Synthetic Biology Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 23.53 Billion |

| Market Size (2031) | USD 56.48 Billion |

| Growth Rate (2026 - 2031) | 19.14% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synthetic Biology Market Analysis by Mordor Intelligence

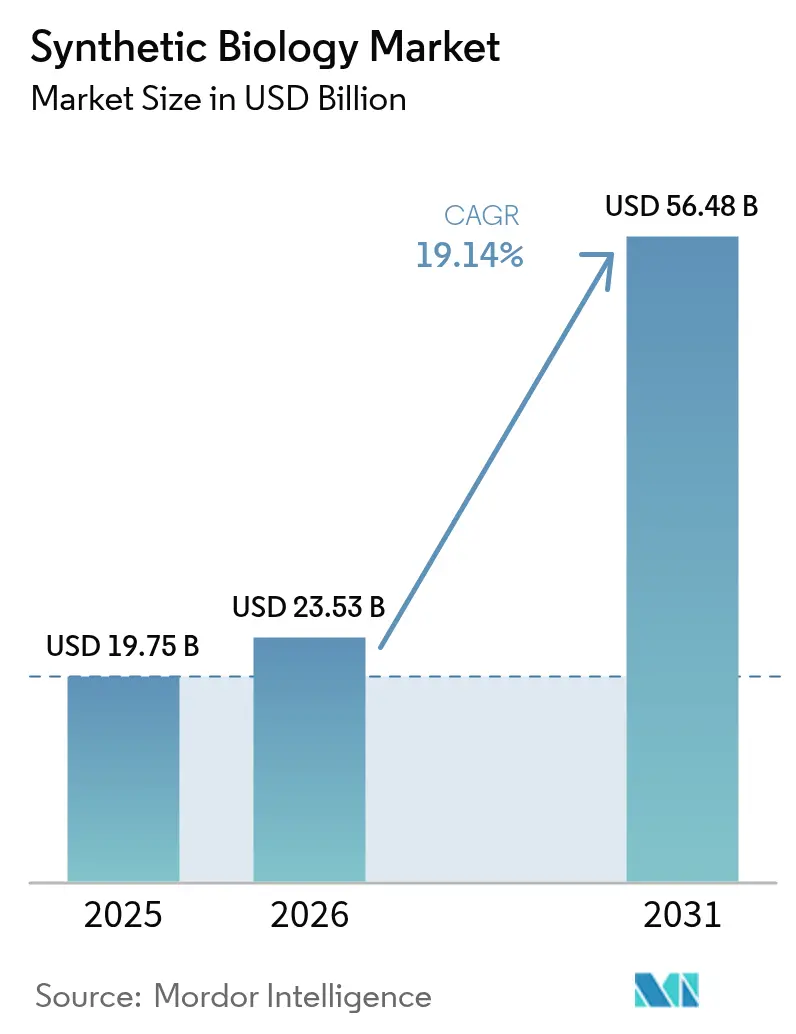

The Synthetic Biology Market size was valued at USD 19.75 billion in 2025 and estimated to grow from USD 23.53 billion in 2026 to reach USD 56.48 billion by 2031, at a CAGR of 19.14% during the forecast period (2026-2031).

Recent gains reflect the transition from proof-of-concept bioengineering to large-scale biomanufacturing. Converging advances in artificial-intelligence-guided protein design, decreasing gene-synthesis costs, and steady government funding have shortened innovation cycles and lowered entry barriers. Corporate net-zero commitments create durable demand for bio-based alternatives to petrochemicals, while breakthroughs in genome editing and automated biofoundries extend addressable applications in healthcare, food, and specialty materials. At the same time, dual-use regulations and talent shortages temper the growth trajectory, placing a premium on regulatory navigation and workforce development across the synthetic biology market.

Key Report Takeaways

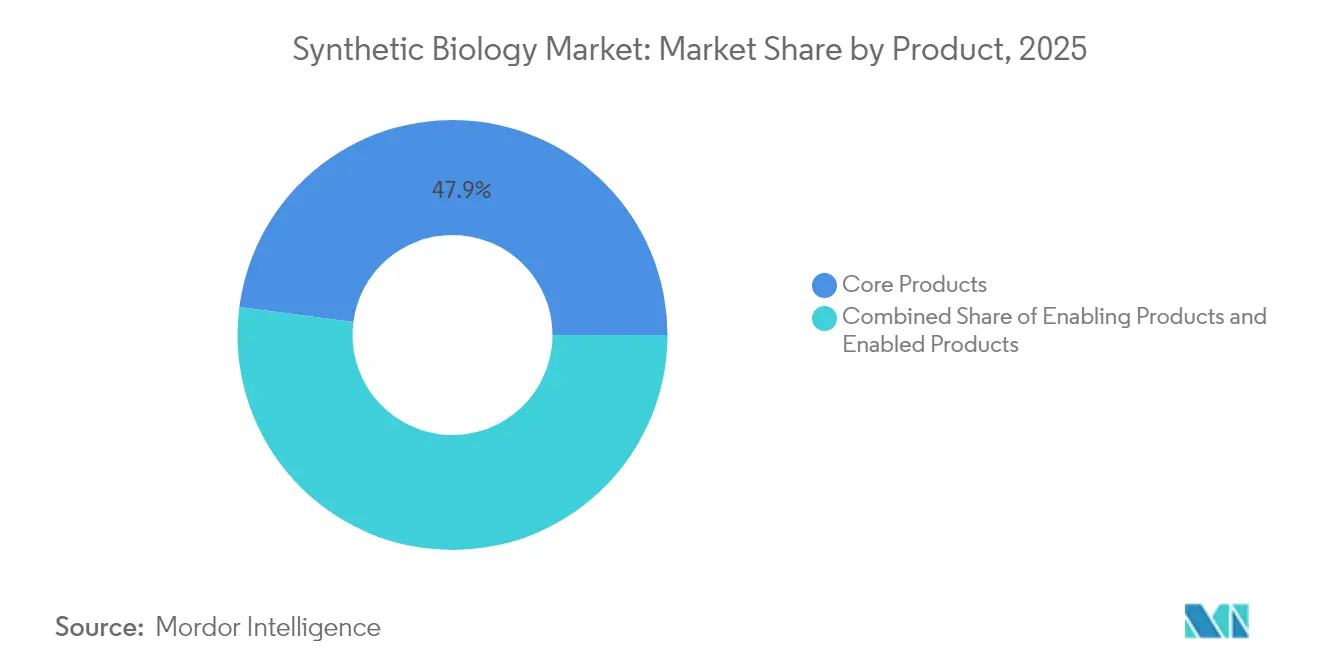

- By product category, Core Products held 47.92% revenue share in 2025, whereas Enabling Products are forecast to expand at a 19.91% CAGR through 2031.

- By technology, Genome Engineering captured 33.21% of market share in 2025, while Bioinformatics & CAD Tools are advancing at 19.56% CAGR to 2031.

- By application, Healthcare accounted for 53.62% of the synthetic biology market size in 2025; Food & Agriculture is set to rise at a 18.62% CAGR between 2026-2031.

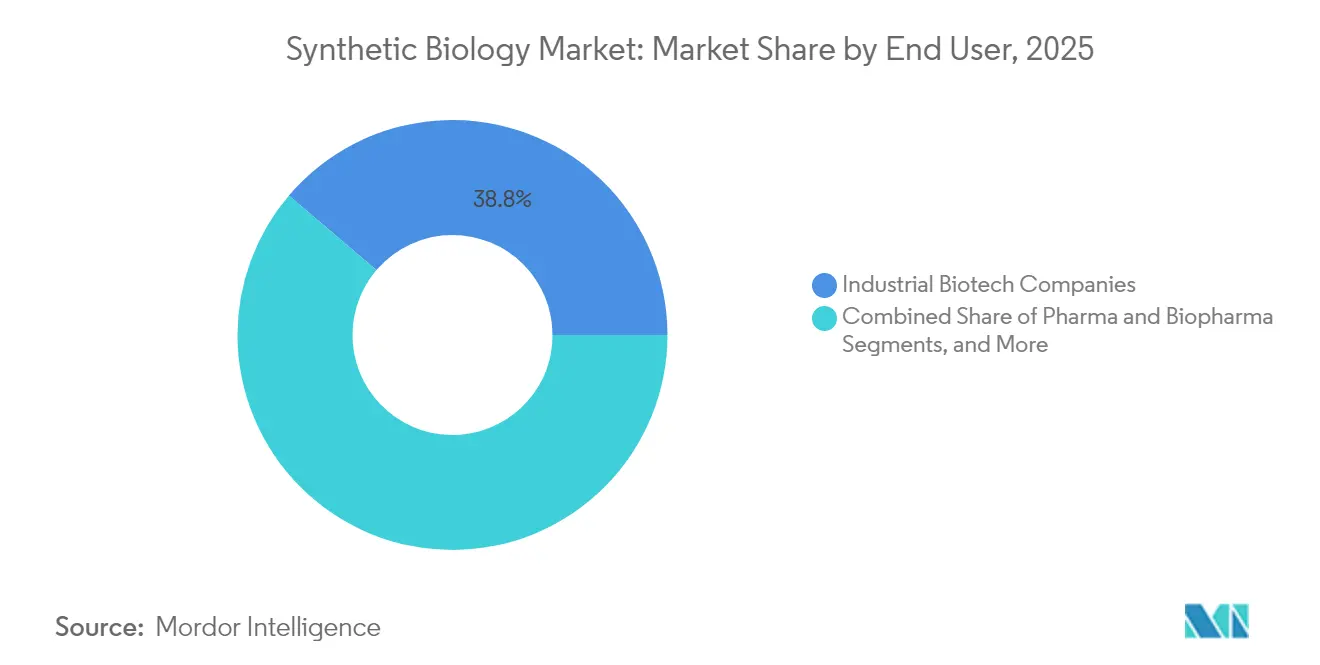

- By end-user, Industrial Biotech Companies commanded 38.76% share in 2025, with Defense & Government Labs growing fastest at 19.22% CAGR.

- By geography, North America led with 43.12% market share in 2025, whereas Asia-Pacific is expanding most rapidly at 21.7% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Synthetic Biology Market Trends and Insights

Drivers Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dual-use bio-threat regulation drag | -1.4% | Global, with varying regulatory intensity | Medium term (2-4 years) |

| Talent bottleneck in bio-informatics engineers | -1.1% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Limited DNA data-storage standards | -0.7% | Global, with early impact in tech-forward regions | Medium term (2-4 years) |

| Societal and ethical concerns over GMO adoption | -0.8% | Global, strongest in EU and developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government & VC Funding Surge

Large-scale public programs are deepening the capital pool that supports biomanufacturing build-outs. The United States enacted a USD 15 billion National Biotechnology Initiative Act to meet 30% of domestic chemical demand through bio-based production by 2040 [1]Jennifer Granholm, “Biden-Harris Administration Launches National Biotechnology and Biomanufacturing Initiative,” U.S. Department of Energy, energy.gov. China committed USD 4.17 billion in 2024 for biomanufacturing infrastructure, signaling technology sovereignty priorities. Horizon Europe’s SYNBEE project nurtures start-ups across 25 nations, while venture funding has remained above pre-pandemic levels according to SynBioBeta. This confluence of public and private capital shortens the “valley of death” from lab bench to pilot plant, accelerating time-to-market across the market.

Falling Cost Curve for Gene Synthesis

Enzymatic DNA synthesis now delivers multi-kilobase constructs in days instead of weeks. Ansa Biotechnologies’ platform synthesizes sequences exceeding 1,000 bp today and targets 10,000 bp capability by 2025 [2]John Cumbers, “Ansa Biotechnologies Extends Enzymatic DNA Synthesis to Kilobase Lengths,” SynBioBeta, synbiobeta.com. Evonetix’s semiconductor-based chips fabricate gene-length fragments 10 times faster than traditional phosphoramidite chemistry. Benchtop synthesizers from Kilobaser and Telesis Bio further democratize access for smaller labs. These innovations cut iteration costs for metabolic-engineering and protein-optimization projects, reinforcing demand across the synthetic biology market.

AI-Driven Protein Design Adoption

Foundation models trained on vast genomic corpora are turning protein engineering into a predictive discipline. Arc Institute’s Evo 2 model identifies disease mutations with 90% accuracy, guiding enzyme redesign. ZymCTRL from Basecamp Research generates novel enzymes with only 30% sequence homology to training data, broadening search space for industrial biocatalysts. Massachusetts General Hospital’s PAMmla evaluates 64 million CRISPR-Cas9 variants to minimize off-targets. Ginkgo Bioworks exposes these capabilities through public APIs, shrinking design-build-test cycles. AI integration therefore enhances project success rates and fuels service revenues within the synthetic biology market.

Breakthroughs in Gene-Editing Platforms Expanding Addressable Applications

Completion of the synthetic yeast chromosome synXVI under the Sc2.0 program illustrates genome-scale rewrite capacity. Yale achieved multiplexed base editing with triple the prior edit count, boosting precision medicine prospects. MIT revealed the compact TIGR system that lifts PAM restrictions, improving plant and microbial engineering flexibility. Approval of CASGEVY for sickle-cell disease sets therapeutic precedent. These advances unlock new market niches—from biofuels to environmental remediation—inside the market.

Corporate Net-Zero Mandates Driving Demand for Bio-Based Chemicals, Fuels, and Materials

Policy signals amplify corporate pull for low-carbon chemistry. The Biden Administration aims to replace 90% of petroleum-based plastics within 20 years. Europe’s Circular Bio-Based Europe Joint Undertaking has allocated USD 2.2 billion to 15 biorefineries [3]Alexander H. Tullo, “Europe Backs 15 Biorefineries in Circular Bio-Based Push,” Chemical & Engineering News, cen.acs.org. Anthrogen’s microbes convert atmospheric CO₂ into drop-in chemicals at 80% of fossil cost. Market-entry barriers now hinge less on demand uncertainty and more on scale-up execution, further energizing the synthetic biology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Dual-use bio-threat regulation drag | -1.4% | Global, with varying regulatory intensity | Medium term (2-4 years) |

| Talent bottleneck in bio-informatics engineers | -1.1% | Global, acute in North America and EU | Short term (≤ 2 years) |

| Limited DNA data-storage standards | -0.7% | Global, with early impact in tech-forward regions | Medium term (2-4 years) |

| Societal and ethical concerns over GMO adoption | -0.8% | Global, strongest in EU and developing markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Dual-Use Bio-Threat Regulation Drag

Compliance burdens grow as policymakers tighten genetic-material screening. SecureDNA screens every order over 30 bp against pathogen databases while preserving customer confidentiality, adding cost and processing time. China’s biosafety framework imposes strict oversight of engineered microbes yet aims to support innovation. Europe postponed its Biotech Act until Q3 2026, prolonging uncertainty. Frontiers research warns that AI-enabled bio-automation may outpace legislative cycles, requiring new governance models. Smaller firms in the synthetic biology market often lack the regulatory-affairs bandwidth to navigate these regimes, slowing product launches.

Talent Bottleneck in Bio-Informatics Engineers

Demand for professionals bridging wet-lab biology and computational modeling exceeds supply. The National Biotechnology Workforce Framework highlights biomanufacturing job creation outpacing aerospace and automotive employment. Europe’s SYNBEE program funds upskilling and diversity initiatives in 25 countries. Yet graduate pipelines remain thin for hybrid skills in metabolic-model construction, digital-twin bioprocessing, and AI algorithm deployment. Industry has responded with internal academies and university partnerships, but capacity gaps still inhibit scale-up speed within the synthetic biology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Core Products Anchor Build-Test Cycles While Enabling Products Accelerate Innovation

Core Products accounted for 47.92% of 2025 revenue as DNA/RNA synthesizers and gene-editing kits formed the indispensable infrastructure of laboratory workflows. Evonetix’s chip-based synthesizer exemplifies hardware innovation, cutting synthesis times by a factor of 10 and anchoring recurring consumables demand. The synthetic biology market size for Core Products is expected to grow steadily, supported by continuous upgrades to accuracy and throughput.

Enabling Products—encompassing oligonucleotides, cloning vectors, and cell-free systems—are forecast to grow at a 19.91% CAGR through 2031, the fastest among product classes. Twist Bioscience’s participation in AI safety consortia underscores the strategic importance of secure DNA sourcing. The first synthetic yeast genome and programmable cell-free protein factories reflect rising complexity needs, which magnify consumables volume across the synthetic biology market.

By Technology: Genome Engineering Dominates Revenue While Bioinformatics Tools Redefine Design

Genome Engineering held 33.21% of synthetic biology market share in 2025, buoyed by widespread CRISPR-Cas9 adoption and emergent alternatives like TIGR. Commercialization milestones such as CASGEVY validate therapeutic revenue pools. Regulatory precedents are encouraging industrial and agricultural genome-editing initiatives, reinforcing leadership of this technology segment.

Bioinformatics & CAD Tools will expand at a 19.56% CAGR, transforming empirical tinkering into algorithmically guided engineering. Researchers describes CodonTransformer’s multi-species optimization framework that shortens path-to-hit timelines . As AI models scale, subscription software revenues are set to rise faster than reagent sales, reshaping the synthetic biology market size distribution among value-chain players.

By Application: Healthcare Commands Cash Flow While Food & Agriculture Scales Fast

Healthcare generated 53.62% of 2025 revenue through gene-therapy vectors, mRNA vaccines, and antibody libraries. Ginkgo Bioworks’ expanded Novo Nordisk alliance highlights platform advantages in chronic-disease therapeutics. Pearl Bio’s USD 1 billion co-development deal with Merck leverages Genomically Recoded Organisms to produce multi-functional proteins. These investments cement healthcare’s centrality to the synthetic biology market.

Food & Agriculture applications will post a 18.62% CAGR, aided by precision-fermentation cost declines. Onego Bio is scaling bioidentical egg-white protein to offset avian-flu supply shocks. Colorado State University’s genetic toggle switch enables on-demand fruit-ripening control. Such innovations broaden consumer-facing exposure, enlarging the synthetic biology market size attributable to agrifood segments.

By End-User: Industrial Biotech Firms Lead Adoption While Defense Labs Accelerate

Industrial Biotech Companies absorbed 38.76% of end-user spending in 2025 as they convert microbial chassis into production workhorses. Primient’s partnership with Synonym to refurbish fermentation assets under a Commerce grant typifies momentum toward domestic bio-infrastructure. Integrated digital twins and continuous fermentation promise further efficiency gains across the synthetic biology market.

Defense & Government Labs are the fastest-growing end-user group at 19.22% CAGR. DARPA’s Ag × BTO program and BIOINT paradigm illustrate strategic intent to neutralize agro-biorisks through rapid-response biosensors. Government labs’ procurement of secure gene-synthesis services and automated biofoundries is likely to cascade into commercialized spin-outs.

By Technology Platform: Automation Scales Production While AI Sharpens Precision

Robot-powered biofoundries such as FAST-PB automate plant-genome edits and tissue-culture workflows, cutting development time for high-oil crops. Self-driving laboratories at the University of Sheffield optimize polymer reactions in real-time, saving weeks of manual iterations. Trilobio’s plug-and-play robots bring no-code automation to resource-constrained labs. DNA nanorobots program lipid membranes for precise drug delivery, foreshadowing smart therapeutics. Together, AI and automation converge to extend the synthetic biology market from kilograms to kilotons of output.

Geography Analysis

North America held 43.12% revenue share in 2025. The USD 15 billion federal biomanufacturing commitment anchors capacity build-outs, while venture capital and established R&D clusters sustain start-up formation. Ginkgo Bioworks’ platform partnerships and Thermo Fisher Scientific’s USD 40-50 billion M&A war chest illustrate consolidation and scale advantages. Nevertheless, U.S. firms face talent bottlenecks in bio-informatics and the compliance load of overlapping federal and state rules, factors that could modulate synthetic biology market growth in the region.

Asia-Pacific is the fastest-expanding region at 21.7% CAGR. China has overtaken Europe in high-impact biotech papers and patents, supported by USD 4.17 billion in 2024 investments and further allocations slated for 2025. Shanghai’s biotech hub leverages co-located manufacturing infrastructure and subsidy programs to accelerate commercialization. Price-competitive production capabilities position the region as a leading export platform, reinforcing its influence on the global synthetic biology market.

Europe combines robust sustainability policy with fragmented regulatory execution. The Circular Bio-Based Europe initiative directs USD 2.2 billion toward 15 biorefineries employing 165,000 workers. Horizon Europe’s SYNBEE extends entrepreneur support to 25 nations. Delays in the EU Biotech Act, however, prolong uncertainty and may slow project financing. Companies like Insempra have raised USD 20 million to scale bio-based ingredients for cosmetics even amid cautious capital markets. Despite hurdles, Europe’s circular-economy ethos secures long-term relevance within the synthetic biology market.

Competitive Landscape

The synthetic biology market remains moderately fragmented, with platform specialists and reagent suppliers co-existing alongside life-science conglomerates. Thermo Fisher Scientific’s planned USD 3 billion purchase of Olink underscores a strategy to secure differentiated proteomics assets. Ginkgo Bioworks is pursuing cost reductions of USD 200 million via workforce realignment to reach EBITDA breakeven by 2026. Meanwhile, AMD’s USD 20 million investment in Absci illustrates semiconductor entrants eyeing AI-enabled drug discovery.

White-space segments include DNA data storage, where DNAformer delivers 3,200-fold write-speed gains. DARPA’s concept of bio-fabricating space structures in microgravity could redefine supply-chain economics for satellite deployment. Emerging players leverage proprietary AI and automation to challenge incumbents on speed and cost, ensuring active competition across the synthetic biology market.

Synthetic Biology Industry Leaders

Genscript

Thermo Fisher Scientific Inc

Amyris Inc

Integrated DNA Technologies Inc. (Danaher Corporation)

Illumina, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Rice University launched the Rice Synthetic Biology Institute to accelerate translational research.

- December 2023: The Allen Institute, Chan Zuckerberg Initiative, and University of Washington unveiled the Seattle Hub for Synthetic Biology focused on cellular-recording technologies.

- May 2023: GenScript Biotech showcased new synthetic-biology tools at SynBioBeta alongside strategic partner Allozymes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the synthetic biology market as revenues generated from engineered biological parts, pathways, and organisms that are purpose-built through DNA/RNA synthesis, genome engineering, cell-free systems, and automated bioprocess platforms. Typical product classes tracked include core tools (synthesizers, gene-editing enzymes), enabling reagents (oligonucleotides, cloning vectors), and enabled outputs such as engineered microbes and cell-free kits. According to Mordor Intelligence, this market is valued at USD 19.75 billion in 2025.

The sizing does not count stand-alone bioinformatics software licenses or routine contract sequencing services.

Segmentation Overview

- By Product

- Core Products

- DNA/RNA Synthesizers

- Gene Editing Kits & Enzymes

- Enabling Products

- Oligonucleotides

- Cloning Vectors

- Enabled Products

- Cell-Free Systems

- Engineered Micro-organisms

- Core Products

- By Technology

- Genome Engineering

- DNA/RNA Synthesis

- Bioinformatics & CAD Tools

- Bioprocessing & Automation

- By Application

- Healthcare

- Drug Discovery

- Gene & Cell Therapy

- Chemicals & Biofuels

- Specialty Chemicals

- Advanced Biofuels

- Food & Agriculture

- Alternative Proteins

- Crop Trait Engineering

- Other (Bio-security, Environment, Data Storage)

- Healthcare

- By End-User

- Industrial Biotech Companies

- Pharma & Biopharma

- Academic & Research Institutes

- Defense & Government Labs

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Desk Research

Our analysts first compile publicly available fundamentals from tier-one sources such as the NIH RePORTER, Eurostat biotech trade codes, the OECD Bioeconomy database, and patent families mined via Questel. Key demand clues are strengthened with production statistics from the U.S. Energy Information Administration for bio-fuels and FAO food protein import data, before being cross-checked with grant disclosures and journal meta-analyses that chart CRISPR and gene-synthesis cost curves. Subscription resources, including D&B Hoovers for company financials and Dow Jones Factiva for timely deal flow, complete the desk scan. These references are illustrative; numerous other materials support data collection, validation, and clarification.

Primary Research

We interview tool vendors' commercial leads, industrial biotech process engineers, clinical geneticists, and venture investors across North America, Europe, and Asia-Pacific. Their insights validate price trajectories, capacity utilization, and regulatory pacing, letting us reconcile desk findings with on-ground adoption sentiment.

Market-Sizing & Forecasting

A blended top-down rebuild of production volumes, gene-synthesis capacity, and venture funding pools is corroborated with selective bottom-up checks (sampled average selling price × volumes from key suppliers) to refine totals. Variables fed into the model include cost per synthesized base pair, national R&D spend on genomics, announced biomanufacturing floor space, CRISPR patent filings, and yeast-based protein output. Multivariate regression, supplemented by ARIMA to capture short-cycle shocks, projects each driver through 2030, and gaps in bottom-up inputs are bridged using region-specific penetration proxies agreed upon in expert calls.

Data Validation & Update Cycle

Outputs undergo variance screening against independent trade and funding series, then pass a multi-analyst review. Reports refresh yearly, with mid-cycle updates triggered by material events. A final analyst pass ensures clients receive the freshest view.

Why Mordor's Synthetic Biology Baseline Is Trusted by Decision-Makers

Published estimates often diverge because providers adopt different segment cut-offs, currency bases, and refresh cadences. External sources put 2025 values anywhere from USD 18.94 billion to USD 24.58 billion. One study even quotes USD 17.09 billion for the same year.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.75 B | Mordor Intelligence | - |

| USD 18.94 B | Global Consultancy A | Narrower tool scope; excludes enabled products such as cell-free systems |

| USD 24.58 B | Trade Journal B | Aggressive ASP progression and inclusion of bioinformatics software revenue |

| USD 17.09 B | Industry Insights C | Extrapolates limited 2024 survey data with sparse Asia-Pacific coverage |

These comparisons show that when scope breadth, variable selection, and annual refresh discipline are harmonized, as in Mordor's approach, the baseline remains balanced, transparent, and repeatable for strategic planning.

Key Questions Answered in the Report

How big is the Synthetic Biology Market?

The Synthetic Biology Market size is expected to reach USD 23.53 billion in 2026 and grow at a CAGR of 19.14% to reach USD 56.48 billion by 2031.

Which region leads the synthetic biology market?

North America leads with 43.12% revenue share, supported by substantial federal funding and a mature venture ecosystem.

Who are the key players in Synthetic Biology Market?

Genscript, Thermo Fisher Scientific Inc, Amyris Inc, Integrated DNA Technologies Inc. (Danaher Corporation) and Illumina, Inc. are the major companies operating in the Synthetic Biology Market.

What product segment is growing fastest within the synthetic biology market?

Enabling Products are projected to grow at a 19.91% CAGR, driven by advances in oligonucleotide chemistry and cell-free systems.

Which region has the biggest share in Synthetic Biology Market?

In 2025, the North America accounts for the largest market share in Synthetic Biology Market.

Which application area holds the largest revenue share?

Healthcare commands 53.62% of revenue, underpinned by gene-therapy approvals and major pharma-platform partnerships.

Page last updated on: