Bioreactor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

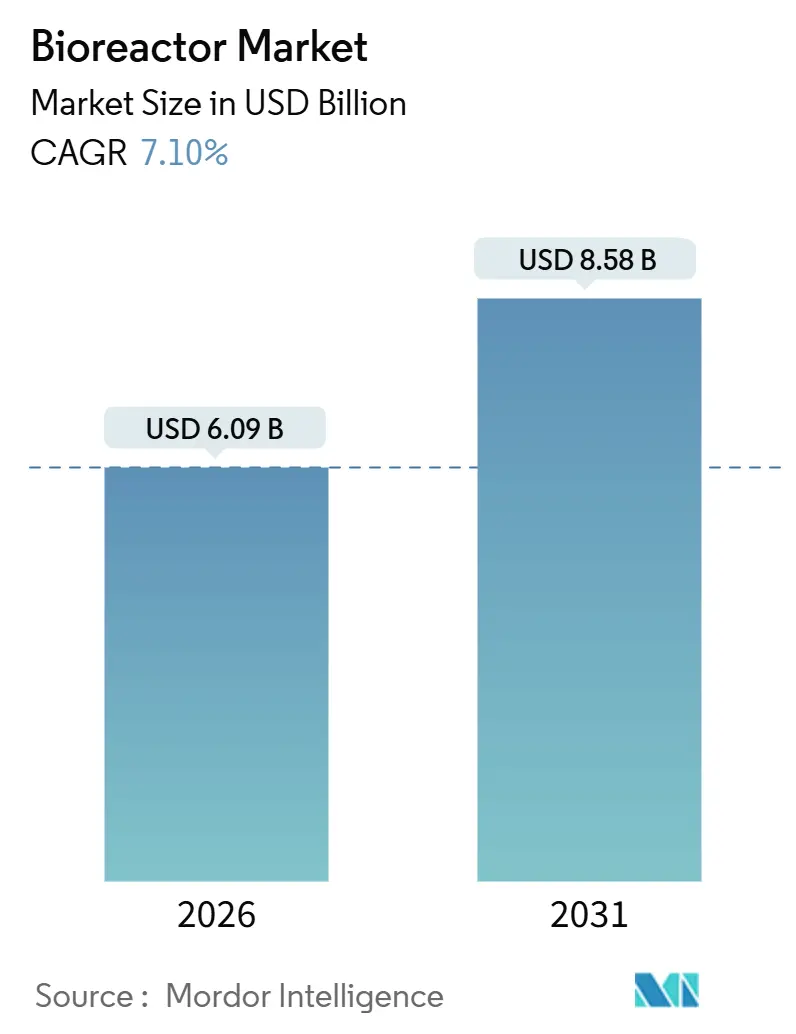

| Market Size (2026) | USD 6.09 Billion |

| Market Size (2031) | USD 8.58 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

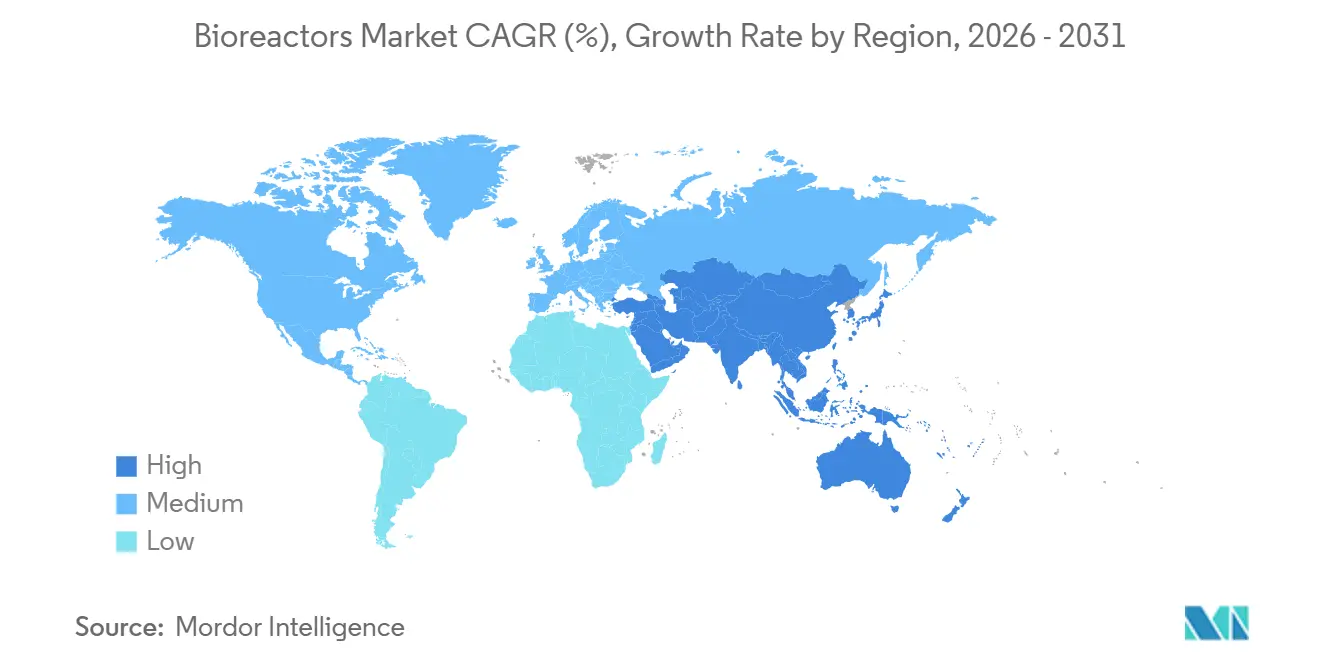

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

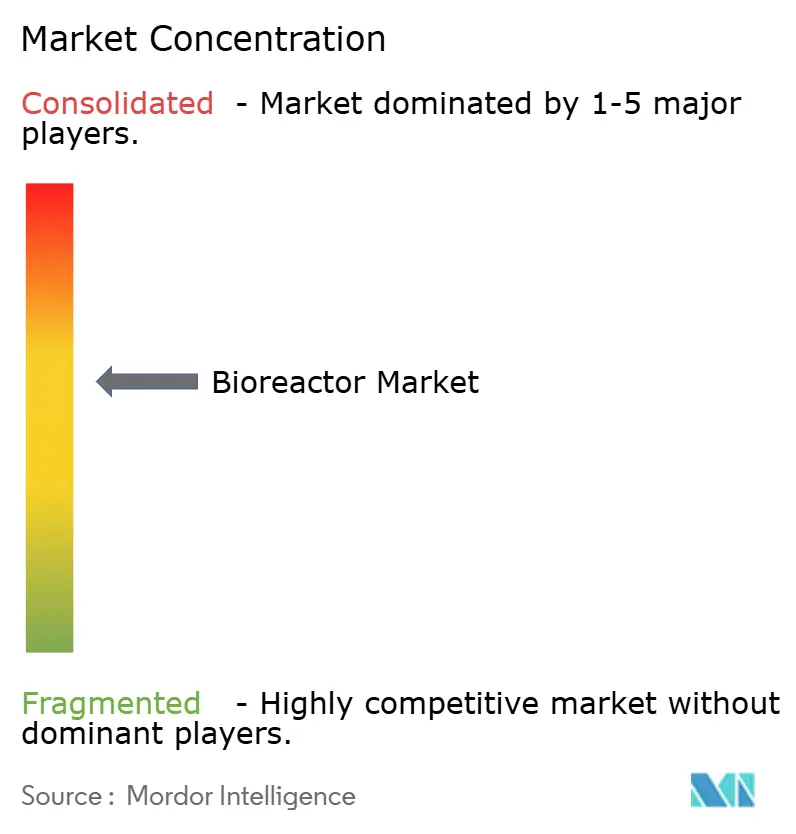

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioreactor Market Analysis by Mordor Intelligence

The Bioreactor Market size is estimated at USD 6.09 billion in 2026, and is expected to reach USD 8.58 billion by 2031, at a CAGR of 7.10% during the forecast period (2026-2031).

The rising demand for flexible capacity in cell and gene therapy, sustained funding for vaccine preparedness, and the broader adoption of single-use technology continue to redefine how biopharma companies and contract manufacturers allocate their capital. Accelerated process-development timelines and the growing acceptance of continuous bioprocessing shorten the path from discovery to commercial supply, while digital twins and in-line analytics push the sector toward real-time parameter control. Competitive intensity is increasing as integrated vendors bundle hardware, consumables, and software, thereby locking customers into ecosystems that promote recurring revenue and high switching costs. Supply-chain fragility for medical-grade polymers and a widening talent gap in bioprocess engineering counterbalance demand, especially in regions racing to onshore capacity to hedge against geopolitical risk.

Key Report Takeaways

- By type, stainless-steel systems led the bioreactor market, accounting for 47.00% of the market share in 2025. In contrast, single-use configurations are forecast to advance at a 10.10% CAGR through 2031.

- By usage, full-scale production accounted for 58.80% of the bioreactor market size in 2025, while pilot-scale installations are projected to expand at a 9.00% CAGR between 2026 and 2031.

- By scale, 200 L – 1,500 L accounted for 39.00% of the bioreactor market size in 2025, while above 1,500 L are projected to expand at a 10.20% CAGR between 2026 and 2031.

- By control type, automated (MFCs) accounted for 64.00% of the bioreactor market size in 2025, and it is projected to expand at an 8.50% CAGR between 2026 and 2031.

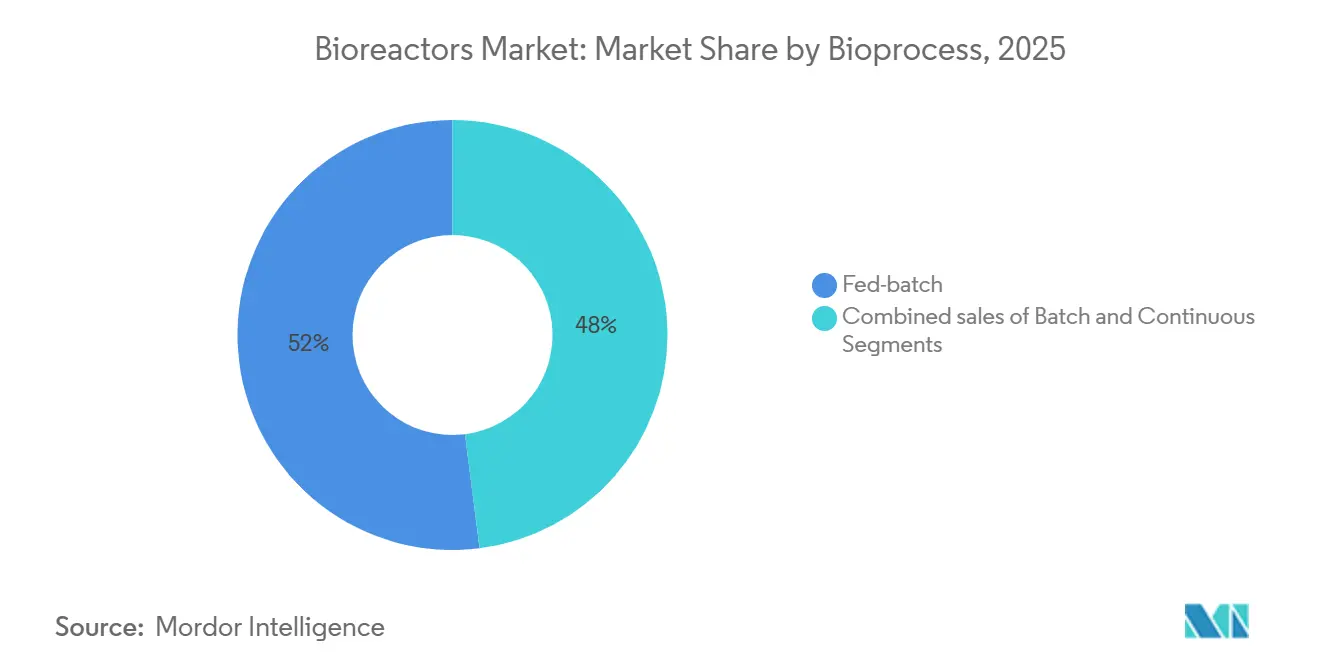

- By 2025, bioprocesses, including fed-batch, retained 52.00% of the bioreactor market share; continuous systems are projected to grow at a 10.50% CAGR through 2031.

- By application, pharmaceutical and biopharmaceutical manufacturing captured 72.00% of revenue in 2025, whereas cell and gene therapy is expected to post a 10.80% CAGR to 2031.

- By geography, North America accounted for 43.00% of the revenue in 2025; the Asia-Pacific region is forecast to register an 8.30% CAGR, the fastest regional growth rate through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bioreactor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Cell & Gene Therapy Manufacturing Pipelines | +2.1% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Growing Adoption of Single-Use Bioreactor Technology | +1.8% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Government Funding for Pandemic Vaccine Capacity | +1.2% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Microbial Fermentation in Alternative Proteins | +0.9% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Integration of Advanced Process Control and Digital Twins | +1.4% | Global | Short term (≤ 2 years) |

| Expansion of Regional Bio-Clusters in Emerging Economies | +0.8% | Asia-Pacific, Latin America, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Cell & Gene Therapy Manufacturing Pipelines

Distributed manufacturing models for autologous CAR-T and allogeneic therapies favor smaller-footprint equipment over centralized mega plants. AGC Biologics has earmarked USD 350 million for a Yokohama site featuring 2,000-liter single-use vessels, while its Copenhagen campus doubled capacity with 16 similar units scheduled for 2026 start-up. Fujifilm Diosynth Biotechnologies is investing USD 1.2 billion in a North Carolina expansion that will utilize 20,000-liter reactors for viral-vector and mRNA programs. AstraZeneca opened a USD 300 million facility in Maryland in 2025 to co-locate clinical and commercial cell therapy production, thereby accelerating technology transfer cycles. These moves show a shift toward owning strategic capacity to protect intellectual property and margins, increasing competition for bioprocess engineers and single-use consumables. As a result, the bioreactor market is moving toward modular, rapidly deployable suites that can be replicated across global sites without extensive civil construction.

Growing Adoption of Single-Use Bioreactor Technology

Single-use platforms have surpassed pilot adoption and now dominate early-stage commercial production. Thermo Fisher Scientific released the HyPerforma DynaDrive 2.0 in 2025, reducing shear stress by 25% and enabling perfusion at cell densities exceeding 100 million cells/mL. Sartorius followed with Biostat STR Generation 3, integrating optical DO sensors and automated pH control that removes four hours of manual calibration per batch. Scale ceilings continue to rise: AGC Biologics plans 5,000-liter single-use runs, pushing the boundaries once thought feasible only in stainless steel. While life-cycle assessments reveal that reusable systems generate three to five times less plastic waste than single-use systems, vendors such as Cytiva and Sartorius have launched take-back programs to recycle spent film and tubing for non-GMP applications. This dynamic keeps sustainability in focus without slowing the momentum of the bioreactor market as it heads into 2026.

Government Funding for Pandemic Vaccine Capacity

Governments now treat local biomanufacturing as strategic infrastructure on par with semiconductors. The United States committed USD 5 billion under Project NextGen, issuing contracts to Fujifilm, Lonza, and Emergent BioSolutions for a combined 500,000 liters of new capacity[1]U.S. Department of Health and Human Services, “Project NextGen Awards,” hhs.gov. The United Kingdom has entered into a 10-year, GBP 520 million (USD 660 million) partnership with Moderna to develop domestic mRNA production lines. Canada’s CAD 2.2 billion (USD 1.6 billion) initiative finances expansions at Sanofi Toronto and a national center in Montreal, ring-fencing supply after COVID-19 bottlenecks. Incentives have shortened payback periods for large stainless-steel projects, keeping the bioreactor market attractive to suppliers that can navigate long procurement cycles and validation requirements. The emphasis on redundancy also drives multi-site capacity planning, increasing equipment demand across regions.

Rising Demand for Microbial Fermentation in Alternative Proteins

Precision fermentation requires higher agitation, elevated dissolved oxygen, and continuous nutrient feeds distinct from mammalian processes. Impossible Foods scaled leghemoglobin production in 10,000-liter reactors and achieved titers of 15 g/L by optimizing Pichia pastoris fermentation. Perfect Day operates 50,000-liter stainless-steel units for whey protein, reducing capital expenditure per kilogram by 40% through continuous operation. Industry analysts expect the precision fermentation segment to reach USD 67.9 billion by 2032, opening up an adjacent growth avenue for the broader bioreactor market. Suppliers able to engineer corrosion-resistant internals and automated cleaning-in-place that tolerate acidic or alkaline broths gain a competitive edge over pharmaceutical-only platforms. Industrial biotech growth, therefore, diversifies vendor revenue streams beyond therapeutics and buffers against drug development cyclicality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Volatility for Medical-Grade Plastic Polymers | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| High Capital Expenditure for Large-Scale Stainless-Steel Facilities | -0.6% | Global, especially emerging markets | Medium term (2-4 years) |

| Limited Availability of Skilled Bioprocess Engineers | -0.7% | Global | Short term (≤ 2 years) |

| Environmental Concerns Over Single-Use Waste Disposal | -0.5% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Volatility for Medical-Grade Plastic Polymers

Spikes of 40%-60% in polyethylene and ethylene-vinyl-acetate resin pricing during 2021-2023 stabilized in 2024 but remain 25% above pre-pandemic levels, squeezing margins on single-use assemblies. Lead times for customized consumables increased from 12 weeks in 2019 to 26 weeks in 2024, forcing CDMOs to carry six months of safety stock, which ties up working capital. The EU’s Single-Use Plastics Directive exempts medical devices yet still pressures bioprocess suppliers to establish recycling schemes; Cytiva launched a European take-back program in 2025 to collect spent bags for mechanical recovery. Smaller manufacturers lack negotiating leverage with resin suppliers, creating a bifurcated market where top CDMOs secure favorable terms. At the same time, mid-tier players delay capacity plans, dampening bioreactor market growth in the short term.

High Capital Expenditure for Large-Scale Stainless-Steel Facilities

Building facilities with individual reactors exceeding 10,000 liters requires USD 300 million to USD 500 million in upfront spending and a three-to-five-year timeline. Samsung Biologics, for instance, invested USD 2.3 billion in Bio Campus 4, which brings 256,000 liters online in Songdo in 2025. Boehringer Ingelheim is investing EUR 500 million (approximately USD 540 million) in a German expansion, with four 15,000-liter units scheduled for completion in 2027. Such figures discourage new entrants in markets where access to low-cost debt is limited, particularly in India, Brazil, and South Africa. Consequently, many emerging-market firms opt for single-use capacity to avoid capital expenditure (capex) drag, but this choice limits maximum batch sizes and prevents direct competition for large biosimilar contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Single-Use Systems Reshape Capacity Economics

Full-scale monoclonal antibody sites maintained stainless-steel supremacy with a 47.00% share in 2025; however, single-use systems are projected to log a 10.10% CAGR to 2031 as cell and gene therapy pipelines expand. Single-use disposability eliminates the need for cleaning validation and reduces changeover times, attracting innovators who manage multiple low-volume products. Thermo Fisher’s DynaDrive 2.0 demonstrates how impeller redesign can reduce cell lysis by 30%, thereby strengthening the performance case for disposable formats.

The installed base of stainless-steel units exceeds 15,000 globally, and replacement cycles span two decades. Hybrid facilities, therefore, dominate the transition period as companies balance their sunk costs against the need for flexibility. Regulatory agencies now treat single-use and stainless steel equally for validation, erasing one of the final barriers that historically hindered adoption. As a result, the bioreactor market exhibits a clear bifurcation: legacy antibody plants continue to invest in scale, while new modalities prioritize agility over volume.

By Usage: Pilot-Scale Gains as Process Development Intensifies

Full-scale production captured 58.80% of the revenue in 2025, but pilot-scale reactors are set to expand at a 9.00% CAGR through 2031. As drug developers compress timelines, they run parallel optimization campaigns in 200-liter to 1,500-liter vessels before committing to capex-heavy commercial lines. Cytiva’s XDR-600 perfusion system exemplifies this bridge technology, allowing process-intensification trials ahead of 2,000-liter scale-up.

Lab-scale equipment remains critical for early discovery, yet budget sensitivity limits revenue upside. Meanwhile, utilization at mega facilities hovered near 70% in 2025, prompting firms to intensify upstream processes rather than add fresh tanks. This dynamic sustains healthy demand for pilot-scale units as companies seek to unlock hidden capacity before approving billion-dollar expansions.

By Scale: Above-1,500-Liter Reactors Capture Biosimilar Demand

Reactors between 200 and 1,500 liters held a 39.00% share in 2025, serving clinical supply and orphan-drug markets. Units above 1,500 liters are expected to grow at a 10.20% CAGR as biosimilar manufacturers in South Korea, China, and India strive to achieve a cost-of-goods below USD 100 per gram. Samsung Biologics’ 30,000-liter stainless-steel vessels produce 15,000 kilograms per batch, reducing per-gram costs by 35% compared to 10,000-liter lines.

Perfusion at 2,000 liters can match the output of 10,000-liter fed-batch systems by sustaining high cell densities for 60-day runs. This “virtual scale-up” value proposition appeals to companies that lack the capital or site footprint for mega tanks. Consequently, the bioreactor market sees divergent investment paths: emerging markets embrace vast stainless-steel formats for volume-driven biosimilars, while innovators invest in intensified mid-scale reactors for speed.

By Control Type: Automation Becomes Table Stakes

Automated systems with mass-flow controllers held a 64.00% share in 2025 and are expected to expand at an 8.50% CAGR. Sartorius added digital twin capabilities that reduced batch failures by 15% during tech transfers, easing regulatory audits. Thermo Fisher now embeds multi-analyte sensors for real-time glucose and lactate monitoring, extending exponential growth phases by 20% relative to fixed-feed cycles.

The FDA’s 2024 guidance, which favors continuous real-time release testing, accelerates demand for automation. Manual systems remain in academia and teaching labs, but are unlikely to regain ground in GMP production. Vendors, therefore, position entry-level automated benches below USD 50,000 to displace legacy gear and capture lifetime consumables revenue.

By Bioprocess: Continuous Systems Challenge Fed-Batch Orthodoxy

Fed-batch controlled 52.00% of 2025 revenue, but continuous systems are expected to grow at a 10.5% CAGR through 2031. Cytiva’s XDR-600 perfusion reactor achieved titers above 10 g/L over 60-day runs, demonstrating three-fold productivity increases. Lonza’s Portsmouth plant pivoted to perfusion, slashing volume needs from 20,000 liters to 6,000 liters for equal annual output.

In 2024, the EMA guidance confirmed that proven analytical controls can substitute for end-of-batch testing, thereby removing a key adoption hurdle. Fed-batch remains relevant for shear-sensitive proteins but faces a steady erosion of its share as next-gen platforms mature. Overall, the bioreactor market is experiencing a gradual yet decisive shift toward continuous operations.

By Application: Cell Therapy Redefines Design Rules

Pharmaceutical and biopharmaceutical companies generated 72.00% of the 2025 revenue, but cell and gene therapy applications are forecasted to expand at a 10.80% CAGR. Bristol Myers Squibb’s USD 380 million deal with Cellares brings closed-system platforms that cut manual steps by 70%. Gilead plans to quadruple CAR-T capacity by 2026, utilizing modular suites that can process eight patient batches in parallel, underscoring the need for compact, closed bioreactors.

Industrial biotechnology’s share currently stands at 8.00%, while alternative proteins and bio-based chemicals are increasing vendor diversification. Suppliers catering to corrosive broths and higher agitation needs carve out niches that pharmaceutical-only vendors cannot efficiently serve. This widening application base strengthens the long-term outlook for the bioreactor market even as drug pipelines fluctuate.

By End User: CDMOs Absorb Outsourcing Wave

Pharma companies still own large in-house fleets, but CDMOs recorded quicker expansion thanks to USD 10 billion of new capacity committed during 2024-2025. WuXi Biologics opened a EUR 325 million site in Ireland, featuring 48,000 liters of single-use mammalian culture capacity. Fujifilm Diosynth spent USD 850 million across three global sites, targeting demand for viral-vector and mRNA products.

Outsourcing allows small biotechs to conserve cash for R&D, while innovators retain early clinical work internally for IP reasons. Utilization rates now diverge: innovators operate about 50%, CDMOs exceed 80%. This dynamic reinforces a two-speed bioreactor market where service providers dominate new equipment orders.

Geography Analysis

North America accounted for 43.00% of 2025 revenue, underpinned by Project NextGen’s USD 5 billion funding and a high concentration of CDMOs. Thermo Fisher’s USD 660 million Massachusetts expansion and Lonza’s USD 1 billion New Hampshire project exemplify the region’s commitment to both stainless-steel and single-use throughput. Canada’s USD 1.6 billion Life Sciences Strategy reduced cross-border dependency by funding 1,500-liter hybrid lines in Toronto and Montreal. While deep talent pools in Boston and San Francisco sustain innovation, high labor costs and lengthy permitting cycles encourage some companies to expand to friendlier jurisdictions overseas.

The Asia-Pacific region is the fastest-growing geography, with an 8.30% CAGR through 2031. Samsung Biologics’ USD 2.3 billion Bio Campus 4 delivers 256,000 liters in South Korea, positioning the country as a biosimilar powerhouse targeting EU and U.S. markets. WuXi Biologics chose Singapore for a USD 1.8 billion site combining mammalian and microbial fermentation, reflecting the city-state’s aggressive incentives. AGC Biologics’ USD 350 million Yokohama project focuses on domestic cell-therapy capacity, while India’s Biocon and Dr. Reddy’s target large-scale antibody work despite regulatory headwinds.

Europe remains a stalwart despite complex rules. Germany, Switzerland, and Ireland secured USD 3 billion in commitments for 2024-2025. Boehringer Ingelheim allocates EUR 500 million for four 15,000-liter reactors in Biberach. Thermo Fisher’s EUR 780 million Cork plant will manufacture single-use components and feature a cell-therapy suite, supported by Ireland’s favorable tax regime. The United Kingdom’s GBP 520 million agreement with Moderna for mRNA supply underscores the government's willingness to underwrite capacity[2]Government of the United Kingdom, “Moderna Partnership Announcement,” gov.uk. Elsewhere, Saudi Arabia and Brazil plan smaller projects under national-self-sufficiency strategies, hinting at future contributions to the bioreactor market after 2027.

Regulatory Landscape

Regulation for bioreactor systems used in GMP manufacturing is shaped by drug-manufacturing requirements (FDA 21 CFR and EU GMP expectations) alongside equipment and quality-system standards that inform hygienic design and validation. ASME BPE-2026 continues to anchor design practices for bioprocess equipment, and ISO 13485 is commonly applied when bioreactor-related components fall under medical-device quality systems or supplier qualification programs.

For advanced therapies, regulators have moved toward more explicit CMC flexibility, which affects how end users specify automation, in-line analytics, and comparability packages for both single-use and stainless-steel systems. In May 2026, the FDA finalized guidance on CMC flexibilities for cell and gene therapy products, building on a staged, risk-based approach the agency highlighted in early 2026 for CGT oversight. Separately, U.S. policy also emphasized domestic manufacturing streamlining through a May 2025 White House executive action calling for reviews of duplicative requirements, and the FDA PreCheck Pilot Program (established in 2025) supports earlier facility engagement for high-priority domestic manufacturing projects.

Value Chain Analysis

The bioreactor value chain runs from upstream material inputs through equipment engineering, assembly, qualification, and lifecycle services to end users operating GMP and non-GMP facilities. Key inputs include stainless steel and engineered plastics for single-use flow paths (films, tubing, connectors), sensors and control hardware (including mass-flow controllers), and software for automation and data integrity; suppliers are qualified under GMP-aligned expectations that can include ISO 13485 and ASME BPE design conventions. Bioreactor OEMs and integrated platform vendors then provide core vessels, control systems, and proprietary consumables, followed by commissioning and installation qualification/operational qualification support, plus ongoing spare parts and consumables replenishment.

Demand is executed through direct biopharma procurement and, increasingly, through CDMOs that buy multi-site fleets to offer geographic redundancy and fast scale-up. Bottlenecks highlighted across advanced-therapy supply chains include constrained specialist labor in QA/QC, variability management during tech transfer, and upstream constraints such as plasmid DNA availability for viral-vector programs, which raises the value of modular suites, intensified processing, and automated, closed systems. Recent collaborations point to this execution layer, where CDMOs and platform providers use long-horizon supply agreements and end-to-end development partnerships to secure throughput and reduce scheduling friction for high-mix pipelines.

Competitive Landscape

Sartorius, Thermo Fisher Scientific, and Danaher’s Cytiva division hold roughly 45%-50% of global revenue, leveraging hardware-consumable-software bundles to lock customers into proprietary ecosystems. Sartorius invested EUR 1 billion in Göttingen during 2024 to increase single-use bag output and shorten lead times amid resin shortages. Thermo Fisher pursues vertical integration by acquiring a specialty film producer in 2024 to secure raw materials for DynaDrive bags. Danaher focuses on digital integration; Cytiva’s data-rich platforms enable predictive maintenance, reducing unplanned downtime by 20%.

Mid-tier firms like Eppendorf and Getinge compete through niche plays such as lower-priced modular benches or stainless-steel systems for legacy lines. Disruptors like PBS Biotech employ vertical-wheel mixing to minimize shear stress, winning contracts with gene-therapy developers. Continuous manufacturing and industrial-biotech niches remain open as adoption sits below 10% of the installed base, giving smaller vendors room to differentiate. ISO 13485 compliance and FDA validation maintain high entry barriers, but shift toward modular designs and software-defined control lowers switching costs, keeping the competitive field dynamic.

Bioreactor Industry Leaders

Sartorius AG

Thermo Fisher Scientific Inc.

Eppendorf AG

Merck KGaA

Danaher Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are concentrated where rapid capacity deployment meets predictable, audit-ready process control for high-mix biologics and advanced therapies. The market is seeing tangible moves toward repeatable, modular capacity blocks that standardize around 2,000 L single-use trains and larger stainless-steel units where biosimilar scale economics dominate. In June 2026, for instance, Chime Biologics inaugurated a new GMP-2 manufacturing facility in Wuhan equipped with eight 2,000-liter single-use bioreactors. In the same period, Lotte Biologics highlighted accelerated commercial production readiness for its 120,000-liter Songdo Plant 1 with eight 15,000-liter stainless-steel bioreactors.

Opportunities also concentrate in software-defined manufacturing and automation layers that reduce batch-release and tech-transfer friction across sites, especially as regulators formalize more flexible CMC approaches for cell and gene therapy. End users are operationalizing dual-site and two-track strategies to manage supply-chain and regional access risks, which increases pull for vendors that can qualify equivalent performance across different facilities and geographies. Capacity expansion announcements such as Celltrion's March 2026 investment plan spanning Songdo and Branchburg (with a stated total capacity target of 571,000 liters) reinforce the scale and speed premium placed on standardized reactor platforms, validated control strategies, and robust consumables supply.

Recent Industry Developments

- May 2026: Sartorius Stedim Biotech opened a new competence center in Freiburg, Germany, for producing critical cell and gene therapy components, supported by an investment of more than EUR 140 million. The added regional capability supports supply assurance for single-use and closed-system workflows where component availability can constrain manufacturing schedules.

- December 2025: PBS Biotech unveiled the MiniPRO platform, a multi-parallel Vertical-Wheel bioreactor designed for high-throughput cell therapy process development. The platform targets faster process screening and more efficient scale-up decisions, aligning with compressed development timelines in advanced therapies.

- October 2024: Univercells Technologies by Donaldson introduced the scale-X nexo bioreactor, a compact fixed-bed system with a 0.5 m2 growth surface for cell culture process development across multiple modalities. The launch expanded options for adherent and fixed-bed processes where footprint and scalability constraints shape equipment selection.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenue from new bioreactor systems (vessels and core control functions) used to grow cells or microbes for research, process development, and commercial production across life science and industrial bioprocessing.

Scope exclusions: Excludes wastewater or effluent-treatment bioreactors, refurbished or resold units, and stand-alone automation skids that are not supplied as a bioreactor system.

Segmentation Overview

- By Type

- Glass

- Stainless Steel

- Single-Use

- By Usage

- Lab-Scale Production

- Pilot-Scale Production

- Full-Scale Production

- By Scale

- 5 L - 20 L

- 20 L - 200 L

- 200 L - 1,500 L

- Above 1,500 L

- By Control Type

- Manual

- Automated (MFCs)

- By Bioprocess

- Batch

- Fed-Batch

- Continuous

- By Application

- Pharmaceutical & Biopharmaceutical Manufacturing

- Cell & Gene Therapy

- Industrial Biotechnology (Biofuels, Enzymes)

- By End User

- Biopharma & Pharma Companies

- Contract Development & Manufacturing Organisations (CDMOs)

- Other End Users

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest Of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest Of Asia-Pacific

- Middle East And Africa

- GCC

- South Africa

- Rest Of Middle East And Africa

- South America

- Brazil

- Argentina

- Rest Of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map the demand pool and set the boundaries before any sizing math was run. We relied on public sources such as US FDA biologics and approvals information, US NIH funding and award databases, and US Census trade and manufacturing statistics to understand the direction of bioprocess investments.

We also reviewed sources such as WHO vaccine and biologics publications, OECD and World Bank macro indicators used for normalization, and peer-reviewed bioprocess engineering journals that explain scale-up practices and typical working volumes. To cross-check supply-side signals, we used company filings, investor presentations, earnings call notes, and reputable press coverage of capacity additions and facility expansions. Where needed, paid subscriptions for company financials and a patent database were referenced to reduce gaps for private players and track technology shifts. These examples are not exhaustive, and many other public and paid sources were consulted for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work converted the desk inputs into assumptions that could be used consistently across regions, and then those assumptions were pressure tested against what buyers reported in the field. We spoke with a mix of equipment-side experts, bioprocess engineers, and procurement or operations leaders at end users such as biopharma manufacturing and research labs, covering APAC, EMEA, and the Americas so regional adoption and pricing differences were not averaged away.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 18% | APAC: 41% |

| Mid tier: 53% | Functional/Unit leaders: 36% | EMEA: 32% |

| Smaller Players: 18% | Managers: 46% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand reconstruction, where biologics and industrial bioprocess activity is translated into required working volumes and reactor counts by region, and then converted to value using typical system pricing. The totals are subsequently checked with selective bottom-up approximations, including sampled average selling price ranges by scale band multiplied by estimated unit demand, followed by distributor and integrator channel checks.

In the model, key inputs include installed and announced biomanufacturing capacity additions, the typical scale mix (lab, pilot, and production), the shift between single-use and stainless steel systems, lead times that affect delivery recognition, and pricing changes linked to automation level and control features (for example, manual versus automated control). We also track application-side signals such as vaccine and biologics pipeline intensity, funding cycles for research labs, and the timing of new facility commissioning, which often moves orders in waves.

Forecasts are built using scenario analysis around capacity build-outs and utilization ramp curves, then adjusted using what interviewees expect on near-term ordering, supply constraints, and budget cycles. When granular unit data is missing for smaller countries, we use proxy indicators such as biopharma production footprint, R&D intensity, and import activity for bioprocess equipment to fill gaps before totals are rolled up.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent checks, including supply-side signals, end-user demand indicators, and pricing sanity checks by scale and control type. Variances are reviewed region by region, and outliers are challenged by re-checking the underlying drivers, followed by a second analyst review before final sign-off.

We refresh the report annually so the base year and near-term assumptions stay aligned with what the industry is actually buying. If a material event happens between cycles, such as a major capacity announcement or a sharp price reset, the model is revisited and select experts are re-contacted to confirm whether the change is temporary or structural. Before delivery, a final pass is done to ensure the latest updates are reflected in the numbers and narrative.

Mordor Intelligence's Bioreactor Market Size Measured Against Other Published Estimates

Published bioreactor market values can look far apart, even when they are describing similar equipment. The main reasons usually come down to what is counted as a bioreactor system, which year is treated as the current estimate, and how aggressively future adoption and pricing are projected.

The table shows a wide spread because some sources bundle adjacent categories and use faster growth assumptions for newer use cases. The table points to this scope effect, and in Mordor Intelligence's model, only new bioreactor vessels of 5 liters and above (including stainless-steel, glass, and single-use formats) are counted, while wastewater-treatment reactors, refurbished units, and stand-alone automation skids are kept out.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.09 B (2026) | |

| Market Publisher A | USD 13.27 B (2025) | Uses an earlier base year and a broader inclusion set by segmenting heavily by molecules and end uses, which can pull in a wider equipment universe and related spending that is not strictly new bioreactor systems. |

| Market Publisher B | USD 18.50 B (2026) | Applies a higher growth profile and often treats the market more expansively across capacity bands and user groups, which can inflate totals if accessories, services, or non-core system elements are blended into the equipment value. |

Taken together, the comparison suggests that the biggest driver is what is included around the core vessel and controls, followed by timing and growth posture. By keeping the model tied to clear equipment boundaries and checking outputs against real-world build-out and purchasing signals, the result is easier to reproduce and track year to year.

Key Questions Answered in the Report

How large is the bioreactor market in 2026 and what CAGR is expected to 2031?

The bioreactor market size is USD 6.09 billion in 2026 and is forecast to reach USD 8.58 billion by 2031 at a 7.10% CAGR.

Which bioreactor type is growing the fastest through 2031?

Single-use systems lead growth with a projected 10.10% CAGR, driven by cell and gene therapy manufacturing needs.

Why is Asia-Pacific the fastest-growing region for bioreactors?

Regional policies in Singapore, South Korea, and China fund large-scale capacity, supporting an 8.30% CAGR through 2031.

What is driving adoption of continuous bioprocessing?

Perfusion reactors can triple productivity and lower facility capex by up to 40.00%, prompting a forecast 10.5% CAGR for continuous systems.

How are supply-chain issues affecting single-use bioreactor adoption?

Elevated resin prices and longer lead times increase working capital needs, but recycling programs and dual-sourcing strategies mitigate long-term risk.

Page last updated on: