Home Loan Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

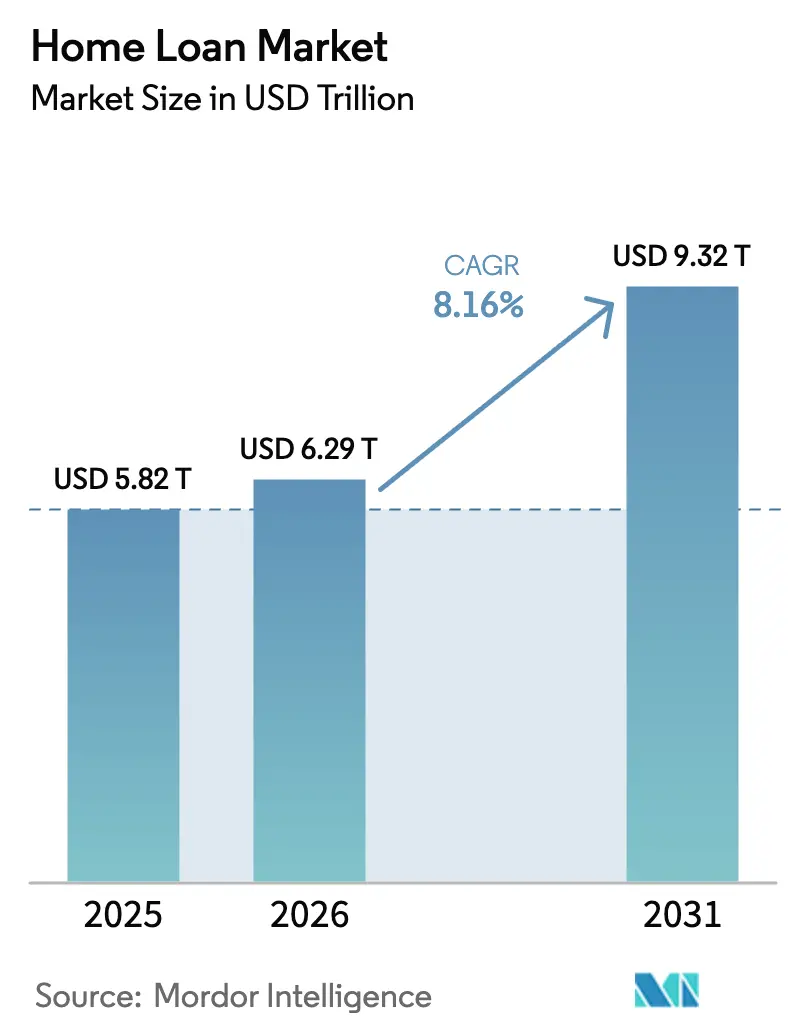

| Market Size (2026) | USD 6.29 Trillion |

| Market Size (2031) | USD 9.32 Trillion |

| Growth Rate (2026 - 2031) | 8.16% CAGR |

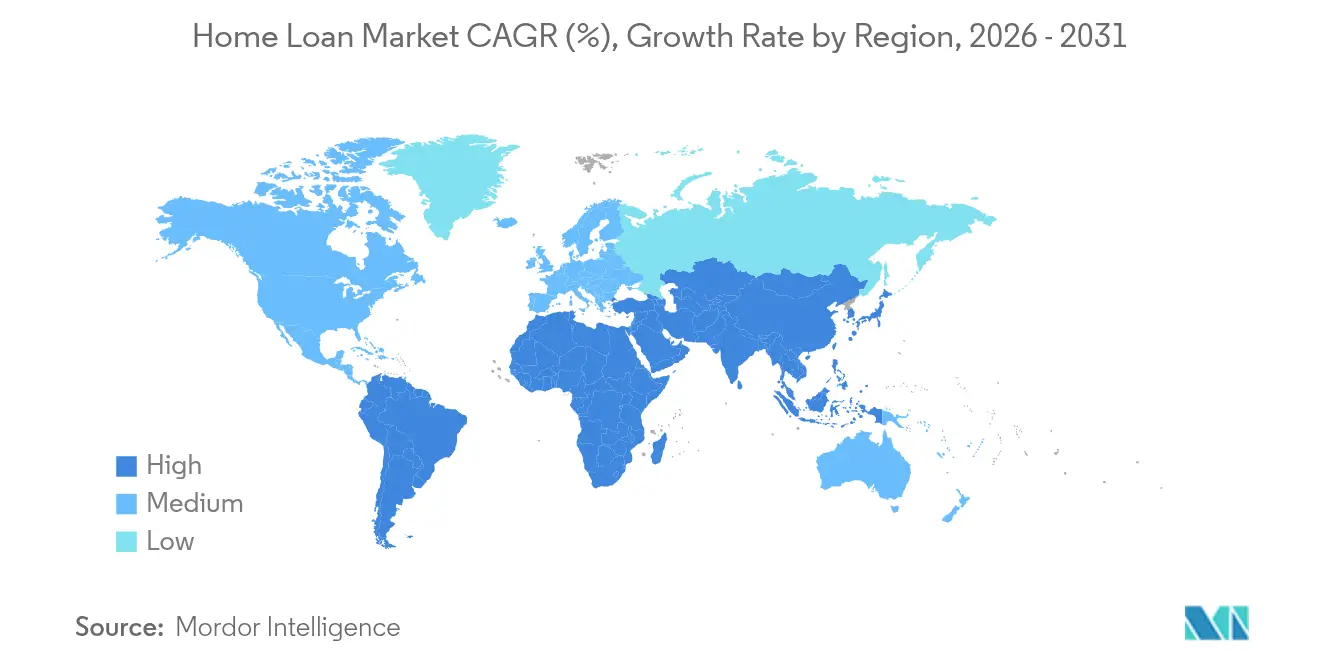

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Home Loan Market Analysis by Mordor Intelligence

The home loan market size was valued at USD 5.82 trillion in 2025 and estimated to grow from USD 6.29 trillion in 2026 to reach USD 9.32 trillion by 2031, at a CAGR of 8.16% during the forecast period (2026-2031). Robust demographic expansion, steady urban migration, and the rapid digitization of mortgage workflows continue to keep annual origination volumes on an upswing despite tightening monetary conditions. Technology-enabled lenders are compressing approval cycles from weeks to days, lowering operating costs and broadening access to credit, especially in underserved regions. Government-backed affordable-housing schemes across emerging markets, together with ESG-linked incentives for energy-efficient dwellings, are further enlarging the total addressable borrower base. At the same time, cross-border labor mobility and the revival of private-label securitization are unlocking new revenue streams for specialized lenders, offsetting headwinds from elevated policy rates and stricter macro-prudential rules.

Key Report Takeaways

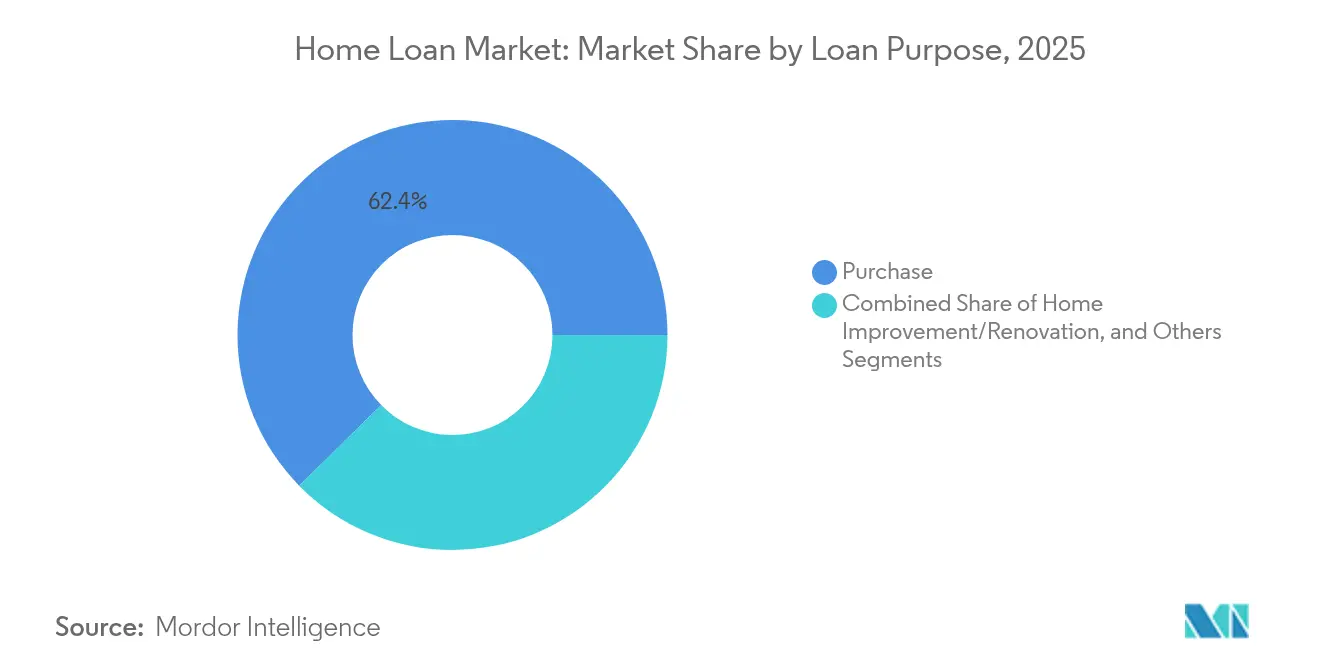

- By loan purpose, purchase mortgages led with 62.36% of the home loan market share in 2025 while expanding at a 8.91% CAGR through 2031.

- By provider, banks accounted for 66.81% share of the home loan market in 2025; alternative lenders are projected to post the fastest 14.84% CAGR to 2031.

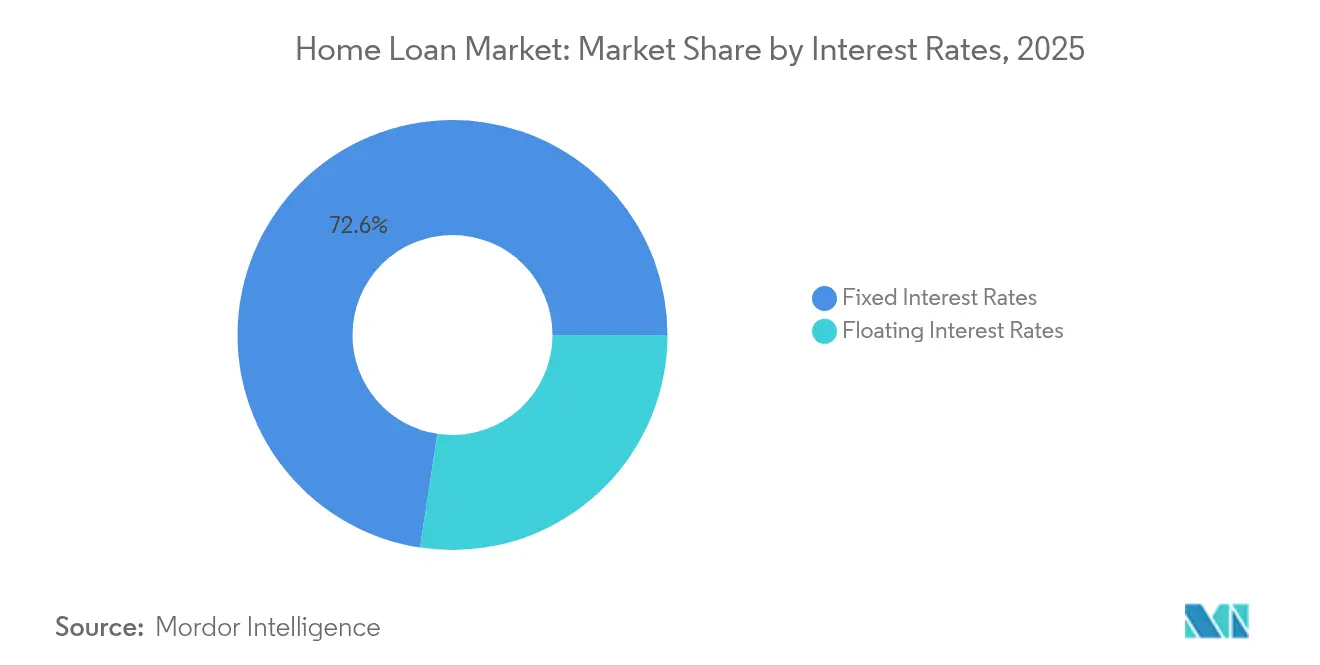

- By interest rate type, fixed-rate products captured 72.59% of the home loan market size in 2025, whereas the floating-rate segment is forecasted to grow at 9.85% CAGR.

- By loan tenure, terms longer than 20 years represented 48.58% of the home loan market size in 2025 and are advancing at a 9.12% CAGR.

- By geography, North America retained a 40.32% share of the home loan market in 2025, while Asia-Pacific is set to grow the fastest at a 9.86% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Home Loan Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid rise of digital-first mortgage platforms | +1.8% | North America, Europe, global spill-over | Short term (≤ 2 years) |

| AI-driven credit scoring broadening the borrower pool | +1.5% | North America, EU, emerging Asia-Pacific | Medium term (2-4 years) |

| Government-backed affordable-housing push | +2.2% | Asia-Pacific, Latin America, Middle East & Africa | Long term (≥ 4 years) |

| Acceleration of green-home incentives | +1.1% | Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Cross-border labor mobility boosting expatriate home-buy demand | +0.9% | Global, concentrated in major financial centres | Short term (≤ 2 years) |

| Expansion of private-label securitization is reviving lender liquidity | +1.3% | North America, emerging in Europe, and Asia-Pacific | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise of Digital-First Mortgage Platforms

Digital-first originators shorten application cycles by up to 20-fold while reducing processing expenses nearly 80%, letting lenders price aggressively and still improve margins. They reach borrowers in locations where branch networks are uneconomical, widening the home loan market. Automated marketing analytics lower acquisition costs and raise conversion ratios, supporting sustained share gains. End-to-end integrations with agents, appraisers, and title firms compress closing timelines, lifting industry throughput. Continuous, 24/7 application status feeds meet rising consumer expectations, decreasing abandonment rates, and stabilizing revenue flows.

AI-Driven Credit Scoring Broadening Borrower Pool

Machine-learning models ingest rental histories, utility payments, and gig-economy income to evaluate creditworthiness beyond traditional scores, enabling previously excluded segments to qualify responsibly. Real-time fraud screens enhance risk controls, aligning with regulatory mandates. Government-sponsored enterprise connectivity streamlines secondary-market execution, freeing up capital for further origination. AI chatbots capture borrower data in MISMO-compliant formats, cutting manual entry and speeding approvals. This approach is particularly beneficial for self-employed professionals, enlarging the effective home loan market.

Government-Backed Affordable-Housing Push

Ambitious initiatives such as India’s Pradhan Mantri Awas Yojana, which aims for 230 million new units by 2047, are guaranteeing vast pipelines of mortgage demand [1]World Bank Staff, “Housing for All by 2030,” World Bank Blogs, blogs.worldbank.org. Kenya’s program funds 250,000 units annually through a 1.5% payroll levy, creating predictable rent-to-own structures. Subsidized interest rates and credit guarantees de-risk lending, encouraging banks and housing-finance companies to scale. Comparable efforts in Brazil and Vietnam reinforce the long-term growth outlook across emerging regions.

Acceleration of Green-Home Incentives

Major lenders in the UK, Germany, and the United States now offer rate or cashback incentives for properties that achieve top-tier energy-performance certifications. The U.S. Inflation Reduction Act sweetens economics through tax credits on qualifying upgrades, making bundled finance packages attractive. Research linking energy efficiency to lower default rates further boosts investor appetite for green mortgage-backed securities. Access to ESG-driven funding pools lets lenders offer competitive pricing while meeting sustainability objectives.

Restraints Impact Analysis of Home Loan Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistently high policy rates | -2.8% | North America, Europe, global spill-over | Short term (≤ 2 years) |

| Tightening macro-prudential rules | -1.9% | Developed markets, spreading to select emerging economies | Medium term (2-4 years) |

| Rising climate-risk insurance premiums in coastal zones | -1.2% | Coastal regions worldwide, notably North America and Europe | Long term (≥ 4 years) |

| Fin-crime compliance costs squeezing thin-margin lenders | -0.8% | Global, higher impact in developed markets | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Persistently High Policy Rates

The U.S. 30-year fixed mortgage rate has hovered above 7% since January 2025 and is widely expected to stay above 6% until 2026, dampening affordability and refinancing volumes. Similar pressures are visible in the UK, where the Bank of England delays substantive rate cuts amid lingering inflation concerns. Eurozone averages have climbed to about 4%, and Canadian borrowers face payment shocks as USD 300 billion in mortgages reset over the next year. Elevated rates deter prospective buyers and lock existing owners into low-coupon loans, muting transaction volumes and slowing home loan market expansion.

Tightening Macro-Prudential Rules

Canada’s 4.5 times loan-to-income cap, effective in 2025, limits borrowing power for first-time purchasers in Toronto and Vancouver. In the United States, Basel III implementation could raise large-bank capital requirements to 25%, pushing up mortgage pricing[2]FDIC Staff, “Basel III end-game outline,” FDIC, fdic.gov. European regulators are heightening stress-test hurdles, prompting lenders to curb high LTV exposures. As compliance costs grow, smaller lenders retreat, reducing competition and constraining credit availability, especially for low-to-moderate-income households.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Home Loan Market Segment Analysis

By Loan Purpose:

Purchase Mortgages Underpin ExpansionPurchase financing dominated 2025 with 62.36% home loan market share and is forecasted to expand at a 8.91% CAGR through 2031, underscoring enduring owner-occupier demand even amid higher borrowing costs. Urban immigration, rising household formation, and growing middle-class wealth in emerging economies are pivotal contributors. Renovation and improvement loans are gaining ground as homeowners unlock accumulated equity to fund energy-efficient upgrades, encouraged by green-subsidy programs. Refinance activity, which had surged during pandemic-era rate cuts, now accounts for a modest slice of the home loan market as less than 3% of outstanding borrowers can economically refinance at prevailing rates. Lenders are therefore refocusing technology investment on purchase-money efficiencies, leveraging AI-driven underwriting to close deals quickly in competitive housing markets.

Lower average ticket sizes in emerging cities, combined with government guarantee schemes, are broadening lender portfolios while mitigating credit risk. In contrast, construction loans remain cyclical, reflecting developer confidence and local regulatory frameworks. Growth prospects through 2031 remain strongest in markets where public housing initiatives dovetail with digital lending adoption, signaling a healthy pipeline for the home loan market.

By Provider:

Banks Lead, Fintech Challengers AccelerateTraditional banks held a 66.81% share in the global home loan market in 2025, benefiting from low-cost deposit funding that supports competitive fixed-rate offers. Nevertheless, fintech and non-bank entities are expanding at a 14.84% CAGR, propelled by agile technology stacks and lighter capital constraints. Housing-finance companies bridge the two models in markets such as India, where Bajaj Housing Finance’s USD 16 billion IPO illustrated investor confidence in specialized lenders. Non-bank lenders in Australia, whose collective book stands at USD 74 billion, are on track to double assets within five years, evidencing global momentum toward alternative funding channels. The home loan market size attributable to these challenger segments is increasing as they target self-employed borrowers and near-prime profiles underserved by banks.

Regulatory arbitrage and securitization access help sustain the growth trajectory, while partnerships with digital-first platforms shorten time-to-yes decisions. Banks are responding by integrating robo-underwriting and adopting cloud-native loan origination systems, but cultural change and legacy infrastructure remain hurdles. Through 2031, the competitive gap is likely to narrow, yet diversified funding bases and niche specializations keep alternative lenders structurally advantaged in specific borrower cohorts within the home loan market.

By Interest Rate Type:

Fixed Dominance, Floating ResurgenceFixed-rate mortgages controlled 72.59% of the global home loan market share in 2025 as consumers sought predictable payments amid volatile rate expectations. The segment’s share is pronounced in the United States, where the 30-year fixed product is almost standard. Conversely, floating-rate loans are projected to outpace overall expansion at a 9.85% CAGR, reflecting lender appetite to shift duration risk and borrower willingness to trade initial discounts for future variability. In many euro-area countries, caps and hybrid structures that reset after five or ten years blur traditional classifications, adding nuance to market statistics.

Households with adjustable loans have curbed discretionary spending by 46%, illustrating macroeconomic spillovers that regulators monitor closely. Hedging solutions and borrower education are becoming differentiators, offering lenders an avenue to market newer tranche-linked floating products. Over the forecast horizon, sophisticated rate-risk transfer tools and fintech-enabled comparison sites are expected to elevate consumer acceptance of floating structures in the home loan market.

By Loan Tenure:

Extended Terms Address AffordabilityLoans exceeding 20 years comprised 48.58% of the global home loan market share in 2025 and are growing at a 9.12% CAGR as rising prices outpace income growth, especially in global gateway cities. Mortgage maturities of 30 years or more are becoming commonplace in Japan, the UK, and the Netherlands, enabling lower monthly outflows but prolonging balance-sheet risk for lenders. The 11–20 year tranche appeals to middle-income cohorts seeking quicker equity accumulation, whereas ≤ 10-year products cater to affluent borrowers targeting interest savings.

Longer average durations mean higher lifetime interest, yet they also stabilize delinquency rates by lowering monthly payment burdens during economic shocks. Policymakers weigh these benefits against the systemic implications of slower amortization. Through 2031, the interplay between affordability, regulatory oversight, and secondary-market appetite for long-dated mortgage-backed securities will shape tenure choices across the home loan market.

Geography Analysis

North America Home Loan Market

North America commanded 40.32% of the global home loan market share in 2025, underpinned by the U.S. secondary-market machinery in which Ginnie Mae guarantees continue to attract 25–33% foreign investment into mortgage-backed securities. Elevated rates above 7% and low existing inventory suppress transaction throughput, evidenced by 26% of 2024 purchases closing in cash. Canada faces USD 300 billion in 2025 renewals, testing household resilience as fixed terms written during 2020 roll off.

APAC Home Loan Market

Asia-Pacific is the fastest-growing geography, projected at a 9.86% CAGR, as India records an 11-year high of 173,000 unit sales during H1 2024 and anticipates the real-estate sector tripling to USD 1.5 trillion by 2034. China’s policy move to trim mortgage rates by 50 basis points and relax second-home down payments to 15% could benefit 50 million households. Mature markets like Australia see durable demand linked to high net migration and tight supply, whereas Japan emphasizes urban redevelopment to offset demographic decline.

Europe Home Loan Market

Europe shows tentative recovery with Q4 2024 nominal home prices up 4.9% year over year, though divergence is stark: German prices fell 7.1% while Poland rose 13%. Mortgage production has sagged amid 4% average rates, and French outstanding balances dipped 0.65% to EUR 1.424 trillion by mid-2024. The Netherlands expects rates to edge lower to 3–3.5% by late 2025, yet continued supply shortages push average transaction values toward EUR 488,000.

Mordor Intelligence provides coverage of the home loan market across other key regional markets. Detailed country-level analysis extends to China, India, United States, and Brazil incorporating local coverage and market participation, as required.

Competitive Landscape

The home loan market is experiencing an intense phase of technological disruption and consolidation that is redefining competitive boundaries. Rocket Companies set the tone in 2025 by absorbing Mr. Cooper for USD 9.4 billion and Redfin for USD 1.75 billion, forging a platform that marries property search, brokerage, origination, and servicing under one roof. Bayview Asset Management’s USD 1.3 billion purchase of Guild Holdings underscores private-equity appetite for scale plays, while India’s Bajaj Housing Finance used its USD 16 billion IPO proceeds to expand digitally into tier-2 cities.

Digital-first lenders are differentiating through speed and cost. AI-enabled underwriters complete decisions in minutes, letting firms quote sharper rates without sacrificing profitability. Platforms such as TidalWave and Synergy One employ machine-learning and blockchain, respectively, to target underserved niches—from equitable lending for minority borrowers to tokenized home-equity lines of credit. HSBC Expat, meanwhile, is capitalizing on global talent flows by bundling cross-border mortgages with currency-hedging features, commanding premium fees from internationally mobile professionals.

Incumbent banks still enjoy low-cost deposit funding but are racing to modernize legacy systems, often through partnerships or selective M&A. Wells Fargo expanded its digital reach by integrating an AI chatbot into its consumer portal, while BNP Paribas invested in cloud-native servicing to trim overheads in low-margin European markets. Strategic themes, therefore, coalesce around vertical integration, technology leadership, and segment specialization. With the top five originators controlling roughly 35% of global volume, rivalry remains balanced; yet operators that best align digital agility, funding diversity, and regulatory compliance are positioned to outpace the broader home loan market through 2030.

Home Loan Industry Leaders

Rocket Mortgage (Quicken Loans)

Wells Fargo & Co.

Bank of America Corporation

JPMorgan Chase & Co.

Citigroup Inc.

- *Disclaimer: Major Players sorted in no particular order

Home Loan Market Companies Covered in this Report

- Rocket Mortgage (Quicken Loans)

- Wells Fargo & Co.

- Bank of America Corporation

- JPMorgan Chase & Co.

- Citigroup Inc.

- HSBC Group

- Goldman Sachs (Marcus)

- Charles Schwab & Co.

- Morgan Stanley

- U.S. Bank

- Barclays plc

- BNP Paribas Personal Finance

- Santander Consumer Finance

- ANZ Bank

- Commonwealth Bank of Australia

- China Construction Bank

- ICICI Bank Ltd.

- LIC Housing Finance Ltd.

- Dewan Housing Finance Corp. Ltd.

- Nationwide Building Society

Recent Industry Developments in Home Loan Market

- June 2025: Bayview Asset Management announced a USD 1.3 billion cash deal to acquire Guild Holdings, continuing a wave of scale-seeking mergers.

- May 2025: India listed its first residential mortgage-backed securities, a milestone expected to deepen capital-market liquidity for local lenders.

- March 2025: Rocket Companies agreed to acquire Mr. Cooper Group for USD 9.4 billion in stock, forming a USD 2.1 trillion servicing portfolio and targeting USD 500 million in annual efficiencies.

- February 2025: FHFA issued its final rule enhancing Federal Home Loan Bank liquidity access by amending unsecured credit treatment.

Global Home Loan Market Report Scope

The global home loan market refers to the financial market where individuals and families borrow money from financial institutions to purchase or refinance residential properties. Home loans, also known as mortgages, are long-term loans typically repaid over several years or decades. Home Loan Market is Segmented by provider (Banks, Housing Finance Companies, and Others), By Interest Rate (Fixed Interest Rate and Floating Interest Rate), By Tenure (Less Than 5 years, 6-10 years, 11-24 years, and 25-30 years), By Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, Latin America). The report offers market size and forecasts for the Home Loan Market in value (USD Billion) for all the above segments.

Segmentation Overview

| Purchase (New/Existing) |

| Home Improvement/Renovation |

| Others (Construction, Refinance, etc.) |

| Banks |

| Housing Finance Companies |

| Others |

| Fixed Interest Rates |

| Floating Interest Rates |

| Less than or equal to 10 Years |

| 11 – 20 Years |

| Longer than 20 Years |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Loan Purpose | Purchase (New/Existing) | |

| Home Improvement/Renovation | ||

| Others (Construction, Refinance, etc.) | ||

| By Provider | Banks | |

| Housing Finance Companies | ||

| Others | ||

| By Interest Rates | Fixed Interest Rates | |

| Floating Interest Rates | ||

| By Loan Tenure | Less than or equal to 10 Years | |

| 11 – 20 Years | ||

| Longer than 20 Years | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the home loan market?

The home loan market is valued at USD 6.29 trillion in 2026 and is projected to reach USD 9.32 trillion by 2031.

Which loan purpose segment leads the home loan market?

Purchase mortgages dominate with 62.36% market share in 2025 and are growing at a 8.91% CAGR through 2031.

Who are the major providers in the home loan industry?

Banks held 66.81% market share in 2025, while fintech and other non-bank lenders are the fastest-growing providers.

Why are longer-tenure home loans becoming popular?

Extended terms over 20 years help borrowers manage higher housing costs by reducing monthly payments, driving a 9.12% CAGR in that segment.

Which region offers the strongest growth prospects for home loans?

Asia-Pacific is forecast to be the fastest-growing region at a 9.86% CAGR, supported by robust urbanization and government housing initiatives.

How are green mortgages influencing the home loan market?

Green mortgage products offer preferential pricing for energy-efficient homes and attract ESG-focused investors, thereby expanding both borrower demand and lender funding options.

Page last updated on: