AI-Based Healthcare Chatbots Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 37.01 Million |

| Market Size (2031) | USD 118.13 Million |

| Growth Rate (2026 - 2031) | 26.13% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

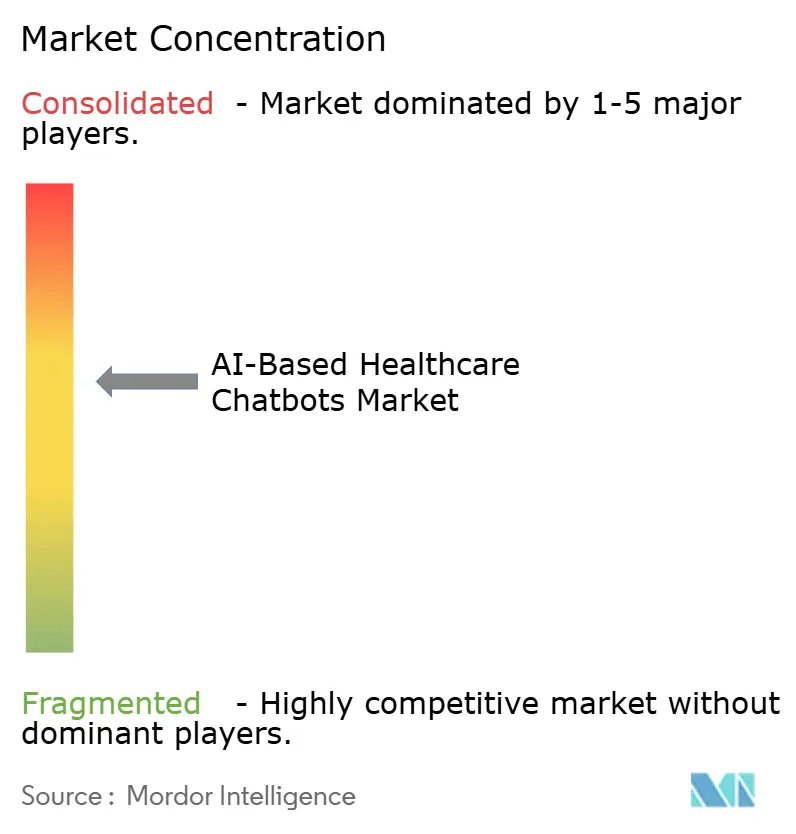

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based Healthcare Chatbots Market Analysis by Mordor Intelligence

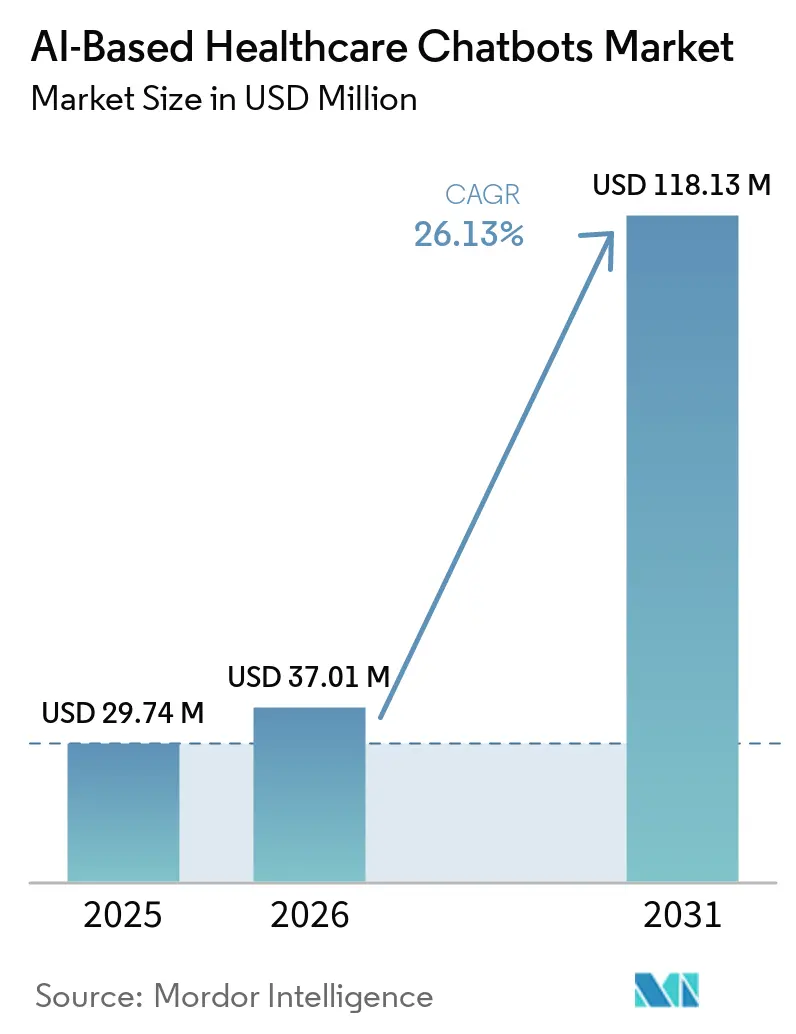

The AI-based healthcare chatbots market is expected to grow from USD 29.74 million in 2025 to USD 37.01 million in 2026 and is forecasted to reach USD 118.13 million by 2031 at 26.13% CAGR over 2026-2031. The main force behind this expansion is the worsening burnout burden on clinicians, which has made administrative offload a core operating need for health systems rather than an optional digital upgrade. Telehealth is also now a normalized care channel, with 71.4% of U.S. physicians using it in 2024, compared with 25.1% before the pandemic, which keeps demand high for automated intake, navigation, and follow-up tools. AI adoption is rising at the same time, with 70% of healthcare organizations actively using AI in 2026, up from 63% in 2025, which gives the AI-based healthcare chatbots market a much larger deployment base than it had even a year earlier. The current growth wave is no longer centered on simple scheduling tools, because buyers are now adopting agents that can support contextual dialogue, symptom triage, adherence reminders, and behavioral health screening inside real care workflows. Deployment is also moving from pilot activity toward core infrastructure, with 37% of digital healthcare respondents in NVIDIA’s 2026 survey naming virtual health assistants and chatbots as their top AI ROI use case, while the EU AI Act and FDA’s TEMPO pilot are pushing vendors toward more structured compliance models in 2026.

Key Report Takeaways

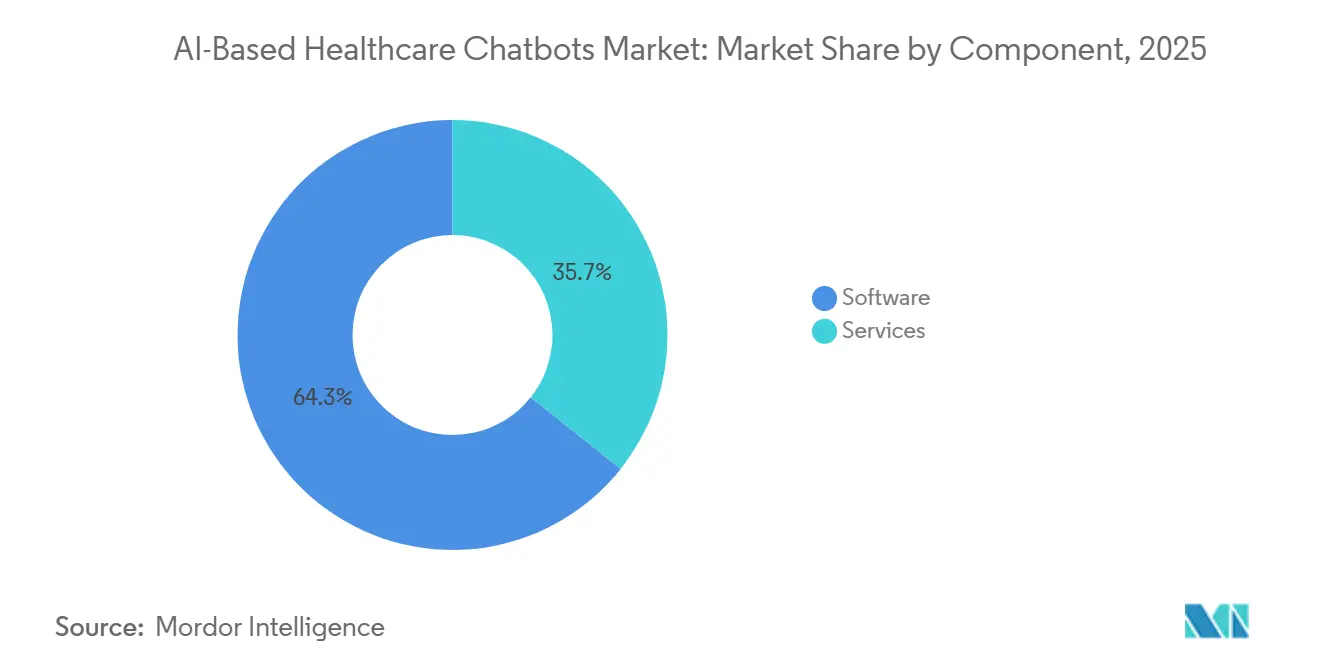

- By component, software held 64.27% of revenue in 2025 and software is also the fastest-growing component, with the AI-based healthcare chatbots market size for this segment projected to expand at 26.92% CAGR through 2031.

- By deployment mode, cloud accounted for 68.22% of revenue in 2025, while hybrid is forecasted to grow fastest at 27.17% CAGR through 2031.

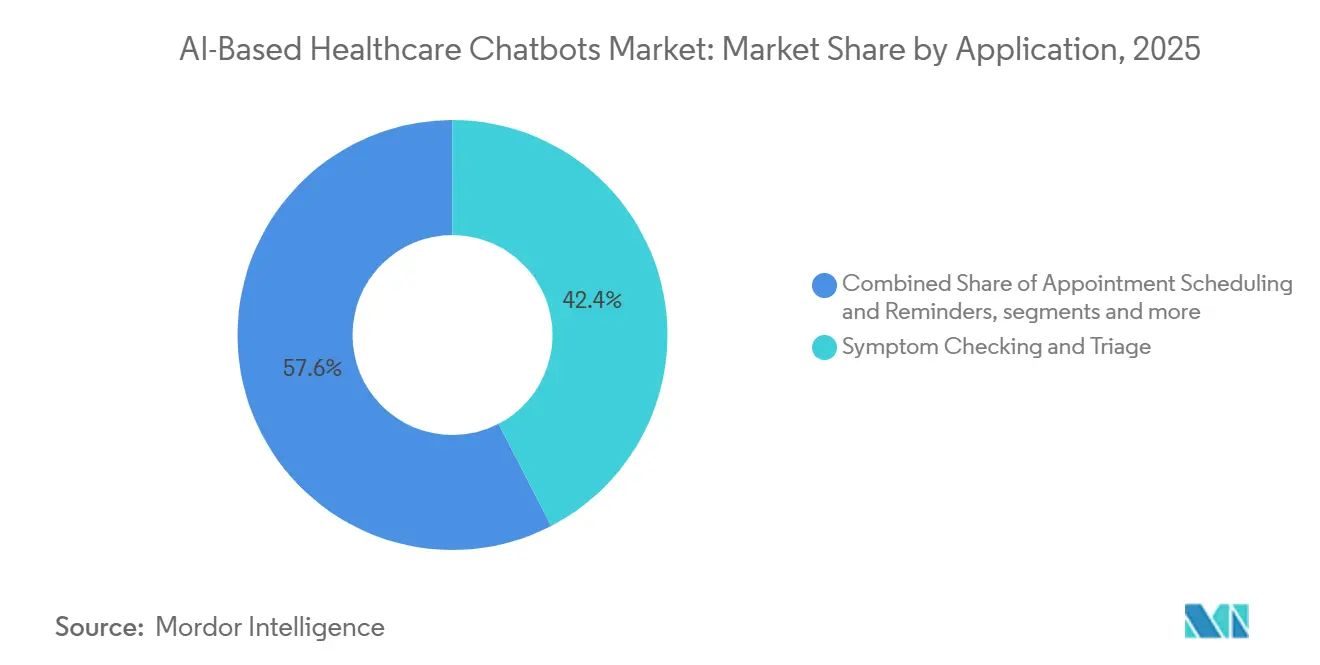

- By application, symptom checking and triage represented 42.36% of revenue in 2025, while mental health and behavioral support is projected to expand at 27.82% CAGR through 2031.

- By end-user, healthcare providers accounted for 47.46% of revenue in 2025, while patients and caregivers are forecasted to record the highest growth at 27.47% CAGR through 2031.

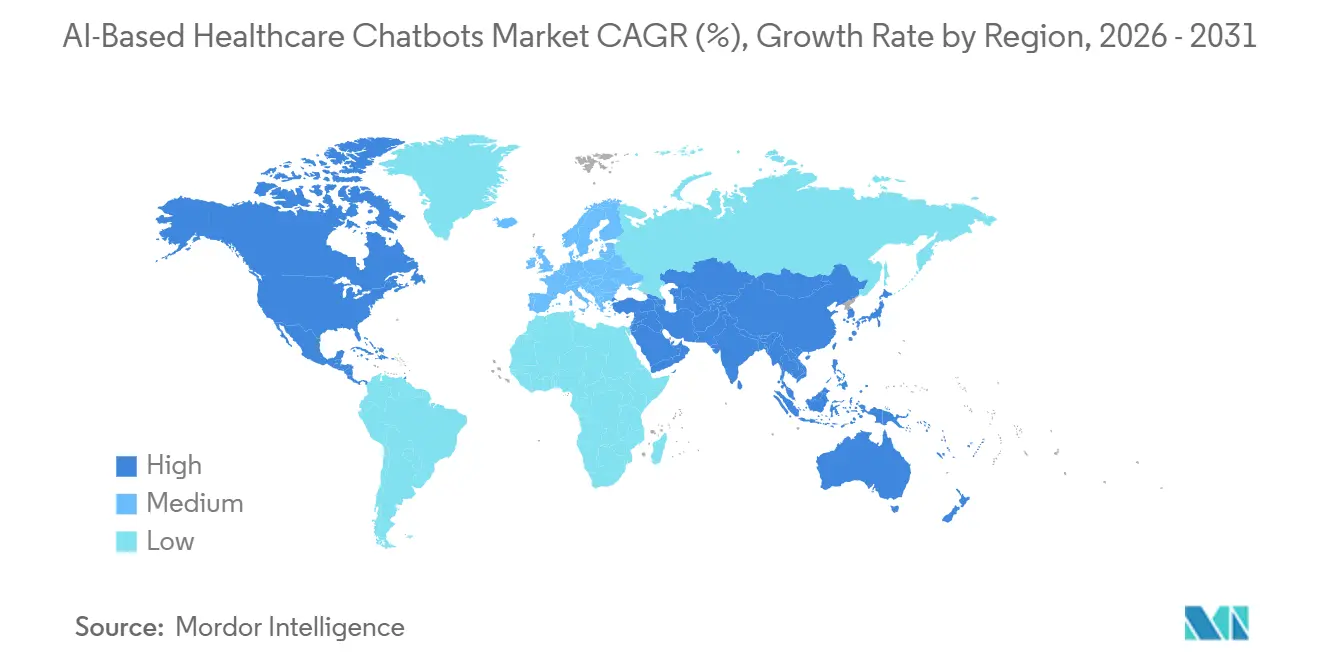

- By geography, North America held 41.22% of revenue in 2025, while Asia-Pacific is projected to grow fastest at 28.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based Healthcare Chatbots Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for 24/7 Patient Engagement and Navigation | +5.5% | Global, strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Faster Triage, Appointment, and Care Routing Workflows | +4.8% | Global, with largest deployments in North America | Short term (≤ 2 years) |

| Expansion of Telehealth, Virtual Care, and Remote Monitoring | +4.5% | North America and Asia-Pacific, spill-over to MEA | Medium term (2-4 years) |

| Increasing Need for Clinician Workflow Offload and Call Deflection | +4.2% | North America and Europe | Short term (≤ 2 years) |

| Multilingual Patient Access Across Fragmented Care Networks | +2.5% | Asia-Pacific core, spill-over to MEA and South America | Medium term (2-4 years) |

| Use of Chatbots for Medication Adherence and Follow-up Nudges | +2.3% | North America and Europe, early adoption in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for 24/7 Patient Engagement and Navigation

Patient volumes are putting steady pressure on after-hours phone lines and front-desk teams, which is making always-on digital engagement a core access requirement in many care settings. Druid AI’s 2025-2026 benchmark showed that patient identity and verification, appointment management, and patient FAQs together represented 57% of chatbot workflow volume across its healthcare customer base, which confirms that front-door access remains the main demand anchor for the AI-based healthcare chatbots market.[1]Druid AI, “2026 AI Adoption in Healthcare Benchmark Report,” Druid AI, druidai.com This pattern matters because it shows that demand is being led by routine navigation tasks that appear in very high volumes across hospitals, clinics, and digital health programs. Wolters Kluwer’s 2026 survey also found that 70% of both clinicians and patients believe AI can improve health literacy and engagement, which increases organizational willingness to fund patient-facing tools.[2]Wolters Kluwer, “Future Ready Healthcare, 2026 Survey on AI Adoption and Patient-Clinician Insights,” Wolters Kluwer, wolterskluwer.comThat combination of provider-side pressure and patient-side acceptance gives the AI-based healthcare chatbots market a broader base than earlier digital engagement cycles. It also means buyers are now treating 24/7 conversational access as part of care navigation, not as a simple service add-on.

Faster Triage, Appointment, and Care Routing Workflows

The AI-based healthcare chatbots market is gaining support from triage tools that reduce the time between a patient’s first report of symptoms and the point of clinical routing. Ada Health reported in April 2026 that its clinical AI study with CUF Hospitais increased the share of patients receiving clinically appropriate care from 29.8% to 64.4% before the visit began. The same study found that 40% of patients who had planned to visit the emergency department shifted to a lower-acuity care setting that an independent physician panel judged appropriate. Infermedica’s 2026 launch of Conversational Triage, which combines large language models with Bayesian models, shows how this category is moving beyond static symptom trees toward more structured clinical navigation. That shift is important for the AI-based healthcare chatbots market because medically ambiguous cases are common in real patient conversations and cannot be managed well by rigid scripts alone. The remaining bottleneck is operational integration, because triage outputs create the most value when they are available inside the EHR before the clinician visit starts.

Expansion of Telehealth, Virtual Care, and Remote Monitoring

Telehealth has stabilized at a much higher level than before the pandemic, which gives the AI-based healthcare chatbots market a durable source of demand for intake, navigation, and follow-up automation. The American Medical Association reported that 71.4% of U.S. physicians used telehealth in 2024, compared with 25.1% before the pandemic, which shows how deeply virtual care is now embedded in delivery models.[3]American Medical Association, “New Data Details How Telehealth Use Varies by Physician Specialty,” AMA, ama-assn.org CMS also continued to support telehealth expansion in 2026, which reduced reimbursement uncertainty around virtual care programs and made enterprise deployment decisions easier for providers. The larger change is that virtual care is moving away from single video visits and toward chronic disease management, post-discharge follow-up, and telebehavioral health, all of which require more frequent automated touchpoints. Chatbots fit these models well because they can keep a patient engaged between formal visits and can support medication adherence and reminder workflows at scale. This change from episodic care to continuous interaction keeps the AI-based healthcare chatbots market tied to long-term virtual care expansion rather than short-term telehealth spikes.

Increasing Need for Clinician Workflow Offload and Call Deflection

Administrative work remains one of the clearest adoption drivers for the AI-based healthcare chatbots market because buyers increasingly judge these tools on measurable load reduction. A 2025 multicenter study in JAMA Network Open found that ambient AI scribe use reduced clinician burnout from 51.9% to 38.8% and cut after-hours documentation by 10.8 minutes per workday across 263 ambulatory clinicians. A parallel 2025 study in the Journal of General Internal Medicine found that ambient clinical documentation reduced documentation delay by 66% after 50 days of use. The same logic extends to patient messaging, intake forms, refill requests, and lab-result questions, because every interaction handled without clinician intervention reduces in-basket pressure and preserves encounter capacity. As a result, the AI-based healthcare chatbots market is increasingly tied to labor productivity and burnout mitigation rather than to experimental AI positioning.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinical Risk from Hallucinated or Incorrect Guidance | -3.5% | Global | Short term (≤ 2 years) |

| Integration Complexity With EHR, CRM, and Payer Systems | -3.2% | North America and Europe | Medium term (2-4 years) |

| Patient Trust Gaps for Sensitive Health Interactions | -2.8% | Global | Medium term (2-4 years) |

| Data Privacy, Consent, and Model Governance Burden | -2.4% | Europe (GDPR/EU AI Act), North America (HIPAA), Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Clinical Risk from Hallucinated or Incorrect Guidance

Clinical misinformation remains the largest adoption brake on the AI-based healthcare chatbots market because patient-facing tools are judged against safety expectations that are much stricter than those in general consumer AI. Researchers at the Icahn School of Medicine at Mount Sinai also found that chatbots often expanded false medical information, although a simple safeguard prompt sharply reduced hallucination incidence. The same study showed that structured prompting, function calling, and retrieval-augmented generation reduced major hallucinations by as much as 75% in controlled tests. That leaves the AI-based healthcare chatbots market with a clear path to mitigation, but it also means vendors must invest in safety architectures before large enterprises will approve full live deployment.

Integration Complexity with EHR, CRM, and Payer Systems

Integration remains a major restraint on the AI-based healthcare chatbots market because the hard part of deployment is usually not the conversation layer but the connection to live enterprise systems. A 2025 JMIR Medical Informatics implementation report showed that real-world deployment required parallel work across clinical development, LLM development, and system integration, while supporting more than 2,200 distinct document forms. Even when organizations claim to support HL7 FHIR, a 2025 Journal of Clinical Medicine article noted that uneven implementation still creates friction and middleware burden. This becomes harder in multi-EHR environments, where the same chatbot must work across different Epic, Cerner, or Meditech data models after merger activity. Even so, bidirectional write access into structured EHR fields is still limited in many health systems, which keeps deployment timelines long and the AI-based healthcare chatbots market less scalable for smaller buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Anchors Platform Spending as Services Scale Up

Software held 64.27% of the AI-based healthcare chatbots market share in 2025 and is also projected to grow at 26.92% CAGR through 2031. This combination of scale and growth shows that most health systems are still buying platform licenses before they reach full deployment across their provider networks. The software layer attracts spending because subscription platforms can be rolled out faster than service-led projects and usually carry stronger recurring revenue economics. It also gives buyers a clearer path to standardization across symptom triage, intake, patient messaging, and follow-up workflows. In the current phase of the AI-based healthcare chatbots market, that makes software the main spending anchor even before utilization reaches its full potential.

The services market should expand in importance as health systems move from vendor selection into actual EHR integration, workflow redesign, and model governance work. Those needs are especially visible where deployments must fit local privacy rules, clinical review processes, and procurement requirements. Infermedica’s work toward EU MDR certification for Conversational Triage in 2026 illustrates how compliance support is becoming a value-added extension of the software proposition rather than a separate purchase. The long-term risk for pure software vendors is that hyperscalers may continue bundling chatbot functions into broader health cloud offerings, which can pressure pricing as the AI-based healthcare chatbots market matures.

By Deployment Mode: Hybrid Models Gain Ground on Cloud Dominance

Cloud deployment held 68.22% of revenue in 2025, which reflects its lower upfront burden and its ease of adoption for mid-sized providers and digital health companies. Cloud remains the default model where speed of implementation matters more than local infrastructure control. It also works well for organizations that want to test patient engagement and routing tools before making larger architectural decisions. Even so, cloud leadership does not mean governance concerns have disappeared inside the AI-based healthcare chatbots market. Large health systems still need strong control over protected health information, audit trails, and data residency.

Hybrid deployment is forecasted to grow at 27.17% CAGR through 2031, which places it ahead of the broader AI-based healthcare chatbots market. This reflects the practical preference of large providers for cloud-based model performance combined with tighter local control over sensitive data and integration layers. On-premises deployment still holds a niche role in settings where localization rules or internal security policy are strict, including parts of India and China. Hybrid adoption is therefore likely to keep rising as enterprises formalize vendor risk reviews and as the AI-based healthcare chatbots market places more value on flexible deployment models.

By Application: Triage Leads While Mental Health Rewrites the Growth Curve

Symptom checking and triage accounted for 42.36% of the AI-based healthcare chatbots market size in 2025, while mental health and behavioral support is projected to expand at 27.82% CAGR through 2031. Triage remains the largest application because it has stronger clinical validation, a more familiar workflow fit, and a clearer compliance path than therapeutic or emotionally sensitive use cases. Appointment scheduling and reminders forms the second-largest application area because it combines low clinical risk with visible administrative savings. Administrative and billing support also remains relevant as providers connect chatbots to revenue cycle and service workflows. Together, these categories show that the AI-based healthcare chatbots market still leans toward use cases where operational value is easier to prove.

Mental health and behavioral support is growing faster because the shortage of licensed professionals is widening and because digital support tools can extend access between human sessions. FDA’s Digital Health Advisory Committee met in November 2025 to review generative AI-enabled digital mental health medical devices, which signaled that this application is moving into a more formal regulatory discussion. The committee highlighted crisis identification, transparency, and continuing model performance oversight as baseline expectations for tools used in mental health settings. That mix creates a dual effect, because it raises the bar for vendors while also giving the segment more legitimacy in buyer evaluations. The AI-based healthcare chatbots market therefore sees mental health as a powerful growth segment, but one where success depends on stronger guardrails than in lower-risk administrative use cases.

By End-User: Providers Anchor Revenue, Consumers are Accelerating Fastest

Healthcare providers accounted for 47.46% of revenue in 2025, while patients and caregivers are projected to grow fastest at 27.47% CAGR through 2031. Providers still anchor spending because they control procurement budgets, own the workflow pain points, and can justify chatbot deployment through labor savings and throughput gains. The provider base gives the AI-based healthcare chatbots industry a stable revenue core even as adoption patterns diversify. It also explains why integration depth still matters more than pure conversational quality in many enterprise deals.

Patients and caregivers are growing faster because major consumer platforms are widening access to health guidance tools outside the hospital buying cycle. Google also launched Health Coach globally on May 19, 2026 through its Health Premium subscription, which added another large consumer entry point. Payers and insurance companies remain an important user group for prior authorization pre-screening, formulary support, and member engagement, while life sciences and CROs are emerging users for recruitment, adverse event reporting, and trial navigation. This means the AI-based healthcare chatbots industry is no longer defined only by institutional buyers, because consumer touchpoints are now changing awareness and usage patterns at a much faster pace.

Geography Analysis

North America held 41.22% of the AI-based healthcare chatbots market share in 2025, which reflects the region’s mature EHR base, strong telehealth use, and advanced AI procurement activity. The region also benefits from a dense concentration of large health systems that can sign enterprise-wide digital agreements and fund long implementation cycles. Competitive pressure is also highest in North America because Amazon and Microsoft are already using existing enterprise relationships to push healthcare-specific AI capabilities into live environments. Even with strong platform coverage at the top end, smaller physician groups and federally qualified health centers still represent a durable opening for lower-cost, EHR-linked tools.

Asia-Pacific is forecasted to grow at 28.22% CAGR through 2031, which makes it the fastest-growing regional segment in the AI-based healthcare chatbots market. Growth is supported by large underserved populations, rising smartphone access, and the use of public digital health programs to extend service reach. India’s Strategy for Artificial Intelligence in Healthcare, published in February 2026, linked AI governance to the Ayushman Bharat Digital Mission and named AIIMS Delhi, PGIMER Chandigarh, and AIIMS Rishikesh as AI Centres of Excellence. India’s eSanjeevani platform also shows how AI-linked public health infrastructure can operate at population scale when policy support and digital channels move together. South Korea, Japan, and Australia offer higher spending per deployment, while India and China remain the main volume centers for future demand.

Europe accounts for the second-largest regional share in the AI-based healthcare chatbots market, supported by digital health policy momentum and strong provider interest in regulated AI tools. The biggest shift is regulatory, because the EU AI Act’s full high-risk obligations for healthcare AI came into effect on August 2, 2026, which raised the burden for conformity assessment, transparency, and post-market monitoring. That higher bar creates short-term complexity, but it also strengthens the position of vendors that invest early in certifiable compliance architecture. The Middle East and Africa remains an earlier-stage region led by GCC healthcare digitalization programs, while South America is led by Brazil and remains more constrained by health system financing and longer procurement cycles.

Competitive Landscape

The AI-based healthcare chatbots market shows moderate-to-low concentration, which fits an early commercial category where no single player dominates across all care settings, use cases, and regions. Amazon Web Services launched Amazon Connect Health in March 2026 with 5 purpose-built agentic healthcare tools for patient scheduling, pre-visit intake, ambient clinical documentation, medical coding, and patient insights. Microsoft expanded Dragon Copilot in 2026 with role-based experiences for physicians, nurses, and radiologists, while also adding 58-language documentation capability and Microsoft 365 Copilot integration. These moves show 2 clear competitive patterns in the AI-based healthcare chatbots market, platform breadth from hyperscalers and clinical validation depth from specialists.

The first group is using installed cloud relationships to win healthcare AI contracts faster and to lower the friction of enterprise deployment. The second group is competing through evidence, workflow specificity, and safety positioning that pure platform vendors may not match as easily. Consumer distribution is now also shaping competition, because Amazon and Google can place health guidance tools directly in front of large user bases without waiting for provider procurement cycles. That shift expands awareness of the AI-based healthcare chatbots market, but it also compresses margins for mid-tier vendors that lack either deep evidence or large-scale distribution. Vendors whose products remain siloed from clinical workflows are now at greater risk of displacement, because buyers increasingly want tools that can read and write across care systems rather than operate as stand-alone chat windows.

White space still exists in multilingual access, clinical trial navigation, and post-acute follow-up, where automation needs are clear but product depth is uneven across the field. Medication adherence and structured follow-up are especially important because they connect patient engagement to measurable care continuity and outcomes. The vendors most likely to gain share are those that combine low hallucination risk, credible regulatory readiness, and workflow integration in one deployable stack. That is why the AI-based healthcare chatbots market is rewarding vendors that can satisfy both operational and clinical gatekeepers at the same time.

AI-Based Healthcare Chatbots Industry Leaders

Microsoft Corporation

Ada Health GmbH

Buoy Health, Inc.

Infermedica

HealthTap, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Ada Health announced that the European Patent Office granted patent EP4679451B1 for its hybrid clinical AI architecture, combining LLMs with a proprietary probabilistic graphical model to deliver hallucination-resistant clinical assessments. The patent went into effect March 25, 2026, and is expected to anchor Ada's licensing and IP strategy across health system and payer partnerships.

- April 2026: Ada Health published a landmark peer-reviewed study with CUF Hospitais, Portugal's largest private healthcare network, demonstrating that its clinical AI more than doubled clinically appropriate care utilization from 29.8% to 64.4% and redirected 40% of planned emergency department visits to lower-acuity settings, with no safety issues identified during follow-up.

- March 2026: Amazon Web Services launched Amazon Connect Health, offering 5 purpose-built agentic AI healthcare agents, patient scheduling, pre-visit intake, ambient clinical documentation, medical coding, and patient insights, as HIPAA-eligible services deployable within existing EHR and telehealth environments. AWS also launched a data transformation agent for automated CCDA-to-FHIR conversion within AWS HealthLake.

- March 2026: Microsoft introduced new capabilities for Dragon Copilot at HIMSS 2026, including role-based experiences for physicians, nurses, and radiologists, partner-built AI apps and agents via Microsoft Marketplace for revenue cycle and clinical decision support, and integration with Microsoft 365 Copilot to surface work-related context alongside patient data. More than 100 health systems are live on the platform in 2026.

Global AI-Based Healthcare Chatbots Market Report Scope

According to the report’s scope, the AI‑based healthcare chatbots market refers to the segment of digital health solutions that use AI‑driven conversational agents to deliver automated, real‑time support across clinical, administrative, and patient‑engagement workflows. These chatbots use NLP, machine learning, and predictive reasoning to triage symptoms, schedule appointments, provide medication reminders, answer health queries, and streamline provider–patient communication, improving accessibility, efficiency, and care continuity.

The AI‑based healthcare chatbots market is segmented into component, deployment mode, application, end-user, and geography. By component, the market is segmented into software and services. By deployment mode, the market is segmented into cloud-based, on-premises, and hybrid. By application, the market is segmented into symptom checking and triage, appointment scheduling and reminders, medication and drug information assistance, patient education and care navigation, mental health and behavioral support, and administrative and billing support. By end-user, the market is segmented into healthcare providers, patients and caregivers, payers and insurance companies, and life sciences and CROs. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Cloud-Based |

| On-Premises |

| Hybrid |

| Symptom Checking and Triage |

| Appointment Scheduling and Reminders |

| Medication and Drug Information Assistance |

| Patient Education and Care Navigation |

| Mental Health and Behavioral Support |

| Administrative and Billing Support |

| Healthcare Providers |

| Patients and Caregivers |

| Payers and Insurance Companies |

| Life Sciences and CROs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| By Deployment Mode | Cloud-Based | |

| On-Premises | ||

| Hybrid | ||

| By Application | Symptom Checking and Triage | |

| Appointment Scheduling and Reminders | ||

| Medication and Drug Information Assistance | ||

| Patient Education and Care Navigation | ||

| Mental Health and Behavioral Support | ||

| Administrative and Billing Support | ||

| By End-User | Healthcare Providers | |

| Patients and Caregivers | ||

| Payers and Insurance Companies | ||

| Life Sciences and CROs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of AI-based healthcare chatbots by 2031?

The AI-based healthcare chatbots market is forecasted to reach USD 118.31 million by 2031, rising from USD 29.74 million in 2025 to USD 37.01 million in 2026 at a 26.13% CAGR over 2026-2031.

Which application area leads revenue and which one is growing fastest?

Symptom checking and triage led with 42.36% of revenue in 2025, while mental health and behavioral support is projected to grow fastest at 27.82% CAGR through 2031.

Which deployment model is gaining the most traction?

Cloud held the largest share at 68.22% in 2025, but hybrid is anticipated to grow faster at 27.17% CAGR because large health systems want cloud scalability with tighter data control.

Which region offers the strongest growth outlook for AI-based healthcare chatbots?

Asia-Pacific has the strongest growth outlook, with a projected 28.22% CAGR through 2031, supported by public digital health programs and large underserved populations.

Page last updated on: