Consumer Durable Loans Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 674.69 Billion |

| Market Size (2031) | USD 989.51 Billion |

| Growth Rate (2026 - 2031) | 7.96% CAGR |

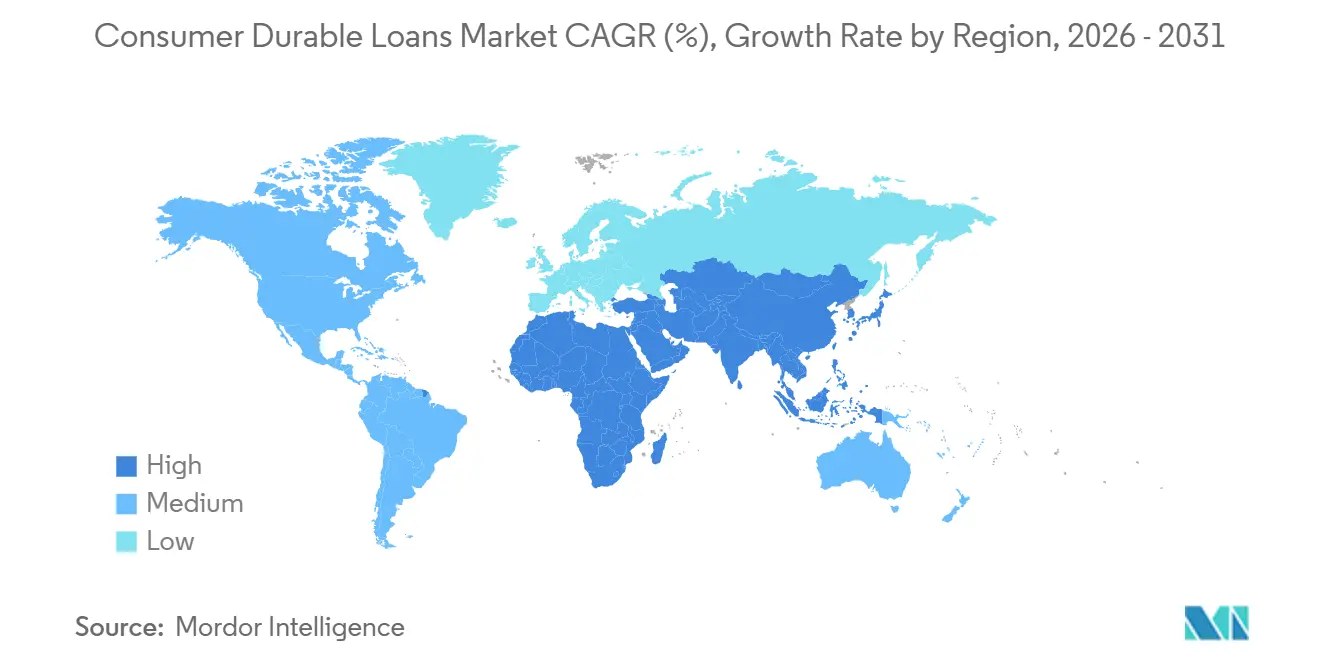

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

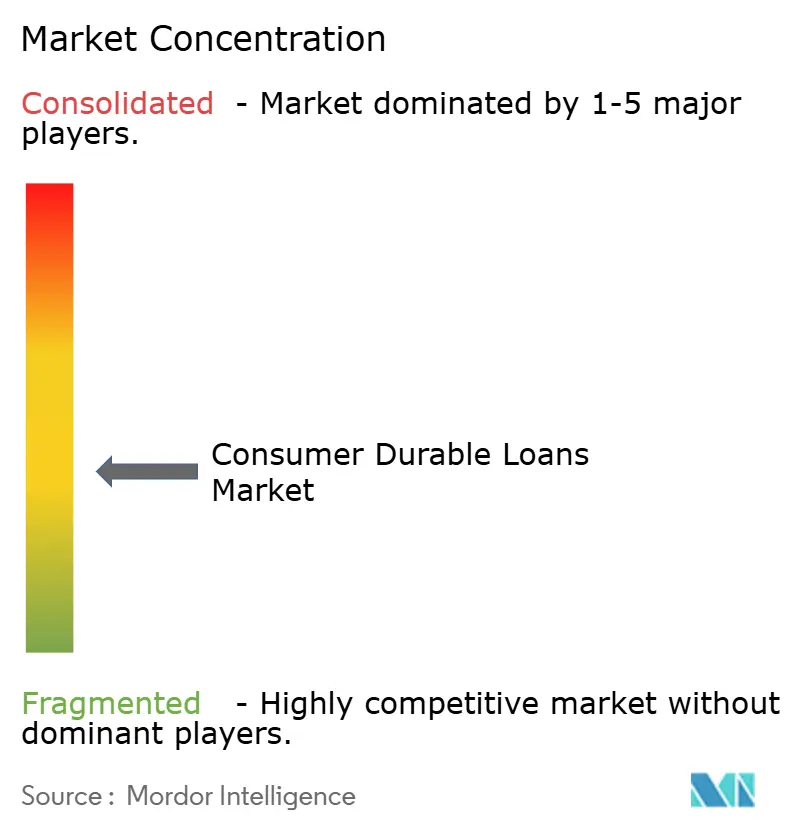

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Consumer Durable Loans Market Analysis by Mordor Intelligence

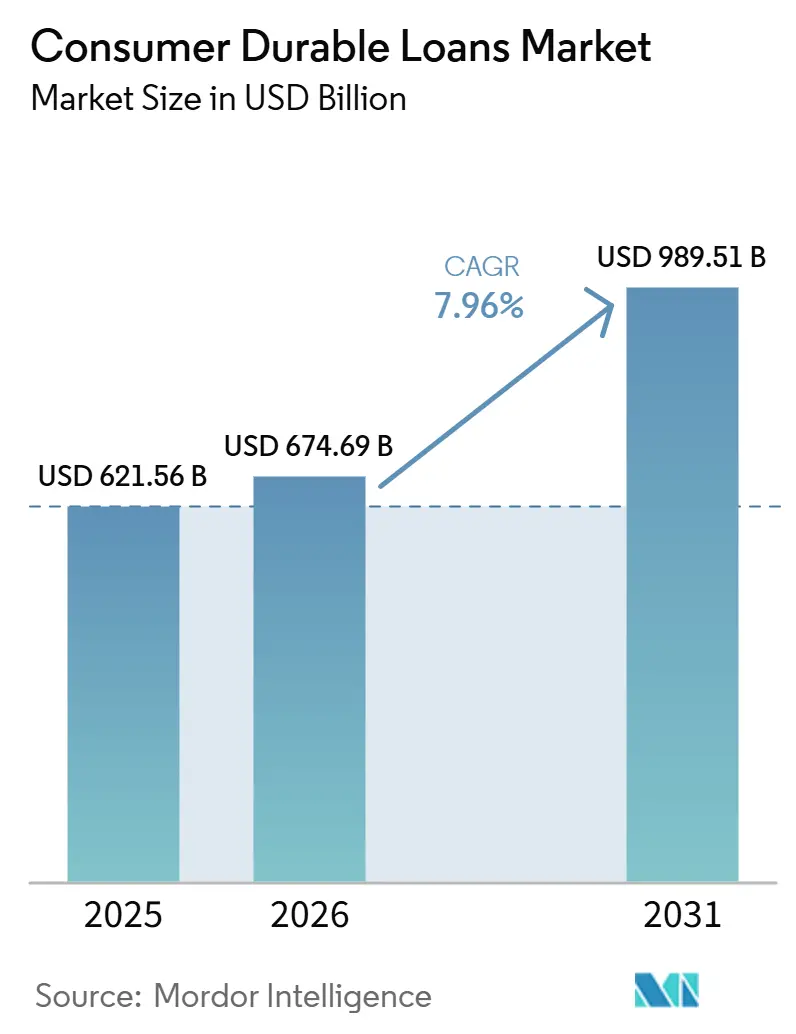

The Consumer Durable Loans Market size was valued at USD 621.56 billion in 2025 and is estimated to grow from USD 674.69 billion in 2026 to reach USD 989.51 billion by 2031, at a CAGR of 7.96% during the forecast period (2026-2031).

The consumer durable loans market is expanding because credit is reaching buyers faster and closer to the point of purchase than in earlier cycles. Embedded finance is reducing drop-off at checkout, and lenders are using those merchant connections to capture demand that earlier approval models often lost. The consumer durable loans market is also benefiting from higher smartphone usage in emerging economies, wider acceptance of installment-based buying across income groups, and retailer interest in higher repeat purchases through financed sales. Regulation and credit performance still matter, but the present structure of the consumer durable loans market rests on replacement demand, broader access to formal credit, and merchant economics that continue to support financed purchases.

Key Report Takeaways

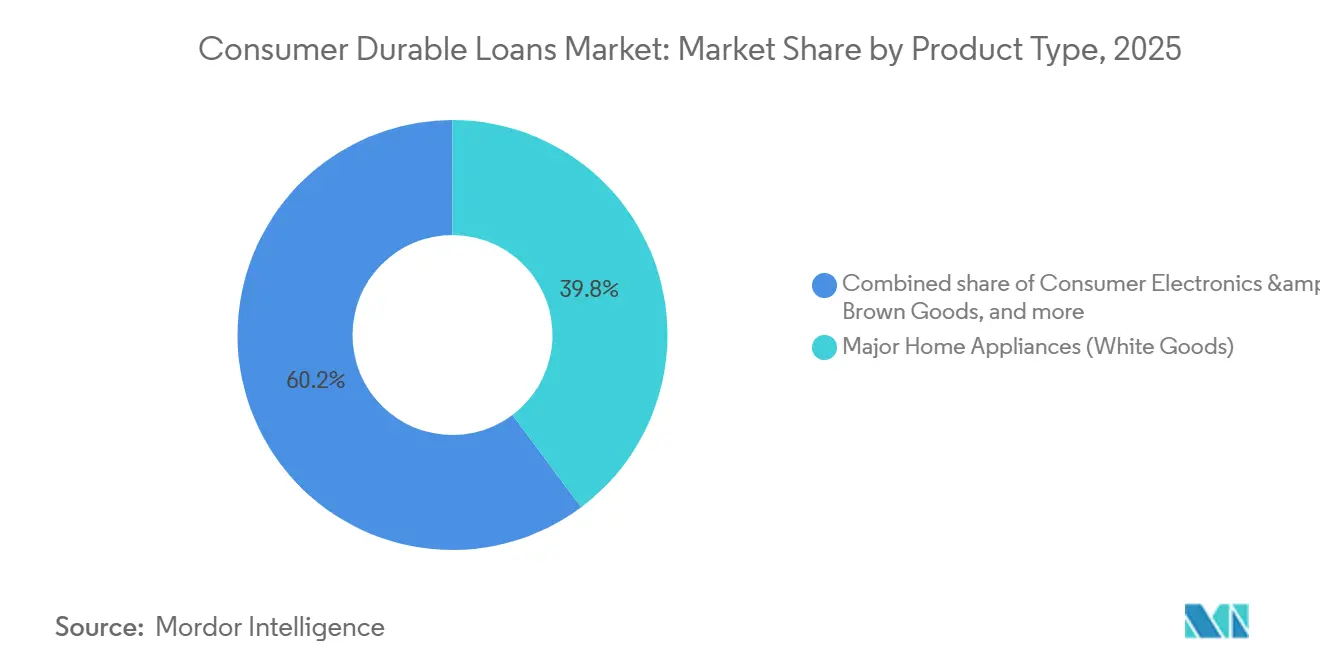

- By product type, major home appliances captured 39.78% of the consumer durable loans market share in 2025, while consumer electronics and brown goods are projected to grow at 9.42% CAGR through 2031.

- By borrower risk profile, prime borrowers accounted for 56.33% of the consumer durable loans market share in 2025, while subprime borrowers are projected to grow at 10.67% CAGR through 2031.

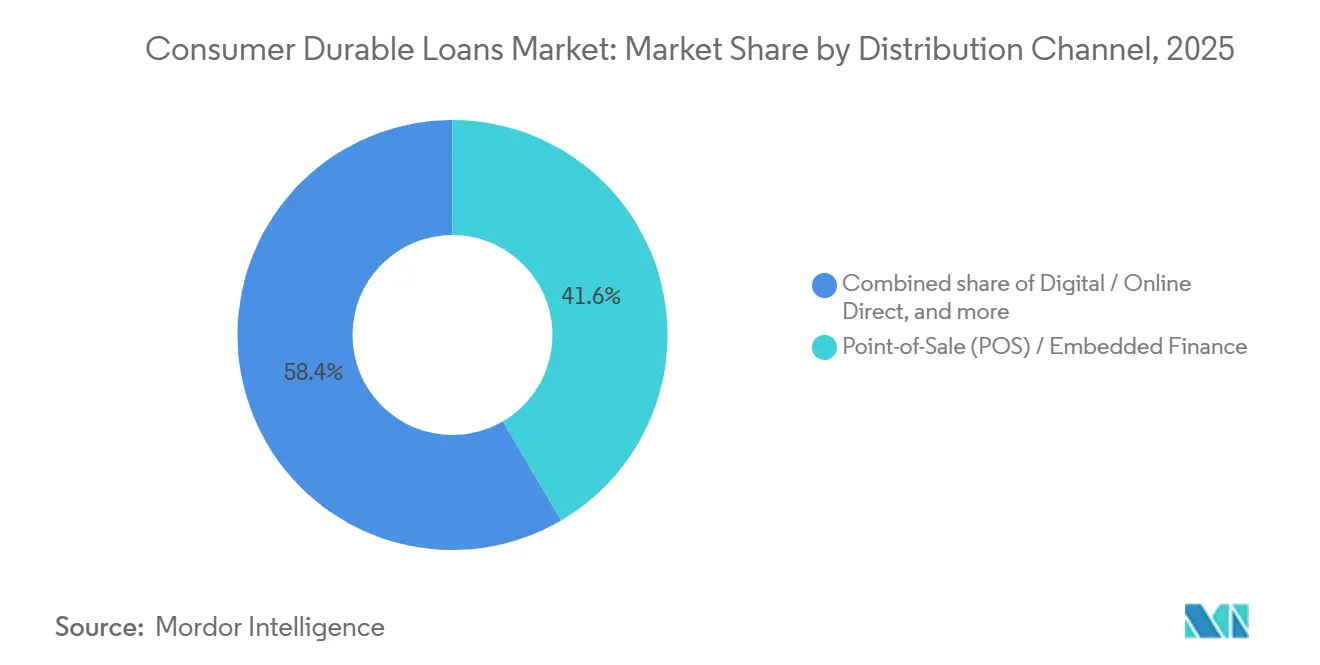

- By distribution channel, point-of-sale and embedded finance captured 41.56% of the consumer durable loans market share in 2025, while digital and online direct is projected to grow at 12.37% CAGR through 2031.

- By lender type, Banks held 46.45% of the consumer durable loans market share in 2025, while fintechs and digital lenders are projected to grow at 13.54% CAGR through 2031.

- By geography, Asia-Pacific captured 48.12% of the consumer durable loans market share in 2025 and is projected to grow at 9.91% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Consumer Durable Loans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Point-Of-Sale Financing Adoption | +2.0% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Zero-Cost EMI Normalization | +1.4% | Asia-Pacific, especially India and Southeast Asia, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Retailer-Lender Embedded Finance Partnerships | +1.3% | Global, strongest in North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Thin-File And Underbanked Borrower Expansion | +1.1% | Asia-Pacific, Middle East and Africa, and South America | Medium term (2-4 years) |

| Appliance And Electronics Replacement Cycles | +0.8% | Global, with stronger impact in North America and Asia-Pacific | Short term (≤ 2 years) |

| AI-Enabled Underwriting And Instant Decisioning | +0.9% | Global, with earlier adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digital Point-of-Sale Financing Adoption

Point-of-sale financing has moved from an optional feature to a normal part of checkout in many retail settings. That shift is supporting faster loan origination in the consumer durable loans market. Merchant demand is now a direct growth lever because financing at checkout helps retailers protect conversion and reduce purchase abandonment. The consumer durable loans market is also widening beyond the largest merchants as more retailers adopt embedded lending models across in-store and online channels. Klarna’s exclusive arrangement with Walmart and OnePay in 2025 shows how deeply installment lending is now built into major retail ecosystems in the United States[1]SEC.GOV https://www.sec.gov/Archives/edgar/data/2003292/000200329225000024/klarnagroupplcf-1a3.htm. Synchrony’s Walmart credit card program and its BNPL expansion with Amazon further show that POS credit is being integrated across multiple product types and checkout paths, which keeps the consumer durable loans market closely tied to retail platform strategy.

Zero-Cost EMI Normalization

Zero-cost EMI has become a standard purchase mechanism in key segments of the consumer durable loans market, especially as premium devices are moving beyond cash affordability for many households. In India, the Reserve Bank of India clarified in 2026 that no loan can truly carry a 0% interest rate. However, the visible borrowing cost is still being absorbed by manufacturers and lenders to preserve demand momentum. That structure is keeping monthly payments central to purchase decisions without weakening the sales message at the point of purchase. Bajaj Finance reported a 45% rise in gadget EMI volumes, and its Insta EMI Card network now spans more than 1.5 lakh partner stores, underscoring how deeply this model is now embedded in retail financing. The consumer durable loans market is therefore seeing a closer link between product marketing budgets and lending activity, as installment subsidies now support volume growth in a direct, repeatable way.

Retailer-Lender Embedded Finance Partnerships

The consumer durable loans market is shifting from lender-led customer acquisition to merchant-led credit origination, altering who controls demand at checkout. Klarna’s March 2025 agreement with Walmart and OnePay made it the exclusive provider of installment financing at Walmart’s United States checkouts, which shows how large retailers are choosing financing partners as part of their commerce stack. In June 2025, Synchrony secured a Walmart credit card program through OnePay and expanded BNPL with Amazon for carts above USD 50, demonstrating that merchant ecosystems can support multiple credit formats simultaneously[2]SYNCHRONY.COM OnePay and Synchrony to Launch New Industry-Leading Credit Card Program With Walmart; Credit Card to Be Powered by Mastercard and Set to Go Live This Fall :: Synchrony Financial (SYF). These partnerships matter because repeat transaction data, merchant integration, and customer retention now carry as much strategic value as the loan product itself. In the consumer durable loans market, this makes retailer access a durable source of competitive advantage rather than a simple referral channel.

Thin-File and Underbanked Borrower Expansion

The consumer durable loans market is expanding because more borrowers with limited conventional credit history are entering formal lending channels. Alternative data tools are helping lenders assess borrowers who were once hard to score, thereby widening the addressable base without relying solely on traditional bureau models. Equifax’s alternative finance scoring offer reflects the growing use of telecom, utility, and other nontraditional data in credit assessment for non-prime segments. TransUnion reported that subprime originations for unsecured personal loans rose 32.5% year over year in Q3 2025, and fintech lenders accounted for 42% of all personal loan originations, suggesting a broader willingness among lenders to serve riskier but still measurable customer groups[3]GLOBENEWSWIRE.COM TransUnion 2026 Originations Forecast Shows Continued. In India, CRIF High Mark showed that NBFC PAR 91-180 improved to 0.44% in March 2026 from 0.65% three months earlier, which supports the view that better targeting and smaller ticket sizes can keep borrower expansion workable for the consumer durable loans market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Tightening On Consumer Credit Disclosure | -1.7% | Global, with stronger effect in North America, the European Union, and India | Medium term (2-4 years) |

| Delinquency Risk In Thin-File Borrower Pools | -1.3% | Global, with higher exposure in South America and Middle East and Africa | Medium term (2-4 years) |

| Funding Cost Sensitivity To High-Rate Cycles | -1.1% | Global, with greater pressure on non-deposit-funded lenders | Short term (≤ 2 years) |

| Digital Origination Fraud And Identity Verification Risk | -0.9% | Global, especially in high-volume digital origination markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Tightening on Consumer Credit Disclosure

Disclosure rules are raising operating costs for lenders in the consumer durable loans market, especially for fintechs and NBFCs that scale across products and geographies. In the United States, the CFPB and the Federal Reserve updated Regulation Z, effective January 1, 2026. They raised the threshold to USD 73,400, which extended disclosure requirements to a larger set of consumer credit and leasing transactions[4]FEDERALRESERVE.GOV Federal Reserve Board - Agencies announce dollar thresholds for applicability of truth in lending and consumer leasing rules for consumer credit and lease transactions. In Europe, the Consumer Credit Directive 2 takes effect in November 2026 and brings BNPL and short-term credit under a stricter and more standardized compliance framework. OECD monitoring across 60 jurisdictions also showed that supervisory actions increased in nearly one-third of jurisdictions between 2024 and 2025, which confirms that digital lending oversight is becoming more active. For the consumer durable loans market, this means firms with established compliance systems are better placed to absorb new rules than smaller lenders with thinner operating capacity.

Delinquency Risk in Thin-File Borrower Pools

Credit quality is a real restraint on the consumer durable loans market because growth in non-prime segments can weaken quickly when underwriting discipline slips. VantageScore reported year-over-year delinquency increases across nearly all credit tiers in August 2025, and TransUnion showed that unsecured personal loan 60+ DPD rose to 3.99% in Q4 2025 from 3.57% a year earlier. The pressure is not uniform, and India presented a more stable picture, with CRIF High Mark recording PAR 31-180, improving to 1.7% in March 2026 from 2.7% a year earlier. The more exposed part of the consumer durable loans market remains high-ticket subprime lending, where thin files, higher device prices, and stretched household budgets can lead to weaker loan vintages. Lenders that combine bureau data with ongoing behavioral monitoring are therefore in a stronger position than those that rely only on static scores at origination.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Appliances Anchor Demand as Electronics Drive Growth

Major home appliances held 39.78% of the consumer durable loan market share in 2025, reflecting the essential nature and higher ticket sizes of refrigerators, washing machines, and air conditioners. These categories remain financing-led because replacement demand usually cannot be delayed for long when a core household appliance fails. Consumer electronics and brown goods are the fastest-growing product segments, forecast to expand at a 9.42% CAGR through 2031, driven by shorter upgrade cycles and higher prices for AI-enabled devices. In the consumer durable loans market, that growth pattern keeps electronics closely tied to installment-based buying because premium smartphones and laptops often exceed cash affordability for many users. The product mix, therefore, combines stable demand from appliances with faster financing velocity in electronics.

Furniture and home furnishings remain a smaller but rising part of the consumer durable loans industry because premium home purchases are increasingly tied to dedicated retail finance programs. Synchrony’s April 2026 launch of the RH credit card shows that high-ticket furnishing purchases are drawing more specialized credit infrastructure from established lending partners. Other consumer durables, including fitness equipment, modular kitchens, and lifestyle products, are also widening the financing pool as merchants extend embedded credit beyond traditional appliance and electronics categories. Samsung’s 2026 exploration of a trade-in financing platform for home appliances points to a future where OEM-led financing could speed up replacement purchases and pull more demand into financed channels. For the consumer durable loans market, this means product expansion is no longer limited to need-based appliances and is increasingly linked to retailer strategy and manufacturer-backed demand creation.

By Borrower Risk Profile: Prime Lending Dominates, Subprime Redefines the Growth Frontier

Prime borrowers accounted for 56.33% of the consumer durable loans market in 2025, which shows that banks and large formal lenders still prefer customers with stronger scores and lower provisioning risk. The consumer durable loans market remains anchored in this segment because prime borrowers can be approved quickly and serviced at a lower risk cost. Subprime borrowers are set to grow at a 10.67% CAGR through 2031. That pace reflects the expansion of fintech underwriting models and broader lender willingness to serve customers outside traditional prime definitions. TransUnion’s data on subprime origination growth in 2025 supports that shift, especially as fintech lenders increased their share of personal loan originations. Near-prime borrowers remain at the midpoint of the risk curve and are increasingly important for lenders seeking growth without moving too far into stressed credit pools.

The subprime opportunity in the consumer durable loans industry is being shaped more by better scoring models than by weaker lending standards. Equifax’s alternative finance scoring approach reflects the wider move toward telecom, utility, and other nontraditional data for decisioning in non-prime lending. Affirm’s 2025 move to report BNPL repayment data to credit bureaus also shows that repayment behavior is being folded more directly into formal scoring pathways, which can improve borrower mobility over time. In the consumer durable loans market, subprime behavior differs from that in other consumer credit categories because ticket sizes are often smaller and loan tenures are shorter. That creates faster feedback on repayment patterns and gives lenders more room to recalibrate underwriting as portfolios season.

By Distribution Channel: POS Finance Holds Scale as Digital Direct Changes Acquisition Economics

Point-of-sale and embedded finance retained 41.56% of the consumer durable loans market in 2025, confirming that financing at checkout remains the largest origination channel for high-ticket household purchases. The consumer durable loans market depends on this channel because it brings loan choice directly into the buying decision and reduces friction between product interest and financing approval. Digital and online direct is the fastest-growing channel. It is projected to expand at a 12.37% CAGR through 2031 as more durable purchases move online and more borrowers manage the full loan process through mobile interfaces. That shift is changing lender competition because speed, prequalification accuracy, and user experience matter more when merchant staff is no longer guiding the transaction. The result is a channel mix where POS retains scale while digital direct takes a larger role in new acquisition.

Intermediated and broker channels remain relevant in parts of the consumer durable loans industry where sales still depend on personal guidance, especially for larger appliance purchases in lower-digitization markets. Physical and branch-based direct also continues to matter for higher-value multi-item purchases and for borrowers who still prefer face-to-face verification. The consumer durable loans market, therefore, remains multi-channel even as digital lending expands. Growth in online direct models is also expanding the lender base, as mid-tier institutions can now access digital origination capabilities that were previously concentrated among large fintechs. This keeps channel competition active across both retail-led financing and app-based direct borrowing.

By Lender Type: Banks Maintain Volume while Fintechs Capture Momentum

Banks held 46.45% of the consumer durable loans market share in 2025, and that lead came from lower funding costs, established underwriting systems, and long-standing customer trust. The consumer durable loans market still routes a large share of prime segment lending through banks because their cost of capital and servicing capacity remain strong. Fintechs and digital lenders are the fastest-growing lender group. They are forecast to expand at a 13.54% CAGR through 2031 as they use alternative data, digital checkout integration, and faster decision-making to win business that banks often serve more slowly. NBFCs are also structurally important, and India showed this clearly when NBFCs accounted for 84.5% of consumer durable loan originations by value in Q4 FY26. Manufacturer captive finance arms remain smaller globally, but they are becoming more relevant as OEMs explore trade-in and upgrade-linked financing.

The structural gap between banks and fintechs in the consumer durable loans industry is clearest in origination speed and business design. SoFi expanded its loan platform business in early 2026 with more than USD 3.6 billion in new loan delivery agreements across three partnerships, demonstrating how digital lenders are increasing scale without taking every loan fully onto their balance sheets. Klarna’s funding and capital market activity points to the same direction, where distribution and financing capacity are being built together rather than separately. In the consumer durable loans market, this gives fintechs more freedom to compete on merchant reach and customer experience rather than only on balance sheet size. Banks still hold scale, but momentum is moving toward lenders that combine funding access with embedded and digital distribution.

Geography Analysis

Asia-Pacific accounted for 48.12% of the consumer durable loans market in 2025 and is also the fastest-growing region, with a 9.91% CAGR through 2031. The consumer durable loans market is strongest in this region because it combines a large middle-income base, rising durable goods prices, and still-expanding formal credit access. China doubled its special bond program to CNY 300 billion (USD 44.16 billion) in 2025 to support appliance replacement and durable goods trade-ins, and consumer durables sales in China are expected to grow 2.5% in 2026. India remains a major growth engine, with the consumer durable loan portfolio outstanding reaching INR 1.0 lakh crore (USD 11,129.8 million) as of March 2026 and FY26 originations reaching INR 1.78 lakh crore (USD 19,811 million), according to CRIF High Mark. The regional picture shows that the consumer durable loans market is moving on both replacement demand and broader credit inclusion, with NBFCs and online lenders gaining more importance in large Asian markets.

North America and Europe represented the next-largest combined base of the consumer durable loans market in 2025, as both regions already had mature credit systems and high ownership of financed household goods. In the United States, Atradius expects a 0.4% contraction in consumer durable sales in 2026, but financed purchases are still rising as households prefer installment structures over full upfront payments. In Europe, regulatory change is becoming a major shaping force, as the Consumer Credit Directive 2 takes effect in November 2026 and extends tighter compliance expectations to BNPL and short-term consumer credit. The consumer durable loans market in these regions is therefore growing more through product format and channel shift than through first-time credit expansion. Open banking and consent-based data access are also supporting the development of more digital credit assessment models across the region.

South America, the Middle East, and Africa accounted for a smaller share of the consumer durable loans market in 2025. However, they remain strategically important because lender penetration is still developing and digital borrowing models are spreading. Brazil leads South America in fintech and NBFC installment lending, while Argentina remains harder to underwrite due to inflation that complicates loan structures and household affordability. In the Middle East, Saudi Arabia and the UAE are leading the adoption of digital lending under more active fintech policy frameworks. South Africa and Egypt remain early-stage markets, but mobile-first financing is enabling broader access for borrowers with limited prior credit history. In the consumer durable loans market, these regions present a mix of near-term risks and longer-term expansion, as the need for household durables remains strong even as formal lending systems are still maturing.

Competitive Landscape

The consumer durable loans market remains moderately concentrated globally, with large banks still commanding major origination volumes, but country-level structures vary widely, with specialist lenders dominating in some local markets. JPMorgan Chase, HSBC, BNP Paribas, and Barclays remain important by scale, while specialized retail credit and embedded finance players are shaping channel competition in faster-growing origination pools. In India, Bajaj Finance held a strong country position, and market reporting showed it accounted for 54% of consumer durable loan disbursements, illustrating how deeply first-mover advantages can lock in when retailer access and financing infrastructure are with the same provider. The consumer durable loans market, therefore, does not follow a single competitive model, as some regions remain bank-led while others are moving toward NBFC- or fintech-heavy structures. That mixed structure is keeping competition active across price, approval speed, merchant integration, and balance-sheet strategy.

Strategic moves in 2025 and 2026 show how leading firms are building both capacity and distribution inside the consumer durable loans market. Klarna completed a USD 1.7 billion Significant Risk Transfer transaction in April 2026 to support more than USD 40 billion in lending capacity, thereby strengthening its ability to scale installment lending without relying solely on retained balance-sheet exposure. Affirm and Fiserv also announced an exclusive collaboration in January 2026 to bring pay-over-time capability to debit card programs for thousands of United States bank and credit union clients, broadening distribution through established financial institutions. Synchrony strengthened its position in high-ticket retail financing through the RH Credit Card and through long-standing retailer relationships that cover more than 70% of Furniture Today’s Top 100 retailers. These moves show that the consumer durable loans market is being shaped by firms that can secure merchant access, access to funding flexibility, and repeat customer data simultaneously.

White space still exists in parts of the consumer durable loans market where no lender has yet built the same retail depth or network effects seen in India’s leading NBFC model. Emerging verticals such as healthcare, automotive, and home improvement also offer opportunities for embedded lending formats to expand beyond traditional appliances and electronics. Manufacturer-backed finance remains a possible disruptor, especially in white goods, because OEMs have installed bases and trade-in pathways that can support financing-linked replacement cycles. Regulatory readiness will also affect competitive position because lenders with stronger audit trails and disclosure systems can expand more smoothly across geographies under tighter rules. The competitive picture in the consumer durable loans market is therefore still open enough for share shifts, even though scale advantages remain important.

Consumer Durable Loans Industry Leaders

Synchrony Financial

Bajaj Finance Limited

HDFC Bank Limited

ICICI Bank Limited

Klarna Bank AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Klarna entered a USD 1.7 billion Significant Risk Transfer transaction with a consortium led by Värde Partners, covering Euro-denominated loans and supporting up to USD 40 billion-plus of lending capacity, the company's sixth and largest SRT to date, reflecting a capital-efficiency strategy that directly funds consumer durable installment lending expansion at scale.

- April 2026: Synchrony Financial launched the RH Credit Card in partnership with luxury home furnishings brand RH, offering promotional financing for gallery and online purchases and further consolidating Synchrony's position across the majority of the top 100 United States furniture retailers, deepening the embedded finance moat in the high-ticket home furnishings category.

- April 2026: Bajaj Finserv reported a 22% rise in consolidated Q4 FY26 net profit to INR 5,553 crore (~USD 663 million at approximate average 2026 rate of INR 83.7/USD), announced a special centenary dividend, and unveiled its 2026-2030 strategic roadmap targeting AUM market share of up to 4% by 2030.

- January 2026: Fiserv and Affirm announced an exclusive collaboration to embed pay-over-time capabilities into debit card programs for thousands of United States Bank and credit union clients, extending BNPL origination capacity to mid-tier financial institutions without requiring new lending products, materially broadening the distribution infrastructure for consumer durable financing.

Global Consumer Durable Loans Market Report Scope

| Major Home Appliances (White Goods) |

| Consumer Electronics & Brown Goods |

| Furniture & Home Furnishings |

| Other Consumer Durables |

| Prime Borrowers |

| Near Prime Borrowers |

| Subprime Borrowers |

| Point-of-Sale (POS) / Embedded Finance |

| Digital / Online Direct |

| Intermediated / Broker / Agent |

| Physical / Branch-Based Direct |

| Banks |

| Non-Banking Financial Companies (NBFCs) |

| Manufacturer Captive Finance Arms |

| Fintechs & Digital Lenders |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Product Type | Major Home Appliances (White Goods) | |

| Consumer Electronics & Brown Goods | ||

| Furniture & Home Furnishings | ||

| Other Consumer Durables | ||

| By Borrower Risk Profile | Prime Borrowers | |

| Near Prime Borrowers | ||

| Subprime Borrowers | ||

| By Distribution Channel | Point-of-Sale (POS) / Embedded Finance | |

| Digital / Online Direct | ||

| Intermediated / Broker / Agent | ||

| Physical / Branch-Based Direct | ||

| By Lender Type | Banks | |

| Non-Banking Financial Companies (NBFCs) | ||

| Manufacturer Captive Finance Arms | ||

| Fintechs & Digital Lenders | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving growth in consumer durable financing through 2031?

Growth is being supported by embedded finance at checkout, wider use of installment plans, stronger fintech underwriting, and durable replacement demand. The market is projected to rise from USD 674.69 billion in 2026 to USD 989.51 billion by 2031 at a 7.96% CAGR.

Which product group leads demand for financed durable purchases?

Major Home Appliances led with a 39.78% share in 2025, reflecting the essential and high-ticket nature of these purchases.

Which borrower category is growing the fastest?

Subprime Borrowers are forecast to grow at a 10.67% CAGR through 2031 as more lenders use alternative data and digital underwriting tools.

Which lending channel is scaling the quickest?

Digital and Online Direct is the fastest-growing distribution channel, with a projected 12.37% CAGR through 2031, even though POS and Embedded Finance remained the largest channel in 2025.

Which region offers the strongest growth outlook?

Asia-Pacific led with 48.12% share in 2025 and is also the fastest-growing region, with a 9.91% CAGR through 2031.

Are banks or fintechs better positioned in this space?

Banks still held the largest lender share at 46.45% in 2025, but fintechs and digital lenders are expanding faster at a 13.54% CAGR because they compete more effectively on speed, alternative data use, and embedded merchant integration.

Page last updated on: