Cafe And Bars Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

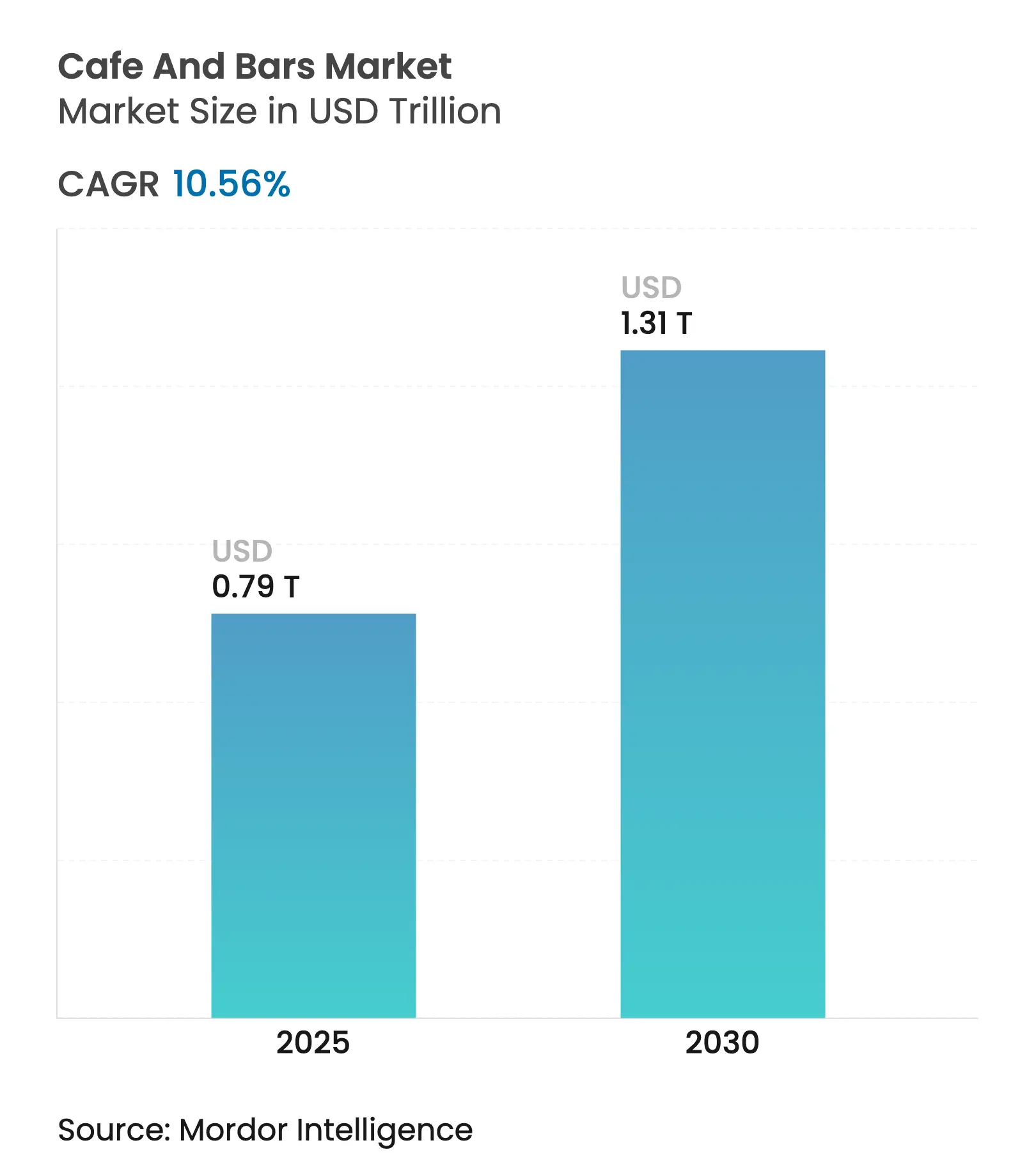

| Market Size (2025) | USD 0.79 Trillion |

| Market Size (2030) | USD 1.31 Trillion |

| Growth Rate (2025 - 2030) | 10.56 % CAGR |

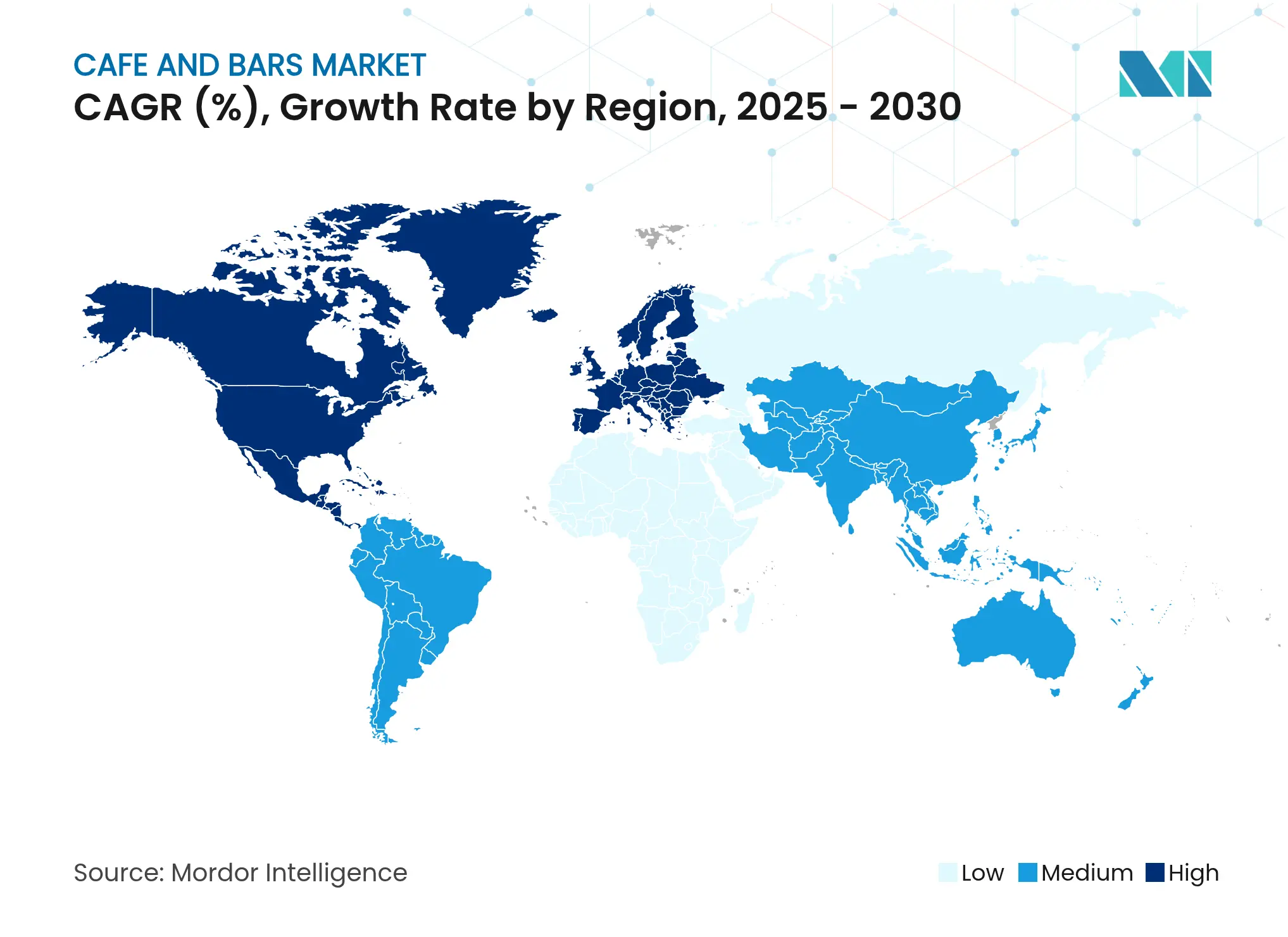

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Cafe And Bars Market Analysis by Mordor Intelligence

In 2025, the cafe and bars market was valued at USD 793.34 billion. By 2030, it's set to soar to an estimated USD 1,310.30 billion, marking a robust CAGR of 10.56%. Urbanization is reshaping neighborhood venues into vital "third places," fostering social interactions and accommodating remote work. These venues adeptly balance their roles as quick-service outlets and immersive social hubs, ensuring steady demand. In emerging regions, rising disposable incomes, coupled with expanding delivery platforms and a growing penchant for premium specialty beverages, are broadening the consumer base. Simultaneously, an uptick in the number of establishments bolsters market growth. Data from the e-Stat Portal, Japan's Official Statistics Organization, reveals that as of March 2024, Japan boasted around 47.53 thousand licensed coffee shops[1]Source: e-Stat Portal, Japan's Official Statistics Organization, "Report on public health administration - food hygiene FY 2023", www.e-stat.go.jp. To enhance convenience and personalization, operators are increasingly turning to digital loyalty programs, AI-driven product testing, and autonomous brewing stations. Moreover, regulatory pushes for greener operations, emphasizing waste reduction and energy efficiency, are influencing capital spending priorities in the market.

Key Report Takeaways

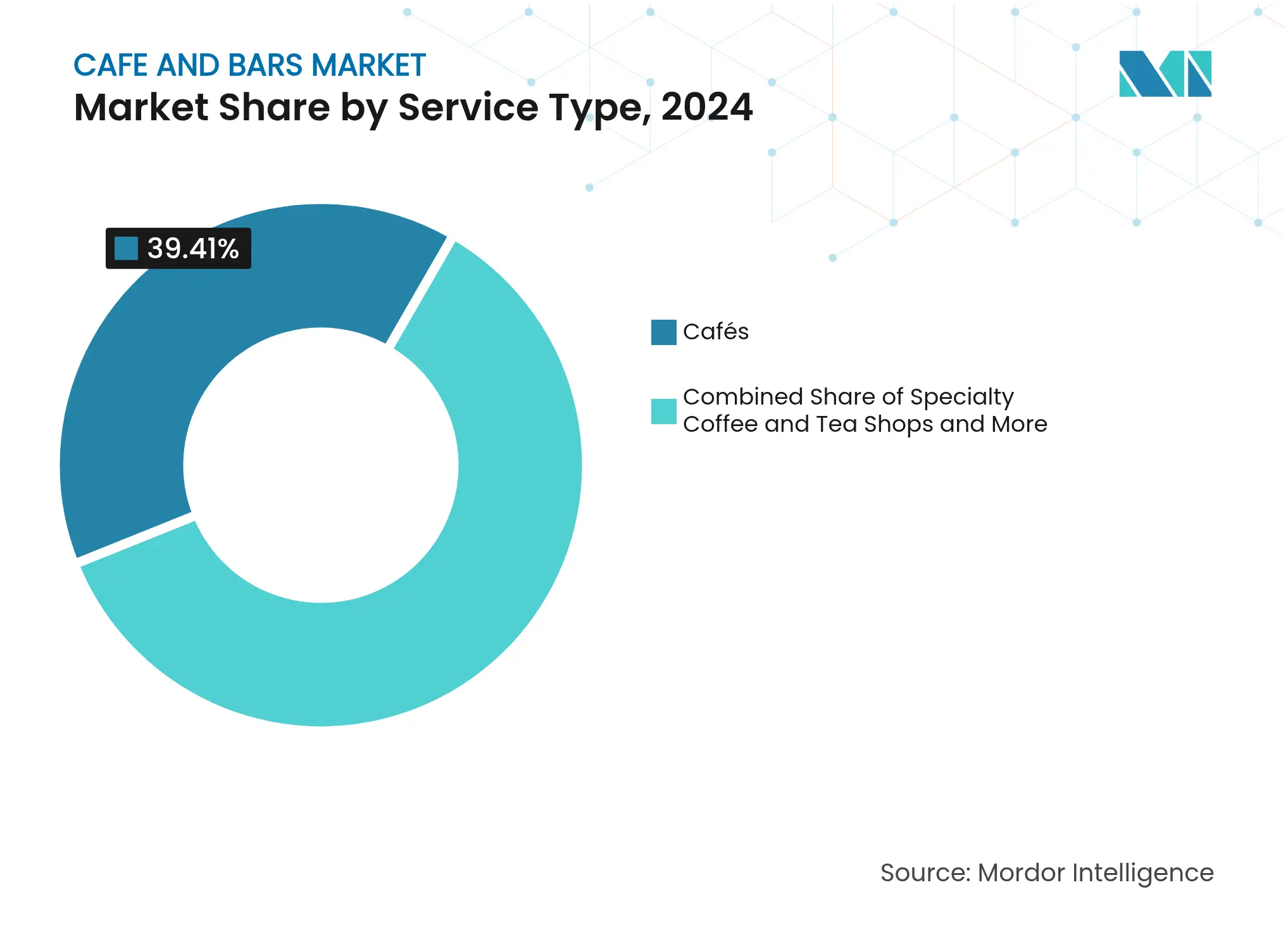

By service type, cafés led with 39.41% revenue share of the cafe and bars market share in 2024, while specialty coffee and tea shops are forecast to expand at a 12.80% CAGR to 2030.

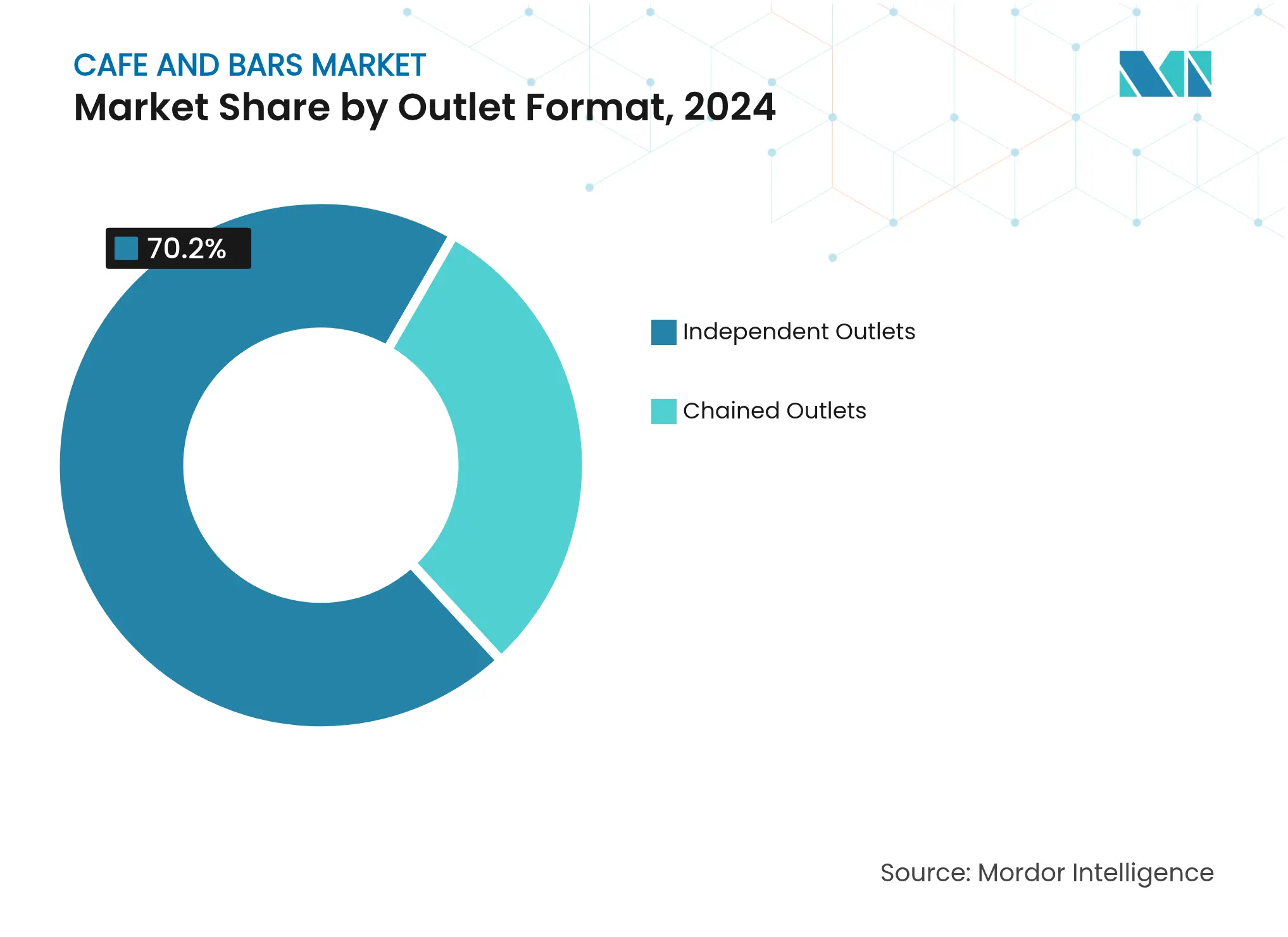

By outlet format, independent operators held 70.20% of the cafe and bars market size in 2024; chained outlets record the highest projected CAGR at 12.60% through 2030.

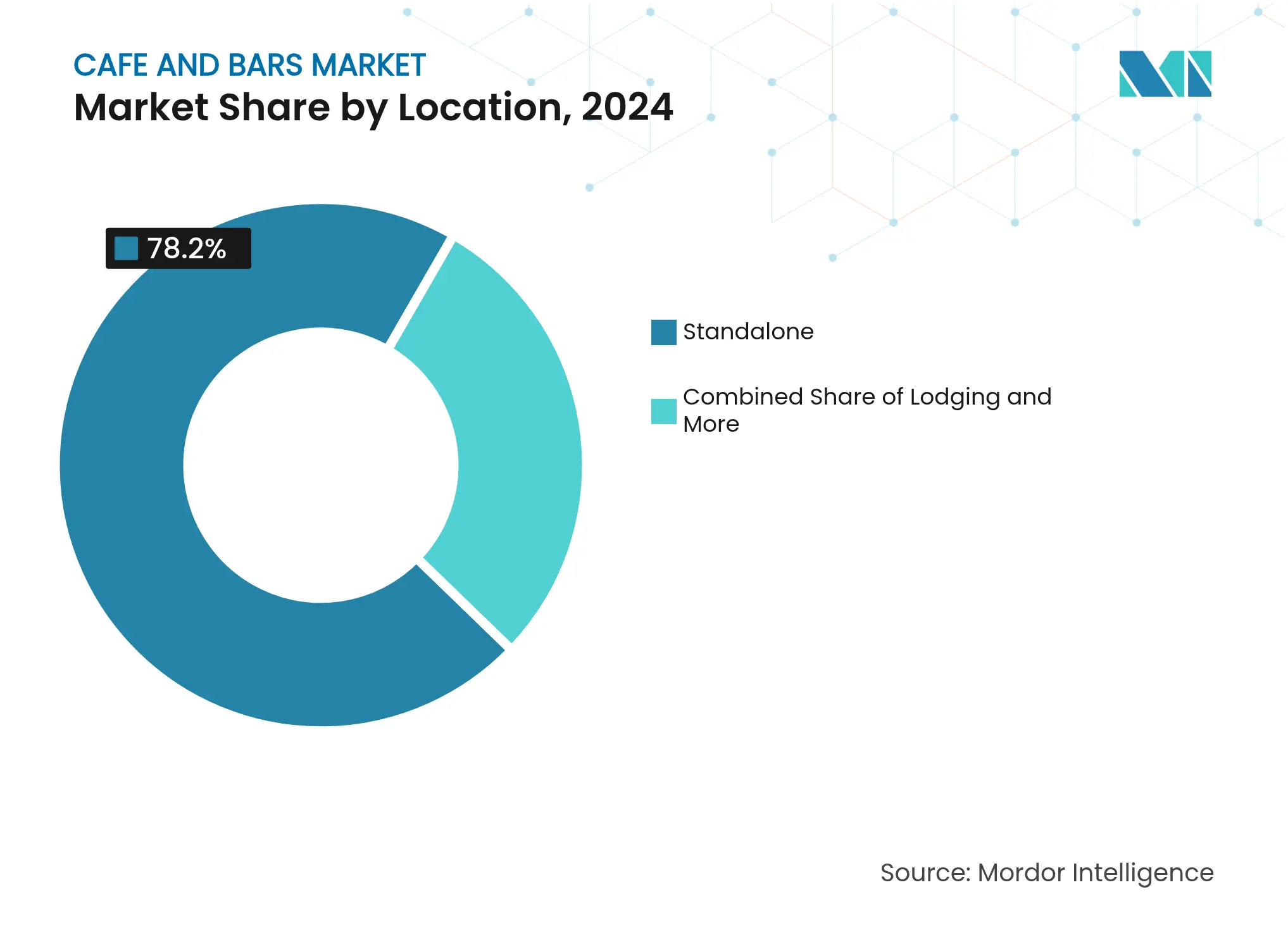

By location, standalone venues accounted for 78.20% share of the cafe and bars market size in 2024, and lodging-integrated concepts are advancing at an 11.47% CAGR through 2030.

By geography, Europe commanded 39.60% of 2024 revenue, whereas the Middle East and Africa region is set to grow at a 14.56% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cafe And Bars Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rise of

Specialty and Craft Beverages

Rise of

Specialty and Craft Beverages

| 2.8% | Global, with a premium focus in North America & Europe | Medium term (2-4 years) |

(~)

% Impact on CAGR Forecast

:

2.8%

|

Geographic

Relevance

:

Global,

with a premium focus in North America & Europe

|

Impact

Timeline

:

Medium

term (2-4 years)

|

Experiential

Retail and Thematic Outlets

Experiential

Retail and Thematic Outlets

| 2.1% | Urban centers globally, strongest in the Asia-Pacific | Medium term (2-4 years) | |||

Menu

Innovation and Health Trends

Menu

Innovation and Health Trends

| 1.9% | North America & Europe leading, expanding to Asia-Pacific | Short term (≤ 2 years) | |||

Influencer

and Pop-Culture Partnerships

Influencer

and Pop-Culture Partnerships

| 1.6% | Global, concentrated in social media-active demographics | Short term (≤ 2 years) | |||

Sustainable

Operations and Circular Models

Sustainable

Operations and Circular Models

| 1.4% | Europe & North America are regulatory-driven, expanding globally | Long term (≥ 4 years) | |||

Hybrid

Concepts and Multi-Functionality

Hybrid

Concepts and Multi-Functionality

| 1.2% | Urban markets in developed economies | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rise of Specialty and Craft Beverages

As consumers increasingly embrace specialty coffee and craft beverages, their expectations have evolved, moving beyond traditional offerings. Artisanal preparation methods now command premium prices, significantly boosting average transaction values. In the 2024 financial year, Starbucks reported a staggering USD 21.88 billion in global revenue, predominantly from its beverage products[2]Source: Starbucks Annual Report, "Starbucks Form 10-K 2024", www.investor.starbucks.com. The third-wave coffee movement champions transparency in sourcing and precision in brewing. Simultaneously, craft cocktail bars are seamlessly incorporating coffee elements, crafting drinks like espresso martinis and cold brew cocktails, effectively blurring the lines between categories. This blending of worlds has led coffee shops to venture into evening alcohol services, while bars are curating sophisticated non-alcoholic programs. In markets such as California, evolving regulatory frameworks now endorse cannabis cafes, allowing them to serve non-alcoholic beverages, thereby broadening the scope of specialty offerings. The trend of premiumization isn't limited to beverages alone; it's now embracing functional ingredients. Adaptogenic compounds and nootropics are making their way into mainstream beverage formulations. Driven by a desire for unique experiences, consumers are increasingly willing to pay a premium, prompting operators to pursue limited-edition collaborations and rotate seasonal menus.

Experiential Retail and Thematic Outlets

Operators in saturated markets stand out through thematic concepts and immersive environments. Book bars, gaming cafes, and co-working hybrids are not just venues; they are destinations, drawing patrons to linger longer and spend more. By weaving retail elements into cafe settings, operators not only boost revenue but also elevate the customer experience with thoughtfully curated products. Airport venues, with their captive audiences, are reaping the rewards of hybrid food-and-beverage retail concepts, making the most of their limited space. Collaborations with influencers and celebrities, though temporary, pack a punch, driving social media buzz and amplifying brand visibility. The evolving "third place" concept now transcends the classic coffeehouse, embracing wellness spaces, pet-friendly zones, and community-driven programs, all fostering deeper local loyalty.

Menu Innovation and Health Trends

Health-conscious consumers are increasingly opting for functional beverages that not only tantalize the taste buds but also offer nutritional benefits. This trend has seen a surge in popularity for protein-packed smoothies, probiotic drinks, and low-sugar alternatives. The British Soft Drinks Association reported that in 2024, the UK saw a consumption of 1.2 billion liters of sports and energy drinks[3]Source: British Soft Drinks Association, "BSDA Annual Report 2024 UK Soft Drinks Report", www.britishsoftdrinks.com. Once considered niche, plant-based milk alternatives have now become mainstream, and adaptogenic ingredients such as lion's mane and ashwagandha are making their way into everyday formulations. The moderation movement is reshaping coffee and alcohol consumption patterns, with many consumers gravitating towards lower-caffeine and alcohol-free choices, allowing them to uphold social rituals without the physiological repercussions. Concerns over liver health are spurring innovations in detoxifying beverages and functional ingredients aimed at enhancing metabolic wellness. As consumers increasingly demand transparency, operators find that clear ingredient sourcing and nutritional labeling can serve as a significant competitive edge.

Sustainable Operations and Circular Models

Driven by environmental consciousness, businesses are reshaping operations to cut waste, optimize resources, and adopt circular economy models, all in a bid to resonate with eco-aware consumers. Starbucks' Greener Stores program, now active in 16% of its locations, showcases a tangible environmental impact, achieving a 30% cut in both energy and water use. Initiatives like Aarhus's coffee cup return program, which successfully collected 735,000 cups in 2024, highlight consumers' readiness to engage in waste reduction, bolstered by reusable cup programs and deposit systems. By sourcing locally, businesses not only curtail transportation emissions but also bolster regional economies and fortify supply chain resilience. Innovative restaurant concepts are redefining waste management, employing composting, local sourcing, and closed-loop cooking to significantly lessen their environmental footprint.

Restrains Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Intense

Market Saturation & Competition

Intense

Market Saturation & Competition

| -1.8% | North America & Western Europe primarily | Short term (≤ 2 years) |

(~)

% Impact on CAGR Forecast

:

-1.8%

|

Geographic

Relevance

:

North

America & Western Europe primarily

|

Impact

Timeline

:

Short

term (≤ 2 years)

|

Stringent

Regulations & Licensing

Stringent

Regulations & Licensing

| -1.2% | Global, varying by jurisdiction | Medium term (2-4 years) | |||

Brand

Dilution from Franchise Overextension

Brand

Dilution from Franchise Overextension

| -0.9% | Mature markets with high chain penetration | Medium term (2-4 years) | |||

Rising

Operational Costs

Rising

Operational Costs

| -1.6% | Global, acute in high-cost urban markets | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Intense Market Saturation & Competition

In developed economies, market saturation exerts pricing pressures, compressing margins and curtailing expansion opportunities. This trend notably impacts independent operators, who find themselves in fierce competition with well-capitalized chains. Starbucks, once a dominant player, now grapples with declining same-store sales and a shrinking market share in China. Its share has plummeted from 34% in 2019 to a mere 14% in 2024, as local rival Luckin Coffee aggressively expands, offering lower-priced alternatives. The surge in coffee shops has led to an overload of choices for consumers, simultaneously fragmenting the market share among a multitude of competitors. In the fiscal year 2024, Cafe Coffee Day, a prominent cafe chain, boasted around 450 cafes spread across diverse Indian cities, reaching out to 141 cities nationwide. This scenario underscores the challenges faced by independent operators in achieving the economies of scale vital for competitive pricing and broader marketing outreach. Urban markets feel the pinch more acutely, where soaring real estate costs, coupled with heightened competition, further erode profitability.

Rising Operational Costs

Operators grapple with tightening margins, squeezed by inflation in labor, real estate, and commodities. Coffee futures, buoyed by climate disruptions in major producing regions, have surged to record highs. Rising labor costs, highlighted by California's USD 20 minimum wage for fast-food workers, have significantly impacted cafes reliant on skilled baristas and extended service hours. Energy costs, particularly for specialty coffee preparation that demands precise temperature control and grinding, further tighten these margins. Additionally, with urban real estate prices soaring, operators are pushed to optimize their space without sacrificing the customer experience. This challenge not only complicates operations but also elevates management overhead. Take Starbucks, for example: in 2024, it reported an annual operating expense of USD 30.767 billion, marking a 2.2% rise from the previous year's USD 30.105 billion, which itself was an 8.95% jump from 2022.

Segment Analysis

By Service Type: Cafés Lead While Specialty Accelerates

In 2024, cafés command a 39.41% market share, leveraging their dual role as quick-service spots and social hubs, catering to varied consumer needs throughout the day. Specialty coffee and tea shops, riding the wave of premiumization, are the fastest-growing segment, boasting a 12.80% CAGR through 2030, as consumers increasingly opt for artisanal and origin-specific offerings at a premium. The rise of AI in product development is evident, with Helsinki's Kaffa Roastery showcasing AI-designed blends, a capability once reserved for industry giants.

Bars and pubs grapple with a patchwork of licensing regulations, with alcohol service permits costing between USD 3,000 and USD 14,000, posing challenges for smaller operators. Juice and smoothie bars, tapping into health trends, integrate functional ingredients. Collaborations, such as Smoothie King's partnership with Dude Perfect, highlight the power of celebrity endorsements in boosting trial and brand visibility. This segment also thrives on clean label trends and protein enhancements, catering to fitness enthusiasts in search of convenient nutrition.

Note: Segment shares of all individual segments available upon report purchase

By Outlet Format: Independent Dominance Faces Chain Efficiency

In 2024, independent outlets capture a dominant 70.20% of the market share, underscoring a consumer shift towards unique experiences and a deeper connection to local communities. This trend sets neighborhood establishments apart from their standardized chain counterparts. Yet, chained outlets are on a faster trajectory, expanding at a 12.60% CAGR through 2030. Their growth is fueled by operational efficiencies, heightened brand recognition, and easier access to capital, all of which pave the way for swift geographic expansion and tech adoption, as highlighted by the National Restaurant Association. A testament to this trend is Blank Street Coffee, which has scaled from a solitary cart to 65 locations, now boasting a valuation of USD 118 million. Their journey underscores a scalable model that adeptly marries tech integration with a focus on local customer engagement.

Independent operators carve out their niche through personalized services, forging partnerships with local suppliers, and curating community-centric programs. These strategies foster customer loyalty that transcends mere transactions. Meanwhile, the rise of regional chains and franchise models offers a balanced approach, merging the flexibility of independents with robust operational support. However, independents face mounting challenges with regulatory compliance, especially in areas like alcohol licensing and food safety. Without dedicated legal resources, navigating these complexities becomes daunting, often favoring those operators with established compliance systems.

By Location: Standalone Venues Adapt to Lodging Integration

In 2024, standalone locations account for 78.20% of venues, enjoying operational flexibility and easy customer access, catering to both planned visits and spontaneous drop-ins. Concepts integrated with lodging are set to grow at an 11.47% CAGR through 2030, leveraging captive audiences and extended hours to boost revenue from prime real estate spots. Airport hotels are now adding rooftop bars and specialty coffee shops, with Nashville's Hilton BNA leading the way, offering panoramic views and music-themed experiences for both travelers and locals.

Locations integrated with retail enjoy the perks of cross-selling and shared foot traffic. In contrast, travel-centric venues can command higher prices, thanks to their convenience and the limited competition in transport hubs. Leisure spots, however, grapple with seasonal fluctuations, necessitating adaptable staffing and menu changes to stay profitable during off-peak times. Standalone venues, like Starbucks with its EV charging stations at over 100 sites, showcase their adaptability to evolving consumer mobility trends, simultaneously tapping into new revenue avenues.

Geography Analysis

In 2024, Europe accounted for 39.60% of global revenues, driven by a deep-rooted café culture and a consumer base willing to embrace premium pricing. Harmonized food safety and labor standards across borders facilitate smoother expansions for chains. Yet, as the market matures, there's a pronounced pivot towards unique offerings—think literary cafés and zero-waste pop-ups—ensuring relevance in a crowded landscape.

Meanwhile, the Middle East and Africa are on a rapid ascent, projected to grow at a 14.56% CAGR until 2030. With Saudi Arabia boasting nearly 50% of the regional store count, the nation reaps the benefits of strong governmental backing in tourism and entertainment. This support paves the way for upscale coffee houses. Operators are also attuning their menus to local tastes, introducing items like cardamom-infused roasts and camel-milk lattes, deepening cultural ties. Notably, global chains are eyeing expansive rollouts, a testament to their faith in continued growth in disposable incomes, even amidst geopolitical uncertainties.

Asia-Pacific presents a mixed bag. While China has surpassed the U.S. in the number of branded stores, it's grappling with profitability, facing fierce discounting wars that slashed average selling prices by 14% in 2024. Conversely, India stands as a promising long-term market, with its burgeoning middle class of 432 million increasingly seeking modern café experiences. In response to urban congestion, regional players are bridging service gaps with innovations like drive-throughs and fully automated preparation stations, bolstering the economic viability of prime café locations.

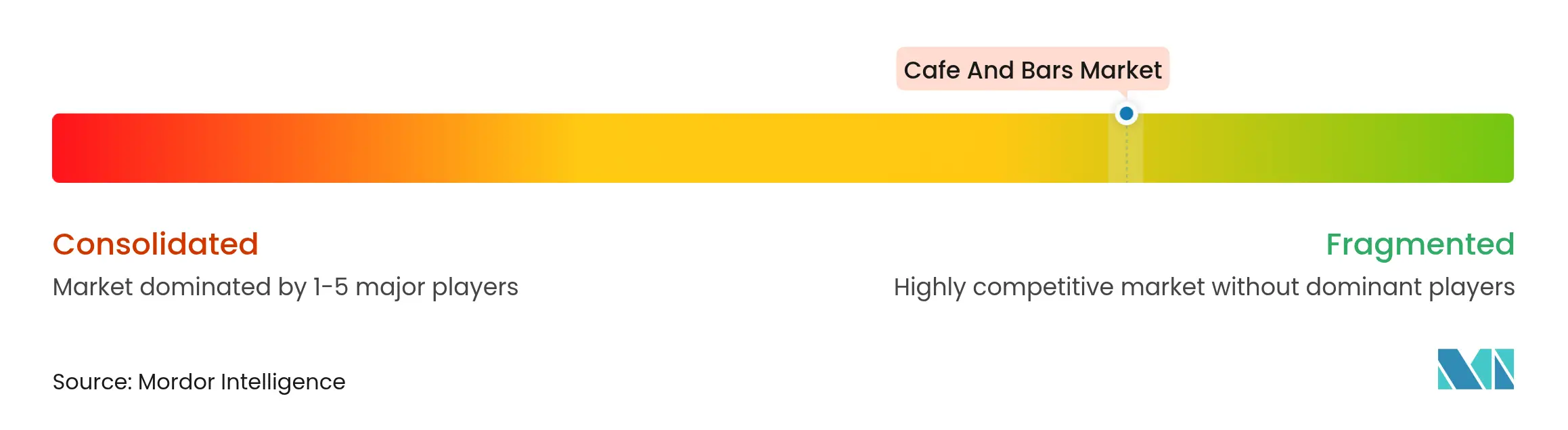

Competitive Landscape

Market Concentration

Despite independents dominating over two-thirds of the market, a wave of consolidation is reshaping the landscape. Private equity funds are snapping up specialty chains, pushing for accelerated growth and streamlined sourcing. Starbucks, the global frontrunner, eyes an ambitious target of 17,000 new stores by 2030. The coffee giant is zeroing in on tier-two cities worldwide, especially those with untapped potential. Simultaneously, it's upgrading legacy stores with energy-efficient equipment, a move aimed at slashing operating costs and hitting environmental benchmarks.

Regional players are harnessing technology to carve out competitive advantages. Luckin Coffee, for instance, leverages app-driven pre-ordering and operates compact, cost-effective units, allowing swift penetration into densely populated neighborhoods. Boutique brands, on the other hand, are cementing their artisanal image with limited-release roasts and immersive origin events. Not to be outdone, hotel and airport operators are launching proprietary café concepts, tapping into additional revenue streams and heightening competition in the "cafe and bars" arena.

Strategic partnerships are on the rise. Beverage giants are pouring investments into specialty coffee roasters, broadening their product range and ensuring premium supply access. Ventures spearheaded by creators, like Emma Chamberlain's physical café debut, spotlight franchising avenues rooted in personal branding over conventional corporate identities. In a bid to challenge established chains, automation firms are teaming up with convenience stores, rolling out robotic barista stations in bustling micro-locations. This blend of strategies paints a picture of a vibrant industry that's moderately concentrated, with the top five players commanding a combined share of nearly 30%, highlighting room for both expansive growth and niche specialization.

Cafe And Bars Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: ELLE Café, the premium coffee brand that’s a licensee of the world-renowned French fashion and lifestyle global ELLE brand and its owner Lagardère Group, expanded its reach to Sprouts Farmers Market. Three of ELLE Café’s single-serve K-Cup compatible varieties were made available at nearly all of Sprouts’ 400+ locations.

- January 2025: Coffee Island entered India in partnership with Vita Nova and opened its first outlet at HQ27 in Gurgaon, which featured its proprietary in-house roasting process and a variety of Global Single Estate Beans, Global Blends, and Home Blends. The company is targeting to open 20 outlets by March 2026 and expand to 250 locations by 2029.

- November 2024: To enter more cities in the United States, Canada-based Fresh Healthy Cafe, which has about 30 locations, has partnered with Fresh USA LLC, owned by Cape Girardeau, Missouri husband-and-wife Rick Hetzel and Cheryl Mothes. The duo owns three locations and will accelerate Fresh Healthy Cafe's U.S. franchise expansion in the coming years.

- November 2024: The Al Qassim-based coffee chain opened an outlet in New York’s ‘Little Yemen’ neighborhood, serving a diverse coffee menu featuring Western and Middle East-inspired beverages. The brand’s US menu features Americanos and lattes alongside Saudi and Turkish coffee.

Table of Contents for Cafe And Bars Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rise of Specialty and Craft Beverages

- 4.2.2Experiential Retail and Thematic Outlets

- 4.2.3Menu Innovation and Health Trends

- 4.2.4Influencer and Pop-Culture Partnerships

- 4.2.5Sustainable Operations and Circular Models

- 4.2.6Hybrid Concepts and Multi-Functionality

- 4.3Market Restraints

- 4.3.1Intense Market Saturation and Competition

- 4.3.2Stringent Regulations and Licensing

- 4.3.3Brand Dilution from Franchise or Chain Overextension

- 4.3.4Rising Operational Costs

- 4.4Consumer Behaviour Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter’s Five Forces

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS

- 5.1By Service Type

- 5.1.1Bars and Pubs

- 5.1.2Cafés

- 5.1.3Specialty Coffee and Tea Shops

- 5.1.4Juice and Smoothies Bar

- 5.2By Outlet Format

- 5.2.1Chained Outlets

- 5.2.2Independent Outlets

- 5.3By Location

- 5.3.1Leisure

- 5.3.2Lodging

- 5.3.3Retail

- 5.3.4Standalone

- 5.3.5Travel

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.1.4Rest of North America

- 5.4.2South America

- 5.4.2.1Brazil

- 5.4.2.2Argentina

- 5.4.2.3Colombia

- 5.4.2.4Chile

- 5.4.2.5Rest of South America

- 5.4.3Europe

- 5.4.3.1United Kingdom

- 5.4.3.2Germany

- 5.4.3.3France

- 5.4.3.4Italy

- 5.4.3.5Spain

- 5.4.3.6Russia

- 5.4.3.7Sweden

- 5.4.3.8Belgium

- 5.4.3.9Poland

- 5.4.3.10Netherlands

- 5.4.3.11Rest of Europe

- 5.4.4Asia-Pacific

- 5.4.4.1China

- 5.4.4.2Japan

- 5.4.4.3India

- 5.4.4.4Thailand

- 5.4.4.5Singapore

- 5.4.4.6Indonesia

- 5.4.4.7South Korea

- 5.4.4.8Australia

- 5.4.4.9New Zealand

- 5.4.4.10Rest of Asia Pacific

- 5.4.5Middle East and Africa

- 5.4.5.1United Arab Emirates

- 5.4.5.2South Africa

- 5.4.5.3Saudi Arabia

- 5.4.5.4Nigeria

- 5.4.5.5Egypt

- 5.4.5.6Morocco

- 5.4.5.7Turkey

- 5.4.5.8Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Starbucks Corporation

- 6.4.2J D Wetherspoon plc

- 6.4.3The Coca-Cola Company

- 6.4.4Odyzean Ltd (Costa Coffee)

- 6.4.5Buffalo Wild Wings (Inspire)

- 6.4.6McDonald's Corporation (McCafé)

- 6.4.7Coffee Day Enterprises

- 6.4.8John Swire & Sons Ltd (Pacific Coffee)

- 6.4.9Luigi Lavazza SpA

- 6.4.10Rome Bidco Ltd (Pret A Manger)

- 6.4.11Dunkin’ (Inspire Brands)

- 6.4.12Whitbread plc

- 6.4.13Restaurant Brands Intl. (Tim Hortons)

- 6.4.14Peet’s Coffee & Tea

- 6.4.15Compass Group (Ritz Coffee Bars)

- 6.4.16Kimly Ltd

- 6.4.17Blue Bottle Coffee Inc.

- 6.4.18Barista Coffee Company

- 6.4.19Minor International (The Coffee Club)

- 6.4.20Eataly SpA (Café Vergnano)

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Global Cafe And Bars Market Report Scope

A café is a style of eatery that offers coffee along with other beverages with snacks. They are often modest businesses with a minimal amount of seating. As a result, they offer an ideal pit break for a quick beverage such as coffee or tea, along with a pastry, sandwich, and other similar kind of foods. Bars, on the other hand, are often used to describe a place to drink mainly alcoholic beverages with snacks. The global café and bars market (henceforth referred to as the market studied) is segmented By service type, By outlet, and geography. By service type, the market is segmented into Bars, Cafes, and Coffee Shops. By outlet, the market is segmented into chained outlets and independent outlets. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).