Transcatheter Embolization And Occlusion Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

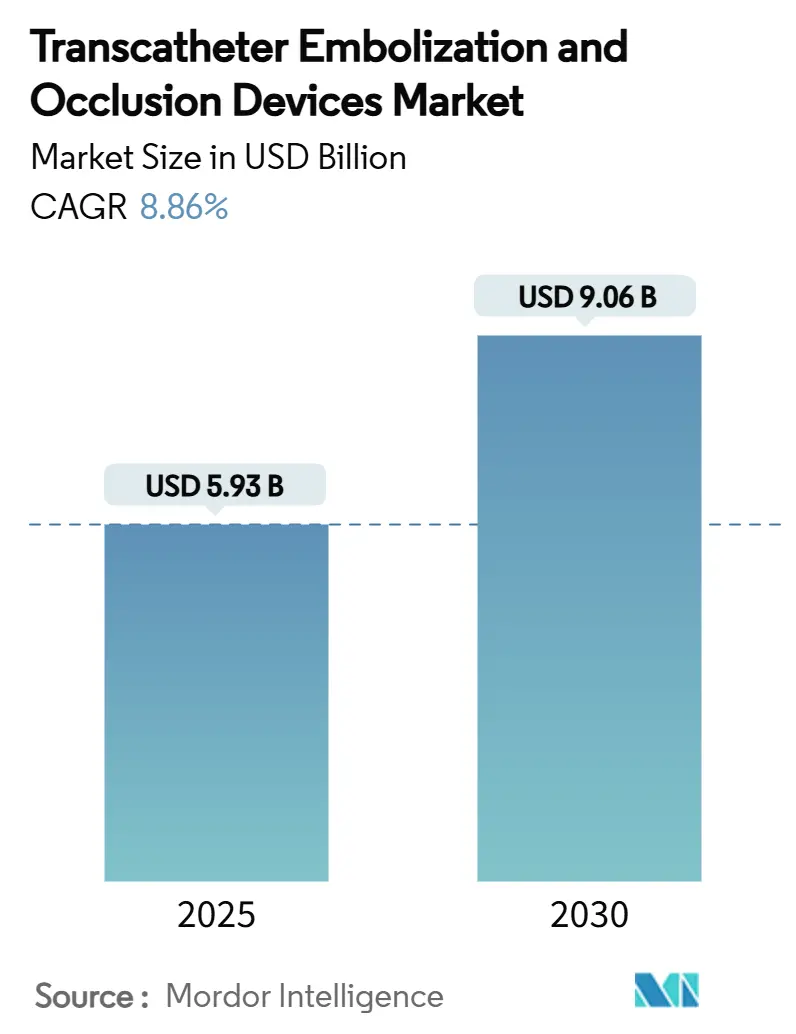

| Market Size (2025) | USD 5.93 Billion |

| Market Size (2030) | USD 9.06 Billion |

| Growth Rate (2025 - 2030) | 8.86% CAGR |

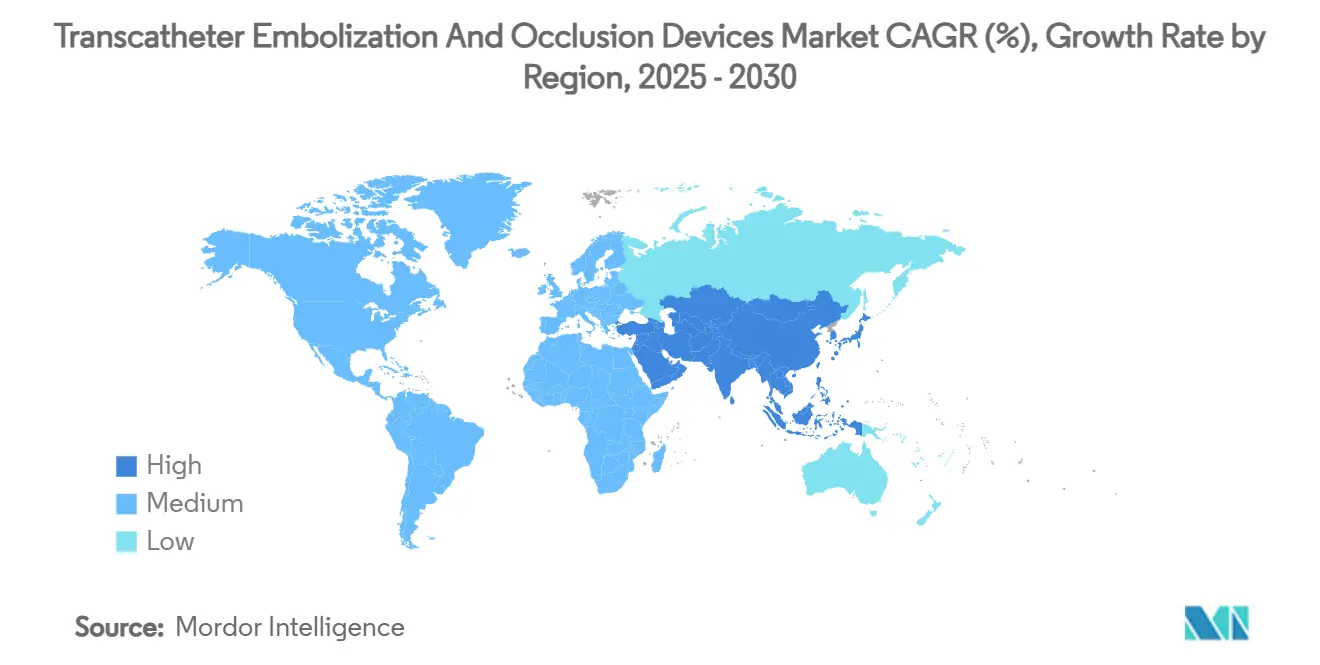

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Transcatheter Embolization And Occlusion Devices Market Analysis by Mordor Intelligence

The transcatheter embolization and occlusion devices market size stands at USD 5.93 billion in 2025 and is projected to reach USD 9.06 billion by 2030, advancing at an 8.86% CAGR. Rising disease prevalence, sustained device innovation, and a decisive shift toward minimally invasive care anchor the growth outlook. Strategic acquisitions by leading manufacturers underline the importance of scale, while policy reforms in major markets sustain reimbursement confidence. North American procedure volumes remain robust, yet Asia-Pacific leads future expansion as hospitals upgrade interventional radiology suites. Sustainability considerations, including bio-resorbable polymers, create fresh differentiation opportunities and support premium pricing in mature economies.

Key Report Takeaways

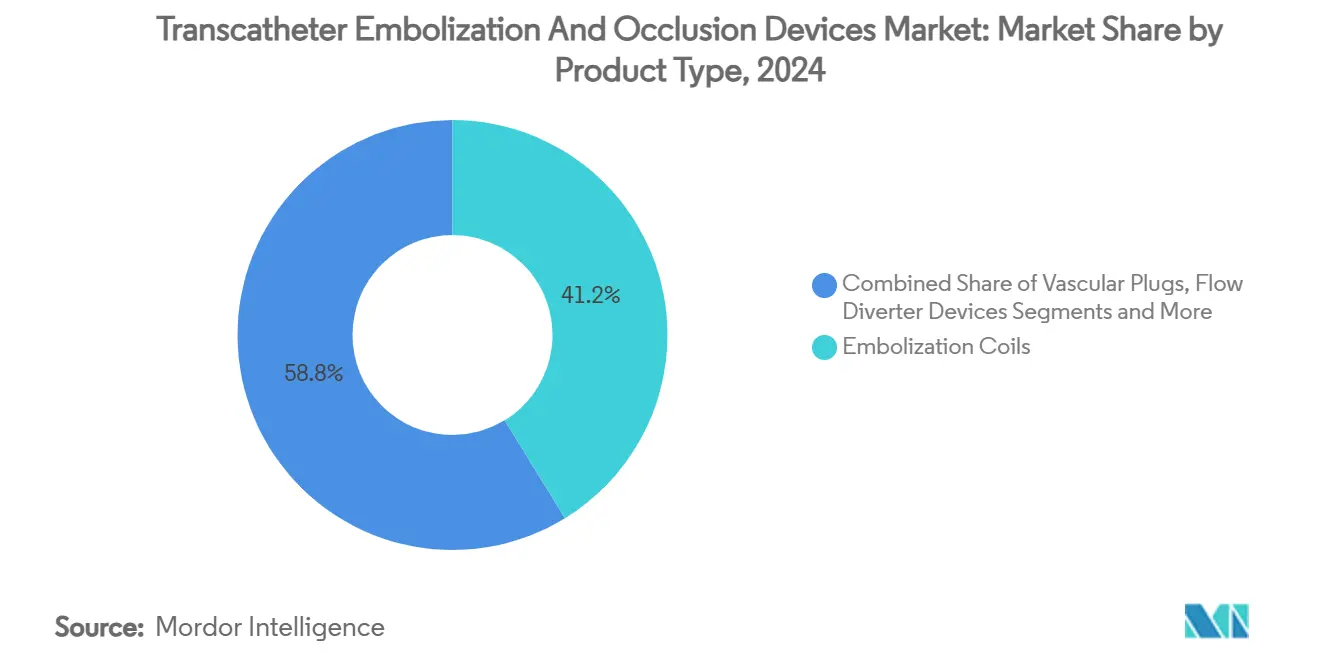

- By product category, embolization coils led with a 41.24% revenue share in 2024, while liquid embolic agents are advancing at a 12.33% CAGR through 2030.

- By application, peripheral vascular disease accounted for 36.34% of the transcatheter embolization and occlusion devices market share in 2024 and oncology is expanding at an 11.69% CAGR to 2030.

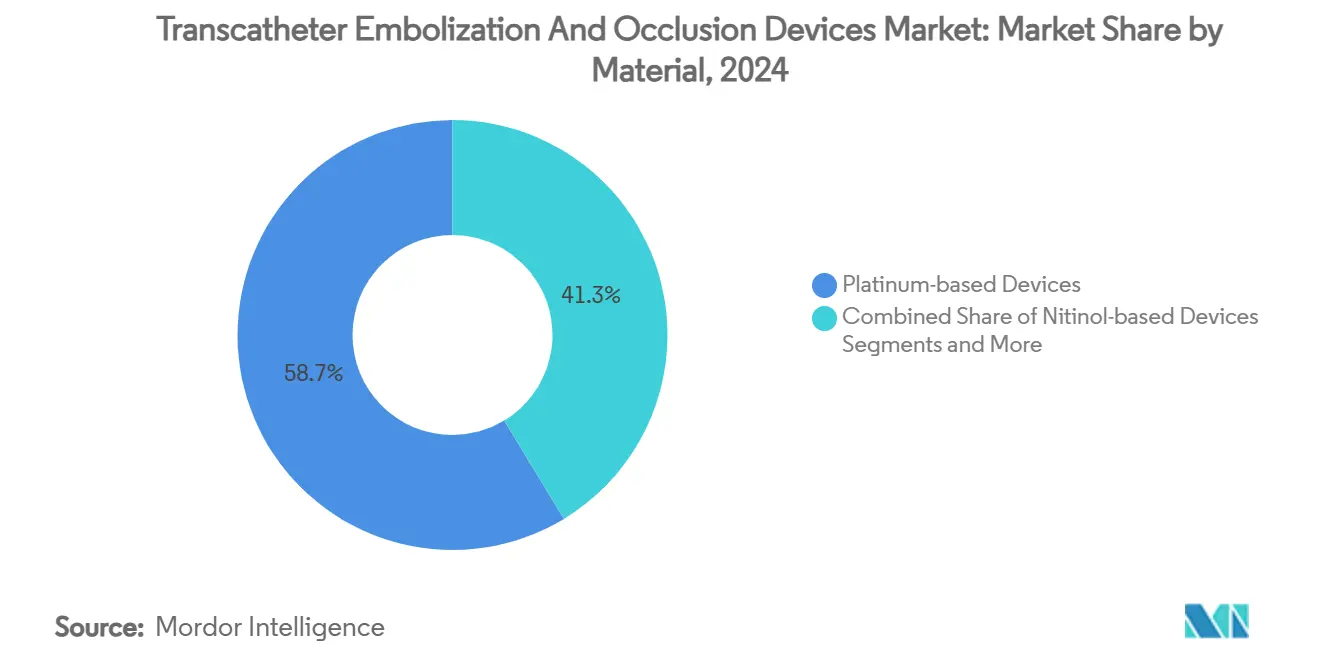

- By material composition, platinum-based devices held 58.67% share in 2024; bio-resorbable polymers are growing at an 11.89% CAGR.

- By end user, hospitals commanded 61.32% of the transcatheter embolization and occlusion devices market size in 2024, whereas ambulatory surgical centers are expanding at a 10.33% CAGR through 2030.

- By geography, North America retained 33.74% share in 2024, yet Asia-Pacific is forecast to post a 10.66% CAGR to 2030.

Global Transcatheter Embolization And Occlusion Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence Of Peripheral & Neurovascular Diseases | + 1.2% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Continuous Device Innovations (Hydrogel Coils, Plugs, Liquid Embolics) | + 1.8% | Global, led by North America & Europe | Long term (≥ 4 years) |

| Favorable Reimbursement & Approvals In Major Markets | + 1.5% | North America & Europe primarily | Short term (≤ 2 years) |

| Outpatient Prostate Artery Embolization Adoption | + 0.9% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Emergence Of Bio-Resorbable / 3-D Printed Occlusion Devices | + 0.6% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| AI-Assisted Catheter Navigation Improving Access | + 0.4% | North America & Europe initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Peripheral and Neurovascular Diseases

Venous thromboembolism affects up to 900,000 people each year in the United States, sustaining demand for advanced occlusion technologies. Aging populations and rising diabetes rates accelerate arterial disease progression, widening the procedural pool for the transcatheter embolization and occlusion devices market. Improved diagnostic imaging uncovers aneurysms earlier, while high occlusion rates of 81.7% achieved by the Pipeline Vantage Flow Diverter validate contemporary device efficacy.[1]Laetitia de Villiers et al., “Initial Experience With Fourth Generation Pipeline Vantage Flow Diverter,” Journal of NeuroInterventional Surgery, jnis.bmj.comThese epidemiologic and clinical dynamics underpin sustained volume growth across high-income and emerging regions alike. Hospitals prioritize embolic technologies that shorten procedure time and limit retreatment, reinforcing purchasing momentum. Combined, these factors support long-term market expansion beyond baseline epidemiologic curves.

Continuous Device Innovations (Hydrogel Coils, Plugs, Liquid Embolics)

Liquid embolic agents post the fastest segment growth at a 12.33% CAGR, reflecting their adaptability in tortuous anatomy and reduced fluoroscopy time. Hydrogel-based coils deliver high packing density, lowering recanalization risk in cerebral aneurysms. MicroVention’s WEB 17 device achieved an 86.5% occlusion rate for ruptured aneurysms in 2024 studies, underscoring performance gains over legacy platinum coils. Bio-resorbable polymers introduce temporary scaffolding without permanent foreign bodies, addressing young patient cohorts who require durable outcomes with limited implant burden. Innovations extend to adjustable flow diverters and shape-memory plugs that conform to irregular vessel morphologies. The technology pipeline therefore deepens clinical confidence, enlarges the addressable case mix, and bolsters premium pricing across the transcatheter embolization and occlusion devices market.

Favorable Reimbursement and Approvals in Major Markets

The Centers for Medicare & Medicaid Services introduced new device pass-through codes in 2024, speeding adoption of next-generation embolics despite an average 2.93% payment rate decrease under the 2025 Physician Fee Schedule. European CE-mark approvals, such as AngioDynamics’ AlphaVac F18 85 System, signal regulatory alignment that shortens commercialization cycles. Accelerated pathways reduce hospital procurement risk and encourage formulary listings. As payers migrate toward value-based care, devices that prove shorter length of stay and low retreatment needs secure favorable coverage determinations. The combination of regulatory agility and reimbursement clarity reinforces early-stage demand and cements a predictable revenue stream for manufacturers.

Emergence of Bio-Resorbable and 3D-Printed Occlusion Devices

Bio-resorbable polymers grow at an 11.89% CAGR, driven by sustainability mandates and demand for implants that disappear post-healing.[2]Yuwei Qiu, “Bronchial Artery Embolization Using Small Particles Is Safe and Effective: A Single-Center 12-Year Experience,” Scientific Reports, pmc.ncbi.nlm.nih.gov Teleflex’s acquisition of BIOTRONIK’s Freesolve scaffold platform underscores industry commitment to degradable solutions that leave no radiopaque residue. Concurrently, 3D-printing enables patient-specific plugs that match vessel geometry, cutting procedure time and contrast load. Early adopters in Europe and North America pursue customized devices for complex congenital anomalies, while emerging markets observe the trend for future adoption. The shift toward eco-responsible designs positions manufacturers to meet forthcoming environmental regulations and physician expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost In Developing Nations | -0.8% | Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Shortage Of Skilled Interventional Specialists | -0.6% | Global, most acute in developing regions | Long term (≥ 4 years) |

| Environmental Concerns Over Radiopaque Micro-Particles | -0.4% | Europe & North America primarily | Long term (≥ 4 years) |

| Supply-Chain Risk For Platinum & Nitinol | -0.3% | Global manufacturing hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device Cost in Developing Nations

Premium pricing for liquid embolics and flow diverters strains budgets in emerging economies where reimbursement is limited. Hospitals in Asia-Pacific and Latin America often restrict purchases to essential coils, delaying adoption of next-generation solutions. Manufacturers experiment with tiered pricing and pared-down kits to gain share, yet the price gap versus traditional surgery remains a hurdle. Currency volatility compounds procurement challenges, prompting bulk-buy agreements to lock in favorable rates. Until economic conditions improve or local production scales up, this restraint tempers the overall growth velocity of the transcatheter embolization and occlusion devices market.

Shortage of Skilled Interventional Specialists

Complex embolization demands deep procedural expertise that remains scarce outside major centers. Training pipelines in many developing regions lag behind demand, capping procedure volumes despite equipment availability. The learning curve for advanced neurovascular devices can span several years, discouraging smaller hospitals from investing in technology. Simulation platforms and vendor-led workshops aim to bridge the gap, yet talent shortages persist, especially in South Asia and Africa. This bottleneck slows penetration of sophisticated devices and limits the addressable market in underserved areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Agents Drive Innovation

The segment generated the largest volume of procedures in 2024, with embolization coils retaining a 41.24% share of the transcatheter embolization and occlusion devices market. Coils remain the default choice for many vascular and neurovascular lesions because of physician familiarity and predictable outcomes. Liquid embolic agents, however, outpace all other categories with a 12.33% CAGR to 2030, buoyed by reduced procedure time and superior vessel penetration. Medtronic’s Onyx HD-500 and Cerenovus Trufill n-BCA systems highlight the performance gains that encourage protocol shifts toward liquids. Flow diverters continue to gain favor in complex aneurysms, while vascular plugs secure rapid closure in peripheral fistulas. Accessories such as micro-catheters and guidewires enjoy steady demand proportional to overall case growth, ensuring recurring revenue lines for suppliers.

Device portfolios diversify further into coil-within-coil architectures, detachable tip designs, and dual-lumen delivery systems that enhance placement accuracy. 3D-printed patient-specific occluders demonstrate early success in pilot studies, especially for congenital malformations. As value-based care spreads, hospitals evaluate total episode cost rather than acquisition price alone, favoring devices that cut fluoroscopy time and minimize retreatment. Market entry barriers for newcomers increase because of intellectual property density and mandatory real-world evidence requirements. Nonetheless, niche innovators carve space with specialized offerings that complement, rather than replace, incumbent solutions, thereby enriching the competitive mosaic of the transcatheter embolization and occlusion devices market.

By Application: Oncology Emerges as Growth Engine

Peripheral vascular disease accounted for 36.34% of procedures in 2024, reflecting entrenched reimbursement and broad physician adoption. Tumor embolization cases rise swiftly, positioning oncology as the fastest-growing application at an 11.69% CAGR through 2030. Balloon-occluded transarterial chemoembolization with Terumo’s Occlusafe system enhances drug deposition in hepatocellular carcinoma, prompting updated clinical protocols. Neurovascular interventions remain technologically intensive, with coated flow diverters such as FRED X achieving 83.6% complete occlusion and reducing anti-platelet regimen duration.

Urology gains momentum as outpatient prostate artery embolization widens access beyond tertiary centers. Trauma and emergency indications provide steady baseline demand that correlates with regional accident rates. Emerging areas, including pelvic venous disorders under Penumbra’s EMBOLIZE study, preview adjacent markets that could add volume over the forecast period. The varied application mix allows suppliers to hedge against cyclical shifts in any single therapeutic area, supporting balanced revenue streams across the transcatheter embolization and occlusion devices market.

By Material Composition: Bio-Resorbable Polymers Gain Momentum

Platinum-based products retained 58.67% share in 2024, yet sustainability imperatives push adoption of degradable alternatives. Bio-resorbable polymers record the highest expansion rate at an 11.89% CAGR, driven by reduced long-term artifact on imaging and elimination of permanent implant. Nitinol maintains relevance through its shape-memory traits essential for flexible plugs in tortuous vessels. Polymer and hydrogel agents enhance viscosity control, allowing tailored flow characteristics for distal embolization. Research into composite materials blends radiopacity with biodegradability, balancing visibility needs with environmental goals. Material innovation therefore reinforces device differentiation and aligns with hospital sustainability charters, anchoring premium tiers within the transcatheter embolization and occlusion devices market.

By End User: Ambulatory Centers Accelerate Growth

Hospitals accounted for 61.32% of 2024 revenue, reflecting their leadership in complex, multidisciplinary procedures. Ambulatory surgical centers, however, grow the fastest at 10.33% CAGR as payers steer volumes toward lower-cost sites of care. Simplified device kits and shorter recovery profiles facilitate adoption in outpatient settings. Specialty clinics focus on neurointerventions and niche vascular services, while academic institutions remain pivotal for early trials and advanced training. Vendors tailor educational programs and inventory solutions to ASC workflows, maximizing procedural throughput and bolstering market penetration in suburban regions. This shift diversifies the facility mix and broadens the reach of the transcatheter embolization and occlusion devices market.

Geography Analysis

North America contributed 33.74% of 2024 revenue, supported by mature reimbursement structures, expansive interventional radiology networks, and rapid clearance pathways under the FDA special controls rule for neurovascular devices.[3]Regulatory Affairs, "21 CFR 882.5950 Neurovascular Embolization Device," U.S. Food and Drug Administration, fda.gov Large acquisitions, such as Stryker's USD 4.9 billion purchase of Inari Medical, reinforce corporate focus on peripheral vascular growth. Ongoing clinical trials, including the Vanguard study of the Pipeline Vantage, further validate technology effectiveness and sustain physician confidence.

Asia-Pacific posts the most aggressive expansion at a 10.66% CAGR, propelled by rising healthcare expenditure, hospital modernization, and regulatory reforms that shorten device approval cycles. China's endorsement of Boston Scientific's FARAPULSE and Japan's proactive neurovascular guidelines highlight growing sophistication in regional care models. India and South Korea invest in training programs that address specialist shortages, while local manufacturing incentives aim to curb import dependence. These initiatives collectively enlarge the installed base of interventional suites and create robust demand across the transcatheter embolization and occlusion devices market.

Europe maintains steady momentum through harmonized CE-mark standards and a strong emphasis on environmental sustainability that favors bio-resorbable materials. Multicenter studies of coated flow diverters report 79% complete occlusion at six months, supporting reimbursement justification. Middle East and Africa witness incremental adoption in tertiary centers, though limited insurance coverage constrains broader uptake. South America, led by Brazil, advances via public–private partnerships that upgrade vascular care infrastructure. Collectively, these geographic trends ensure that while North America remains the revenue anchor, future growth will be geographically diversified across the transcatheter embolization and occlusion devices market.

Competitive Landscape

The market shows moderate consolidation following landmark deals in 2024-2025, including Boston Scientific’s USD 1.26 billion Silk Road Medical acquisition and Teleflex’s EUR 760 million purchase of BIOTRONIK’s vascular portfolio. Top players leverage broad catalogues that span coils, plugs, and flow diverters, allowing bundled tenders that crowd out single-line competitors. Mid-cap firms target technology white spaces such as AI-guided navigation, bio-resorbable scaffolds, and patient-specific 3D-printed devices to secure differentiated footholds.

Regulatory classifications shape strategic planning. The FDA’s Class II designation with special controls raises evidence thresholds that favor incumbents with established clinical datasets. Yet, venture-backed entrants like Jupiter Endovascular, freshly capitalized at USD 21 million for pulmonary embolism trials, demonstrate continued appetite for niche innovation. Partnerships between device firms and software developers accelerate AI deployment, creating ecosystem plays that extend value beyond hardware. Overall, competition centers on delivering demonstrable clinical improvement together with economic value, themes that will intensify as pay-for-performance models expand.

Transcatheter Embolization And Occlusion Devices Industry Leaders

-

Medtronic plc

-

Boston Scientific Corporation

-

Terumo Corporation

-

Abbott Laboratories

-

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex completed the acquisition of BIOTRONIK’s vascular intervention business for EUR 760 million, adding drug-coated balloons and the Freesolve resorbable scaffold to its portfolio.

- June 2025: Penumbra received FDA clearance and launched the Ruby XL coil system, offering the longest and softest detachable coil for large-vessel embolization.

- January 2025: Stryker announced an agreement to acquire Inari Medical for USD 4.9 billion, widening its presence in venous thromboembolism care.

Global Transcatheter Embolization And Occlusion Devices Market Report Scope

| Embolization Coils |

| Embolization Particles / Microspheres |

| Liquid Embolic Agents |

| Vascular Plugs |

| Flow Diverter Devices |

| Coiling-Assist Devices (Balloons/Stents) |

| Accessories (Micro-catheters, Guidewires) |

| Peripheral Vascular Disease |

| Oncology (Tumor Embolization) |

| Neurology (Aneurysm, AVM) |

| Urology (Prostatic Artery Embolization) |

| Trauma & Other Emergencies |

| Platinum-based Devices |

| Nitinol-based Devices |

| Polymer / Hydrogel-based Agents |

| Bio-resorbable Polymers |

| Hospitals |

| Specialty Clinics |

| Ambulatory Surgical Centers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Embolization Coils | |

| Embolization Particles / Microspheres | ||

| Liquid Embolic Agents | ||

| Vascular Plugs | ||

| Flow Diverter Devices | ||

| Coiling-Assist Devices (Balloons/Stents) | ||

| Accessories (Micro-catheters, Guidewires) | ||

| By Application | Peripheral Vascular Disease | |

| Oncology (Tumor Embolization) | ||

| Neurology (Aneurysm, AVM) | ||

| Urology (Prostatic Artery Embolization) | ||

| Trauma & Other Emergencies | ||

| By Material Composition | Platinum-based Devices | |

| Nitinol-based Devices | ||

| Polymer / Hydrogel-based Agents | ||

| Bio-resorbable Polymers | ||

| By End User | Hospitals | |

| Specialty Clinics | ||

| Ambulatory Surgical Centers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current market size of the transcatheter embolization and occlusion devices market?

The market is valued at USD 5.93 billion in 2025 and is projected to reach USD 9.06 billion by 2030, reflecting an 8.86% CAGR.

2. Which product category holds the largest revenue share today?

Embolization coils lead the market with a 41.24% share in 2024, driven by widespread clinical familiarity and proven efficacy.

3. What application segment is expanding the fastest?

Oncology applications are growing at an 11.69% CAGR through 2030 as tumor embolization procedures gain wider acceptance in liver and renal cancers.

4. Which region is forecast to post the highest growth rate?

Asia-Pacific is expected to advance at a 10.66% CAGR to 2030, propelled by rising healthcare spending and rapid expansion of interventional radiology services.

Page last updated on: