Medical Enzyme Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 5.05 Billion |

| Market Size (2030) | USD 6.77 Billion |

| Growth Rate (2025 - 2030) | 6.06% CAGR |

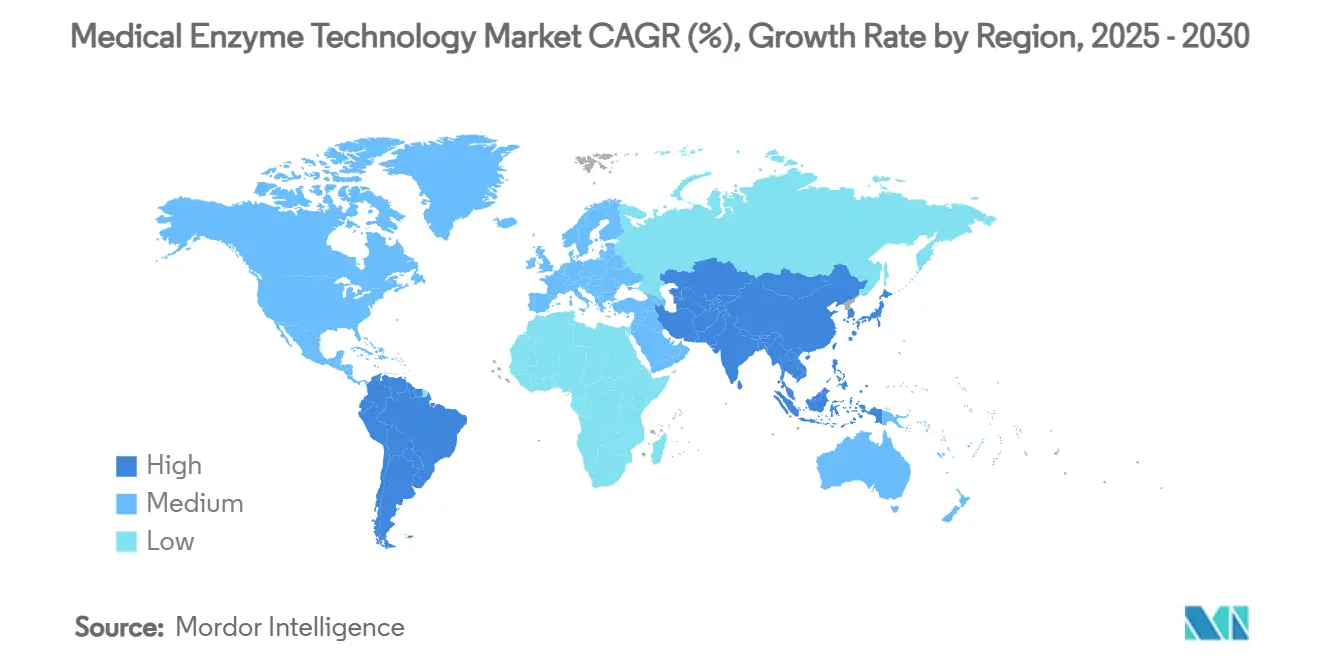

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

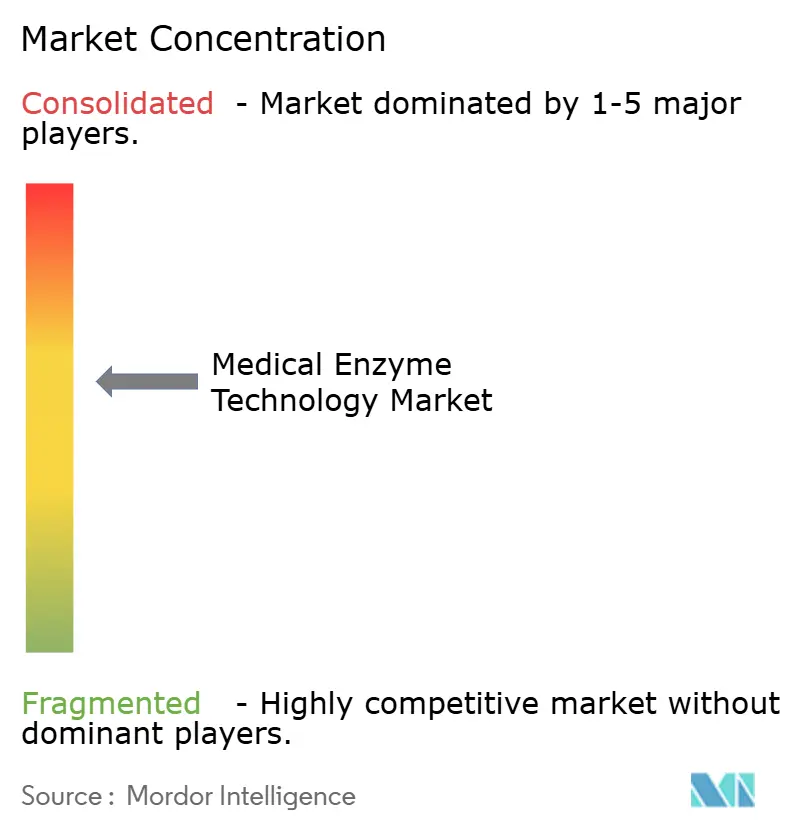

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Medical Enzyme Technology Market Analysis by Mordor Intelligence

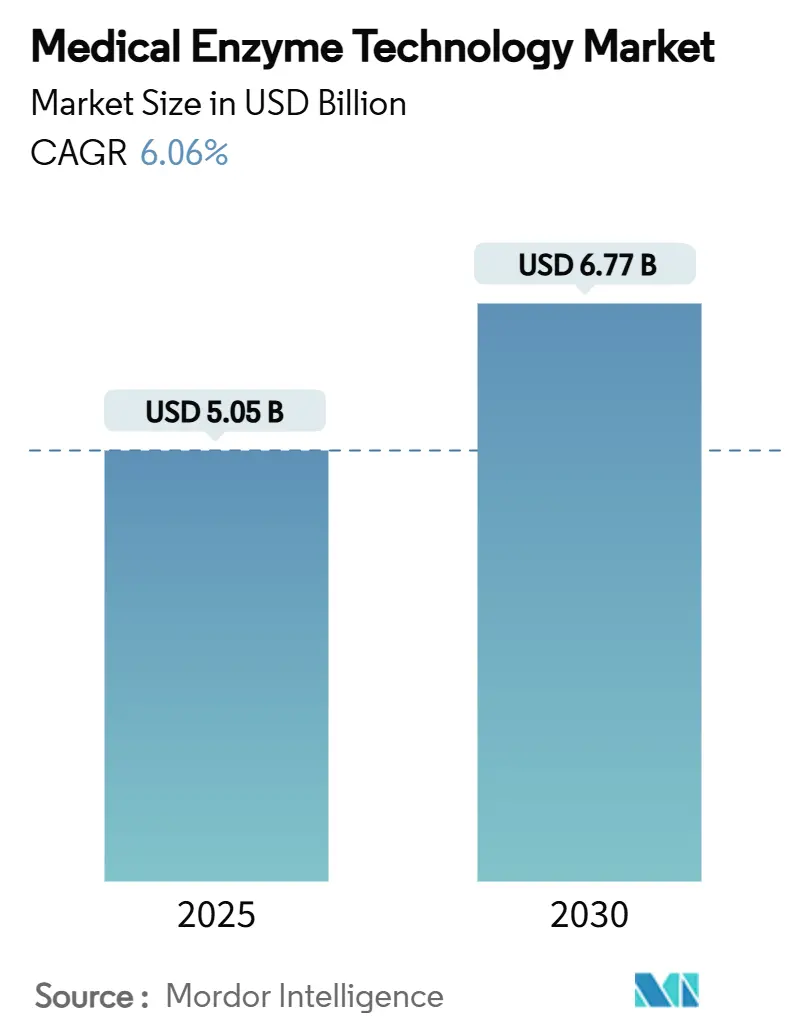

The medical enzyme technology market size is valued at USD 5.05 billion in 2025 and is forecast to reach USD 6.77 billion by 2030, reflecting a 6.06% CAGR over the period. The medical enzyme technology market is evolving beyond traditional diagnostic roles as recombinant engineering, artificial intelligence‐guided biocatalyst design, and continuous manufacturing move into routine practice. Growing demand stems from rising chronic disease incidence, the spread of point-of-care platforms, and sustained investment in advanced therapy manufacturing. Technology differentiation, particularly through AI-assisted protein modeling, is widening competitive gaps among suppliers. Supply chain vulnerabilities for rare cofactors and elongated multi-regional approval timelines temper momentum, yet sustained public and private R&D funding keeps long-term prospects positive.

Key Report Takeaways

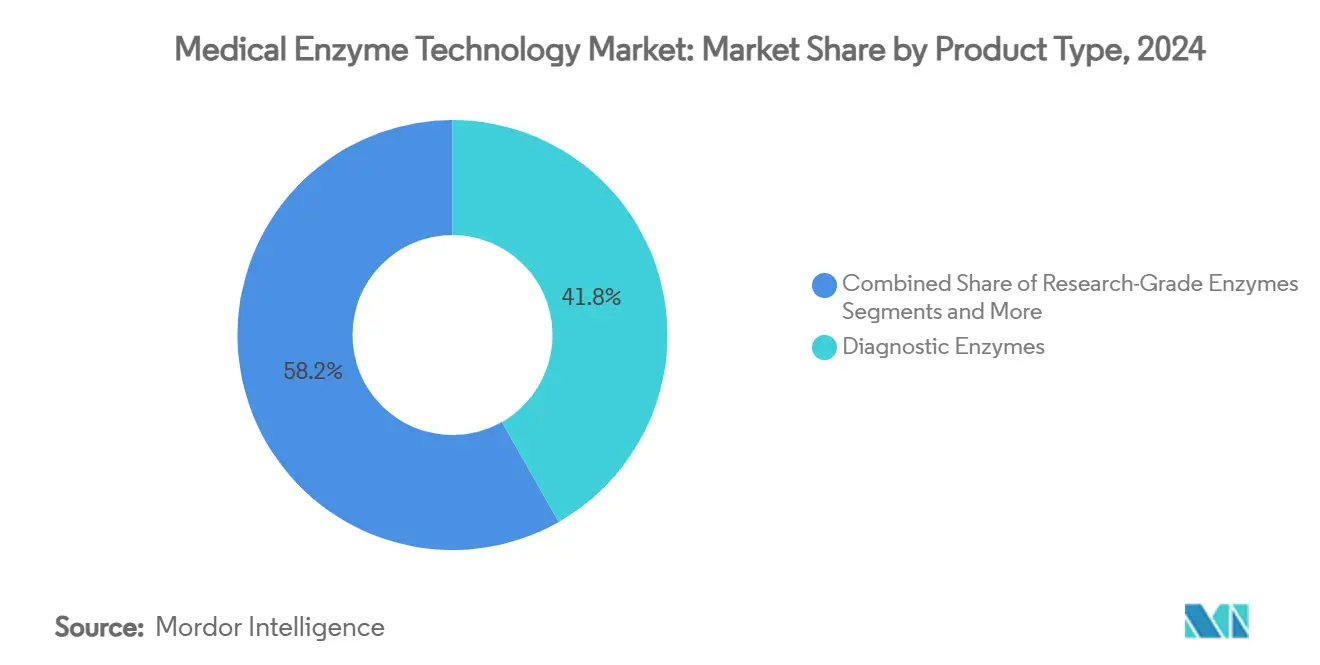

- By product type, diagnostic enzymes held 41.77% of the medical enzyme technology market share in 2024, while therapeutic enzymes are advancing at a 10.34% CAGR through 2030.

- By application, disease diagnostics accounted for 39.68% of the medical enzyme technology market size in 2024 and gene editing and molecular diagnostics are projected to expand at 10.88% CAGR to 2030.

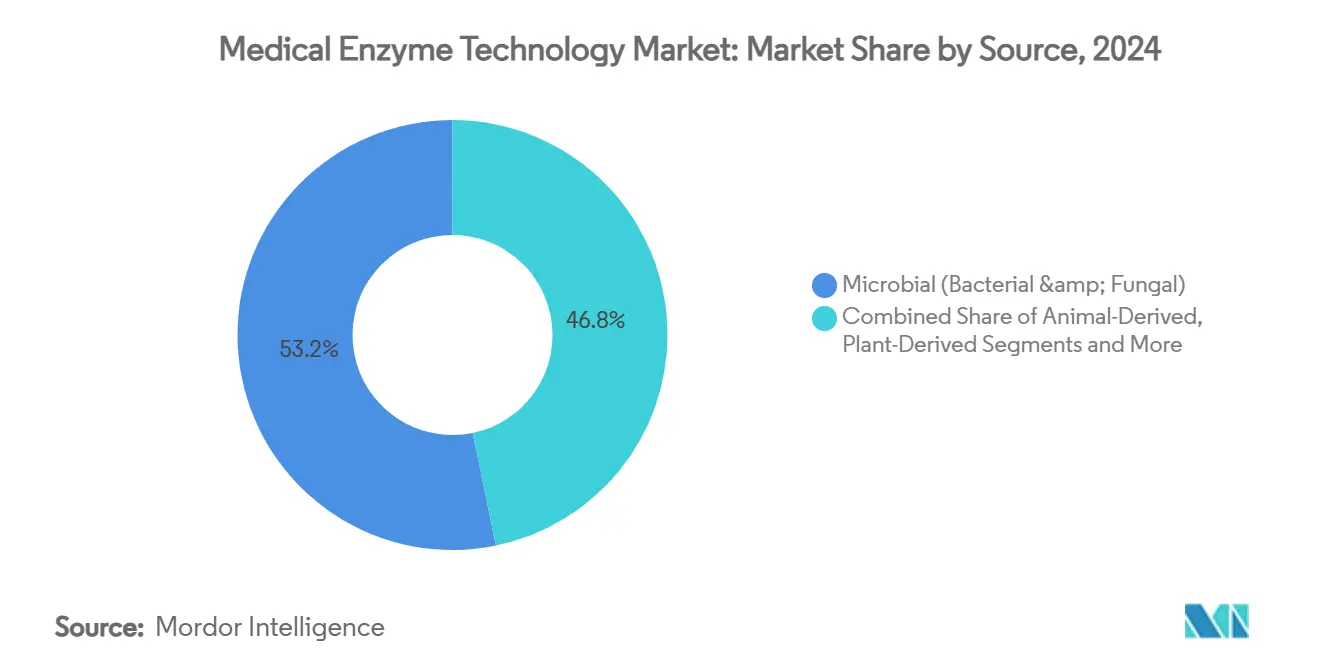

- By source, microbial systems captured 53.23% share of the medical enzyme technology market size in 2024, while recombinant and engineered enzymes are growing at 9.24% CAGR.

- By end user, hospitals and diagnostic laboratories held 41.18% of the medical enzyme technology market size in 2024; point-of-care settings record the highest projected CAGR at 8.22% through 2030.

- By geography, North America led with 33.12% share of the medical enzyme technology market size in 2024 and Asia-Pacific is forecast to register an 8.43% CAGR between 2025 and 2030.

Global Medical Enzyme Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of chronic and metabolic diseases | +1.8% | North America, Europe, global high-burden regions | Long term (≥ 4 years) |

| Growth of point-of-care enzymatic diagnostics | +1.2% | APAC, North America | Medium term (2-4 years) |

| Advances in recombinant enzyme biomanufacturing | +0.9% | North America, Europe, expanding APAC | Medium term (2-4 years) |

| Integration of enzyme-mediated CRISPR diagnostics | +0.7% | North America, Europe, selective APAC markets | Long term (≥ 4 years) |

| Emergence of enzyme-enabled wearable microfluidic sensors | +0.6% | North America, developed APAC | Medium term (2-4 years) |

| Expansion of advanced-therapy manufacturing capacity | +0.4% | North America, Europe, China, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic and Metabolic Diseases

Diabetes, affecting 537 million adults in 2024, is reshaping demand for glucose oxidase and broader multi-analyte enzyme panels that track lipid and inflammatory markers.[1]Heidi Ledford, “'Remarkable' New Enzymes Built by Algorithm with Physics Know-How,” Nature, nature.com Aging populations in high-income countries now rely on routine enzyme-based assays for preventive health programs. Pharmaceutical pipelines feature emergent therapies such as condoliase for lumbar disc herniation awaiting FDA approval, reflecting direct therapeutic use cases. Payers encourage preventive screening, amplifying adoption of enzyme platforms in primary care. These forces combine to keep chronic-disease-driven demand on a long-term upward slope for the medical enzyme technology market.

Growth of Point-of-Care Enzymatic Diagnostics

COVID-19 underscored the value of decentralized testing, speeding roll-out of compact, cartridge-based enzyme assays that deliver near-lab accuracy within minutes.[2]Mohamed S. Draz, “New Method of DNA Testing: Expanding Scientific Innovation,” Science Daily, sciencedaily.com Enzyme stabilization advances permit room-temperature storage, essential for rural distribution in emerging economies. Microfluidic integration allows multiplex detection from finger-stick samples, supporting chronic disease management in home settings. Economic evaluations show lower total testing costs when early diagnosis reduces hospital admissions. Together, these attributes position point-of-care formats as the fastest expanding use case in the medical enzyme technology market.

Advances in Recombinant Enzyme Biomanufacturing

Synthetic biology, AI-guided protein modeling, and single-use bioreactors are cutting production cycles and enhancing batch consistency. Continuous manufacturing, complemented by digital twins for real-time process control, reduces cost of goods by up to 20%. Proprietary platforms such as Codexis ECO Synthesis shorten variant optimization timelines from years to months, enabling quicker commercial launch. These efficiencies encourage shift from animal-derived to recombinant formats, broadening therapeutic and diagnostic pipelines across the medical enzyme technology market.

Integration of Enzyme-Mediated CRISPR Diagnostics

Hybrid systems pair CRISPR precision with enzyme amplification to detect pathogens and genetic mutations rapidly.[3]Ewen Callaway, “CRISPR Diagnostic Tests: These Paper Strips Could Help Detect Disease in Minutes,” Nature, nature.com Thermostable Cas variants expand use in resource-limited settings. Programmable cartridges allow quick re-targeting, supporting outbreak response. Regulators are drafting guidance tailored to this convergence, lowering approval uncertainty and encouraging investment. The result is a new generation of diagnostics that accelerate personalized medicine adoption.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-regional regulatory approval timelines | -0.8% | EU, Japan, global innovators | Long term (≥ 4 years) |

| Competition from non-enzymatic biosensing modalities | -0.6% | Developed markets | Medium term (2-4 years) |

| Fragile supply chain for rare enzyme cofactors | -0.5% | Global, niche applications | Short term (≤ 2 years) |

| Persistently high production costs for GMP-grade enzymes | -0.4% | Price-sensitive regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Regional Regulatory Approval Timelines

Approval cycles for novel enzyme therapeutics often exceed 18–24 months beyond initial projections because dossiers must satisfy divergent evidence standards in the United States, Europe, and Japan. Cost to generate redundant data can reach USD 100 million, slowing global roll-out. Companies stage submissions, focusing first on high-value markets, which delays patient access elsewhere and lowers early revenue for the medical enzyme technology market. Collaborative initiatives are progressing, yet tangible convergence remains slow.

Competition From Non-Enzymatic Biosensing Modalities

Nanomaterial-based electrochemical and optical sensors are narrowing performance gaps while promising longer shelf life and simpler handling. Continuous data output in real time enhances clinical utility. Enzymes still excel in specificity and complex cascade amplification, but pricing pressure from enzyme-free alternatives is intensifying.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutics Drive Innovation Momentum

Diagnostic enzymes generated the largest portion of the medical enzyme technology market in 2024 by accounting for 41.77% of revenue. Demand stems from established clinical chemistry sets and expanding point-of-care cartridges. Therapeutic enzymes, although smaller in value, are growing fastest at a 10.34% CAGR, buoyed by enzyme replacement therapies for genetic disorders and novel interventions such as condoliase for spinal disc herniation.

The pipeline of AI-designed enzymes capable of targeting previously undruggable reactions is widening the addressable patient pool. These developments are expected to shift revenue weight toward the therapeutic segment over the forecast horizon as successful approvals accumulate.

By Application: Gene Editing Reshapes Market Dynamics

Disease diagnostics applications contributed 39.68% of revenue in 2024, underscoring the historical primacy of enzyme assays in routine testing. However, the gene editing and molecular diagnostics segment is projected to climb at 10.88% CAGR, reflecting integration of enzymes with CRISPR-Cas and precision oncology workflows.

Emerging wearable microfluidic devices blur diagnostic and monitoring lines, offering continuous biomarker readouts and suggesting fresh blended categories for the medical enzyme technology market. As regulatory clarity improves, investment in gene editing diagnostics is expected to accelerate further.

By Source: Recombinant Engineering Gains Momentum

Microbial fermentation remains the backbone of production, representing 53.23% of 2024 revenue and benefiting from proven scalability and cost structure. Yet the recombinant slice is climbing at 9.24% CAGR because engineered variants deliver higher stability, specificity, and reproducibility.

AI-powered protein modeling and automated directed evolution cut development timeframes considerably, making recombinant pathways attractive for both diagnostics and therapeutics. Plant and animal sources continue in niche roles but face declining share due to variability and sourcing constraints.

By End User: Point-of-Care Settings Emerge

Hospitals and diagnostic laboratories dominated usage with 41.18% share in 2024, supported by centralized testing volumes and reimbursement frameworks. Point-of-care settings, however, display the highest momentum at an 8.22% CAGR as decentralized healthcare models expand.

Retail clinics, telehealth providers, and at-home test kit brands are integrating enzyme cartridges that meet clinical accuracy yet fit consumer workflows. Pharmaceutical and biotechnology firms remain critical purchasers for R&D and manufacturing quality control, while academic institutes drive exploration of next-generation applications.

Geography Analysis

North America held 33.12% of 2024 revenue, benefiting from strong venture funding, deep clinical trial networks, and clear regulatory pathways. Capital investment has also flowed into continuous manufacturing and AI-enabled enzyme design hubs, reinforcing technological leadership. Government reimbursement for preventive diagnostics sustains baseline demand and encourages adoption of new assay panels.

Asia-Pacific is the fastest growing region at an 8.43% CAGR, propelled by rising chronic disease prevalence, improving healthcare access, and large-scale biomanufacturing investments in China and South Korea. Regional governments offer tax incentives and grants for biologics production, drawing multinationals to localize supply chains. Japan’s sophistication in microfluidic design and Singapore’s contract development scene inject technical depth that supports rapid scaling of the medical enzyme technology market.

Europe maintains robust high-value niches, with Germany, the United Kingdom, and France emphasizing therapeutic enzymes and specialized diagnostics. Complex but predictable regulatory processes encourage quality leadership, even as approval timelines stretch relative to North America. Collaborative R&D projects, such as Novonesis partnerships with EU universities, reinforce innovation flow while cross-border regulatory initiatives aim to speed market entry.

Competitive Landscape

The medical enzyme technology market is moderately fragmented. Novonesis and DSM-Firmenich lead through vertical integration that spans strain engineering to global GMP manufacturing. Lallemand’s stake in Livzym shows that strategic investments accelerate entry into emerging geographies and niche applications.

Technology differentiation increasingly hinges on AI-enhanced design success rates, where cutting-edge platforms report 18% hit rates against legacy processes’ 1.6%. Continuous bioprocessing and digital twins lower production costs, creating price flexibility and supporting penetration of lower-income markets. Patent activity in enzyme-CRISPR integration is accelerating, hinting at intensifying competition over precision diagnostics.

Supply chain resilience strategies focus on dual-sourcing critical cofactors and investing in regional production nodes to hedge geopolitical risk. Players that couple rapid design capabilities with secure manufacturing capacity stand to gain share as regulatory approvals for therapeutic enzymes pick up pace.

Medical Enzyme Technology Industry Leaders

Novozymes A/S

F. Hoffmann-La Roche Ltd

DSM-Firmenich

Codexis Inc.

Sekisui Diagnostics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Researchers at Tokyo University of Science discovered a gut-derived β-galactosidase with prebiotic glycan specificity, opening microbiome therapeutic avenues.

- September 2024: Asahi Kasei agreed to transfer its diagnostics business, including enzyme plants, to Nagase & Co., with completion slated for Jul 2025.

- March 2024: Novonesis and UC San Diego formed a consortium to expand human milk oligosaccharide research for gut health solutions.

Global Medical Enzyme Technology Market Report Scope

| Therapeutic Enzymes |

| Diagnostic Enzymes |

| Research-Grade Enzymes |

| Bioprocessing & Manufacturing-Aid Enzymes |

| Disease Diagnostics |

| Drug Formulation & Delivery |

| Gene Editing & Molecular Diagnostics |

| Regenerative Medicine & Tissue Engineering |

| Microbial (Bacterial & Fungal) |

| Animal-Derived |

| Plant-Derived |

| Recombinant / Engineered |

| Hospitals & Diagnostic Laboratories |

| Pharmaceutical & Biotechnology Companies |

| Academic & Research Institutes |

| Point-of-Care Settings |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Therapeutic Enzymes | |

| Diagnostic Enzymes | ||

| Research-Grade Enzymes | ||

| Bioprocessing & Manufacturing-Aid Enzymes | ||

| By Application | Disease Diagnostics | |

| Drug Formulation & Delivery | ||

| Gene Editing & Molecular Diagnostics | ||

| Regenerative Medicine & Tissue Engineering | ||

| By Source | Microbial (Bacterial & Fungal) | |

| Animal-Derived | ||

| Plant-Derived | ||

| Recombinant / Engineered | ||

| By End User | Hospitals & Diagnostic Laboratories | |

| Pharmaceutical & Biotechnology Companies | ||

| Academic & Research Institutes | ||

| Point-of-Care Settings | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the medical enzyme technology market in 2025?

The medical enzyme technology market size stands at USD 5.05 billion in 2025.

What is the expected CAGR for medical enzyme technology through 2030?

The market is forecast to grow at a 6.06% CAGR between 2025 and 2030.

Which product category commands the largest share?

Diagnostic enzymes captured 41.77% of revenue in 2024.

Which region leads revenue contribution?

North America held 33.12% of global revenue in 2024.

What segment shows the fastest growth?

Gene editing and molecular diagnostics applications are projected to post a 10.88% CAGR through 2030.

What is the main restraint affecting growth?

Extended multi-regional regulatory approval timelines reduce speed to market and curb CAGR by 0.8 percentage points.

Page last updated on: