Embedded Lending Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

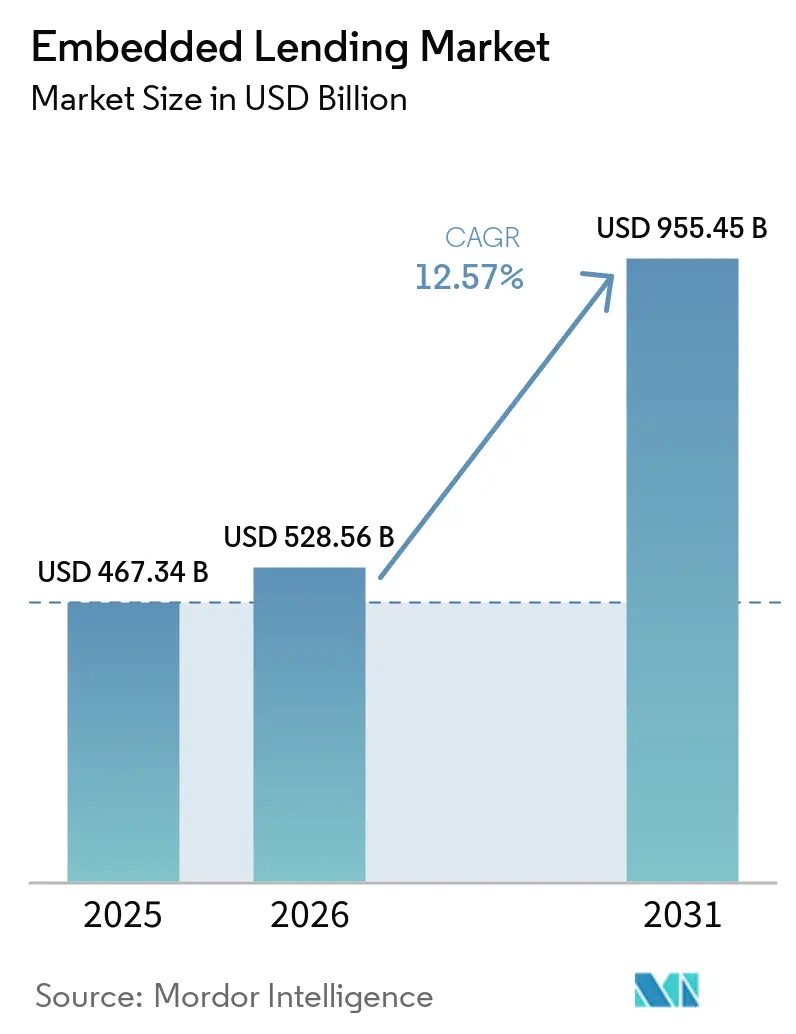

| Market Size (2026) | USD 528.56 Billion |

| Market Size (2031) | USD 955.45 Billion |

| Growth Rate (2026 - 2031) | 12.57% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Embedded Lending Market Analysis by Mordor Intelligence

The Embedded Lending Market size is projected to expand from USD 467.34 billion in 2025 and USD 528.56 billion in 2026 to USD 955.45 billion by 2031, registering a CAGR of 12.57% between 2026 to 2031.

The embedded lending market is expanding as credit products are being built directly into non-financial digital platforms, including e-commerce checkouts, SaaS portals, healthcare payment interfaces, and supply chain software. The move away from standalone lending and toward contextual credit at the point of need is bringing platform operators, fintech firms, and banks into the same operating space. The current phase of the market is being supported by more mature infrastructure, especially API-based credit engines that can handle origination at scale across integrated ecosystems. The market is also showing a clearer split between distribution platforms and infrastructure providers as compliance, funding, and underwriting demands become more specialized. Revenue capture is becoming increasingly uneven across the embedded lending industry: some platforms earn fee income without carrying credit risk, while others face capital and compliance demands when they share in the loan book.

Key Report Takeaways

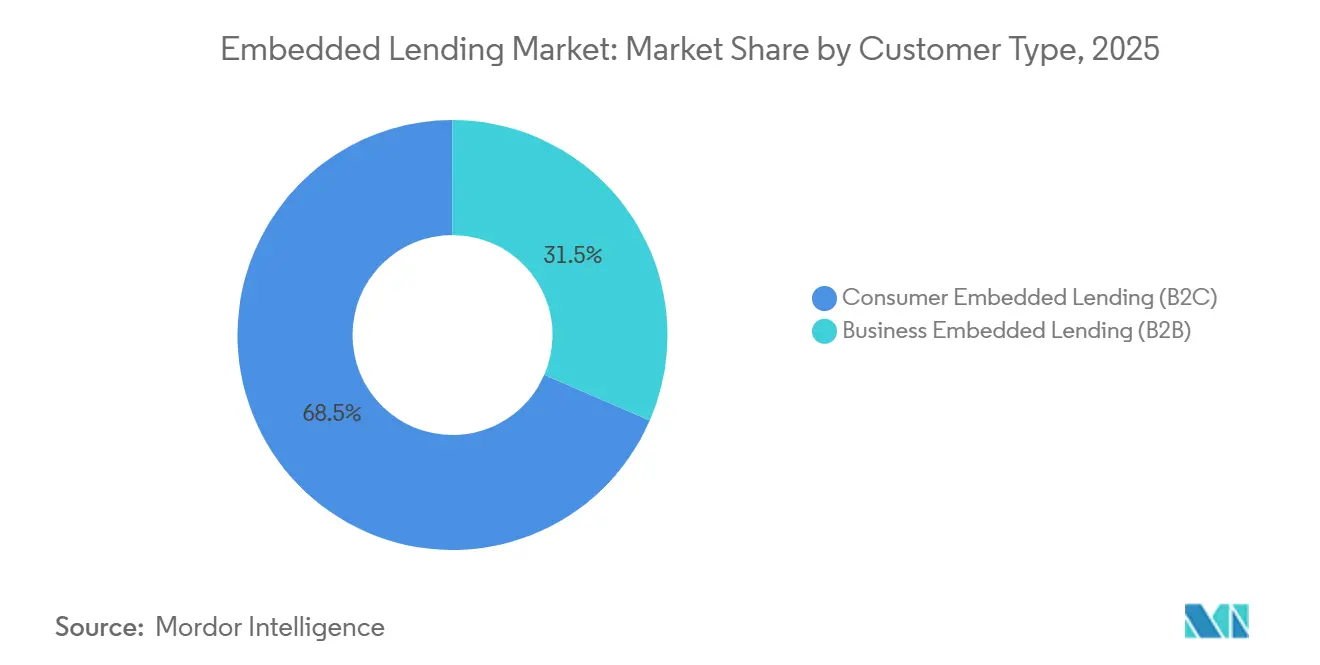

- By customer type, consumer embedded lending captured 68.5% of the embedded lending market share in 2025, while business embedded lending is projected to grow at 15.6% CAGR through 2031.

- By industry vertical, e-commerce and retail platforms accounted for 37.4% of the embedded lending market share in 2025, while professional services are projected to grow at 16.1% CAGR through 2031.

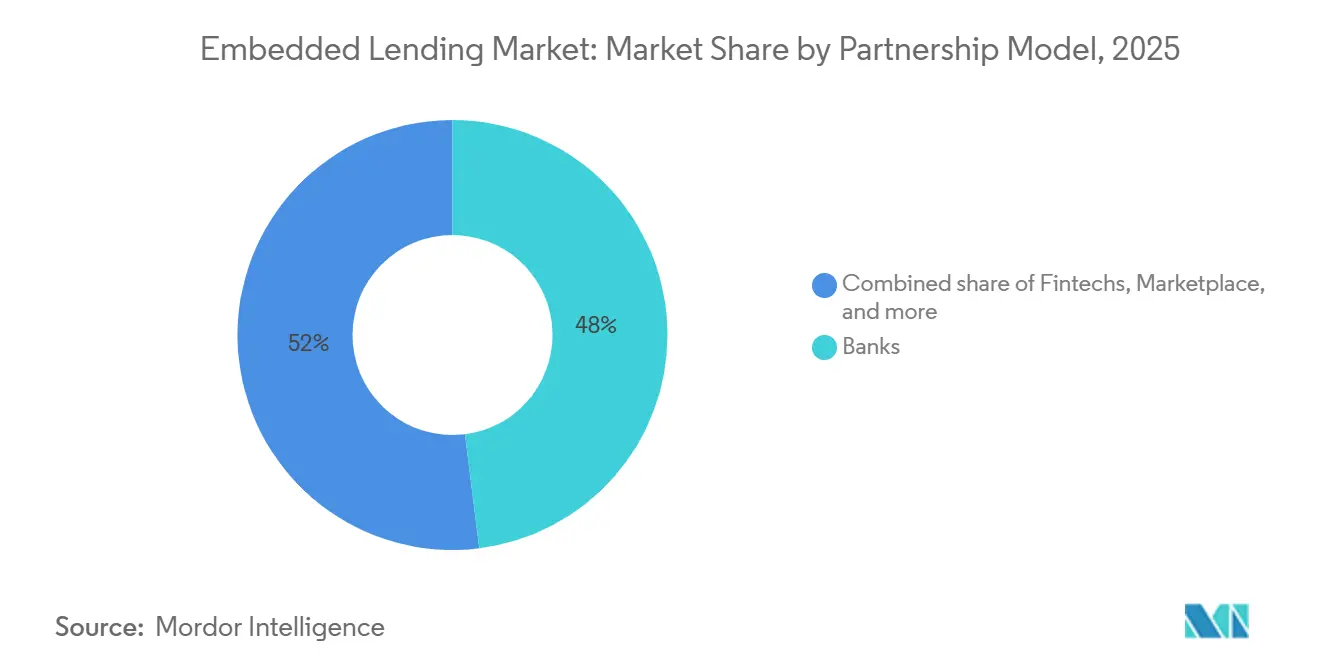

- By the partnership model, banks held 48% of the embedded lending market share in 2025, while fintechs are projected to grow at 14.7% CAGR through 2031.

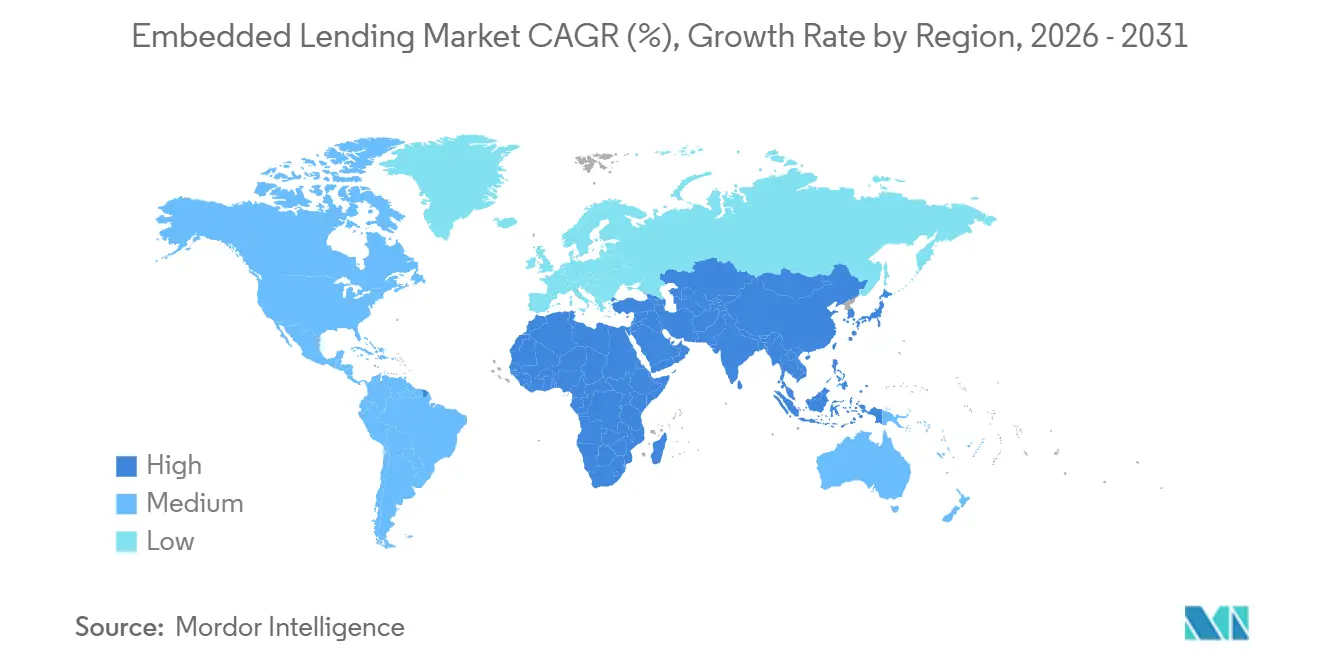

- By geography, North America held 42.1% of the embedded lending market share in 2025, while Asia-Pacific is projected to grow at 15.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Embedded Lending Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Digitization Of Checkout Lending Journeys | +2.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Real-Time Cash Flow Underwriting For SMEs | +2.1% | Asia-Pacific, Europe, North America | Medium term (2-4 years) |

| Vertical SaaS Monetization Through Embedded Credit | +1.6% | North America, with spillover into Europe and the Asia-Pacific | Medium term (2-4 years) |

| Open Banking Data Access And API Orchestration | +1.9% | The EU and the United Kingdom are expanding into Southeast Asia | Medium term (2-4 years) |

| Cross-Border Compliance Architecture As A Differentiator | +1.0% | EU27, the United Kingdom, and the Asia-Pacific cross-border corridors | Long term (≥ 4 years) |

| AI-Enabled Credit Decisioning With Lower Manual Review Load | +2.3% | Global | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Digitization of Checkout Lending Journeys

Checkout finance has moved from an optional feature to a standard conversion tool across many digital commerce platforms. In the embedded lending market, this matters because financing is now appearing inside the same user flow where the purchase decision is made. Affirm expanded its Stripe partnership in March 2026 to support Shared Payment Tokens, which helped keep BNPL available inside AI-initiated purchase flows rather than only in browser checkouts[1]AFFIRM Affirm expands Stripe partnership to support Shared Payment Tokens for agentic commerce | Affirm Holdings, Inc. | March 03, 2026. Klarna made a similar move with Stripe in March 2026, and then extended flexible payments into Google Search and the Gemini app through Google Pay in May 2026. The practical result for the embedded lending market is that providers that embed early into AI-driven checkout layers are better placed to retain share as purchasing moves beyond conventional web and app journeys.

Real-Time Cash Flow Underwriting for SMEs

Traditional bank underwriting still relies heavily on historical financial statements, which often fail to reflect how an SME is performing at the moment credit is needed. The embedded lending market is changing that model by using live transactions and cash flow signals directly from the platforms where merchants operate every day. Mastercard integrated Small Business Credit Analytics into its Open Finance platform in February 2026, enabling lenders to combine near-real-time merchant sales data with cash-flow analytics when making SME credit decisions[2]Mastercard, “Mastercard Open Finance Empowers Small Businesses in the US with Service That Enhances Credit Access,” Mastercard Insights, mastercard.com. This approach fits the embedded lending market because it reduces the gap between operational activity and underwriting, enabling platforms to offer credit within ERP systems, payment processors, and other workflow tools. It also supports better conversion economics because businesses applying within their operating platform face less friction than those redirected to a separate lending portal.

AI-Enabled Credit Decisioning with Lower Manual Review Load

AI is shortening credit decision times in the embedded lending market by reducing the manual review required in early screening and approval steps. The underlying advantage comes from using platform behavior, including purchase frequency, return patterns, and payment timing, as additional underwriting signals that do not sit inside traditional bureau records. Lendflow stated that AI-assisted pre-qualification on its platform enabled funding 42% faster, demonstrating how automation can move the user experience closer to instant-credit delivery. The embedded lending market also benefits when these models are paired with robust compliance controls, as faster decisions are only useful when they remain auditable. That requirement is likely to favor providers that can show explainability, workflow governance, and model discipline as lending volumes rise across more regulated environments.

Open Banking Data Access and API Orchestration

Open banking is becoming more important to the embedded lending market because it broadens the data available for credit assessment beyond card and payment history alone. The strongest effect appears when proprietary platform data and permissioned financial data are combined inside a single underwriting flow. YouLend and Intuit launched the QuickBooks Capital Marketplace in the United Kingdom in February 2026, following a successful 2025 pilot, placing working capital offers directly within the accounting software used by SMEs[3]YouLend and Intuit, “YouLend and Intuit Team Up to Bring Embedded Capital to QuickBooks UK Customers,” YouLend Blog, webflow.ylinternalapi.com. That example shows how the embedded lending market is moving toward data models embedded in daily business tools rather than sitting alongside them. It also reinforces the advantage of vertically integrated ecosystems that can connect data access, origination logic, and offer delivery with less friction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Lending, Privacy, And Consumer Protection Rules | -1.8% | Global, with acute pressure in the United States, Europe, and the United Kingdom | Short term (≤ 2 years) to Medium term (2-4 years) |

| Partner Dependency And Revenue-Sharing Margin Pressure | -1.0% | Global | Medium term (2-4 years) to Long term (≥ 4 years) |

| Fraud, Synthetic Identity, And Adverse Selection Risk | -1.3% | Global, with elevated pressure in high-growth Asia-Pacific, Middle East, and Africa markets | Medium term (2-4 years) |

| Legacy Core Integration And Data Standardization Constraints | -0.9% | Emerging markets, with acute pressure in Southern and Central Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Lending, Privacy, and Consumer Protection Rules

The regulatory environment remains a key constraint on the speed at which the embedded lending market can scale across jurisdictions. The United Kingdom brought deferred payment credit under a formal regime on July 15, 2026, requiring authorization, affordability checks, and data reporting for BNPL activity[4]Financial Conduct Authority, “Regulating Buy Now Pay Later,” FCA, fca.org.uk. New York State also moved earlier with the Buy-Now-Pay-Later Act in May 2025, adding state-level licensing, disclosure, dispute-resolution, and privacy requirements for providers. In the embedded lending market, these uneven rules matter because platform operators often want to scale a single product across several regions, while local lending, servicing, and disclosure requirements do not align neatly. The result is that smaller operators may struggle to absorb compliance costs, which can push origination toward players that already have multi-jurisdiction control frameworks.

Legacy Core Integration and Data Standardization Constraints

Legacy banking systems still slow parts of the embedded lending market because they were not built for real-time decisioning, API-first data exchange, or platform-native onboarding. When a platform relies on a bank's balance sheet, delays in data mapping, service integration, and approval workflows can weaken the user experience that embedded credit is meant to improve. Finastra reported in its 2026 State of the Nation survey that 29% of financial institutions cited embedding blockchain for lending decisioning, workflow automation, and automated loan applications as priorities, signaling active modernization but also indicating that the transition is still underway. The embedded lending market feels this gap more sharply in regions where verification data and banking protocols remain inconsistent across countries and institutions. Platforms that rely on a single bank partner may gain speed in the short run, but they also face concentration risk when funding, integration, and compliance depend on a single provider.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Customer Type: B2B Embedded Credit Gaining Structural Momentum

Consumer embedded lending accounted for 68.5% of the embedded lending market in 2025, which shows how strongly BNPL, checkout installments, and wallet-linked credit still anchor current volume. This side of the embedded lending industry is mature because demand already sits inside everyday digital purchase journeys, where approval speed and payment flexibility can directly influence conversion. The consumer model works best in environments where financing is tied closely to merchant checkout flows, higher-ticket purchases, and repeat digital spending. It also benefits from greater user familiarity, as many shoppers already recognize installment offers as a standard checkout option. That combination kept the consumer side in the lead even as the broader embedded lending market began to diversify beyond retail-led use cases.

Business embedded lending is projected to grow at 15.6% CAGR between 2026 and 2031, making it the fastest-moving customer segment in the embedded lending market. Growth is coming from invoice financing, working capital, trade finance, and term lending, which can be offered within ERP systems, procurement tools, and payment platforms rather than through separate bank channels. The operating economics are often stronger in B2B because loan sizes are larger, transaction records are richer, and merchant relationships tend to be more stable when credit is embedded into daily workflows. Cross Riverbank announced a forward-flow commitment of up to USD 360 million for Parafin, and Parafin later expanded its warehouse facility in May 2026, showing that capital structures are being built to support higher B2B origination volumes. The regulatory burden is also lighter in many commercial lending settings than in consumer finance, which gives this side of the embedded lending industry more room to scale efficiently.

By Industry Vertical: E-commerce Entrenched, Professional Services Emerges

E-commerce and retail platforms accounted for 37.4% of the embedded lending market in 2025, underscoring the close link between financing and purchase completion in digital checkout flows. This vertical remains the largest because lending at checkout can lift basket values, reduce abandonment, and keep repayment attached to a familiar transaction context. Mobility, travel, and transportation are expanding their use of deferred payment tools for higher-value bookings and operating purchases. Healthcare, wellness, and medical services are also embedding payment options into booking and billing software to reduce collection friction and expand payment flexibility. Supply chain and logistics, real estate and home services, and automotive are still early in their rollouts, but each is moving toward broader adoption as software operators seek stronger retention and monetization levers.

Professional services are projected to grow at 16.1% CAGR between 2026 and 2031, making it the fastest-rising vertical in the embedded lending market. The shift matters because it shows embedded credit moving from one-time retail transactions into service relationships built around contracts, retainers, and project fees. Affirm partnered with ServiceTitan in 2026 and also partnered with Vagaro, which shows how software platforms in contractor, beauty, wellness, and fitness settings are using financing to deepen client engagement. Education and EdTech are moving in a similar direction through tuition plans and related credit structures that sit close to the service being purchased. As a result, the embedded lending market is broadening its vertical base without losing the central logic of point-of-need credit delivery.

By Partnership Model: Banks Hold Volume, Fintechs Drive Architecture

Banks retained 48% of the partnership landscape in 2025, giving them the largest share of the embedded lending market, as they still offer licensed infrastructure, funding depth, and regulatory credibility. Many platform operators prefer this model when they want to scale lending without building the full compliance and balance sheet stack themselves. The bank-led approach also remains important where consumer credit rules are tightening, and platforms need a partner that already understands supervision, reporting, and servicing controls. Visa described this type of setup as a model in which banks supply the regulated foundation while fintech partners shape the technology and user experience. That structure kept banks in the lead even as technology specialists expanded their role across the embedded lending market.

Fintechs are projected to grow at 14.7% CAGR between 2026 and 2031, making them the fastest-moving partnership model in the embedded lending market. Their advantage comes from API-native integration, faster deployment cycles, and greater flexibility in serving SMEs and consumers that traditional lenders have not served well. Fiserv and Affirm announced an exclusive collaboration in January 2026, so thousands of United States banks and credit unions could offer pay-over-time capabilities through debit programs, with Affirm handling underwriting and origination. Marketplace models sit between these two poles by matching borrowers, platforms, and multiple funding sources, thereby reducing dependence on a single capital partner. The result is a more varied partnership structure across the embedded lending market, even though banks still hold the largest current volume.

Geography Analysis

North America held 42.1% of the embedded lending market share in 2025, giving the region the largest current position in the global landscape. The region benefits from a mature digital payments infrastructure, established BNPL behavior, and a dense base of platform operators already active in commerce and merchant services. Large infrastructure providers, including Stripe, PayPal, and Fiserv, support this position by enabling merchants and platforms to access embedded credit capabilities more easily. The embedded lending market in North America also has enough scale to absorb rising compliance overhead more easily than smaller markets. New York's May 2025 BNPL framework illustrates that oversight is tightening, but the region still retains depth in distribution, funding, and merchant adoption.

Asia-Pacific is projected to grow at 15.2% CAGR between 2026 and 2031, making it the fastest-expanding region in the embedded lending market. Growth is being supported by large underserved SME populations, strong mobile-first behavior, and digital ecosystems that already connect payments, commerce, and platform services. The region also benefits from super-app structures and account-to-account frameworks that make native credit integration more attractive for platforms. In practical terms, that means the embedded lending market can scale through transaction-driven workflows rather than through traditional branch-led banking relationships. Countries across Southeast Asia, along with India, China, South Korea, and Australia, are each contributing through different combinations of platform density, mobile payments, and B2B credit demand.

Europe, South America, and the Middle East and Africa add important but uneven growth paths to the embedded lending market. Europe is gaining structure through consumer credit harmonization and the development of open finance, which can improve data access and reduce fragmentation over time. South America offers a different setup: instant-payment infrastructure in Brazil creates stronger transaction data rails, while Argentina's unstable macro backdrop is increasing demand for short-term working capital solutions. In the Middle East and Africa, GCC markets are opening up through fintech licensing reforms, while South Africa and Egypt are emerging as notable hubs for SME-focused alternative credit. Taken together, these regions show that the embedded lending market is not growing from a single template but from several local models shaped by payment rails, regulatory progress, and platform maturity.

Competitive Landscape

The embedded lending market operates across two broad layers: one comprising infrastructure providers and the other comprising balance-sheet lenders that originate and fund credit. The consumer BNPL side is becoming more concentrated around a small set of global names, while B2B and SME-focused embedded credit still has a wider field of specialist competitors. Klarna expanded its reach in May 2026 by launching flexible payments in Google Search and the Gemini app via Google Pay, bringing its offer closer to AI-led shopping behavior. Affirm also strengthened its position in March 2026 by extending its Stripe partnership to support Shared Payment Tokens for AI-initiated purchase flows. These moves show that leading firms in the embedded lending market are now competing as much on distribution presence and integration depth as on the credit product itself.

The B2B- and SME-focused side of the embedded lending market remains more fragmented, with players such as Parafin, YouLend, Liberis, Lendflow, Kanmon, Biz2X, Banxware, and Hokodo pursuing growth through platform integration and precision underwriting. YouLend's QuickBooks Capital Marketplace launch in the United Kingdom in February 2026 showed how working capital can be placed directly inside accounting workflows rather than through external application channels. Liberis used a similar model in February 2026 when it partnered with Deliveroo to launch Deliveroo Capital inside the Deliveroo Partner Hub for restaurants in the United Kingdom. Parafin's expanded funding structure in 2026 also showed how white-label infrastructure can scale across merchant ecosystems, including Amazon, DoorDash, TikTok Shop, and Walmart. This makes the competitive picture of the embedded lending market broader in B2B than in consumer BNPL, even though both sides depend on deep platform access.

Compliance architecture is becoming a stronger differentiator across the embedded lending market because regulatory scrutiny now affects product design, partner selection, and expansion speed. Finastra was named a Leader in the IDC MarketScape for worldwide AI-enabled embedded trade financing applications for 2025-2026, which supports its position in institutional and B2B lending infrastructure. Large institutions are also investing in modernization to support more complex corporate and cross-border credit programs with stronger control frameworks. That trend favors providers that can combine integration speed with auditable underwriting, reporting, and servicing controls. As a result, the embedded lending market is likely to keep separating into firms that own merchant distribution, firms that supply regulated infrastructure, and firms that bring the funding layer.

Embedded Lending Industry Leaders

Stripe, Inc.

PayPal Holdings, Inc.

Klarna Bank AB

Affirm Holdings, Inc.

Block, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Klarna launched flexible payment options within Google's Gemini app and Google Search via Google Pay in the US, extending BNPL access to AI-driven shopping environments and removing dependency on browser-based checkout for embedded finance origination.

- May 2026: Parafin expanded its warehouse credit facility with Silicon Valley Bank, Trinity Capital, and new A-note lender EverBank, increasing borrowing capacity and reducing cost of capital to scale embedded financing for merchants on Amazon, DoorDash, TikTok Shop, and Walmart.

- March 2026: Affirm expanded its Stripe partnership to support Shared Payment Tokens (SPTs), enabling Affirm BNPL to function within AI-agent-initiated purchase flows, a strategic move for sustaining embedded lending relevance as agentic commerce scales.

- February 2026: YouLend and Intuit launched the QuickBooks Capital Marketplace in the United Kingdom following a successful 2025 pilot, offering SMEs working capital from GBP 1,000 to GBP 2 million embedded directly within their accounting software

Global Embedded Lending Market Report Scope

| Consumer Embedded Lending (B2C) | BNPL |

| Installment Loans | |

| Revolving Credit Lines | |

| Other Consumer Credit Products | |

| Business Embedded Lending (B2B) | Invoice Financing |

| Working Capital | |

| Term Loans | |

| Trade Finance | |

| Other Business Credit Products |

| E-commerce and Retail Platforms |

| Mobility, Travel and Transportation |

| Healthcare, Wellness and Medical Services |

| Professional Services |

| Supply Chain and Logistics |

| Automotive |

| Education and EdTech |

| Real Estate, Home Services and Construction |

| Other Verticals |

| Banks |

| Fintechs |

| Marketplace |

| Other Partnership Structures |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Customer Type | Consumer Embedded Lending (B2C) | BNPL |

| Installment Loans | ||

| Revolving Credit Lines | ||

| Other Consumer Credit Products | ||

| Business Embedded Lending (B2B) | Invoice Financing | |

| Working Capital | ||

| Term Loans | ||

| Trade Finance | ||

| Other Business Credit Products | ||

| By Industry Vertical | E-commerce and Retail Platforms | |

| Mobility, Travel and Transportation | ||

| Healthcare, Wellness and Medical Services | ||

| Professional Services | ||

| Supply Chain and Logistics | ||

| Automotive | ||

| Education and EdTech | ||

| Real Estate, Home Services and Construction | ||

| Other Verticals | ||

| By Partnership Model | Banks | |

| Fintechs | ||

| Marketplace | ||

| Other Partnership Structures | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of embedded lending by 2031?

The embedded lending market is projected to reach USD 955.5 billion by 2031, up from USD 528.6 billion in 2026, with 12.6% CAGR over 2026-2031.

Which customer segment is growing faster, B2C or B2B?

B2B is growing faster, with a projected 15.6% CAGR between 2026 and 2031, while B2C remained the largest segment with 68.5% share in 2025.

Why do e-commerce platforms lead current adoption?

E-commerce and retail led with 37.4% share in 2025 because financing is placed directly inside checkout, where it can improve purchase completion and payment flexibility.

Which region leads current revenue and which region is expanding fastest?

North America held the largest share at 42.1% in 2025, while Asia-Pacific is forecast to grow the fastest at 15.2% CAGR through 2031.

How are banks and fintechs dividing roles in this space?

Banks held 48% of the partnership landscape in 2025 because they bring funding and regulatory infrastructure, while fintechs are growing faster at 14.7% CAGR because they offer faster integration and flexible product design.

What is changing competition among leading providers?

Competition is shifting from standalone product features toward distribution reach, workflow integration, compliance readiness, and access to platform data, especially as AI-led shopping and embedded B2B workflows expand.

Page last updated on: