Micro Lending Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

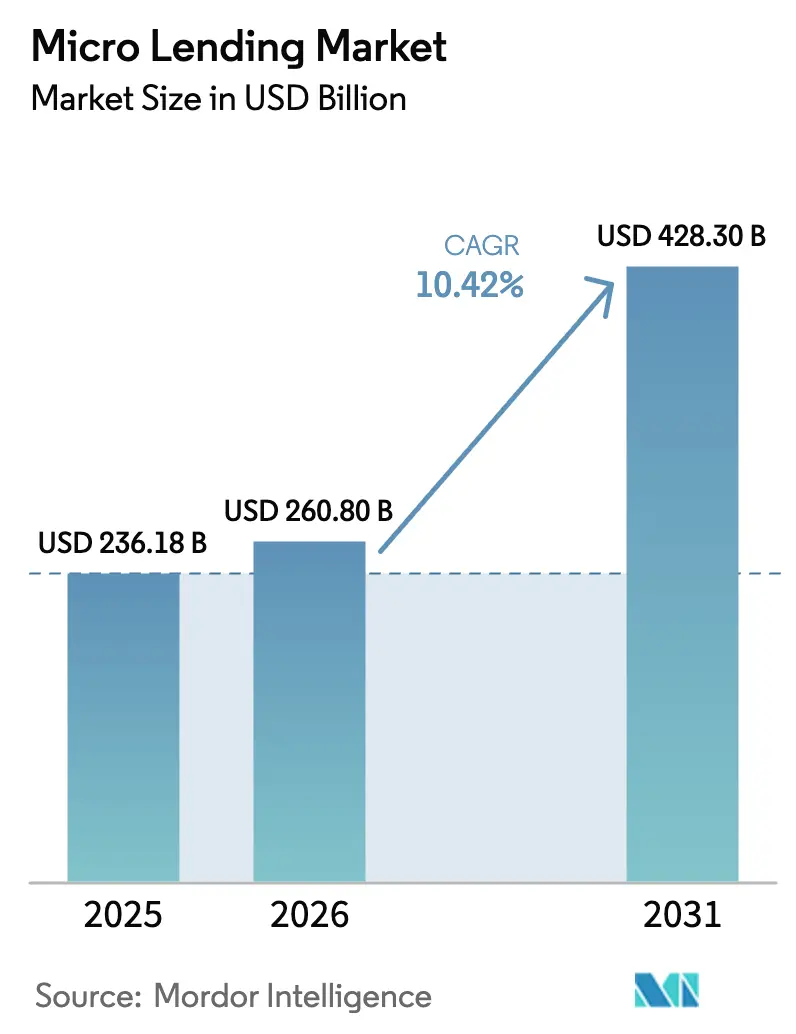

| Market Size (2026) | USD 260.8 Billion |

| Market Size (2031) | USD 428.3 Billion |

| Growth Rate (2026 - 2031) | 10.42% CAGR |

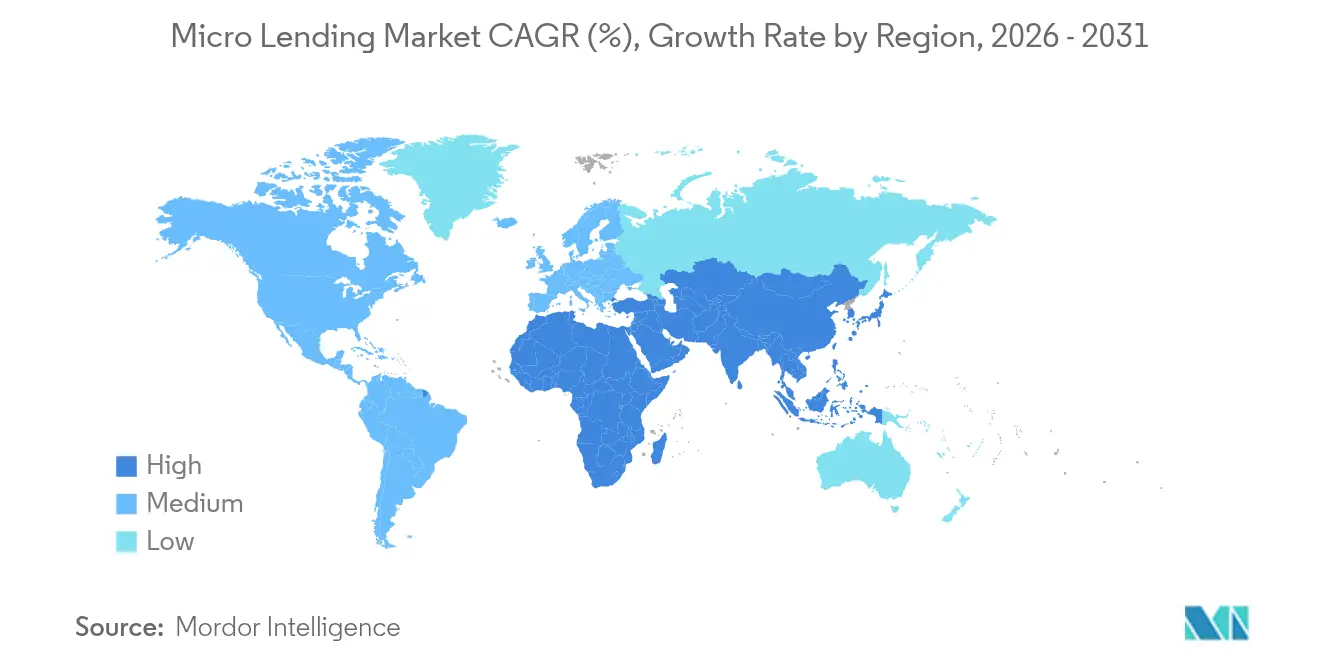

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Micro Lending Market Analysis by Mordor Intelligence

The micro lending market size was valued at USD 236.18 billion in 2025 and estimated to grow from USD 260.8 billion in 2026 to reach USD 428.3 billion by 2031, at a CAGR of 10.42% during the forecast period (2026-2031). Expansion is anchored in digital onboarding, alternative-data credit scoring, and government inclusion mandates that collectively unlock new borrower cohorts. The micro lending market benefits from fintech cost advantages that compress acquisition costs by 60-70%, allowing rapid scale in geographies where branch infrastructure remains thin. Growing participation from impact-driven and ESG-linked funds is broadening the capital base, while embedded-finance partnerships move loans closer to real-time checkout experiences. At the same time, the micro lending market faces tempering forces such as post-pandemic portfolio stress and capital adequacy rules that raise funding hurdles for tier-2 institutions, yet well-capitalized providers with credible risk models continue to capture share.

Key Report Takeaways

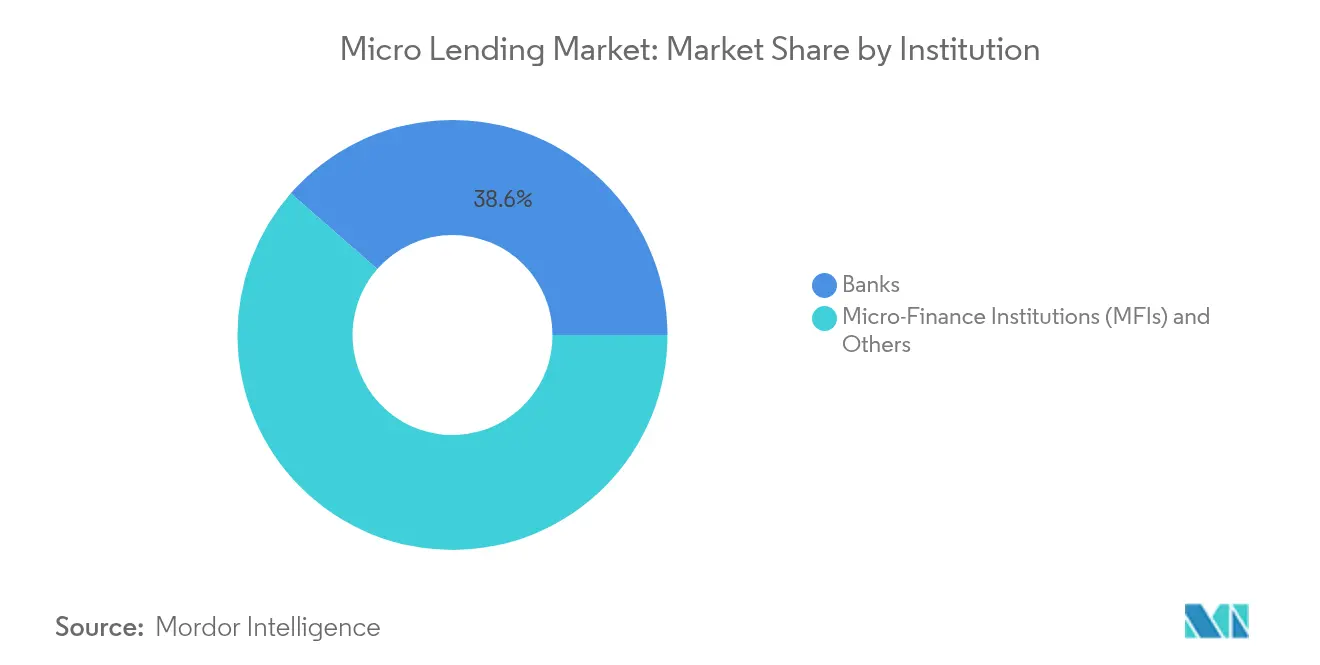

- By institution, microfinance institutions and other non-bank lenders held 61.45% of the micro lending market share in 2025, while the cohort is projected to post a 12.28% CAGR to 2031.

- By end-user, business lending accounted for 65.10% share of the micro lending market size in 2025, and the segment is expected to advance at an 11.08% CAGR through 2031.

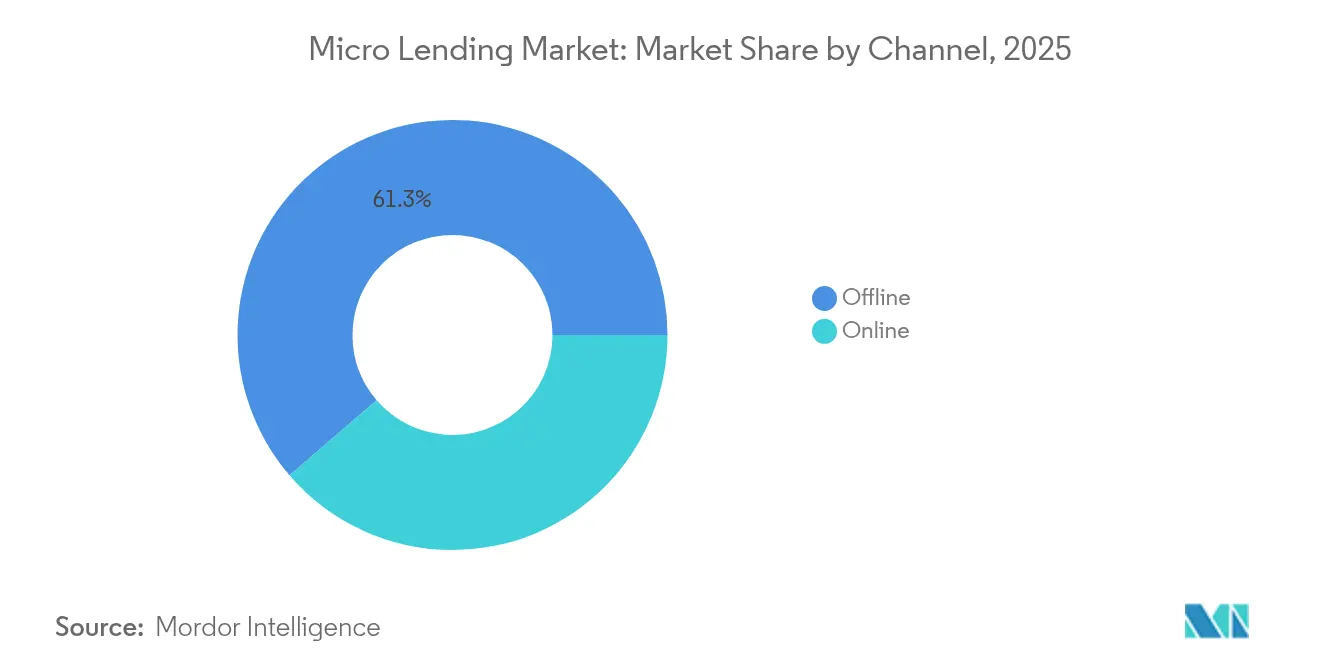

- By channel, the offline segment captured 61.30% share of the micro lending market in 2025; the online channel is forecasted to expand at a 14.19% CAGR to 2031.

- By region, Asia-Pacific led with 43.20% of micro lending market share in 2025, and the segment is set to register the fastest regional CAGR at 12.74% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Micro Lending Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fintech & mobile-first customer acquisition boom | +2.8% | Global, with Asia-Pacific and Latin America leading adoption | Medium term (2–4 years) |

| Government financial-inclusion mandates & subsidies | +2.1% | Emerging markets, particularly India, Bangladesh, and Sub-Saharan Africa | Long term (≥4 years) |

| Surge in impact/ESG-linked micro-credit funds | +1.4% | Global, with concentrated activity in North America and Europe | Medium term (2–4 years) |

| Expansion of P2P / marketplace platforms into MSE lending | +1.2% | Developed markets expanding to emerging economies | Short term (≤2 years) |

| Embedded-finance loans at e-commerce & POS check-out | +0.9% | North America, Europe, and urban centers in Asia-Pacific | Short term (≤2 years) |

| AI-based alternative-data scoring unlocking “thin-file” borrowers | +1.8% | Global, with fastest adoption in Asia-Pacific and Latin America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fintech & Mobile-first Customer Acquisition Boom

Mobile-centric lenders deploy AI to analyze more than 70,000 data points from devices, thereby scoring thin-file borrowers at scale. Customer acquisition costs are 60-70% lower than branch models, permitting profitable ticket sizes as small as USD 40 while maintaining default rates near 5% [1]Harvard Business School, “Fintech Lending in Emerging Markets,” hbs.edu. Success in Kenya and Mexico illustrates how rapid disbursement deepens client income and loyalty, reinforcing a virtuous cycle of repeat borrowing. Fintech scalability continues to pull capital into the micro lending market, especially as platforms prove that digital repayment footprints create predictive risk signals. The result is a rising share of micro lending market originations occurring entirely on smartphones, with lenders in markets such as the Philippines onboarding 1 million customers in 10 months.

Government Financial Inclusion Mandates & Subsidies

Policies such as India’s Open Credit Enablement Network or the U.S. National Strategy for Financial Inclusion are lowering onboarding friction, standardizing data sharing, and offering guarantee schemes that derisk lender exposure. Collateral-free guarantee programs already cover 10 million loans, catalyzing business lending demand that dominates the micro lending market. Subsidized interest windows and refinancing facilities blunt pandemic-era stress, ensuring liquidity to smaller MFIs. Over the long term, coordinated frameworks that link identity, payments, and credit are expected to expand the addressable customer pool by tens of millions.

Surge in Impact/ESG-linked Micro-credit Funds

Impact investors channel fresh capital toward inclusive finance, motivated by gender, climate, and poverty metrics that can be measured credibly at the loan-book level. Dedicated green-lending windows reward projects that cut emissions or advance female entrepreneurship, helping borrowers secure lower pricing. Islamic sustainable-finance structures add momentum by mobilizing faith-aligned pools of capital that favor risk-sharing. Institutions able to document social outcomes increasingly access concessional funding at spreads 100-150 bp below commercial lines, enhancing their competitiveness in the micro lending market.

Expansion of P2P / Marketplace Platforms into MSE Lending

Marketplace lenders originally built for consumer credit now pivot to micro-enterprise financing, chasing a USD 4.9 trillion credit gap. Proprietary cash-flow underwriting and API links to e-commerce sites shorten approval cycles from days to minutes, positioning platforms to capture fast-turnover working-capital demand. Regulators in markets such as Singapore and Mexico are crafting proportional capital and disclosure regimes that legitimize these non-bank models, further widening the addressable supply for the micro lending market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic spike in portfolio-at-risk & write-offs | −1.8% | Global, with acute impact in Sub-Saharan Africa and South Asia | Short term (≤2 years) |

| Rate-caps & tightening consumer-protection rules | −1.2% | Developed markets and emerging economies with mature regulatory frameworks | Medium term (2–4 years) |

| Climate-driven agri borrower defaults in rural cohorts | −0.9% | Rural areas in climate-vulnerable regions, particularly South Asia and Sub-Saharan Africa | Long term (≥4 years) |

| Basel-III risk-weight hikes starving tier-2 MFIs of bank credit | −1.4% | Global, with European MFIs experiencing the largest impact | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic Spike in Portfolio-at-risk & Write-offs

Lockdowns disrupted cash flows for millions of micro-entrepreneurs, pushing PAR30 ratios to multi-year highs and forcing lenders to restructure sizable portions of their loan books. Africa’s default rate reached 6.7% in 2024, well above the 4.1% global mean[2]International Finance Corporation, “Global Microfinance Portfolio Review,” ifc.org. Although repayments have gradually normalized, risk costs remain elevated for rural and informal borrowers, limiting immediate balance-sheet growth. Providers with diversified funding and granular data tracking have resumed originations faster, but the episode reinforces the sensitivity of the micro lending market to external shocks.

Rate Caps & Tightening Consumer-protection Rules

New usury ceilings in Kenya, Indonesia, and parts of Latin America compress net interest margins for lenders serving the riskiest clients. Simultaneously, operational-resilience and climate-risk regulations derived from Basel III and DORA add compliance overhead. Some tier-2 MFIs face higher funding costs or exit certain provinces altogether, temporarily slowing geographic expansion in the micro lending market. Innovation in cost-light digital delivery partially offsets these pressures, but the regulatory pendulum is expected to restrain aggressive pricing strategies over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Institution: MFIs Extend Specialized Leadership

MFIs and other non-bank lenders commanded 61.45% of the micro lending market share in 2025, and the segment is projected to compound at 12.28% annually through 2031. The segment’s dominance is rooted in low operating costs, mission-aligned funding, and field-agent intimacy that sustain loyalty among thin-file borrowers. Those attributes translate into quick disbursement and flexible repayment options, giving MFIs a cost-to-income advantage of 10-15 percentage points over banks in comparable ticket sizes.

Banks maintain relevance through partnerships, captive subsidiaries, and securitization channels that recycle on-balance-sheet portfolios into capital-market paper. Yet Basel III capital inflation of 4.9% for European Group 1 banks continues to divert scarce lending headroom toward lower-risk asset classes, indirectly steering smaller borrowers toward specialized MFIs. Securitization hubs such as Luxembourg offer a liquidity valve by converting seasoned micro-loan pools into tradable instruments, a model that now represents roughly 8% of the micro lending market size traded in secondary form.

By End-User: Business Lending Underpins Growth

Business lending represented 65.10% of the micro lending market in 2025 and is forecasted to grow at 11.08% CAGR, reflecting acute credit gaps for micro-enterprises that power local employment. Asia-Pacific alone hosts 98.7% of micro, small, and medium enterprises out of total business establishments, translating to persistent working-capital demand unmet by traditional banks. Collateral-free guarantee schemes and invoice-financing APIs now route capital in under 48 hours, propelling business-loan share gains within the micro lending market size.

Retail micro credit remains a vital inclusion gateway, but regulators increasingly encourage transition from consumption toward income-generating loans. Digital payroll links, inventory analytics, and supply-chain data help lenders structure cash-flow-based repayments, lowering default risk by 200–300 bp relative to equal-instalment consumer products. The confluence of policy and technology keeps micro-enterprise financing at the forefront of the micro lending market demand.

By Channel: Online Adoption Accelerates

Offline segment accounted for 61.30% of the micro lending market in 2025, but the online channel is on pace for a 14.19% CAGR to the end of the decade as smartphones become de facto branches. Digital adoption directly lifts GDP per capita by 0.10 percentage point and trims informal employment by 0.06 percentage point, reinforcing a structural tilt to online origination. The micro lending market benefits when borrowers repay via wallets because automated reminders and biometric log-ins raise on-time repayments by up to 8 percentage points.

Trust remains a barrier in low-literacy pockets, so leading MFIs blend agent visits with in-app tutorials, guiding first-time users through biometric onboarding. Embedded-finance tools further embed loan offers at e-commerce checkout, compressing decision time to seconds and widening reach to digitally native youth segments. In Tajikistan, Bank Arvand’s digital upgrade pushed self-service transactions to 65%, illustrating how hybrid models can grow share without alienating rural clients.

Geography Analysis

Asia-Pacific held 43.20% share of the micro lending market in 2025 and is projected to compound at 12.74% through 2031. Massive unbanked populations and real-time payment rails like India’s UPI create fertile ground for scale. Government programs anchor demand: Jan Dhan accounts surpass 500 million, offering lenders authenticated identity and transaction histories that compress KYC costs by 80%. Fintech partnerships embed credit within everyday super-apps, making India, Indonesia, and the Philippines hotspots for digital disbursement.

Latin America and the Caribbean contribute a smaller yet rapidly expanding slice of the micro lending market. IDB-backed investments funnel capital to women-owned businesses, and companies such as Tala leverage alternative data to underwrite 3 million Mexican customers with USD 500 million disbursed in 2024. Institutional trust markedly influences digital adoption; individuals expressing higher trust show a 62% greater likelihood of using mobile payments. That trust dividend underpins robust loan growth as borrowers migrate from payday shops to app-based credit.

Sub-Saharan Africa combines opportunity with portfolio risk. Mobile-money rails pioneered in Kenya yield unrivaled distribution reach, yet climate-induced crop failures raise defaults in agri books. Regional default rates stayed elevated at 6.7% in 2024, compared with the micro lending market global average of 4.1%. Innovative hybrids like micro-insurance plus micro-credit aim to hedge weather shocks, and regulators encourage digital sandboxes to test such solutions. Over time, improved risk pooling is expected to narrow loss-given-default and unlock further expansion.

Competitive Landscape

The micro lending market displays moderate concentration but sharp regional contrasts. In Asia-Pacific, incumbents such as Grameen, Bandhan, and BTPN Syariah collectively hold a considerable market share, whereas Latin America remains fragmented across hundreds of cooperatives and fast-scaling fintechs. Digital entrants enjoy acquisition costs up to 70% lower than traditional branches, allowing aggressive pricing while sustaining 10-point net-interest margins. Incumbents respond by launching mobile apps and entering API alliances that keep them visible within embedded-finance ecosystems.

Strategic investments accelerate technology adoption. TJ-based Bank Arvand secured a minority investment from Japan’s Gojo to ramp up cloud migration and AI scoring. Tala raised USD 150 million of debt underwritten by institutional investors, earmarking flexible limits and dynamic pricing for small business borrowers. Apple’s integration of BNPL provider Affirm into Apple Pay shows how global tech can insert lending at checkout, potentially siphoning affluent users from local MFIs in developed markets.

White-space remains vast in rural corridors where smartphone penetration lags or agents still carry paper ledgers. Players leveraging satellite imagery for crop estimates or cooperative data for community-based guarantees increasingly differentiate their credit models. Blockchain pilots for remittance-backed loans and tokenized securitizations inch forward, although regulation and cost keep adoption nascent. Over the next five years, the competitive edge will likely hinge on how well lenders harness alternative data while meeting heightening consumer-protection standards without inflating costs.

Micro Lending Industry Leaders

Accion International

BlueVine Inc.

Funding Circle

Kabbage Inc.

OnDeck

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Tala secured a USD 150 million debt facility managed by Neuberger Berman to expand Mexico operations, supporting higher limits and dynamic pricing for its 3 million-plus customer base.

- February 2025: Gojo & Company acquired a 9% stake in CJSC Bank Arvand to deepen digitalization in Tajikistan, where 65% of transactions are already processed online.

- January 2025: FINCA crossed 3 million customers globally after rolling out preferred-rate clean-energy loans and insurance products supported by AI-driven customer research.

- September 2024: Axis Bank partnered with Next Bharat Ventures to deliver collateral-free working-capital finance for impact-oriented MSMEs across India.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

According to Mordor Intelligence, our analysis defines the global micro-lending market as the total value of new, unsecured loans below USD 50,000 that are extended by banks, micro-finance institutions, non-bank finance companies, peer-to-peer platforms, and other licensed providers to micro, small, and solo enterprises and to low-income individuals seeking livelihood or working-capital finance.

Scope Exclusion: We do not include savings, micro-insurance, remittance, or any other non-credit microfinance services in this sizing.

Segmentation Overview

- By Institution

- Banks

- Micro-Finance Institutions (MFIs) and Others

- By End-Users

- Businesses

- Retail (Consumers)

- By Channel

- Online

- Offline

- By Region

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Colombia

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Benelux (Belgium, Netherlands, and Luxembourg)

- Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with senior risk heads at MFIs in India, Kenya, and Mexico, product managers at digital-only lenders in the United States, and cooperative leaders in the Philippines. Their insights validated borrower churn, effective interest spreads, and planned capital raises, closing gaps left by secondary data.

Desk Research

We first gathered macro and sector indicators from open sources such as the World Bank Global Findex, IMF Financial Access Survey, and ILO SME datasets. These outline borrower pools and digital penetration. Trade association notes from the MicroFinance Network and central-bank bulletins helped us benchmark average ticket sizes, yields, and portfolio quality. Annual filings, 10Ks, and investor decks of listed micro-lenders revealed cost-of-funds and disbursement growth, while news pulls on Dow Jones Factiva and intelligence from D&B Hoovers mapped competitive moves. This mix gives us a grounded starting grid, and many additional niche sources were reviewed before numbers were locked.

A second sweep drew on Questel patent families around alternative-data scoring, Volza shipment logs for handset imports that enable mobile credit, and policy alerts from the World Bank's CGAP. These feeds let us refine regional weightings without leaning on paywalled competitor figures. The list above is illustrative rather than exhaustive.

Market-Sizing & Forecasting

We applied a top-down credit-demand pool reconstruction anchored on working-age micro-entrepreneur counts, loan-penetration ratios, and average ticket sizes, which are then cross-checked with bottom-up lender roll-ups sampled across the ten largest markets. Core variables include GDP per capita shifts, smartphone adoption, gender-focused credit mandates, wholesale funding costs, regulatory interest caps, and portfolio-at-risk trends. A multivariate regression with ARIMA overlays projects volumes and yields through 2030, and scenario tests adjust for funding shocks. Any gap in sub-market data is bridged using calibrated penetration proxies.

Data Validation & Update Cycle

Before sign-off, our team runs variance checks against industry NPL ratios and capital-adequacy signals, flags outliers for peer review, and re-contacts sources when deviations exceed three percentage points. The model is refreshed annually, with interim updates after major regulatory or funding events.

Why Mordor's Micro Lending Baseline Earns Global Credibility

We acknowledge that published estimates diverge because firms select differing loan definitions, provider sets, and refresh timings. We openly trace our scope to on-book, new-issue micro-credit only, and we update each year so users gain a current anchor.

Key gap drivers arise when some publishers omit peer-to-peer flow, others freeze on 2021 values without inflation lift, or roll interest income into size rather than principal disbursed, inflating totals.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 236.18 bn (2025) | Mordor Intelligence | |

| USD 104.03 bn (2024) | Global Consultancy A | excludes NBFC portfolios and uses conservative ticket values |

| USD 31.85 bn (2022) | Trade Journal B | early base year and limited to bank channels |

| USD 212.42 bn (2024) | Industry Tracker C | omits marketplace peer-to-peer micro-loans |

Taken together, we believe our disciplined scope selection and yearly refresh deliver a balanced, transparent baseline that decision-makers can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the current size of the micro lending market?

The micro lending market is valued at USD 260.8 billion in 2026 and is projected to reach USD 428.3 billion by 2031.

Which region holds the largest share of the micro lending market?

Asia-Pacific leads with 43.20% of the micro lending market share in 2025, driven by large unbanked populations and supportive inclusion policies.

Why is business lending the dominant end-user segment?

Business lending captured 65.10% of the micro lending market in 2025 because micro-enterprises represent the majority of employers in emerging economies and seek flexible working-capital solutions that mainstream banks often cannot provide.

Which is the fastest growing region in Micro Lending Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Micro Lending Market?

In 2025, the Asia Pacific accounts for the largest market share in Micro Lending Market.

How fast is the online channel growing in the micro lending market?

Online micro-loan originations are forecast to grow at a 14.19% CAGR through 2031 as mobile-first platforms broaden reach and embed credit into digital commerce.

What are the key risks facing the micro lending industry?

Portfolio-at-risk spikes post-pandemic, rate caps, and new consumer-protection regulations pose near-term challenges by pressuring margins and raising compliance costs.

How are ESG considerations influencing micro lending?

Impact and ESG-linked funds supply concessional capital to lenders that demonstrate measurable social or environmental outcomes, encouraging growth in gender-focused and green micro-credit products.

Page last updated on: