Biopreservation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

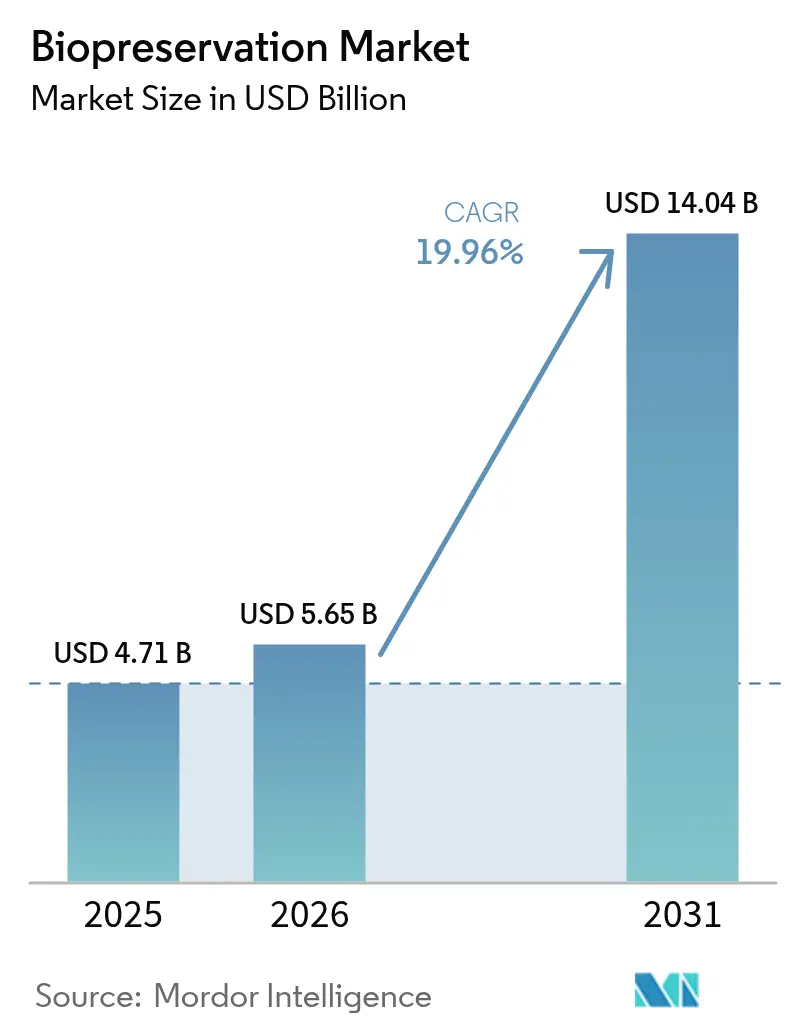

| Market Size (2026) | USD 5.65 Billion |

| Market Size (2031) | USD 14.04 Billion |

| Growth Rate (2026 - 2031) | 19.96% CAGR |

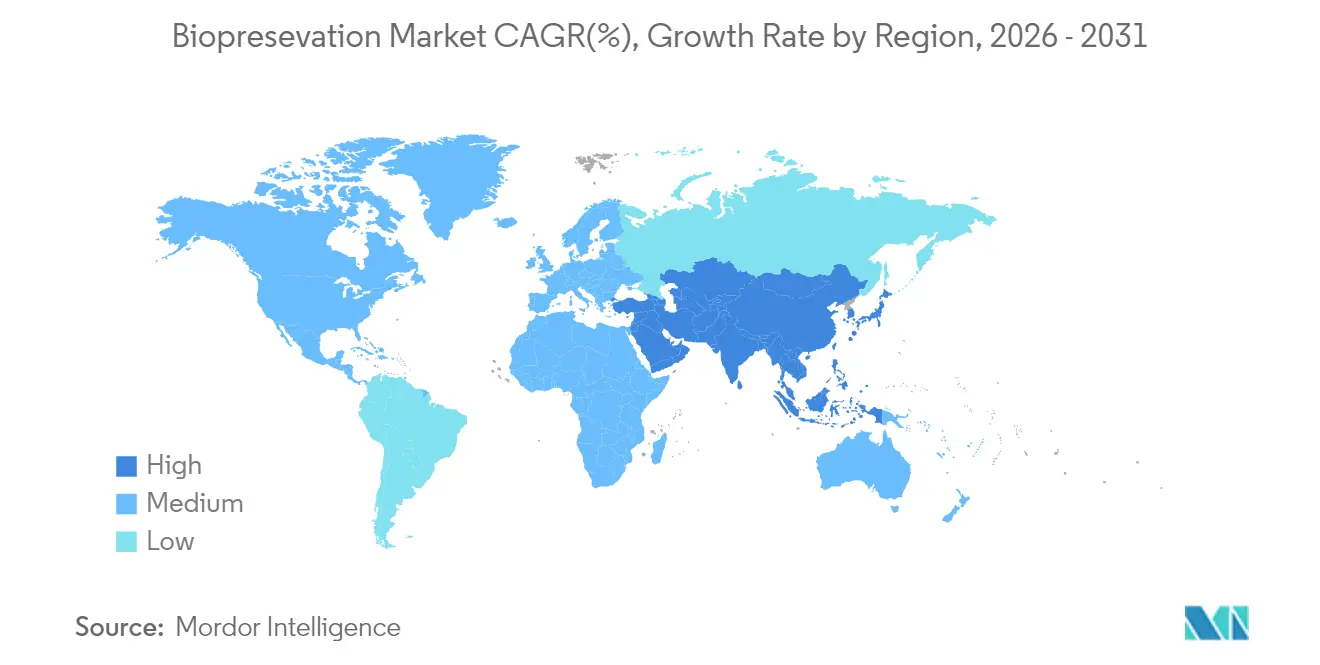

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biopreservation Market Analysis by Mordor Intelligence

Biopreservation market size in 2026 is estimated at USD 5.65 billion, growing from 2025 value of USD 4.71 billion with 2031 projections showing USD 14.04 billion, growing at 19.96% CAGR over 2026-2031. The surge is underpinned by the acceleration of personalized medicine, stronger regulatory support for advanced biologics, and deployment of vaccine-era ultra-low temperature logistics. Rapid digitization of biobank inventories plus artificial-intelligence analytics is increasing specimen utility and encouraging long-term sample maintenance. In parallel, investments in cryogenic robotics and predictive monitoring improve reliability and reduce manual error, further broadening the biopreservation market footprint. Supply-side innovation, ranging from non-cryogenic polymer matrices to ice-recrystallization-inhibitor media, adds technological depth and opens new revenue streams across research and clinical settings.

Key Report Takeaways

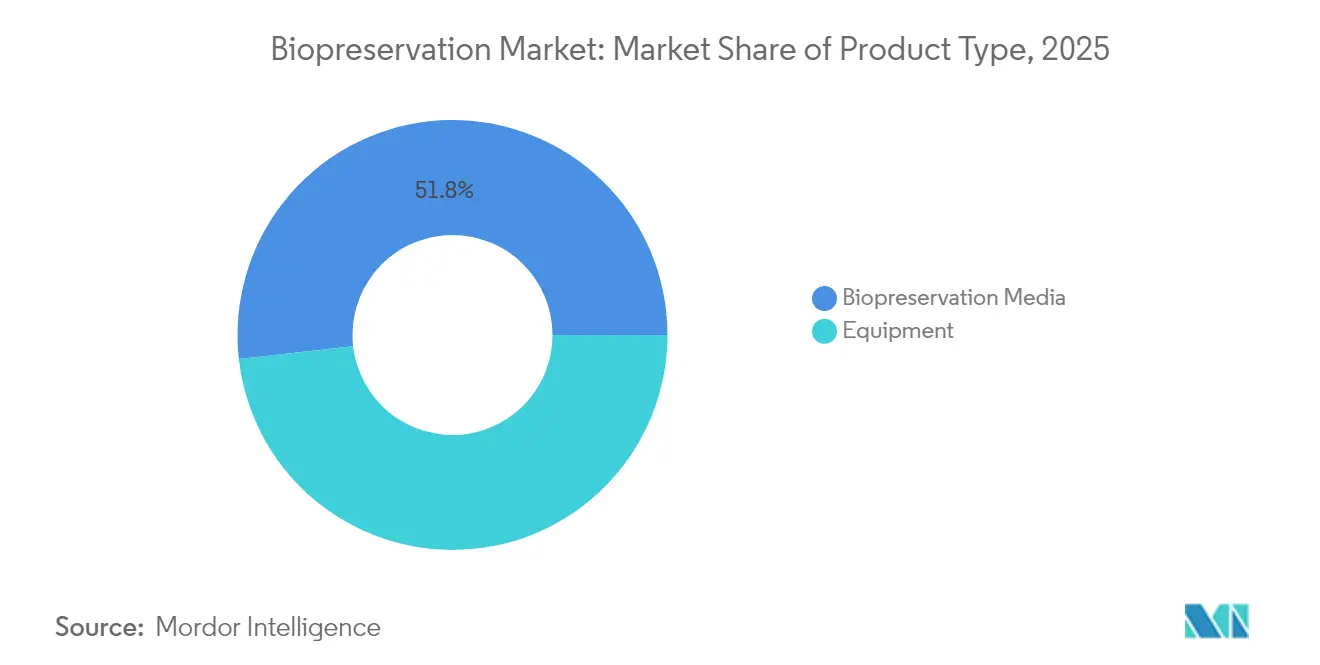

- By product type, biopreservation media held 51.78% of the biopreservation market share in 2025, while equipment is forecast to grow at a 22.05% CAGR to 2031.

- By biospecimen, human tissues led with 29.06% revenue share in 2025; stem cells are projected to advance at a 22.9% CAGR through 2031.

- By preservation method, cryopreservation accounted for 70.64% of the biopreservation market size in 2025, whereas vitrification is set to expand at a 22.58% CAGR to 2031.

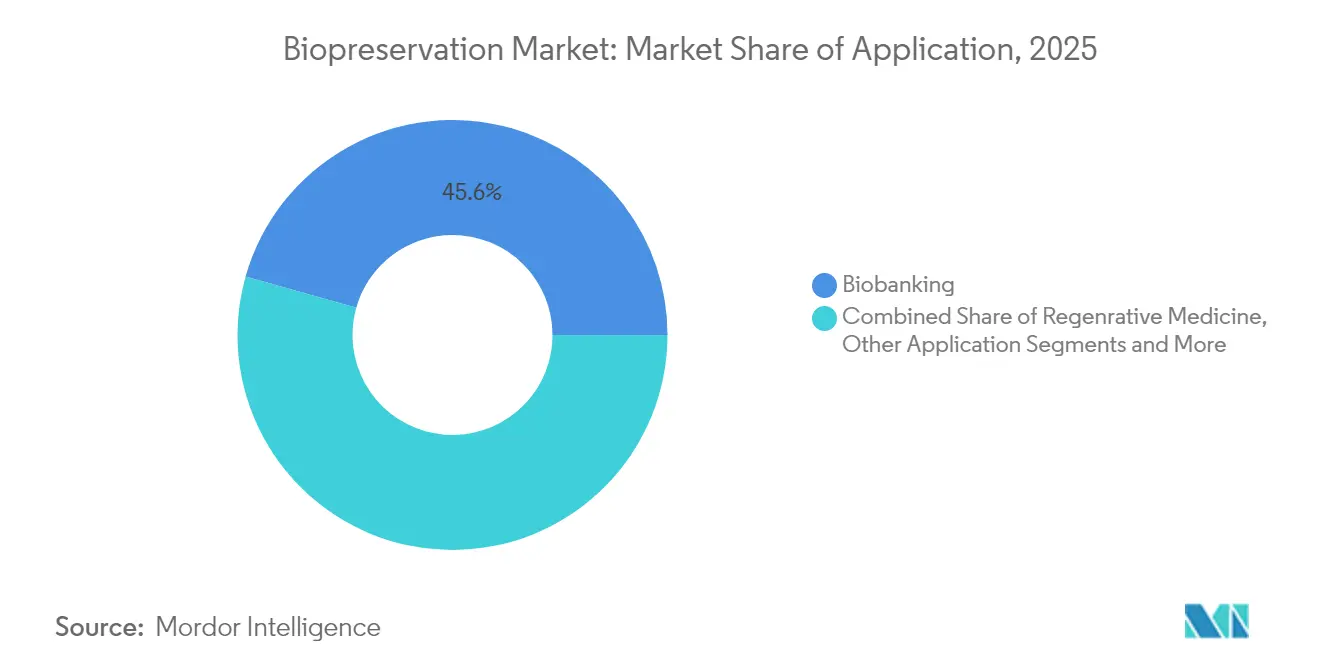

- By application area, biobanking commanded 45.62% of the biopreservation market size in 2025 and regenerative medicine is growing at a 20.71% CAGR between 2026-2031.

- By end user, biobanks and gene banks held 37.1% of the biopreservation market share in 2025, while pharmaceutical companies record the highest projected CAGR at 21.54% through 2031.

- By geography, North America dominated with 38.12% share of the biopreservation market in 2025; Asia-Pacific is the fastest-growing region at a 22.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Biopreservation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Healthcare & Life-Science R&D Budgets | +4.2% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Expansion Of Biobanking For Personalised Medicine | +3.8% | Global, with early gains in APAC core markets | Long term (≥ 4 years) |

| Rapid Adoption Of Hospital-Based, In-House Sample Storage | +3.1% | North America & EU, spill-over to APAC | Short term (≤ 2 years) |

| Decentralised Trials Driving Point-Of-Care Preservation | +2.9% | Global, with emphasis on emerging markets | Medium term (2-4 years) |

| Repurposed Ultra-Low-Temp Logistics From mRNA Supply Chain | +2.7% | Global, with established cold chain infrastructure | Short term (≤ 2 years) |

| Venture Funding Into Cryogenic Robotics & Monitoring | +2.5% | North America & EU, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Healthcare & life-science R&D budgets

Record-high corporate and public R&D allocations now exceed USD 200 billion annually in the United States, prompting pharmaceutical firms to outsource sample handling to specialist providers that guarantee consistent quality.[1]Center for Biologics Evaluation and Research, “2024 Biological Device Application Approvals,” Food and Drug Administration, fda.gov Companies such as Discovery Life Sciences integrate flow cytometry with molecular analytics, illustrating how outsourced services accelerate specimen throughput, reduce cycle times, and stimulate fresh demand for consumables and equipment. Robust funding also supports artificial-intelligence models that mine multi-omic datasets, increasing the quantity and diversity of materials entering the biopreservation market. Capital availability cushions high upfront equipment costs, allowing research networks to adopt automated, energy-efficient freezers and cloud-based monitoring.

Biobanking for personalized medicine

Large-scale initiatives like the UK Biobank, now surpassing 500,000 participants, underscore the shift from passive storage to dynamic data integration platforms. Brazil’s institutional repositories follow suit, validating a global appetite for diverse, longitudinal specimens that underpin precision diagnostics. Growing sample diversity demands unified quality control protocols, which translate into higher sales of advanced media and vitrification devices. As genomic, proteomic, and electronic health-record data converge, the biopreservation market benefits from repeat specimen retrievals that extend storage horizons and encourage premium service contracts.

Hospital-based in-house sample storage

Clinics and academic centers increasingly deploy their own ultra-low temperature infrastructure to gain real-time access to specimens for clinical decision support. Studies at the University of Edinburgh reveal that adjusting freezers from −80 °C to −70 °C cuts energy use by 28%, making onsite storage financially appealing.[2]Martin Farley et al., “Efficient ULT Freezer Storage,” University of Edinburgh, ed.ac.uk Automated systems like the BioArc Ultra can complete up to 9 million robotic picks per year, ensuring rapid retrieval while minimizing deviation risks. The resulting operational autonomy accelerates translational research and enlarges the addressable biopreservation market within hospital networks.

Decentralized trials and point-of-care needs

Remote trial designs oblige sponsors to safeguard sample integrity at dispersed collection sites. Specialized couriers such as DHL-owned CRYOPDP now manage over 600,000 ultra-cold shipments yearly across 15 nations. Portable freezers and phase-change shippers maintain consistent temperatures and feed tracking data to cloud dashboards. These capabilities enable timely biomarker analyses, reduce resampling costs, and reinforce confidence in the biopreservation market as a facilitator of flexible clinical operations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Operating Costs Of Cryogenic Equipment | -2.8% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Risk Of Cell/Tissue Viability Loss During Preservation | -2.1% | Global, with emphasis on complex tissue types | Medium term (2-4 years) |

| Medical-Grade Liquid-Nitrogen Supply-Chain Fragility | -1.9% | Global, with concentration in remote regions | Short term (≤ 2 years) |

| ESG Pressure On Energy-Intensive Long-Term Storage | -1.7% | EU & North America, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cryogenic equipment capital & operating costs

High-performance freezers range from USD 15,000-50,000, compounded by electricity expenses of USD 3,000-5,000 per unit each year. Smaller institutes struggle with acquisition and maintenance, delaying adoption in cost-sensitive regions. Though temperature optimization and shared facilities mitigate expenses, the upfront barrier suppresses immediate penetration of the biopreservation market in emerging economies.

Risk of viability loss during preservation

Ice formation and osmotic stress continue to threaten post-thaw cell recovery. Research on mesenchymal stem cell spheroids shows variable outcomes even with FDA-approved media, signaling residual uncertainty among end users.[3]Cho J., “Comparison of Cryopreservation Media for Mesenchymal Stem Cell Spheroids,” Biopreservation and Biobanking, liebertpub.com While vitrification and novel cryoprotectants improve outcomes, the persistent perception of quality risk tempers uptake for high-value clinical applications, limiting the attainable scope of the biopreservation market in the near term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rapid automation ignites equipment demand

Equipment sales are accelerating at a 22.05% CAGR, reflecting the push toward robotics, predictive maintenance, and cryogen-free technology. The biopreservation market size for equipment is on track to climb from USD 2.27 billion in 2025 to USD 7.5 billion by 2031. Ultra-low temperature freezers now feature internet-of-things sensors that transmit operational data for proactive servicing. Automated storage modules can sort, pick, and re-rack millions of vials annually, cutting labor costs and enhancing biospecimen traceability. Parallel advances in vapor-phase nitrogen systems curb frost accumulation and reduce liquid nitrogen consumption, addressing both safety and ESG requirements.

Consumables and accessories exhibit steady growth alongside rising sample volumes. Integrated media-hardware solutions illustrate a convergence trend, where proprietary cryoprotectants are optimized for precise cooling profiles delivered by automated platforms. This symbiosis locks in customers and strengthens recurring-revenue streams, anchoring long-term resilience for suppliers within the biopreservation market.

By Biospecimen: Stem cells power therapeutic expansion

Human tissue banks still account for the largest revenue slice, yet stem cells are the star performer with a 22.9% CAGR. Approval of cord-blood-based Omisirge validates the clinical payoff of high-quality stem-cell preservation. Sophisticated protocols now govern everything from sourcing to thaw, ensuring viability for regenerative surgeries and immunotherapies.

Organs remain experimentally challenging, but the successful thaw-and-transplant of a rat kidney demonstrates tangible progress toward clinical organ repositories. DNA, plasma, and other bio-fluids benefit from room-temperature polymer matrices that slash cold chain costs and broaden global research collaboration. This biospecimen diversification magnifies end-market opportunities and underscores the long-run momentum of the biopreservation market.

By Preservation Method: Vitrification emerges as premium option

Cryopreservation continues to dominate, yet the elegance of ice-free vitrification is converting new users in reproductive medicine, tissue engineering, and cell therapy manufacturing. Consistent glass-like solidification eliminates ice damage, improves post-thaw viability, and supports stringent GMP workflows. The biopreservation market size for vitrification technologies is projected to expand 2.76-fold between 2026 and 2031, driven by falling equipment costs and availability of turnkey media kits.

Hypothermic storage, while modest in share, addresses critical short-haul logistics and same-day surgical needs. Lyophilization delivers shelf-stable formats for proteins and viruses, lowering transport expenses in vaccine programs. The methodological toolkit now mirrors the varied shelf-life, biosafety, and cost profiles demanded across today’s life-science landscape.

By Application Area: Regenerative medicine accelerates revenue mix

Biobanking retains the largest contribution to the biopreservation market, supplying academics and life-science companies with well-annotated cohorts for biomarker discovery. Meanwhile, regenerative medicine’s 20.71% CAGR outpaces every other application thanks to dozens of autologous and allogeneic cell therapies in late-stage trials. Each clinical milestone raises the demand for GMP-certified storage, shipment, and thawing protocols.

Drug discovery, preclinical toxicology, and forensic sciences constitute complementary growth pockets. Integrated sample-to-data pipelines shorten development timelines and spur repeat purchases of media and single-use accessories. As digital twins and AI-driven design mature, preserved specimens will continue serving as ground-truth anchors, safeguarding the long-term relevance of the biopreservation market.

By End User: Pharma-biotech segment catalyzes commercial scale

Biopharma firms increasingly outsource logistics while insourcing analytical control, creating compound demand for full-service cold chain providers and on-site automation. Strategic alliances, such as the SK pharmteco-Cryoport collaboration, tie manufacturing with long-distance cryogenic transport, ensuring product integrity. The projected biopreservation market size for pharmaceutical users climbs from USD 1.32 billion in 2025 to USD 4.25 billion by 2031.

Biobanks and gene banks remain volume anchors, housing population-level collections for omics studies. Hospitals adopt modular freezers to support precision oncology programs, while research institutes pioneer next-generation protocols that later filter into commercial toolkits. The varied user profile expands the cumulative installed base, reinforcing the structural growth outlook for the biopreservation market.

Geography Analysis

North America continues to command the largest regional stake, holding 38.12% of the biopreservation market in 2025. Federal guidance on cell and gene therapy safety plus steady venture funding make the United States the supply-chain nexus for cryogenic equipment and specialized logistics. Canadian consortia and Mexican manufacturing corridors complement the ecosystem, adding cross-border efficiencies and broadening market access.

Asia-Pacific is the clear growth engine at a 22.88% CAGR. Chinese biopharma revenues are set to exceed CNY 1.4 trillion by 2029, fueling infrastructure orders for freezers, nitrogen generators, and monitoring software. Japan’s stimulus packages and tax incentives aim to triple the domestic biotech market, accelerating adoption of advanced vitrification kits and automated biobank modules. India’s contract manufacturers leverage Production-Linked Incentives to build GMP cold-chain warehouses that conform to global audit standards, opening new export pathways for preserved cell therapies.

Europe holds a mature yet evolving position. The United Kingdom’s 16 million-sample expansion validates sustained government backing for national biobanks. Germany and France integrate energy-efficiency mandates, encouraging deployment of −70 °C operations and liquid-nitrogen recapture systems. Environmental, social, and governance requirements push suppliers to deliver greener cooling technologies, ensuring that sustainability and performance advance together within the regional biopreservation market.

Competitive Landscape

The market remains moderately fragmented, though scale leaders are edging toward consolidation. Thermo Fisher Scientific’s plan to invest up to USD 50 billion in acquisitions illustrates the race to assemble end-to-end offerings and lock down share across equipment, consumables, and services. BioLife Solutions focuses on specialty media and acquired ice-recrystallization inhibitor technology to cement leadership in cell-therapy-grade formulations.

Logistics giants are entering the fray. DHL Group’s acquisition of CRYOPDP extends reach into temperature-controlled courier operations that handle hundreds of thousands of biologic shipments each year. Integrated transport plus storage packages resonate with pharma sponsors seeking single-vendor accountability. Meanwhile, smaller innovators such as Atelerix scale hydrogel platforms that remove cold-chain dependence for short-term shipment, differentiating through niche applications and licensing deals with regional distributors.

Automation, AI, and hybrid preservation techniques are focal points of competition. Companies deploy predictive maintenance algorithms that cut unplanned downtime and protect high-value inventories. Collaborative R&D programs with academic centers accelerate proof-of-concept trials for organ vitrification and synthetic cryoprotectants. As intellectual property portfolios widen, licensing and joint-venture models grow more common, eventually reshaping ownership patterns in the biopreservation market.

Biopreservation Industry Leaders

BioLife Solutions

Merck KGaA

Thermo Fisher Scientific Inc.

Azenta US Inc.

Cryoport Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Teknova and Pluristyx unveiled PluriFreeze™, an integrated cryopreservation system that boosts cell-therapy viability and shortens development timelines

- March 2025: DHL Group completed the acquisition of CRYOPDP, adding 15-country coverage and 600,000 annual ultra-cold shipments to its life-science logistics network

- January 2025: Azenta secured a contract with UK Biocentre to install BioArc Ultra automation, expanding capacity by 16 million samples for the Our Future Health study.

- December 2024: The FDA granted approval to Symvess, the first acellular tissue-engineered vessel for extremity trauma, marking a regulatory milestone for preserved biological implants.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the biopreservation market as the worldwide revenue generated from purpose-built freezers, immune cold-storage units, tailored preservation media, consumables, and supporting laboratory information systems that keep cells, tissues, organs, and bio-fluids viable for research, therapeutic, and commercial use.

Scope exclusion: We exclude routine pharmaceutical cold-chain distribution equipment and food-grade preservative additives.

Segmentation Overview

- By Product Type

- Biopreservation Media

- Equipment

- Temperature-Maintaining Units

- Consumables

- Accessories & Monitoring Systems

- By Biospecimen

- Cells & Cell Lines

- Human Tissues

- Organs

- Stem Cells

- Other Bio-fluids (DNA/RNA, Plasma, etc.)

- By Preservation Method

- Cryopreservation

- Vitrification

- Hypothermic Storage

- Lyophilisation

- By Application Area

- Biobanking

- Regenerative Medicine

- Drug Discovery & Pre-clinical Testing

- Other Applications

- By End User

- Biobanks & Gene Banks

- Hospitals & Transplant Centres

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed biobank directors in North America and Europe, transplant surgeons in Asia, and quality managers at media suppliers. These conversations validated storage capacity assumptions, average fill volumes, and regional certification costs, filling gaps left by secondary data.

Desk Research

We began by mapping the installed base of biobanks, transplant centers, and regenerative medicine facilities through open sources such as ClinicalTrials.gov, NIH RePORTER, Eurostat medical device files, and the International Society for Biological and Environmental Repositories. UN Comtrade shipment codes for cryogenic equipment, patent families from Questel, and company 10-K disclosures on preservation media sales shaped initial demand and price curves, while paid feeds from D&B Hoovers and Dow Jones Factiva clarified private firm revenue splits. The sources listed here are illustrative, and many additional datasets were consulted to ground volumes, pricing, and utilization trends.

In a second sweep, we reviewed peer-reviewed journals on post-thaw survival rates and regulatory guidance from the FDA and EMA, which refined replacement cycles for ultra-low freezers and liquid nitrogen tanks.

Market-Sizing & Forecasting

A top-down build starts with global biospecimen inventories and annual sample inflows reported by registry bodies, multiplied by median preservation spend per sample. Supplier roll-ups of freezer shipments and sampled average selling prices give a bottom-up sense check before totals are finalized. Key variables include cord blood units stored, clinical trial starts for stem cell therapies, average freezer energy draw, liquid nitrogen price trends, and regional electricity tariffs. A multivariate regression of these drivers projects value through 2030, and scenario analysis captures faster uptake of regenerative medicine products where applicable.

Data Validation & Update Cycle

Outputs pass automated variance alerts, peer review, and senior analyst sign-off. We refresh the dataset each year, with interim updates triggered by material shifts in capital spending or trial volumes, ensuring buyers receive the latest calibrated view.

Why Mordor's Biopreservation Market Baseline Remains Dependable

Published estimates often diverge because firms choose different product mixes, vintage base years, and currency conversions. Mordor's disciplined scope alignment, annual refresh cadence, and dual-track validation create a balanced midpoint that decision makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 4.71 B (2025) | Mordor Intelligence | |

| USD 4.4 B (2024) | Global Consultancy A | Focuses mainly on media, light primary validation |

| USD 2.90 B (2023) | Industry Publication B | Older base year, omits consumables, extrapolates from equipment only |

| USD 4.11 B (2025) | Research Boutique C | Applies uniform CAGR without triangulating biobank growth |

These comparisons show that when scope breadth, update frequency, and driver realism are weighed together, Mordor's numbers stand out as the most transparent and reproducible baseline for strategic planning.

Key Questions Answered in the Report

What is the current biopreservation market size and how fast is it growing?

The biopreservation market size stands at USD 5.65 billion in 2026 and is forecast to reach USD 14.04 billion by 2031, expanding at a 19.96% CAGR.

Which region leads the biopreservation market?

North America holds the leading position with 38.12% share, supported by mature biobanking infrastructure and strong R&D funding.

What segment is growing the fastest within the biopreservation market?

Equipment is the fastest-growing product segment with a 22.05% CAGR, driven by automation and cryogen-free technologies.

Why is vitrification gaining attention?

Vitrification avoids ice-crystal damage, improving post-thaw viability for complex tissues and gametes, which is essential for regenerative and reproductive medicine.

What key restraint could limit market expansion?

High capital and operating costs for ultra-low temperature equipment remain a significant barrier, especially for smaller institutions in emerging markets.

Page last updated on: