Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.1 Billion |

| Market Size (2026) | USD 7.56 Billion |

| Market Size (2031) | USD 10.36 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Coffee Creamer Market Analysis by Mordor Intelligence

The US coffee creamer market size was valued at USD 7.1 billion in 2025 and estimated to grow from USD 7.56 billion in 2026 to reach USD 10.36 billion by 2031, at a CAGR of 6.49% during the forecast period (2026-2031). Ongoing demand for at-home coffee customization, format breakthroughs such as canned cold foam, and rising adoption of plant-based formulations continue to push category growth. Manufacturers are channeling capital into new aseptic lines and regional capacity, especially in the Southwest, to shorten supply chains and serve fast-growing metropolitan areas. Clean-label reformulation, driven by new FDA nutrient-content rules, underpins premiumization as labels move toward shorter ingredient decks and lower added sugars. At the same time, e-commerce subscriptions deepen household penetration by automating replenishment and offering a wide flavor catalog to consumers in suburban and rural ZIP codes.

Key Report Takeaways

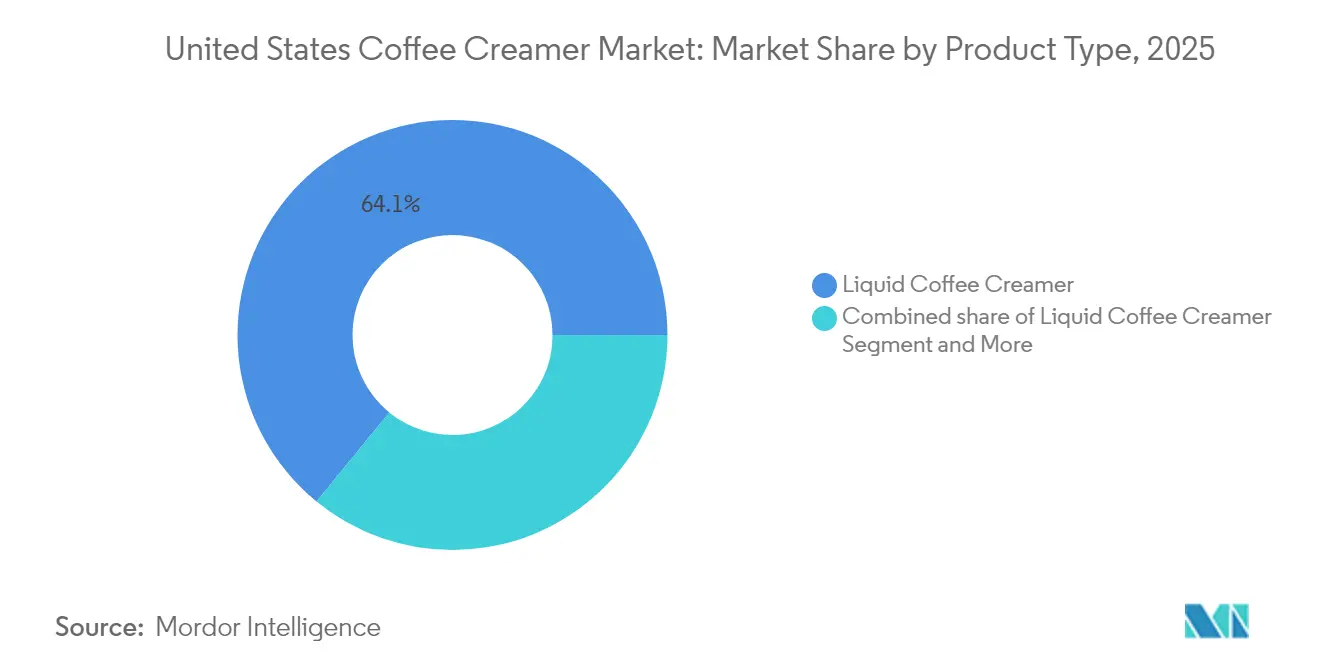

- By product type, liquid coffee creamers led with 64.10% of US coffee creamer market share in 2025. Powder coffee creamers are projected to post the fastest 7.01% CAGR from 2026-2031 within the product-type segmentation.

- By flavor, flavored formats accounted for a 61.05% share of the US coffee creamer market size in 2025, while unflavored products are expected to advance at the quickest 6.63% CAGR through 2031.

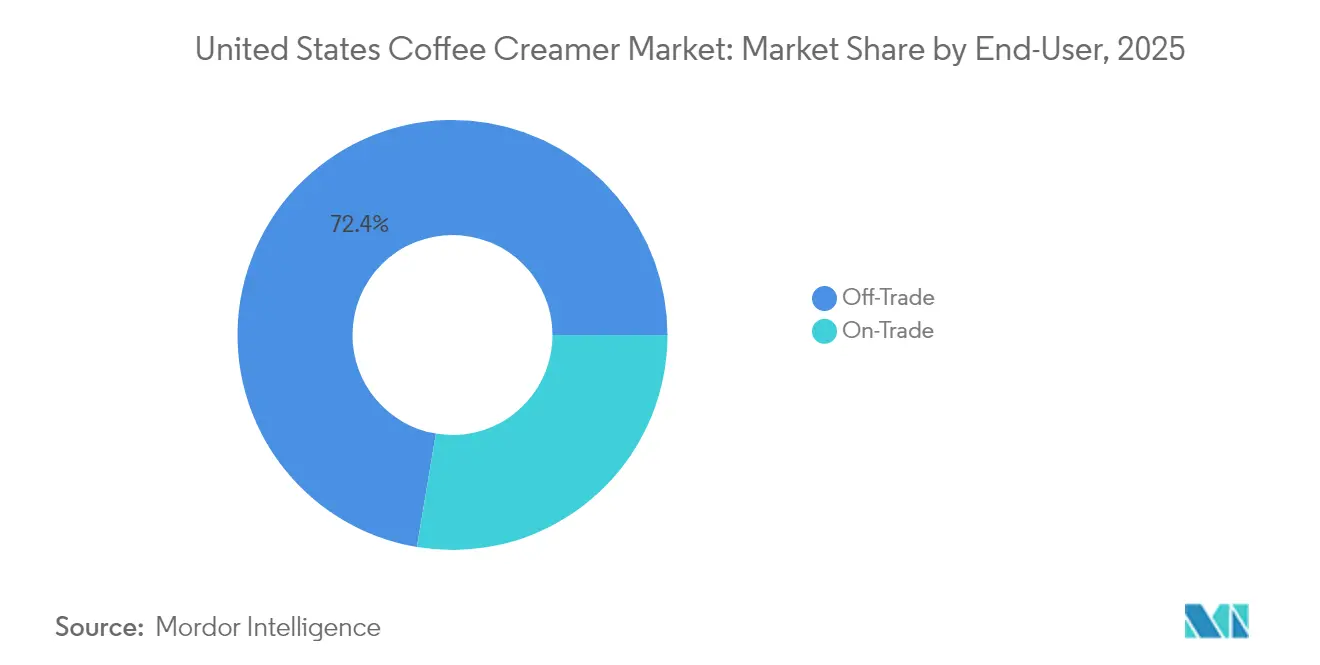

- By end-user, off-trade channels captured 72.35% of the US coffee creamer market size in 2025; on-trade applications are poised to record the highest 6.95% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Coffee Creamer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Flavor and format innovation surge | +1.8% | Global; early gains in major metropolitan areas | Short term (≤ 2 years) |

| Rising clean-label and plant-based demand | +1.5% | National; concentration on West Coast and Northeast | Medium term (2-4 years) |

| E-commerce subscription boom | +1.2% | National; accelerated in suburban and rural markets | Medium term (2-4 years) |

| Cold-foam/RTD coffee pull-through | +1.4% | Urban centers; widening to secondary markets | Short term (≤ 2 years) |

| Southwestern aseptic capacity build-out | +0.9% | Southwest and West; distribution nationwide | Long term (≥ 4 years) |

| Functional keto/MCT trend | +0.7% | National; premium health-conscious demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Flavor and Format Innovation Surge

Richer flavor pipelines and entirely new delivery systems are broadening the US coffee creamer market. Nestlé’s Coffee-mate has partnered with confectionery brands to roll out KIT KAT and seasonal Caramel Apple Crisp variants, while Danone’s International Delight immersed itself in pop-culture tie-ins such as the Home Alone Hot Chocolate Marshmallow launch[1] Nestlé USA, “Coffee-mate Cold Foam Launch Press Release,” nestle-usa.com. The category’s first mass-market cold-foam dispensers dispense a micro-foamed creamer that claims 25% less sugar and 25% more servings per can than standard rivals. Engagement spikes on social media underscore strong resonance with Gen Z; the hashtag #ColdFoam registered more than 321 million TikTok views, indicating that shareable, café-style experiences can be recreated at home. Flavor licensing, limited-time drops, and a convenient canned format collectively accelerate velocity on shelf while cementing the perception of creamers as an affordable indulgence relative to out-of-home espresso beverages.

Rising Clean-Label and Plant-Based Demand

Ingredient transparency now influences brand choice as consumers scrutinize additives such as carrageenan and artificial sweeteners. SPINS panel data shows plant-based creamers as the only dairy-alternative sub-category to register positive value growth in 2023, rising 10% to USD 701 million[2]Prepared Foods, “SPINS 2023 Plant-Based Update,” preparedfoods.com. Oatly’s life-cycle analysis reveals a 44-76% lower climate footprint than cow’s milk, supporting the sustainability narrative embraced by affluent coastal shoppers. Darigold’s Belle series features just five ingredients and no oils, targeting lactose-intolerant households seeking a recognizable ingredient list. FDA’s revised “healthy” icon set for February 2025 forces formulators to cap added sugars and saturated fat, incentivizing investments in natural sweeteners and coconut-oil-free emulsification[3]Federal Register, “Food Labeling; Updated Definition of Healthy,” federalregister.gov. The emphasis on straightforward labels positions plant-based and simplified dairy formulations to capture incremental shelf space, especially in premium refrigerator doors.

E-Commerce Subscription Boom

Direct-to-consumer (DTC) platforms accelerate trial and retention for emerging creamer players. Nutpods began as a Kickstarter campaign and scaled roughly 500% CAGR across two years before lining up conventional retail listings, demonstrating the flywheel effect of online validation. Subscription bundles lower customer acquisition costs because automatic monthly shipments lock in repeat volume and deliver flavor variety without distribution slotting fees. Ratings and reviews on Amazon function as trust badges, often elevating challenger brands to bestseller ranks ahead of incumbents with broader brick-and-mortar presence. Legacy manufacturers are responding with their own DTC microsites and loyalty programs to recapture data-rich relationships initially ceded to marketplaces.

Cold-Foam/RTD Coffee Pull-Through

The ready-to-drink (RTD) coffee segment shapes consumption patterns for adjunct products such as creamers. Refrigerated RTD coffee posted 7% growth to USD 1.2 billion in 2024, while premium cold-brew volumes slid 30% to USD 147 million, signaling a tilt toward convenient multi-serve bottles. Starbucks retained top share at USD 465 million in refrigerated sales, but Stōk’s 28% jump to USD 348 million underscores nimble challenger momentum. Retail cold-foam products echo this convenience trend by letting consumers mimic café froth atop RTD bases at home. Dunkin’s Valentine’s Day-themed cold-foam cans at USD 5.99 fuse seasonal cues with a popular coffeehouse brand, making foam customization a mass phenomenon and offering incremental sales both for RTD coffee and creamers.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sugar & additive health backlash | -1.3% | National; higher impact in health-conscious metros | Medium term (2-4 years) |

| Raw-material cost volatility | -1.1% | Global supply chain; regional manufacturing variations | Short term (≤ 2 years) |

| FDA added-sugar label proposals | -0.8% | Nationwide regulatory compliance | Long term (≥ 4 years) |

| Climate risk on coconut/oat crops | -0.6% | Global sourcing; plant-based segment pricing | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sugar & Additive Health Backlash

Public-health advocates increasingly link added sugars and emulsifiers to chronic disease risk, prompting consumer skepticism toward legacy formulas. Mandatory “added sugar” disclosure on Nutrition Facts panels magnifies visibility of sweetener loads and forces brands to benchmark labels against competitors. Influential cardiology bloggers have spotlighted carrageenan and partially hydrogenated oils, swelling demand for cleaner dairy and plant-based variants. In response, Coffee-mate’s cold foam positions a 25% sugar reduction compared with leading flavored liquids, while Darigold substitutes fillers with real cream and enzyme-based lactose removal. Yet taste expectations limit the pace at which mainstream offerings can slash sugar without risking volume losses, creating a delicate balancing act between health, flavor, and price.

Raw-Material Cost Volatility

Milk, coconut, and oats—all foundational inputs—face fluctuating commodity indices and climate-related disruptions. Texas milk prices fell from USD 23.68 to USD 18.98 per hundredweight between 2022 and 2023, highlighting revenue swings that ripple into creamer margins. Oat futures remain susceptible to Canadian drought cycles, and coconut supply chains face typhoon risks in Southeast Asia, complicating cost forecasting for plant-based SKUs. Investment in domestic manufacturing—over USD 7 billion in announced U.S. dairy processing projects—can offset logistics fees but requires sustained throughput to reach breakeven. Brands with diversified ingredient contracts and hedged positions are better placed to buffer shelf-price inflation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquid Formats Lead Category Evolution

Liquid coffee creamers held 64.10% of US coffee creamer market share in 2025 and are estimated to maintain a 6.55% CAGR to 2031, a trajectory underpinned by consumer preference for ready-to-pour convenience and novelty flavors. Non-dairy liquids reinforce growth by addressing lactose intolerance and vegan preferences, aligning with the broader plant-based narrative already adding USD 701 million in 2023 value. Powder formats remain a fixture in institutional and on-the-go occasions thanks to longer shelf life and portion-controlled packets.

Cold foam, the newest liquid subset, commands a premium ticket at USD 4.68-5.99 per 14-ounce can and is projected to further enlarge the US coffee creamer market size over the forecast horizon. Early sell-through rates indicate a favorable reception among younger households and indulgence-seekers replicating café micro-foam at home. The powder segment responds through dairy-based keto powder launches featuring MCT oils, a nod to functional demand pockets, yet volumes trail liquid counterparts. FDA labeling stipulations for “non-dairy” powders containing sodium caseinate require explicit allergen call-outs, nudging manufacturers toward either full dairy or full plant formulations.

By Flavor: Customization Drives Premium Positioning

Flavored variants captured 61.05% of US coffee creamer market share in 2025 and are predicted to expand at a 6.38% CAGR through 2031. Vanilla and hazelnut remain anchor flavors, but licensed extensions such as KIT KAT and White Lotus tie-ins elevate average price while spurring social-media buzz. Unflavored SKUs fulfill demand among coffee purists and cost-sensitive buyers, yet incremental growth gravitates toward dessert-inspired, seasonal, and zero-sugar flavored lines.

Flavor innovation acts as a direct lever to lift transaction size, since shoppers frequently trade up to 32-ounce bottles for limited drops. Social channels distribute flavor “leaks” that create pre-launch anticipation, a tactic especially effective among Gen Z and millennial audiences. As manufacturers trim artificial colors and sweeteners to comply with forthcoming health-claim criteria, natural flavor houses gain strategic importance for delivering clean-label yet indulgent profiles.

By End-User: Off-Trade Dominance Mirrors Home-Brew Trends

Off-trade venues—including supermarkets, club stores, and e-commerce—accounted for 72.35% of US coffee creamer market size in 2025 and are forecast to post a 6.41% CAGR through 2031. Pandemic-era habits entrenched daily home brewing, while DTC subscriptions lock in monthly re-orders. TreeHouse Foods leverages scale as the world’s largest private-label powder producer, serving retailers intent on price-fighting national brands.

On-trade utilization persists in foodservice, thanks to high-volume kegged creamers and portion-control tubes favored by cafés and offices. Technomic shows 75% of convenience-store patrons purchase regular coffee, making single-serve creamer cups a traffic driver. Office-coffee service also rebounds as hybrid work schedules stabilize, though overall share remains below pre-2020 levels. Regulatory calorie-disclosure rules for vending machines compel clear front-label calorie display, nudging operators to stock lower-sugar options as a compliance safeguard.

Geography Analysis

Regional dynamics shape the coffee landscape, influenced by demographic clusters, supply-chain footprints, and local coffee cultures. After launching a USD 675 million plant in Arizona, Nestlé bolsters the Southwest's status as a manufacturing hub. This facility is set to distribute Coffee-mate, Natural Bliss, and Starbucks creamers across the nation. By deploying aseptic lines, the company not only reduces freight costs to West Coast retail distribution centers but also mitigates challenges posed by limited cross-country refrigerated trucking capacities. On the West Coast, a dense population of flexitarian consumers, coupled with a network of specialty grocers promoting climate-friendly products, drives plant-based adoption beyond national averages. Oatly’s climate-footprint labeling strategy finds a receptive audience in California and Washington, propelling plant-based sales ahead of dairy alternatives. Meanwhile, the Northeast, with its affluent urban corridors from Boston to New York, leans towards premium and artisanal creamers, bolstered by a culture of boutique roasters.

While Midwestern and Southeastern states traditionally favor dairy and value pricing, there's a notable surge in e-commerce adoption in suburban areas, especially where grocery selections might miss niche flavors. Texas, pouring over USD 7 billion into dairy processing projects, is becoming a key player, supplying both fluid milk and whey derivatives. This bolsters regional sourcing for hybrid dairy-plant blends. Nationwide, retailers are standardizing flavor offerings in their planograms, diminishing historical regional differences in shelf sets. However, they still roll out holiday exclusives selectively, testing localized demand.

Competitive Landscape

Regional dynamics shape the coffee landscape, influenced by demographic clusters, supply-chain footprints, and local coffee cultures. After launching a USD 675 million plant in Arizona, Nestlé bolsters the Southwest's status as a manufacturing hub. This facility is set to distribute Coffee-mate, Natural Bliss, and Starbucks creamers across the nation. By deploying aseptic lines, the company not only reduces freight costs to West Coast retail distribution centers but also mitigates challenges posed by limited cross-country refrigerated trucking capacities. On the West Coast, a dense population of flexitarian consumers, coupled with a network of specialty grocers promoting climate-friendly products, drives plant-based adoption beyond national averages. Oatly’s climate-footprint labeling strategy finds a receptive audience in California and Washington, propelling plant-based sales ahead of dairy alternatives. Meanwhile, the Northeast, with its affluent urban corridors from Boston to New York, leans towards premium and artisanal creamers, bolstered by a culture of boutique roasters.

While Midwestern and Southeastern states traditionally favor dairy and value pricing, there's a notable surge in e-commerce adoption in suburban areas, especially where grocery selections might miss niche flavors. Texas, pouring over USD 7 billion into dairy processing projects, is becoming a key player, supplying both fluid milk and whey derivatives. This bolsters regional sourcing for hybrid dairy-plant blends. Nationwide, retailers are standardizing flavor offerings in their planograms, diminishing historical regional differences in shelf sets. However, they still roll out holiday exclusives selectively, testing localized demand.

United States Coffee Creamer Industry Leaders

Heartland Food Products Group

Nestlé S.A

Danone S.A

TreeHouse Foods Inc.

Califia Farms LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Coffee Mate is launching two limited-edition Harry Potter-inspired creamers, the Toffee Cauldron Cake Flavored Creamer and the Zero Sugar White Chocolate Peppermint Toad Flavored Creamer, both modeled after treats from the Hogwarts sweet shop Honeydukes.

- February 2024: Danone North America, through its brand Dunkin, launched a new coffee creamer named "Dunkin Brownie Batter Creamer." As per the brand’s claim, the new product has been made with real cream and real sugar and would help bring nostalgic sweetness to the coffee.

- January 2024: Nestle, as part of expanding its portfolio, entered a partnership with Kellanova Waffles’ brand, Eggo. Through this partnership, Nestle launched breakfast-inspired coffee creamers under the Coffee Mate and Eggo brands.

United States Coffee Creamer Market Report Scope

A coffee creamer is a store-bought powder or liquid that is commonly added to coffee or black tea in place of a milk product like half-and-half or cream. The US coffee creamer market is segmented by product type and distribution channel. By product type, the market is segmented into powder coffee creamer and liquid coffee creamer. Based on distribution channels, the market is segmented into supermarkets/hypermarkets, convenience stores, online channels, and other retail channels. The market sizing has been done in value terms (USD) for all the abovementioned segments.

By Product Type

| Powder Coffee Creamer | Dairy-based Powder |

| Non-dairy Powder | |

| Liquid Coffee Creamer | Dairy-based Liquid |

| Non-dairy Liquid |

By Flavor

| Unflavored | |

| Flavored | Vanilla |

| Hazelnut | |

| Caramel | |

| Chococlate | |

| Others |

By End-User

| On-trade | |

| Off-Trade | Supermarkets / Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Others |

| By Product Type | Powder Coffee Creamer | Dairy-based Powder |

| Non-dairy Powder | ||

| Liquid Coffee Creamer | Dairy-based Liquid | |

| Non-dairy Liquid | ||

| By Flavor | Unflavored | |

| Flavored | Vanilla | |

| Hazelnut | ||

| Caramel | ||

| Chococlate | ||

| Others | ||

| By End-User | On-trade | |

| Off-Trade | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Others | ||

Key Questions Answered in the Report

What is the current value of the US coffee creamer market?

The market is valued at USD 7.56 billion in 2026.

How fast is the category growing?

It is forecast to post a 6.49% CAGR through 2031.

Which product format holds the largest share?

Liquid creamers lead with 64.10% share in 2025.

Why are plant-based creamers gaining traction?

Clean-label demands and lower climate footprints push plant-based dollar sales up 10% to USD 701 million in 2023.

Page last updated on: