Car Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

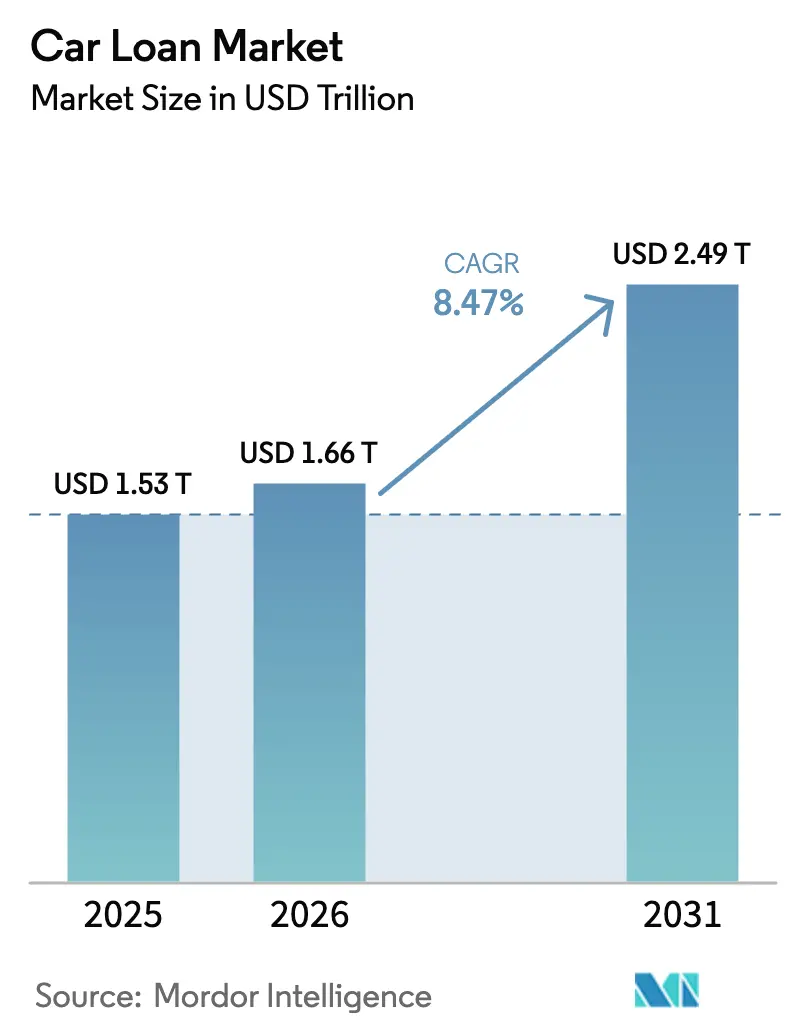

| Market Size (2026) | USD 1.66 Trillion |

| Market Size (2031) | USD 2.49 Trillion |

| Growth Rate (2026 - 2031) | 8.47% CAGR |

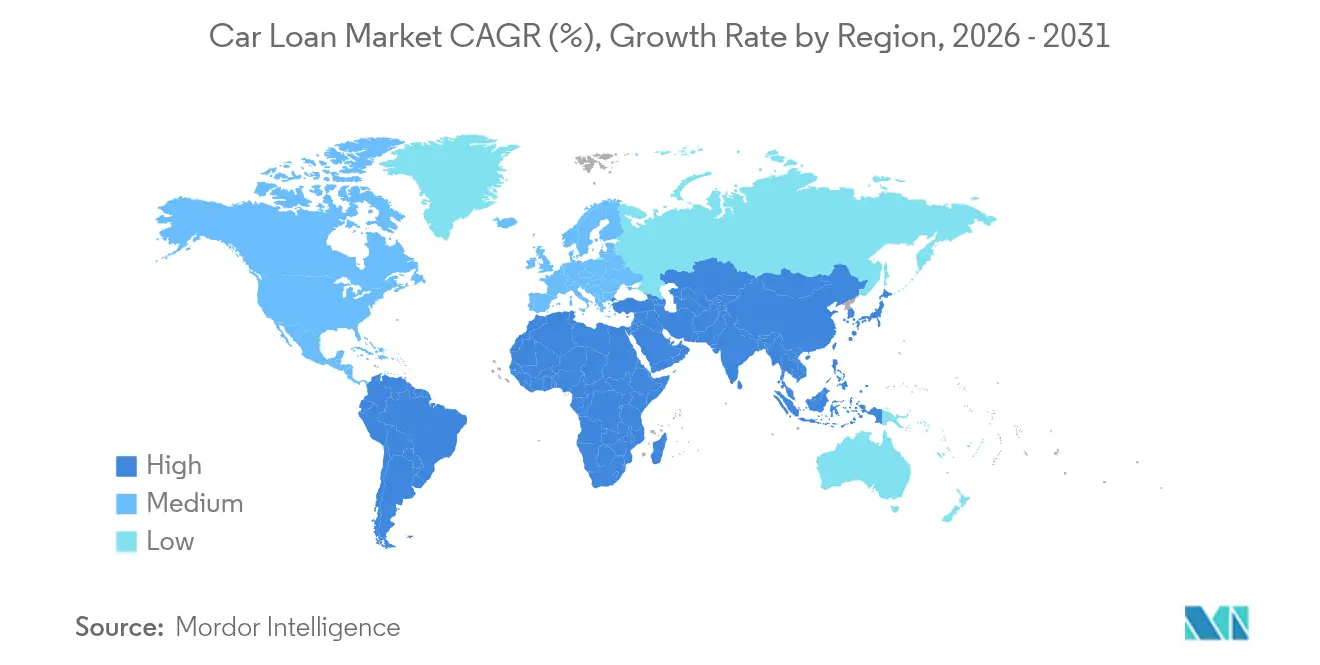

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Car Loan Market Analysis by Mordor Intelligence

The Car Loan Market size is expected to increase from USD 1.53 trillion in 2025 to USD 1.66 trillion in 2026 and reach USD 2.49 trillion by 2031, growing at a CAGR of 8.47% over 2026-2031.

The growth follows rapid digitization of lending, regulatory easing in large emerging economies, and changing consumer preferences that favor convenient, technology-enabled financing. Asia-Pacific leads current demand and growth, propelled by the removal of mandatory down-payments in China and interest-rate caps in India that lower borrower costs. Digital lenders are expanding instant-approval products that shorten credit decision times from days to minutes, while captive finance arms are scaling to secure end-to-end customer relationships. Used-vehicle financing is rising quickly as online platforms make vehicle history and prices more transparent, and commercial-vehicle electrification is pushing innovative loan structures that account for high upfront costs and residual-value uncertainty.

Key Report Takeaways

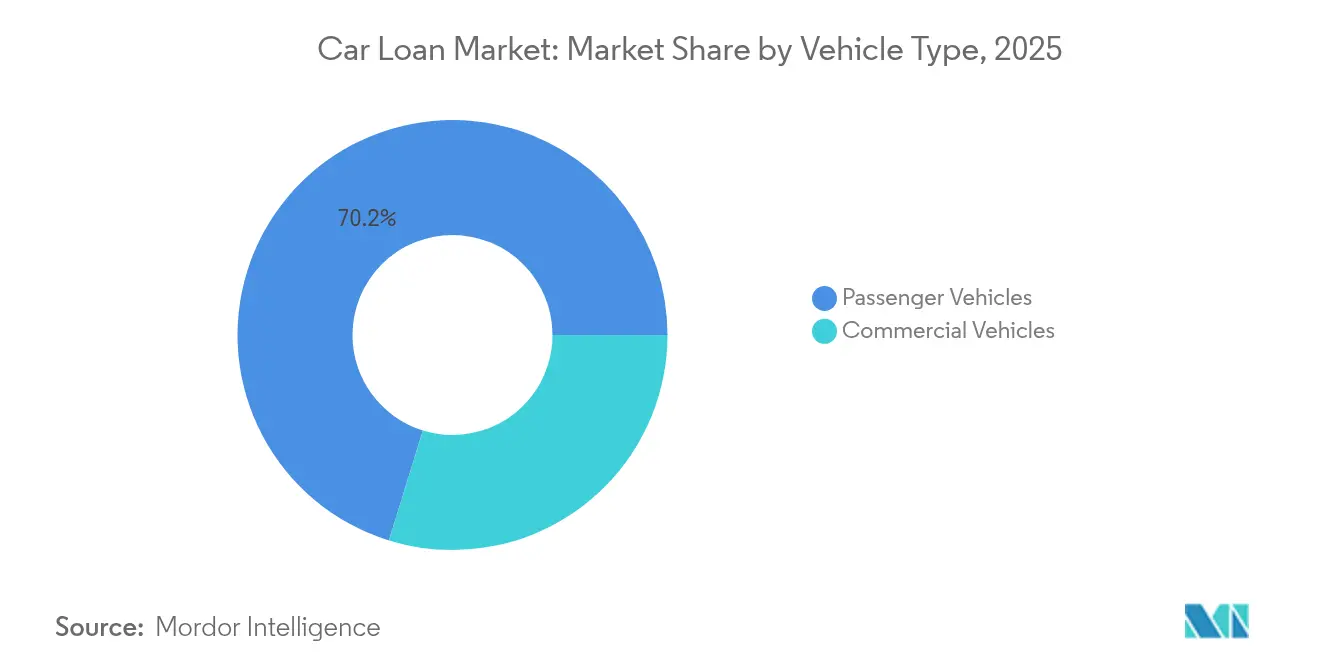

- By vehicle type, passenger vehicles led with 70.22% of the car loan market share in 2025, while commercial vehicles are projected to expand at a 9.05% CAGR to 2031.

- By ownership, new vehicles held a 60.37% share of the car loan market in 2025; used vehicles are expected to record the fastest growth at a 10.03% CAGR through 2031.

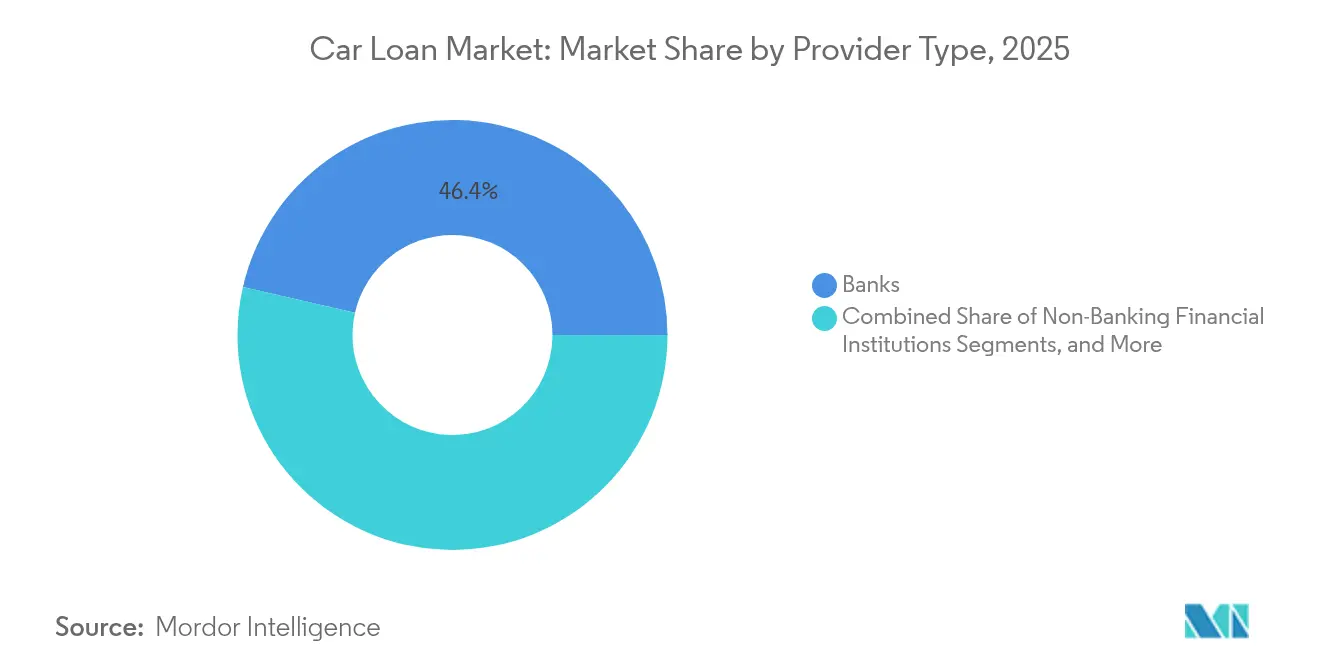

- By provider type, banks retained a 46.41% share of the car loan market in 2025, whereas fintech providers post the highest forecast CAGR at 14.12%.

- By tenure, 3–5-year loans captured a 51.99% share of the car loan market in 2025; loans exceeding five years are advancing at a 10.18% CAGR.

- By region, Asia-Pacific controlled 34.25% of the car loan market in 2025 share and is set to grow at a 9.74% CAGR, the fastest of all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Car Loan Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for luxury vehicles in emerging markets | +1.3% | Asia-Pacific core, spill-over to Latin America | Medium term (2-4 years) |

| Expansion of automakers’ captive finance arms | +1.0% | Global, emphasis on North America & Europe | Long term (≥ 4 years) |

| Growing penetration of online used-car platforms | +1.5% | North America & Europe, expanding to APAC | Short term (≤ 2 years) |

| Digital lending & instant approvals via fintech APIs | +1.7% | Global, led by North America & China | Short term (≤ 2 years) |

| Subscription-based ownership models boosting bundled finance | +0.7% | Europe & North America, pilot programs in APAC | Medium term (2-4 years) |

| Carbon-credit-linked interest rebates for EV purchases | +0.5% | Europe & California, expanding to China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for luxury vehicles in emerging markets

Disposable-income growth in China and India is outpacing vehicle price inflation, pulling premium models into mainstream consideration. Beijing’s decision to drop the long-standing down-payment requirement on personal car loans has widened access to high-ticket cars[1]Reuters Staff, “China Scraps Minimum Down Payments for Car Loans,” reuters.com. Automakers are matching the policy pivot with aggressive captive-finance offers tailored to luxury buyers, often at preferential rates that reflect lower default risk. Banks react by designing underwriting models aligned to higher loan amounts and longer asset lifecycles. Lenders that embed early in this segment gain brand loyalty and cross-sell potential as buyers upgrade.

Expansion of automakers’ captive finance arms

Original-equipment manufacturers are scaling finance subsidiaries such as Ford Credit, which managed USD 133.2 billion in receivables in 2023 [2]Securities and Exchange Commission, “Ford Motor Company Form 10-K 2024,” sec.gov. Control over residual-value data and maintenance insights lets captive lenders price loans more precisely than independent banks. Preferential bundles that combine insurance, software, and service contracts differentiate offers and lock in recurring revenue. Competitors are forced to focus on niche borrower bands or enhance speed and simplicity through technology alliances. This deeper integration also provides automakers with granular feedback loops that inform product design and marketing.

Growing penetration of online used-car platforms

Carvana reported USD 13.67 billion revenue in 2024 after integrating credit, vehicle selection, and delivery into a single user journey. Algorithm-driven pricing and instant credit decisions remove dealer mark-ups, attracting younger borrowers who value transparency. Lenders partner with marketplaces or risk losing prime digital traffic. The model also yields richer loan-performance data that refines risk scoring. Their scale economies in reconditioning and logistics lower per-unit costs, reinforcing the appeal of the online-first channel.

Digital lending & instant approvals via fintech APIs

Partnerships such as NXTsoft and Upstart connect banks and credit unions to AI-driven underwriting engines that cut manual reviews by more than 70%. Borrowers receive approval in minutes, and institutions reduce per-loan processing costs. Global adoption is accelerating, led by North America, where regulatory clarity favors open-banking interfaces. Providers lacking API capabilities cede volume to faster rivals. As more credit unions plug into open APIs, standardized data flows improve fraud detection and compliance reporting.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising interest rates & tighter monetary policy | -2.1% | Global, emphasis on developed markets | Short term (≤ 2 years) |

| High delinquency risk among sub-prime borrowers | -1.3% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Shared-mobility uptake reducing vehicle purchases | -0.8% | Urban centers globally, led by North America & Europe | Long term (≥ 4 years) |

| Stricter debt-to-income caps in key markets | -0.6% | Europe & Asia-Pacific, selective US markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising interest rates & tighter monetary policy

Elevated policy rates have pushed average auto-loan coupons to multi-decade highs. In April 2025, the European Central Bank recorded a composite cost of 3.27% for new household loans, down only 5 basis points from the prior month[3]European Central Bank, “Composite Cost of Borrowing April 2025,” ecb.europa.eu. North American consumers respond by lengthening loan terms to protect their monthly budgets. Lenders face margin squeeze as funding costs outrun yield gains, prompting revised pricing grids and stricter debt-to-income caps. Dealers are offering buydown incentives, but these measures only partly offset rising monthly obligations.

High delinquency risk among subprime borrowers

Default rates in the lowest credit tiers climbed through 2024, triggering tighter underwriting and higher loss provisions. European regulators advise banks to enhance IFRS 9 models to capture new geopolitical and climate-related risks. U.S. lenders deploy AI tools to segment risk more finely, but many scale back sub-prime exposure, creating credit-access gaps for vulnerable borrowers. Portfolio rebalancing supports long-term stability but temporarily limits loan origination volumes. Secondary-market investors demand higher spreads on asset-backed securities backed by subprime loans, raising funding costs for specialty lenders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Commercial Vehicles Drive Growth

Passenger vehicles retained 70.22% of the 2025 car loan market share, benefiting from established dealer networks and broad consumer appetite. Commercial-vehicle financing posted a 9.05% CAGR outlook for 2026-2031, surpassing passenger-vehicle growth yet composing a smaller revenue base. Fleet electrification mandates and booming last-mile logistics expand demand for asset-backed loans that incorporate operational data.

Regulatory targets for carbon reduction push transport companies toward electric vans and trucks that carry higher sticker prices. Lenders design utilization-based repayment models and residual-value guarantees to mitigate technology risk. Passenger-vehicle lenders focus on digital origination and loyalty programs that package insurance, maintenance, and connectivity under single-invoice plans.

By Ownership: Used Vehicles Accelerate Digital Transformation

New-vehicle loans held a 60.37% share in the global car loan market in 2025, while used-vehicle financing is projected to grow at a 10.03% CAGR, outpacing the growth of new-vehicle loans. Online marketplaces expand inventory transparency, while improved reconditioning standards boost buyer confidence. The car loan market size for used vehicles is poised to widen as platforms integrate credit and warranty products in-app.

New-vehicle financing relies on automaker incentives and captive finance arms, yet faces affordability tension from rising MSRP and interest rates. As credit conditions tighten, value-conscious consumers pivot to late-model cars, feeding used-vehicle momentum. Lenders diversify portfolios across both ownership segments to balance growth and risk.

By Provider Type: Fintech Disruption Accelerates

Banks held a 46.41% share in the global car loan market in 2025, but fintech lenders are projected to expand at a 14.12% CAGR by scaling API-driven origination and automated risk models. The car loan industry sees alliances such as traditional banks embedding fintech tools to retain customers who expect instant decisions.

Non-bank finance companies evolve funding mixes after regulators in emerging markets liberalize wholesale borrowing. Captive lenders exploit proprietary telematics and maintenance data to sharpen pricing, while fintechs compete on user experience and speed. Competitive gaps narrow as incumbents digitize, but first-mover advantage favors agile platforms.

By Tenure: Extended Terms Reflect Affordability Pressures

Loans of 3-5 years comprised 51.99% of the 2025 car loan market share, yet contracts exceeding five years grow at 10.18% CAGR as consumers offset high rates and vehicle prices by stretching payments. The car loan market size for extended-term products is gaining prominence amid inflationary income stress.

Longer maturities increase cumulative interest and default exposure. Lenders introduce step-up payment schedules and periodic credit reviews to manage risk. Prime borrowers still prefer shorter durations to minimize cost, maintaining healthy demand in the under-3-year segment. Product variety enables institutions to match offers with household cash-flow profiles.

Geography Analysis

Asia-Pacific led with 34.25% of the 2025 car loan market share and is forecasted to advance at a 9.74% CAGR through 2031. China’s removal of down-payments opened credit to new segments, while India’s ban on foreclosure charges for floating-rate loans enhances borrower flexibility. Rising middle-class car ownership, growing EV penetration, and wider fintech adoption underpin regional momentum.

North America remains a mature yet innovative arena. Deep credit bureaus enable granular risk-based pricing, and firms such as Ford Credit leverage scale to fund USD 133.2 billion in receivables. Electric-vehicle incentives and digital-first banks like Ally Financial broaden product choice and push competitive pricing.

Europe navigates a complex policy mix of consumer protection and cross-border banking reforms. The European Central Bank promotes integrated capital markets, encouraging lenders to scale beyond domestic borders. Subscription models and carbon-credit-linked rate discounts spread quickly as regulators accelerate zero-emission goals. Interest-rate relief remains modest, but stable employment and sustainability policies sustain steady loan demand.

Mordor Intelligence provides coverage of the car loan market across other key regional markets, including Europe and Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to United Kingdom, China, France, Brazil, Russia, South Korea, India, and Japan incorporating local coverage and market participation, as required.

Competitive Landscape

Market concentration is moderate as incumbent finance arms, banks, and fintech entrants contest share. Ford Credit’s substantial receivables base illustrates incumbent scale, though 2023 earnings before tax fell to USD 1,322 million amid higher funding costs. GM Financials’ withdrawal of a bank application highlights regulatory uncertainty shaping strategy.

Fintech platforms emphasize user-centric design and AI risk scoring; Upstart’s bank partnerships automate more than 70% of loan workflows. Captive lenders deepen loyalty with bundled services and data-driven pricing. Traditional banks respond by investing in APIs or acquiring technology firms to upgrade speed.

White-space opportunities include commercial-EV financing, subscription-ownership credit bundles, and cross-border loans enabled by regulatory harmonization. Competitive advantage now rests on blending scale, technology, and compliance. Providers that master cost-efficient digital origination while managing asset risk gain sustainable margins in the evolving car loan market.

Car Loan Industry Leaders

Toyota Financial Services

Ford Credit

Ally Financial

Chase Auto Finance

Wells Fargo Auto

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Carvana recorded USD 13.67 billion in 2024 revenue, up 27% year over year, and an adjusted EBITDA margin of 10.1%, reinforcing the viability of direct-to-consumer digital auto financing.

- June 2024: GM Financial withdrew its deposit-insurance application, indicating continued evaluation of banking strategy in a shifting regulatory landscape.

- April 2024: China removed mandatory down-payment rules for personal car loans, its most significant easing since 2018.

- February 2024: Ford Credit reported USD 133.2 billion net receivables and USD 25.7 billion liquidity, yet margins tightened due to higher borrowing costs.

Global Car Loan Market Report Scope

A car loan, also known as an auto loan or vehicle loan, is a type of financing provided by a financial institution or lender to help individuals purchase a car. A complete background analysis of the car loan market globally includes an assessment of the industry associations, the overall economy, and emerging market trends by segment. Significant changes in the market dynamics and market overview are also covered in the report. The car loan market is segmented by product, which includes passenger vehicles and commercial vehicles. Ownership includes new vehicles and used vehicles, and provider types include banks, NBFCs (non-bank financial companies), credit unions, and others such as fintech companies. By tenure includes less than three years, 3-5 years, more than 5 years, and by geography includes North America, Europe, Asia-Pacific, Latin America, the Middle East, and Africa.

The report offers market size and forecasts for the car loan market in terms of revenue (USD) for all the above segments.

| Passenger Vehicle |

| Commercial Vehicle |

| New Vehicles |

| Used Vehicles |

| Banks |

| Non-Banking Financial Institutions |

| Original Equipment Manufacturers |

| Other Provider Types (Fintech Companies) |

| Less than 3 Years |

| 3-5 Years |

| More than 5 years |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Vehicle Type | Passenger Vehicle | |

| Commercial Vehicle | ||

| By Ownership | New Vehicles | |

| Used Vehicles | ||

| By Provider Type | Banks | |

| Non-Banking Financial Institutions | ||

| Original Equipment Manufacturers | ||

| Other Provider Types (Fintech Companies) | ||

| By Tenure | Less than 3 Years | |

| 3-5 Years | ||

| More than 5 years | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected growth rate for the car loan market through 2031?

The market is forecast to grow at an 8.47% CAGR, advancing from USD 1.53 trillion in 2025 to USD 2.49 trillion by 2031.

Which region is expected to show the fastest expansion?

Asia-Pacific is projected to post a 9.74% CAGR, supported by regulatory easing and growing middle-class demand.

Why are fintech lenders gaining share in automotive financing?

Fintechs provide instant approvals using API-based underwriting, resulting in a 14.12% CAGR that outpaces traditional banks.

How are rising interest rates affecting car loan affordability?

Elevated rates lengthen loan terms and compress lender margins, with cost-of-borrowing indicators still above pre-2022 levels.

What factors drive growth in used-vehicle financing?

Online marketplaces enhance price transparency and speed of credit decision, pushing used-vehicle loan growth above 10% CAGR.

How are electric-vehicle trends influencing loan products?

Lenders introduce carbon-credit-linked rate discounts and longer terms to support higher-priced EV purchases while meeting sustainability goals.

Page last updated on: