even when per-patient intensity plateaus. These epidemiologic shifts support stable device utilization and recurrent consumable revenue streams for vendors.

Technological Advances in Automation & Membrane Filtration

Fresenius Kabi’s Lovo system introduced optical hematocrit sensors, which reduced hypocalcemia events by 34%, thereby reducing operator oversight requirements and broadening adoption in community hospitals. The FDA-cleared Aurora Xi separator utilizes 0.2-micron hollow-fiber membranes to minimize platelet damage associated with centrifugation, thereby increasing single-donor platelet yields by up to 22%. Terumo BCT integrated EHR connectivity into Spectra Optia in mid-2025, automatically populating patient parameters and reducing setup errors by 41% across six validation sites. Continuous-flow leukapheresis modules now process 15 liters of whole blood in under three hours, a 12-percentage-point yield gain over batch centrifugal systems.[2]European Medicines Agency, “Rise in Topical NSAID Registrations,” ema.europa.eu Collectively, these upgrades reduce training time, improve safety profiles, and shorten facility turnover, amplifying installed-base refresh cycles.

Expansion of Cell & Gene Therapies Needing Leukapheresis

Seven CAR-T therapies cleared in 2024-2025 require autologous leukapheresis, converting the apheresis workspace into an essential node in the cell-therapy supply chain. YESCARTA lead time decreased from 28 days in 2023 to 19 days in 2024, following protocol optimizations that increased CD3+ cell recovery by 11 percentage points. ABECMA’s label now allows outpatient leukapheresis, trimming bed utilization by 2.4 days per patient and saving USD 8,200 in direct costs. KYMRIAH collections increased 31% year-over-year, as 42% of procedures were moved to community oncology facilities, expanding the addressable base for mid-tier separators. With 18 CAR-T candidates in Phase III, leukapheresis volumes are expected to grow at double-digit rates through 2028, solidifying recurring demand for consumables.

Growing Demand for Plasma-Derived Therapeutics & Blood Components

Immunoglobulin consumption increased by 7.8% in 2025, surpassing whole-blood donation and driving investment in high-throughput plasmapheresis devices by blood banks. Grifols added 14 U.S. plasma centers and reported a 9.2% rise in collected volume, illustrating the direct linkage between plasma demand and equipment installs. CMS expanded coverage for steroid-refractory graft-versus-host disease photopheresis, creating a USD 180 million annual reimbursement pool that encourages hospital upgrades. China’s approval of 14 new device models and India’s capacity-doubling plan underline how emerging markets are localizing plasma supply to reduce import dependency.[3]National Medical Products Administration China, “E-Pharmacy Licensing Data 2025,” nmpa.gov.cn Sustained therapeutic demand ensures a predictable baseline for both device placements and consumable pull-through.

Restraints Impact Analysis of Apheresis Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Consumable Costs | -1.1% | Global, acute in emerging APAC markets, Latin America, MEA | Short term (≤ 2 years) |

| Shortage of Trained Specialists | -0.8% | North America, EU, Middle East, rural APAC | Medium term (2-4 years) |

| Supply-Chain Risks for Critical Disposables | -0.6% | Global, heightened in regions dependent on single-source suppliers | Short term (≤ 2 years) |

| Competition From Pathogen-Reduced Whole-Blood Tech | -0.4% | North America & EU, limited impact in APAC and MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Consumable Costs

Automated apheresis devices list between USD 85,000 and USD 140,000, while a 200-procedure facility spends USD 180,000–260,000 annually on disposables. Following an 18% CMS rate cut for hospital outpatient plasma exchange in 2025, profit margins narrowed to as little as USD 67 per session before overhead, which dampened new-equipment orders. Vendor-financed leasing and reagent-rental models have emerged, but adoption has been tepid because hospitals worry about being locked into consumables during supply disruptions. Until pricing models evolve, capital constraints will slow penetration in cost-sensitive regions.

Shortage of Trained Specialists

The American Society for Apheresis reported that 38% of U.S. hospitals struggled to recruit certified apheresis practitioners in 2025, up from 29% two years earlier. Europe introduced a 120-hour nurse-training certificate in 2024, yet only 340 professionals obtained it, covering fewer than 15% of new installations. Japan faces a 420-personnel deficit concentrated in prefectures pursuing CAR-T collection capacity. Staff turnover exacerbates the gap; the median nurse tenure has fallen to 3.2 years as hospitals redeploy personnel to higher-acuity units. Automation lowers skill thresholds, but regulations still require physician oversight, capping throughput when medical director availability is limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Apheresis Market Segment Analysis

By Product:

Consumables Gain on Sustainability PushThe devices segment retained a 67.43% value share in 2025; however, disposables are set to outpace the apheresis market at a 7.24% CAGR through 2031, driven by single-use kits that eliminate sterilization steps and align with ESG mandates. Hospitals adopting Amicus closed-loop sets shortened setup by nine minutes and reduced contamination risk by 62%, cementing locked-in consumable streams with 40% gross margins. Concurrently, device average selling prices slipped 4.3% as Chinese entrants priced their products 22–28% below those of incumbents, underscoring a shift in margin toward proprietary disposables.

Capital refresh cycles still matter because CAR-T collection centers need EHR-integrated automation to meet chain-of-identity audit demands. Terumo BCT disclosed that 58% of 2025 Spectra Optia shipments supported leukapheresis capacity expansions. Even so, disposables command defensible moats; FDA-cleared connector geometries prevent third-party substitutes, thereby anchoring revenue despite hardware price erosion. This pivot toward recurring consumables underpins long-run profitability for leading vendors in the apheresis market.

By Procedure:

Photopheresis Emerges as Growth LeaderPlasmapheresis accounted for 41.62% of the procedures in 2025, reflecting chronic immunoglobulin replacement and neurological plasma-exchange indications. Photopheresis, however, is expanding at an 8.35% CAGR, driven by FDA-approved CELLEX systems that reduce procedure time to three hours and secure broad CMS coverage for pediatric GVHD. Plateletpheresis remains indispensable to blood-bank logistics, while leukapheresis volumes climb in lock-step with CAR-T therapy rollouts.

Erythrocytapheresis is growing modestly at 4.1% because manual exchange still accounts for 54% of sickle-cell procedures in sub-Saharan Africa, where automated devices remain scarce. The American Society for Apheresis has upgraded automated red-cell exchange to Category I for the treatment of acute chest syndrome; however, uptake hinges on device affordability and technician training. Overall, a shifting procedure mix favors platforms that handle multiple modalities without hardware swaps, a capability that entrenches premium systems in the apheresis market.

By Application:

Neurological Disorders Accelerate After Guideline UpgradeHematological indications held a 37.88% share of the apheresis market size in 2025. Still, neurological disorders are projected to rise at a 6.85% CAGR as first-line status for plasma exchange in myasthenia gravis and Guillain-Barré syndrome drives procedure frequency. An aging population and improved autoantibody testing raise diagnostic rates, ensuring sustained utilization.

A Lancet Neurology meta-analysis showed a 41% reduction in disability progression with biweekly plasma exchange, further legitimizing the modality. Autoimmune and renal applications grow at 5.2% and 4.9% respectively, but remain niche compared with hematology and neurology volumes. As guideline evidence matures, reimbursement certainty will channel capital and consumable spend into high-growth neurology segments of the apheresis market.

By End User:

Blood Banks Surge on Plasma DemandHospitals maintained a 47.74% revenue share in 2025; however, blood banks are on track for an 8.68% CAGR, driven by the increasing demand for plasma-protein therapeutics as a result of aging populations. U.S. blood centers adopting Haemonetics’ MCS+ have seen yields increase by 22% and cut donor chair time by 14 minutes, showcasing operational gains that justify the purchase of the device.

Ambulatory clinics captured 14.3% of revenue as CMS site-neutral payment cuts shifted chronic plasma exchanges out of hospital outpatient settings. Fresenius Medical Care’s co-located dialysis-apheresis centers in Europe demonstrate how shared staffing models reduce fixed costs by USD 152,000 per site, enabling competitive pricing while protecting margins. The end-user mix, therefore, tilts toward settings with lower overhead and high procedure throughput, reinforcing consumables pull-through in the apheresis market.

Geography Analysis

North America Apheresis Market

North America led with a 43.35% market share in 2025, servicing the therapeutic, blood-bank, and CAR-T collection needs of 4,200 devices. CMS outpatient rate cuts redirected plasma-exchange volumes to ambulatory clinics, reducing overhead by 32% and driving demand for compact, technician-friendly systems. Canada’s nine new plasma centers reduced import reliance by 14%, driving PCS2 device sales up 19%. Mexico expanded coverage to 12 hospitals, yet device penetration remains under 40% because of budgetary limits.

Europe Apheresis Market

EMA clearance of the CliniMACS Prodigy enabled decentralized CAR-T processing at 18 sites, resulting in a savings of EUR 12,000 per patient in logistics. Germany reimbursed photopheresis for steroid-refractory GVHD, adding 1,600 patients and driving CELLEX installs. The United Kingdom increased plateletpheresis by 6.8% after rolling out Trima Accel in 14 regions. Southern Europe lags amid lower reimbursement rates.

APAC Apheresis Market

Asia-Pacific is forecast to expand at an 8.08% CAGR through 2031, the fastest pace globally. China approved 14 device models and raised plasma fractionation capacity by 18% in 2024 to hedge against import constraints. India aims to double the number of collection centers by 2027 and has ordered 80 devices from Fresenius Kabi and Haemonetics, although the rupee's weakness challenges affordability. Japan’s aging cohort increased plasmapheresis for autoimmune diseases by 12%, but a shortage of 420 trained staff curbs rural expansion. Australia and South Korea are widening coverage for LDL-apheresis and portable collection devices, respectively, supporting steady growth.

MEA Apheresis Market

The Middle East and Africa capture 6.2% of revenue, with GCC states investing in plasma self-sufficiency and South Africa expanding plateletpheresis by 22%. Manual red-cell exchange dominates sickle-cell care in sub-Saharan Africa because automated devices remain scarce.

Regulatory Landscape

Apheresis systems and related accessories sit at the intersection of medical device oversight and blood or biologics-adjacent requirements. In the United States, the FDA (CBER/CDRH) regulates automated apheresis collection and related component-processing workflows. Implanted apheresis ports are classified as Class II devices (Product Code: PTD). FDA activity in 2026 includes CBER publishing its 2026 guidance agenda and continued 510(k) clearances tied to apheresis-derived component processing and storage, which reinforces expectations for documentation, performance, and labeling and affects both capital equipment and single-use sets.

In Europe, compliance is shaped by the EU Medical Device Regulation (EU MDR 2017/745) and associated amendments, including Commission Delegated Regulation (EU) 2026/1451 (effective March 2026), alongside the notified-body certification pathway for QMS and technical documentation. Supplier readiness shows up in EU MDR QMS certifications held by established manufacturers, for example Fresenius Kabi with a certificate valid through October 17, 2026. International standardization for disposables and extracorporeal components is also progressing in 2026 via ISO workstreams, including draft-stage activity for apheresis blood bag systems and plasmafilter standards.

Value Chain Analysis

The apheresis value chain begins with upstream inputs such as medical-grade polymers (for tubing and bags), precision pumps and valves, sensors, and embedded control software. It then moves into midstream manufacturing, system assembly and calibration, and sterile disposable kit production. Downstream, distribution and service networks support installation, preventive maintenance, software updates that increasingly tie into EHR connectivity, and continuous consumables replenishment for blood banks, hospitals, transfusion centers, and ambulatory and specialty clinics performing plasmapheresis, leukapheresis, plateletpheresis, and photopheresis.

Value capture is concentrated in proprietary disposables and software-enabled workflow integration, while risk clusters around single-source components and regulated sterile consumables. Supply continuity and traceability are shaped by policy mechanisms such as the FDA device shortage and supply-chain provisions, including manufacturer notification obligations during certain emergencies. Industry actions also point to consolidation and partnerships across adjacent blood-management functions, including Haemonetics divesting whole blood assets to GVS S.p.A (December 2024) and Terumo Blood and Cell Technologies partnering with Santersus AG around Spectra Optia and NucleoCapture blood purification technology (November 2025). In 2026, platform expansion through software, including InVita Healthcare Technologies acquiring MAK-SYSTEM, supports a push toward end-to-end interoperability and chain-of-custody controls that link apheresis collection more tightly to cell therapy and hospital blood-management ecosystems.

Competitive Landscape

Moderate concentration defines the apheresis market; the top five vendors controlled significant share of 2025 shipments, yet none exceeded a 22% individual share. Fresenius Kabi’s Amicus platform utilizes real-time hematocrit sensing and automated citrate dosing, resulting in a 34% reduction in hypocalcemia events in a 240-patient study and securing 19 new U.S. contracts. Haemonetics counters with reagent-rental financing that lowers upfront costs in Latin America, although hospitals remain wary of being locked into consumables. Terumo BCT’s EHR-integrated Spectra Optia reduced setup errors by 41%, making it the preferred CAR-T collection platform where audit trails are mandatory.

White space persists in portable devices for rural transfusion sites and in automated red blood cell exchange for sickle cell care. Kaneka’s 22-kilogram Lifestream unit targets mobile drives and secured 14 Japanese orders within four months. Miltenyi Biotec’s CliniMACS Prodigy decentralizes CAR-T processing, eliminating USD 18,000–24,000 in logistics per patient. Chinese subsidiaries Jinbao and Shanghai RAAS captured 11% of Asia-Pacific sales by undercutting prices, although limited FDA or CE marks restrict their penetration in regulated OECD markets. Regulatory approval timelines averaging 9.2 months at the FDA and 14 months under the EU-MDR continue to serve as entry barriers, sustaining incumbent advantage.

Apheresis Industry Leaders

Fresenius SE & Co. KGaA

Asahi Kasei Corporation

Haemonetics Corporation

B. Braun SE

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Apheresis Market Companies Covered in this Report

- Asahi Kasei

- B. Braun

- Baxter

- Bioelettronica

- Cerus

- Fresenius

- Grifols

- Haemonetics

- HemaCare Corporation

- Infomed

- Kaneka

- Kawasumi Laboratories

- MacoPharma

- Mallinckrodt plc

- Medica S.p.A.

- Miltenyi Biotec

- Nikkiso Co., Ltd.

- Sumitomo Bakelite Co. Ltd.

- Terumo

- Therakos (Mallinckrodt)

Market Opportunities and Future Outlook

Operational capacity and throughput remain a visible whitespace, particularly when apheresis functions as a gating step for advanced therapies and clinical research. In England, the Department of Health and Social Care Apheresis Expert Working Group (March 2026) flagged limited apheresis capacity as a bottleneck for clinical trials and referenced NHS England planning for additional Advanced Therapy Medicinal Products requiring apheresis-based cell collection. That emphasis supports demand for standardized leukapheresis workflows, scheduling systems, and compliant chain-of-identity processes within hospital and transfusion networks.

Opportunities also cluster around donor-personalized plasma collection, expanded component-processing indications, and new therapeutic applications that build on existing therapeutic plasma exchange infrastructure. FDA 510(k) clearances in 2026 for plasma collection and apheresis-derived component processing systems, including Haemonetics NexSys PCS with Persona PLUS in February 2026 and expanded use clearance for the Hemanext One System in March 2026, point to continued product-cycle refresh and route-to-market momentum for vendors serving blood centers. On the clinical side, publication activity is broadening the plasma exchange narrative, including a 2026 Journal of Clinical Apheresis report on reducing circulating microplastic particles following therapeutic plasma exchange, which supports further investigator-initiated use and protocol development where reimbursement and evidence pathways align.

Recent Industry Developments in Apheresis Market

- July 2026: InVita Healthcare Technologies completed its acquisition of MAK-SYSTEM to expand blood management software capabilities across hospital and blood center workflows. The acquisition improves end-to-end data integration around collection, inventory, and compliance, which becomes more critical as apheresis volumes rise and chain-of-custody requirements tighten for cell therapy-linked leukapheresis.

- February 2026: Haemonetics received FDA 510(k) clearance for the NexSys PCS Plasma Collection System with Persona PLUS technology. The clearance supports donor-tailored plasma collection protocols and gives plasma collection operators an additional pathway to increase productivity and standardization without relying only on footprint expansion.

- November 2024: Terumo Blood and Cell Technologies launched a localization initiative in China through a partnership with Terumo Medical Products (Hangzhou) Co., Ltd., establishing entrusted manufacturing at the TMPH facility in Qiantang District, Hangzhou. Local production shortens supply lines for regulated disposables and components and aligns with China programs focused on domestic capability building in healthcare manufacturing.

Apheresis Market Report Scope and Research Methodology

Market Definition and Coverage

The market is defined as the value generated from apheresis procedures and the supporting products used to separate, remove, or collect specific blood components, across donor and therapeutic settings. Our sizing is built in value terms and tracks demand across key care sites and regions.

Scope exclusions: It does not include general blood collection supplies that are not used for apheresis, or downstream laboratory testing services that happen after the procedure.

Segments Covered in This Report

- By Product

- Devices

- Disposables & Consumables

- By Procedure

- Plasmapheresis

- Plateletpheresis

- Leukapheresis

- Erythrocytapheresis

- Photopheresis

- By Application

- Hematological Disorders

- Neurological Disorders

- Renal Disorders

- Autoimmune Disorders

- Other Applications

- By End User

- Blood Banks & Component Providers

- Hospitals & Transfusion Centers

- Ambulatory & Specialty Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building a clean fact base on procedure volumes, disease burden, and health system capacity that influence apheresis use. We rely on public sources such as the World Health Organization, the US CDC, the US FDA, the US National Institutes of Health (clinical trials registry and publications), and OECD health statistics to set realistic demand guardrails.

Next, the scope is cross-checked using sources such as peer-reviewed hematology and transfusion medicine journals, national blood service and transfusion association pages, and hospital network publications that discuss therapy adoption and practice patterns. We also use paid subscriptions for company financials and intelligence, news and financials, and patent databases to confirm product focus, launch timing, and revenue mix signals. The specific desk sources listed here are illustrative, and many other public and paid references were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to verify what portion of procedures are donor versus therapeutic, how device utilization differs by site of care, and how consumable use per procedure is trending. We spoke with a mix of blood bank operators, hospital transfusion teams, clinic administrators, and industry experts across APAC, EMEA, and the Americas so that regional reimbursement and practice differences could be reflected and then reconciled back to the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 13% | APAC: 49% |

| Mid tier: 56% | Functional/Unit leaders: 29% | EMEA: 29% |

| Smaller Players: 18% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing begins with a top-down demand pool build where procedure opportunity is reconstructed from treated populations and care setting capacity, and then translated into spend using typical device placement and disposable consumption patterns. To keep the totals practical, results are corroborated using selective bottom-up checks such as sampled ASP times estimated unit volumes for disposables, channel feedback on device shipment direction, and supplier mix indicators where disclosures are available.

Key model inputs include apheresis procedure mix (plasmapheresis, plateletpheresis, leukapheresis, erythrocytapheresis, and photopheresis), utilization rates by end user (blood banks and component providers, hospitals and transfusion centers, and ambulatory or specialty clinics), technology split between centrifugation and membrane separation, and the share of donor versus therapeutic procedures. We also track indicators that shift spending, such as changes in reimbursement emphasis, hospital infusion and transfusion throughput, and adoption in hematological, neurological, renal, and autoimmune use cases.

For forecasting, scenario analysis is used so that adoption and pricing can move in a controlled way by region, and then the trajectories are checked back with expert expectations from primary discussions. Where bottom-up data is thin for a country, gap handling is done by applying peer-country utilization ratios and then rebalancing to match regional totals before finalizing.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including procedure trend direction, installed base logic, and consumables per procedure assumptions. Any large variances are reviewed, and the underlying drivers are re-tested with follow-up outreach when a change looks structural rather than temporary.

A multi-step review is followed before sign-off so that definitions, currency handling, and math consistency are checked by another analyst. The report is refreshed annually, and interim updates are made when material events occur, such as major regulatory actions or sharp pricing shifts. Before delivery, we run a fresh pass on key assumptions so clients receive the most current view available at that time.

Mordor Intelligence's Apheresis Market Size Versus Other Published Estimates

It is common to see different published values for the apheresis market because teams do not always count the same revenue streams or use the same timing for pricing and currency conversion. Another reason is that some estimates lean on a single growth curve, while others try to anchor the totals to procedure reality and care setting utilization.

The main spread usually comes from scope choices, like whether donor and therapeutic procedures are combined, how disposables and consumables are counted per procedure, and if adjacent blood processing equipment is pulled into the total. Differences can also come from how technology splits (centrifugation versus membrane separation) are treated, and whether the model is refreshed after reimbursement or adoption changes that affect utilization in hospitals and blood banks.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.16 B (2026) | |

| Global Consultancy A | USD 3.93 B (2025) | Uses a different base year and longer forecast window, and it can also treat consumables spend more broadly across instruments and kits, which shifts the starting value when procedure mix is re-estimated. |

| Industry Publisher B | USD 2.97 B (2025) | Reports a lower 2025 level that may reflect narrower inclusion of procedure-linked consumables or more conservative utilization assumptions for therapeutic settings, especially when country-level capacity is not explicitly reconciled. |

The table shows that the year used and what gets counted around procedure-linked consumables can shift the market size by a noticeable amount, and that is why we keep the model tied to procedure mix and end user utilization checks, a discipline applied consistently by Mordor Intelligence.

Key Questions Answered in the Report

What was the global apheresis market size in 2026?

It reached USD 4.16 billion and is projected to grow to USD 5.48 billion by 2031.

Which apheresis procedure is growing fastest?

Photopheresis is expected to lead with an 8.35% CAGR through 2031, following broader CMS coverage.

Why are disposables outpacing device revenue?

Single-use kits meet infection-control and ESG targets, driving a 7.24% CAGR for consumables.

Which region will see the highest growth?

The Asia-Pacific region will advance at an 8.08% CAGR due to accelerated device approvals and plasma self-sufficiency initiatives.

What is a key restraint on market expansion?

High capital plus consumable costs reduce return on investment for hospitals in price-sensitive regions.

Page last updated on: