In-vitro Transcription Templates Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

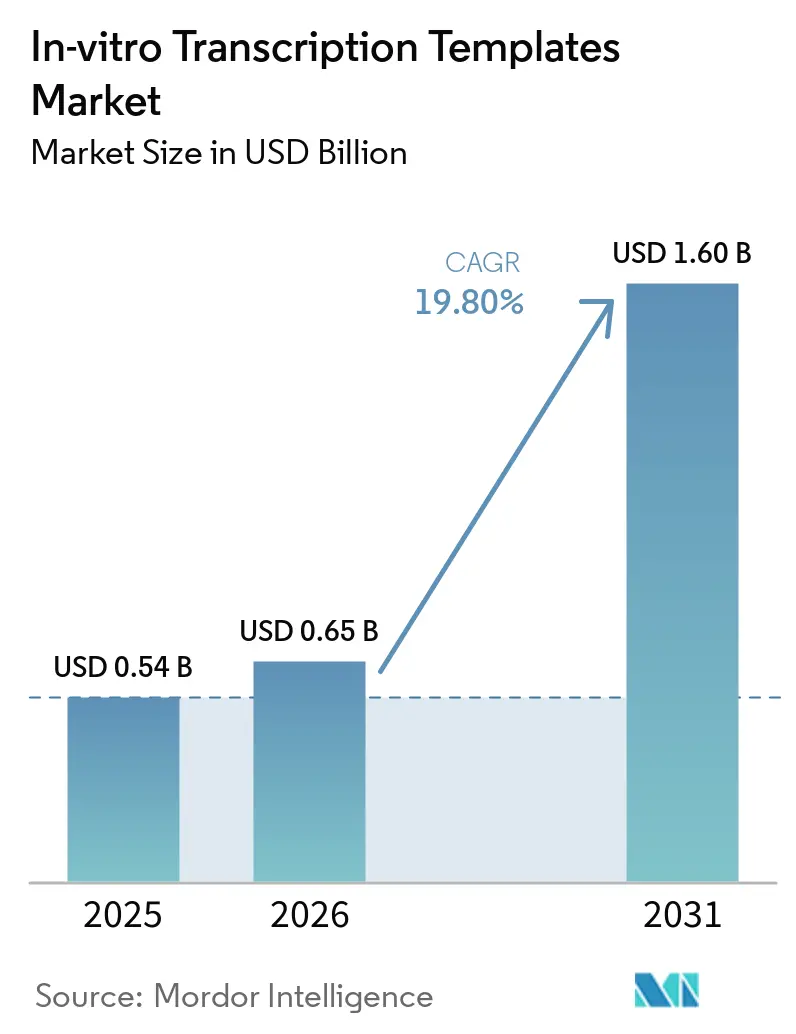

| Market Size (2026) | USD 0.65 Billion |

| Market Size (2031) | USD 1.60 Billion |

| Growth Rate (2026 - 2031) | 19.80% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

In-vitro Transcription Templates Market Analysis by Mordor Intelligence

The In-vitro Transcription Templates Market size is expected to grow from USD 0.54 billion in 2025 to USD 0.65 billion in 2026 and is forecast to reach USD 1.60 billion by 2031 at 19.80% CAGR over 2026-2031.

Persistent demand for high-fidelity RNA starting materials is sustaining capacity expansions even after the pandemic emergency. Drug sponsors are transitioning from single-product mRNA vaccine initiatives to diversified pipelines focusing on oncology, rare diseases, and gene editing. This diversification is increasing template complexity, driving the need for sequence-verified, endotoxin-free constructs that comply with residual host-cell DNA thresholds established by regulatory authorities in 2024. Contract manufacturers are addressing this demand by implementing analytical ultracentrifugation and next-generation sequencing at the batch-release stage, resulting in downstream mRNA yield improvements of 15% to 25%. Regionally, North America maintains regulatory leadership, while significant capital investments in Asia-Pacific are gradually shifting the industry's focus eastward.

Key Report Takeaways

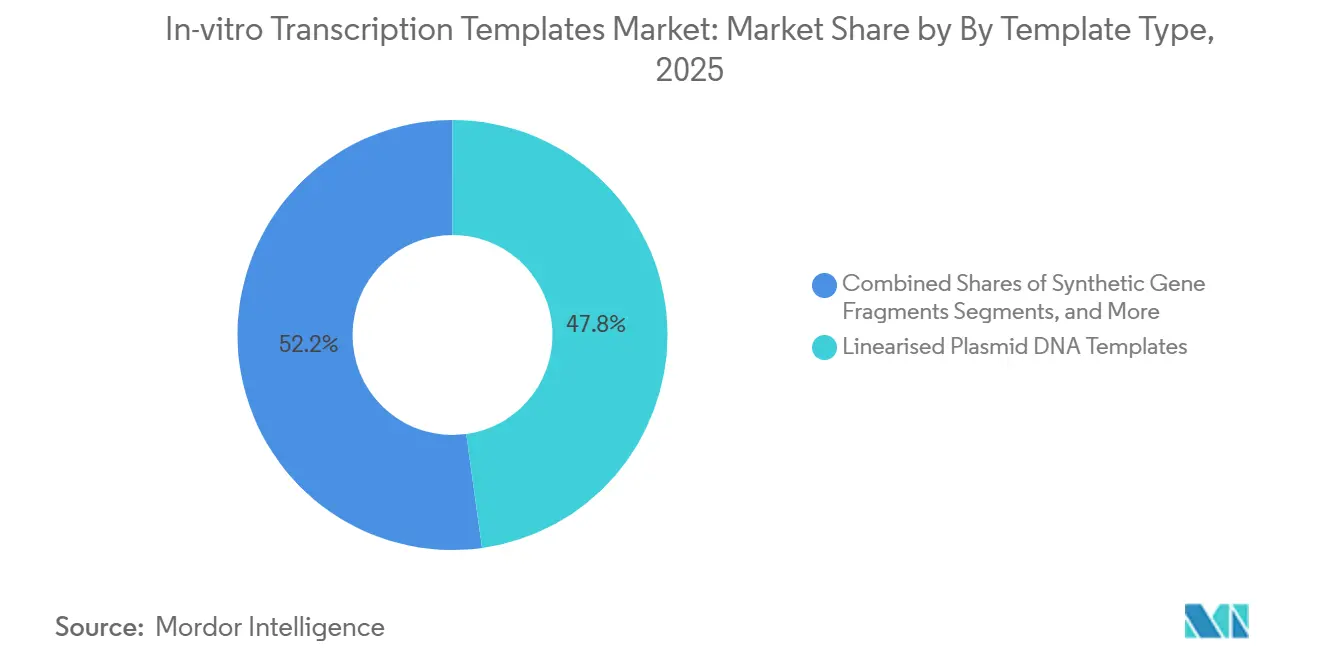

- By template type, linearised plasmid DNA templates led with 47.8% of the in-vitro transcription templates market share in 2025, and synthetic gene fragments are forecast to expand at a 20.45% CAGR through 2031, the fastest among template types.

- By application, mRNA therapeutics and vaccines accounted for 52.3% of the in-vitro transcription templates market size in 2025, and cell and gene therapy applications are advancing at a 22.5% CAGR to 2031, outpacing vaccine demand.

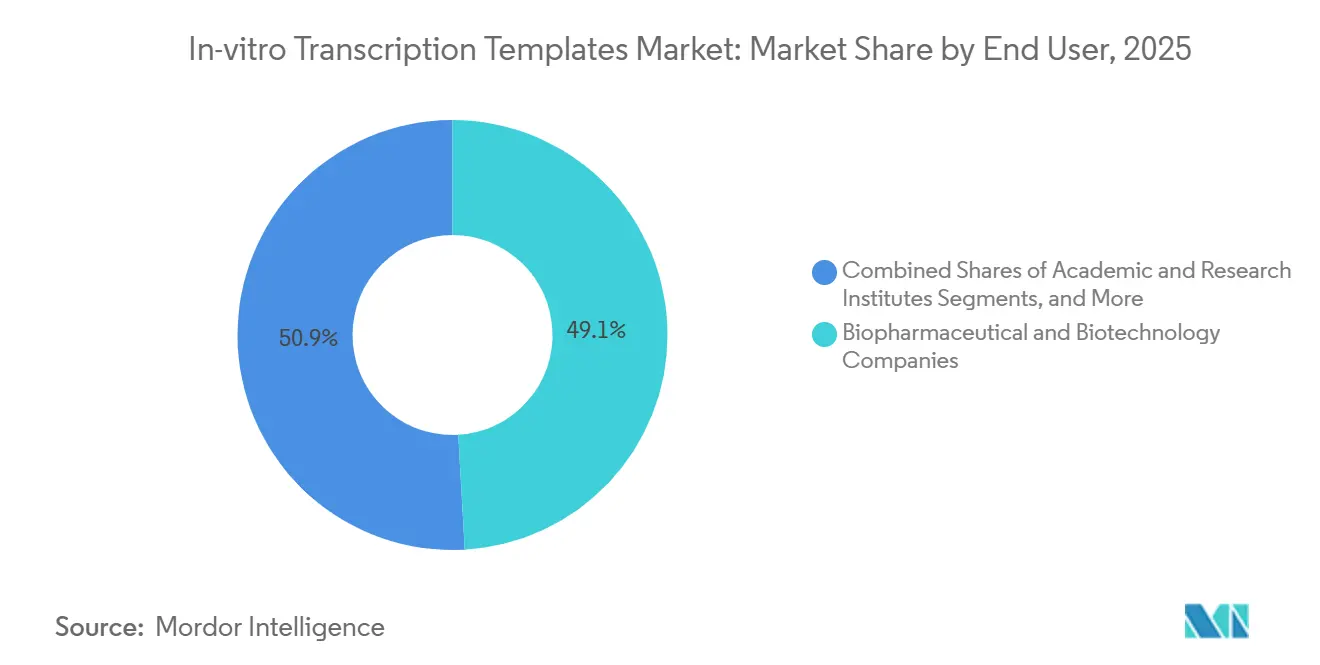

- By the end of 2025, biopharmaceutical and biotechnology companies held 49.1% share of end-user demand, in 2025 and contract research and manufacturing organizations are projected to grow at a 19.78% CAGR through 2031.

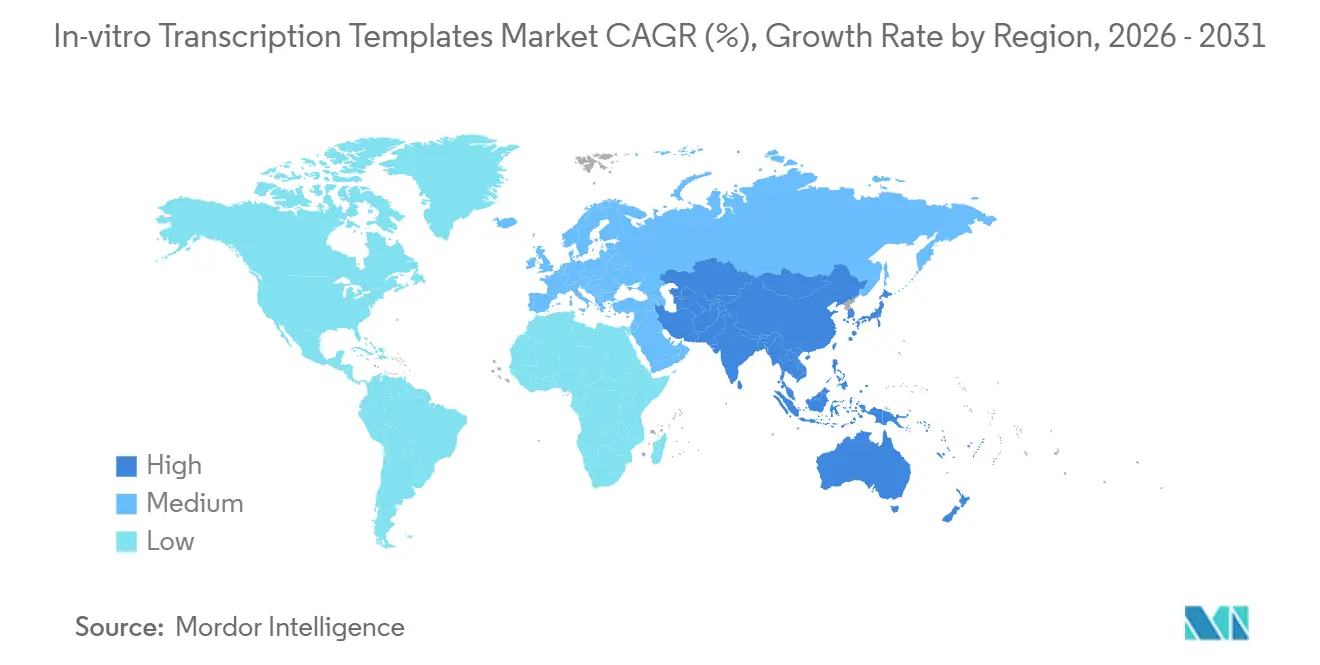

- By geography, North America commanded 39.61% share in 2025, and Asia-Pacific is forecast to register a 21.34% CAGR through 2031, the fastest among regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global In-vitro Transcription Templates Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid scale-up of mRNA vaccine manufacturing | +4.2% | Global, concentrated in North America, Europe, APAC hubs | Medium term (2-4 years) |

| Growing adoption of CRISPR guide RNA synthesis | +3.8% | North America and Europe, spill-over to APAC research institutes | Medium term (2-4 years) |

| Rising investments in cell & gene therapy CDMOs | +3.5% | Global, with APAC core expansion in China, India, Japan, South Korea | Long term (≥4 years) |

| Advent of synthetic biology foundries standardizing IVT workflows | +2.9% | North America and Europe, early adoption in Singapore and Australia | Long term (≥4 years) |

| Biopharma demand for GMP-grade linearised plasmid templates | +3.1% | Global, driven by FDA, EMA, PMDA regulatory influence | Short term (≤2 years) |

| Cloud-based automation of template design & error-checking | +2.3% | Global, with technology leaders in North America and Israel | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

mRNA Vaccine Manufacturing Expands Rapidly

As pandemic-era demand stabilizes, the In-vitro Transcription Templates market continues to grow, driven by seasonal influenza initiatives and oncology pipelines. In 2024, Moderna expanded its Norwood, Massachusetts, facility by 200,000 square feet to enhance its multi-product mRNA production capacity.[1]Moderna, “Facility Expansion Announcement,” modernatx.com In June 2024, the FDA introduced a new benchmark requiring sponsors to maintain residual host-cell DNA levels below 10 ng per dose.[2]U.S. Food and Drug Administration, “Quality Considerations for Plasmid DNA Vaccines,” fda.gov Template suppliers are adopting next-generation sequencing for lot release, which, while increasing per-unit costs, improves downstream transcription yields by up to 25%. In 2025, efforts to accelerate synthetic DNA template development for rapid-response vaccine platforms further reinforced the demand for high-purity templates.

CRISPR Guide-RNA Synthesis Services See Rising Adoption

As clinical programs transition from ex vivo edits to in vivo delivery, the demand for guide-RNA volumes per patient is increasing, along with higher standards for template quality. By 2025, significant production of cGMP guide-RNA batches supported multiple investigational new-drug applications. Advanced cloud design engines now integrate off-target prediction with IVT template optimization, identifying secondary structures in the T7 promoter that can reduce transcription efficiency by 40%. While the FDA modernized its gene-therapy framework in 2024, the European Medicines Agency has yet to align its purity specifications fully, requiring global sponsors to comply with dual regulatory standards.

Surge in Investments for Cell & Gene Therapy CDMOs

With a growing trend toward outsourcing, contract developers are heavily investing in dedicated plasmid suites. In 2025, a major facility was launched in Yokohama with a significant investment to provide gene and cell therapy services, with plans to add mRNA capacity by 2026. Gross margins for GMP plasmid templates at CDMOs range between 40–60%, significantly exceeding those of recombinant proteins.[3]AGC Biologics, “Yokohama Facility Investment,” agcbio.com This profitability has attracted new entrants, even as bioprocessing equipment orders slowed during 2024–2025. As a result, the In-vitro Transcription Templates market benefits from both organic and outsourced demand streams.

Synthetic Biology Foundries Revolutionize IVT Workflows

Automated foundries are significantly reducing design–build–test cycles from months to weeks. In 2025, a new platform was introduced, achieving plasmid DNA yields exceeding 1 g/L through AI-driven media optimization. By the end of 2026, a leading company plans to operate 60% of its global capacity on AI-driven “lights-out” production lines. Standardization minimizes human error and enhances reproducibility, which is critical for regulatory submissions that depend on consistent template performance.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Batch-to-batch variability in T7 polymerase yields | -2.1% | Global, acute in regions lacking enzyme-engineering capacity | Short term (≤2 years) |

| Limited availability of gmp-compliant nucleotide raw materials | -1.8% | Global, with supply concentration in North America and Europe | Medium term (2-4 years) |

| IP cross-licensing disputes on promoter sequences | -1.3% | North America and Europe | Long term (≥4 years) |

| Environmental regulations on plasmid-prep waste streams | -1.1% | Europe, emerging in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Batch-to-Batch Variability in T7 Polymerase Yields

Wild-type T7 polymerase lots experience activity variations of 20% to 40%, resulting in the generation of double-stranded RNA contaminants that reduce translation efficiency. A 2024 study demonstrated that a G47A+884G mutant enzyme decreased dsRNA formation by 85%. However, scaling up production remains a challenge, as fermentation titers are 30% lower compared to the wild type. To mitigate the risk of low-activity lots, sponsors often procure excess enzyme, increasing the cost of goods by 10% to 15%. Additionally, implementing real-time activity assays extends delivery timelines by 2 to 3 weeks, exposing the In-vitro Transcription Templates market to potential scheduling delays.

Limited Availability of GMP-Compliant Nucleotide Raw Materials

Fewer than 10 suppliers worldwide can provide GMP-grade nucleotide triphosphates at scale. Roche’s enzymatic synthesis approach minimizes metal-ion contamination, but production capacity remains limited to pilot scale. Thermo Fisher prioritizes its GMP nucleotides for long-term contracts, leaving spot buyers vulnerable during periods of high demand. Delays in nucleotide supply can disrupt production lines that are otherwise ready, negatively impacting the revenue potential of the In-vitro Transcription Templates market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Template Type: Plasmid DNA Anchors, Synthetic Fragments Accelerate

In 2025, linearised plasmid DNA templates accounted for 47.8% of the In-vitro Transcription Templates market, reflecting their longstanding regulatory acceptance and compatibility with established mRNA workflows. However, the market for synthetic gene fragments is projected to grow significantly, with a strong 20.45% CAGR. A notable development in 2025 was the commercialization of ENFINIA IVT-Ready DNA, which offers delivery in under seven days, significantly faster than the traditional 4-6 week plasmid cloning timeline. Sequence-verified fragments streamline processes by bypassing fermentation, eliminating endotoxin remediation, and reducing the risk of host-cell DNA contamination.

By Application: CRISPR Therapeutics Outpace Vaccine Demand

In 2025, mRNA therapeutics and vaccines captured 52.3% of the In-vitro Transcription Templates market share. However, demand for Guide-RNA is growing rapidly as cell and gene therapy programs advance from preclinical to clinical stages. The market size for In-vitro Transcription Templates dedicated to CRISPR applications is expected to grow at a robust 22.5% CAGR through 2031. In 2025, significant milestones included the delivery of 50,000 custom guide RNAs and support for multiple INDs, reflecting the maturation of regulatory pathways. In-vivo editing requires larger guide-RNA payloads per patient compared to ex-vivo, driving a substantial increase in template volumes.

By End User: CDMOs Capture Outsourcing Wave

In 2025, biopharmaceutical and biotechnology companies generated 49.1% of the revenue. However, outsourcing is gaining momentum as companies increasingly rely on contract research and manufacturing organizations (CDMOs). These organizations are growing at a strong 19.78% CAGR as sponsors seek to offload plasmid linearization, avoiding clean-room capital costs estimated at USD 15 to 25 million. A new 128,000-square-foot facility opened in 2025, strategically co-locating plasmid, AAV, and lentiviral services to streamline operations. Additionally, a major biocampus investment integrates mRNA suites with antibody-drug conjugate lines, positioning CDMOs for multi-product master service agreements.

Geography Analysis

In 2025, North America held a 39.61% market share, supported by FDA guidance that sets global purity standards and the strong presence of established industry players. However, the Asia-Pacific region is expected to grow significantly, with a projected 21.34% CAGR in the In-vitro Transcription Templates market through 2031. Major investments in the region include a large-scale biocampus featuring advanced cell-gene therapy and mRNA suites. Plans to automate a significant portion of global capacity by 2026 further enhance the region's competitive edge. In Europe, growth is moderated by hazardous-waste fees under regulatory directives, prompting the adoption of closed-loop bioreactors despite their high costs.

Emerging regions remain below a 10% market share. India is advancing in the value chain with the announcement of a significant biologics CDMO facility in 2026, signaling its ambition to compete in this space. Dual-sourcing strategies are becoming increasingly common as companies balance regulatory certainty in North America and Europe with cost efficiencies in the Asia-Pacific region.

Competitive Landscape

The In-vitro Transcription Templates market exhibits a moderate concentration. The top five players, including Danaher (comprising Aldevron and Cytiva), Thermo Fisher Scientific, GenScript, Maravai LifeSciences, and Merck KGaA, collectively account for 50–60% of the market share, with none exceeding 15%. In its 2026 earnings call, Danaher emphasized its expanded capacities at Cytiva's single-use systems and Aldevron's plasmid facilities, reinforcing its vertical integration strategy. Maravai strategically acquired Molecular Assemblies’ FES enzymatic DNA synthesis platform in January 2025 to mitigate potential disruptions in plasmid workflows. Meanwhile, Merck KGaA’s MilliporeSigma division is piloting a continuous-flow plasmid purification method, targeting a 40% reduction in buffer consumption.

New entrants are focusing on speed. Elegen offers a 7-day delivery for sequence-verified fragments, while DNA Script’s benchtop printer provides same-day service for templates up to 10 kb. Established players are responding by integrating AI for error correction and optimizing supply chains from nucleotide synthesis to the final fill-finish stage. Regulatory compliance remains a significant barrier, as the FDA’s residual DNA limit of 10 ng per dose requires orthogonal analytics, increasing the capital expenditure for new entrants without GMP-compliant facilities.

In-vitro Transcription Templates Industry Leaders

Thermo Fisher Scientific Inc.

New England Biolabs Inc.

Promega Corporation

Agilent Technologies Inc.

OriGene Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Aurobindo Pharma’s TheraNym unit announced a USD 150–175 million investment in a 60-kiloliter mammalian facility for MSD, widening India’s biologics CDMO footprint.

- March 2025: WuXi Biologics introduced its EffiX platform, reaching plasmid DNA yields above 1 g/L via AI-driven media optimization.

- January 2025: Maravai LifeSciences acquired Molecular Assemblies’ enzymatic DNA synthesis technology, integrating rapid-template capability.

- January 2025: Applied DNA Sciences commissioned a GMP site for LineaDNA linear templates and partnered with Alphazyme to scale RNAP for commercial launch in late 2026.

Global In-vitro Transcription Templates Market Report Scope

As per the scope of the report, in vitro transcription (IVT) templates are specialized, cell-free DNA sequences (linearized plasmids or PCR products) containing a specific promoter recognized by RNA polymerase (e.g., T7, T3, or SP6). They serve as blueprints for generating RNA molecules, including mRNA for vaccines and synthetic biology studies.

The In-Vitro Transcription Templates Market is segmented into template type, application, end user, and geography. By template type, the market is segmented into linearised plasmid DNA templates, synthetic gene fragments, PCR amplicon templates, oligonucleotide templates, and others. By application, the market is segmented into mRNA therapeutics & vaccines, cell & gene therapy (CRISPR gRNA, siRNA), diagnostic probes, RNA structural studies, and synthetic biology & protein engineering. By end user, the market is segmented into biopharmaceutical & biotechnology companies, contract research & manufacturing organizations (CROs & CMOs), academic & research institutes, and clinical & diagnostic laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and trends for 17 countries across major regions worldwide. The report offers market size and forecasts in value (USD) for the above segments.

| Linearised Plasmid DNA Templates |

| Synthetic Gene Fragments |

| PCR Amplicon Templates |

| Oligonucleotide Templates |

| Others |

| mRNA Therapeutics & Vaccines |

| Cell & Gene Therapy (CRISPR gRNA, siRNA) |

| Diagnostic Probes |

| RNA Structural Studies |

| Synthetic Biology & Protein Engineering |

| Biopharmaceutical & Biotechnology Companies |

| Contract Research & Manufacturing Organisations (CROs & CMOs) |

| Academic & Research Institutes |

| Clinical & Diagnostic Laboratories |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Template Type | Linearised Plasmid DNA Templates | |

| Synthetic Gene Fragments | ||

| PCR Amplicon Templates | ||

| Oligonucleotide Templates | ||

| Others | ||

| By Application | mRNA Therapeutics & Vaccines | |

| Cell & Gene Therapy (CRISPR gRNA, siRNA) | ||

| Diagnostic Probes | ||

| RNA Structural Studies | ||

| Synthetic Biology & Protein Engineering | ||

| By End User | Biopharmaceutical & Biotechnology Companies | |

| Contract Research & Manufacturing Organisations (CROs & CMOs) | ||

| Academic & Research Institutes | ||

| Clinical & Diagnostic Laboratories | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the In-vitro Transcription Templates market expected to grow?

The In-vitro Transcription Templates market size is forecast to rise from USD 0.65 billion in 2026 to USD 1.6 billion by 2031, reflecting a 19.8% CAGR.

Which template type commands the largest share today?

Linearised plasmid DNA templates led with 47.8% of the In-vitro Transcription Templates market share in 2025, thanks to established regulatory acceptance.

What is the fastest-growing application segment?

Cell and gene therapy programs that rely on CRISPR guide-RNA synthesis are projected to expand at a 22.5% CAGR through 2031, outpacing vaccine applications.

Why are CDMOs gaining traction?

Sponsors facing USD 15.25 million capex for GMP plasmid suites prefer outsourcing; CDMOs therefore capture business at a 19.78% CAGR by offering turnkey template services.

Which region will post the highest growth to 2031?

Asia-Pacific is expected to register a 21.34% CAGR, propelled by large-scale investments from Samsung Biologics and GenScript that add mRNA and gene-therapy capacity.

What regulatory threshold shapes template purity?

FDA draft guidance issued in June 2024 stipulates residual host-cell DNA levels below 10 ng per dose, pushing suppliers toward advanced analytics and orthogonal purification.

Page last updated on: