Embolization Particle Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

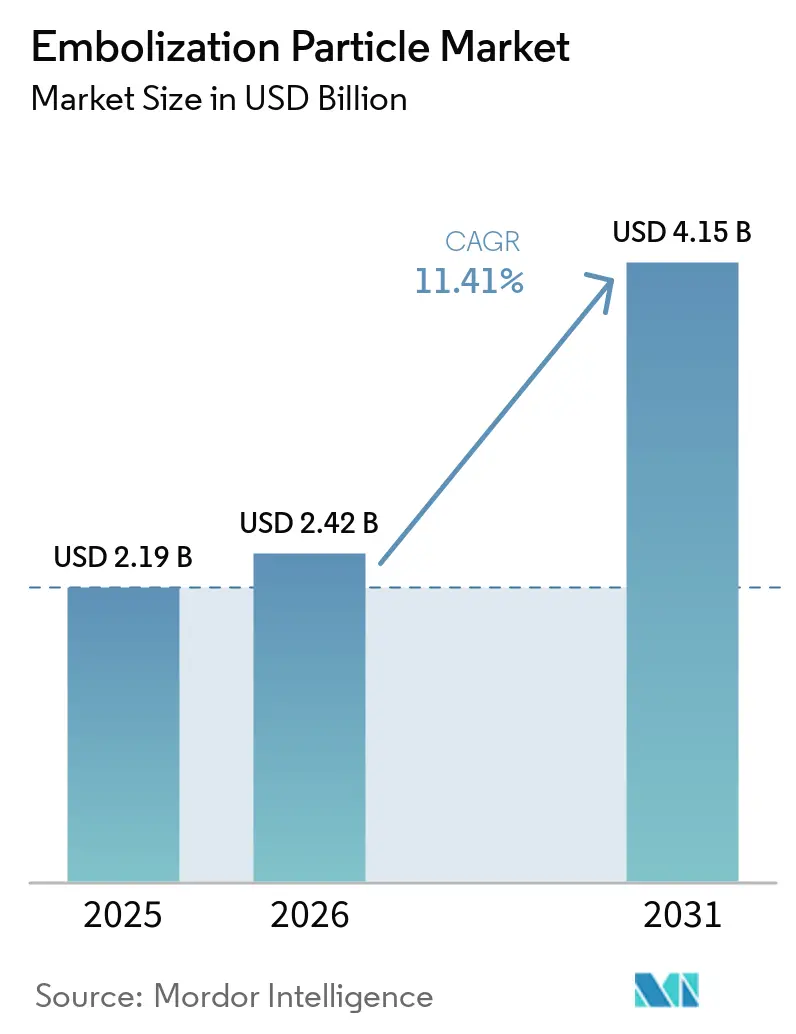

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 4.15 Billion |

| Growth Rate (2026 - 2031) | 11.41% CAGR |

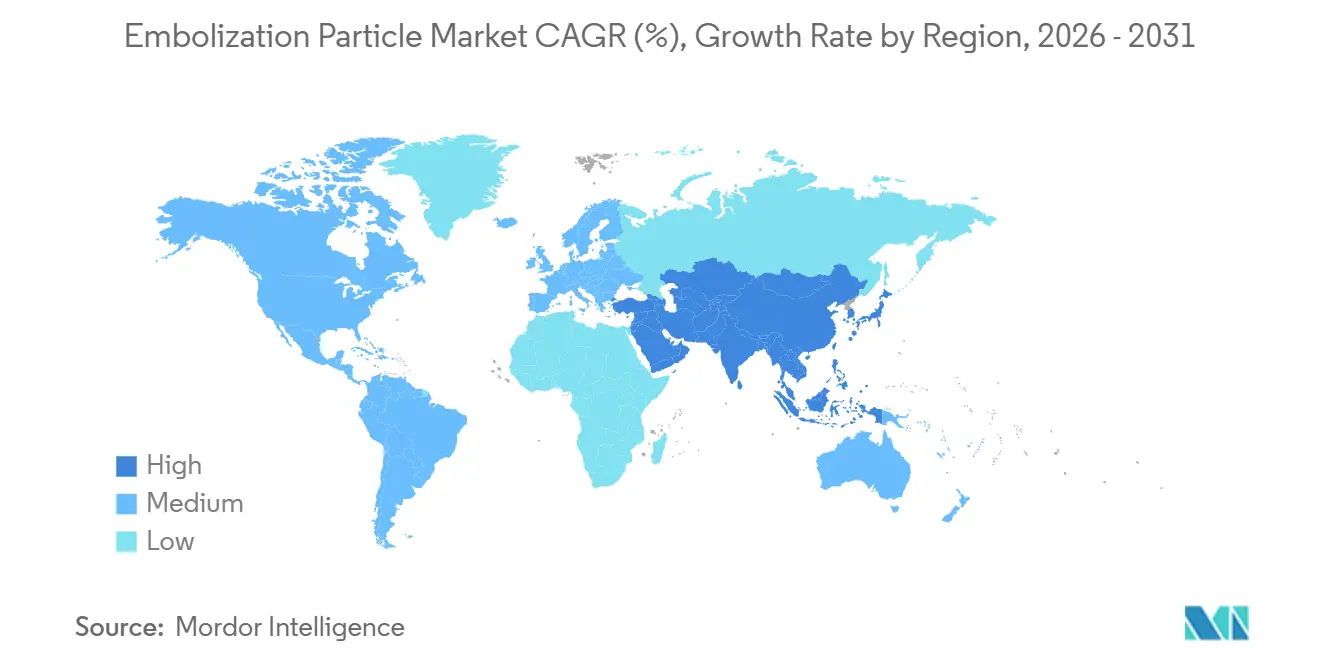

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

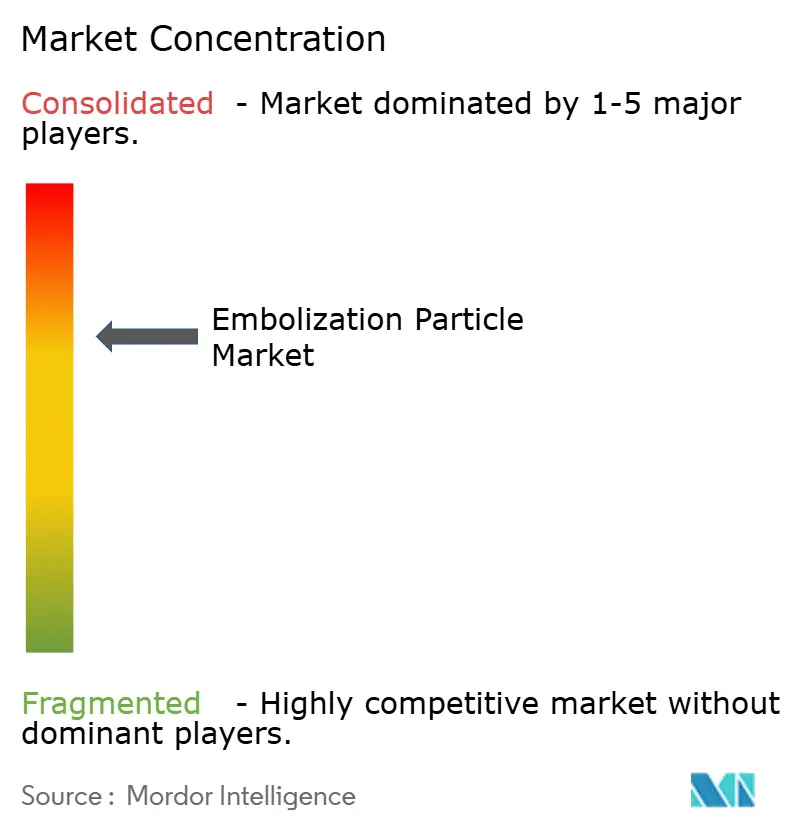

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embolization Particle Market Analysis by Mordor Intelligence

The Embolization Particle Market size is projected to expand from USD 2.19 billion in 2025 and USD 2.42 billion in 2026 to USD 4.15 billion by 2031, registering a CAGR of 11.41% between 2026 to 2031.

The embolization particle market is being supported by the steady rise in liver cancer burden, especially hepatocellular carcinoma, which continues to expand the eligible pool for locoregional treatment in patients who are not surgical candidates. The July 2025 U.S. approval of SIR-Spheres for unresectable HCC strengthened radioembolization as a mainstream treatment option and widened the commercial runway for suppliers with established clinical training and dosimetry capabilities. Demand is also broadening outside liver oncology as prostate artery embolization gains guideline support, which adds a procedural growth stream that is less dependent on hospital oncology pathways alone. Competition is becoming more focused on imageable materials, calibrated delivery, and evidence-backed outcomes rather than simple portfolio breadth, which favors companies that can pair product performance with physician training and workflow support. Growth still faces pressure from uneven reimbursement and high procedure costs, yet the ongoing move toward outpatient embolization, together with broader clinical acceptance, keeps the long-term expansion case intact.

Key Report Takeaways

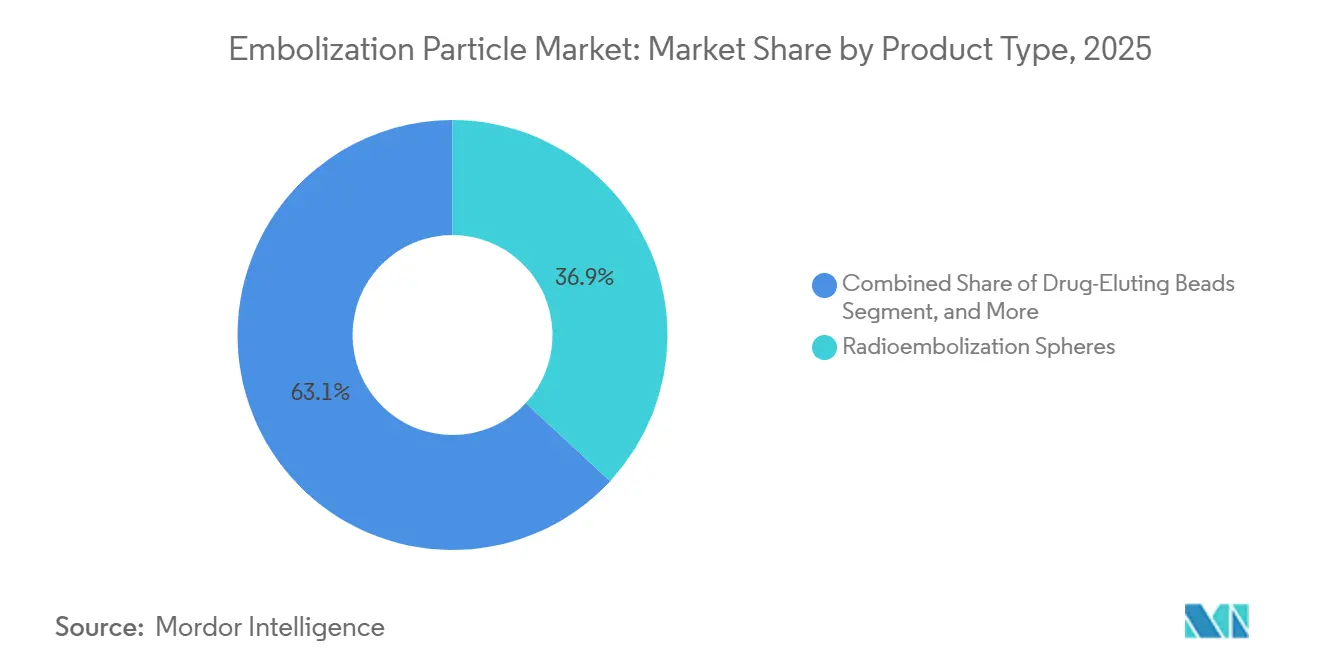

- By product type, radioembolization spheres led with 36.93% of the embolization particle market size in 2025, while drug-eluting beads are forecast to expand at a 12.84% CAGR through 2031.

- By embolic material, synthetic materials held 56.16% share in 2025, while natural materials are projected to grow at a 12.39% CAGR through 2031.

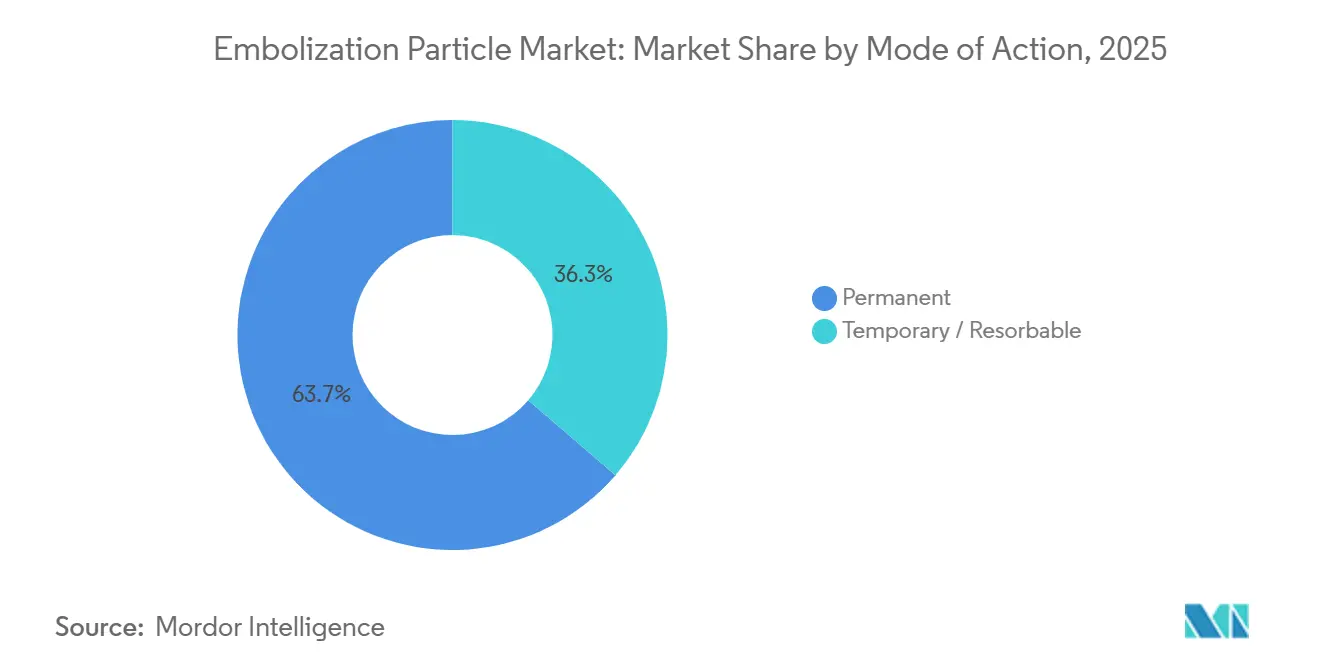

- By mode of action, permanent embolization agents accounted for 63.69% share in 2025, while temporary and resorbable agents are projected to advance at a 13.82% CAGR through 2031.

- By application, oncology accounted for 42.71% of the embolization particle market size in 2025, while urology is advancing at a 15.64% CAGR through 2031.

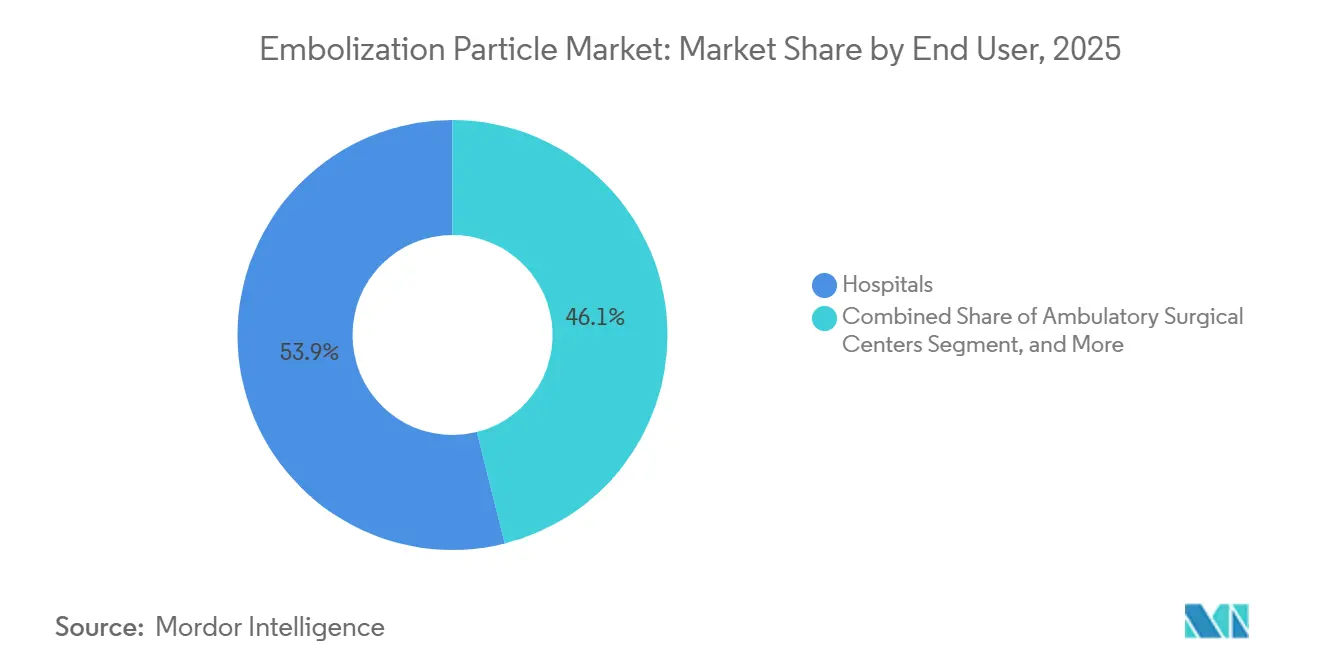

- By end user, hospitals held 53.88% of the embolization particle market share in 2025, while ambulatory surgical centers are projected to expand at a 14.32% CAGR through 2031.

- By geography, North America held 36.05% of the embolization particle market share in 2025, while Asia-Pacific is projected to grow at a 15.36% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Embolization Particle Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Liver Cancer And Embolization Volumes | +2.8% | Global, with highest intensity in China, Southeast Asia, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Shift Toward Minimally Invasive Embolization | +1.9% | North America and Europe, with acceleration in Asia-Pacific | Medium term (2-4 years) |

| Advances In Radiopaque, Calibrated, And Drug-Eluting Particles | +2.5% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Expansion Of Hospital-To-Outpatient Embolization Workflows | +1.4% | North America, with early spillover to Western Europe | Medium term (2-4 years) |

| FDA Expansion Of SIR-Spheres For Unresectable HCC | +1.6% | United States, with spillover into Europe | Short term (≤ 2 years) |

| Guideline Mainstreaming Of Prostate Artery Embolization | +1.3% | North America and Europe, with early gains in Japan and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Liver Cancer and Embolization Case Volumes

The embolization particle market is closely tied to liver cancer incidence because transarterial therapies remain central for patients who present beyond the surgical window. Global liver cancer cases rose 26% between 2010 and 2021 to 529,202, and hepatocellular carcinoma accounted for 80% to 85% of that burden, which directly supports higher use of embolization in unresectable disease.[1]En Ying Tan et al., “Liver Cancer in 2021: Global Burden of Disease Study,” Journal of Hepatology, sciencedirect.com Liver cancer also remains one of the leading causes of cancer death worldwide, and its absolute burden continues to rise with aging populations even where age-standardized rates have stabilized or declined. China remains especially important because national clinical literature states that 64% of HCC patients are diagnosed at intermediate to advanced stages, where TACE is recommended as first-line treatment for CNLC IIb and IIIa disease. A second demand stream comes from liver metastases, since colorectal cancer continues to generate a large pool of patients who may later require embolization-based control of hepatic lesions.

Advances in Radiopaque, Calibrated, and Drug-Eluting Particles

The embolization particle market is also moving forward because product design is becoming more precise in how particles are visualized, distributed, and loaded with therapy. A 32-study meta-analysis covering 4,367 HCC patients found that DEB-TACE improved overall survival by 3.54 months and progression-free survival by 3.07 months versus conventional TACE, which supports continued clinical conversion toward drug-eluting platforms. Boston Scientific’s DC Bead LUMI and LC Bead LUMI introduced inherent radiopacity through covalently bound iodine, which allows physicians to visualize particle delivery through CT, fluoroscopy, and cone-beam CT during the procedure itself.[2]Boston Scientific, “DC Bead LUMI Radiopaque Microsphere,” Boston Scientific, bostonscientific.com A parallel development came from absorbable microspheres made with hyaluronic acid and microfluidic manufacturing, which showed vessel-adaptive adhesion and more than 90% degradation within 2 months in preclinical models, pointing to broader future use where permanent occlusion is not preferred. Better particle uniformity is also improving procedural predictability, which matters to hospitals because more precise endpoint control can limit waste, reduce repeat intervention risk, and strengthen the clinical case for premium embolics.

FDA Expansion of SIR-Spheres for Unresectable HCC

The embolization particle market gained a major regulatory lift when the FDA approved SIR-Spheres Y-90 resin microspheres for unresectable HCC in July 2025. The approval was based on the DOORwaY90 study, which reported a 98.5% overall response rate and 100% local tumor control in 65 HCC patients treated across 18 U.S. centers. Follow-up results presented in 2026 showed a 90% complete response rate, a 99% overall response rate, and durable local control with stable liver function in more than 95% of patients, which reinforced physician confidence in the platform. The commercial effect goes beyond label expansion because the DOORwaY90 protocol centered on personalized dosimetry, and that shifts more value toward particles that support precision planning and standardized dose delivery. It also raises the bar for competitors because hospitals and referral centers increasingly prefer products backed by pivotal data, training support, and workflow familiarity rather than products that compete mainly on price.

Guideline Mainstreaming of Prostate Artery Embolization for BPH/LUTS

The embolization particle market is widening beyond oncology because prostate artery embolization now has clearer clinical standing in lower urinary tract symptom management. The American Urological Association guideline includes PAE as a conditional recommendation for LUTS attributed to BPH and specifies 300 to 500 µm microspheres, which turns guideline language into direct product criteria for procedural use.[3]American Urological Association, “Management of Lower Urinary Tract Symptoms Attributed to Benign Prostatic Hyperplasia: AUA Guideline,” American Urological Association, auanet.org That support matters because PAE is increasingly discussed as an option for patients who want symptom relief with a lower risk of ejaculatory dysfunction than TURP, which expands demand among younger and more preference-sensitive patients. The same procedural logic is beginning to extend into musculoskeletal embolization, where NEXTBIOMEDICAL’s fast-resorbable Nexsphere-F entered pivotal clinical development and later gained Health Canada approval for pain embolization use. As these non-oncology uses grow, suppliers that once depended heavily on liver interventions gain access to broader procedure volumes, more diversified referral sources, and a more balanced revenue mix across the embolization particle market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure Costs And Uneven Reimbursement | -1.2% | Global, with the strongest effect in emerging markets and in the United States for advanced radioembolization | Medium term (2-4 years) |

| Stringent Regulatory And Evidence Requirements | -0.9% | Global, across FDA, EU MDR, and national approval pathways | Long term (≥ 4 years) |

| Interventional Radiology Workforce Shortages | -0.8% | North America, Europe, and emerging markets with limited specialist density | Long term (≥ 4 years) |

| Tariff-Driven Supply Chain And Input Cost Volatility | -0.7% | United States and global manufacturers with cross-border sourcing exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure Costs and Uneven Reimbursement

The embolization particle market still faces meaningful friction from cost because advanced embolization procedures require expensive consumables, trained teams, imaging support, and, in the case of Y-90, complex planning steps. A time-driven activity-based costing study of 123 uterine artery embolization procedures found that embolic agents represented 51% of consumable costs, which made them the single largest cost component in the case bundle. That kind of cost profile pushes hospitals and value-analysis committees to ask whether premium-calibrated or radiopaque particles can reduce procedure time, repeat use, or downstream complications enough to justify higher prices. Reimbursement remains uneven across settings and indications, which can delay adoption even when physicians support the clinical case for embolization. This is why established products with stronger real-world evidence, longer registries, and clearer coding support often displace newer entrants that lack the same economic proof package.

Interventional Radiology Workforce Shortages

The embolization particle market is also limited by specialist capacity because procedure growth depends on trained interventional radiologists, dedicated staff, and imaging-equipped suites. The Royal College of Radiologists reported a 30% shortfall in U.K. clinical radiologists in its 2023 census, and it projected that the shortfall could widen to 40% by 2028 if workforce expansion does not improve. Short staffing creates a direct constraint on embolization throughput because even where product availability is adequate, referral backlog, limited room time, and delayed multidisciplinary coordination reduce the number of treatable cases. It also slows the adoption of newer workflows such as outpatient oncology embolization and personalized dosimetry, since these models need protocol discipline and experienced operators. As a result, procedure demand in the embolization particle market is not converted evenly into revenue, and suppliers remain dependent on concentrated centers of excellence for a large share of advanced case volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Radioembolization Leads, Drug-Eluting Beads Accelerate

Radioembolization spheres held the largest share at 36.93% in 2025, which gave this category the leading revenue position in the embolization particle market. This lead reflects the established place of Y-90 therapies in liver cancer care, especially in centers that already have dosimetry expertise, nuclear pharmacy access, and multidisciplinary oncology workflows. The July 2025 FDA approval of SIR-Spheres for unresectable HCC widened the resin microsphere opportunity, while TheraSphere continued to support the glass microsphere base in high-acuity programs. The combination of these two platforms gives hospitals more treatment flexibility and supports continued physician training across both established and expanding radioembolization programs.

Drug-eluting beads are forecast to grow at a 12.84% CAGR through 2031, making them the fastest-expanding product type in the embolization particle market. Their momentum is linked to stronger comparative evidence, since a meta-analysis of 4,367 HCC patients found that DEB-TACE improved both overall survival and progression-free survival versus conventional TACE. A randomized clinical trial in HCC with portal vein tumor thrombus also reported median overall survival of 12 months with CalliSphere 100 to 300 µm beads versus 7 months with conventional TACE. Embolic microspheres, PVA particles, and gelatin sponge still hold durable roles in fibroid embolization, hemorrhage control, and pre-operative devascularization, which keeps innovation in the embolization particle industry spread across several procedural niches rather than concentrated in one format.

By Embolic Material: Synthetic Materials Dominant, Natural Materials Gaining Ground

Synthetic materials commanded 56.16% share in 2025, which placed them at the center of the embolization particle market across oncology and vascular intervention. Their lead comes from the long clinical history of PVA, acrylic, PMMA, PEG hydrogel, resin, and glass platforms, all of which offer predictable sizing, controlled delivery, and familiar handling in microcatheter-based procedures. Synthetic particles also benefit from stronger post-market datasets, which give regulators and hospital committees more confidence when these products are considered for wider protocol adoption. In practice, this means suppliers with standardized synthetic platforms are better placed to support repeat purchasing, physician preference, and multi-indication use.

Natural materials are projected to grow at a 12.39% CAGR through 2031, reflecting rising interest in temporary occlusion and repeat-procedure flexibility within the embolization particle market. Instylla’s Tembo Embolic System received FDA 510(k) clearance in January 2025 as a bioresorbable dry gelatin particle for hypervascular tumor and peripheral vascular embolization, which gave this part of the category a clearer commercial foothold in the United States. The appeal of gelatin and starch-based materials is strongest where recanalization can be clinically useful, such as selected gynecologic, musculoskeletal, or staged embolization settings. Even so, the embolization particle industry is likely to remain synthetic-heavy over the medium term because permanent and calibrated platforms still align more closely with the needs of high-volume oncology practice.

By Mode of Action: Permanent Embolics Lead While Resorbable Agents Challenge

Permanent embolization agents held a 63.69% share in 2025, which kept them firmly in the lead across the embolization particle market. Their position reflects the needs of tumor-directed treatment, where the therapeutic goal is often durable vascular shutdown rather than temporary modulation. This clinical logic remains strongest in hepatic oncology, where durable response data continue to support products designed for lasting occlusion and long tumor control windows. The 12-month DOORwaY90 results, which showed sustained local control and preserved liver function, reinforced the preference for permanent embolic strategies in advanced liver-directed care.

Temporary and resorbable agents are expected to expand at a 13.82% CAGR through 2031, making them the fastest-growing mode of action in the embolization particle market. Their growth is being driven by applications where physicians want targeted effects without leaving a lasting implant, particularly in pain embolization, fertility-aware procedures, and repeat-treatment settings. NEXTBIOMEDICAL secured FDA Breakthrough Device Designation for Nexsphere-F in March 2025 and later received Health Canada approval in January 2026, which strengthened the commercial and regulatory visibility of fast-resorbable embolics. That pattern suggests resorbable technologies will keep challenging conventional practice in procedures where repeat access, tissue preservation, and lower long-term foreign-body exposure matter more than permanent vessel closure.

By Application: Oncology Anchors Revenue While Urology Scales Fast

Oncology held the largest share at 42.71% in 2025, which made it the core demand center for the embolization particle market. This dominance comes from the long-standing role of TACE and radioembolization in hepatocellular carcinoma, where embolization remains deeply embedded in treatment algorithms for unresectable disease. Japan’s updated HCC Clinical Practice Guidelines 2025 devoted dedicated attention to TA(C)E, including embolic material selection and imaging evaluation, which shows how central embolization remains in formal cancer management pathways. Oncology use is also broadening beyond HCC into liver metastases, neuroendocrine tumors, renal tumors, and pre-operative devascularization, which gives the embolization particle market a wide procedural base even within one application group.

Urology is the fastest-growing application at a 15.64% CAGR through 2031, reflecting a structural expansion beyond the liver-focused base of the embolization particle market. The AUA guideline support for PAE has clarified patient selection and particle sizing, which helps move the procedure from specialized centers into broader referral conversations with urologists. This matters because PAE brings embolization into a high-volume benign disease setting, where demand is less tied to oncology bed capacity and more tied to patient preference, symptom relief, and outpatient workflow. Gynecology, neurology, peripheral vascular disease, and hemorrhage control still contribute meaningful volume, but the newer non-oncology expansion path is what most clearly widens the long-term addressable base of the embolization particle industry.

By End User: Hospitals Dominate While Ambulatory Surgical Centers Accelerate

Hospitals held 53.88% of the end-user share in 2025, which kept them as the main care setting in the embolization particle market. Their lead is structural because complex oncology cases, Y-90 planning, nuclear pharmacy coordination, and post-procedure monitoring still sit most comfortably within hospital infrastructure. For high-acuity liver-directed treatment, hospitals remain better equipped to manage multidisciplinary coordination, mapping scans, radiation handling, and emergency backup if complications occur. This concentration means hospital purchasing committees still play a defining role in which embolization platforms gain broad access and long-term protocol inclusion.

Ambulatory surgical centers are forecast to grow at a 14.32% CAGR through 2031, making them the fastest-expanding end-user channel in the embolization particle market. Migration is strongest in procedures such as uterine fibroid embolization, prostate artery embolization, and selected peripheral embolization cases, where recovery times are shorter, and admission is often avoidable. A freestanding ambulatory surgery center series showed that oncologic interventional radiology procedures could be performed safely in carefully selected patients, while 2025 reimbursement schedules also supported the financial case for outpatient migration. Specialty clinics remain smaller, but they are gaining relevance in elective procedures where simple logistics, repeat visits, and patient convenience matter more than hospital-level support.

Geography Analysis

North America held 36.05% of global revenue in 2025, and the embolization particle market in the region remained the largest worldwide. The United States anchors this lead because it has both established radioembolization infrastructure and high-volume interventional radiology practices that can support advanced oncologic procedures. The July 2025 FDA approval of SIR-Spheres for unresectable HCC widened physician choice and strengthened the commercial position of Y-90 therapy in liver-directed care. Outpatient migration is also more advanced here, with 85% of North American radioembolization procedures performed as outpatient cases versus 13% in Europe, which helps volume growth without matching hospital bed expansion. Canada and Mexico remain smaller, but both benefit from growing tertiary care capability and referral pathways that gradually widen access to embolization procedures.

Europe is a mature region, and the embolization particle market there is shaped more by evidence-led adoption than by abrupt volume surges. Germany, the United Kingdom, France, Italy, and Spain continue to anchor regional demand through dense specialist networks and active interventional oncology practice. A global survey found that 84% of European sites used personalized dosimetry for radioembolization versus 71% in North America, which favors suppliers that can support software integration, imaging alignment, and training depth. EU MDR requirements also place heavier post-market evidence demands on suppliers, which tends to support larger manufacturers with established clinical registries and stronger regulatory teams.

Asia-Pacific is the fastest-growing region, with the embolization particle market forecast to expand at a 15.36% CAGR through 2031. China remains central because liver cancer burden is high and national clinical literature recommends TACE as first-line treatment for CNLC IIb and IIIa disease, where surgery is not feasible. Japan supports stable procedural demand through its updated 2025 HCC guidance and reimbursement recognition for DC Bead in arterial chemoembolization. Middle East and Africa and South America are smaller today, but rising tertiary care investment, medical tourism, and local commercialization efforts still support long-term expansion across these emerging regions.

Competitive Landscape

The embolization particle market is moderately consolidated at the top, with Boston Scientific, Sirtex Medical, Merit Medical, Terumo, and Cook Medical holding the strongest global positions through broad portfolios, clinical training networks, and multi-indication reach. Boston Scientific continues to benefit from the integration of former BTG assets and from radiopaque bead technology that strengthens procedure visualization and quality assurance during embolization. Sirtex remains one of the most visible competitors in radioembolization after the U.S. approval of SIR-Spheres for unresectable HCC and the publication of strong follow-up response data. Merit Medical and Terumo maintain relevance because they serve widely used embolic categories that fit established hospital protocols and physician familiarity. This leaves competition in the embolization particle market centered on evidence quality, workflow fit, and platform trust rather than on short-term price competition alone.

Emerging companies are shaping the embolization particle market through targeted innovation rather than broad portfolio competition. ABK Biomedical advanced Eye90 through FDA IDE Stage 2 approval for the ROUTE90 pivotal study, which positions CT-imageable Y-90 glass microspheres as a direct attempt to simplify visualization and reduce dependence on separate post-procedure imaging steps. Instylla gained FDA PMA for Embrace in August 2025, giving it a differentiated position in liquid embolics for peripheral hypervascular tumors. NEXTBIOMEDICAL has built a distinct place around fast-resorbable embolics through Breakthrough Device recognition and Health Canada approval, which gives it a visible early lead in musculoskeletal pain embolization.

Strategic moves in the embolization particle market show that scale now depends as much on execution as on product novelty. ABK Biomedical strengthened its commercial readiness in 2026 through a long-term manufacturing partnership with COR Development and a radioisotope activation supply partnership with the University of Missouri Research Reactor, both of which support future Eye90 scale-up. Instylla expanded from temporary embolization into a PMA-cleared hydrogel platform, which shows a deliberate move from niche access toward broader oncology relevance. Sirtex, ABK, and NEXTBIOMEDICAL all show that the next competitive cycle will favor companies that combine regulatory progress, manufacturing preparedness, and procedure-level differentiation rather than those that rely on a narrow product claim alone.

Embolization Particle Industry Leaders

Boston Scientific Corporation

Cook Medical LLC

Instylla, Inc.

Medtronic plc

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ABK Biomedical partners with COR Development to establish a long-term commercial manufacturing facility for Eye90 microspheres in Ashland, Missouri, building commercial-scale supply chain infrastructure ahead of anticipated FDA approval.

- April 2026: Sirtex Medical announces 12-month DOORwaY90 results at

- SIR 2026: 90% complete response, 99% overall response, 100% local tumor control, and 95%+ stable liver function maintained in Y-90 resin microsphere-treated unresectable HCC patients

- March 2026: ABK Biomedical partners with University of Missouri Research Reactor (MURR) for long-term radioisotope activation supply supporting Eye90 Y-90 glass microspheres cancer therapy program.

- January 2026: NEXTBIOMEDICAL receives Health Canada approval for Nexsphere-F for musculoskeletal pain embolization, enabling commercial entry into the Canadian market and underscoring regulatory momentum ahead of the U.S. RESORB pivotal trial.

Global Embolization Particle Market Report Scope

The embolization particle market comprises the medical devices, materials, and technologies used to deliberately block or restrict blood flow in targeted blood vessels.

The embolization particle market is segmented across several dimensions that reflect the diversity of products and clinical applications. By product type, it includes radioembolization spheres, drug-eluting beads, embolic microspheres, polyvinyl alcohol (PVA) particles, and gelfoam/gelatin sponge. In terms of embolic material, the market is divided into synthetic and natural categories. The mode of action is further classified into permanent and temporary/resorbable solutions. By application, embolization particles are used in oncology, urology, gynecology, neurology, and peripheral vascular disease. The end users include hospitals, ambulatory surgical centers (ASCs), and specialty clinics. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, Middle East & Africa (MEA), and South America. Forecasts are provided in terms of market value (USD), highlighting the expected financial trajectory of this therapeutic segment.

| Radioembolization Spheres | Resin Microspheres |

| Glass Microspheres | |

| Drug-Eluting Beads | Doxorubicin-Loadable Beads |

| Irinotecan-Loadable Beads | |

| Other Drug-Loadable Beads | |

| Embolic Microspheres | Trisacryl Gelatin Microspheres |

| PEG / Hydrogel Microspheres | |

| Acrylic / PMMA-Based Microspheres | |

| PVA Particles | |

| Gelfoam / Gelatin Sponge Particles |

| Synthetic Materials | Polyvinyl Alcohol |

| Acrylic / PMMA | |

| PEG / Hydrogel | |

| Resin / Glass / Ceramic | |

| Natural Materials | Gelatin |

| Starch-Based |

| Permanent |

| Temporary / Resorbable |

| Oncology |

| Urology |

| Gynecology |

| Neurology |

| Peripheral Vascular Disease and Hemorrhage Control |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Radioembolization Spheres | Resin Microspheres |

| Glass Microspheres | ||

| Drug-Eluting Beads | Doxorubicin-Loadable Beads | |

| Irinotecan-Loadable Beads | ||

| Other Drug-Loadable Beads | ||

| Embolic Microspheres | Trisacryl Gelatin Microspheres | |

| PEG / Hydrogel Microspheres | ||

| Acrylic / PMMA-Based Microspheres | ||

| PVA Particles | ||

| Gelfoam / Gelatin Sponge Particles | ||

| By Embolic Material | Synthetic Materials | Polyvinyl Alcohol |

| Acrylic / PMMA | ||

| PEG / Hydrogel | ||

| Resin / Glass / Ceramic | ||

| Natural Materials | Gelatin | |

| Starch-Based | ||

| By Mode of Action | Permanent | |

| Temporary / Resorbable | ||

| By Application | Oncology | |

| Urology | ||

| Gynecology | ||

| Neurology | ||

| Peripheral Vascular Disease and Hemorrhage Control | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast for embolization particles through 2031?

The space is projected to grow from USD 2.42 billion in 2026 to USD 4.15 billion by 2031 at an 11.41% CAGR, supported by rising liver cancer cases, wider PAE adoption, and stronger outpatient use.

Which product category currently leads revenue?

Radioembolization spheres led in 2025 with a 36.93% share, helped by the established role of Y-90 therapies in liver-directed oncology care.

Which application is expanding the fastest?

Urology is the fastest-growing application at a 15.64% CAGR through 2031, driven mainly by broader acceptance of prostate artery embolization for BPH and LUTS.

Why are drug-eluting beads gaining traction?

Their uptake is supported by comparative evidence showing better survival outcomes than conventional TACE in HCC, which makes them the fastest-growing product segment at a 12.84% CAGR.

Why do hospitals still dominate procedure volume?

Hospitals held 53.88% of end-user share in 2025 because Y-90 workflows, nuclear pharmacy coordination, and complex oncology cases still require hospital-level infrastructure.

Page last updated on: