Student Loans Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

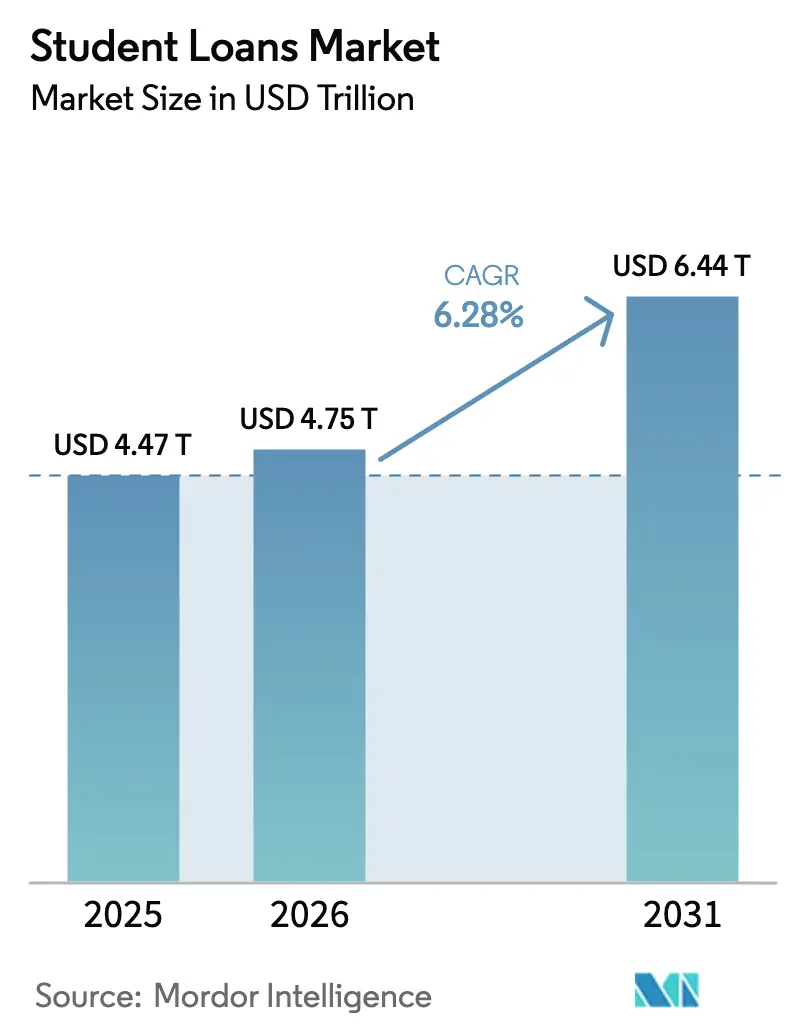

| Market Size (2026) | USD 4.75 Trillion |

| Market Size (2031) | USD 6.44 Trillion |

| Growth Rate (2026 - 2031) | 6.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Student Loans Market Analysis by Mordor Intelligence

The student loans market size in 2026 is estimated at USD 4.75 trillion, growing from 2025 value of USD 4.47 trillion with 2031 projections showing USD 6.44 trillion, growing at 6.28% CAGR over 2026-2031. Sustained demand arises from tuition inflation that continues to exceed wage growth, the rapid globalization of higher-education enrolment, and lender innovation that lowers approval frictions. Fintech-enabled risk models accelerate loan origination while demographic shifts—especially the surge in students under 25—anchor long-run volume growth. Regulatory turbulence around the SAVE plan has created mixed incentives: flexible federal programs attract many borrowers, yet policy uncertainty also nudges credit-worthy graduates toward private refinancing. Meanwhile, cross-border education flows spur specialized lending platforms that can navigate multi-jurisdictional rules, further broadening the student loans market.

Key Report Takeaways

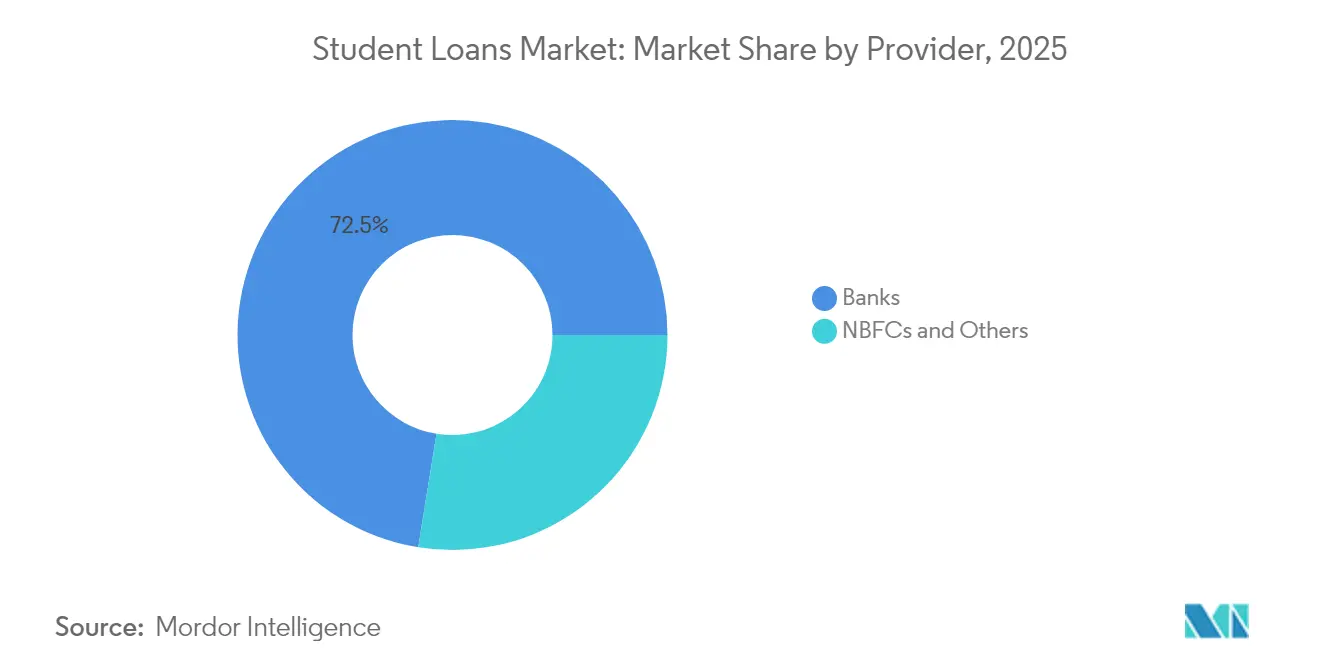

- By provider, banks led with a 72.45% share in 2025 of the student loans market; NBFCs and alternative lenders are set to expand at 7.61% CAGR through 2031.

- By repayment plan, income-driven options held 42.10% of the student loans market size in 2025 and are expected to grow at 7.74% CAGR to 2031.

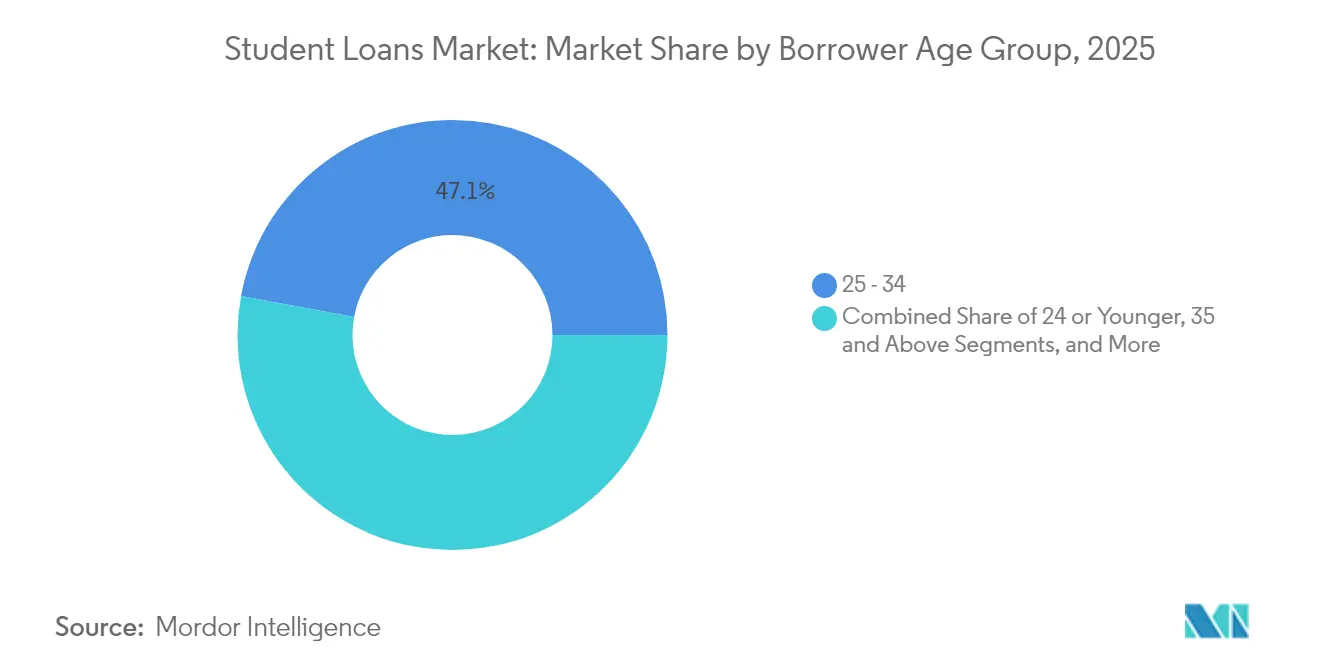

- By borrower age, the 25-34 segment accounted for 47.10% share of the student loans market in 2025, while the 24-or-younger cohort is on track to grow at 7.55% CAGR.

- By education level, undergraduate loans captured 61.60% share of the student loans market in 2025; graduate and professional programs are forecasted to rise at 8.12% CAGR.

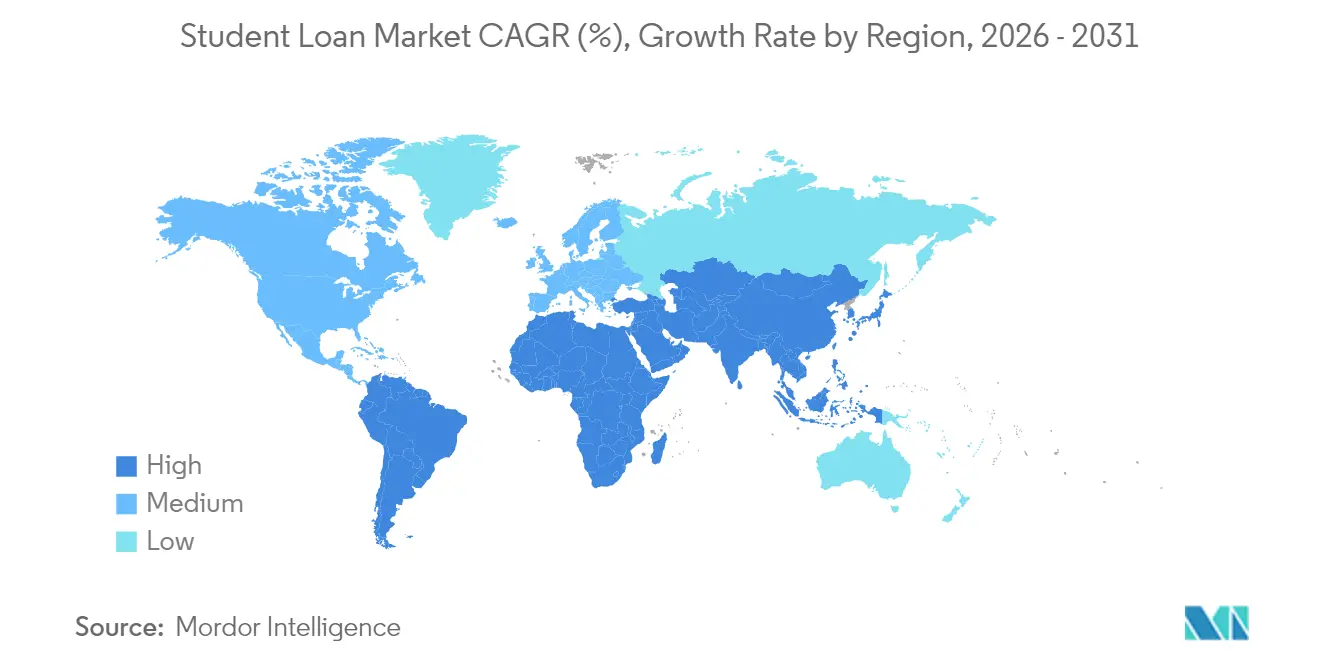

- By region, North America commanded 42.20% share of the student loans market in 2025, whereas Asia-Pacific is projected to post a 7.22% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Student Loans Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government funding expansion & new IDR rules | +1.5% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Tuition inflation outpacing wage growth | +1.2% | Global, acute in North America & Australia | Long term (≥4 years) |

| Surge in international student mobility | +0.8% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Fintech-driven alternative credit scoring | +0.9% | North America & EU leading, expanding to APAC | Short term (≤2 years) |

| Tokenised income-share & blockchain loans | +0.6% | Pilot markets in North America, early adoption in Africa | Long term (≥4 years) |

| Ageing borrower base driving refinancing wave | +0.4% | North America primarily, emerging in Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Government Funding Expansion & New IDR Rules

Income-Driven Repayment (IDR) account adjustments credited more than 3.6 million borrowers in early 2025, materially lowering scheduled payments for a broad swath of the federal loan book[1]U.S. Department of Education, “SAVE Plan Fact Sheet,” ed.gov. Private lenders now recalibrate lifetime loss-given-default assumptions because retroactive adjustments may recur. The Department of Education’s decision to keep Income-Contingent Repayment enrollment open through July 2027 signals durable federal support for flexible options that may curb incremental federal-to-private migration. Legal challenges to the SAVE plan inject uncertainty that pushes some borrowers toward immediate private consolidation. Universities must comply with Financial Value Transparency rules that expose debt-to-earnings ratios, potentially steering students to lower-cost programs. Collectively, these shifts underpin a structural pivot toward adaptive repayment designs across the student loans market.

Tuition Inflation Outpacing Wage Growth

Average tuition continues to rise faster than household earnings in most developed economies, sustaining a baseline need for leverage even as cost-conscious families explore grant and scholarship alternatives. Graduate borrowers face higher rates—8.08% for 2024-25 Direct Unsubsidized Loans—yet still perceive outsized lifetime earnings premiums that justify large loan packages[2]Federal Register, “Annual Student Loan Interest Rates 2024-25,” federalregister.gov. Private fixed-rate offers now compete directly with rising federal benchmarks, especially for credit-worthy applicants seeking certainty. Employers augment affordability by covering roughly one-third of tuition in many large-firm benefit plans, but the residual gap still pushes workers toward credit channels. Persistent wage-tuition divergence, therefore, cements upward momentum in the student loans market.

Surge in International Student Mobility

OECD destinations hosted more than 4.6 million foreign students by 2022, a rebound that restores multi-currency lending demand. India alone accounts for nearly 1.3 million outbound scholars, supporting rapid volume gains for cross-border fintech lenders that offer collateral-free loans in hard currency. Sub-Saharan Africa’s youthful demographics promise a next-wave pipeline, yet currency volatility and sparse credit data require bespoke risk models. Destination-country housing shortages, such as the estimated 350,000-bed deficit in UK university towns, may constrain enrolment and temper near-term disbursements. Still, rising self-funding rates among Asia-Pacific students underpin steady origination growth for region-focused lenders.

Fintech-Driven Alternative Credit Scoring

U.S. Bank’s partnership with Pagaya and Suncoast Credit Union’s deployment of Zest AI illustrate mainstream acceptance of machine-learning underwriting that looks beyond FICO to education pedigree and employment prospects. These models expand credit access for thin-file borrowers while improving portfolio granularity. BankMobile’s Upstart integration specifically targets recent graduates with limited history, blending school selectivity and projected income into probability-of-default projections. Regulatory focus on explainability slows blanket adoption but enhances sustainability. SoFi’s record 2025 loan originations demonstrate commercial viability, with declining charge-off ratios reinforcing investor confidence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising benchmark interest rates & spreads | -0.7% | Global, with acute impact in North America & Europe | Short term (≤ 2 years) |

| Borrower credit-worthiness gaps | -0.3% | Global, particularly acute in emerging markets | Medium term (2-4 years) |

| Regulatory whiplash on forgiveness programs | -0.5% | North America primarily, emerging concerns in Europe | Medium term (2-4 years) |

| Employer-funded tuition benefits crowd out demand | -0.2% | North America & Europe, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Benchmark Interest Rates & Spreads

Federal Direct Stafford loan rates climbed to 6.53% for undergraduates and 8.08% for graduates in the 2024-25 cycle, pressuring borrowers who weigh refinancing against higher private coupons. Lenders experience squeezed margins because wholesale funding costs rise quicker than the yields they can pass through. Default indicators in U.S. student loan ABS worsened through Q4 2024, with constant default rates touching 5.53% in the FFELP pool, raising securitization costs. Nonetheless, credit-worthy alumni still refinance at lower spreads, creating a bifurcated market where weaker borrowers face shrinking access. This rate environment tempers headline growth yet invites innovation in variable-rate and hybrid products across the student loans market.

Regulatory Whiplash on Forgiveness Programs

Litigation around the SAVE plan’s debt-relief provisions prolongs policy ambiguity, forcing the Department of Education to offer provisional extensions that complicate borrower decisions. Enforcement actions, such as the CFPB’s proposed order against Navient, heighten servicer compliance costs and push some incumbents to exit ancillary businesses. MOHELA’s investigations underscore operational risk tied to billing errors, amplifying reputational stakes. Proposed hardship-based relief rules would add predictive assessments that may shift millions into lower-payment tracks, altering cash-flow projections for private competitors. Such volatility cools investor appetite for long-dated student loan ABS and moderates expansion in the student loans industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Provider: Banks Face Fintech Pressure Despite Market Leadership

Banks controlled 72.45% share of the student loans market in 2025, yet rising funding costs and digital competition narrowed spreads. Alternative lenders and NBFCs are projected to grow at 7.61% CAGR, leveraging lean operating models to offer quick approvals and niche products that target high-potential majors within the student loans market. Discover’s USD 10.8 billion portfolio sale to Carlyle and KKR signaled a strategic retreat that opens the door for Sallie Mae and fintech rivals.

Fintech platforms differentiate through AI underwriting and mobile-first interfaces that cut application times from weeks to minutes. SoFi’s USD 1.2 billion Q1 2025 originations illustrate scale benefits, while partnerships between regional banks and white-label platforms create hybrid models. Competition thus intensifies as incumbents update tech stacks to defend their student loans market share against agile entrants.

By Repayment Plan: Income-Driven Dominance Reflects Economic Uncertainty

Income-Driven Repayment plans held 42.10% of the student loans market size in 2025 and are set to expand at 7.74% CAGR. The SAVE framework would cap undergraduate payments at 5% of discretionary income, reinforcing borrowers' tilt toward variable payment schedules. Standard 10-year plans remain prevalent among higher-earning graduates who favor amortization certainty, while graduated options attract those expecting income trajectories to rise.

Federal payment-count adjustments for 3.6 million borrowers in 2025 accelerate IDR adoption. Chapter 13 bankruptcy rules now credit each plan-qualified month, even without explicit enrollment, broadening eligibility. These regulatory nudges cement flexible structures as the default pathway across the student loans market.

By Borrower Age Group: Younger Cohorts Drive Market Expansion

Borrowers aged 25-34 commanded a 47.10% share of the student loans market in 2025, but the fastest growth of 7.55% CAGR belongs to students aged 24 or younger who are borrowing earlier and often across multiple degrees. Their digital fluency aligns with app-based origination and AI-enabled credit scoring that favors expedited approvals.

Employers deploy tuition benefits to attract Gen Z talent, often covering one-third of annual costs, yet residual expenses keep these workers engaged with lenders. Younger borrowers’ lifetime repayment horizons extend portfolio duration, offering lenders steady revenue streams. This demographic shift supports long-term volume gains in the student loans market.

By Education Level: Graduate Programs Command Premium Financing

Undergraduate loans represented 61.60% share of the student loans market in 2025, but graduate and professional programs are expected to grow at 8.12% CAGR as candidates chase career-accelerating credentials. Average graduate loan sizes exceed undergraduate amounts by more than 2×, boosting interest revenues and securitization volumes.

Financial Value Transparency rules oblige schools to publish debt-to-earnings ratios, pressing low-ROI programs to moderate tuition. Even so, earnings premiums for specialized degrees keep demand robust. Ascent Funding’s career-education securitization shows investor appetite for outcome-linked pools, signaling maturation in the graduate slice of the student loans market size.

Geography Analysis

North America held a 42.20% share of the student loans market in 2025, anchored by the United States’ significant federal portfolio that serves more than 46 million borrowers. Elevated delinquency rates—20.5% seriously delinquent as of February 2025—create both risk and refinancing opportunity. Consolidation, such as Capital One’s USD 35.3 billion Discover buy, underscores regional scale plays that can absorb compliance costs while diversifying fee income.

Asia-Pacific is the fastest-growing geography at 7.22% CAGR to 2031, propelled by expanding middle-class enrolments and outbound mobility from India, China, and emerging Southeast Asian states . Currency shifts and patchy credit bureaus prompt fintechs to deploy alternate risk analytics, while government-backed schemes in markets such as Australia smooth capital flows. Enrolment data show that 75% of APAC international students self-fund, with 19% using formal loans, pointing to a runway for penetration growth.

Europe maintains moderate expansion within a mature infrastructure. The UK attracts significant Asian capital into purpose-built student housing, highlighting a 350,000-bed supply gap that indirectly raises demand for maintenance loans. Continental securitization set a EUR 137 billion record in 2024, giving lenders deep secondary-market liquidity. Yet Brexit policy shifts complicate visa routes, causing some students to choose alternate hubs and diffusing growth across the broader student loans market.

Mordor Intelligence provides coverage of the student loans market across other key regional markets. Detailed country-level analysis extends to United Kingdom, Australia, and Canada incorporating local coverage and market participation, as required.

Competitive Landscape

The student loans industry features mixed concentration: federal entities dominate volumes in the United States, yet private and fintech challengers rapidly scale share in refinancing and international segments. Incumbent banks wield low-cost deposit funding but lag on digital experience, leading many to partner with white-label platforms. Private equity’s acquisition of Discover’s portfolio demonstrates institutional appetite for predictable cash-flow assets tied to the student loans market.

Technology provides a strategic moat. AI underwriting lowers acquisition costs and broadens addressable markets, illustrated by U.S. Bank’s approval of previously rejected applicants through Pagaya’s model. Array’s 2024 purchase of Payitoff signals demand for in-app repayment optimization tools that cut delinquency. Blockchain pilots, such as Lukenya University’s interest-free pool, showcase experimental pathways that may disintermediate conventional lenders.

Servicing is under intense scrutiny. CFPB penalties against Navient and investigations into MOHELA push the segment toward data-driven compliance frameworks. Nelnet’s new Department of Education contract and 15.8 million-borrower footprint position it as a scale leader, yet legacy systems must modernize quickly to meet experience expectations. Overall, firms that combine regulatory fluency with technology agility are best placed to capture incremental growth in the student loans market.

Student Loans Industry Leaders

Sallie Mae

SoFi Technologies

Navient

Citizens Bank

Discover Financial Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Capital One closed its USD 35.3 billion acquisition of Discover Financial Services and announced a USD 265 billion Community Benefits Plan.

- April 2025: SoFi Technologies posted record Q1 2025 revenue of USD 772 million and originated USD 1.2 billion in student loans, up 59% year over year.

- March 2025: Lukenya University introduced a blockchain-based interest-free loan system on Celo with an initial USD 522.51 endowment.

- January 2025: The U.S. Department of Education extended Income-Contingent Repayment enrollment through July 2027 to accommodate SAVE plan adjustments.

Global Student Loans Market Report Scope

A student loan is a specific type of loan made for students to assist them in covering the costs of their post-secondary education and any related expenses, including tuition, books, supplies, and living costs. Government agencies, private financial institutions, or educational institutions themselves typically provide these. These loans are designed to assist students who may need more immediate financial means to cover the full cost of their education.

The global education/student loans market is segmented by type (federal/government loan and private loan), by repayment plan (standard repayment plan, graduated repayment plan, revised pay as you earn (REPAYE), income-based, and other repayment plans), by age group (24 or younger, 25 to 34, and above 35), by end-user (graduate students, high school student, and other end-users), and by region (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa).

The report offers market size and forecasts in value (USD) for all the above segments.

| Banks |

| NBFCs and Others |

| Standard Repayment |

| Graduated Repayment |

| Income-Driven Plans |

| Other Plans |

| 24 or Younger |

| 25 - 34 |

| 35 and Above |

| Undergraduate |

| Graduate / Professional |

| Continuing & Non-degree |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Provider | Banks | |

| NBFCs and Others | ||

| By Repayment Plan | Standard Repayment | |

| Graduated Repayment | ||

| Income-Driven Plans | ||

| Other Plans | ||

| By Borrower Age Group | 24 or Younger | |

| 25 - 34 | ||

| 35 and Above | ||

| By Education Level | Undergraduate | |

| Graduate / Professional | ||

| Continuing & Non-degree | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the student loans market?

The student loans market was valued at USD 4.75 trillion in 2026 and is forecasted to reach USD 6.44 trillion by 2031.

Which region is growing fastest in student loan origination?

Asia-Pacific is projected to grow at a 7.22% CAGR between 2026 and 2031 due to rising middle-class enrolment and outbound study demand.

Why are income-driven repayment plans gaining popularity?

Regulatory updates such as SAVE reduce required payments to 5% of discretionary income for many borrowers, making flexible schedules more attractive.

How are fintech lenders changing the competitive landscape?

They use AI-based underwriting to approve thin-file borrowers quickly, offer mobile-first interfaces, and partner with banks for balance-sheet funding.

What impact do rising interest rates have on borrowers?

Higher federal and private benchmarks increase monthly payments, prompting credit-worthy graduates to refinance while limiting access for higher-risk applicants.

Are graduate loans growing faster than undergraduate loans?

Yes. Graduate and professional programs are set to expand at an 8.12% CAGR, reflecting higher tuition and earnings expectations that support larger loan amounts.

Page last updated on: