Biotech Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

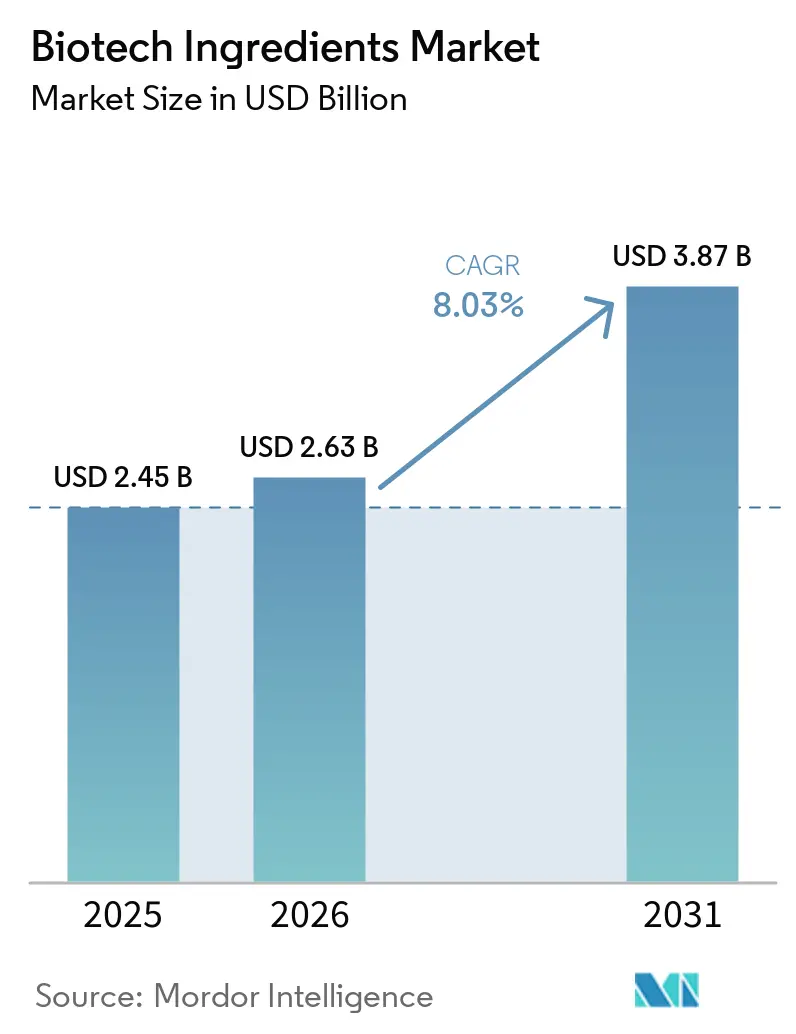

| Market Size (2026) | USD 2.63 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

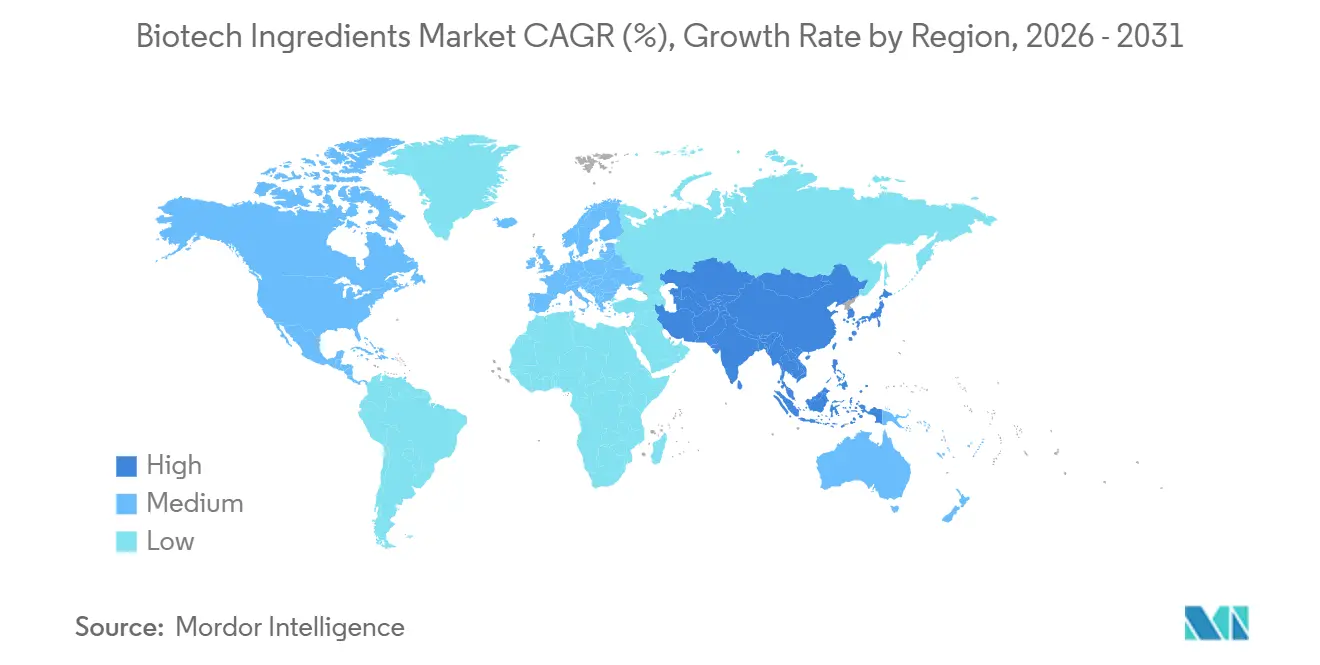

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biotech Ingredients Market Analysis by Mordor Intelligence

The Biotech Ingredients Market size is projected to expand from USD 2.45 billion in 2025 and USD 2.63 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 8.03% between 2026 to 2031.

The biotech ingredients market is moving toward biologically engineered production routes as manufacturers across pharmaceuticals, food, cosmetics, and agriculture reduce dependence on petrochemical synthesis and conventional extraction methods. This shift is strengthening demand for fermentation platforms, synthetic biology tools, and integrated downstream capabilities that can deliver purity, traceability, and more stable supply outcomes. The biotech ingredients market is also seeing a clear move toward value-added formats, as producers invest beyond core production into formulation, finished specifications, and closer alignment with end-use customer requirements. Competitive positioning in the biotech ingredients market is increasingly tied to ownership of microbial strains, scale-ready fermentation assets, and internal process development, which gives established suppliers an advantage in speed, cost control, and regulatory execution. Feedstock volatility, scale-up risk, purification complexity, and strain-specific licensing still create friction, yet the biotech ingredients market remains supported by a wide application base that spans clinical, nutritional, cosmetic, and agricultural uses.

Key Report Takeaways

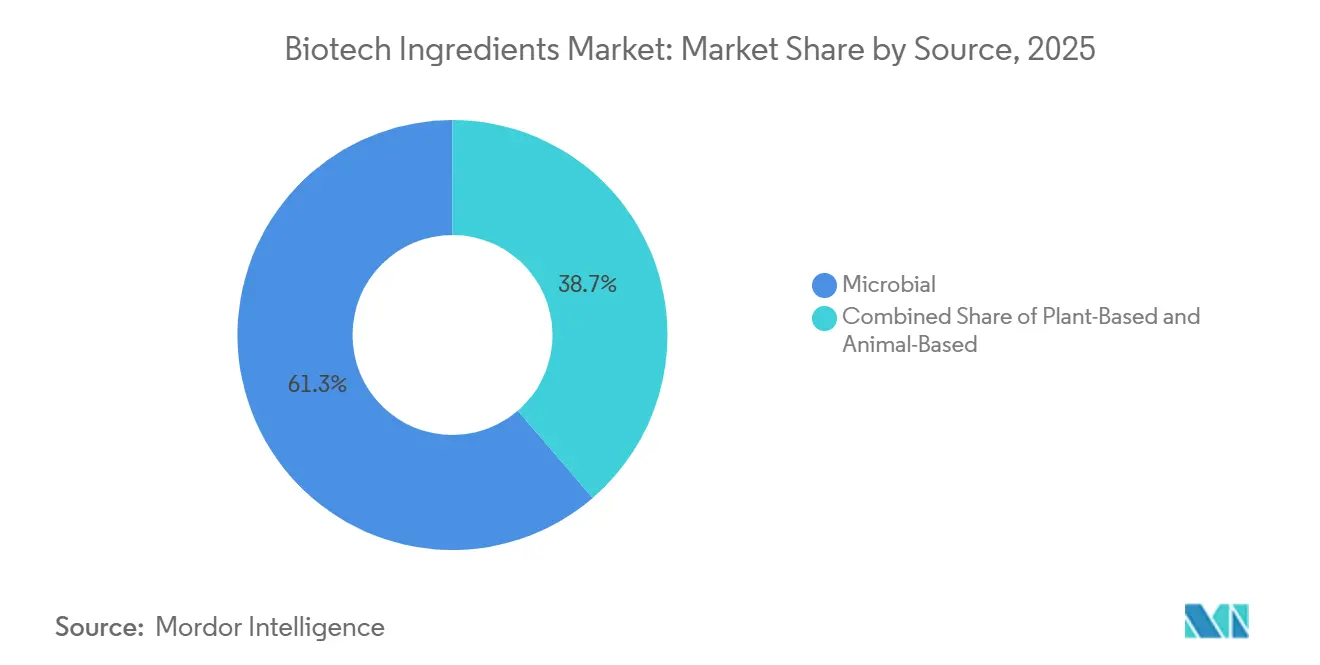

- By source, microbial ingredients led with 61.31% of the global total in 2025, while animal-based ingredients are projected to record the fastest growth at 8.68% through 2031.

- By ingredient type, enzymes held the largest share at 29.68% in 2025, while proteins and peptides are forecast to expand at 10.12% through 2031.

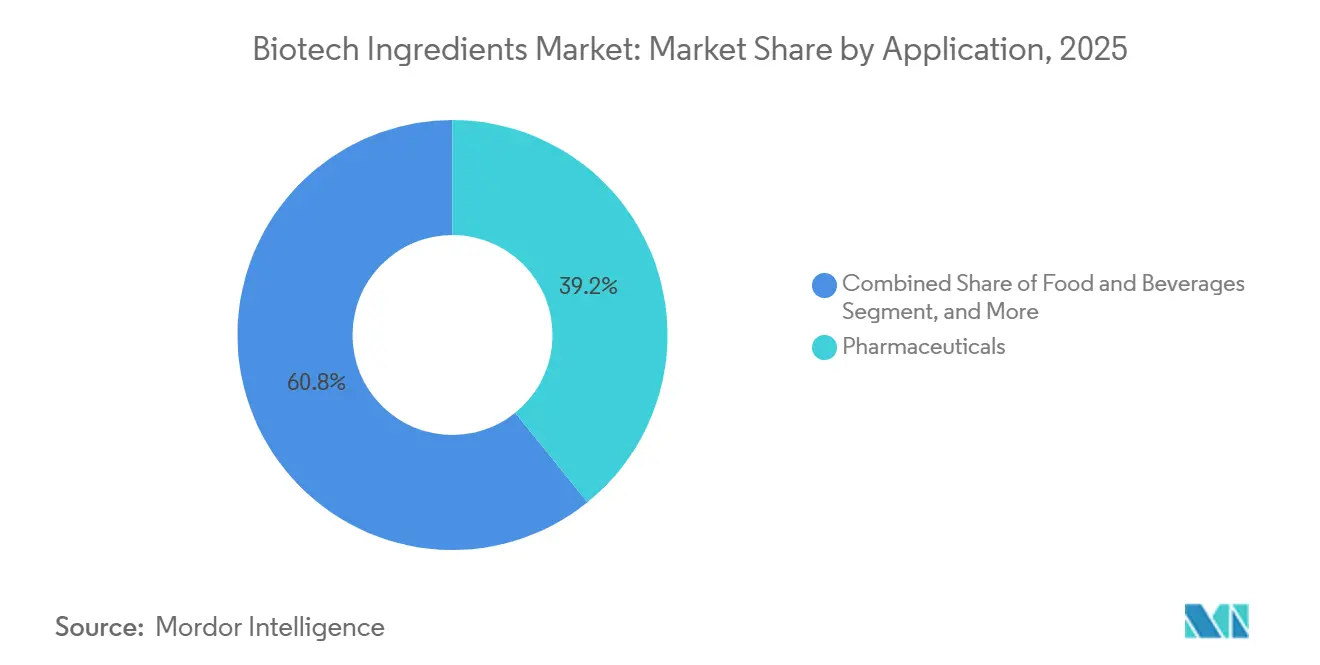

- By application, pharmaceuticals accounted for 39.16% of demand in 2025, while plant nutrition and health care are projected to grow the fastest at 9.34% through 2031.

- By technology, fermentation commanded 33.62% of the biotech ingredients market size in 2025, while synthetic biology is projected to advance at 10.98% through 2031.

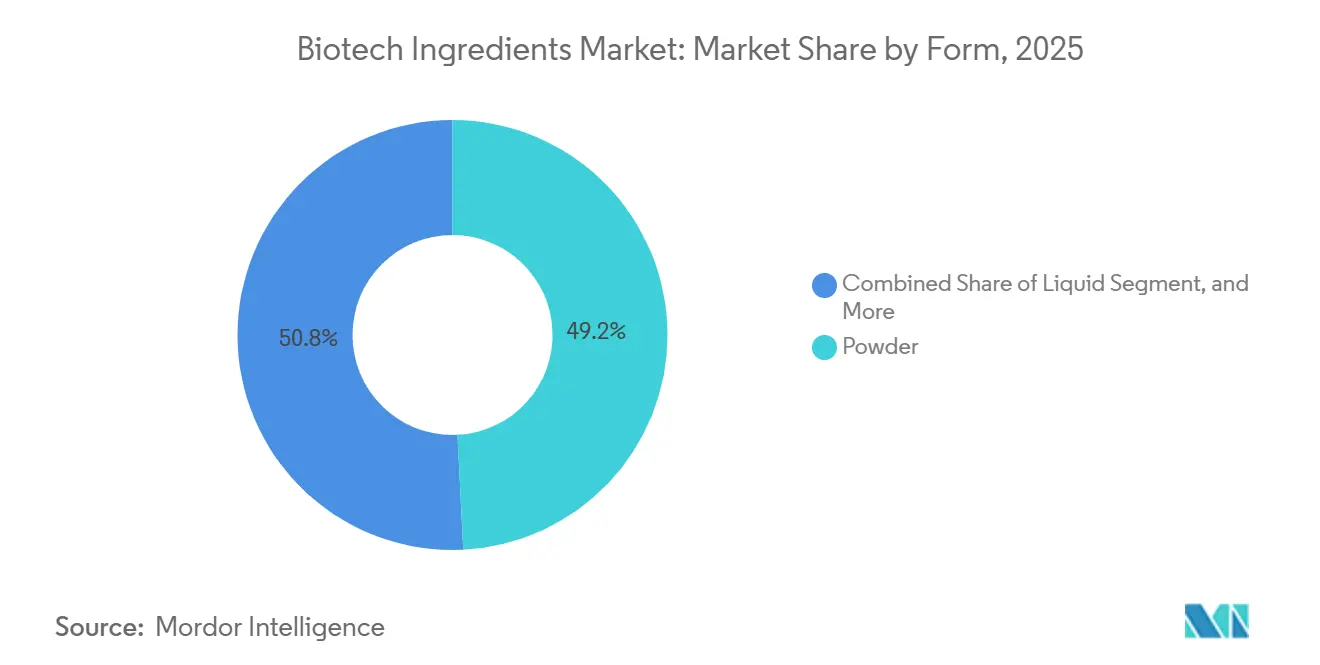

- By form, powder represented 49.19% of the market in 2025, while liquid format is expected to grow at 8.57% through 2031.

- By process, downstream processing held 32.83% of the market in 2025, while formulation is projected to grow at 9.66% through 2031.

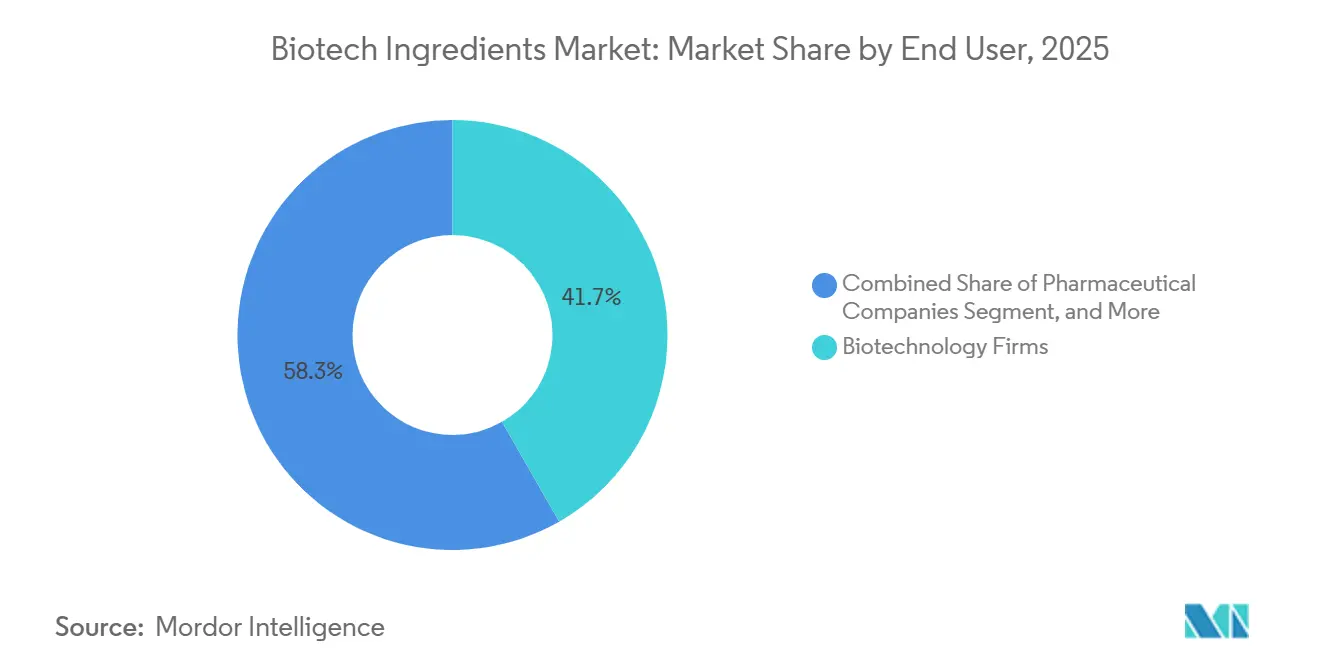

- By end user, biotechnology firms held 41.74% of the biotech ingredients market share in 2025, while research institutes are expected to expand at 8.36% through 2031.

- By geography, North America led with 43.64% in 2025, while Asia-Pacific is forecast to record the highest regional CAGR at 9.96% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Biotech Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Shift Toward Bio-Based Formulation Substitution in Cosmetics and Personal Care | +1.1% | Europe and North America | Medium term (2-4 years) |

| Expansion of Precision Fermentation Platforms for High-Value Functional Ingredients | +1.8% | Global, with early adoption in North America and Europe | Short term (≤ 2 years) |

| Biomanufacturing Capacity Buildout for Non-Pharma Ingredient Supply Security | +1.1% | Asia-Pacific core, with spillover to Latin America | Medium term (2-4 years) |

| Clean Label and Allergen-Reduction Pressure in Food, Flavor, and Fragrance Formulations | +0.8% | North America and Europe | Short term (≤ 2 years) |

| Regulatory Preference for Naturally Derived and Traceable Inputs in Premium Consumer Goods | +0.7% | Europe, with spillover to North America and Asia-Pacific | Long term (≥ 4 years) |

| Rising Demand for Biotech-Derived Therapeutic and Nutritional Ingredients in High-Value Health Segments | +1.4% | Global, strongest in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Precision Fermentation Platforms for High-Value Functional Ingredients

The biotech ingredients market is seeing precision fermentation replace conventional extraction in a growing number of high-value molecules. Engineered microbial hosts are now being used to produce hyaluronic acid, squalane, recombinant collagen, and resveratrol at commercially relevant yields.[1]Ishani Bhatt and Sonal Patel, “Precision Fermentation as a Tool for Sustainable Cosmetic Ingredient Production,” Applied Sciences, mdpi.com Research published in Applied Sciences in 2025 showed that engineered Bacillus subtilis strains delivered hyaluronic acid yields above 7 g/L in 11 hours, which cut fermentation time sharply versus conventional Streptococcus processes while also improving purity and reducing purification burden. The same production shift is improving cost competitiveness, as fermentation-derived squalane is priced below olive-derived alternatives, making supply substitution easier for personal care formulators without forcing product redesign. The OECD also noted in 2025 that AI and machine learning are reducing development time by as much as 70%, which is improving the economics of fast-cycle molecule development and favoring early platform leaders in the biotech ingredients market.

Rising Shift Toward Bio-Based Formulation Substitution in Cosmetics and Personal Care

The biotech ingredients market is gaining support from personal care brands that are replacing conventional inputs with bio-based alternatives. Consumer sustainability preferences in Europe have become strong enough to shape active reformulation programs at major cosmetics companies, which is pushing ingredient suppliers toward biotechnology-backed solutions. Evonik showed this direction clearly at in-cosmetics Global 2025, where it highlighted biotechnology-based biosurfactants, biopolymers, vegan collagen, and ceramides, and reported a climate footprint reduction above 60% for selected enzymatically produced emollients compared with chemical process alternatives.[2]Evonik Industries AG, “In-Cosmetics Global 2025, Evonik Meets Growing Customer Demand for High-Performance, Eco-Friendly Solutions,” Evonik, evonik.com BASF also expanded its Isobionics portfolio in March 2025 with two fermentation-derived flavor ingredients that offer consistent purity and more reliable supply than agricultural extraction routes. In the biotech ingredients market, this move is not only about sustainability, because brands also want steadier quality, fewer seasonal disruptions, and better traceability under tighter compliance frameworks in premium beauty and personal care channels.

Biomanufacturing Capacity Buildout for Non-Pharma Ingredient Supply Security

The biotech ingredients market is also being shaped by investment in non-pharma production capacity, as suppliers try to reduce logistics exposure and regional concentration risk. In April 2026, Novonesis acquired a production facility in Rayong, Thailand, for USD 50 million, which expanded its fermentation footprint in Southeast Asia and aligned with its long-term growth push in emerging markets. Givaudan opened its White Biotechnology Innovation Center in Toulouse in 2025, bringing fermentation labs and biocatalysis development into one site so that the company can tighten the link between discovery, development, and scale-up. Amyris added a fourth precision fermentation line at its Barra Bonita facility in Brazil in March 2026, which showed that scale investment is spreading beyond traditional pharmaceutical manufacturing clusters. As the biotech ingredients market expands, companies with dedicated internal capacity are in a stronger position in terms of speed, purity control, and customer responsiveness than suppliers that still depend heavily on third-party tolling arrangements.

Rising Demand for Biotech-Derived Therapeutic and Nutritional Ingredients in High-Value Health Segments

The biotech ingredients market is benefiting from demand for therapeutic and nutrition-focused molecules that need higher purity, stronger traceability, and more consistent functional performance. Precision fermentation is widening the addressable set of proteins, peptides, and bioactive compounds that can serve medical nutrition, pharmaceutical diagnostics, and other regulated health applications. This is reinforcing demand for animal-identical and fermentation-derived inputs that can meet strict specification needs without the sourcing variability tied to conventional animal extraction. AbbVie’s Q1 2026 announcement of a USD 380 million investment in new API manufacturing facilities highlighted the level of capital now being directed into biotechnology-enabled manufacturing systems that support high-value therapeutic production.[3]AbbVie Inc., “AbbVie Reports First-Quarter 2026 Financial Results,” AbbVie Investor Relations, abbvie.com In the biotech ingredients market, that same production logic supports stronger returns when one platform can serve multiple premium channels, especially where clinical, nutritional, and beauty use cases increasingly overlap.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Scale-Up Failure Risk Between Lab, Pilot, and Commercial Fermentation | -0.9% | Global | Short term (≤ 2 years) |

| Downstream Purification Complexity for Multi-Compound Ingredient Streams | -0.7% | Global | Medium term (2-4 years) |

| Feedstock Volatility for Sugar, Oil, and Waste-Carbon Inputs | -0.6% | Asia-Pacific and Latin America, with global supply chain spillover | Short term (≤ 2 years) |

| IP Friction and Strain-Specific Licensing Constraints in Engineered Biology | -0.5% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Scale-Up Failure Risk Between Lab, Pilot, and Commercial Fermentation

The biotech ingredients market still faces a major hurdle when laboratory performance must be reproduced in pilot and commercial systems. The OECD described this transition as a persistent structural bottleneck in synthetic biology, affecting both early-stage companies and larger producers. Oxygen transfer, shear stress, pH behavior, and nutrient distribution change in larger bioreactors, which often makes laboratory benchmarks unreliable at full scale. Genetic instability adds another problem, because engineered strains can lose or silence target traits during longer commercial runs, which reduces yields and raises batch failure risk. The pressure is greater for smaller companies in the biotech ingredients market, because repeated scale-up setbacks consume cash, extend launch timelines, and require engineering capabilities that are usually stronger at incumbent manufacturers.

Downstream Purification Complexity for Multi-Compound Ingredient Streams

The biotech ingredients market also faces cost pressure in downstream purification, especially for complex ingredient streams produced through metabolic engineering and synthetic biology. Applied Sciences reported in 2025 that downstream processing can account for most of the total production cost in cosmetic-grade biotech ingredients, particularly when residual host proteins, mycotoxins, or endotoxins must be removed through several stages. These requirements increase solvent, energy, and water use, which places pressure on both margins and operating efficiency. Advanced bioseparation tools such as single-use chromatography, tangential flow filtration, and membrane crystallization are becoming important profit differentiators even when upstream fermentation performance looks similar. In the biotech ingredients market, suppliers without strong internal downstream engineering capabilities remain at a cost and quality disadvantage in pharmaceutical and premium cosmetic applications, where purity thresholds are difficult to negotiate downward.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Microbial Platforms Command Volume as Animal-Identical Precision Fermentation Redefines the Animal-Based Segment

Microbial ingredients accounted for 61.31% of the biotech ingredients market size in 2025, which reflected long-standing industrial investment in yeast, bacterial, and fungal production hosts across enzymes, amino acids, vitamins, and organic acids. This scale advantage came from decades of fermentation learning, established production infrastructure, and broad regulatory familiarity across end-use sectors. In the biotech ingredients market, microbial sourcing remains the most commercially proven route for high-volume output because it combines flexibility with reliable economics across many standardized ingredient categories. The segment also benefits from compatibility with both commodity and specialty product pipelines, which gives producers room to allocate capacity based on changing demand profiles.

Novonesis remains a major anchor in this segment after the merger of Novozymes and Chr. Hansen, and its production network widened further with the Rayong facility acquisition in 2026. Plant-based sourcing still holds a differentiated position in biotech ingredients tied to alkaloids, terpenoids, and glycosides where traceable natural origin matters to buyers and can support premium pricing. Animal-based sourcing is the fastest-growing source segment, with the biotech ingredients market size for this segment expected to expand at 8.68% CAGR between 2026 and 2031. That growth is increasingly tied to recombinant collagen, lactoferrin, and other animal-identical proteins produced through microbial fermentation rather than conventional animal extraction, which changes the meaning of the category without changing the functional value that customers want.

By Ingredient Type: Enzymes Drive Volume, Proteins and Peptides Lead Value Growth

Enzymes held the largest ingredient-type share at 29.68% in 2025, which kept them at the center of the biotech ingredients market because they remain essential in detergents, food processing, pharmaceutical production, and industrial biotechnology. Their position is supported by repeat-use demand, well-established customer qualification cycles, and strong compatibility with microbial production platforms. In the biotech ingredients market, enzymes also benefit from a wide spread of applications, which reduces dependence on any one downstream customer group. That base makes the category stable even as newer bioactive segments attract more attention and capital.

Proteins and peptides are projected to grow at 10.12% through 2031, making them the fastest-growing ingredient category in the biotech ingredients market. This growth reflects rising commercial use in medical beauty, infant and clinical nutrition, diagnostics, and premium performance nutrition. Dyadic International’s AlbuFree DX launch showed how recombinant albumin is moving historically familiar molecules into higher-value, animal-free, specification-driven use cases. BASF and IFF also expanded work on next-generation enzyme systems in 2025, which showed that established players are still investing in foundational categories even while higher-growth protein platforms gain share. Amino acids remain important as the second-largest category, while vitamins, organic acids, polysaccharides, terpenoids, alkaloids, and glycosides continue to diversify demand across flavors, fragrances, agriculture, and nutraceutical channels. Collagen and gelatin are in transition, because conventional animal-derived volumes remain relevant in food and pharmaceuticals, but recombinant and fermentation-derived collagen is expanding in high-value cosmetic and medical use cases where purity and consistency matter more.

By Application: Pharmaceuticals Anchor Volumes as Agrobiologicals Define the Growth Frontier

Pharmaceuticals represented 39.16% of the biotech ingredients market share in 2025, which kept them as the largest application segment. This leadership reflects deep dependence on fermentation-derived APIs, excipients, biologic precursors, and tightly specified processing inputs. The biotech ingredients market continues to draw support from pharmaceutical demand because this segment values reproducibility, purity, and supply assurance, all of which reward suppliers with strong process control. AbbVie’s 2026 decision to invest USD 380 million in new API manufacturing capacity showed that major drug producers are still expanding biotechnology-enabled production systems at scale.

Plant nutrition and health care is projected to grow at 9.34% through 2031, making it the fastest-growing application in the biotech ingredients market. Growth in this segment is supported by demand for biopesticides, biostimulants, and soil-active biological inputs that can deliver targeted performance under tighter residue and sustainability requirements. Food and beverages remain an important demand channel for enzymes, amino acids, vitamins, and fermentation-derived aroma compounds, even as price competition remains visible in some standardized categories. Personal care and cosmetics are expanding on the back of biotechnology-based bioactives, with Evonik and Symrise both showing how bio-derived formulations are moving deeper into premium beauty pipelines. Animal nutrition and health care, along with medical beauty, are smaller segments by volume, yet they remain strategically important because they absorb differentiated molecules with stronger pricing power and more specialized performance claims.

By Technology: Fermentation Anchors Commercial Scale as Synthetic Biology Resets the Innovation Curve

Fermentation accounted for 33.62% of the biotech ingredients market size in 2025, which kept it as the largest production technology. This position rests on mature infrastructure, established economics, and wide regulatory acceptance across amino acids, enzymes, vitamins, and organic acids. In the biotech ingredients market, fermentation remains the commercial backbone because it can support both high-volume output and complex specialty molecules when paired with advanced strain engineering. Its leadership also reflects the installed asset base that incumbent producers already operate across major regions.

Synthetic biology is projected to grow at 10.98% through 2031, making it the fastest-growing technology in the biotech ingredients market. This reflects tighter integration of AI-led strain design, genome editing, and automated screening into molecule development workflows. Ginkgo Bioworks reported in February 2026 that its GPT-5-driven autonomous laboratory improved cell-free protein synthesis efficiency by 40%, which showed how AI-biology convergence is starting to reshape development speed and cost structure. Biocatalysis continues to serve highly selective applications, while metabolic engineering expands the range of molecules that can be produced in standard hosts. Cell culture and genetic engineering remain important enabling technologies, especially in recombinant proteins and biologic precursor systems, where technical performance matters as much as scale.

By Form: Powder Dominates Logistics, Liquid Gains Ground in High-Bioavailability Actives

Powder accounted for 49.19% of the biotech ingredients market in 2025, which made it the leading form because it simplifies transport, extends shelf life, and supports global trade in enzymes, amino acids, and vitamin concentrates. Powder also reduces sensitivity to moisture and spoilage, which makes it the practical choice for long-distance movement across global supply chains. In the biotech ingredients market, formulators continue to favor powder when stability, storage flexibility, and easier inventory management matter more than immediate processing convenience. This explains why the form remains dominant across several standardized and semi-specialized ingredient categories.

Liquid is projected to grow at 8.57% through 2031, making it the fastest-growing form in the biotech ingredients market. This reflects rising use of ready-to-use enzyme concentrates, cosmetic actives, and serum-format ingredients that perform best in solution and reduce reconstitution steps during manufacturing. Growth in liquid formats is being helped by improvements in cold-chain logistics, especially in emerging markets where better distribution systems are reducing spoilage risk and widening commercial reach. Granules and pellets remain relevant in plant and animal nutrition applications, where handling performance and controlled release matter more than solubility. The shift toward liquid also fits personal care formulation trends, because many fermentation-derived actives can move more directly into finished products when they are delivered in stabilized solution form.

By Process: Downstream Processing Holds Share as Formulation Captures Margin

Downstream processing held 32.83% of the market among process categories in 2025, which reflected the cost and technical weight of separation, filtration, crystallization, and drying in biotech ingredient production. This category remains central because high-purity applications in pharmaceuticals and cosmetics place strict demands on impurity removal and final specification control. In the biotech ingredients market, downstream steps often determine whether an otherwise successful fermentation process can achieve acceptable commercial margins. That makes process capability an important competitive factor, especially for suppliers serving regulated or premium applications.

Formulation is expected to grow at 9.66% through 2031, making it the fastest-growing process category in the biotech ingredients market. Producers are expanding into blending, encapsulation, and microencapsulation so they can sell more finished and application-ready ingredients rather than basic intermediates. This shift allows suppliers to capture more value per unit and reduce the reformulation burden for customers. It also gives vertically integrated producers a stronger position when they need to support performance, stability, and sustainability claims with full process control. Upstream processing and specialized purification continue to matter, but the direction of travel is clearly toward higher-value finished specifications that sit closer to the customer’s final use case.

By End User: Biotechnology Firms Lead Consumption as Research Institutes Drive Exploratory Demand

Biotechnology firms represented 41.74% of the biotech ingredients market share in 2025, which made them the largest end-user group. Their demand base covers amino acids, vitamins, enzymes, recombinant proteins, and other inputs used in bioprocess development, cell culture media, and GMP manufacturing workflows. The biotech ingredients market depends heavily on this customer set because biotechnology firms require consistent quality, repeatable batch performance, and close technical alignment with evolving R&D programs. Pharmaceutical companies remain the second-largest end-user category, supported by ongoing requirements in API production, excipient sourcing, and biologic precursor systems.

Research institutes are projected to grow at 8.36% through 2031, making them the fastest-growing end-user segment in the biotech ingredients market. Their role is important because early work in strain discovery, pathway validation, and proof-of-concept process development often feeds directly into later commercial agreements with ingredient suppliers and specialty manufacturers. Contract research organizations remain smaller by volume, yet they matter strategically because they help qualify performance, support dossier development, and prepare ingredients for scale-up and commercialization. The OECD noted in 2025 that underfunding of research institutes could weaken long-term innovation pipelines, which means continued public support remains relevant to future molecule development in the biotech ingredients market. Together, these end users show that demand is concentrated not only in mature production systems, but also in the research networks that feed future commercial portfolios.

Geography Analysis

North America held 43.64% of the biotech ingredients market share in 2025, which kept it as the largest regional market. This position rests on strong pharmaceutical biomanufacturing capacity, established fermentation infrastructure, and an innovation ecosystem that still supports commercialization of new biotech-derived actives. AbbVie’s USD 380 million investment in new API manufacturing facilities in Q1 2026 showed that large-scale capacity expansion is still active in the region. North America also benefits from a dense base of ingredient developers, specialty manufacturers, and platform technology companies that can support scale-up, qualification, and downstream application work. In the biotech ingredients market, this combination of production depth and financing capacity continues to favor North America in high-value therapeutic, nutritional, and industrial ingredient categories.

Asia-Pacific is projected to grow at 9.96% through 2031, making it the fastest-growing region in the biotech ingredients market. Growth is being supported by capacity expansion in China, India’s contract biotechnology manufacturing base, and new facility investment across Southeast Asia. Novonesis’ Rayong acquisition in Thailand is a clear example of how suppliers are positioning for regional feedstock access, lower operating costs, and faster delivery into local demand centers. Japan and South Korea add strength in high-value amino acid, vitamin, and personal care bioactive development, which supports regional depth beyond volume manufacturing.

Europe remains a major center in the biotech ingredients market because it combines industrial biotechnology capability with strong customer demand for traceable and sustainability-backed inputs. Evonik, BASF, and related suppliers continue to anchor enzyme, amino acid, and personal care ingredient supply across the region. Givaudan’s White Biotechnology Innovation Centre in Toulouse strengthened France’s position in advanced fragrance and beauty bioactives. South America is increasingly relevant as a production base, with Amyris expanding precision fermentation capacity in Brazil on the back of feedstock and cost advantages. The Middle East and Africa remain at an earlier stage, yet demand is rising in food security, nutraceutical, and pharmaceutical inputs, even though the region still depends more on imports than local production.

Competitive Landscape

The biotech ingredients market shows moderate concentration in enzymes, amino acids, and industrial vitamins, where large incumbents benefit from proprietary strains, installed fermentation assets, and established customer relationships. Novonesis, BASF, Evonik Industries, dsm-firmenich, and IFF remain the most visible large players across the broader biotech ingredients market because they combine scale with technical breadth. Their position is strengthened by internal R&D, global logistics capabilities, and the ability to serve multiple end-use sectors from the same production base. Even so, the biotech ingredients market is more fragmented in higher-value proteins, terpenoids, and specialized aroma compounds, where specialist companies can still defend premium niches. That split means competition is not uniform, because leadership is stronger in mature categories than in emerging precision-fermented bioactives.

Strategic portfolio moves are reshaping the biotech ingredients market. dsm-firmenich announced in 2026 that it would divest its Animal Nutrition and Health business to CVC Capital Partners, sharpening its focus on nutrition, health, and beauty ingredients. Novonesis agreed in 2025 to acquire dsm-firmenich’s stake in the Feed Enzyme Alliance, which tightened its control over enzyme sales and value-chain integration. BASF and IFF also entered a strategic collaboration in 2025 to accelerate next-generation enzyme and polymer development, which showed how large incumbents are still using partnerships to extend platform depth.

The biotech ingredients market is also drawing pressure from platform specialists that compete on both molecule performance and manufacturing control. Amyris has continued to build internal precision fermentation capability in Brazil, while Ginkgo Bioworks is pushing AI-enabled laboratory workflows that could reduce development time for customers without full in-house design capability. CIR’s 2025 safety assessment of four Lactobacillus ferment ingredients for cosmetic use in the United States also showed how safety documentation can widen the addressable set of commercial ingredients and favor early compliant suppliers. Novonesis reported 7% organic sales growth and a 37.1% adjusted EBITDA margin in its 2025 annual report, which sets a demanding performance benchmark for smaller competitors in the biotech ingredients market.

Biotech Ingredients Industry Leaders

dsm-firmenich

Evonik Industries AG

Givaudan

Merck KGaA

Novozymes A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Novonesis acquired a production facility in Rayong, Thailand from Meihua for USD 50 million, expanding Southeast Asian fermentation capacity in alignment with its GROW strategy toward 2030, which targets emerging markets as a key growth driver.

- March 2026: Amyris launched a fourth precision fermentation line at its Barra Bonita, Brazil facility, adding a 2×80 m³ configuration to three existing 2×200 m³ lines to enable more agile commercial-scale production of specialty molecules across flavor, fragrance, agriculture, and personal care applications.

- February 2026: Ginkgo Bioworks and OpenAI reported a 40% improvement in cell-free protein synthesis efficiency through a GPT-5-driven autonomous laboratory, reducing reaction costs and showing that AI-directed biological experimentation can compress biotech ingredient development timelines.

- February 2026: dsm-firmenich announced the divestment of its Animal Nutrition and Health business to CVC Capital Partners, refocusing its portfolio on consumer nutrition, health, and beauty ingredient categories.

Global Biotech Ingredients Market Report Scope

Biotech ingredients are substances derived from biological sources such as microorganisms, plants, or animal cells using advanced processes like genetic engineering, cell culture, and precision fermentation. These lab-developed compounds replace synthetic or animal-based materials, providing highly sustainable, consistent, and eco-friendly alternatives across various industries.

The Biotech Ingredients Market is segmented by source, ingredient type, application, technology, form, process, end user, and geography. By source, biotech ingredients are derived from Microbial, Plant-Based, and Animal-Based origins. By ingredient type, the market includes Enzymes, Amino Acids, Organic Acids, Proteins and Peptides, Collagen and Gelatin, Vitamins, Terpenoids, Alkaloids, Glycosides, and Polysaccharides. By application, biotech ingredients are used in Pharmaceuticals, Food and Beverages, Personal Care and Cosmetics, Plant Nutrition and Health Care, Animal Nutrition and Health Care, and Medical Beauty. By technology, production methods include Fermentation, Biocatalysis, Cell Culture, Genetic Engineering, Synthetic Biology, and Metabolic Engineering. By form, biotech ingredients are available as Liquid, Powder, Granule, and Pellet. By process, the market is segmented into Upstream Processing, Downstream Processing, Formulation, and Purification. By end user, biotech ingredients are utilized by Pharmaceutical Companies, Biotechnology Firms, Research Institutes, and Contract Research Organizations.

Geographically, the market spans North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, Rest of Middle_East & Africa), and South America (Brazil, Argentina, Rest of South America).

| Microbial |

| Plant-Based |

| Animal-Based |

| Enzymes |

| Amino Acids |

| Organic Acids |

| Proteins and Peptides |

| Collagen and Gelatin |

| Vitamins |

| Terpenoids |

| Alkaloids |

| Glycosides |

| Polysaccharides |

| Pharmaceuticals |

| Food and Beverages |

| Personal Care and Cosmetics |

| Plant Nutrition and Health Care |

| Animal Nutrition and Health Care |

| Medical Beauty |

| Fermentation |

| Biocatalysis |

| Cell Culture |

| Genetic Engineering |

| Synthetic Biology |

| Metabolic Engineering |

| Liquid |

| Powder |

| Granule |

| Pellet |

| Upstream Processing |

| Downstream Processing |

| Formulation |

| Purification |

| Pharmaceutical Companies |

| Biotechnology Firms |

| Research Institutes |

| Contract Research Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Microbial | |

| Plant-Based | ||

| Animal-Based | ||

| By Ingredient Type | Enzymes | |

| Amino Acids | ||

| Organic Acids | ||

| Proteins and Peptides | ||

| Collagen and Gelatin | ||

| Vitamins | ||

| Terpenoids | ||

| Alkaloids | ||

| Glycosides | ||

| Polysaccharides | ||

| By Application | Pharmaceuticals | |

| Food and Beverages | ||

| Personal Care and Cosmetics | ||

| Plant Nutrition and Health Care | ||

| Animal Nutrition and Health Care | ||

| Medical Beauty | ||

| By Technology | Fermentation | |

| Biocatalysis | ||

| Cell Culture | ||

| Genetic Engineering | ||

| Synthetic Biology | ||

| Metabolic Engineering | ||

| By Form | Liquid | |

| Powder | ||

| Granule | ||

| Pellet | ||

| By Process | Upstream Processing | |

| Downstream Processing | ||

| Formulation | ||

| Purification | ||

| By End User | Pharmaceutical Companies | |

| Biotechnology Firms | ||

| Research Institutes | ||

| Contract Research Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the biotech ingredients sector by 2031?

The biotech ingredients market is forecast to reach USD 3.87 billion by 2031, rising from USD 2.63 billion in 2026 at an 8.03% CAGR over the forecast period.

Which application area currently leads demand for biotech ingredients?

Pharmaceuticals led demand in 2025 with a 39.16% share, supported by ongoing use of fermentation-derived APIs, excipients, and biologic precursors.

Which technology is growing the fastest in biotech ingredient production?

Synthetic biology is projected to grow the fastest at 10.98% through 2031 as AI-led strain design, genome editing, and automated screening improve development speed.

Why do microbial sources dominate biotech ingredient supply?

Microbial sources led with 61.31% in 2025 because they benefit from established fermentation infrastructure, wide regulatory familiarity, and broad applicability across major ingredient classes.

Which region is expected to expand the fastest through 2031?

Asia-Pacific is projected to grow the fastest at 9.96% CAGR through 2031, supported by capacity additions in China, India, and Southeast Asia.

What is the main operational risk in scaling biotech ingredient production?

Scale-up failure between lab, pilot, and commercial fermentation remains the most important risk because larger bioreactors can change oxygen transfer, strain stability, and product consistency.

Page last updated on: