Antiplatelet Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.18 Billion |

| Market Size (2031) | USD 16.57 Billion |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

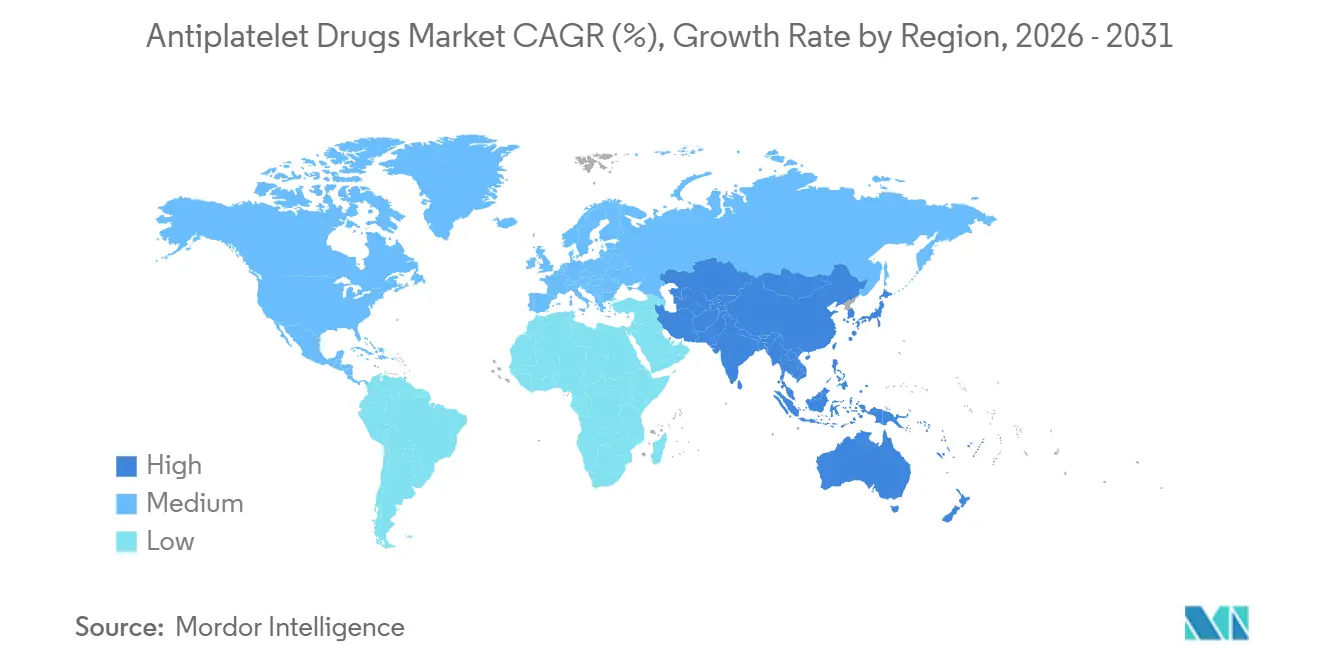

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

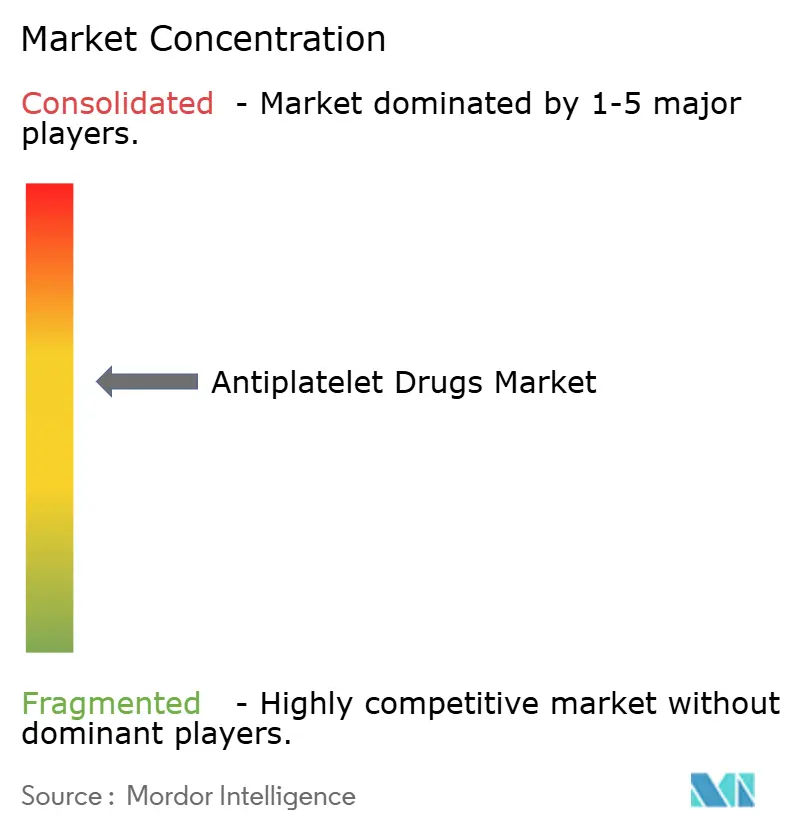

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antiplatelet Drugs Market Analysis by Mordor Intelligence

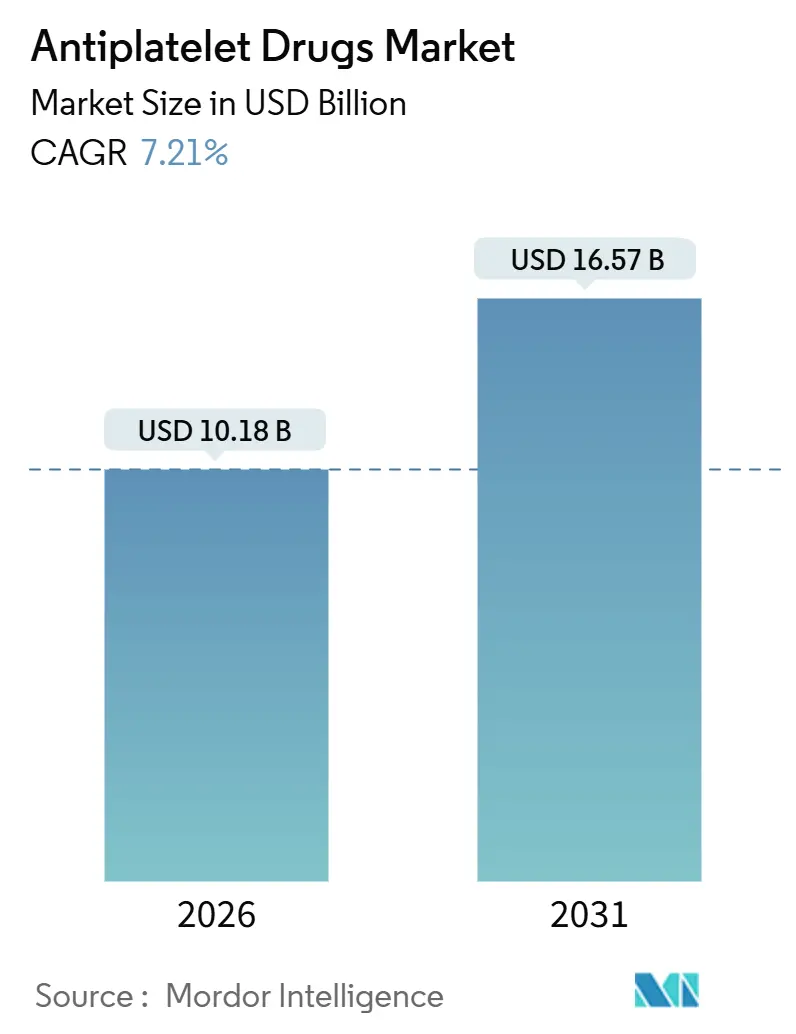

The Antiplatelet Drugs Market size is estimated at USD 10.18 billion in 2026, and is expected to reach USD 16.57 billion by 2031, at a CAGR of 7.21% during the forecast period (2026-2031).

Robust growth is anchored by three structural forces: rising cardiovascular mortality, wider use of guideline-endorsed potent P2Y12 inhibitors, and rapid expansion of percutaneous coronary intervention (PCI) capacity in emerging economies. Parallel trends include an aging population that intensifies thrombotic risk, payer acceptance of potent dual antiplatelet therapy, and manufacturer investments in ethnically targeted formulations that address genotype-driven variation in drug response. Competitive strategy now hinges on balancing superior efficacy with bleeding risk, expanding injectable portfolios for acute care, and leveraging digital adherence platforms to extend therapy duration. Opportunities abound in Central and Eastern Europe, Latin America, and Southeast Asia, where PCI penetration lags high-income benchmarks. At the same time, headwinds stem from major bleeding concerns and direct oral anticoagulants being substituted for atrial fibrillation patients. Over the forecast horizon, the antiplatelet drugs market is expected to remain volume-driven but price-competitive as generic ticagrelor and domestic P2Y12 biosimilars erode branded margins in Asia and Europe.

Key Report Takeaways

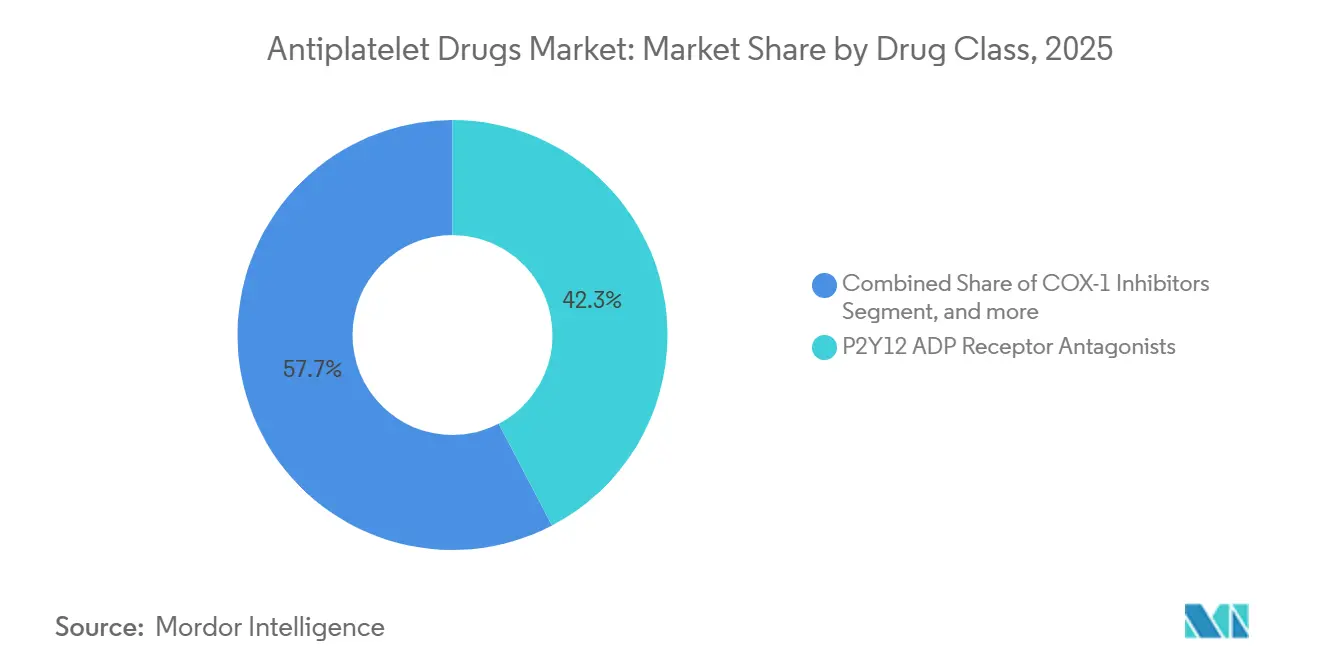

- By drug class, P2Y12 inhibitors led with 42.34% antiplatelet drug market share in 2025; glycoprotein IIb/IIIa agents are forecast to expand at a 9.54% CAGR to 2031.

- By application, myocardial infarction accounted for 36.54% of the antiplatelet drugs market in 2025, while PCI demand is advancing at a 9.43% CAGR through 2031.

- By route of administration, oral formulations accounted for 72.34% of revenue share in 2025; injectables are projected to grow at a 9.76% CAGR through 2031.

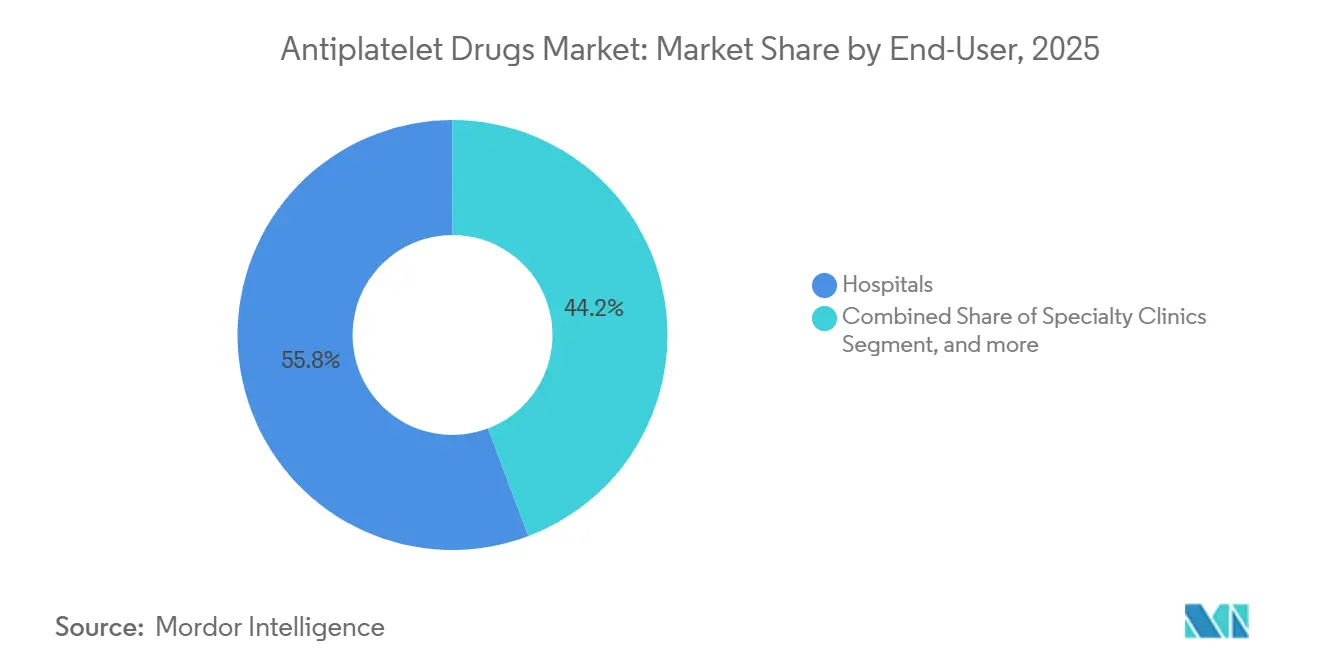

- By end user, hospitals accounted for 55.76% of global volume in 2025, whereas home care settings are growing at a 10.54% CAGR.

- By geography, North America accounted for 43.12% of global revenue in 2025, and Asia-Pacific is the fastest-growing region at an 8.43% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Antiplatelet Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Global Cardiovascular Disease Burden | +1.8% | Global, with acute pressure in South Asia, Sub-Saharan Africa | Long term (≥ 4 years) |

| Rapidly Growing Geriatric Population | +1.5% | North America, Europe, Japan; emerging in China | Long term (≥ 4 years) |

| Guideline-Driven Uptake of Dual Antiplatelet Therapy | +1.3% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Proliferation of Percutaneous Coronary Interventions | +1.2% | Asia-Pacific core, spill-over to Middle East & Latin America | Medium term (2-4 years) |

| Expansion of Platelet-Function Testing-Guided Personalized Therapy | +0.7% | North America, select European centers | Short term (≤ 2 years) |

| Development of Ethnically-Targeted Oral P2Y12 Inhibitors | +0.6% | East Asia (China, Japan, South Korea), Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Cardiovascular Disease Burden

Cardiovascular mortality reached 19.8 million deaths in 2022, of which ischemic heart disease contributed 9 million, reinforcing the need for secondary-prevention therapy worldwide. Low- and middle-income countries now account for 80% of these fatalities, yet antiplatelet coverage remains under 30% of eligible patients, underpinning sizable unmet demand in South Asia and Sub-Saharan Africa. The World Health Organization’s 2025 Global Action Plan aims for 50% antiplatelet coverage by 2030, a goal that requires initiating therapy for an additional 200 million patients. Governments in India, Nigeria, and Indonesia have responded with procurement tenders that favor generic clopidogrel, expanding the patient pool eligible for treatment while challenging branded pricing. Manufacturers, therefore, face a dual imperative: maintain abundant supply volumes and develop cost-optimized formulations for budget-constrained health systems.

Rapidly Growing Geriatric Population

Adults 65 years and older show threefold higher platelet reactivity and fivefold greater thrombotic risk versus younger cohorts, positioning them as primary users of chronic antiplatelet therapy[1]United Nations, “World Population Ageing 2024,” un.org. The United Nations projects that 1.6 billion people will be in this age group by 2050, with the steepest climb in East Asia and Southern Europe. Japan illustrates the challenge: patients over 75 accounted for 68% of acute coronary syndrome admissions in 2024, yet standard-dose ticagrelor raised bleeding complications by 40%, prompting adoption of reduced-dose regimens. Similar dynamics in China and Italy are fueling research into lower-dose tablets, genotype screening, and platelet-function testing to personalize therapy intensity. The broadening elderly base thus expands demand but amplifies safety scrutiny.

Guideline-Driven Uptake of Dual Antiplatelet Therapy

The 2025 ACC/AHA/SCAI guideline gave ticagrelor or prasugrel Class I status for acute coronary syndrome patients undergoing PCI, relegating clopidogrel to a fallback option. U.S. hospital formularies quickly aligned: ticagrelor occupied 61% of post-PCI prescriptions in 2025, up from 42% two years earlier. European guidance mirrored this priority for patients with diabetes and multivessel disease, although national payers slowed implementation through step-therapy rules. Consequently, North America and Scandinavia exhibit rapid adoption, while Southern and Eastern Europe lag by up to two years. Overall, guideline reinforcement sustains premium segments but heightens payer scrutiny of bleeding risk and budget impact.

Expansion of Platelet-Function Testing-Guided Personalized Therapy

Point-of-care assays such as VerifyNow and thromboelastography revealed that 28% of clopidogrel-treated patients display high on-treatment platelet reactivity, with a 2.3-fold rise in recurrent MI risk[2]Journal of the American College of Cardiology, “High On-Treatment Platelet Reactivity Study,” jacc.org. Fourteen U.S. academic centers integrated routine testing in 2025, escalating non-responders to ticagrelor or prasugrel. Economic modeling shows that preventing a single recurrent MI offsets the USD 150-USD 300 cost of testing. Barriers persist, including the absence of standardized cut-offs and patchwork reimbursement, yet adoption is expected to grow as guidelines evolve and device costs fall.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of Major Bleeding Events | -1.4% | Global, acute in elderly populations (North America, Europe, Japan) | Medium term (2-4 years) |

| High Cost of Novel Antiplatelet Agents | -1.1% | Low- and middle-income countries (Sub-Saharan Africa, South Asia, Latin America) | Long term (≥ 4 years) |

| Genetic Polymorphisms Limiting Drug Responsiveness | -0.6% | East Asia, Middle East, select European subgroups | Medium term (2-4 years) |

| Shift Toward Direct Oral Anticoagulants as Substitutes | -0.8% | North America, Western Europe (atrial fibrillation cohorts) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Risk of Major Bleeding Events

BARC type 3 or 5 bleeding affects 2%-4% of ticagrelor or prasugrel users each year, compared with 1.5%-2.5% for clopidogrel, intensifying clinician concern for elderly patients. A 2024 meta-analysis showed each year above age 75 raises bleeding risk by 8%. European centers mitigate this by switching stable patients from potent agents to clopidogrel after 3 months, halving major bleeds without increasing thrombotic events. The U.S. FDA’s 2025 safety communication underlined intracranial hemorrhage risk in adults over 80 and encouraged shorter therapy durations[3]U.S. Food and Drug Administration, “Safety Communication on Antiplatelet Therapy,” fda.gov. To preserve share, manufacturers are testing reduced-dose tablets and fixed combinations with proton-pump inhibitors.

High Cost of Novel Antiplatelet Agents

Monthly retail prices of USD 300-USD 400 for ticagrelor or prasugrel render them unaffordable in many low-income settings, where patients often pay 40%-70% of pharmacy costs out of pocket. India’s pricing authority capped branded ticagrelor at INR 1,200 (USD 14) in 2024, forcing companies to pivot toward generic partnerships. In Sub-Saharan Africa, even clopidogrel at USD 5 per month is beyond reach for most post-MI survivors, leading to high discontinuation rates. Cost-effectiveness analyses exceed USD 150,000 per QALY in these settings, prompting payers to restrict reimbursement to the highest-risk cohorts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: Potent P2Y12 Inhibitors Dominate Revenue While IIb/IIIa Agents Accelerate

P2Y12 antagonists held 42.34% of 2025 revenue, underscoring their entrenchment in post-MI and post-PCI care. The 2025 ACC/AHA guideline propelled ticagrelor and prasugrel ahead of clopidogrel, solidifying their leadership. In contrast, glycoprotein IIb/IIIa inhibitors, although smaller in absolute value, are projected to grow at 9.54% CAGR as interventionalists rely on bailout dosing during complex PCI. COX-1 inhibitors remain fundamental yet commoditized, limiting upside. The antiplatelet drugs market size for glycoprotein IIb/IIIa agents is projected to expand at 9.54% CAGR between 2026 and 2031, outpacing all other classes. Competitive dynamics are shifting: generic ticagrelor captured 22% European volume by 2025, eroding branded share even as new entrants queue for approval.

Drug-class mix will keep evolving as hospitals weigh bleeding risk against ischemic benefit. The antiplatelet drugs industry increasingly segments therapy intensity by genotype and bleeding propensity, a pattern likely to accelerate once ongoing dose-optimization studies read out in 2027.

By Application: PCI-Linked Prescriptions Outstrip MI Maintenance

Myocardial infarction accounted for 36.54% revenue in 2025, yet PCI applications are rising at a 9.43% CAGR as catheter-based revascularization becomes the global standard. In China, PCI procedure growth of 12% annually translates directly into higher dual antiplatelet volumes. The antiplatelet drugs market share for PCI-related prescriptions is projected to reach 40% by 2031. While arterial thrombosis and stroke prevention remain important, their slower growth reflects limited guideline evolution. Future upside lies in chronic total occlusion interventions and peripheral artery revascularization, both of which extend the duration of dual therapy.

Emerging markets demonstrate the steepest ramp as they transition from thrombolytics to PCI. Each procedural gain increases demand for potent loading doses in emergency departments, reinforcing injectable and oral synergy within the hospital channel.

By Route of Administration: Oral Formulations Command Scale, Injectables Provide Acute Flexibility

Oral drugs seized 72.34% of 2025 revenue through chronic outpatient use. Nonetheless, injectables are forecast at a 9.76% CAGR on the back of new eptifibatide syringe formats that cut prep time by 40% and minimize dosing errors, making them practical for community hospitals. The antiplatelet drugs market for injectables is expected to reach USD 3.2 billion by 2031, driven by the growth of complex PCI procedures. Oral discontinuation remains problematic—up to 40% of patients stop therapy early—so digital adherence tools and online pharmacy auto-refill programs are expected to mitigate attrition.

By End-User: Hospitals Hold the Lion’s Share, Homecare Grows Fastest

Hospitals consumed 55.76% of volume in 2025, reflecting the initiation of therapy during acute events. Specialty clinics manage dose titration, while home care settings, aided by telemedicine and remote platelet function tests, are scaling at a 10.54% CAGR. Over time, the antiplatelet drugs market size flowing through home care is poised to rival clinic channels as remote monitoring reimbursement expands in the United States, Scandinavia, and Japan.

By Distribution Channel: Hospital Pharmacies Lead, Online Platforms Expand Access

Hospital pharmacies generated 58.65% of dispensing volume in 2025. Yet online pharmacies are growing at a 10.45% CAGR after regulators allowed 90-day supplies of cardiovascular medicines to be mailed directly to patients. Cross-border e-pharmacy rules in the European Union now permit Polish and Romanian consumers to purchase lower-cost ticagrelor from German or Dutch sites, intensifying competitive pricing.

Geography Analysis

North America captured 43.12% of 2025 revenue, fueled by high PCI volumes, unrestricted Medicare coverage for ticagrelor, and strong guideline adherence. The United States accounts for 85% of regional sales, while Canada and Mexico are growing steadily as formularies expand access. Payer pressure to contain bleeding costs encourages de-escalation to clopidogrel in frail seniors, but robust procedure counts keep absolute volumes elevated.

Europe ranks second, yet national payer policies fragment its landscape. Germany and the United Kingdom show high per capita consumption due to dense cath-lab networks—Germany performed 5,200 PCIs per million residents versus a continental average of 2,383.9 in 2022. Southern and Eastern Europe move more slowly owing to step-therapy mandates, although EMA approval of generic ticagrelor and cross-border e-pharmacy legislation are narrowing gaps.

Asia-Pacific posts the fastest outlook at 8.43% CAGR. China’s 1.1 million PCIs in 2024 anchor the regional scale, aided by financing reforms that cut patient co-pays to 30%. India’s 18% annual PCI surge widens penetration beyond tier-1 cities through mobile cath labs. Japan, with a 72% ticagrelor share in the post-PCI segment, exemplifies genotype-driven substitution for clopidogrel. Southeast Asia remains price-sensitive, but domestic biosimilars and government tenders promise a gradual upgrade from aspirin-only regimens.

The Middle East & Africa and South America trail in absolute size but gain momentum as cardiovascular programs scale and procurement pools negotiate volume discounts for generics. Brazil and Saudi Arabia are funding new cath labs, ensuring steady uptake of both oral and injectable products.

Competitive Landscape

The field is moderately concentrated: AstraZeneca, Sanofi, and Eli Lilly collectively hold about 55% of branded sales, while dozens of generic manufacturers fragment clopidogrel and ticagrelor volumes. AstraZeneca’s Brilinta delivered USD 1.5 billion in 2024 sales, supported by outcome data and label extensions. Yet European generics sliced 22% of volume in 2025, trimming average selling prices by 60%. Sanofi’s once-flagship clopidogrel slipped to USD 400 million revenue as mature markets went off-patent, though brand equity preserves share in parts of Africa and South Asia. Eli Lilly’s prasugrel is indicated for high-risk PCI patients but remains constrained by bleeding risk.

White spaces include genotype-tailored P2Y12 inhibitors, fixed combinations that mitigate gastrointestinal bleeding, and digital adherence ecosystems. Hanmi Pharmaceutical’s 2025 patent filing for a ticagrelor-esomeprazole tablet represents one such niche. Device-drug integration is also advancing: AstraZeneca and Medtronic’s 2024 collaboration embedded Brilinta adherence alerts into implantable monitors, reducing discontinuations by 12% over 6 months. Market entry for biosimilar ticagrelor in China, India, and the EU will intensify pricing pressure but grow total treated populations.

Antiplatelet Drugs Industry Leaders

AstraZeneca

Lilly

Sanofi

Bristol-Myers Squibb Company

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Concept Medical Inc. has announced the successful enrollment of the first patients in the STARS DAPT trial, a study evaluating a polymer-free sirolimus-based nanocarrier eluting stent for STEMI patients. This milestone marks a key step in testing the new drug delivery technology's effectiveness. The trial aims to compare short dual antiplatelet therapy with conventional treatment.

- October 2024: EU harmonized cross-border e-pharmacy rules, enabling price-sensitive consumers to source antiplatelet drugs from lower-cost member states

Global Antiplatelet Drugs Market Report Scope

As per scope of the report, antiplatelet drugs are medications that prevent blood cells (platelets) from clumping together to form clots. They are primarily used to reduce the risk of heart attack, stroke, and other cardiovascular events. Common examples include aspirin, clopidogrel, and ticagrelor.

The Antiplatelet Drugs Market is Segmented by Drug Class (COX-1 Inhibitors, P2Y12 ADP Receptor Antagonists, Glycoprotein IIb/IIIa Inhibitors, Phosphodiesterase Inhibitors, and PAR-1 Antagonists), Application (Myocardial Infarction, Percutaneous Coronary Interventions, Arterial Thrombosis, and Other Applications), Route of Administration (Oral and Injectable), End-User (Hospitals, Specialty Clinics, Homecare, and Other End-Users), Distribution Channel (Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| COX-1 Inhibitors |

| P2Y12 ADP Receptor Antagonists |

| Glycoprotein (GP) IIb/IIIa Inhibitors |

| Phosphodiesterase (PDE) Inhibitors |

| PAR-1 Antagonists |

| Myocardial Infarction |

| Percutaneous Coronary Interventions |

| Arterial Thrombosis |

| Other Applications |

| Oral |

| Injectable |

| Hospitals |

| Specialty Clinics |

| Homecare |

| Other End-Users |

| Hospital Pharmacy |

| Retail Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Drug Class | COX-1 Inhibitors | |

| P2Y12 ADP Receptor Antagonists | ||

| Glycoprotein (GP) IIb/IIIa Inhibitors | ||

| Phosphodiesterase (PDE) Inhibitors | ||

| PAR-1 Antagonists | ||

| By Application | Myocardial Infarction | |

| Percutaneous Coronary Interventions | ||

| Arterial Thrombosis | ||

| Other Applications | ||

| By Route Of Administration | Oral | |

| Injectable | ||

| By End-User | Hospitals | |

| Specialty Clinics | ||

| Homecare | ||

| Other End-Users | ||

| By Distribution Channel | Hospital Pharmacy | |

| Retail Pharmacy | ||

| Online Pharmacy | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

How large is global demand for antiplatelet drugs in 2026?

The antiplatelet drugs market size is USD 10.18 billion in 2026 and is forecast to grow at a 7.21% CAGR to 2031.

Which drug class is expanding fastest through 2031?

Glycoprotein IIb/IIIa inhibitors are projected to rise at a 9.54% CAGR as interventional cardiologists use them during complex PCI.

Why is Asia-Pacific the quickest-growing regional segment?

Rising cardiovascular burden, expanded PCI capacity, and launch of lower-cost ticagrelor biosimilars drive an 8.43% CAGR in Asia-Pacific.

What is the main safety concern limiting potent P2Y12 uptake?

Major bleeding, especially in patients aged over 75, curtails long-term use of ticagrelor and prasugrel.

How are online pharmacies influencing therapy adherence?

Regulatory changes allowing 90-day mail supplies and subscription models from providers such as Amazon cut missed doses by 15%.

Which companies lead in branded revenue?

AstraZeneca, Sanofi, and Eli Lilly together hold roughly 55% of branded sales, with AstraZenecaÕs Brilinta contributing the largest share.

Page last updated on: