U.S. Specialty Coffee Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

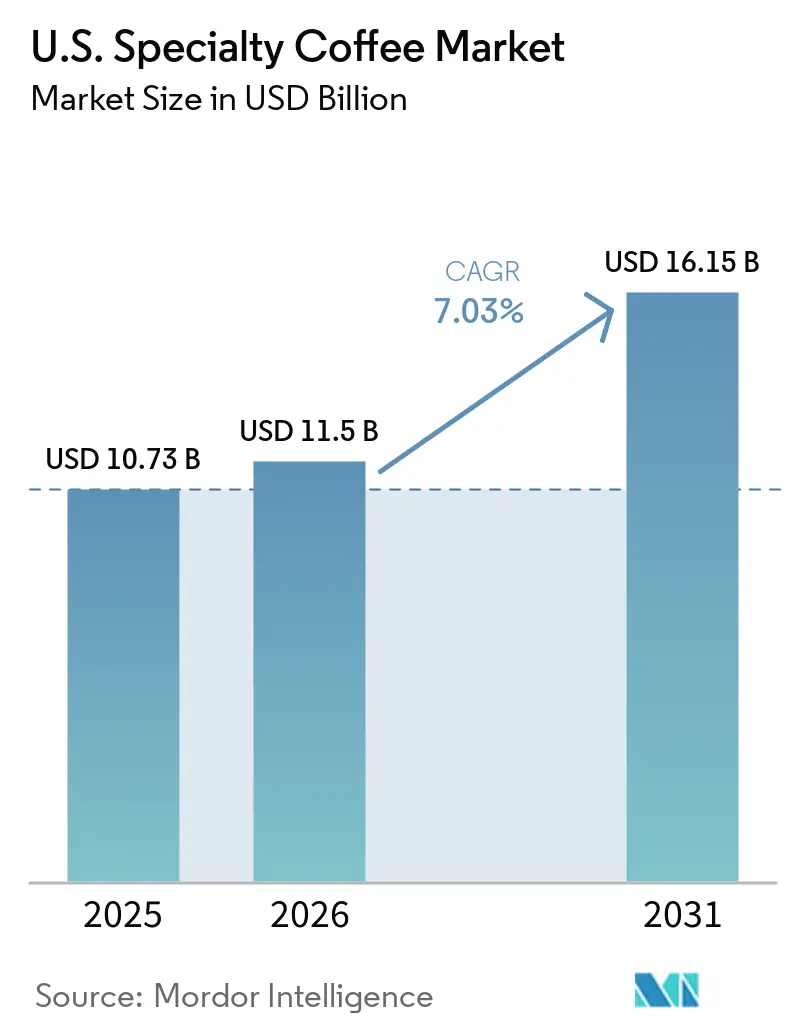

| Base Year Market Size (2025) | USD 10.73 Billion |

| Market Size (2026) | USD 11.5 Billion |

| Market Size (2031) | USD 16.15 Billion |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

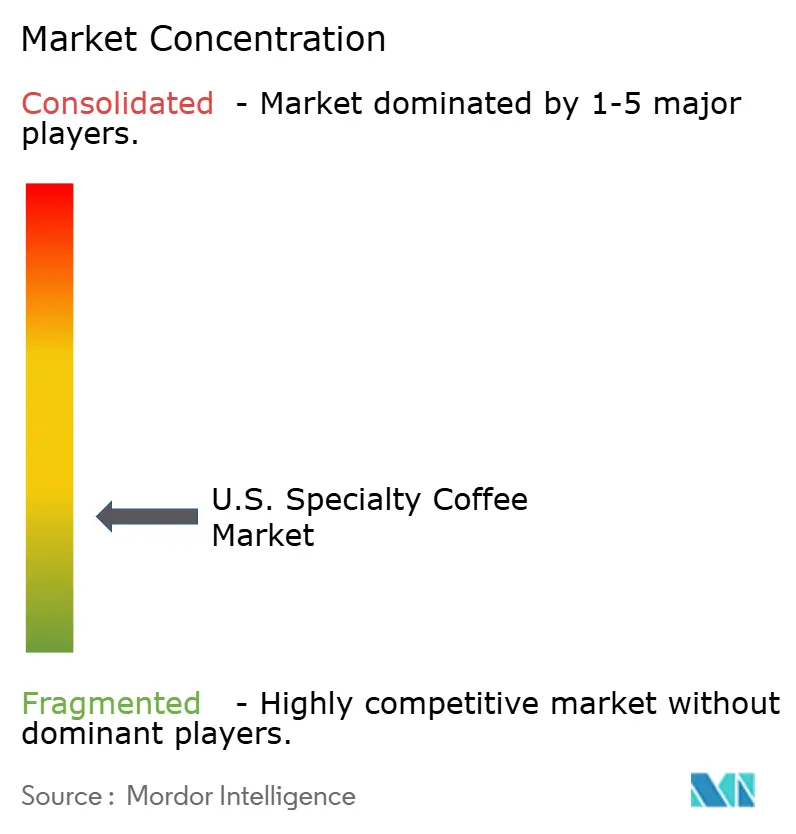

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

U.S. Specialty Coffee Market Analysis by Mordor Intelligence

The U.S. specialty coffee market was valued at USD 10.73 billion in 2025. The market is projected to grow from USD 11.50 billion in 2026 to USD 16.15 billion by 2031, at a CAGR of 7.03% over the period 2026-2031. The market is growing through sustained consumer interest in premium beverage experiences, even as other discretionary spending categories face pressure from tightening household budgets. A key structural driver of this growth is a generational shift in consumption habits. According to the National Coffee Association (NCA), Americans increasingly view specialty coffee as a daily ritual rather than an occasional indulgence, making demand relatively resilient to macroeconomic challenges. In 2025, 47% of American adults consumed specialty coffee in a single day, maintaining a record-high level and surpassing traditional coffee consumption (42%) for the third consecutive year [1]Source: National Coffee Association, "NCA Newsroom", ncausa.org. This trend is further supported by consumers' growing preference for quality, transparency into origin, and personalized beverage experiences, attributes closely associated with specialty coffee. The expansion of premium coffeehouse chains, independent roasters, and direct-to-consumer subscription models has also enhanced accessibility to specialty coffee products nationwide. As specialty coffee becomes an integral part of daily consumption habits, the category is expected to continue gaining share in the broader U.S. coffee market.

Key Report Takeaways

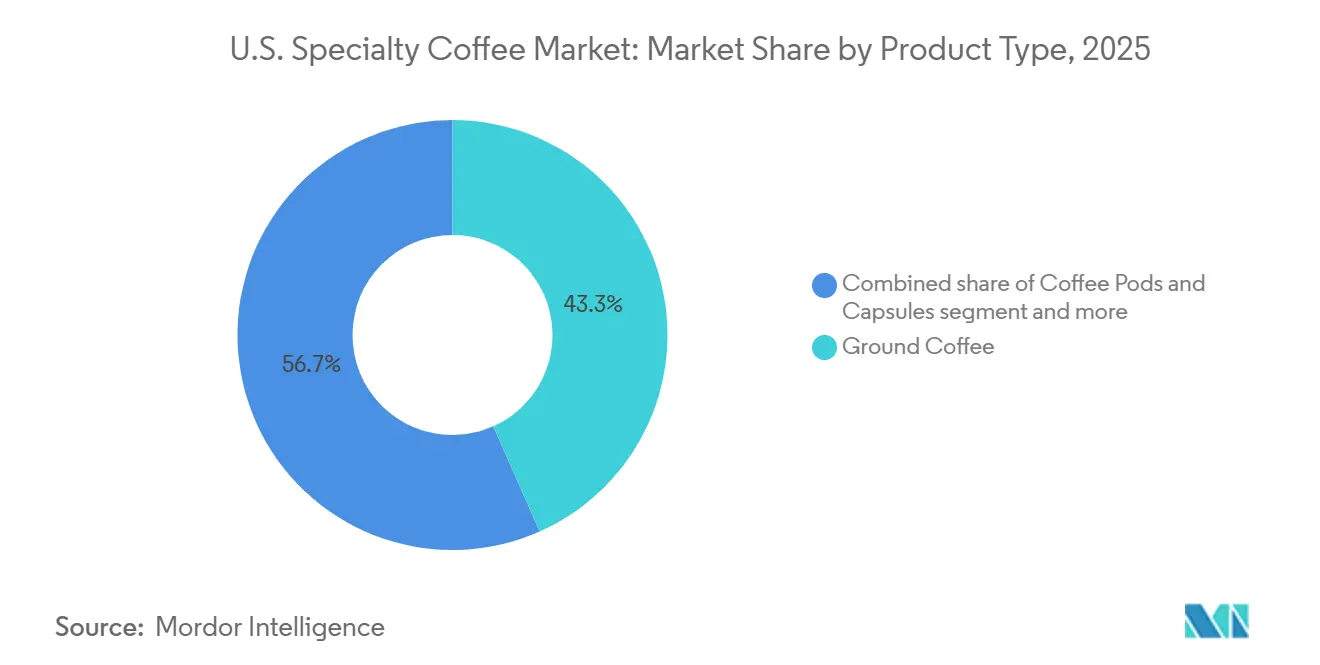

- By product type, ground coffee captured 43.34% of the 2025 market, while coffee pods and capsules are advancing at a 7.59% CAGR through 2031.

- By roast profile medium retained a 30.19% share of the U.S specialty coffee market size in 2025, while the dark segment is forecast to grow at a 7.83% CAGR through 2031.

- By category, conventional commanded 60.76% of demand in 2025, whereas organic is expanding fastest at 8.01% CAGR between 2026-2031.

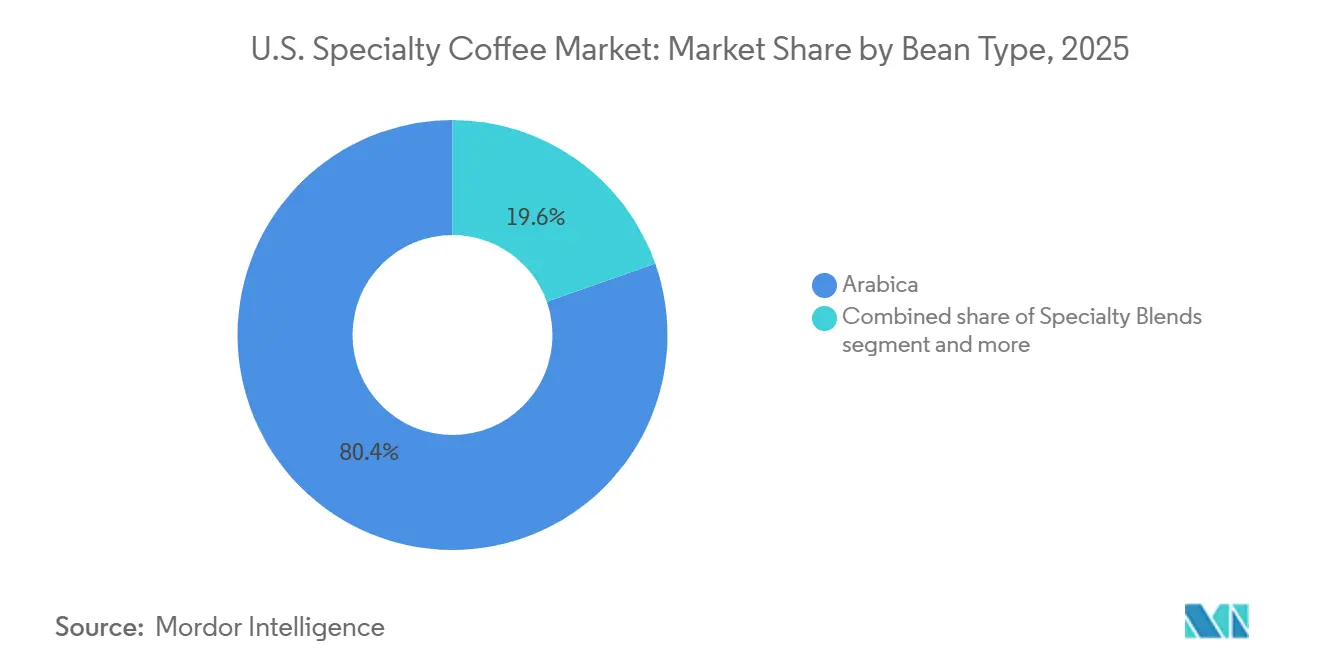

- By bean type, arabica accounted for 80.40% of 2025 revenue, while specialty blends is the fastest-growing segment, with a 8.21% CAGR through 2031.

- By end user, on-trade commanded 67.11% of demand in 2025, whereas off-trade is expanding fastest at 7.96% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Specialty Coffee Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer premiumization across food and beverage spending | +1.8% | National; highest concentration in Northeast and West Coast metros; accelerating in secondary Southern cities | Medium term (2–4 years) |

| Growth of third-wave coffee culture | +1.3% | National, with deepest penetration on the Pacific Coast and in New York metro; expanding into Midwestern cities | Long term (≥ 4 years) |

| Growth of specialty coffee subscription and DTC models | +1.1% | National; e-commerce-driven, with strongest incremental reach in suburban and non-metro areas underserved by local roasters | Medium term (2–4 years) |

| Health, wellness, and functional positioning of coffee | +1.2% | National; concentrated among Gen Z and Millennial segments across all metro categories | Medium term (2–4 years) |

| Rising preference for cold brew, nitro, and RTD specialty formats | +1.4% | National; accelerated in Southeast and Southwest warm-weather markets and convenience-dense corridors | Short term (≤ 2 years) |

| Rapid expansion of premium café and branded coffee chains | +0.9% | National; growth concentrated in underserved Midwestern and Southern secondary cities with limited legacy specialty café infrastructure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising consumer premiumization across food and beverage spending

Premiumization has become a significant growth driver for the U.S. specialty coffee market, as consumers increasingly value quality, craftsmanship, and unique consumption experiences over price-focused purchasing decisions. This trend directly benefits specialty coffee, with consumers demonstrating a higher willingness to pay for single-origin beans, artisanal roasting techniques, traceable sourcing, and customized beverages. Coffee has transitioned into an affordable luxury, offering premium experiences at a relatively low cost compared to other discretionary purchases. This spending pattern is particularly prominent among affluent consumer groups, whose purchasing power supports demand for high-end food and beverage products. As of January 2026, the United States had approximately 935 billionaires [2]Source: Americans For Tax Fairness Organization, "U.S. BILLIONAIRES GOT $1.5 TRILLION RICHER IN TRUMP’S FIRST YEAR", americansfortaxfairness.org. The growing affluent population, combined with a rising preference for premium and experience-driven consumption, continues to drive demand for specialty coffee products, premium café offerings, and high-quality at-home brewing solutions.

Growth of third-wave coffee culture

The growth of third-wave coffee culture is a significant factor driving the U.S. specialty coffee market. This trend has shifted coffee consumption from a routine purchase to an experience focused on quality, craftsmanship, and origin. Consumers are showing increased interest in the provenance of coffee beans, roasting techniques, brewing methods, and sustainability practices, which has enhanced the appreciation for specialty-grade coffee. This has led to rising demand for single-origin coffees, micro-lot offerings, artisanal roasting, and manual brewing methods such as pour-over and cold brew. Independent specialty cafés and premium coffee roasters have played a key role in educating consumers about coffee quality, encouraging a shift from conventional coffee products. As consumers become more knowledgeable and engaged in the coffee-making process, third-wave coffee culture continues to drive demand for premium specialty coffee in both café and at-home consumption settings.

Growth of specialty coffee subscription and DTC models

The growth of specialty coffee subscription services and direct-to-consumer (DTC) sales channels is driving the expansion of the U.S. specialty coffee market. These models provide consumers with access to freshly roasted, high-quality coffee delivered directly to their homes, offering enhanced variety, convenience, and personalization compared to traditional retail options. Subscription services allow customers to explore single-origin coffees, limited-edition roasts, and tailored flavor profiles, promoting stronger brand loyalty and repeat purchases. Simultaneously, DTC channels enable specialty coffee roasters to establish direct connections with consumers, enhance customer engagement, and extend their reach beyond regional markets. With the increasing popularity of online shopping and at-home coffee consumption, subscription and DTC models are becoming key drivers for boosting specialty coffee adoption and consumption frequency across the United States.

Health, wellness, and functional positioning of coffee

The perception of coffee as a functional beverage is driving demand in the U.S. specialty coffee market. Consumers are increasingly associating premium coffee with energy, wellness, and cognitive benefits, owing to its natural antioxidants and its role in enhancing focus and productivity. Specialty coffee brands are responding to this trend by offering products that highlight clean ingredients, low sugar content, organic certifications, and functional additions such as adaptogens, mushrooms, collagen, and protein. As health-conscious consumers prioritize beverages that combine enjoyment with wellness benefits, specialty coffee is being positioned as a premium functional drink, contributing to growth across retail and foodservice channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns about excessive caffeine consumption are limiting market growth | -0.5% | National; most pronounced among older consumer segments and parents of young adults; influencing labeling and portion strategies | Short term (≤ 2 years) |

| Arabica price volatility and margin compression | -0.8% | National; disproportionately affecting independent roasters and small-format café operators with limited hedging capacity | Medium term (2–4 years) |

| Substitution pressure from energy drinks and functional beverages | -0.5% | National; most acute in convenience and quick-service channels serving 18-to-24-year-old consumers | Medium term (2–4 years) |

| Supply chain disruptions and freight cost inflation | -0.4% | National; import-dependent roasters most exposed; sharpest impact on importers from Vietnam, Ethiopia, and Central America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health concerns about excessive caffeine consumption are limiting market growth.

Increasing awareness of the health risks associated with excessive caffeine consumption poses a challenge for the U.S. specialty coffee market. Although specialty coffee remains popular, some consumers are reducing their intake due to concerns about anxiety, sleep disturbances, elevated heart rates, and caffeine dependency. This trend is particularly significant as specialty coffee beverages often have higher caffeine content and larger serving sizes compared to traditional coffee products. Regulatory and health organizations, such as the U.S. Food and Drug Administration (FDA), highlight the importance of responsible caffeine consumption, noting that rapid intake of approximately 1,200 milligrams of caffeine can lead to toxic effects, including seizures [3]Source: Food and Drug Administration, "Spilling the Beans: How Much Caffeine is Too Much?", fda.gov. As health-conscious consumers increasingly monitor their stimulant intake, concerns about excessive caffeine consumption may reduce consumption frequency among specific demographic groups and drive demand for decaffeinated or lower-caffeine options.

Arabica price volatility and margin compression

Volatility in Arabica coffee prices poses a significant challenge for the U.S. specialty coffee market, as specialty roasters and coffeehouse operators rely heavily on high-quality Arabica beans. Factors such as weather disruptions, crop diseases, supply constraints in key producing countries, and fluctuations in global coffee futures markets can lead to rapid increases in green coffee procurement costs. Specialty coffee businesses often struggle to fully pass these cost increases on to consumers, particularly in competitive café and retail environments, resulting in margin compression. This impact is more severe for independent roasters and smaller specialty chains, which lack the purchasing scale, hedging capabilities, and supply diversification of larger operators. Consequently, prolonged Arabica price volatility can reduce profitability, hinder expansion plans, and intensify pricing pressures throughout the U.S. specialty coffee value chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ground Coffee Anchors Volume While Pods Lead Growth

Ground coffee held a dominant 43.34% share of the U.S. specialty coffee market in 2025, driven by strong consumer preference for freshly brewed coffee and greater control over brewing methods. Specialty coffee consumers increasingly choose ground coffee due to its compatibility with popular brewing techniques such as pour-over, French press, drip brewing, and cold brew preparation. This segment also benefits from the growing at-home coffee culture, where consumers aim to replicate café-quality experiences while maintaining flexibility in bean selection, grind size, and brewing customization. Furthermore, specialty roasters are expanding their portfolios with single-origin and premium ground coffee offerings, reinforcing the segment's leading position.

Coffee pods and capsules are expected to be the fastest-growing product type, with a projected CAGR of 7.59% during 2026–2031. This growth is fueled by increasing demand for convenience without compromising coffee quality, particularly among busy professionals and younger consumers. Specialty coffee brands are introducing premium pod formats featuring single-origin, organic, and sustainably sourced coffees, elevating the category beyond traditional convenience-focused offerings. Advances in pod technology, broader compatibility with single-serve brewing systems, and the expansion of direct-to-consumer subscription models are further driving adoption, positioning coffee pods and capsules as a significant growth driver within the U.S. specialty coffee market.

By Roast Profile: Medium Holds Mainstream; Dark Gathers Momentum

In 2025, medium roast accounted for the largest share of the U.S. specialty coffee market at 30.19%, driven by its balanced flavor profile that retains the bean's origin characteristics while offering a smooth body and moderate acidity. It remains the preferred choice among specialty coffee consumers due to its optimal balance between the bright, nuanced flavors of light roasts and the richer notes of darker roasts. Specialty roasters also favor medium roasts for highlighting single-origin coffees and premium blends, contributing to its widespread popularity across both retail and coffeehouse channels.

Dark roast is anticipated to be the fastest-growing roast profile, with a projected CAGR of 7.83% during 2026–2031. This growth is supported by increasing consumer demand for bold, full-bodied flavor profiles and the rising popularity of espresso-based beverages. Dark roasts are becoming more popular among consumers seeking stronger taste intensity and lower perceived acidity, particularly in specialty café settings. Additionally, the growing demand for premium espresso blends, cold brew concentrates, and specialty coffee beverages with robust flavor characteristics is expected to further drive growth in the dark roast segment.

By Category: Conventional Commands Share as Organic Accelerates Fastest

Conventional specialty coffee held the largest share of the U.S. specialty coffee market, accounting for 60.76% in 2025. This dominance is attributed to its widespread availability, established supply chains, and relatively lower price points compared to certified organic alternatives. Conventional specialty coffee allows roasters and retailers to provide premium-quality products while ensuring accessibility to a broader consumer base. Additionally, the segment benefits from the abundant supply of specialty-grade Arabica beans sourced from key coffee-producing regions, enabling manufacturers to meet increasing demand across retail and foodservice channels.

Organic specialty coffee is projected to be the fastest-growing category, with a CAGR of 8.01% during 2026–2031. This growth is driven by increasing consumer interest in sustainably produced and chemical-free food and beverage products. Health-conscious consumers are gravitating toward organic coffee due to its perceived higher quality, environmental sustainability, and cleaner production methods. Moreover, specialty coffee roasters are expanding their organic product offerings and focusing on traceability and certification claims, which is expected to boost adoption and drive robust growth in the organic segment.

By Bean Type: Arabica Commands Scale While Specialty Blends Signal Innovation Depth

Arabica accounted for an 80.40% share of the U.S. specialty coffee market in 2025, underscoring its status as the preferred bean type for premium coffee products. This dominance is attributed to its superior flavor complexity, aromatic profile, and smoother taste. Specialty coffee roasters primarily use Arabica beans due to their nuanced flavor notes, higher perceived quality, and suitability for single-origin and premium offerings. The segment's strong position is further reinforced by consumer preference for high-quality coffee experiences and the extensive use of Arabica beans in specialty cafés, retail products, and direct-to-consumer channels.

Specialty blends are anticipated to be the fastest-growing bean type, with a projected CAGR of 8.21% during 2026–2031. This growth is driven by rising consumer demand for unique and consistent flavor profiles that combine characteristics of beans from multiple origins. Specialty coffee roasters are increasingly creating proprietary blends to diversify their product portfolios, enhance flavor customization, and meet varied consumer preferences. Furthermore, specialty blends offer greater flexibility in managing supply fluctuations while ensuring product consistency, contributing to their expanding adoption in both retail and foodservice segments

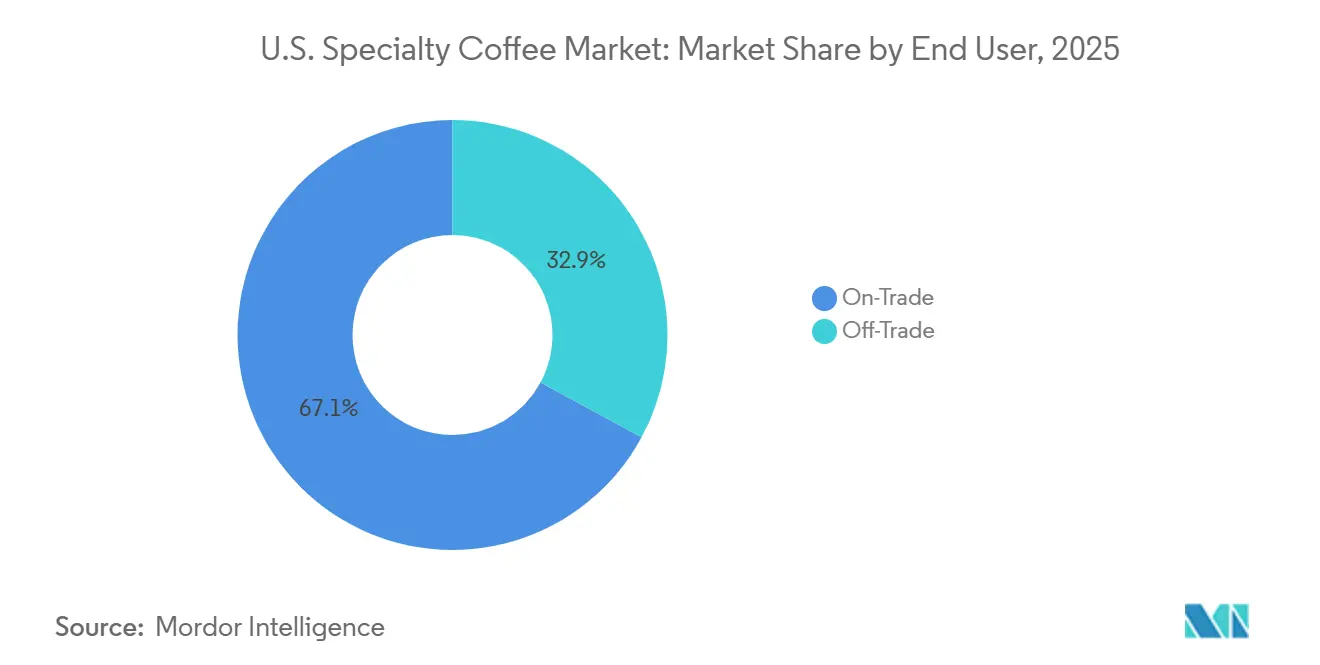

By End User: On-Trade Scale Coexists With Off-Trade's Growth Velocity

On-trade accounted for the largest share of the U.S. specialty coffee market at 67.11% in 2025, driven by the strong presence of specialty coffeehouses, cafés, restaurants, and premium foodservice establishments. Specialty coffee consumption remains highly experience-oriented, with consumers valuing barista craftsmanship, beverage customization, and the social atmosphere provided by coffee shops. The continued expansion of specialty café chains and independent roasters, along with growing demand for premium espresso-based beverages, has reinforced the dominance of the on-trade channel across the U.S. market.

Off-trade is projected to be the fastest-growing end-user segment, expanding at a CAGR of 7.96% during 2026–2031. This growth is driven by increasing at-home consumption of specialty coffee, supported by the rising adoption of premium brewing equipment, coffee subscriptions, and e-commerce platforms. Consumers are increasingly seeking café-quality experiences at home through specialty beans, ground coffee, pods, and ready-to-drink formats. Furthermore, the expansion of direct-to-consumer sales channels and broader retail availability of specialty coffee products is expected to accelerate growth in the off-trade segment over the forecast period.

Geography Analysis

The geographic demand profile of the U.S. specialty coffee market aligns with the country's demographic and urbanization patterns, showing notable performance differences between coastal and interior markets. These gaps are expected to narrow during the forecast period. The market is currently in a phase of premiumization depth, where consumer acquisition is largely complete. The competitive focus has shifted to format innovation, extending premium price tiers, and capturing a greater share of direct-to-consumer (DTC) subscriptions. Starbucks' prioritization of the Midwest and South for U.S. expansion, supported by a new Nashville support center and plans for up to 5,000 additional locations, serves as both a commercial signal and an industry catalyst. Historically, the entry of national chains has accelerated consumer trials and increased category awareness in underserved regional markets.

The Southeast and South are emerging as the fastest-growing regions for specialty coffee in the U.S. This growth is driven by demographic in-migration, rising household incomes in secondary cities, and the expansion of drive-through premium café formats, which cater to car-centric consumption patterns.Hispanic populations in the Northeast and West Coast also show a 67% past-week penetration rate, reinforcing that ethnicity is a more reliable predictor of specialty coffee demand than age or income alone. This insight suggests that geographic investment strategies should focus on community-specific brand-building initiatives rather than relying solely on broad metro-level demographic indicators.

Hispanic Americans exhibit the highest specialty coffee consumption rate among all ethnic groups in the U.S., with a 67% past-week penetration rate in 2026. Their geographic concentration in states like California, Texas, and Florida contributes to a disproportionate demand intensity in these regions. These states are already significant specialty coffee markets but still have per-capita growth potential compared to Northeastern benchmarks. Additionally, regions with rapidly growing South Asian and East Asian populations, such as the Texas Triangle, Northern New Jersey, and the San Francisco Bay Area, are increasingly served by café formats that combine specialty coffee quality with culturally specific flavor profiles. This trend is driving hyper-local product segmentation within the off-trade retail channel.

Competitive Landscape

The U.S. specialty coffee market is highly fragmented, with competition spread across multinational coffee chains, regional specialty roasters, independent coffeehouses, and direct-to-consumer brands. Market participants focus less on price competition and more on product differentiation, emphasizing single-origin sourcing, artisanal roasting methods, sustainability initiatives, and direct-trade relationships to achieve premium positioning. Brand authenticity and transparent communication of coffee origins have become critical competitive advantages as consumers increasingly prioritize high-quality and ethically sourced coffee.

Competition is shifting toward omnichannel engagement, with leading companies expanding beyond traditional café formats into e-commerce, subscription services, ready-to-drink products, and retail packaged coffee. Significant investments are being made in customer retention strategies, loyalty programs, and personalized product offerings to build recurring revenue streams. As specialty coffee consumption grows in at-home settings, businesses with robust distribution networks and diversified sales channels are gaining a competitive edge.

Technology adoption is becoming a key differentiator in the competitive landscape, particularly for specialty coffee brands with direct-to-consumer models. Tools such as advanced analytics, AI-driven recommendation engines, and flavor-preference profiling are being utilized to personalize product offerings, enhance customer retention, and optimize subscription models. Additionally, digital ordering platforms, mobile applications, and data-driven marketing strategies are helping companies strengthen consumer engagement, lower acquisition costs, and improve long-term customer value.

U.S. Specialty Coffee Industry Leaders

-

Starbucks Coffee Company

-

Keurig Dr Pepper Inc.

-

Blue Bottle Coffee, Inc.

-

Stumptown Coffee Roasters

-

Counter Culture Coffee

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Diamond Brew announced the successful completion of an oversubscribed seven-figure pre-seed funding round aimed at supporting the expansion of its innovative brewless coffee platform. The company plans to use the investment to scale production, accelerate product development, expand retail distribution, and strengthen its direct-to-consumer presence. Diamond Brew's flagship brewless coffee pod utilizes proprietary flash-freezing technology to deliver specialty coffee flavors that dissolve instantly in hot or cold water, eliminating the need for traditional brewing equipment.

- June 2026: Lavazza has accelerated its North American growth strategy with the launch of Tablì, a new single-serve coffee system featuring proprietary tabs made entirely from 100% compressed coffee, without plastic capsules, coatings, or individual wrapping. Tablì, positioned as the company's most ambitious product innovation, combines a dedicated brewing machine with ready-to-use coffee tabs designed to deliver café-quality espresso while prioritizing convenience and sustainability. Developed over five years of research and development and supported by more than 15 patents, this launch underscores Lavazza's commitment to expanding its presence in the North American premium coffee market through innovative at-home coffee solutions and differentiated single-serve formats.

- March 2026: Keurig Dr Pepper announced a definitive agreement to acquire JDE Peet’s in an all-cash transaction valued at approximately EUR 15.7 billion (around USD 18 billion). This acquisition will create one of the world's largest coffee businesses. Following the transaction, the company plans to separate into two independent publicly traded entities: a North America-focused beverage company and a dedicated global coffee company. The combined coffee business will integrate leading brands such as Keurig, Peet’s Coffee, Jacobs, L’OR, and Douwe Egberts, establishing a coffee platform with operations in over 100 countries and approximately USD 16 billion in annual sales.

U.S. Specialty Coffee Market Report Scope

| Whole Bean Coffee |

| Ground Coffee |

| Coffee Pods and Capsules |

| Ready-to-Drink (RTD) Specialty Coffee |

| Others |

| Light |

| Medium |

| Dark |

| Conventional |

| Organic |

| Arabica |

| Robusta |

| Specialty Blends |

| On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

| By Product Type | Whole Bean Coffee | |

| Ground Coffee | ||

| Coffee Pods and Capsules | ||

| Ready-to-Drink (RTD) Specialty Coffee | ||

| Others | ||

| By Roast Profile | Light | |

| Medium | ||

| Dark | ||

| By Category | Conventional | |

| Organic | ||

| By Bean Type | Arabica | |

| Robusta | ||

| Specialty Blends | ||

| By End User | On-Trade | |

| Off-Trade | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

Key Questions Answered in the Report

What is the size of the U.S. specialty coffee market in 2026?

The U.S. specialty coffee reached USD 11.50 billion in 2026.

What is the projected CAGR of the U.S. specialty coffee market during 2026–2031?

The market is expected to grow at a CAGR of 7.03% from 2026 to 2031.

Which product type held the largest share of the U.S. specialty coffee market in 2025?

Ground coffee led the market with a 43.34% share in 2025.

Which segment is expected to grow the fastest in the U.S. specialty coffee market?

Specialty blends are projected to be the fastest-growing segment, with a CAGR of 8.21% during 2026–2031.

Page last updated on: