Recurring Payments Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 48.96 Trillion |

| Market Size (2031) | USD 66.51 Trillion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Recurring Payments Market Analysis by Mordor Intelligence

The Recurring Payments Market size is projected to expand from USD 46.17 trillion in 2025 and USD 48.96 trillion in 2026 to USD 66.51 trillion by 2031, registering a CAGR of 6.32% between 2026 to 2031.

The 2026 market level shows that automated and consent-based billing is now embedded across consumer, enterprise, and public payment flows. The recurring payments market is advancing as subscription billing becomes more central to streaming, software, financial services, and utility collections. At the same time, account-to-account rails, wallet-based authorizations, and smarter recovery workflows improve payment continuity. Competitive activity is also shifting, as processors, billing platforms, and payment networks are building broader multi-rail capabilities and using acquisitions and product launches to deepen control over recurring transaction flows. The recurring payments market also has room to expand through enterprise billing digitization, adoption of local rail systems in emerging economies, and improved credential management for agent-initiated payments. At the same time, the pace of growth will depend on how well merchants manage fraud exposure, legacy system integration, and tighter compliance thresholds around recurring authorizations.

Key Report Takeaways

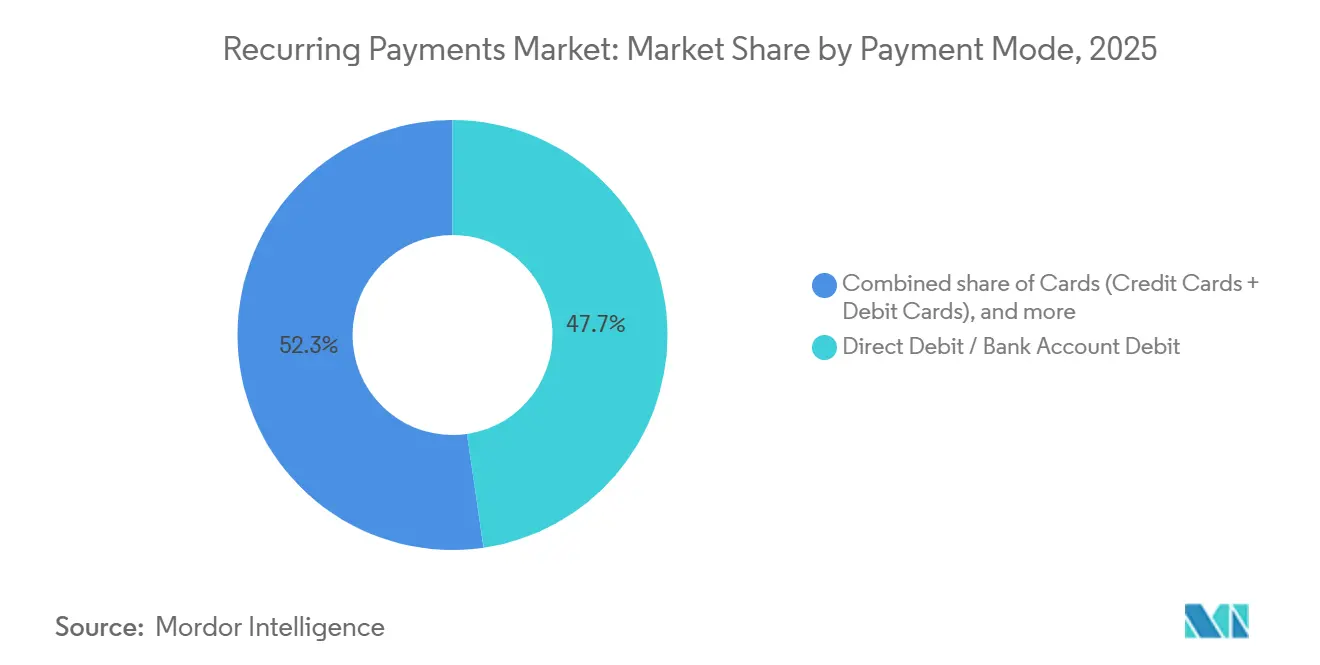

- By payment mode, direct debit/bank account debit accounted for 47.7% of the recurring payments market share in 2025, while digital wallets & e-money are projected to grow at 9.4% CAGR through 2031.

- By payment type, consumer (B2C) captured 66.9% of the recurring payments market share in 2025, while business (B2B) is projected to grow at 8.1% CAGR through 2031.

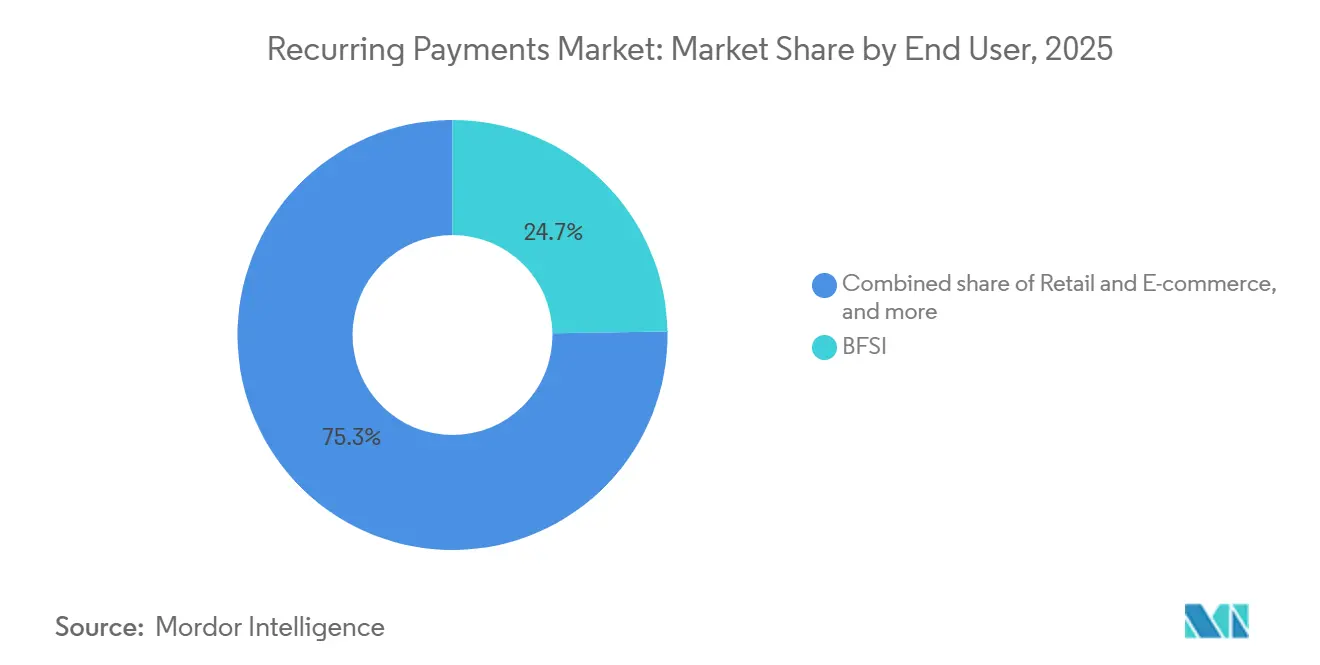

- By end user, BFSI held 24.7% of the recurring payments market share in 2025, while media and entertainment is projected to grow at 8.8% CAGR through 2031.

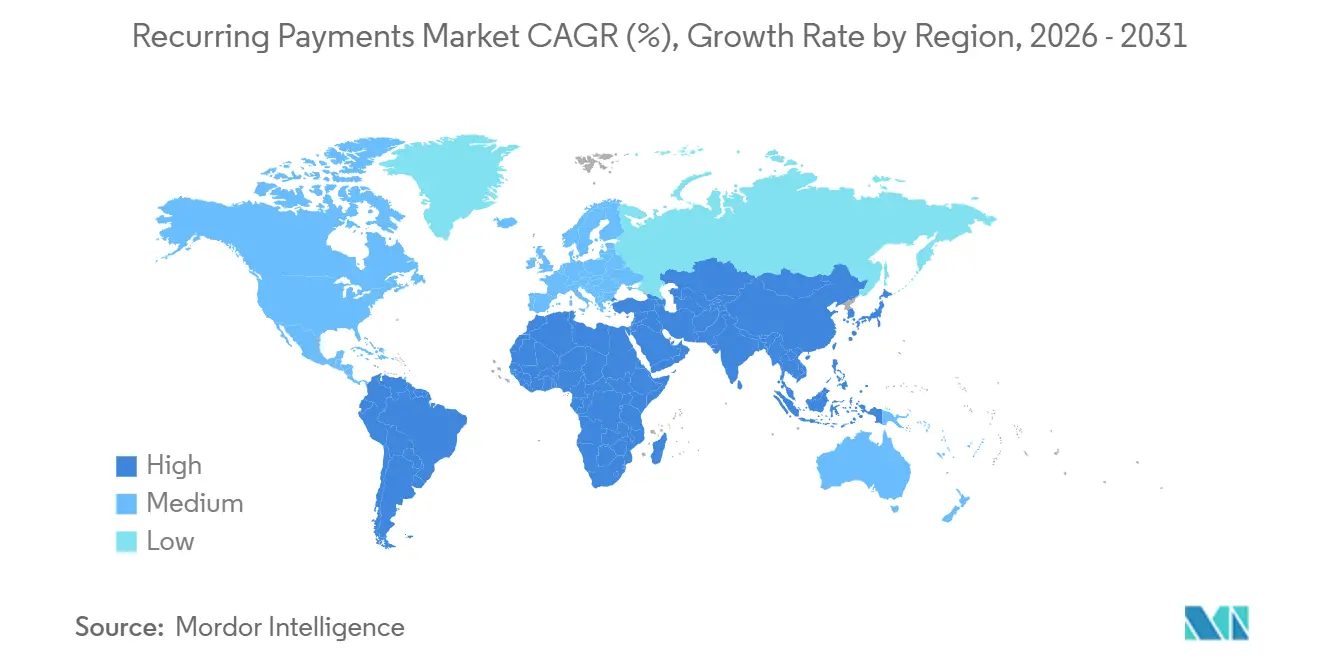

- By geography, North America held 31.4% of the recurring payments market share in 2025, while Asia-Pacific is projected to grow at 9.1% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Recurring Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Subscription Economy Across Digital Services | +1.8% | Global | Medium term (2-4 years) |

| Shift Toward Automated Billing to Reduce Churn | +1.1% | Global, concentration in North America & Europe | Short term (≤ 2 years) |

| Expansion of Digital Wallet and A2A Payment Rails | +1.4% | Asia-Pacific core; spill-over to South America and MEA | Medium term (2-4 years) |

| Merchant Demand for Real-Time Retry and Dunning Automation | +0.9% | Global | Short term (≤ 2 years) |

| Growing Need for Tokenized Credentials in Agentic Commerce | +0.8% | North America & Europe, early gains in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Subscription Economy Across Digital Services

The recurring payments market is benefiting from stronger monetization across subscription businesses that now rely on longer customer relationships rather than one-time purchases. Recurly stated in its 2026 State of Subscriptions report, based on 76 million unique subscribers and 2,200 global merchants, that subscription revenue growth reached 12.6%[1]Recurly, “2026 State of Subscriptions Report,” Recurly, recurly.com. The same report showed that micro-subscriptions converted 13% of buyers into long-term recurring plans, which supports wider adoption in lower-ticket categories where upfront commitment has historically been weaker. Recurly also found that annual plans generated 50% to 60% higher revenue per user than monthly plans, which gives merchants a clear reason to push longer billing cycles and more stable payment relationships. As a result, the recurring payments market is seeing stronger demand for billing systems that can support plan flexibility, retention workflows, and multi-service consent management without disrupting renewal performance.

Expansion of Digital Wallet and A2A Payment Rails

The recurring payments market is also being lifted by wider adoption of account-to-account rails and recurring wallet authorizations, which reduce card dependency and lower payment acceptance friction. In the United Kingdom, commercial Variable Recurring Payments went live through the United Kingdom Payments Initiative on June 2, 2026, covering 75% of current accounts in Wave 1 across utilities, regulated financial services, and charities[2]GoCardless, “GoCardless Launches Recurring Pay by Bank as Part of New UK Payment Scheme,” GoCardless, gocardless.com. In the European Union, the ECON Committee approved PSD3 and the Payment Services Regulation in May 2026, and the expected rule path will standardize open-banking API performance for recurring payment initiation across member states around 2028. In Brazil, Pix Automático recorded 14.7 million monthly charges in May 2026, and EBANX reported that 64% of users paying through Pix Automático were net-new subscribers to digital services, which shows that better rails can expand usage rather than shift existing payment volume. EBANX extended recurring alternative payments to 12 emerging markets in April 2026, targeting a base of 1 billion users across digital wallets and A2A methods that had been difficult to serve through card-on-file recurring models.

Merchant Demand for Real-Time Retry and Dunning Automation

The recurring payments market is gaining support from merchants investing in revenue recovery tools, as failed renewals remain a direct source of involuntary churn. The user-supplied material states that involuntary churn accounts for 20% to 40% of subscriber loss across recurring billing verticals, and that 10% to 15% of subscription charges fail on the first attempt globally. Stripe released Smart Retry Intelligence in April 2026 to determine optimal retry windows for declined recurring charges, showing that payment recovery is becoming a core processor capability rather than a specialist add-on. Zuora states that its billing platform can recover up to 20% more subscription revenue through configurable retry logic and multi-gateway orchestration. At the same time, Chargebee launched Smart Revenue Operations in May 2025 to unify revenue recognition across Stripe, Braintree, and Adyen[3]Zuora, “Flexible Recurring Billing Software,” Zuora, zuora.com. At the same time, Visa reduced its monitoring threshold to 1.5% in April 2026, meaning merchants need recovery systems that improve authorization performance without pushing dispute ratios into expensive compliance programs.

Growing Need for Tokenized Credentials in Agentic Commerce

The recurring payments market is entering a new phase as agent-initiated purchasing introduces credential-handling requirements beyond traditional checkout flows. Mastercard launched Agent Pay on April 29, 2025, and introduced Mastercard Agentic Tokens for programmable payments, including recurring subscriptions[4]Mastercard, “Mastercard Unveils Agent Pay, Pioneering Agentic Payments Technology to Power Commerce in the Age of AI,” Mastercard, mastercard.com. Fiserv integrated with Mastercard’s Agent Pay Acceptance Framework in December 2025, while also collaborating with Visa on agentic commerce enablement, which positions it close to the merchant acceptance layer for AI-initiated recurring transactions. Stripe also introduced agentic commerce solutions and announced 288 products and features at Stripe Sessions 2026 that expand tokenization and orchestration capabilities for recurring billing environments. This is pushing the recurring payments market toward platforms that can manage tokenization, permissions, billing logic, and payment execution within one architecture.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border Fraud and Chargeback Exposure | -0.9% | Global, most acute in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Legacy ERP and CRM Integration Complexity | -0.7% | Global, concentration in North America & Europe | Medium term (2-4 years) |

| Fragmented Regulatory and Data-Residency Requirements | -0.6% | EU, Asia-Pacific, MEA | Medium term (2-4 years) |

| Subscription Fatigue and Payment Authorization Drop-Offs | -0.5% | North America, Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cross-Border Fraud and Chargeback Exposure

The recurring payments market faces a persistent constraint from cross-border dispute risk, especially where billing descriptors and merchant locations are less familiar to customers and issuers. Sift reported in its Q4 2025 Digital Trust Index that B2C SaaS and services chargebacks rose 83% year over year, which supports the view that subscription confusion and first-party fraud are material pressure points for recurring billing flows. Visa tightened its VAMP threshold from 2.2% to 1.5% in April 2026, meaning a merchant with 5,000 monthly billings could enter the excessive monitoring band after 45 combined fraud alerts and disputes and face a USD 10-per-dispute fine. The user-supplied material also notes that foreign acquirer routing can lower statement descriptor recognition and issuer approval rates, thereby increasing both revenue losses and compliance costs. For the recurring payments market, this means local processing coverage and multi-acquirer routing are becoming defensive requirements rather than optional optimization tools.

Legacy ERP and CRM Integration Complexity

The recurring payments market also remains constrained by the difficulty of integrating modern billing workflows with older ERP and CRM systems. The user-supplied material states that recurring billing systems generate mid-cycle upgrades, dunning events, consent revocations, and proration changes that many legacy systems were not designed to absorb in real time. Corpay, citing Nacha data from 2026, stated that roughly 40% of the United States. B2B transactions still moved on paper checks, highlighting the extent of workflow fragmentation in enterprise payment operations. Chargebee launched Smart Revenue Operations in May 2025 to unify revenue recognition across multiple processors and support ASC 606- and IFRS 15-aligned reporting, reflecting sustained demand for integration-layer fixes rather than a temporary backlog. This integration drag slows migration into the recurring payments market for mid-sized enterprises and limits the speed at which advanced billing tools can scale across more complex operating environments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Mode: Direct Debit Dominates as Digital Wallets Accelerate

Digital Wallets & E-Money is the fastest-growing payment mode in the recurring payments market, with a 9.4% CAGR from 2026 to 2031. This growth is being supported by consent-based wallet authorizations in Southeast Asia and super-app ecosystems where wallet-to-subscription flows do not depend on card issuance. EBANX expanded recurring capabilities in April 2026 for Maya and GCash in the Philippines, OVO and DANA in Indonesia, and TrueMoney in Thailand, extending recurring access to a large user base previously outside card-on-file models. Even so, Direct Debit / Bank Account Debit held 47.7% of the recurring payments market in 2025, showing that bank-pull structures remain the core foundation for large-scale recurring collections. This part of the recurring payments industry benefits from lower exposure to card expiry and from entrenched use in utilities, insurance, financial services, and software billing.

Cards also remain important in the recurring payments market, especially in North American and European consumer use cases where card-on-file billing is already deeply embedded. The user-supplied material notes that ACH in the United States, SEPA Direct Debit in the European Union, and Bacs in the United Kingdom continue to support very large recurring billing flows across essential service categories. In the United Kingdom, commercial Variable Recurring Payments went live in June 2026, offering a lower-cost account-to-account alternative that will expand further as Wave 2 reaches SaaS and streaming in the second half of 2026. The main challenge for wallet-led recurring billing is interoperability, because recurring authorization depends on the wallet provider, processor connection, app-store design, and local regulatory rules. That means the recurring payments market will likely continue to support multiple payment modes in parallel, even as wallet and A2A adoption rise faster than card-based recurring payments.

By Payment Type: Consumer Volume Anchors While B2B Digitization Accelerates

Business (B2B) is the fastest-growing payment type in the recurring payments market, with an 8.1% CAGR from 2026 to 2031. The user-supplied material links this growth to still-unfinished digitization across enterprise accounts payable and accounts receivable processes. Melio launched an autonomous B2B payment network on June 17, 2026, enabling AI agents to execute supplier payments through existing AR systems without requiring new supplier portal onboarding. This development matters because it narrows the operational gap between enterprise billing systems and payment execution infrastructure. It also shows that the recurring payments market is expanding beyond classic consumer subscriptions and into repeatable supplier and intercompany payment flows.

Consumer (B2C) payments still held a 66.9% share of the recurring payments market in 2025, keeping consumer renewals at the center of current transaction volume. Streaming services, software subscriptions, digital health plans, and other card-on-file and bank-debit models continue to anchor this side of the recurring payments industry. Recurly reported in 2026 that win-back campaigns converted nearly 1 in 4 new sign-ups from former subscribers, which highlights how retention economics are shaping payment design as much as new customer acquisition. The user-supplied material also notes that ISO 20022 adoption is improving the carriage of structured data in B2B recurring flows, which supports better reconciliation and lower exception-handling costs. Over time, the recurring payments market should see a more balanced mix between high-volume consumer renewals and higher-value enterprise billing streams as digitization spreads further into business payment operations.

By End User: BFSI Anchors as Media and Entertainment Disrupts

Media and Entertainment is the fastest-growing end-user segment in the recurring payments market, with an 8.8% CAGR from 2026 to 2031. The user-supplied material attributes this growth to streaming platform expansion, creator economy subscriptions, and bundled access models that are adding more recurring charges to everyday digital consumption. This segment is also forcing providers to improve plan flexibility, pause options, and recovery logic, as customers move more frequently between services and price tiers. In this part of the recurring payments market, billing performance is closely linked to retention because many users can cancel or rejoin with limited switching costs. That keeps demand high for subscription management tools that can reduce failed renewals and improve continuity across changing payment credentials.

BFSI held 24.7% of the recurring payments market share in 2025, reflecting the scale of insurance premium collections, loan repayment mandates, investment top-ups, and bank-managed subscription tools. The user-supplied material notes that Capital One, U.S. Bank, and Mastercard introduced subscription management capabilities within consumer banking apps between late 2024 and 2025, extending recurring payment visibility inside financial institution ecosystems. Retail and E-commerce, Healthcare & Life Sciences, and Utilities & Energy remain meaningful contributors as embedded finance partnerships and usage-based pricing models spread across service categories. Telecom also continues to move from flat-fee structures toward metered subscription arrangements that require more advanced billing engines and stronger recurring authorization controls. Across end users, the recurring payments market is gradually shifting from simple periodic billing toward more dynamic payment relationships that require stronger orchestration, customer communication, and revenue recovery workflows.

Geography Analysis

North America accounted for 31.4% of the recurring payments market in 2025, making it the largest regional contributor by current market share. The region benefits from a high concentration of subscription-native software businesses and from a mature ACH infrastructure that processed nearly USD 93 trillion in 2025. Visa launched its Enhanced Subscription Manager for North American issuers in March 2026, giving consumers a centralized portal to track, pause, or cancel recurring charges within banking environments. South America is a rising contributor to the recurring payments market because payment innovation is improving access rather than only replacing existing card activity. In Brazil, Pix Automático reached 14.7 million monthly transactions in May 2026, and EBANX stated that 64% of those users were net-new digital service subscribers.

Europe remains one of the most important regions for the recurring payments market, as regulation and infrastructure are reshaping billing economics. In the United Kingdom, commercial Variable Recurring Payments covered 75% of current accounts in Wave 1 as of June 2, 2026, creating a lower-cost A2A route for recurring collections in selected sectors. The same initiative is scheduled to extend to SaaS, streaming, and subscription retail in the second half of 2026, which could improve the commercial case for bank-based recurring billing in more digital categories. In the European Union, PSD3 and the Payment Services Regulation received ECON Committee approval in May 2026, with most compliance obligations expected to apply around 21 months after publication. This gives the recurring payments market a clearer path toward more consistent open-banking API standards, fraud liability rules, and recurring initiation performance across member states.

Asia-Pacific is forecast to be the fastest-growing region in the recurring payments market, with a 9.1% CAGR from 2026 to 2031. Growth is being driven by digital-wallet adoption in Southeast Asia, UPI AutoPay penetration in India, and broader payment infrastructure maturation across large digital economies. Alipay launched its AI Wallet on May 26, 2026, and introduced subscription and per-call billing via its Token Pay solution, demonstrating how recurring billing in China is increasingly tied to AI service monetization. The Middle East and Africa remain smaller in their present scale. Still, EBANX’s April 2026 rollout of Capitec Pay Recurring in South Africa shows that infrastructure build-out can unlock new recurring use cases where card-on-file access has historically been limited.

Competitive Landscape

The recurring payments market remains moderately fragmented at the infrastructure layer, but concentration is increasing among larger processors that can support multiple rails, regions, and billing functions. Global Payments completed its USD 24.25 billion acquisition of Worldpay in January 2026, while FIS simultaneously completed the USD 13.5 billion acquisition of Global Payments’ Issuer Solutions business, which reshaped the upper tier of transaction processing and commerce enablement. The recurring payments market is also seeing increased pressure from combinations that bring local payments, cards, and bank-debit capabilities together into a single platform. Mollie signed a definitive agreement in December 2025 to acquire GoCardless for EUR 1.1 billion (USD 1.25 billion), combining checkout and local payment capabilities with bank-payment infrastructure focused on recurring collections. This direction suggests that scale in the recurring payments market is no longer defined solely by processing volume, but also by the ability to orchestrate multiple payment methods within a single billing environment.

Strategic differentiation in the recurring payments market is converging around payment recovery, tokenized agentic commerce, and multi-rail orchestration. Stripe released Smart Retry Intelligence in April 2026, while Chargebee’s Smart Revenue Operations addressed cross-processor revenue recognition and lifecycle management, showing that billing performance and finance control are now tightly linked. Fiserv strengthened its position in December 2025 through integrations with Mastercard’s Agent Pay Acceptance Framework and Visa’s Intelligent Commerce-related initiatives, placing it close to the emerging flow of AI-initiated transactions at merchant scale. EBANX expanded recurring alternative payments across 12 emerging markets in April 2026, demonstrating that a competitive advantage in the recurring payments market is also being built through localized access, not just through global processor scale. Melio’s June 2026 autonomous B2B payment network adds another example, because it targets a white space where recurring supplier payments still face integration and onboarding friction.

Specialist billing platforms such as Zuora, Chargebee, and Recurly still hold an important role in the recurring payments market because they offer deeper lifecycle tooling for subscription-native businesses. At the same time, processors such as Stripe, Global Payments, and GoCardless are moving closer to that software layer by embedding billing, recovery, and orchestration functions into broader payment stacks. Compliance thresholds under Visa monitoring rules and chargeback programs serve as quality filters, as merchants increasingly prefer providers that can combine authorization performance with fraud control and local routing resiliency. This means the recurring payments market is likely to continue consolidating around platforms that can support scale, local compliance, multi-method acceptance, and recovery intelligence simultaneously.

Recurring Payments Industry Leaders

Stripe, Inc.

PayPal Holdings, Inc.

Adyen N.V.

Square, Inc. (Block, Inc.)

GoCardless Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Melio launched an autonomous B2B payment network enabling AI agents to execute supplier payments directly through existing AR systems across tens of thousands of SMBs, without requiring supplier portal onboarding, eliminating a key friction point in B2B recurring payment digitization.

- June 2026: The United Kingdom Payments Initiative went live on June 2, 2026, deploying commercial Variable Recurring Payments across five low-risk sectors with 75% United Kingdom current account coverage in Wave 1, the first new United Kingdom payment scheme since Faster Payments in 2008. Wave 2 expansion to SaaS and streaming is planned for H2 2026.

- May 2026: The EU Parliament’s ECON Committee approved PSD3 and the Payment Services Regulation on May 5, 2026. An Official Journal publication is expected in the second half of 2026, with mandatory compliance obligations for open-banking recurring payment APIs applying approximately 21 months after publication.

- April 2026: EBANX expanded its recurring alternative payments offering to 12 emerging markets, enabling consent-based digital wallet and A2A recurring billing for platforms including Maya and GCash in the Philippines, OVO and DANA in Indonesia, and Capitec Pay in South Africa, unlocking access to a potential 1 billion users and targeting 1.3 billion adults without credit or debit cards.

Global Recurring Payments Market Report Scope

| Cards (Credit Cards + Debit Cards) |

| Direct Debit / Bank Account Debit |

| Digital Wallets & E-Money |

| Other Payment Modes |

| Consumer (B2C) |

| Business (B2B) |

| BFSI |

| Retail and E-commerce |

| Healthcare & Life Sciences |

| Utilities & Energy |

| Telecommunications |

| Education |

| Media and Entertainment |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Indonesia | |

| Thailand | |

| Malaysia | |

| Singapore | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Payment Mode | Cards (Credit Cards + Debit Cards) | |

| Direct Debit / Bank Account Debit | ||

| Digital Wallets & E-Money | ||

| Other Payment Modes | ||

| By Payment Type | Consumer (B2C) | |

| Business (B2B) | ||

| By End User | BFSI | |

| Retail and E-commerce | ||

| Healthcare & Life Sciences | ||

| Utilities & Energy | ||

| Telecommunications | ||

| Education | ||

| Media and Entertainment | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Indonesia | ||

| Thailand | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of recurring payments by 2031?

The recurring payments market is projected to reach USD 66.51 trillion by 2031, rising from USD 48.96 trillion in 2026 at a 6.3% CAGR.

Which payment mode leads recurring billing today?

Direct Debit / Bank Account Debit led in 2025 with a 47.7% share, supported by its strong role in utilities, insurance, BFSI, and software collections.

Which payment type is growing faster between B2C and B2B?

B2B is growing faster, with an 8.1% CAGR from 2026 to 2031, while B2C remains the larger category with a 66.9% share in 2025.

Which end-user group is creating the fastest expansion?

Media and Entertainment is the fastest-growing end-user segment, with an 8.8% CAGR through 2031, driven by streaming, creator subscriptions, and bundled digital access.

Which region shows the strongest growth outlook?

Asia-Pacific has the highest projected regional growth at a 9.1% CAGR from 2026 to 2031, supported by digital wallets, UPI AutoPay, and broader payment infrastructure development.

What are the main risks affecting recurring billing performance?

The main risks are cross-border chargebacks, tighter compliance thresholds, and integration gaps with legacy ERP and CRM systems that slow recovery, routing, and reconciliation performance.

Page last updated on: