Nano-biotechnology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

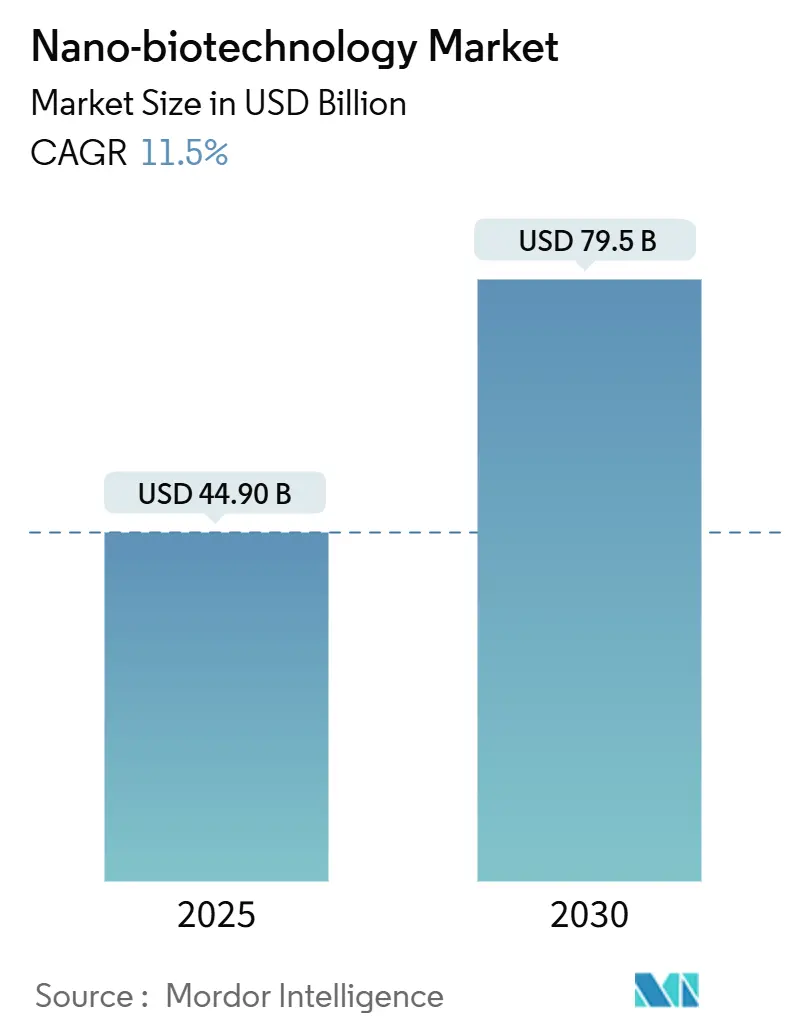

| Market Size (2025) | USD 44.90 Billion |

| Market Size (2030) | USD 79.5 Billion |

| Growth Rate (2025 - 2030) | 11.50% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nano-biotechnology Market Analysis by Mordor Intelligence

The nano-biotechnology market size reached USD 44.9 billion in 2025 and is forecast to register an 11.5% CAGR to reach USD 79.5 billion by 2030. The market size expansion mirrors the steady maturation of nano-enabled drug delivery, diagnostics, regenerative medicine and environmental applications. Precision-targeted lipid and polymer nanocarriers, sharply rising FDA and EMA approvals of nano-enabled therapeutics, and falling lab-on-chip fabrication costs are widening commercial adoption. Large-scale public funding through programs such as the EU Cancer Mission and the United States Advanced Manufacturing Technologies Designation Program continues to de-risk research pipelines while distributed tabletop nanomanufacturing reduces supply-chain exposure during health emergencies. Competition remains active as pharmaceutical majors partner with specialist firms to access nanotechnology expertise. Yet, headline risks tied to metallic nanoparticle toxicity, capital-intensive good-manufacturing-practice (GMP) plants, and uneven global nano-waste rules temper investor confidence.

Key Report Takeaways

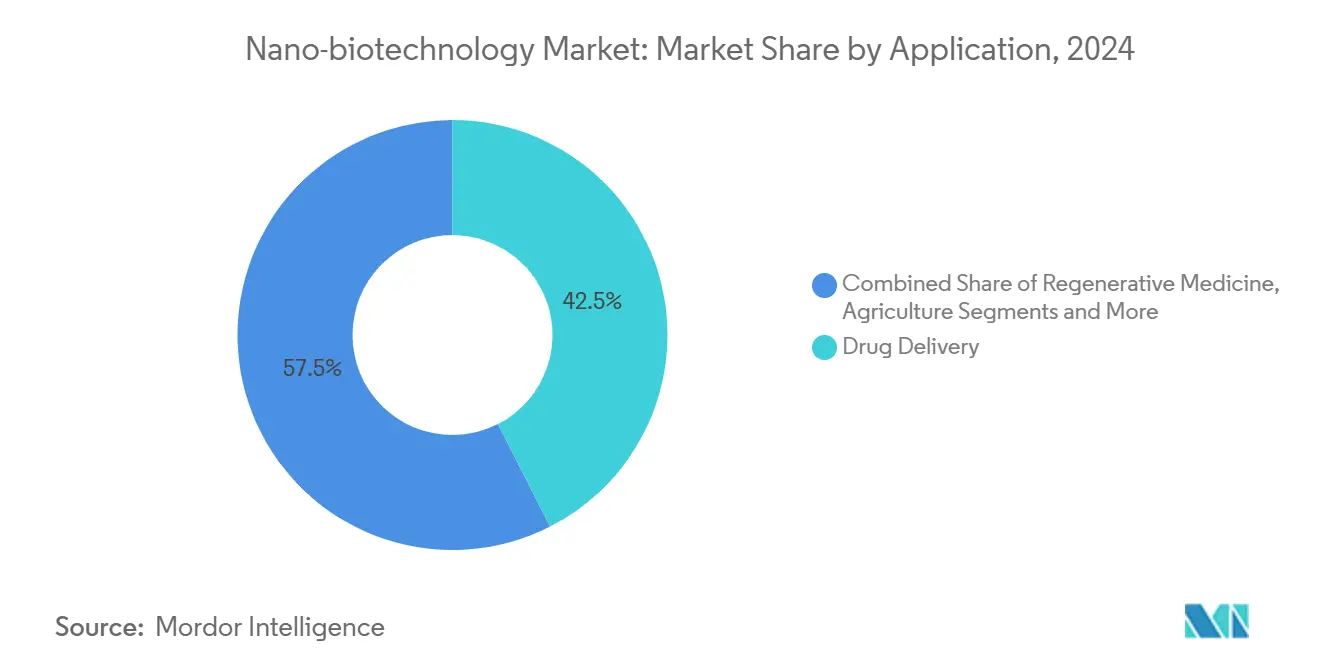

- By application, drug delivery led with 42.5% nano-biotechnology market share in 2024, while regenerative medicine is forecast to expand at a 16.8% CAGR through 2030.

- By nanomaterial type, lipid-based nanocarriers held 28.1% share of the nano-biotechnology market size in 2024 and DNA/RNA origami structures are projected to advance at an 18.9% CAGR to 2030.

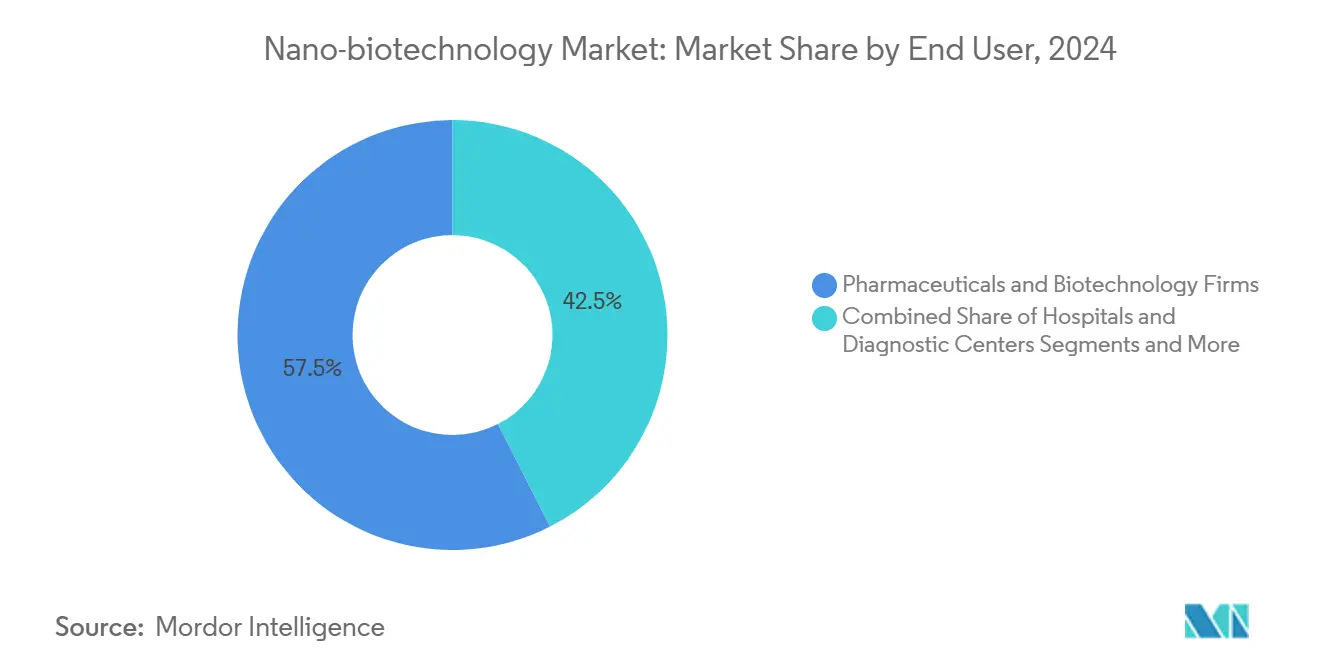

- By end-user industry, pharmaceuticals and biotechnology commanded 57.5% revenue share in 2024, whereas hospitals and diagnostic centers are expected to post a 13.4% CAGR through 2030.

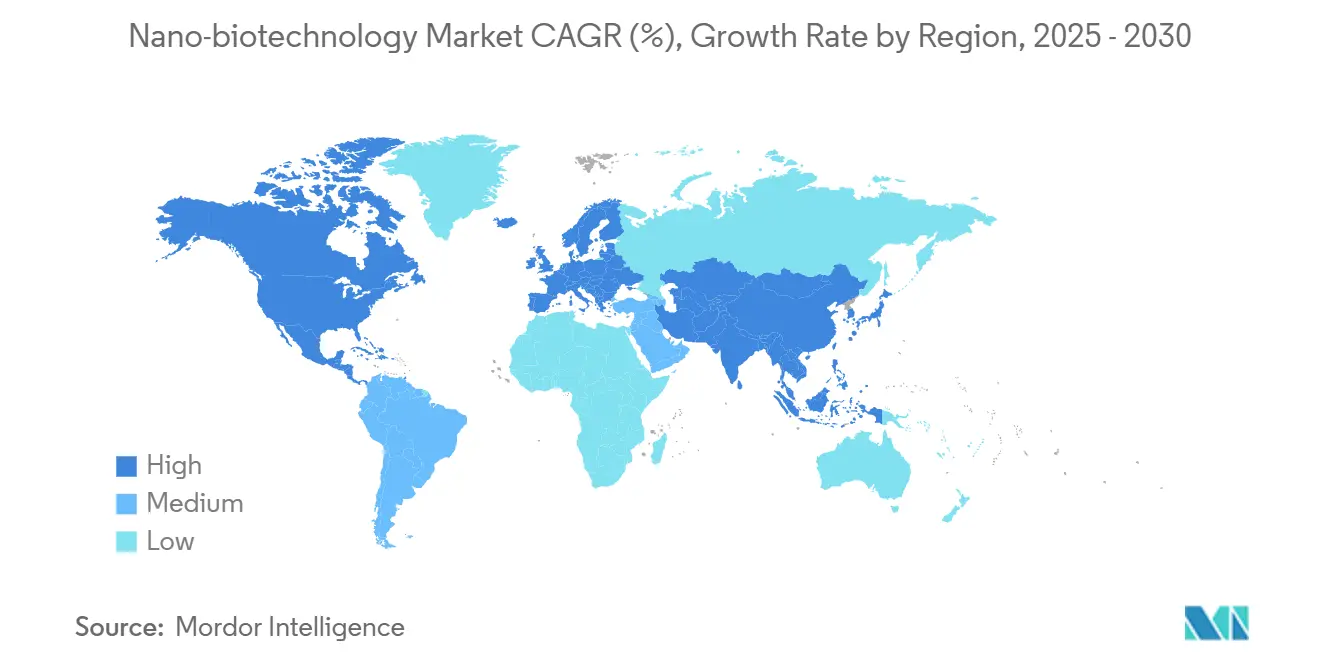

- By geography, North America accounted for 39.2% of the nano-biotechnology market size in 2024, and the Asia Pacific is anticipated to record the fastest 13.6% CAGR up to 2030.

Global Nano-biotechnology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Precision-Targeted Drug-Delivery Success With Lipid & Polymer Nano-Carriers | +2.80% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Surge In FDA/EMA Approvals Of Nano-Enabled Therapeutics & Diagnostics | +2.10% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Rapid Cost Decline Of Lab-On-Chip Nanofabrication Tools | +1.90% | Global, with early adoption in APAC manufacturing hubs | Medium term (2-4 years) |

| Government Nanomedicine Megaprojects (E.G., EU Cancer Mission) | +1.60% | EU core, North America, selective APAC markets | Long term (≥ 4 years) |

| In-Silico Nano-Material Design Via Generative AI Platforms | +1.40% | Global, with concentration in tech-advanced regions | Short term (≤ 2 years) |

| Distributed Tabletop Nanomanufacturing For On-Site Vaccine Production | +1.20% | Global, with priority in pandemic-vulnerable regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Precision-targeted Drug-Delivery Success with Lipid & Polymer Nano-Carriers

Lipid nanoparticle platforms now extend beyond messenger RNA vaccines into oncology and rare disease pipelines, where fast-track designations shorten clinical timetables from the traditional decade to roughly half that span.[1]Food and Drug Administration, “Nanotechnology Research at NCTR,” fda.gov Investor appetite has followed, driving venture capital into start-ups that refine encapsulation chemistries and surface coatings tailored for organ-specific uptake. Polymer nanocarriers complement lipids by offering programmable release kinetics and improved protein stabilization in circulation, which is attractive for complex biologics. The combined platform versatility positions these carriers as templates for next-generation precision medicines that can bypass systemic toxicity and dosing hurdles.

Surge in FDA/EMA Approvals of Nano-Enabled Therapeutics & Diagnostics

Regulators in the United States and Europe have codified risk-based assessment paths for nanoscale materials, culminating in coordinated review frameworks that remove duplicate studies and lower development costs.[2]European Medicines Agency, “Draft Guideline on the Development and Manufacture of Oligonucleotide-Based Medicinal Products,” ema.europa.eu The clarity fuels cross-Atlantic trial designs and encourages multinational sponsors to align chemistry, manufacturing, and control packages early. Faster time-to-market improves net present value calculations and stimulates pipeline expansion across therapeutics, imaging agents and point-of-care diagnostics, thereby lifting the overall nano-biotechnology market.

Rapid Cost Decline of Lab-on-Chip Nanofabrication Tools

Bottom-up, additive processes now print nanoscale features with 99% lower input costs than legacy lithography, slashing capital barriers for academic incubators and small enterprises. Continuous microfluidic manufacturing converts batch steps into real-time flows that reduce wastage and enable in-line analytics for stringent quality control. Digital twins paired with machine-learning algorithms fine-tune process variables to enhance yield and material uniformity, collectively compressing scale-up timelines for nano-formulated therapeutics and diagnostics.

Government Nanomedicine Megaprojects (EU Cancer Mission)

The European Union earmarks annual Horizon Europe budgets in excess of EUR 95.5 billion (USD 111.65 billion) aimed at oncology solutions that integrate nanoscale drug delivery, diagnostics, and regenerative interventions. Complementary National Institutes of Health programs in the United States carve out multi-year appropriations for translational nanomedicine. Such sustained public expenditure subsidizes high-risk research that private capital often shuns and creates shared infrastructure from animal facilities to GMP suites, which collectively accelerate proof-of-concept milestones and commercialization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Toxicity/Biopersistence Uncertainties Of Metallic Nanoparticles | -1.80% | Global, with stricter oversight in EU & North America | Long term (≥ 4 years) |

| Capital-Intensive GMP Nanofabrication Facilities | -1.40% | Global, with higher barriers in emerging markets | Medium term (2-4 years) |

| IP Land-Rush Driving Patent Thickets That Slow Collaboration | -1.10% | Global, with concentration in US, EU, China patent jurisdictions | Medium term (2-4 years) |

| Fragmented Global Nano-Waste Regulation Raising Disposal Costs | -0.90% | Global, with regulatory gaps in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Chronic Toxicity/Biopersistence Uncertainties of Metallic Nanoparticles

Pre-clinical studies link prolonged exposure to certain metallic nanoparticles with cardiovascular or neurological stress, prompting European regulators to assign high-risk classifications to medical devices incorporating nanoscale metals. Developers now deploy multi-omics assays and advanced imaging to map particle fate and degradation in vivo. While surface functionalization strategies reduce cytotoxicity, lengthy bridging studies inflate timelines and budgets, which may deter smaller firms from entering metallic particle programs despite their utility for imaging and hyperthermia therapies.[3]Mauro Grigioni, “Nanostructured Medical Devices: Regulatory Perspective and Current Applications,” materials.mdpi.com

Capital-Intensive GMP Nanofabrication Facilities

Building or upgrading nano-specific cleanrooms demands specialized airflow systems, robotics and real-time analytics, pushing investment tickets from EUR 20 million (USD 23.38 million) for narrow-scope suites to USD 400 million for fully integrated biopharmaceutical campuses. Modular pods and single-use flow paths offer cost relief yet still require high-spec metrology and contamination-control measures to satisfy regulatory scrutiny, especially for sterile parenteral products. The heavy capital load nudges start-ups toward virtual models that rely on contract development and manufacturing organizations, creating potential supply bottlenecks during peak demand periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Drug Delivery Dominates Therapeutic Innovation

Drug delivery accounted for 42.5% of nano-biotechnology market share in 2024, reflecting the clinical validation of lipid nanoparticles and sustained-release polymeric systems. The segment benefits from clear guidance on nanomaterial characterization and stability testing, which streamlines dossier preparation and accelerates approvals. Regenerative medicine registers the fastest 16.8% CAGR through 2030 as nanofiber scaffolds and nano-engineered hydrogels enhance stem-cell adhesion, proliferation, and differentiation. Diagnostics leverage quantum dots and super-paramagnetic nanoparticles for higher resolution imaging, while nanosensors enable pathogen detection at the point of care. Environmental remediation employs iron oxide and carbon nanomaterials to capture heavy metals and degrade organic contaminants with higher efficiency than legacy adsorbents.

Synergies between DNA nanotechnology and drug delivery create programmable payload carriers that respond to microenvironmental cues such as pH or enzymatic markers, thus elevating on-target therapeutic indices. Regulatory convergence across major markets further reduces duplication in toxicity testing and aligns quality-by-design expectations. Agriculture applications gain traction as nanoscale fertilizers and pesticides boost nutrient uptake efficiency, which supports sustainable intensification of crop production.

By Nanomaterial Type: DNA Origami Structures Lead Innovation

Lipid-derived carriers retained 28.1% share of the nano-biotechnology market size in 2024 due to their accepted safety profile and scalable manufacturing for mRNA vaccines and small-interfering RNA therapies. DNA/RNA origami structures exhibit an 18.9% CAGR through 2030, driven by their addressable surfaces that facilitate multivalent ligand display and logic-based release functions. Polymeric nanoparticles, especially poly(lactic-co-glycolic acid), remain workhorses in controlled-release injectables, while metallic nanoparticles, despite regulatory scrutiny, offer unmatched photothermal and contrast-enhancement properties in oncology settings. Carbon nanomaterials such as graphene and carbon nanotubes serve emerging biosensing and filtration use-cases, although throughput and cost constraints limit near-term scale-up.

Commercial momentum around DNA origami is illustrated by companies launching kits that program nanoscale drug carriers through computer-aided design interfaces. These programmable constructs can assemble in hours inside microreactors, improving reproducibility and opening avenues for point-of-care biomanufacturing. Meanwhile, surface-passivated metallic nanoparticles continue to progress in targeted radiotherapy and theranostics, provided developers generate robust long-term clearance data.

By End-user Industry: Pharmaceutical Dominance with Healthcare Expansion

Pharmaceutical and biotechnology companies controlled 57.5% revenue in 2024 because they integrate nano-formulated active pharmaceutical ingredients into high-margin pipelines. Their strong regulatory and commercialization infrastructure allows rapid uptake of platform improvements such as continuous nanomaterial synthesis and AI-enabled formulation screening. Hospitals and diagnostic centers record the highest 13.4% CAGR to 2030 as decentralized point-of-care devices and nano-enabled imaging expand precision-medicine workflows. Academic institutes act as feeders for intellectual property and workforce training, while agriculture, food processing, environmental, and energy companies adopt nanotechnology to improve productivity and sustainability metrics.

Hospital systems' investment in onsite nanodiagnostic labs shortens turnaround time for infectious-disease panels and therapeutic drug monitoring, translating into improved patient outcomes and cost savings. Growing collaborations between academic centers and industry accelerate tech transfer by embedding GMP suites within research parks, thereby reducing scale-up friction for early-stage discoveries.

Geography Analysis

North America commands 39.2% share owing to a clear regulatory roadmap and strong venture activity. The United States Advanced Manufacturing Technologies Designation Program accelerates novel production lines, which lowers scale-up risk for emerging companies. Canadian provincial funds co-finance pilot GMP nanofabrication suites that serve regional start-ups, while Mexico introduces tax credits to recruit contract manufacturing orders. Partnerships such as Johnson & Johnson’s licensing of Nanobiotix oncology assets illustrate how incumbents outsource specialized nanotechnology to reduce development risk.

Asia Pacific displays the highest growth potential at 13.6% CAGR through 2030. China’s state-backed research parks and patent subsidies help domestic enterprises file aggressively across drug delivery, diagnostics and nanomanufacturing, ensuring local supply chains for advanced therapies. India’s BioE3 framework aligns fiscal incentives, venture debt and skill-development programs to build a USD 300 billion bio-economy, with nano-enabled precision farming and biomaterials as priority verticals. Japan, South Korea and Australia channel grants into biomanufacturing consortia focused on cell and gene therapies that depend on high-purity nanocarrier inputs.

Europe benefits from Horizon Europe funding streams exceeding EUR 95.5 billion each year that underwrite collaborative projects on nano-enabled oncology, infectious diseases and green manufacturing. The European Medicines Agency draft guideline on oligonucleotide therapeutics clarifies quality expectations for nanoparticle carriers, which reduces regulatory uncertainty and encourages venture flows. Germany, France and the United Kingdom spearhead process-development expertise, while Nordic countries sponsor demonstration plants for nano-remediation of contaminated industrial sites. Middle East & Africa and South America showcase smaller but fast-growing demand for nano-formulated vaccines and point-of-care diagnostics as public health agencies upgrade immunization campaigns and surveillance networks.

Competitive Landscape

The nano-biotechnology industry remains moderately fragmented but shows consolidation signs as large pharmaceutical players prefer strategic licensing or equity stakes instead of building nano expertise in-house. Johnson & Johnson’s multibillion-dollar tie-up with Nanobiotix for the NBTXR3 radioenhancer underscores this partnership model, granting the giant access to validated nano-platforms while the specialist gains global commercial channels. Chinese enterprises dominate patent output, which intensifies IP negotiations and can impede cross-border co-development unless broad freedom-to-operate opinions are secured early.

Competitive advantage pivots on rapid formulation iteration through AI-assisted molecular modeling, continuous nanomaterial synthesis, and early alignment with regulators on characterization methods. DNA origami start-ups differentiate with programmable devices that perform logic-based release or sensing, opening white-space indications in immuno-oncology and rare genetic disorders. Capital access remains a barrier because GMP nano-fabrics demand high upfront outlays, but contract manufacturers are expanding capacity to capture growing outsourcing volumes. Companies that master cost-efficient large-scale production while maintaining physicochemical precision stand to win share as the nano-biotechnology market grows.

Nano-biotechnology Industry Leaders

Johnson & Johnson

Pfizer Inc.

Novartis AG

Thermo Fisher Scientific

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: University of Chicago researchers created biomimetic nanocarriers that slip past immune defenses and deliver drugs at target sites with 10-times the efficiency of standard systems, tackling a long-standing barrier in nanomedicine delivery.

- May 2025: Nanobiotix shared positive pancreatic-cancer data for its radioenhancer JNJ-1900 (NBTXR3) and, in the same period, dosed the first lung-cancer patient in the CONVERGE study, reinforcing nanoparticle-based radiotherapy as a viable option in hard-to-treat tumors.

- May 2025: FUJIFILM Diosynth Biotechnologies committed GBP 400 million (USD 500 million) to enlarge its United Kingdom site, adding viral gene therapy, mammalian cell culture and mRNA production suites—and creating 350 new jobs—to meet rising demand for nano-enabled medicines.

Global Nano-biotechnology Market Report Scope

| Drug Delivery |

| Diagnostics & Imaging |

| Regenerative Medicine & Tissue Engineering |

| Agriculture & Food Safety |

| Environmental Remediation |

| Lipid-based Nanocarriers |

| Polymeric Nanoparticles |

| Metallic Nanoparticles |

| Carbon-based Nanomaterials (CNT, Graphene, Q-dots) |

| DNA/RNA Origami Structures |

| Pharmaceuticals & Biotechnology Firms |

| Hospitals & Diagnostic Centers |

| Academic & Research Institutes |

| Agriculture & Food Processing Companies |

| Environmental & Energy Enterprises |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Application | Drug Delivery | |

| Diagnostics & Imaging | ||

| Regenerative Medicine & Tissue Engineering | ||

| Agriculture & Food Safety | ||

| Environmental Remediation | ||

| By Nanomaterial Type | Lipid-based Nanocarriers | |

| Polymeric Nanoparticles | ||

| Metallic Nanoparticles | ||

| Carbon-based Nanomaterials (CNT, Graphene, Q-dots) | ||

| DNA/RNA Origami Structures | ||

| By End-user Industry | Pharmaceuticals & Biotechnology Firms | |

| Hospitals & Diagnostic Centers | ||

| Academic & Research Institutes | ||

| Agriculture & Food Processing Companies | ||

| Environmental & Energy Enterprises | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the forecast growth rate for the nano-biotechnology market to 2030?

The nano-biotechnology market is projected to expand at an 11.5% CAGR from 2025 to 2030.

Which application currently generates the highest revenue?

Drug delivery leads, accounting for 42.5% nano-biotechnology market share in 2024.

Which region is expected to grow fastest over the forecast period?

Asia Pacific is anticipated to record a 13.6% CAGR through 2030 on the back of strong patent activity and supportive government programs.

Which nanomaterial type shows the most rapid adoption?

DNA/RNA origami structures post the highest 18.9% CAGR driven by their programmability and precision.

Why are metallic nanoparticles facing regulatory scrutiny?

Concerns over long-term biopersistence and potential cardiovascular or neurological toxicity prompt stricter classification and require extensive safety data packages.

How are pharmaceutical companies accessing nano expertise?

Most form strategic partnerships or licensing deals with specialized providers, as illustrated by Johnson & Johnsons agreement with Nanobiotix.

Page last updated on: