Cold Brew Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

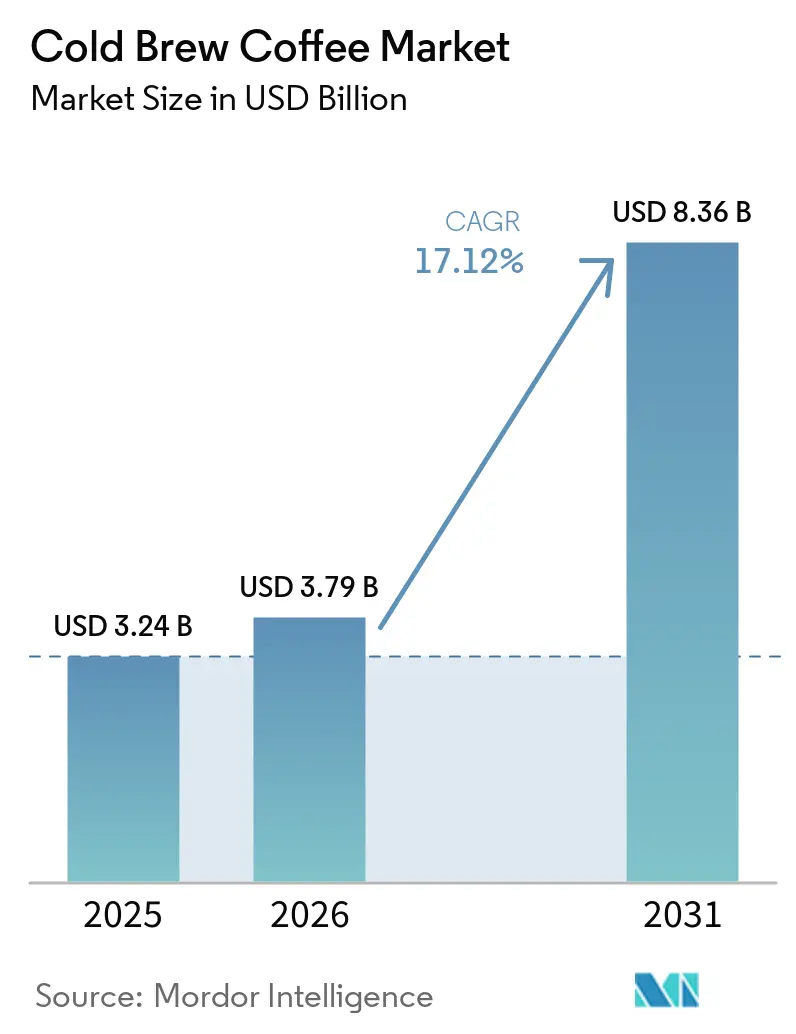

| Market Size (2026) | USD 3.79 Billion |

| Market Size (2031) | USD 8.36 Billion |

| Growth Rate (2026 - 2031) | 17.12% CAGR |

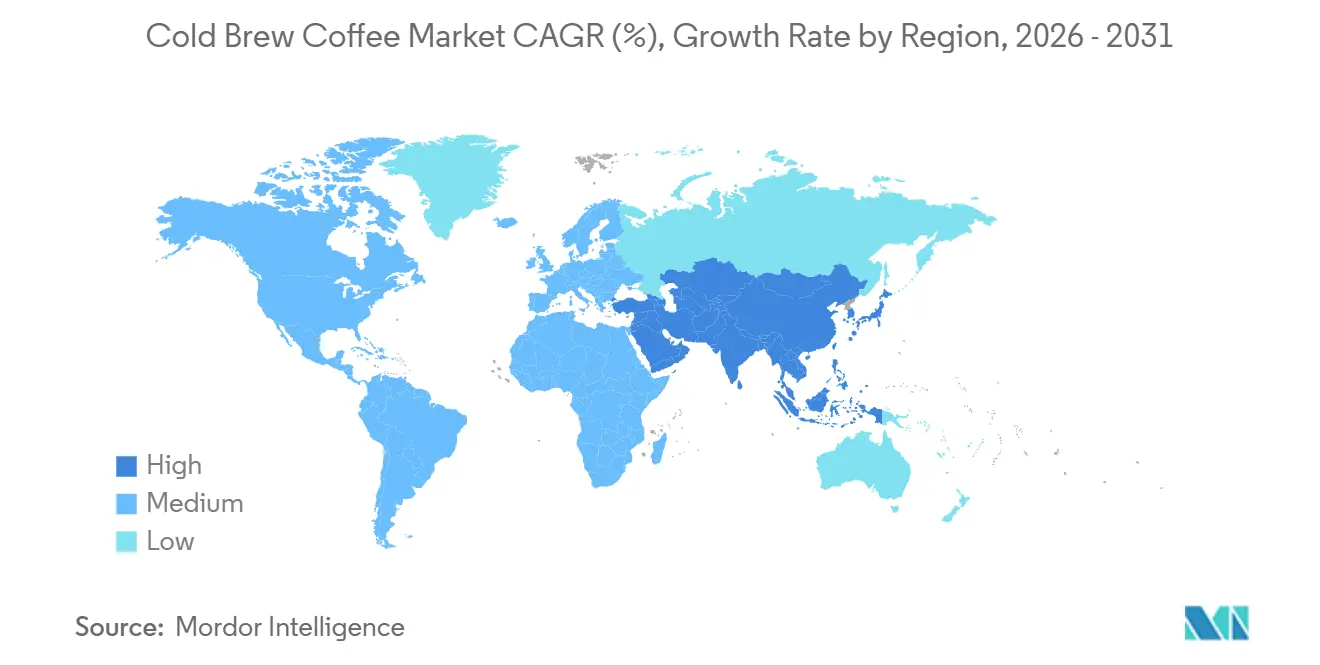

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cold Brew Coffee Market Analysis by Mordor Intelligence

The cold brew coffee market size is expected to increase from USD 3.24 billion in 2025 to USD 3.79 billion in 2026 and reach USD 8.36 billion by 2031, growing at a CAGR of 17.12% over 2026-2031. As younger consumers in the cold brew coffee market pivot from instant products to premium options, the demand is leaning towards slow-extracted, lower-acidity beverages. These premium choices often highlight single-origin beans and innovative flavor profiles, appealing to a growing segment of coffee enthusiasts seeking unique and high-quality experiences. While North America held a 40.03% market share in 2025, the Asia-Pacific region is set to surge at an 18.98% CAGR. This growth is fueled by rising incomes, urbanization, and the proliferation of specialty cafés, particularly in China, India, and Southeast Asia, where coffee culture is rapidly evolving. Ready-to-drink (RTD) products in the cold brew coffee market dominate sales in grocery and convenience stores, offering convenience and variety to consumers. Meanwhile, pods and flash-chill systems are making artisanal coffee extraction accessible in home kitchens, catering to the increasing demand for premium coffee experiences at home. The cold brew coffee market is expanding in both retail and foodservice sectors, driven by a growing interest in organic certifications, recyclable aluminum cans, and functional additives like protein and adaptogens, which align with consumer preferences for sustainability and health-focused products.

Key Report Takeaways

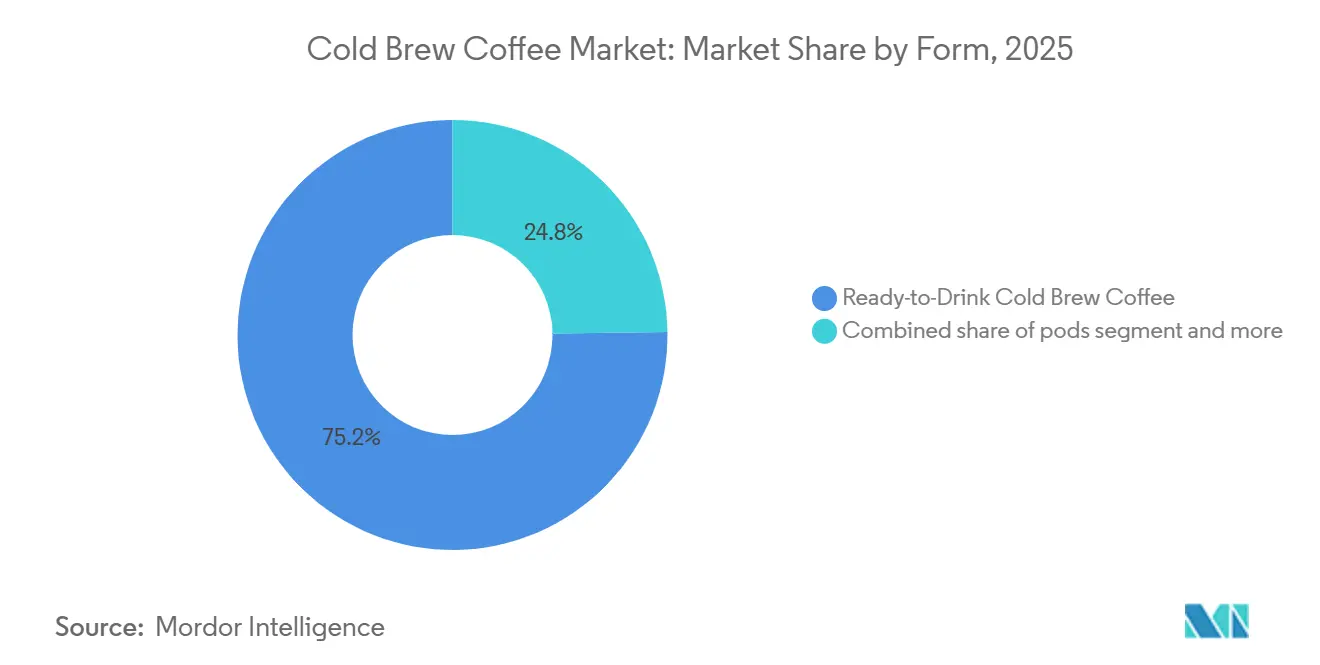

- By form, RTD products held 75.23% of the 2025 cold brew coffee market share and pods are forecast to record an 18.33% CAGR through 2031.

- By flavor, unflavored variants led with 56.71% revenue share in 2025, whereas flavored cold brew is set to advance at a 19.07% CAGR to 2031.

- By packaging, bottles captured 55.34% share in 2025, yet cans are projected to grow at 18.81% CAGR.

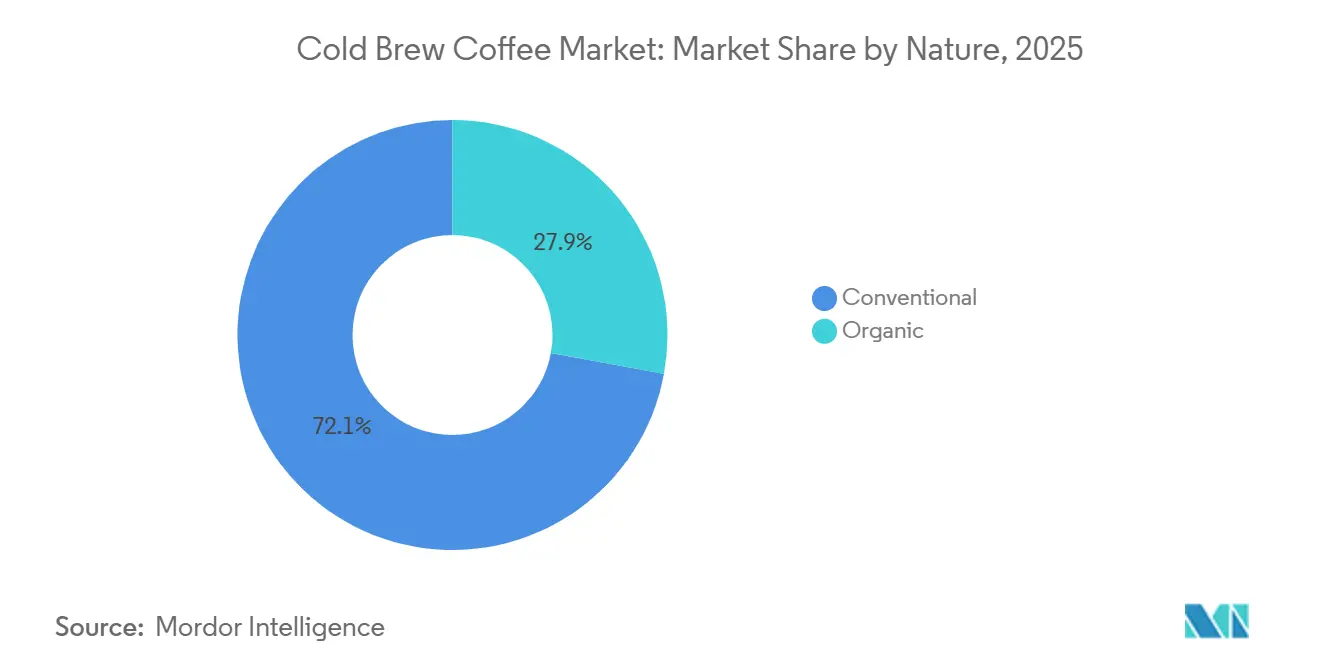

- By nature, conventional production accounted for 72.12% of volume in 2025, while organic offerings are projected to post a 19.22% CAGR between 2026-2031.

- By distribution channel, off-trade held 58.34% share in 2025 and on-trade is forecast to expand at 19.36% CAGR through 2031.

- Regionally, North America retained the largest 2025 share at 40.03%, but Asia-Pacific is positioned as the fastest-growing territory at 18.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cold Brew Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer preference for distinctive coffee beverages | +3.2% | Global, with early gains in North America, Western Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Preference for premium and specialty coffee | +2.8% | North America, Europe, Asia-Pacific core markets | Medium term (2-4 years) |

| Popularity of ready-to-drink (RTD) formats | +4.1% | Global, strongest in North America, the Middle East and North Africa, Latin America | Short term (≤ 2 years) |

| At-home mixology culture fuelling cold-brew experimentation | +2.3% | North America, Europe, with spill-over to Asia-Pacific urban centers | Medium term (2-4 years) |

| Energy-positive brewing and carbon-reduction initiatives | +1.6% | Europe, North America, with regulatory push in Asia-Pacific | Long term (≥ 4 years) |

| Integration into functional foods and nutraceuticals | +2.1% | North America, Europe, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising consumer preference for distinctive coffee beverages

In a notable departure from traditional consumption habits, 47% of consumers aged 18 to 24 reported having coffee in the previous day, highlighting a growing preference for coffee among younger demographics[1]Source: National Coffee Association, "Daily coffee consumption at 20-year high, up nearly 40%," ncausa.org. In the cold brew coffee market, cold extraction, producing 67% less acidity than the hot drip method, enables roasters to emphasize terroir and adopt innovative techniques like anaerobic fermentation, which enhances flavor complexity and uniqueness. While chains infuse regional flavors, such as ube coconut or banana cold foam, to drive social media buzz and attract a broader audience, independent cafés serve as innovation hubs, experimenting with new ideas and shortening the journey from concept to market to under 18 months. By 2025, a median price of USD 5.58 for ready-to-drink (RTD) coffee underscores consumers' readiness to invest in unique flavor profiles and premium offerings, even as traditional plain drip coffee sees a decline in popularity due to shifting preferences.

Preference for premium and specialty coffee

In 2025, U.S. consumption of espresso-based and cold specialty drinks surged to 45%[2]Source: Specialty Coffee Association, "2025 National Coffee Data Trends Specialty Coffee Breakout Report", sca.coffee. This growth in the cold brew coffee market reflects shifting consumer preferences toward premium and innovative beverage options, driven by a demand for high-quality and differentiated products. Brands like La Colombe leverage transparency in direct trade and single origin to bolster their premium positioning, allowing them to market 11-ounce RTD draft lattes at USD 3.29, boasting 50% less sugar than the category average. Within the cold brew coffee market, packaging plays a pivotal role in reinforcing this value: glass bottles exude craft authenticity, appealing to consumers seeking artisanal products, while nitrogen-charged cans mimic a draft pour, enhancing the retail experience and offering a unique sensory appeal. These packaging innovations not only elevate the perceived value of the product but also align with consumer expectations for convenience and premium quality in ready-to-drink beverages.

Popularity of ready-to-drink formats

In 2024, the global ready-to-drink (RTD) segment of the cold brew coffee market experienced significant growth. However, the cold brew segment is expanding at a faster pace due to its strong growth potential. In Europe, the addition of premium chillers in convenience stores contributed to a notable increase in value sales. Meanwhile, the Middle East observed a substantial rise in RTD coffee consumption over recent years. Yet, challenges persist: while high-temperature pasteurization can mute flavors, cold-chain distribution significantly inflates logistics costs. Manufacturers are increasingly investing in innovative packaging solutions to address shelf-life concerns. Additionally, advancements in cold-chain technology are being explored to optimize logistics efficiency without compromising product quality. Consumer preferences for convenient and premium beverages are further driving innovation in the RTD coffee market. Moreover, sustainability initiatives, such as eco-friendly packaging, are gaining traction as companies aim to align with evolving environmental standards.

At-home mixology culture fueling experimentation

Seventy-five percent of Gen Z consumers in the cold brew coffee market are customizing drinks at home, sparking a surge in interest for modular brewers and eco-friendly pods. Keurig's K-Rounds and QuickChill system promise café-quality cold coffee in under three minutes. Meanwhile, start-ups are introducing easily transportable recyclable concentrates. Accessories in the cold brew coffee market, like nitro kegs and cold-foam makers, are turning cold brew into a versatile platform, compelling RTD brands to stand out with enhanced functions or eye-catching packaging. This trend highlights the growing demand for personalization and sustainability in the beverage market. Companies are increasingly focusing on innovative solutions to cater to these evolving consumer preferences. Additionally, the shift toward at-home beverage customization is reshaping the competitive landscape, encouraging brands to innovate rapidly. As a result, the market is witnessing a blend of technology-driven solutions and environmentally conscious offerings to meet consumer expectations.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent preference for instant / traditional hot coffee | -2.4% | Global, strongest in Asia-Pacific (China, India), Latin America, and price-sensitive segments | Short term (≤ 2 years) |

| Stringent global food-safety and labelling regulations | -1.3% | North America (FDA), Europe (EU regulations), with emerging compliance in Asia-Pacific | Medium term (2-4 years) |

| Limited arabica-bean supply volatility from climate shocks | -2.7% | Global, with acute impact in Brazil, Colombia, Central America production zones | Short term (≤ 2 years) |

| Quality degradation in long-haul e-commerce fulfilment | -0.8% | Global, particularly affecting DTC brands and rural/remote delivery zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent preference for instant/traditional hot coffee

In 2025, plain cold brew orders experienced a decline at Toast POS locations, while lattes and energy drinks saw growth. This cold brew coffee market trend highlights cold brew's competition not only with hot coffee but also with other caffeinated beverages. In Brazil, domestic coffee consumption decreased as retail prices for roasted and ground coffee rose. At the same time, consumption of soluble (instant) coffee increased, reflecting a shift by price-conscious consumers. This pattern underscores a structural challenge for cold brew: its lengthy extraction process and premium positioning make it more expensive than instant granules or hot drip coffee, limiting its appeal in price-sensitive markets. In the cold brew coffee market in the Asia-Pacific region, instant coffee continues to dominate in India's tier-2/3 cities and in China, while cold brew remains a niche product in urban areas. Although India's cold brew market is expected to grow significantly, it is starting from a small base. On the on-premise side, cold brew demand was notably higher in summer compared to winter. However, this seasonality creates challenges for brands, including inventory risks and underutilized production during colder months.

Stringent global food-safety and labeling regulations

RTD brands must now disclose caffeine content and use high-temperature short-time processing for shelf stability, as mandated by FDA guidance. However, this processing method can mute flavor nuances. While cold-chain strategies safeguard taste, they also elevate freight costs and restrict retail placement. U.S. exporters face added compliance challenges in Europe, where multilingual labels and recyclability icons are the norm. These regulations in the cold brew coffee market require brands to invest in localized packaging solutions, which can increase production costs. Additionally, navigating varying regulatory frameworks across European countries adds complexity to market entry strategies. As a result, companies must balance compliance efforts with maintaining competitive pricing and product quality. Furthermore, the need for sustainable packaging to meet European environmental standards adds another layer of operational challenges. This shift toward sustainability often necessitates collaboration with specialized suppliers, further impacting supply chain dynamics. Companies must also allocate resources for ongoing monitoring of regulatory updates to ensure continued compliance in international markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: RTD Anchors Volume, Pods Accelerate Penetration

In 2025, ready-to-drink (RTD) formats dominated the global cold brew coffee market, capturing a significant 75.23% share. Their ubiquitous presence in supermarket chillers, convenience store coolers, and foodservice fountain systems has ensured easy accessibility for consumers. While growth is projected to moderate to the mid-teens due to market saturation in North America, innovation continues to drive demand. New product extensions, such as protein-enriched variants, plant-based milk infusions, and carbonated cold brew options, are injecting fresh energy into the category. Additionally, the trend of on-the-go consumption further cements RTD's leading position.

Pod-based systems are rapidly emerging in the cold brew coffee market as the fastest-growing segment. Projections suggest an impressive 18.33% CAGR through 2031, with the segment eyeing a valuation of USD 1.46 billion and a 17% share of the global market. This growth surge is largely due to advancements in single-serve technology, especially features like programmable flow rates and flash-chill, which replicate the traditional slow immersion brewing method. Keurig's introduction of K-Rounds, backed by a substantial base of 45 million installed brewers, paves the way for rapid market penetration. At the same time, European appliance manufacturers are developing open-system capsules, broadening compatibility and diversifying consumer options. Unlike ground coffee, pods simplify the brewing process by removing the need for measuring and extended steeping, making them particularly appealing to busy consumers.

By Flavor: Purist Core Meets Seasonal Creativity

In 2025, unflavored cold brew commanded the largest cold brew coffee market share, making up 56.71% of total consumption. Coffee purists, who prioritize single-origin transparency, back this dominance, often paying a premium for quality and authenticity. The segment's strong emphasis on simplicity and craftsmanship resonates deeply with dedicated coffee enthusiasts. Brands are doubling down on origin storytelling and showcasing brewing expertise to nurture consumer loyalty. Consequently, even as the category sees rising experimentation, unflavored offerings enjoy a stable and committed base.

Flavored cold brew is on a rapid ascent, with projections indicating a CAGR of 19.07%, pushing it past the USD 3.1 billion mark by 2031. This surge is fueled by brands rolling out enticing seasonal flavors such as ube coconut, toasted banana, and lavender Earl Grey, which drive repeat purchases. The power of social media is undeniable, with viral sensations like Starbucks’ Iced Ube Coconut racking up over 50 million views on TikTok shortly after launch. Yet, companies tread carefully, balancing innovative flavors with traditional taste preferences, as an overly sweet profile might alienate some consumers. To navigate this, brands are strategically pairing their experimental flavors with classic black offerings, broadening their appeal while keeping the momentum alive.

By Packaging Format: Glass Signals Craft, Cans Capture Mobility

Bottled formats led the global cold brew coffee market in 2025, capturing 55.34% of the total share. Their dominance is largely driven by premium positioning, as transparent packaging allows brands to showcase layered textures and foam, enhancing visual appeal. Glass bottles, in particular, align well with high-end branding and artisanal perceptions. This format remains popular among consumers seeking quality and aesthetic presentation in ready-to-drink beverages. As a result, bottled products continue to anchor the premium segment despite rising competition from alternative packaging.

In the cold brew coffee market, aluminum cans are the fastest-growing segment, projected to expand at a CAGR of 18.81% in the coming years. With a 32% market share in 2025, cans are gaining traction due to their lightweight, fully recyclable nature and retailer preference for sustainable formats. Innovations such as nitro-widget technology enable cans to replicate the creamy, draft-like texture of freshly poured cold brew. Additionally, cans are well-suited for channels where glass is restricted, including vending machines, airlines, and fitness centers. This versatility is expanding consumption occasions beyond traditional settings, supporting rapid growth and potential to surpass glass by 2029.

By Nature: Conventional Scale Versus Organic Upside

In 2025, conventional coffee beans held a commanding 72.12% share of the cold brew coffee market. Their dominance stems from scale efficiencies, widespread availability, and competitive pricing, outpacing specialty alternatives. By sourcing conventionally, brands tap into mass-market demand while keeping costs in check. Bolstered by established supply chains and steady production, this segment remains the category's backbone, even as interest in premium and sustainable options rises. Additionally, the ability of conventional coffee to meet consistent quality standards and cater to diverse consumer preferences further strengthens its position in the cold brew coffee market.

Organic coffee is on a rapid ascent, with projections indicating a CAGR of 19.22% through 2031. This surge is fueled by heightened retail visibility, especially in the U.S. and Germany, where certified organic products enjoy prime shelf space. Yet, challenges loom: Brazil's 2024–2025 drought poses risks to organic arabica supplies. Still, with price premiums reaching USD 1.36 per pound, many farmers are tempted to make the switch. While the three-year certification process poses hurdles, consumers' readiness to pay 20–30% more for verified organic sourcing propels the trend. Furthermore, the growing awareness of environmental sustainability and health benefits associated with organic coffee is driving its adoption among a broader consumer base. As a result, organic coffee is set to surpass a 35% market share by 2031.

By Distribution Channel: Off-Trade Dominance Faces On-Trade Acceleration

In 2025, the off-trade segment led the global cold brew coffee market, capturing 58.34% of total revenue and solidifying its role as the primary volume driver. Its dominance stems from its widespread presence in supermarkets, hypermarkets, and the swiftly growing e-commerce platforms, ensuring easy consumer access. The allure of ready-to-drink formats and multi-pack deals bolsters regular household consumption. Moreover, robust distribution networks and strategic promotional pricing cement its leading stance. Consequently, even as consumption trends evolve, the off-trade segment remains the market's volume backbone.

Conversely, the on-trade segment in the cold brew coffee market is rapidly gaining momentum, with projections indicating a CAGR of 19.36% from 2025 to 2031. The cold brew coffee market value, starting at USD 1.36 billion in 2025, is set to soar past USD 4 billion by 2031, fueled by trends of premiumization and a focus on experiential consumption. Establishments like coffee shops, quick-service restaurants, and hotels are elevating their offerings. Innovations such as nitro taps, cold foam textures, and eye-catching presentations not only enhance the experience but also justify premium pricing. Furthermore, technological strides, particularly AI-driven inventory tracking, are refining the management of perishable cold brew kegs, curbing waste, and bolstering margins. This blend of heightened consumer experience and streamlined operations is propelling the on-trade segment's growth.

Geography Analysis

In 2025, North America held a dominant 40.03% of the cold brew coffee market share, bolstered by its extensive café networks, sophisticated Direct Store Delivery (DSD) routes, and consumers willing to spend USD 5.58 on a ready-to-drink (RTD) coffee can. However, as the market reaches saturation, growth has decelerated to high single digits, pushing brands to innovate with functional blends and eco-friendly packaging. The region's established infrastructure and consumer familiarity with premium coffee products have contributed to its sustained leadership. Additionally, the focus on sustainability aligns with evolving consumer preferences, creating opportunities for brands to differentiate themselves.

Asia-Pacific is on a rapid ascent, boasting an 18.98% CAGR projected through 2031. In 2025, China's coffee servings surged by 15%, Indonesia's consumption saw a threefold increase over five years, and in India, specialty roasters are leveraging direct-to-consumer (DTC) channels to engage urban millennials. The region's growing middle class and increasing urbanization are driving demand for RTD coffee products. Furthermore, the aggressive expansion of café chains highlights the untapped potential in emerging markets, making the Asia-Pacific region a focal point for global players.

In the cold brew coffee market, Europe experienced a 9.4% uptick in RTD coffee value in 2024, driven by petrol stations and convenience stores dedicating more chiller space to canned nitro brews. While France, Germany, and Italy dominate in volume, the UK and Netherlands are setting trends with oat-milk-based cold brew lattes. The ready-to-drink coffee market in the United Kingdom is expanding, mirroring a wider European embrace of cold brew offerings[3]Source: Center for the Promotion of Imports, "The United Kingdom’s market potential for coffee," cbi.eu. The shift toward plant-based and specialty coffee options reflects changing consumer preferences in the region. Moreover, the increasing availability of RTD coffee in non-traditional retail channels is further boosting its accessibility and appeal.

The Middle East and North Africa in the cold brew coffee market are also making their mark: Saudi Arabia's coffee market crossed the USD 1.6 billion threshold in 2024, and Dubai, with over 4,000 coffee shops, is experimenting with new RTD flavors to cater to its tourist influx. The region's cultural affinity for coffee and rising disposable incomes are fueling market growth. Additionally, the focus on innovation and premiumization is helping brands capture the attention of both local consumers and international visitors.

Competitive Landscape

The cold brew coffee market's moderate concentration facilitates both multinational consolidations and disruptions by niche brands. Keurig Dr Pepper is set to finalize its USD 18 billion acquisition of JDE Peet’s by April 2026, paving the way for the creation of the world’s largest pure-play coffee entity. This new giant is poised to boast annual sales nearing USD 16 billion, complemented by a synergistic distribution network spanning pods, ready-to-drink (RTD) beverages, and food services. The acquisition is expected to significantly enhance Keurig Dr Pepper's market position in the global coffee industry. Additionally, it highlights the growing trend of consolidation among major players to achieve economies of scale and expand their product portfolios.

Meanwhile, Chobani's foray into craft RTD lattes with its USD 900 million acquisition of La Colombe is not without its challenges; a trademark tussle with Danone over the “Bright & Mellow” label underscores the intensifying brand-protection skirmishes on crowded retail shelves. This acquisition within the cold brew coffee market allows Chobani to diversify its offerings and strengthen its presence in the premium coffee segment. The ongoing trademark dispute also reflects the increasing competition and the need for companies to safeguard their intellectual property in a saturated market.

Califia Farms has successfully garnered USD 225 million in funding, aiming to globalize its oat-milk nitro lattes, seamlessly merging the plant-based movement with the functionality of cold brews. The funding will enable Califia Farms to expand its production capabilities and enhance its distribution network across key markets. Furthermore, the company’s focus on innovation aligns with the rising consumer demand for healthier and sustainable beverage options.

In a notable move, UPTIME Energy has bolstered its energy-drink lineup by acquiring RISE Brewing, bringing onboard their nitro expertise. This acquisition within the cold brew coffee market highlights the growing convergence between the realms of functional beverages and coffee. It also positions UPTIME Energy to cater to a broader consumer base seeking energy drinks with unique flavor profiles. The integration of RISE Brewing’s expertise is expected to drive product differentiation and innovation within UPTIME Energy’s portfolio.

Royal Cup's USD 28 million acquisition of Farmer Brothers not only amplifies its route distribution but also enhances its private-label roasting prowess. The deal is anticipated to strengthen Royal Cup’s operational efficiency and expand its footprint in the coffee supply chain. Moreover, it underscores the strategic importance of private-label capabilities in meeting the evolving demands of both retailers and consumers. As the competition heats up, players in the market are channeling investments towards sustainability, functional ingredients, and a broad omni-channel approach, all in a bid to carve out a significant share in the burgeoning cold brew coffee arena.

Cold Brew Coffee Industry Leaders

-

Starbucks Corporation

-

Nestlé S.A.

-

JAB Holding Company

-

The Coca-Cola Company

-

Danone S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Portland Coffee Roasters has launched its inaugural Original and Nitro Ready-To-Drink canned cold brew. This cold brew is crafted through an extended brewing process, resulting in a smoother, less acidic beverage that's packed with higher caffeine content. The drink boasts notes of dried fruit and chocolate, enhanced by a touch of natural sweetness. Made exclusively with filtered water and 100% specialty grade Arabica coffee, this cold brew is free from additives, sweeteners, and preservatives.

- October 2024: STōK Cold Brew Coffee, a leading name in the multi-serve Ready to Drink coffee segment, has launched STōK Cold Brew Energy. This innovative product merges cold brew coffee with caffeine, ginseng, B-vitamins, and guarana, all packaged in a convenient single-serve format.

- May 2024: Nescafé launched a cold brew coffee concentrate, empowering consumers to craft barista-style iced coffee right at home. This premium liquid coffee concentrate boasts a blend of handpicked coffee varieties, expertly roasted and brewed for a rich, bold flavor.

- March 2024: Pop & Bottle launched a new multi-serve cold brew coffee. This 48-oz organic blend, unsweetened and boasting up to 100 mg of caffeine per serving, comes in light roast, medium roast, and vanilla flavors, and is now available at select Target locations.

Global Cold Brew Coffee Market Report Scope

Cold brew coffee is a beverage made by steeping coarsely ground coffee in cold water for an extended period, typically 12 to 24 hours, resulting in a smooth, refreshing drink. The scope of the report includes form, packaging type, flavor, nature, distribution channel, and geography. Based on the form, the market is segmented into liquid ground and pods. By flavor, the market is segmented into flavored and unflavored. By packaging type, the market is segmented into bottles, cans, bags, and others. By distribution channel, the market is segmented into on-trade and off-trade. The market provides a detailed analysis of the major economies across North America, Europe, Asia-Pacific, South America, the Middle East, and Africa.

| Ground |

| Cold Brew Pods |

| RTD Cold Brew Coffee |

| Others(Liquid concentrates and others) |

| Flavored |

| Unflavored |

| Bottle |

| Can |

| Others(sachets and others) |

| Conventional |

| Organic |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail | |

| Other Off-Trade Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Ground | |

| Cold Brew Pods | ||

| RTD Cold Brew Coffee | ||

| Others(Liquid concentrates and others) | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Packaging Format | Bottle | |

| Can | ||

| Others(sachets and others) | ||

| By Nature | Conventional | |

| Organic | ||

| By Distribution Channel | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Online Retail | ||

| Other Off-Trade Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the cold brew coffee market?

The category is valued at USD 3.79 billion in 2026 and is forecast to reach USD 8.36 billion by 2031, reflecting a 17.12% CAGR.

Which region leads the cold brew coffee market?

North America commanded 40.03% of sector revenue in 2025, supported by extensive RTD infrastructure and consumer familiarity.

Which form segment is growing fastest?

Pods are the fastest-growing form, projected to expand at an 18.33% CAGR between 2026-2031 on the back of single-serve convenience.

Why are cans gaining popularity in cold brew packaging?

Cans offer portability, recyclability, and lower unit costs and are forecast to grow at an 18.81% CAGR through 2031.

Page last updated on: