Coffee Substitute Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 17.5 Billion |

| Market Size (2031) | USD 21.89 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

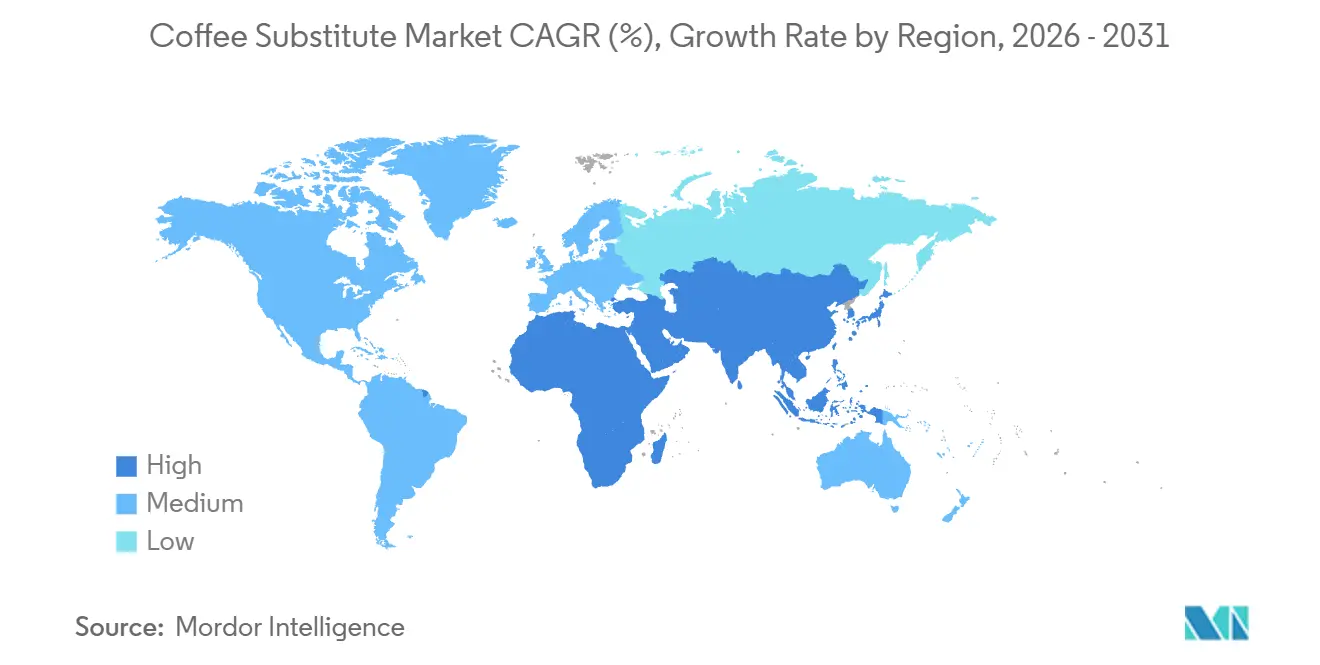

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Coffee Substitute Market Analysis by Mordor Intelligence

In 2025, the coffee substitute market was valued at USD 16.7 billion and is projected to reach USD 21.9 billion by 2031, growing at a CAGR of 4.6% from 2026 to 2031. Initially a fallback for those reducing caffeine, the market is now establishing itself as a distinct category focused on health, routine, and functionality. Consumers are shifting toward beverages that support sleep, gut health, and low-stimulation lifestyles, reducing reliance on coffee price trends. Premium positioning drives growth, as health-conscious buyers are willing to pay more for products with functional ingredients, clean labels, or added convenience. Specialist brands lead with functional offerings and subscription models, while larger beverage companies are reshaping portfolios to include higher-margin functional formats, leaving room for challenger brands to grow. However, the market faces challenges such as supply concentration in key ingredients, sensitivity to premium pricing in value segments, and competition from other health-focused beverage categories.

Key Report Takeaways

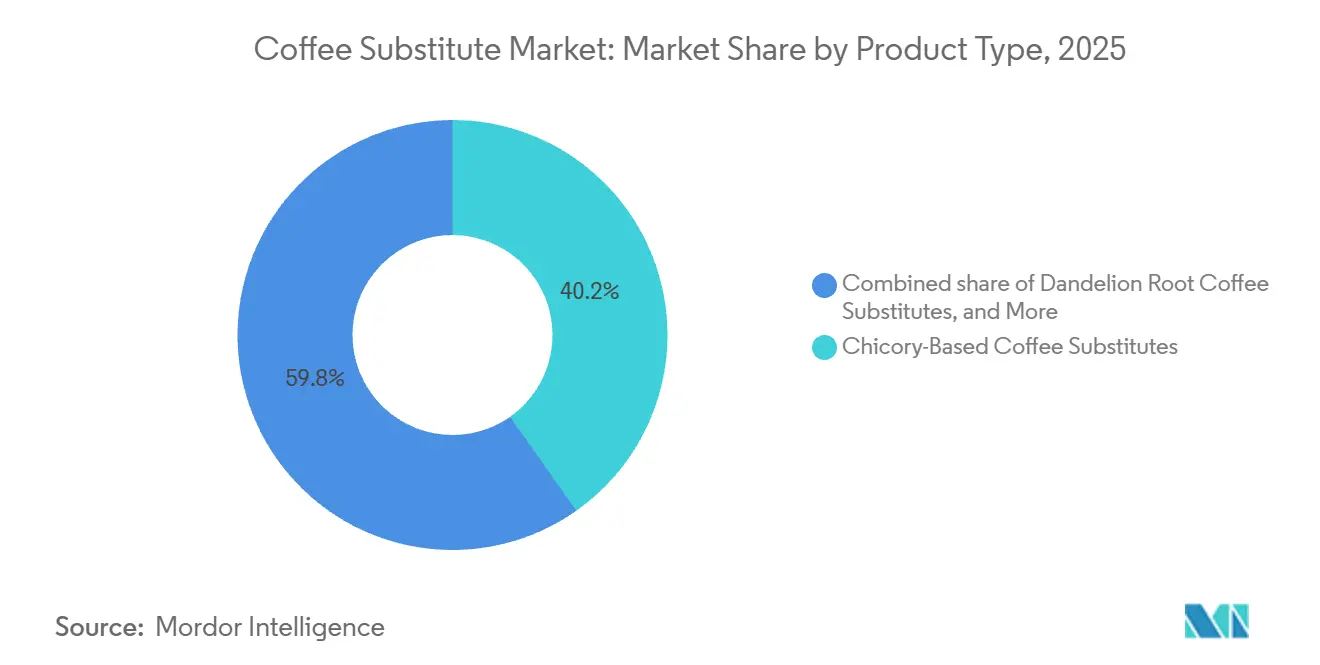

- By product type, chicory-based products held 40.23% of the coffee substitute market share in 2025, while dandelion root products are projected to grow at a 5.65% CAGR through 2031.

- By form, powder products accounted for 65.71% of the coffee substitute market size in 2025, while RTD beverages are forecast to expand at a 4.93% CAGR through 2031.

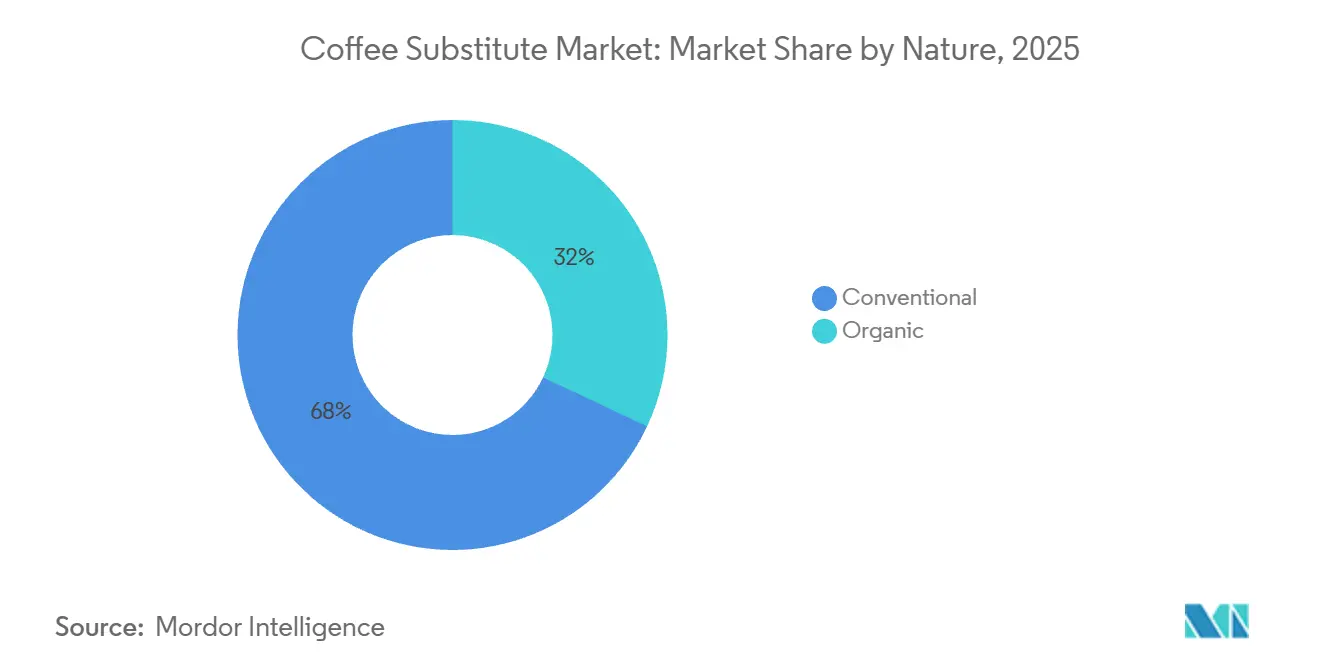

- By nature, conventional products led with 68.02% share in 2025, while organic products are expected to record the fastest CAGR of 6.28% through 2031.

- By distribution channel, off-trade channels represented 82.33% of the market in 2025, while on-trade channels are projected to advance at a 5.94% CAGR through 2031.

- By geography, Europe captured 37.72% of market value in 2025, while Asia-Pacific is set to grow at a 6.82% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Coffee Substitute Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Caffeine-Free Functional Beverages | +1.2% | Global, with stronger concentration in North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Health, Sleep Quality, And Anxiety Management Priorities | +0.9% | Global, with highest intensity in the United States, South Korea, Japan, and Germany | Short term (≤ 2 years) |

| Innovation In Flavor Profiles And Product Offerings | +0.8% | North America and Europe, with spread into premium Asia-Pacific segments | Short term (≤ 2 years) |

| Plant-Based, Clean-Label, And Sustainability Preferences | +0.7% | Core in Europe and North America, with spillover into Australia and urban Asia-Pacific | Medium term (2-4 years) |

| Growth In E-Commerce Grocery Penetration And Direct-To-Consumer Models | +0.6% | Global, with strongest effect in North America and e-commerce-led Asia-Pacific markets | Short term (≤ 2 years) |

| Volatility In Coffee Supply And Sustainability Mandates | +0.5% | Global, with greater effect in price-sensitive Asia-Pacific and Middle East and Africa markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Caffeine-Free Functional Beverages

Consumers now view beverages as essential to daily health management, driving growth in the coffee substitute market. Demand has shifted beyond avoiding caffeine, with buyers seeking products that support sleep, digestion, calmness, and stable energy. ADM research in 2026 revealed 68% of consumers were interested in sleep-supporting products, and 49% were willing to pay a premium for effective solutions. This pricing flexibility strengthens the market for functional coffee alternatives. Premium products now compete on purpose and ingredient quality rather than being cheaper coffee substitutes. For instance, Rasa Original Adaptogenic Coffee, priced at USD 29.99 for 30 servings in 2026, reflects consumers' readiness to invest in functionality and daily value. As a result, the coffee substitute market is building a wellness-focused identity, expanding its appeal beyond traditional caffeine-reduction products.

Health, Sleep Quality, and Anxiety Management Priorities

Consumers are increasingly focusing on sleep quality and stress management, providing the coffee substitute market with a stronger foundation. In 2024, Treatt reported that 60% of adults in France, Spain, and Italy reduced caffeine intake to protect their sleep, highlighting steady demand in key European beverage markets. Similarly, ADM's 2026 data showed 61% of respondents felt stress affected their sleep, rising to 72% in South Korea. In the U.S., spending on mood and relaxation beverages grew 42% in 2026, reflecting their shift from occasional treats to daily routines. Japan also demonstrated this trend, with its mood and sleep-supporting food and beverage segment reaching JPY 1,904 billion (USD 13.0 billion) in 2024 and growing 8.7% year-on-year. This growth indicates that low-stimulant functional beverage demand in Asia-Pacific could surpass current coffee substitute penetration. These evolving habits are driving the coffee substitute market through routine-based consumption, recovery, and lower stimulation preferences.

Innovation in Flavor Profiles and Product Offerings

Product development is closing the taste gap that once hindered first-time adoption. The coffee substitute market is innovating rapidly with chicory blends, mushroom-based products, adaptogen mixes, and hybrid formats that mimic coffee without full caffeine intensity. In 2025, the functional mushroom-based coffee substitute market reached USD 1.9 billion, with projections to exceed USD 2.2 billion by 2026, highlighting its growing acceptance in the functional beverage space. Four Sigmatic plans to launch 11 new products by summer 2025, including coffees, lattes, teas, and mushroom-adaptogen blends, reflecting innovation levels comparable to larger beverage categories. The market is expanding its audience as some brands now offer products blending coffee and substitutes, appealing to households seeking reduced caffeine rather than complete elimination. This variety lowers the trial barrier and creates more opportunities for consumption throughout the day, from mornings to afternoons and on-the-go occasions.

Plant-Based, Clean-Label, and Sustainability Preferences

The coffee substitute market is gaining momentum due to rising demand for plant-based and clean-label products. Many of its core ingredients naturally meet these preferences. Consumers now prioritize ingredient simplicity, transparent sourcing, and minimal processing, strengthening the appeal of plant-derived substitutes in premium retail. A 2026 report by Innova Market Insights revealed that 64% of global consumers prefer plant-based products with less processing, favoring root-based and grain-based coffee alternatives with simpler ingredient profiles. Clean-label expectations now extend beyond claims, with traceability and transparency becoming essential. In Europe, stricter organic farming rules proposed in May 2026 emphasized tighter controls on imported organic labels and sourcing standards, raising the bar for premium organic coffee substitutes. For this market, brands combining organic or plant-based positioning with transparent sourcing and clear functionality are better positioned to sustain premium pricing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions | -0.9% | Global, with strongest exposure in European chicory cultivation zones and Asia-Pacific botanical sourcing hubs | Medium term (2-4 years) |

| Competition From Other Beverage Categories | -0.8% | Global | Short term (≤ 2 years) |

| Regulatory Hurdles And Complex Food Safety Standards | -0.5% | Europe, North America, and Asia-Pacific | Long term (≥ 4 years) |

| Taste And Aroma Replication Gap | -0.7% | Global, with strongest effect on first-trial conversion in North America and South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions

The coffee substitute market faces significant supply risks due to its reliance on limited ingredient sources. Belgium and the Netherlands supply 85% of Europe’s chicory root, while Belgium and France dominate roasted chicory production. Notably, 75% of chicory acreage depends on ALS seed varieties, which are increasingly incompatible with new European crop protection products, and scalable alternatives are unavailable. Concentrated ingredient sourcing has led brands to adopt defensive procurement strategies and maintain buffer inventories, increasing working capital needs. External disruptions, such as 2025 tariff changes on Indian goods and 2026 shipping risks in the Strait of Hormuz, further strain the market. These challenges raise costs, reduce formulation consistency, and limit margin flexibility for premium brands, potentially slowing market growth.

Competition from Other Beverage Categories

The coffee substitute market competes not only with coffee but also with a growing range of health-focused, low-caffeine beverages. Functional teas, adaptogenic waters, botanical mocktails, and reduced-caffeine coffee blends all target similar wellness-oriented moments, such as afternoons or evenings. This overlap fragments the market, as consumers often see these options as interchangeable for reducing stimulation or promoting relaxation. Brands relying on a single ingredient or narrow functional claim face higher substitution risks, as competing categories often offer similar benefits with better flavor familiarity or wider availability. The challenge grows as major beverage companies shift toward functional, premium products, and coffee industry consolidation expands reduced-caffeine options in mainstream channels. As a result, the coffee substitute market must focus on daily relevance, taste, and repeat use rather than just caffeine avoidance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chicory-Based Volume Concentrated, but Dandelion Root Disruptive

In 2025, chicory-based products led the coffee substitute market with a 40.23% share, driven by strong consumer recognition in Europe and a well-integrated supply chain. Chicory's long history ensures a trusted safety profile, enabling quicker market entry compared to newer formats facing scrutiny over novel ingredients. Herbal coffee alternatives maintain a niche among health-conscious users, while mushroom-based products are gaining traction in the mid-premium tier. Chicory remains vital due to its familiar taste, routine compatibility, and broad retail acceptance—qualities that newer formats struggle to match. The market relies on chicory as a bridge for consumers seeking a coffee-like experience without caffeine. Meanwhile, mushroom variants are expanding their appeal by linking beverages to focus, mood, and adaptogenic benefits.

Dandelion root is projected to grow fastest, with a 5.65% CAGR through 2031, fueled by demand for plant-based ingredients offering flavor and digestive benefits. Its inulin content and alignment with gut-health trends set it apart from grain-based or traditional herbal options, though supply challenges may arise as demand increases. Despite its current scale, dandelion root drives growth by emphasizing health benefits, particularly prebiotic value, which supports premium pricing. This differentiation is crucial as the market shifts focus from category presence to unique offerings. Consumers seeking digestive support or holistic wellness may prefer dandelion products over basic cereal blends. However, scaling this segment depends on securing stable supply and maintaining consistent taste at higher volumes.

By Form: Powder Entrenches Market Access, RTD Beverages Reshape Occasion

In 2025, powder products dominated the coffee substitute market with a 65.71% share. Their popularity was driven by affordability, ease of preparation, and compatibility with existing brewing habits. Consumers could adjust intensity, mix with dairy or plant-based beverages, and use powders throughout the day. Granules remained significant in Europe due to chicory traditions, while liquid concentrates served niche premium needs, especially in foodservice. Powders' ease of distribution, storage, and use encouraged repeat purchases and pantry stocking. Their adoption required no new equipment or rituals, making them accessible. As home preparation remains key, powders are expected to retain their leading position even as newer formats grow.

RTD beverages are projected to grow at a 4.93% CAGR through 2031, making them the fastest-growing segment in the coffee substitute market. Their growth is fueled by urban, on-the-go lifestyles and demand for ready-made products. Online grocery sales, expected to reach USD 452 billion by 2028, further support RTD adoption, with beverages driving digital revenue. RTD products cater to commuting, travel, and workplace settings, expanding use occasions beyond powders' home routines. They also simplify trial by removing brewing uncertainties and offering consistent flavor. As the market evolves, RTD is reshaping when and where coffee substitutes are consumed, while powders continue to lead in revenue.

By Nature: Conventional Anchors Scale, Organic Captures Premium Growth

In 2025, conventional products led the coffee substitute market with a 68.02% share, driven by affordable pricing and broad retail availability in both established and price-sensitive markets. Consumers often seek an affordable, coffee-like experience, which conventional products deliver better than organic options. Grain and cereal blends gained popularity during 2024 and 2025 due to coffee price volatility, offering a cost-effective alternative. These blends are well-known in Europe, especially chicory blends, helping the market reach mainstream households beyond premium buyers. Conventional products ensure accessibility in mid-tier retail and emerging markets, making a fully premium-led market unlikely. Repeat demand in this segment stems from affordability, habit, and routine, providing resilience during tighter budgets.

Organic products are projected to grow at a 6.28% CAGR through 2031, making them the fastest-growing segment in the coffee substitute market. This growth is driven by clean-label demand, health-conscious consumers willing to pay more, and a focus on sourcing transparency. A 2025 USDA report highlighted global growth in organic certification, with North America and Europe leading in certification volumes and retail premiums[1]Source: USDA Agricultural Marketing Service, “International Trade Policies, European Union, Organic Certification”, ams.usda.gov. Organic products perform best when paired with added benefits like prebiotics, adaptogens, or traceability, securing shelf space in specialty retail. However, certification alone doesn’t guarantee repeat purchases. Consumers value a complete package, not just a label. Brands combining organic status with strong ingredient credibility are better positioned to maintain pricing, especially as European regulations tighten. Organic growth will remain premium-driven, but top performers will integrate certification into a broader value proposition.

By Distribution Channel: Off-Trade Dominant, On-Trade Gaining Strategic Importance

In 2025, off-trade channels led the coffee substitute market with an 82.33% share, driven by household pantry stocking and repeated at-home use. Supermarkets, hypermarkets, convenience stores, and online platforms cater to both mainstream and premium consumers. Top brands combine shelf presence with direct-to-consumer strategies like subscriptions, boosting customer value, and reducing reliance on single channels. Many coffee substitutes are tied to home routines, making the off-trade dominant. Online retail is growing within the off-trade, supported by the 2026 FMI and NielsenIQ forecast of USD 452 billion in U.S. online grocery sales by 2028. Subscription-driven businesses benefit from consumers’ openness to routine orders and premium product discovery, strengthening their competitive edge.

On-trade channels are projected to grow at a 5.94% CAGR through 2031, becoming the fastest-growing segment in the coffee substitute market. Cafés, restaurants, and hotels allow consumers to try chicory blends, mushroom beverages, and dandelion lattes in a low-risk setting, encouraging later at-home purchases and creating dual revenue streams. Prefer’s 2026 café partnerships in Tokyo highlight how on-trade builds awareness before retail expansion. On-trade also supports higher prices per serving, funding innovation and maintaining premium positioning. While smaller in scale, on-trade influences category perception by offering curated first-use experiences and normalizing substitutes alongside premium beverages. Its role in driving trial, awareness, and brand identity will continue to grow.

Geography Analysis

In 2025, Europe held a 37.72% share of the coffee substitute market, making it the largest regional contributor. Countries like Germany, France, Belgium, and the Netherlands have long embraced chicory and grain-based alternatives, integrating them into their food culture and retail networks. Tchibo’s 2026 Kaffee-Report revealed that German per-capita coffee consumption dropped from 169 liters in 2021 to 161 liters in 2025, indicating growing interest in coffee substitutes. Additionally, Belgium and the Netherlands, as key chicory cultivation and export hubs, provide European manufacturers with a sourcing edge over global competitors.

Asia-Pacific is projected to grow at a strong 6.82% CAGR through 2031, making it the fastest-growing region in the coffee substitute market. Urbanization, changing beverage habits, and rising health awareness are expanding the consumer base in India and China. India’s new front-of-pack labeling rules for coffee-chicory blends, effective July 1, 2026, reflect the category’s growth and the need for clearer consumer communication. Japan offers a favorable market for premium products, with an established demand for low-stimulant and functional beverages. Brands like Prefer are using café-led models to build awareness before broader launches.

North America, led by the U.S., is a key market for premium functional variants like mushroom-based and dandelion root products, primarily sold through direct-to-consumer channels. Subscription models by specialist brands have driven higher customer retention and acquisition rates compared to traditional retail. South America and the Middle East & Africa are emerging markets, with growth driven by coffee price pressures, retail development, and rising health awareness among urban affluent consumers. In the Middle East and Africa, South Africa and the UAE stand out as strong entry points due to advanced retail infrastructure and health-conscious shopper groups.

Competitive Landscape

The coffee substitute market is moderately fragmented, with no single company controlling pricing. Brands like Teeccino Caffe, Dandy Blend, MUD/WTR, Four Sigmatic, and Rasa focus on functional ingredients, cleaner labels, and direct consumer relationships. This allows smaller players to influence premium segments despite lacking large beverage groups' distribution networks. Subscription models further boost customer lifetime value beyond traditional shelf-based metrics.

Major consumer goods firms benefit from wide retail reach, funding, and strong execution but focus on broader beverage portfolios. This creates opportunities for specialist brands to innovate faster and connect with health-conscious consumers. Key areas of competition include mushroom blends, chicory-adaptogen mixes, and improved flavor and mouthfeel. Four Sigmatic's product launches through summer 2025 highlight the rapid growth of functional beverage specialists. Similarly, MUD/WTR's 2026 launch of a lower-caffeine hybrid coffee format reflects efforts to appeal to mainstream households beyond coffee alternatives.

Strategic moves by larger companies significantly impact the category. In April 2026, Keurig Dr Pepper acquired JDE Peet’s, strengthening its coffee platform and distribution power. Nestlé's 2026 sale of Blue Bottle Coffee signaled a shift toward scalable, high-margin coffee formats. Hain Celestial refined its portfolio in 2026, emphasizing innovation in health-focused beverages beyond coffee substitutes. The market's key opportunity lies in brands that combine credible health benefits, better taste, and affordable pricing for long-term success.

Coffee Substitute Industry Leaders

Teeccino Caffe, Inc.

Dandy Blend

MUD/WTR

Postum

Rasa, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Koppie, a Belgium-based food-tech startup, secured additional funding from DOEN Ventures, taking its total funding to over EUR 2 million, alongside support from the Food Pioneer Accelerators program. The company also completed its first industrial-scale production run and is preparing for a commercial launch of its beanless and hybrid coffee products by the end of 2026.

- January 2026: Not Coffee announced the expansion of its caffeine-free coffee substitute, developed from a blend of organic carob, chicory root, and herbs. Founded by Sila Gatti following her diagnosis with Graves’ Disease, the product is designed to replicate the taste, aroma, and brewing experience of traditional coffee without caffeine, bitterness, or acidity.

- October 2025: Cauxffee launched its first ready-to-drink, caffeine-free nitro cold brew coffee alternative at the 2025 Holistic Oklahoma Wellness Event. According to the brand, the product is formulated with eight whole-brewed functional herbs, including adaptogens and nootropics, to deliver a coffee-like taste and experience without caffeine, added sugars, dairy, or artificial ingredients.

Global Coffee Substitute Market Report Scope

| Chicory-Based Coffee Substitutes |

| Dandelion Root Coffee Substitutes |

| Mushroom-Based Coffee Substitutes |

| Grain/Cereal-Based Coffee Substitutes |

| Herbal Coffee Substitutes |

| Others |

| Powder |

| Granules |

| Liquid Concentrates |

| Ready-to-Drink (RTD) Beverages |

| Organic |

| Conventional |

| On-trade | |

| Off-trade | Supermarkets/ Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Chicory-Based Coffee Substitutes | |

| Dandelion Root Coffee Substitutes | ||

| Mushroom-Based Coffee Substitutes | ||

| Grain/Cereal-Based Coffee Substitutes | ||

| Herbal Coffee Substitutes | ||

| Others | ||

| By Form | Powder | |

| Granules | ||

| Liquid Concentrates | ||

| Ready-to-Drink (RTD) Beverages | ||

| By Nature | Organic | |

| Conventional | ||

| By Distribution Channel | On-trade | |

| Off-trade | Supermarkets/ Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2031 value forecast for coffee substitutes?

The category is forecast to reach USD 21.9 billion by 2031, up from USD 16.7 billion in 2025, with a 4.6% CAGR during 2026-2031.

Which product type leads revenue today?

Chicory-based products led with 40.23% of 2025 value, supported by strong consumer familiarity and an integrated European supply chain.

Which format is expanding fastest through 2031?

RTD beverages are the fastest-growing format, with a projected 4.93% CAGR, as convenience and on-the-go consumption become more important.

Which region offers the best growth opportunity?

Asia-Pacific is the fastest-growing region with a 6.82% CAGR, supported by urban lifestyle changes, stronger health awareness, and category formalization in markets such as India and Japan.

Page last updated on: