AI In Wearable Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 15.28 Billion |

| Market Size (2031) | USD 39.18 Billion |

| Growth Rate (2026 - 2031) | 20.72% CAGR |

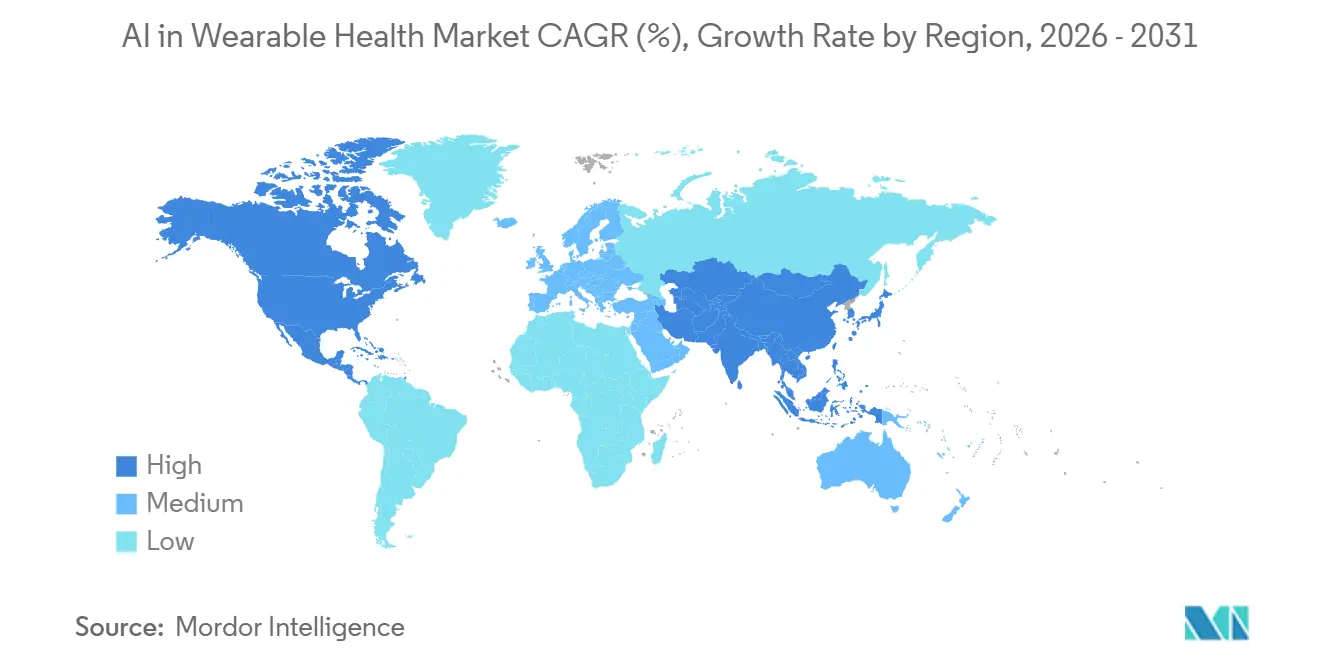

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

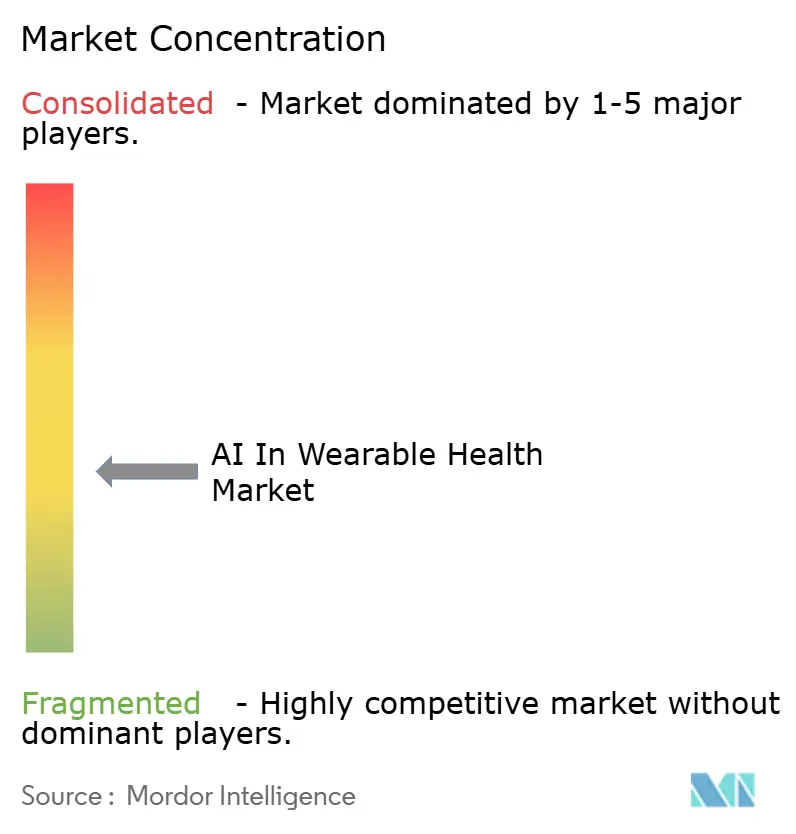

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Wearable Health Market Analysis by Mordor Intelligence

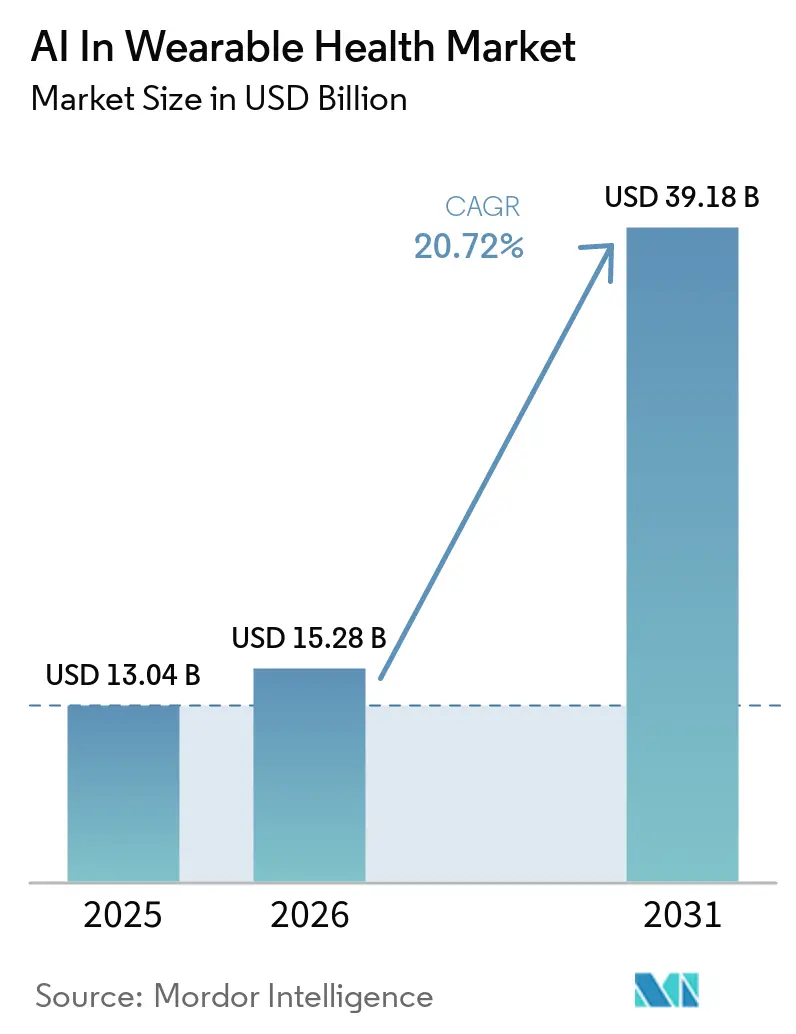

The AI in wearable health market size is expected to grow from USD 13.04 billion in 2025 to USD 15.28 billion in 2026 and is forecasted to reach USD 39.18 billion by 2031 at 20.72% CAGR over 2026-2031. The AI in wearable health market is expanding because value is moving away from device shipment volume and toward the software and inference layer that makes data clinically useful. On-device processing is changing wearables from passive trackers into tools that can support screening, monitoring, and care follow-up in daily settings. That shift is widening demand beyond consumer electronics buyers and is bringing in providers, insurers, and enterprise wellness programs that now have clearer use cases for continuous data collection. The AI in wearable health market also remains fragmented across device makers, software vendors, and clinical specialists, although recent product launches and regulatory progress point to gradual consolidation around platforms that combine sensors, algorithms, and integration. Battery limits, regulatory uncertainty, and sensor drift still weigh on adoption, but chipset miniaturization, privacy-preserving model design, and revised remote monitoring reimbursement keep the growth base intact.

Key Report Takeaways

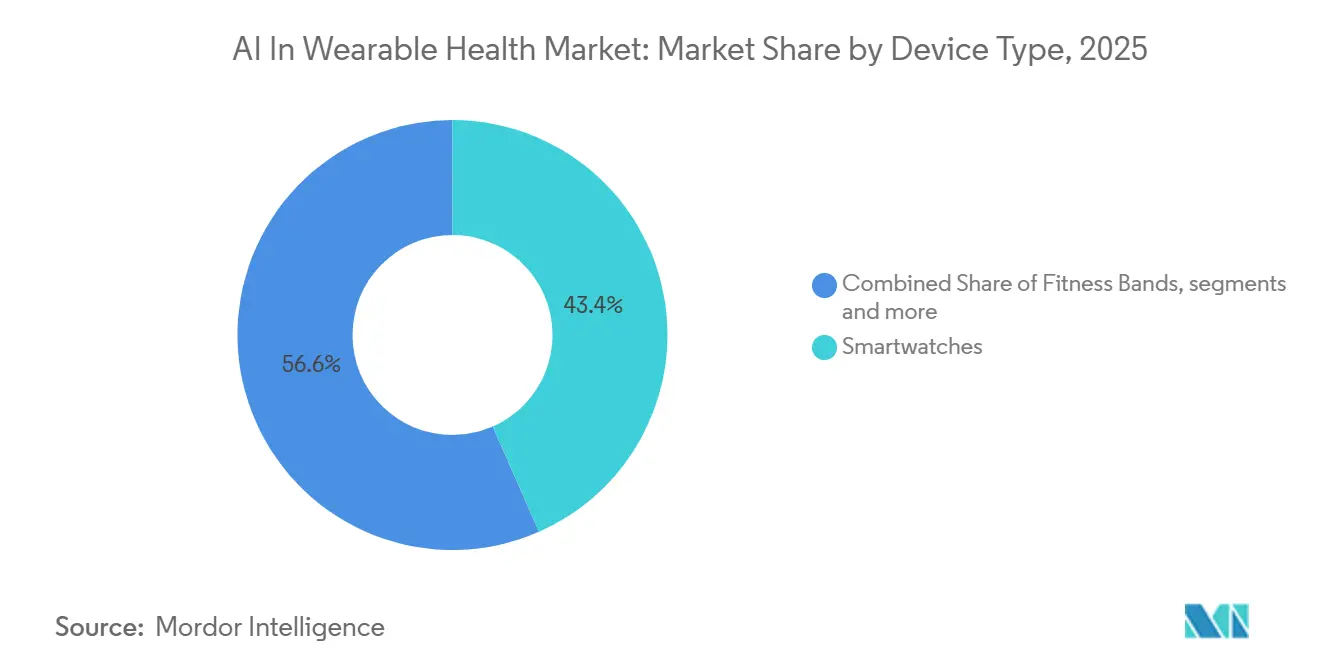

- By device type, smartwatches led with 43.44% revenue share in 2025, while medical-grade wearables are expected to expand at 21.69% CAGR through 2031.

- By component, software held 59.53% revenue share in 2025, while hardware is projected to grow at 21.78% CAGR through 2031.

- By application, sports and fitness monitoring accounted for 51.47% of revenue in 2025, while remote patient monitoring is anticipated to rise at 22.29% CAGR through 2031.

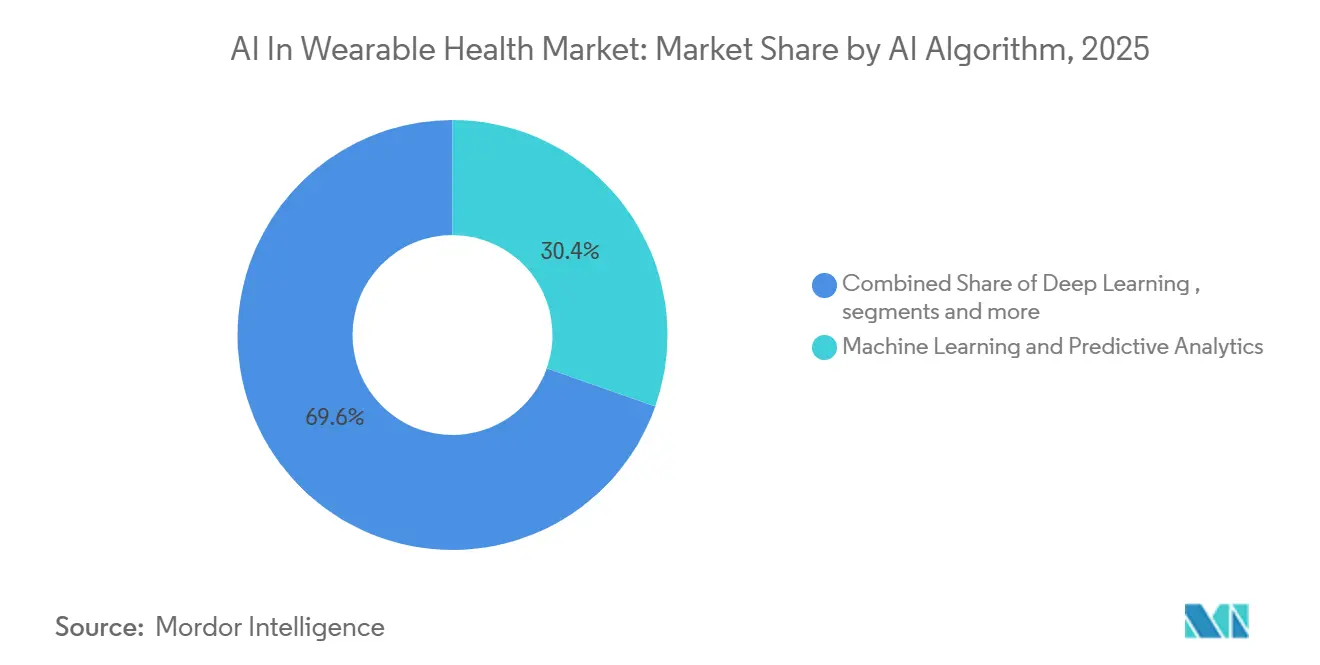

- By AI algorithm, machine learning and predictive analytics captured 30.36% of revenue in 2025, while edge AI and embedded intelligence are expected to grow at 22.15% CAGR through 2031.

- By end-user, individual users represented 46.71% of revenue in 2025, while healthcare providers are expected to advance at 22.26% CAGR through 2031.

- By geography, North America held 54.19% of revenue in 2025, while Asia-Pacific is projected to record the fastest growth at 23.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Wearable Health Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Continuous Miniaturization of Low-Power AI Chipsets | +3.8% | Global, with APAC manufacturing core and North America and Europe consumption spillover | Medium term (2-4 years) |

| Integration of Wearable Data into EHR and EMR Ecosystems | +2.6% | North America and Europe, early adoption in APAC tier-1 urban markets | Medium term (2-4 years) |

| Shift to Value-Based Care and Remote Patient Monitoring Reimbursement | +4.1% | North America core, spillover to EU and select APAC markets | Short term (≤ 2 years) |

| Consumer Demand for Preventive Health and Wellness Insights | +3.2% | Global, strongest in North America, Europe, and APAC urban centers | Short term (≤ 2 years) |

| Federated Learning Rollouts to Solve Privacy-Regulated Data Scarcity | +1.8% | EU driven by GDPR, North America driven by HIPAA, expanding globally | Medium term (2-4 years) |

| On-Device Foundation Models Enabling Multimodal Vitals Interpretation | +3.0% | North America and APAC early adopters, EU expansion as regulation clarifies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Continuous Miniaturization of Low-Power AI Chipsets

The AI in wearable health market is gaining from smaller and more power-efficient silicon that improves performance without raising device size or charging burden. Ambiq and Bravechip introduced the BCL603S3H chiplet platform in January 2026, and the launch claimed smart ring bill-of-materials cuts of up to 85% and production yield improvement of 20% while supporting on-device analysis of SpO₂, heart rate variability, and sleep metrics with battery life of up to 7 days.[1]Ambiq Micro, Inc., “Ambiq and Bravechip Cut Smart Ring Costs by 85% with New Edge AI Chiplet,” Ambiq Micro, Inc., ambiq.com That scale of cost compression matters because it widens the addressable base from wellness buyers to patients who need frequent monitoring but remain price sensitive. Qualcomm also announced Snapdragon Wear Elite in 2026, showing that wearable chip design is moving toward stronger local inference capability and more direct hardware differentiation. The AI in wearable health market should keep benefiting as low-power NPUs become standard in watches, rings, and medical sensors, because the hardware base then supports richer models without depending on the cloud.

Shift to Value-Based Care and Remote Patient Monitoring Reimbursement

The AI in wearable health market is also being pulled forward by reimbursement reform that makes short-duration monitoring economically workable for providers. CMS finalized new RPM and parallel RTM supply coding under the CY 2026 Medicare Physician Fee Schedule, allowing billing for as few as 2 to 15 monitoring days in a 30-day period at the same reimbursement level as the earlier 16-day minimum threshold.[2]Centers for Medicare & Medicaid Services, “Medicare Physician Fee Schedule Final Rule CY 2026,” Federal Register, govinfo.gov That change increases eligibility for post-discharge care, acute episodes, and lower-adherence patients who often failed to qualify under the prior standard. It also improves the case for episodic wearable deployment, which had weak economics when reimbursement depended on longer data collection windows. The same CMS rule recognizes device supply cost using a methodology that captures software, storage, and cybersecurity inputs, which is important for the AI in wearable health market because much of the value sits in software rather than the physical sensor.

Consumer Demand for Preventive Health and Wellness Insights

The AI in wearable health market continues to draw demand from consumers who now expect advice and interpretation rather than raw metrics. Samsung’s Galaxy Watch8 launch in July 2025 added vascular load monitoring, AI-guided coaching, and an antioxidant index built from a 5-second skin measurement, which shows how consumer devices are expanding passive and repeatable health signals. Apple’s Series 11 launch in September 2025 added hypertension notifications as a background function, which further pushed the device role from fitness logging toward risk awareness and daily screening support. In Germany, 63% of respondents said AI influenced their purchase of preventive health products, and the share rose to nearly 90% among people under 29, which suggests younger buyers are normalizing AI-led health interpretation faster than older cohorts. Oura’s 2025 revenue reaching USD 1 billion shows that the AI in wearable health market can sustain premium consumer pricing when users believe the insight layer is credible and useful between physician visits.

On-Device Foundation Models Enabling Multimodal Vitals Interpretation

The AI in wearable health market is moving toward smaller foundation models that can interpret multiple biosignals from one local architecture. A January 2026 Nature Communications paper introduced PHIA, an agent framework that combined PPG, accelerometry, sleep staging, and self-reported outcomes into actionable health interpretation through iterative reasoning.[3]M. A. Merrill et al., “Transforming Wearable Data into Personal Health Insights Using Large Language Model Agents,” Nature Communications, nature.comAs these models shrink into wearable memory and power budgets, the AI in wearable health market is likely to see a sharper overlap between wellness devices and diagnostic workflows. That overlap will force regulators and incumbent device makers to defend category boundaries that are becoming less clear.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uncertain Regulatory Pathways for AI-Driven Clinical Claims | -1.5% | Global, most acute in North America and EU | Short term (≤ 2 years) |

| Battery-Life Limitations Constrain Always-On Inference | -1.0% | Global | Medium term (2-4 years) |

| Edge-AI Model Drift Caused by Sensor Degradation Over Time | -0.8% | Global, most acute in medical-grade and clinical deployments | Medium term (2-4 years) |

| Ethical Concerns Around Emotion-Recognition Wearables in Workplaces | -0.7% | EU under the AI Act, expanding to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Uncertain Regulatory Pathways for AI-Driven Clinical Claims

The AI in wearable health market still faces slower commercialization when companies want to attach formal clinical claims to AI-driven outputs. The FDA published draft guidance in January 2025 on lifecycle management and marketing submissions for AI-enabled device software functions, but most wearable products still move through existing 510(k) or De Novo routes instead of a dedicated AI-device pathway. That creates friction because many newer algorithms evolve faster than the available predicate base. Incumbents with cleared predicates and prior submission experience can usually manage that uncertainty better than startups building novel algorithms from scratch. The AI in wearable health market therefore risks seeing its most clinically ambitious entrants slowed by regulatory process even while demand for higher-acuity applications keeps rising.

Battery-Life Limitations Constrain Always-On Inference

The AI in wearable health market also remains limited by the power cost of continuous local inference. NXP noted in 2025 that many advanced compute-equipped wearables such as AI glasses carry batteries in the 150 to 300 mAh range, which supports only 60 to 90 minutes of continuous AI-mode operation at standard loads. Ambiq’s compressionKIT helps by reducing memory and transmission load at the source, but that mainly improves communication efficiency rather than solving the core inference budget problem. Innatera’s Pulsar neuromorphic microcontroller showed sub-milliwatt inference levels in 2025, which indicates a path toward lower battery drain for sensor-edge tasks. The challenge for the AI in wearable health market is that multimodal health models demand more compute depth than current low-power chips can yet deliver at scale. That gap is likely to keep always-on clinical inference uneven across product categories over the next few product cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Medical-Grade Wearables Disrupt the Smartwatch Growth Narrative

Smartwatches held 43.44% of AI in wearable health market share in 2025, which kept them as the largest device category because they combine wide consumer familiarity with broad health feature sets. They remain the main access point for ECG, blood oxygen, and hypertension-related monitoring in the AI in wearable health market. A 2024 meta-analysis published in the American Journal of Cardiology series reported 94.8% sensitivity and 95% specificity for the Apple Watch ECG app in atrial fibrillation detection across 4,241 participants. Fitness bands still matter in cost-sensitive settings because they offer a lower entry price for basic health monitoring and support broader penetration in emerging consumer segments. Hearables are also widening the device mix as audio products add medically relevant testing and interpretation.

Medical-grade wearables are projected to expand at 21.69% CAGR through 2031, making them the fastest-growing device segment in the AI in wearable health market. University of Chicago researchers also demonstrated a stretchable AI patch in 2026 that executes inference directly on the body, which points to a longer-term shift toward textile and patch form factors with embedded local intelligence. Those developments show that future growth in the AI in wearable health industry will come from devices designed for continuous care pathways rather than only daily wellness tracking.

By Component: Software's Revenue Dominance Masks Hardware's Strategic Importance

Software accounted for 59.53% of the AI in wearable health market size in 2025, which reflects the pricing power of algorithms, clinical applications, and analytics layers relative to device manufacturing. That revenue structure shows where margins and customer lock-in are strongest in the AI in wearable health market. Research published in Healthcare in 2025 found that combining AI, EHR, and wearable data through HL7 FHIR and SMART on FHIR supports predictive and patient-centered decision support in clinical settings. As interoperability improves, software becomes the layer that turns biosignals into triage flags, workflow prompts, and documentation-ready outputs.

Hardware is anticipated to be the fastest-growing component, with 21.78% CAGR projected through 2031, because the AI in the wearable health market now depends on more capable local processing and better power management. The AI in wearable health market therefore treats hardware as more than a low-margin shell, because sensor layout, NPU performance, and power design are becoming core competitive inputs. Even when revenue concentration sits in software, platform-level control is still shaped by hardware choices that determine what kind of model can run continuously and how long the device can stay on the body.

By Application: Remote Patient Monitoring Overtakes Consumer Wellness as the Value Center

Sports and fitness monitoring captured 51.47% of revenue in 2025, which kept it as the largest application because the installed base of consumer wearables remained much larger than clinical deployments. That position reflects lower regulatory barriers and faster release cycles in the wellness part of the AI in wearable health market. Consumer demand continues to support this segment as brands add coaching, sleep scoring, vascular indicators, and background alerts to familiar products. The segment also benefits from frequent upgrade behavior, because many users replace watches and bands faster than medical devices are refreshed.

Remote patient monitoring is projected to grow at 22.29% CAGR through 2031, which makes it the fastest-moving application in the AI in wearable health market. A January 2026 post-ablation study also showed that Apple Watch users detected AFib recurrence a median of 16 days earlier than standard care, with fewer unplanned hospitalizations. Those findings matter because they shift wearables from supportive data sources to operational tools inside home-based care models. In the AI in wearable health industry, that application is where reimbursement, clinical workflow, and software economics are now converging most clearly.

By AI Algorithm: Edge AI Accelerates as Privacy Mandates Redraw Architecture Choices

Machine learning and predictive analytics held 30.36% of revenue in 2025, making them the largest algorithm group in the AI in wearable health market. Their lead came from wide use in activity classification, sleep staging, anomaly alerts, and baseline risk estimation across commercial devices. These methods remain common because they are easier to validate, lighter to deploy, and already embedded in many existing product lines. Deep learning is gaining ground in ECG interpretation and seizure detection, where peer-reviewed studies continue to report near-clinician performance in defined tasks.

Edge AI and embedded intelligence are projected to grow at 22.15% CAGR through 2031, making them the fastest-growing algorithm category in the AI in wearable health market. Privacy regulation is a central driver because local processing reduces the need to move sensitive health data into cloud environments governed by more demanding compliance obligations. A 2026 Nature Sensors paper also described a cross-modal epidermal sensor that fuses biopotential and biomechanical signals through a single-channel design, which could reduce hardware complexity while improving multimodal inference. As architecture choices shift toward local and hybrid processing, the AI in wearable health market is likely to reward vendors that can balance privacy, latency, and battery performance rather than cloud scale alone.

By End-User: Institutional Adoption Overtakes Individual Users as the Growth Engine

Individual users represented 46.71% of revenue in 2025, which kept them as the largest end-user group in the AI in wearable health market. Consumer spending still supports broad unit volumes because watches, rings, and bands remain easier to purchase than clinically reimbursed solutions. Employers and corporate wellness programs still offer room for expansion, but the EU AI Act has narrowed what is allowed in workplace emotion recognition and similar biometric use cases.

Healthcare providers are expected to grow at 22.26% CAGR through 2031, which makes them the fastest-growing end-user group in the AI in wearable health market. The main reason is that interoperability and reimbursement are now improving at the same time. Long-term care and home healthcare providers are also moving faster because value-based care increasingly depends on monitoring patients outside inpatient settings. That makes institutional adoption less a pilot activity and more a care delivery choice tied to staffing, follow-up quality, and readmission management. The AI in wearable health market is therefore shifting from consumer-led volume toward provider-led value capture, even if individual users remain the largest revenue source today.

Geography Analysis

North America held 54.19% of AI in wearable health market share in 2025, which kept it as the clear revenue leader. The region benefits from concentrated device leadership, deeper insurance infrastructure, and a more established path for digital health reimbursement. The FDA continued shaping market behavior through lifecycle guidance and change-control expectations for AI-enabled software functions, which gave manufacturers more direction on post-market model management. Canada and Mexico are growing contributors, but the United States still anchors regional demand because most reimbursement, platform development, and clinical integration activity remains centered there.

Asia-Pacific is projected to grow at 23.24% CAGR through 2031, making it the fastest-growing region in the AI in wearable health market. China’s policy-backed focus on digital health and remote care is helping move wearables closer to formal healthcare delivery, especially where connectivity and hospital information systems are improving. Japan is also becoming more important because remote care need is rising against physician shortages and because consumer devices with diagnostic features are gaining more attention.

Europe held a meaningful but secondary position in the AI in wearable health market during 2025. Germany remained one of the more mature markets, supported by wider digital health adoption and stronger healthcare IT readiness. The EU AI Act is shaping deployment choices by prohibiting workplace emotion recognition, which limits some enterprise wearable use cases and pushes vendors to focus more clearly on clinical and wellness boundaries. The European Health Data Space and related FHIR-based interoperability efforts may be a short-term compliance burden, but they also support longer-term scaling by making wearable data easier to integrate into formal care systems. South America and the Middle East and Africa remain early-stage contributors, with Brazil and the GCC serving as the main entry points for digital health expansion.

Competitive Landscape

The AI in wearable health market is moderately fragmented overall, even though a few large platforms hold strong positions in select product categories. Apple and Samsung remained central in consumer wearables during 2025 because both companies combine hardware control, operating systems, health apps, and growing AI functionality inside one stack. Apple’s Series 11 hypertension notifications show how a vertically integrated model can turn proprietary data, hardware access, and software updates into a durable advantage. Abbott and Dexcom hold stronger positions in biosensing, where intellectual property, clinical evidence, and regulatory familiarity create higher barriers than those seen in consumer watches.

Clinical monitoring niches remain more distributed, with Masimo, Medtronic, Philips, and Omron competing through cleared portfolios and hospital relationships. AI-native and precision-wellness firms such as Oura, Withings, AliveCor, and Valencell are important because they pressure larger incumbents in specialized sensing, algorithm licensing, and focused use cases. BioIntelliSense’s hospital-scale BioButton deployment is one example of a strategic move that links device credibility with EHR workflow integration rather than direct-to-consumer volume.

There is still open space in long-term care, home healthcare, and multimodal post-surgical monitoring, where no single company has yet built an unquestioned scale advantage. The FDA’s approach to predetermined change control planning gives incumbents with established clearances more room to update AI models efficiently, which can reinforce their lead once a platform is already in clinical use. At the same time, compliance frameworks such as FDA controls, ISO 13485, and GDPR are serving both as entry barriers and as vendor selection filters for institutional buyers. The AI in wearable health market is therefore likely to keep rewarding companies that can combine evidence, integration, and update discipline rather than those that compete on device novelty alone.

AI In Wearable Health Industry Leaders

Apple Inc.

Alphabet Inc.

Samsung Electronics

Garmin Ltd.

Huawei Technologies

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Abbott secured CE Mark for Libre Duo and Libre Duo 10 Day, the world's first dual glucose-ketone continuous monitoring biowearables, measuring both analytes every minute in real time. The approval opens a new clinical market for diabetic ketoacidosis (DKA) prevention monitoring outside hospital settings and is set to launch in select European markets in late 2026.

- March 2026: Ambiq introduced details of Atomiq110, an upcoming SoC built on its 12nm SPOT® platform designed to operate at ultra-low voltages down to 300 mV, targeting always-on AI inference for advanced medical-grade wearables. Production is scheduled for 2027.

- March 2026: Nordic Semiconductor announced broad commercial availability of the nRF54LM20B NPU-enabled SoC for ultra-low-power edge AI in wearable medical sensors, enabling real-time activity detection, anomaly identification, and movement interpretation without cloud dependence.

Global AI In Wearable Health Market Report Scope

According to the report’s scope, AI in wearable health market refers to the use of artificial intelligence technologies in wearable devices, such as smartwatches, fitness trackers, and biosensors, to collect, analyze, and interpret health data in real time. These solutions enable continuous health monitoring, predictive insights, personalized wellness recommendations, early disease detection, and improved patient care through data-driven decision-making.

The AI in wearable health market is segmented into device type, component, application, AI algorithm, end-user, and geography. By device type, the market is segmented into smartwatches, fitness bands, hearables, smart clothing and patches, medical-grade wearables, and other device types. By component, the market is segmented into software and hardware. By application, the market is segmented into remote patient monitoring, chronic disease management, sports and fitness monitoring, clinical and diagnostic monitoring, and other applications. By AI algorithm, the market is segmented into machine learning and predictive analytics, deep learning, edge AI and embedded intelligence, and multimodal AI (sensor fusion). By end-user, the market is segmented into individual users, healthcare providers, long-term care and home healthcare providers, employers and corporate wellness programs, and payers and insurance companies. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Smartwatches |

| Fitness Bands |

| Hearables |

| Smart Clothing and Patches |

| Medical-Grade Wearables |

| Other Device Types |

| Software |

| Hardware |

| Remote Patient Monitoring |

| Chronic Disease Management |

| Sports and Fitness Monitoring |

| Clinical and Diagnostic Monitoring |

| Other Applications |

| Machine Learning and Predictive Analytics |

| Deep Learning |

| Edge AI and Embedded Intelligence |

| Multimodal AI (sensor fusion) |

| Individual Users |

| Healthcare Providers |

| Long-Term Care and Home Healthcare Providers |

| Employers and Corporate Wellness Programs |

| Payers and Insurance Companies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Device Type | Smartwatches | |

| Fitness Bands | ||

| Hearables | ||

| Smart Clothing and Patches | ||

| Medical-Grade Wearables | ||

| Other Device Types | ||

| By Component | Software | |

| Hardware | ||

| By Application | Remote Patient Monitoring | |

| Chronic Disease Management | ||

| Sports and Fitness Monitoring | ||

| Clinical and Diagnostic Monitoring | ||

| Other Applications | ||

| By AI Algorithm | Machine Learning and Predictive Analytics | |

| Deep Learning | ||

| Edge AI and Embedded Intelligence | ||

| Multimodal AI (sensor fusion) | ||

| By End-User | Individual Users | |

| Healthcare Providers | ||

| Long-Term Care and Home Healthcare Providers | ||

| Employers and Corporate Wellness Programs | ||

| Payers and Insurance Companies | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in AI in wearable health through 2031?

Growth is being supported by on-device AI, smaller low-power chipsets, and stronger reimbursement for remote monitoring. The market is projected to rise from USD 13.04 billion in 2025 to USD 15.28 billion in 2026 to reach USD 39.18 billion by 2031 at 20.72% CAGR.

Which device category leads revenue today?

Smartwatches lead revenue with 43.44% share in 2025 because they combine broad adoption with features such as ECG, blood oxygen, and hypertension-related monitoring.

Why is software larger than hardware in this field?

Software held 59.53% of revenue in 2025 because algorithms, clinical decision support, and analytics create more margin and stronger customer retention than physical devices alone.

Which region is likely to expand the fastest?

Asia-Pacific is expected to grow at 23.24% CAGR through 2031, helped by policy support, rising remote care needs, and strong wearable adoption across major regional markets.

Page last updated on: