Cafe Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 326.34 Billion |

| Market Size (2031) | USD 423.49 Billion |

| Growth Rate (2026 - 2031) | 5.35% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

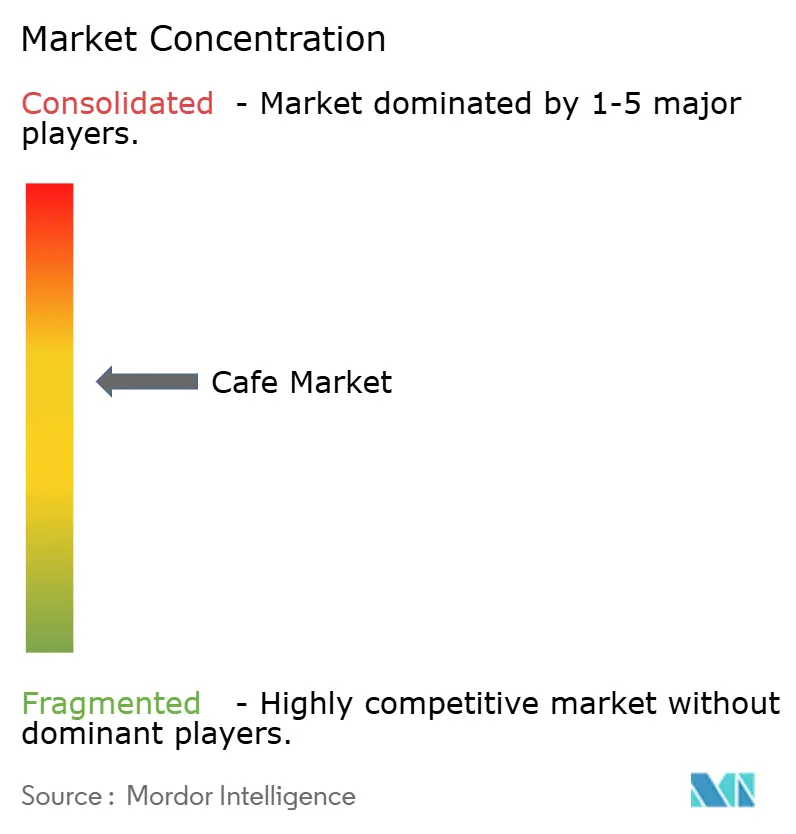

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Cafe Market Analysis by Mordor Intelligence

The cafe market size is expected to grow from USD 309.77 billion in 2025 to USD 326.34 billion in 2026 and is forecast to reach USD 423.49 billion by 2031 at 5.35% CAGR over 2026-2031. Germany recorded 125,500 tons of out-of-home coffee consumption in 2025, which set a new high even as price pressure remained elevated, showing that café visits still hold up well when household budgets tighten. In the United States, specialty coffee surpassed traditional coffee consumption in 2025, and 46% of adults consumed specialty coffee daily, which points to a durable premiumization shift across the cafe market. Urbanization and hybrid work patterns are also supporting the cafe market because cafés increasingly serve both as social spaces and practical work settings. Digital ordering and delivery are widening access, while larger operators are using loyalty platforms and procurement scale to protect traffic and margins. Mature demand in Europe still anchors the cafe market, while underpenetrated cities in Asia and the Middle East continue to provide a long runway for outlet expansion and format innovation.

Key Report Takeaways

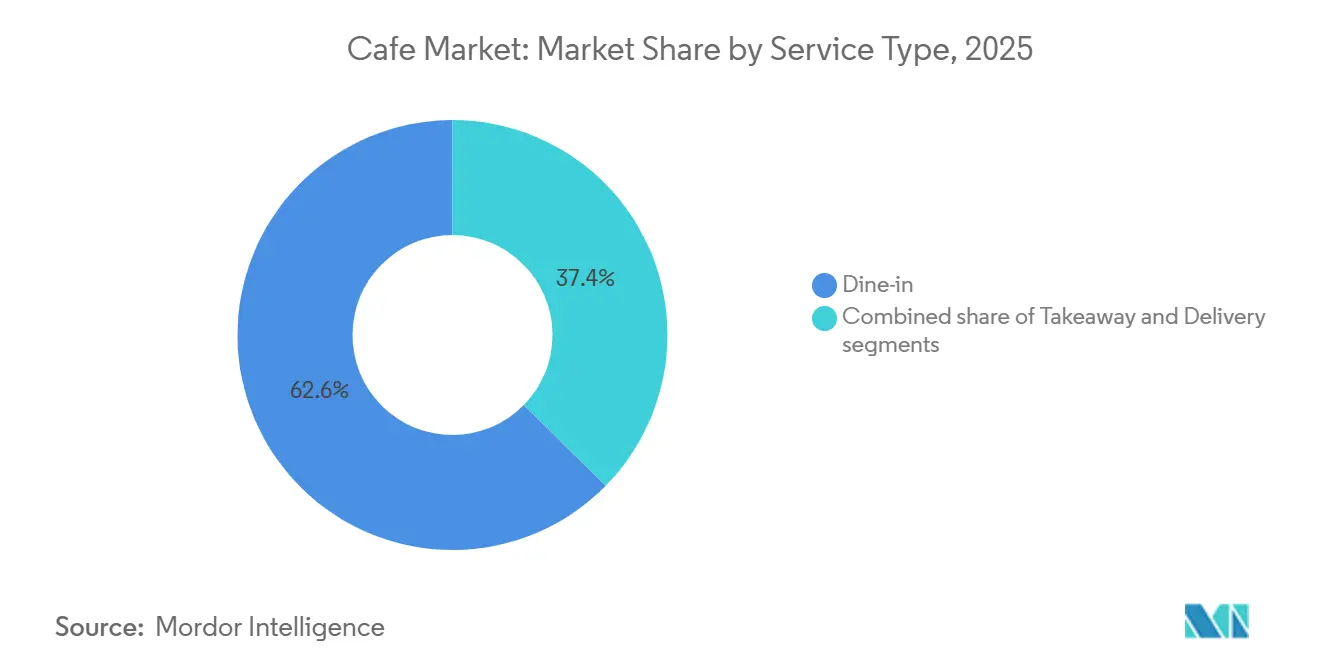

- By service type, dine-in held 62.64% of the cafe market share in 2025, while delivery is projected to expand at a 7.45% CAGR through 2031.

- By outlet, independent outlets accounted for 69.41% of the cafe market size in 2025, while chained outlets are forecast to record the highest CAGR at 8.23% through 2031.

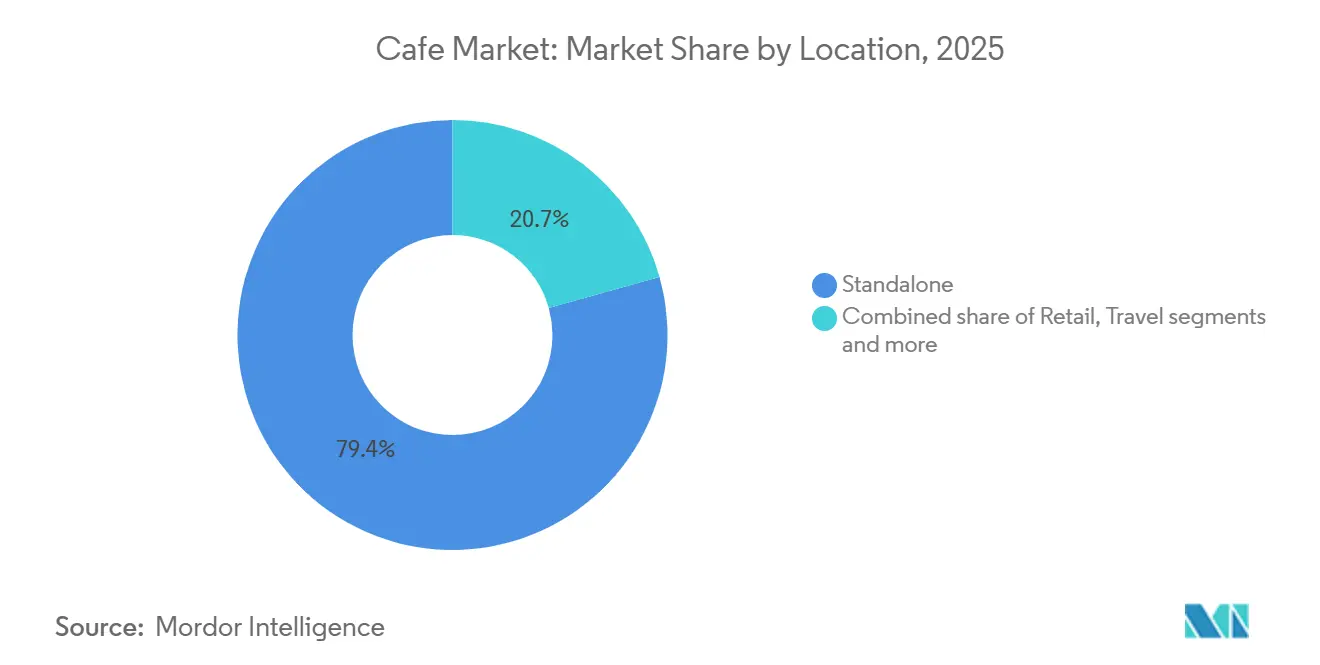

- By location, standalone cafés represented 79.35% of the cafe market size in 2025, while travel locations are expected to grow fastest at a 6.85% CAGR through 2031.

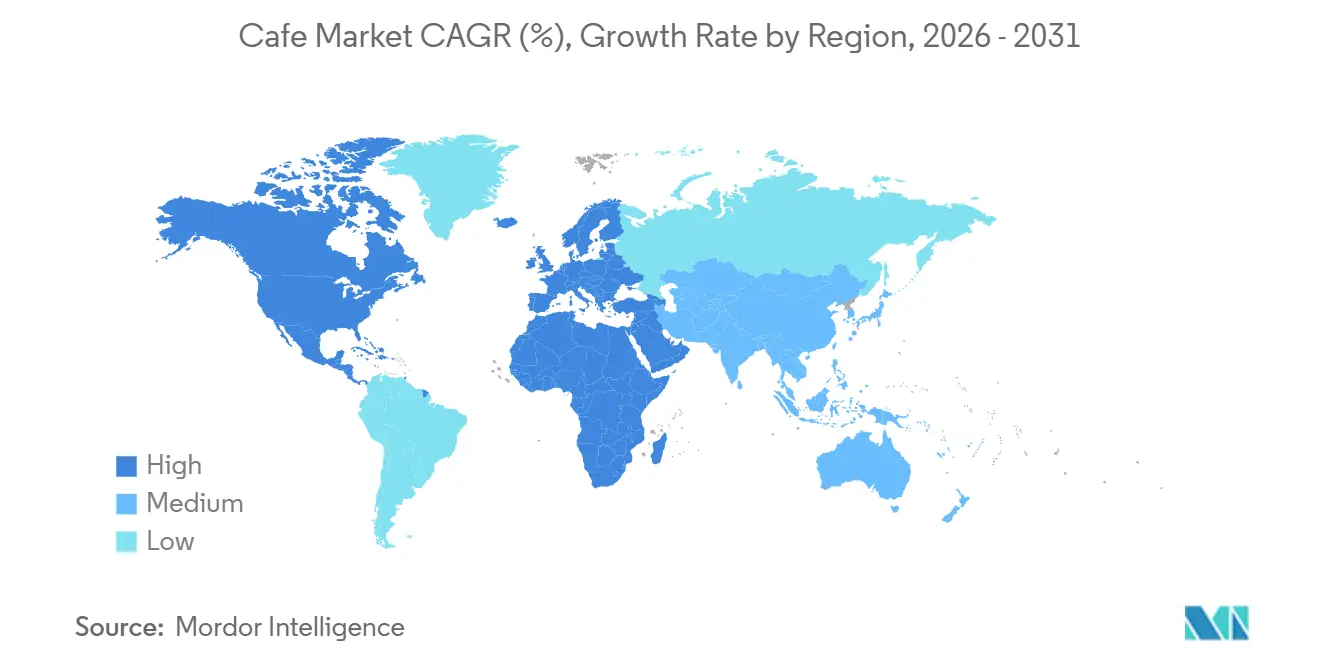

- By geography, Europe captured 38.45% of the global cafe market share in 2025, while the Middle East & Africa is projected to post the fastest regional growth at a 7.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cafe Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global coffee consumption and café culture adoption | +1.1% | Global | Medium term (2-4 years) |

| Expansion of specialty coffee and premium beverage demand | +0.8% | North America & Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Growing consumer preference for social dining and experiential spaces | +0.7% | North America, Europe, Asia-Pacific urban centres | Long term (≥ 4 years) |

| Rising penetration of international and regional café chains | +0.8% | Asia-Pacific, Middle East and Africa, Global | Long term (≥ 4 years) |

| Increasing adoption of digital ordering and food delivery platforms | +0.6% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Expansion of remote working and café-based work culture | +0.3% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising global coffee consumption and café culture adoption

The growth of global coffee consumption and the rapid adoption of café culture are major factors driving the expansion of the café market worldwide. Consumers are increasingly viewing cafés as social, professional, and lifestyle-oriented destinations rather than solely beverage outlets. The rising popularity of specialty coffee, premium beverages, and personalized café experiences has significantly increased café visitation across both developed and emerging economies. Younger consumers, particularly millennials and Generation Z, are strongly contributing to the demand for experiential coffee consumption and café-based social interactions. According to the National Coffee Association 2025 report, nearly two-thirds of American adults consume coffee daily, with 66% of the adult population drinking coffee every day, highlighting the strong and consistent consumer demand for coffee beverages[1]Source: National Coffee Association, "More Americans drink coffee each day than any other beverage, bottled water back in second place", ncausa.org. In addition, the expansion of international café chains, digital ordering platforms, and takeaway formats has further strengthened coffee accessibility across urban markets.

Expansion of specialty coffee and premium beverage demand

The rising demand for specialty coffee and premium beverages is becoming a major growth driver for the global café market. Consumers are increasingly shifting toward high-quality coffee experiences that include artisanal brewing methods, single-origin beans, cold brews, flavored beverages, and customized drink options. Premium café offerings are particularly gaining popularity among millennials and younger consumers who value product quality, authenticity, and experiential consumption. According to the National Coffee Association, specialty coffee consumption in the United States reached a 14-year high in 2025, with 46% of American adults consuming specialty coffee daily. The association also reported that specialty coffee consumption has increased by 84% since 2011 and, for the first time, surpassed traditional coffee consumption, which stood at 42%[2]Source: National Coffee Association, "Specialty coffee consumption hits 14-year high", ncausa.org. This trend reflects the growing consumer preference for premiumized coffee products and elevated café experiences across mature and emerging markets alike.

Growing consumer preference for social dining and experiential spaces

The growing consumer preference for social dining and experiential spaces is significantly driving the expansion of the global café market. Modern consumers increasingly view cafés as lifestyle destinations that offer social interaction, relaxation, work-friendly environments, and personalized dining experiences beyond traditional beverage consumption. Cafés are becoming popular venues for informal meetings, remote working, social gatherings, and leisure activities, particularly among millennials and Generation Z consumers. The increasing emphasis on ambiance, interior aesthetics, specialty beverages, live experiences, and premium service offerings is encouraging higher café visitation rates globally. According to the Auguste Escoffier School of Culinary Arts, U.S. consumers spent an average of USD 191 per person per month on dining out in 2024, compared to approximately USD 166 per month in 2023, highlighting the rising consumer willingness to spend on foodservice and experiential dining occasions[3]Source: Auguste Escoffier School of Culinary Arts, "2025 Consumer Dining Trends: How Americans Are Spending on Restaurants and Takeout", escoffier.edu. Café operators are responding by investing in premium store designs, community-focused concepts, themed café experiences, and enhanced seating environments to strengthen customer engagement.

Rising penetration of international and regional café chains

The rising penetration of international café chains is significantly driving the growth of the global café market. Leading global brands are aggressively expanding their presence across emerging and developed markets through franchising, strategic partnerships, and rapid outlet expansion strategies. International café operators are benefiting from strong brand recognition, standardized product quality, digital loyalty programs, and premium café experiences that attract a broad consumer base. The growing urban population and increasing exposure to western foodservice culture are further accelerating the adoption of branded café chains, particularly across Asia-Pacific, the Middle East, and Latin America. Companies such as Starbucks, Tim Hortons, Costa Coffee, and Luckin Coffee are continuously expanding into high-traffic urban centers, shopping malls, airports, and commercial districts to strengthen market penetration. In addition, international café chains are increasingly localizing their menus by introducing region-specific beverages, snacks, and seasonal offerings to improve consumer engagement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operational and rental costs in prime urban locations | -0.5% | Global urban centres; acute in North America and Europe | Short term (≤ 2 years) |

| Volatility in coffee bean and dairy ingredient prices | -0.7% | Global; disproportionate in markets with high Arabica dependency | Short term (≤ 2 years) |

| Labor shortages and increasing employee wage pressures | -0.4% | North America and Europe | Medium term (2–4 years) |

| Rising consumer shift toward home brewing and ready-to-drink beverages | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High operational and rental costs in prime urban locations

High operational and rental costs represent a significant challenge restraining the growth of the global café market. Café operators, particularly those located in prime urban areas, shopping malls, airports, and commercial districts, face substantial expenses related to rent, utilities, labor, and daily operations. Rising real estate prices in metropolitan cities are increasing the financial burden on both independent cafés and large café chains, affecting overall profitability margins. In addition, cafés require continuous investments in interior design, seating arrangements, premium equipment, and customer experience enhancements to remain competitive in the market. Labor-intensive operations, including skilled baristas, customer service staff, and food preparation personnel, further contribute to escalating operational expenditures. Small and independent café operators are especially vulnerable to fluctuating costs, making long-term business sustainability more challenging.

Volatility in coffee bean and dairy ingredient prices

Volatility in coffee bean and dairy ingredient prices is a major factor restraining the growth and profitability of the global café market. Coffee prices are highly influenced by changing climatic conditions, supply chain disruptions, geopolitical uncertainties, and fluctuations in global agricultural production, particularly in major coffee-producing countries such as Brazil, Vietnam, and Colombia. Adverse weather events including droughts, excessive rainfall, and frost conditions can significantly impact coffee crop yields, leading to unpredictable price increases. Similarly, dairy ingredient prices are affected by rising feed costs, livestock production challenges, inflationary pressures, and global supply-demand imbalances. Since coffee beans and dairy products represent core raw materials for cafés, frequent cost fluctuations directly impact operating margins and menu pricing strategies. Many café operators, especially independent businesses, face difficulties in absorbing higher ingredient costs without increasing consumer prices, which may affect customer demand and competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Delivery Reshapes a Dine-In Core

The dine-in segment accounted for 62.64% of the global café market share in 2025, making it the dominant service type within the industry. The segment’s leadership is primarily driven by consumer preference for social interaction, premium café ambiance, and experiential dining environments. Cafés are increasingly being used as meeting spaces for professionals, students, and social gatherings, particularly in urban areas. The expansion of specialty coffee shops, bakery cafés, and premium café chains has further strengthened dine-in consumption across both developed and emerging markets. In addition, consumers often associate dine-in café experiences with product freshness, customization, and a relaxed atmosphere, encouraging longer visit durations and higher spending per customer.

The delivery segment is projected to register the fastest growth in the café market, expanding at a CAGR of 7.45% through 2031. The rapid adoption of online food delivery platforms and mobile ordering applications has significantly transformed café consumption patterns worldwide. Consumers increasingly prefer convenient access to coffee beverages, snacks, and bakery products through home delivery and office delivery services. Café operators are actively partnering with third-party delivery platforms and investing in digital ordering ecosystems to improve customer accessibility and operational efficiency. The growth of remote working culture and rising demand for convenience-based foodservice solutions are further accelerating delivery segment expansion.

By Outlet: Independent Operators Anchor Market, Chains Accelerate

Independent outlets accounted for 69.41% of the global café market size in 2025, making them the leading outlet category within the industry. The strong presence of local cafés, specialty coffee shops, and family-owned establishments has significantly contributed to the segment’s dominance across both developed and emerging markets. Consumers often prefer independent cafés for their personalized customer service, unique ambiance, artisanal beverage offerings, and locally inspired menus. These cafés also benefit from greater flexibility in product innovation, allowing operators to quickly adapt to regional taste preferences and changing consumer trends. In many urban areas, independent cafés serve as social and community gathering spaces, strengthening customer loyalty and repeat visitation rates.

Chained outlets are projected to register the fastest growth in the café market, expanding at a CAGR of 8.23% through 2031. The rapid expansion of international and regional café chains is being driven by increasing franchising activity, strong brand recognition, and rising consumer demand for standardized product quality and service consistency. Major café chains are aggressively investing in outlet expansion across high-traffic urban locations, shopping malls, airports, and transit hubs to strengthen market penetration. The segment is also benefiting from advanced digital ecosystems, including mobile ordering applications, loyalty programs, delivery partnerships, and AI-driven customer engagement strategies. In emerging markets, chained cafés are increasingly attracting younger consumers seeking premium coffee experiences and modern café environments.

By Location: Standalone Dominance Meets Travel-Format Growth

Standalone cafés represented 79.35% of the global café market size in 2025, making them the dominant location segment within the industry. The strong performance of this segment is largely driven by high consumer accessibility, independent brand visibility, and flexible operational models associated with standalone café outlets. These cafés are commonly located in urban centers, residential neighborhoods, and high-footfall commercial districts, allowing operators to build a loyal and recurring customer base. Standalone locations also provide café owners with greater control over store design, ambiance, seating capacity, and customer experience strategies. The segment has particularly benefited from the growing popularity of specialty coffee culture, social dining trends, and remote working habits that encourage longer café visits.

Travel locations are expected to register the fastest growth in the café market, expanding at a CAGR of 6.85% through 2031. The increasing recovery of global tourism, rising airport passenger traffic, and growing intercity travel activity are significantly contributing to demand for cafés in travel hubs. Café operators are actively expanding their presence across airports, railway stations, highways, and transit terminals to capitalize on increasing consumer demand for convenient food and beverage options during travel. Consumers increasingly prefer premium coffee beverages, ready-to-eat snacks, and quick-service café formats while commuting, creating strong opportunities for café brands in travel-oriented locations.

Geography Analysis

Europe accounted for 38.45% of the global café market share in 2025, making it the largest regional market worldwide. The region’s dominance is primarily supported by its deeply established coffee culture, high café density, and strong consumer preference for premium coffee experiences. Countries such as Italy, France, Germany, and the United Kingdom continue to witness strong footfall across specialty cafés, bakery cafés, and branded coffee chains. The presence of major international operators alongside a large network of independent cafés has further strengthened market penetration across urban and suburban areas. In addition, consumers in Europe increasingly prefer artisanal beverages, organic coffee products, and café environments that offer social and work-friendly experiences. The growing popularity of specialty coffee, premium bakery products, and sustainable café concepts continues to reinforce Europe’s leadership position in the global café market.

The Middle East & Africa region is projected to register the fastest growth in the global café market, expanding at a CAGR of 7.11% through 2031. Rapid urbanization, rising disposable incomes, and changing consumer lifestyles are significantly increasing café visitation rates across countries such as the United Arab Emirates, Saudi Arabia, and South Africa. International café chains are aggressively expanding their regional presence through franchising and premium outlet development in shopping malls, commercial districts, and travel hubs. The increasing young population and growing demand for premium coffee beverages are also supporting higher café consumption across metropolitan cities. Furthermore, the region is witnessing strong growth in specialty coffee culture, particularly among millennials and working professionals seeking premium social dining experiences.

North America remains one of the most mature café markets globally, supported by high per capita coffee consumption and the strong presence of established café chains and specialty coffee brands. The United States and Canada continue to drive regional demand through premium coffee offerings, loyalty programs, and expanding drive-through and takeaway formats. Asia-Pacific is emerging as a highly attractive growth market due to rapid urbanization, increasing westernization of food habits, and expanding middle-class populations in countries such as China, India, Japan, and South Korea. The region is witnessing strong outlet expansion from both international and domestic café brands, particularly in metropolitan areas. Meanwhile, South America maintains stable market growth supported by its strong coffee production base and evolving café culture across countries such as Brazil, Colombia, and Argentina.

Competitive Landscape

The café market operates with a moderately fragmented competitive landscape, characterized by the presence of multinational café chains, regional operators, and a large number of independent coffee shops. Major companies compete on the basis of brand recognition, store expansion, premium beverage offerings, digital ordering capabilities, and customer experience. Starbucks Corporation continues to maintain a dominant global position through its extensive outlet network, strong loyalty ecosystem, and continuous product innovation across beverages and food categories. The company is also investing heavily in drive-through formats, digital engagement, and sustainable sourcing initiatives to strengthen consumer retention and operational efficiency.

Restaurant Brands International Inc., through its Tim Hortons brand, remains a significant player in the café market, particularly across Canada and selected international markets. The company focuses on value-oriented beverage offerings, breakfast menus, and aggressive franchising strategies to expand its footprint. Meanwhile, Luckin Coffee Inc. has emerged as one of the fastest-growing café operators globally, supported by its app-driven business model, competitive pricing strategy, and rapid expansion across China. The company’s digitally integrated ordering and delivery ecosystem has intensified competition within the Asia-Pacific café sector.

The market is also witnessing increasing competition from specialty coffee chains, boutique cafés, bakery cafés, and quick-service restaurant operators expanding into premium coffee offerings. Companies are increasingly emphasizing experiential café concepts, seasonal beverage launches, sustainability initiatives, and localized menu innovation to differentiate themselves in highly competitive urban markets. In addition, strategic partnerships with food delivery platforms, expansion into emerging economies, and investments in automated café technologies are becoming key competitive strategies among leading participants. The growing demand for premium coffee experiences and convenience-based consumption continues to encourage both global and regional players to expand aggressively across high-growth markets.

Cafe Industry Leaders

-

Starbucks Corporation

-

Restaurant Brands International (Tim Hortons)

-

Caffè Nero Group Ltd

-

Barista Coffee Company Limited

-

Luckin Coffee Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Costa Coffee opened its 400th drive-thru outlet in the United Kingdom and plans to launch up to 40 additional drive-thru stores during 2026. The company stated that drive-thru formats have become one of the fastest-growing components of its retail estate, driven by increasing consumer demand for convenience-oriented coffee consumption during commuting, school runs, and travel occasions.

- January 2026: Tim Hortons planned to expand its presence in South Korea by increasing the number of outlets from 24 to 50 by 2026. The company also aims to achieve a total of 160 outlets nationwide by 2028. This growth strategy focuses on menu localization and enhancing its bakery offerings to cater to local preferences.

- January 2026: Starbucks Corporation unveiled a revamped Starbucks Rewards program, aiming to bolster customer engagement, personalization, and loyalty throughout its worldwide café chain. The refreshed program rolled out three membership tiers: Green, Gold, and Reserve. Each tier comes with progressively enhanced perks, including quicker Star accumulation, exclusive merchandise access, tailored promotions, and premium experiential rewards.

Global Cafe Market Report Scope

A café is a foodservice establishment that primarily serves coffee, tea, and other beverages along with light meals, snacks, bakery products, and desserts in a casual dining environment. The cafe market is segmented by service type, outlet, location and geography. Based on service type, the market is segmented into dine-in, takeaway and delivery. Based on outlet, the market is segmented into independent outlets and chained outlets. Based on location, the market is segmented into leisure, lodging, retail, standalone and travel. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market sizing and forecasting have been done in value terms (USD million).

| Dine-in |

| Takeaway |

| Delivery |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East & Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Service Type | Dine-in | |

| Takeaway | ||

| Delivery | ||

| By Outlet | Chained Outlets | |

| Independent Outlets | ||

| By Location | Leisure | |

| Lodging | ||

| Retail | ||

| Standalone | ||

| Travel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East & Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the cafe market?

The cafe market was valued at USD 309.77 billion in 2025 and is estimated at USD 326.34 billion in 2026, with a projected rise to USD 423.49 billion by 2031.

How fast is the cafe market expected to grow through 2031?

The cafe market is forecast to grow at a 5.35% CAGR from 2026 to 2031, supported by resilient coffee consumption, premium beverage demand, and wider digital access.

Which service format is growing the fastest in cafes?

Delivery is the fastest-growing service type, with a projected 7.45% CAGR through 2031.

Are independent cafes still more important than chains globally?

Yes. Independent outlets held 69.41% of the market in 2025, but chained outlets are growing faster, with an 8.23% CAGR forecast through 2031.

Which region leads global cafe demand?

Europe led the global market with a 38.45% share in 2025, supported by mature coffee habits and strong out-of-home consumption in markets such as Germany.

Page last updated on: