Beverage Flavoring Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

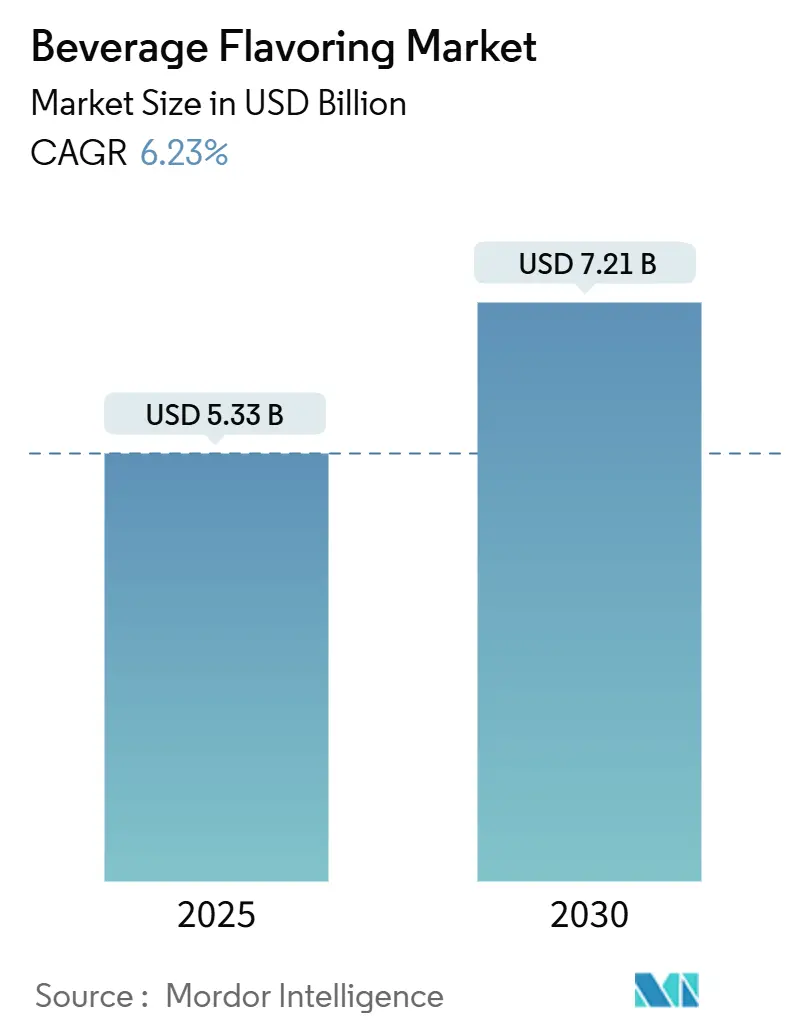

| Market Size (2025) | USD 5.33 Billion |

| Market Size (2030) | USD 7.21 Billion |

| Growth Rate (2025 - 2030) | 6.23% CAGR |

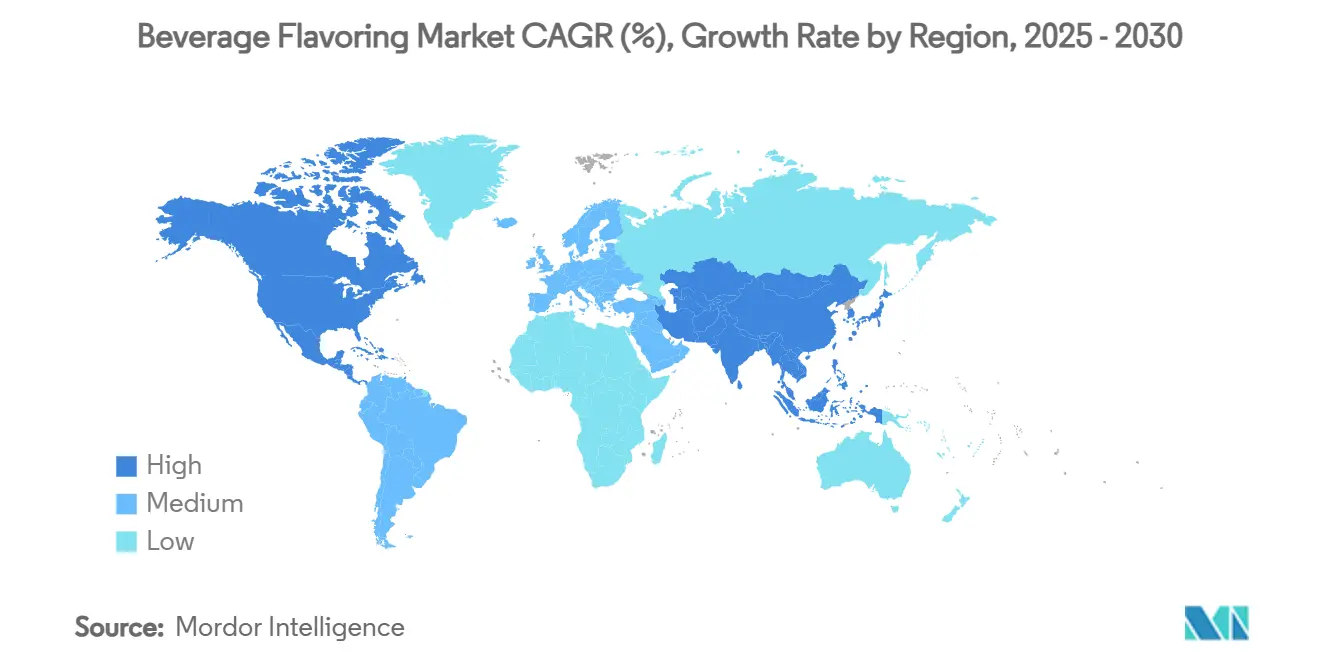

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Beverage Flavoring Market Analysis by Mordor Intelligence

The Beverage Flavoring Market size is estimated at USD 5.33 billion in 2025, and is expected to reach USD 7.21 billion by 2030, at a CAGR of 6.23% during the forecast period (2025-2030). This growth trajectory reflects the industry's adaptation to evolving consumer preferences for natural ingredients, functional beverages, and premium flavor experiences. The market's expansion is underpinned by regulatory shifts toward transparency, with the FDA's potential elimination of self-affirmed GRAS determinations creating both compliance challenges and competitive advantages for established players. Robust flavor innovation, rising RTD consumption, and improved biotechnology processes strengthen the competitive position of established players and nimble specialists alike. Moreover, citrus ingredient shortages are accelerating demand for synthetic replacers and biotechnology-derived alternatives, positioning companies with fermentation capabilities for competitive advantage. Asia-Pacific retains a dominant 35.03% slice of the beverage flavors market and also delivers the fastest regional growth at 7.83% CAGR, buoyed by India’s health beverage boom and ongoing premiumization across China, Indonesia, and Vietnam

Key Report Takeaways

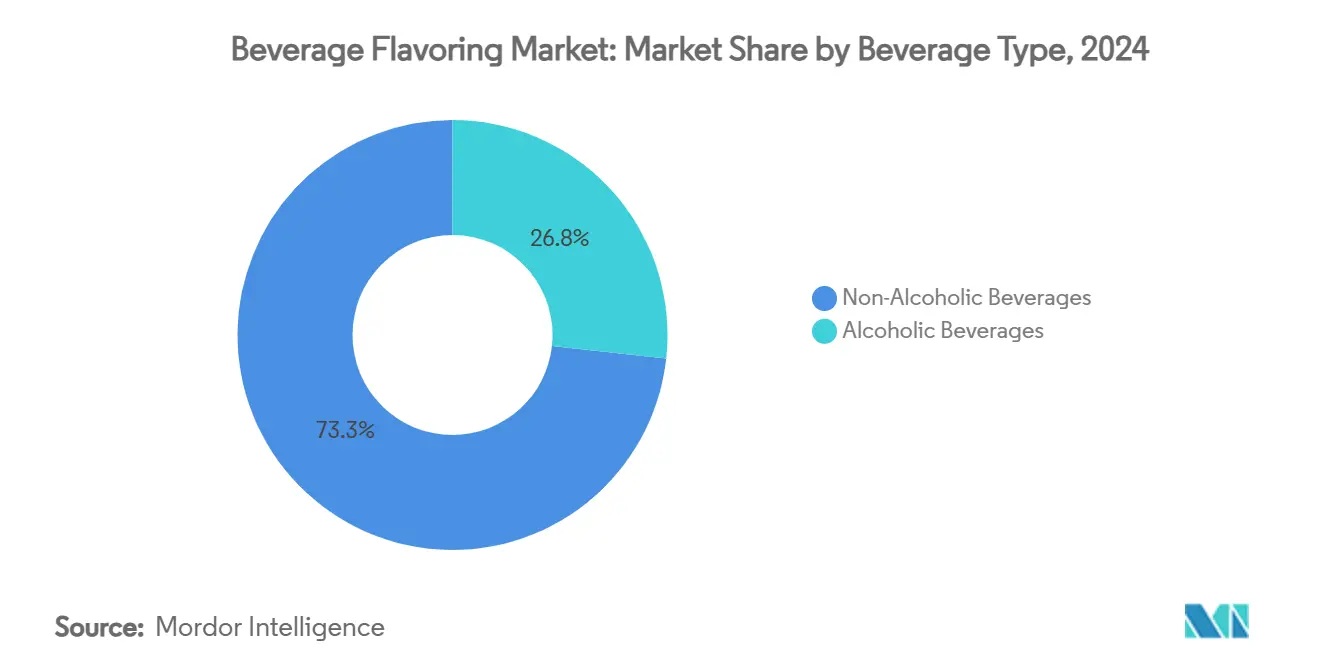

- By beverage type, non-alcoholic drinks held a 73.25% revenue share in 2024, while alcoholic beverages are accelerating at an 8.06% CAGR to 2030.

- By category, artificial variants commanded 56.67% of the beverage flavors market share in 2024; natural flavors are expanding more quickly at 6.85% CAGR through 2030.

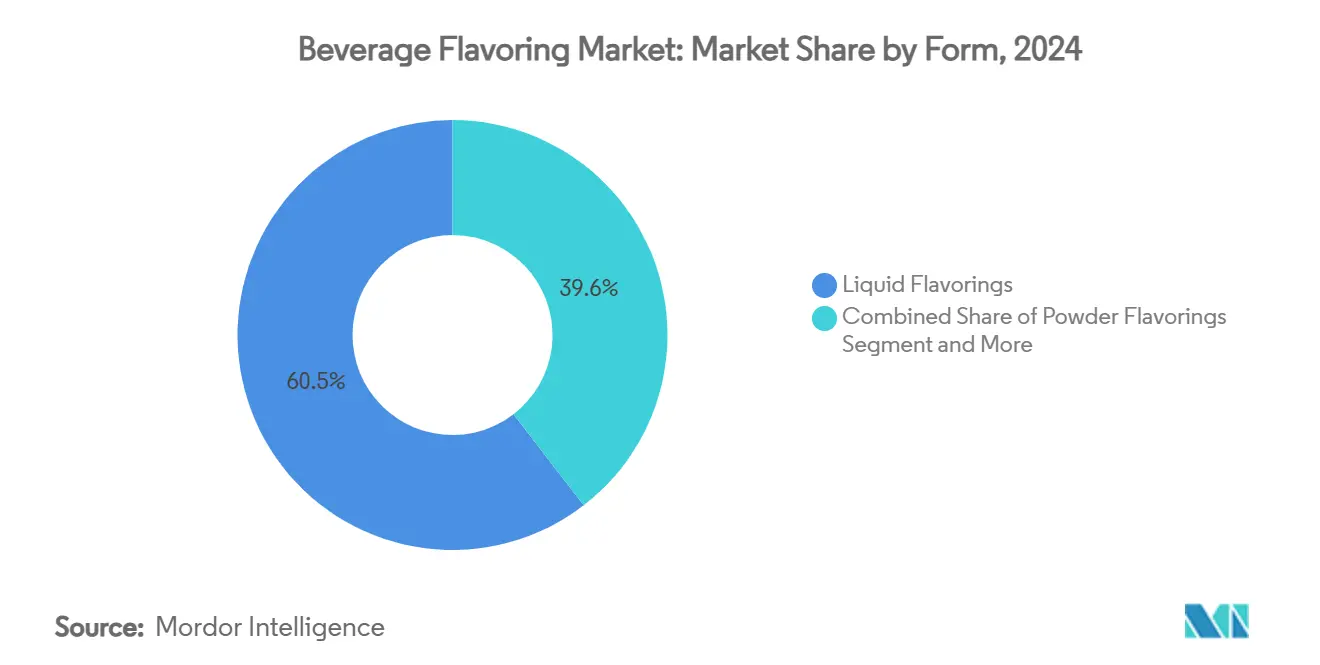

- By form, liquid systems accounted for 60.45% of the beverage flavors market size in 2024, yet powder formats are projected to rise at 8.32% CAGR to 2030.

- By end-user, foodservice led with 63.74% revenue contribution in 2024, whereas the beverage manufacturing segment posts the strongest 7.07% CAGR outlook to 2030.

- By geography, Asia-Pacific captured 35.03% of the beverage flavors market size in 2024 and is set to climb at a 7.83% CAGR through 2030.

Global Beverage Flavoring Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Preference for Natural and Clean-Label Flavors | +1.2% | Global, with strongest impact in North America & Europe | Medium term (2-4 years) |

| Emergence of Exotic and Botanical Flavor Innovations | +0.8% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Expansion of Low-Sugar Beverage Flavor Solutions | +1.0% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Ready-to-Drink Segment Driving Flavor Development | +1.3% | Global, with strongest growth in Asia-Pacific & North America | Short term (≤ 2 years) |

| Premium Beverage Market Fueling Unique Flavor Combinations | +0.9% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Functional Beverage Requiring Advanced Flavoring | +1.1% | Global, with fastest adoption in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Preference for Natural and Clean-Label Flavors

Consumer demand for transparency is reshaping flavor formulation strategies as brands respond to the 94% of innovations incorporating sustainability values reported by industry leaders. The USDA's Policy Memo 11-1 specifies that natural flavors must comprise 0.05% to 0.40% of food products and be derived from nonsynthetic sources without artificial preservatives, creating formulation constraints that drive premium pricing[1]Source: USDA National Organic Program, "Policy Memorandum", ams.usda.gov. However, the regulatory landscape is tightening with HHS Secretary Robert F. Kennedy Jr.'s directive to eliminate self-affirmed GRAS determinations, potentially requiring FDA pre-market approval for new natural flavor ingredients. This shift will favor established companies with extensive regulatory documentation while creating barriers for smaller natural flavor innovators. The biotechnology sector is responding with precision fermentation techniques that produce natural-identical compounds, with companies like Spero Renewables developing corn fiber-derived vanillin that competes directly with rice-bran alternatives. This technological convergence suggests natural flavor premiums may compress as biotech production scales, fundamentally altering the economics of clean-label positioning.

Emergence of Exotic and Botanical Flavor Innovations

McCormick's designation of Aji Amarillo as the 2025 Flavor of the Year, with projected 59% menu growth over 4 years, exemplifies the industry's pivot toward tropical and botanical profiles that transcend traditional flavor boundaries. Kerry's 2025 Taste Charts identify "Tropical Vibes" and "Deliciously Unexpected" as key trends, driven by Gen Z consumers seeking personalized experiences that balance adventure with wellness. The botanical trend extends beyond flavor to functional benefits, with companies leveraging seaweed-derived hydrocolloids for texture enhancement while delivering umami complexity. Regulatory frameworks are adapting to accommodate these innovations, with FEMA's GRAS 30 publication including novel botanical extracts that previously lacked safety documentation [2]Source: Flavor and Extract Manufacturers Association of the United States (FEMA), "GRAS 30", femaflavor.org. The convergence of exotic flavors with functional benefits creates premium positioning opportunities, particularly in the Asia-Pacific market where traditional botanical knowledge intersects with modern beverage formats. This trend is accelerating biotechnology adoption as companies seek consistent supply chains for rare botanical compounds through fermentation rather than agricultural extraction.

Expansion of Low-Sugar Beverage Flavor Solutions

The low-sugar beverage segment is driving flavor innovation as manufacturers address taste masking challenges while maintaining consumer acceptance in health-conscious formulations. Sensient's BioSymphony platform demonstrates how biotransformation enhances flavor complexity while masking off-notes in high-protein beverages, addressing the dual challenge of nutrition and palatability. The regulatory environment supports this trend through FDA guidance on natural flavor definitions under 21 CFR 101.22, which permits flavor enhancement without artificial constituent additions. However, the technical complexity of low-sugar formulations requires advanced flavor delivery systems, with powder technologies gaining traction due to their stability in reduced-water activity environments. The RTD beverage market's projected growth is partially driven by low-sugar innovations that maintain taste satisfaction. This trend is creating competitive advantages for companies with biotechnology capabilities, as fermentation-derived flavor enhancers offer superior performance in sugar-reduced matrices compared to traditional extraction methods.

Ready-to-Drink Segment Driving Flavor Development

The RTD beverage category's explosive growth is fundamentally altering flavor development priorities as manufacturers optimize for shelf stability, temperature tolerance, and direct consumption rather than dilution-based applications. Givaudan's 27.3% sales growth in Latin America reflects the region's RTD adoption, with beverages contributing significantly to the company's CHF 3,752 million Taste & Wellbeing segment revenue. The technical requirements for RTD applications favor liquid flavoring systems that integrate seamlessly during production, explaining liquid flavors' 60.45% market dominance despite powder flavors' faster growth trajectory. Regulatory considerations become more complex in RTD applications as flavor stability must be maintained across extended shelf life without preservative systems that could trigger additional labeling requirements under 21 CFR 172.510. The convergence of RTD growth with functional beverage trends is creating demand for flavor systems that can mask botanical extracts, vitamins, and protein additions while maintaining consumer appeal. This technical challenge is driving consolidation as smaller flavor companies lack the R&D resources to develop sophisticated masking technologies, benefiting integrated players with both flavor and functional ingredient capabilities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Production and Certification Expenses for Natural Flavors | -0.7% | Global, with highest impact in North America & Europe | Medium term (2-4 years) |

| Complex Regulatory Framework for Flavor Additives | -0.5% | Global, with varying intensity by region | Long term (≥ 4 years) |

| Raw Material Supply Chain Constraints | -0.8% | Global, with acute impact on vanilla and citrus sourcing | Short term (≤ 2 years) |

| Flavor Variant Proliferation: Consumer Fatigue Concerns | -0.3% | Developed markets primarily, North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Production and Certification Expenses for Natural Flavors

Natural flavor production costs are escalating due to complex extraction processes, organic certification requirements, and the analytical verification methods required to prove natural sourcing under increasingly stringent regulatory frameworks. The FDA's potential elimination of self-GRAS determinations will require comprehensive safety documentation for new natural ingredients, with compliance costs potentially reaching hundreds of thousands of dollars per ingredient. FEMA's biotechnology evaluation framework requires additional safety assessments when production methods change, creating recurring certification expenses for companies adopting fermentation technologies. The analytical verification requirements under C-14 isotopic analysis for natural flavor authentication add significant testing costs, particularly for exotic botanical extracts where reference standards may not exist. These escalating costs are creating competitive advantages for larger companies that can amortize certification expenses across broader product portfolios, while smaller natural flavor specialists face margin compression. The cost pressure is accelerating biotechnology adoption as fermentation-derived natural flavors offer more predictable production economics compared to agricultural extraction methods subject to weather and geopolitical volatility.

Complex Regulatory Framework for Flavor Additives

The regulatory landscape for flavor additives is becoming increasingly fragmented across global markets, with the EU maintaining stricter natural flavor definitions requiring traditional production methods while the US allows broader biotechnology applications under FDA guidance. The Center for Science in the Public Interest's 2024 report highlights the USD 14 billion global flavor market's regulatory complexity, noting that thousands of untested chemicals operate under the GRAS loophole without FDA oversight. The regulatory divergence between markets creates compliance costs as companies must maintain separate formulations and documentation systems for different regions, particularly challenging for smaller companies lacking regulatory expertise. The anticipated tightening of GRAS regulations will likely consolidate the industry as compliance costs favor larger players with established regulatory infrastructure, while creating barriers to entry for innovative biotechnology companies developing novel flavor compounds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Beverage Type: Alcoholic Beverages Drive Premium Innovation

Non-alcoholic beverages dominate with 73.25% market share in 2024, reflecting their ubiquity across consumer demographics and consumption occasions, while alcoholic beverages are experiencing faster growth at 8.06% CAGR through 2030 as craft spirits and premium cocktail culture demand sophisticated flavor profiles. The alcoholic segment's growth acceleration stems from premiumization trends where consumers pay higher prices for unique flavor experiences, creating margin opportunities that justify complex flavor development investments. Non-alcoholic beverages benefit from health consciousness trends and functional ingredient integration, but face margin pressure from retailer private label competition and regulatory scrutiny over sugar content and artificial additives.

The RTD alcoholic beverage category is driving flavor innovation as manufacturers seek shelf-stable formulations that maintain taste integrity without traditional bar-mixing techniques, requiring flavor systems optimized for direct consumption rather than dilution applications. Symrise's double-digit growth in beverage applications during Q1 2025 reflects this premiumization trend, with the company gaining market share through innovative solutions that address both alcoholic and non-alcoholic segments. The convergence of health trends with alcoholic beverages is creating demand for functional ingredients that require advanced masking technologies, positioning companies with biotechnology capabilities for competitive advantage in both segments.

By Category: Natural Flavors Gain Despite Artificial Dominance

Artificial flavors maintain 56.67% market share in 2024 due to cost advantages and consistent supply reliability, while natural flavors are growing faster at 6.85% CAGR through 2030 as consumer preferences shift toward clean-label products and regulatory frameworks increasingly favor transparency. The growth differential reflects the premium pricing power of natural flavors, with companies willing to invest in higher-cost ingredients to capture consumer willingness to pay for perceived health benefits and environmental sustainability. However, the artificial segment's resilience demonstrates that performance and cost considerations remain paramount in many applications, particularly in price-sensitive markets and functional beverage formulations where flavor masking requirements favor synthetic solutions.

The regulatory environment is reshaping the competitive dynamics between natural and artificial flavors, with the FDA's potential elimination of self-GRAS determinations creating compliance advantages for established artificial flavor compounds with extensive safety documentation. Biotechnology is blurring the traditional boundaries between natural and artificial categories, with fermentation-derived compounds meeting natural flavor definitions while offering the consistency and cost advantages traditionally associated with synthetic production. Companies like Spero Renewables are developing corn fiber-derived vanillin that competes directly with both synthetic vanillin and traditional natural sources, suggesting the natural-artificial distinction may become less relevant as biotechnology scales.

By Form: Powder Technologies Enable Functional Innovation

Liquid flavorings command 60.45% market share in 2024 due to their ease of integration in traditional beverage production processes and superior dispersion characteristics in aqueous systems, while powder flavorings are experiencing the fastest growth at 8.32% CAGR through 2030 driven by their stability advantages in functional beverage applications and reduced transportation costs. The powder segment's growth acceleration reflects the industry's shift toward functional beverages where ingredient stability during extended shelf life becomes critical, particularly for protein-fortified and vitamin-enhanced formulations that are sensitive to moisture and temperature fluctuations. Powder technologies also enable innovative delivery systems such as instant beverage mixes and on-demand flavoring solutions that cater to personalization trends.

The technical advantages of powder flavoring systems are becoming more pronounced as beverage manufacturers seek to reduce water content in concentrated products and minimize cold chain requirements for global distribution. Encapsulation technologies are advancing rapidly, with spray drying and fluid bed coating enabling controlled release profiles that can deliver flavor bursts during consumption while maintaining stability during storage. The "Others" category, including syrups and sprays, represents emerging delivery formats that bridge liquid and powder advantages, particularly in foodservice applications where portion control and consistency are paramount. The convergence of powder technologies with biotechnology-derived flavors is creating new possibilities for functional beverage applications, as fermentation-produced compounds often demonstrate superior stability in dried formats compared to traditional extraction-based flavors.

By End-User: Beverage Industry Integration Accelerates

The foodservice segment leads with 63.74% market share in 2024, reflecting the sector's role as a flavor innovation laboratory where new taste profiles are tested and refined before broader market introduction, while the beverage industry segment is growing faster at 7.07% CAGR through 2030 as manufacturers integrate flavor capabilities internally rather than relying on external suppliers. This growth differential indicates a strategic shift toward vertical integration as beverage companies seek greater control over flavor formulations and supply chain security, particularly for proprietary blends that differentiate their products in competitive markets. The retail segment's fragmentation across multiple channels creates complexity for flavor suppliers, with supermarkets/hypermarkets requiring different packaging and labeling compared to online retail platforms.

The beverage industry's faster growth reflects the RTD market expansion and the need for flavors optimized for direct consumption rather than dilution-based applications, requiring different technical specifications compared to foodservice concentrates. Custom Flavors' USD 7.75 million investment in North Carolina demonstrates this trend, with the company establishing an Eastern hub to serve beverage manufacturers directly rather than through distributor networks. The online retail channel's growth is creating new requirements for flavor packaging and stability, as direct-to-consumer shipments may experience temperature fluctuations and extended transit times that challenge traditional flavor delivery systems.

Geography Analysis

Asia-Pacific dominates with 35.03% market share in 2024 while simultaneously exhibiting the fastest regional growth at 7.83% CAGR through 2030, driven by India's health beverage market tripling to USD 30 billion by 2026 and China's expanding middle class demanding premium flavor experiences in both traditional and Western beverage formats. The region's dual leadership reflects both scale advantages and demographic trends, with urbanization and rising disposable incomes creating demand for convenient, flavorful beverage options. Symrise's strong performance in the EAME and Asia/Pacific regions during Q1 2025 demonstrates the competitive advantages available to companies that can adapt global flavor technologies to local taste preferences and regulatory requirements.

North America and Europe represent mature markets where growth is driven by premiumization and functional ingredient integration rather than volume expansion, creating different competitive dynamics and margin structures. This growth is fueled by increasing preference for botanical and plant-based flavors, strict regulations on artificial additives, and rising popularity of flavored waters, energy drinks, and organic beverages. The European market emphasizes innovation in healthier and authentic flavor profiles to meet evolving consumer tastes and regulatory demands.

The Middle East and Africa represent emerging opportunities where beverage consumption patterns are evolving rapidly, but regulatory frameworks remain fragmented and supply chain infrastructure requires continued investment. South America's growth is driven by Brazil's large domestic market and the region's role as a testing ground for tropical flavor innovations that subsequently expand to global markets. This dual-region focus on natural, authentic, and innovative flavors highlights the evolving competitive dynamics shaping the global beverage flavoring industry.

Competitive Landscape

The beverage flavors market exhibits moderate consolidation, enabling both established multinational corporations and specialized biotechnology firms to compete effectively through differentiated innovation strategies and regional market expertise. Some of the significant players include Givaudan, International Flavors & Fragrances Inc., Jeneil Biotech, Kerry Group plc, and MB-Holding GmbH & Co. KG (MartinBauer). Market leaders like Givaudan, IFF, etc. are leveraging their scale advantages to invest in biotechnology platforms and global R&D infrastructure, while smaller players focus on niche applications such as organic certifications, exotic botanical extracts, or specialized delivery systems for functional beverages. These companies are expanding their portfolios toward plant-based, botanical, and hybrid flavor formulations designed for emerging beverage categories like adaptogenic drinks, kombucha, and electrolyte-enhanced waters.

The competitive intensity is increasing as regulatory changes favor companies with established GRAS documentation and compliance infrastructure, creating barriers to entry for new participants while rewarding incumbents with comprehensive safety databases. Strategic patterns reveal a shift toward vertical integration and biotechnology adoption, with major acquisitions including Glanbia's USD 300 million purchase of Flavor Producers and McCormick's USD 710 million acquisition of FONA International demonstrating the premium valuations placed on natural flavor capabilities and customer relationships. Symrise dominate with extensive R&D capabilities, leveraging advanced extraction technologies and AI-driven flavor mapping to meet evolving consumer preferences that prioritize clean-label, health-conscious, and authentic flavor profiles.

Besides the large flavor houses, market competition intensifies with startups and smaller players pushing novel and regional flavor blends, fueling product differentiation. The increasing consumer demand for exotic, natural, and personalized flavors pushes manufacturers to innovate with flavor encapsulation technologies that extend shelf life while preserving aroma and taste. Moreover, sustainability and traceability have become key competitive factors, with companies investing in bio-based sources and eco-friendly production methods. The growing beverage segments such as ready-to-drink teas, functional beverages, and flavored waters are particularly lucrative, further deepening competition. Overall, agility in innovation, strategic collaborations, and the ability to align with health and sustainability trends define success in the current beverage flavoring market landscape

Beverage Flavoring Industry Leaders

-

International Flavors & Fragrances Inc.

-

Jeneil Biotech

-

Kerry Group plc

-

Givaudan S.A.

-

MB-Holding GmbH & Co. KG (MartinBauer)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sensient Flavors & Extracts launched a portfolio of natural flavors developed through biotransformation called BioSymphony. Sensient Flavors & Extracts stated BioSymphony, which used ingredients found in nature, eliminated the need for special regional labeling and simplified formulations for global brands. The portfolio delivered value for food and beverage manufacturers in three ways including: premiumization, flavor expansion and ingredient challenge solutions.

- March 2025: Isobionics, a biotechnology brand of BASF Aroma Ingredients, launched two new natural ingredients in the flavor market. Isobionics Natural beta-Sinensal 20 and Isobionics Natural alpha-Humulene 90 were produced using a fermentation process, making them a new addition to the flavor industry. This flavor ingredient has a high purity and is suitable for non-alcoholic and alcoholic beverages – especially for mango, raspberry, mint, and citrus flavors.

- April 2024: Torani, a leader in the flavor industry launched Torani Dragon Fruit Syrup to its portfolio of more than 150 syrups and sauces. In contrast to its distinctive appearance, dragon fruit had a light, refreshing flavor with floral notes and was often likened to pear and kiwi. Torani Dragon Fruit Syrup was well-suited to layer with a variety of mainstream flavors to create a new and interesting combination of tastes.

Global Beverage Flavoring Market Report Scope

| Alcoholic Beverages |

| Non-Alcoholic Beverages |

| Natural |

| Artificial |

| Liquid |

| Powder |

| Others |

| Beverage Industry | |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Beverage Type | Alcoholic Beverages | |

| Non-Alcoholic Beverages | ||

| By Category | Natural | |

| Artificial | ||

| By Form | Liquid | |

| Powder | ||

| Others | ||

| By End-user | Beverage Industry | |

| Foodservice | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores/Grocery Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the global beverage flavors market in 2025?

The beverage flavors market size is valued at USD 5.33 billion in 2025 and is projected to reach USD 7.21 billion by 2030.

Which region contributes most to flavor revenues?

Asia-Pacific leads with 35.03% of global value and shows the fastest 7.83% CAGR to 2030.

Why are powder flavors gaining ground?

Powder systems grow at 8.32% CAGR because they improve functional ingredient stability, lengthen shelf life, and reduce freight costs.

What is driving natural flavor demand?

Regulatory tightening and consumer preference for clean-label products increase natural flavor uptake even though artificial variants remain cheaper.

Page last updated on: