Healthcare Interoperability AI Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 0.98 Billion |

| Market Size (2031) | USD 2.28 Billion |

| Growth Rate (2026 - 2031) | 18.25% CAGR |

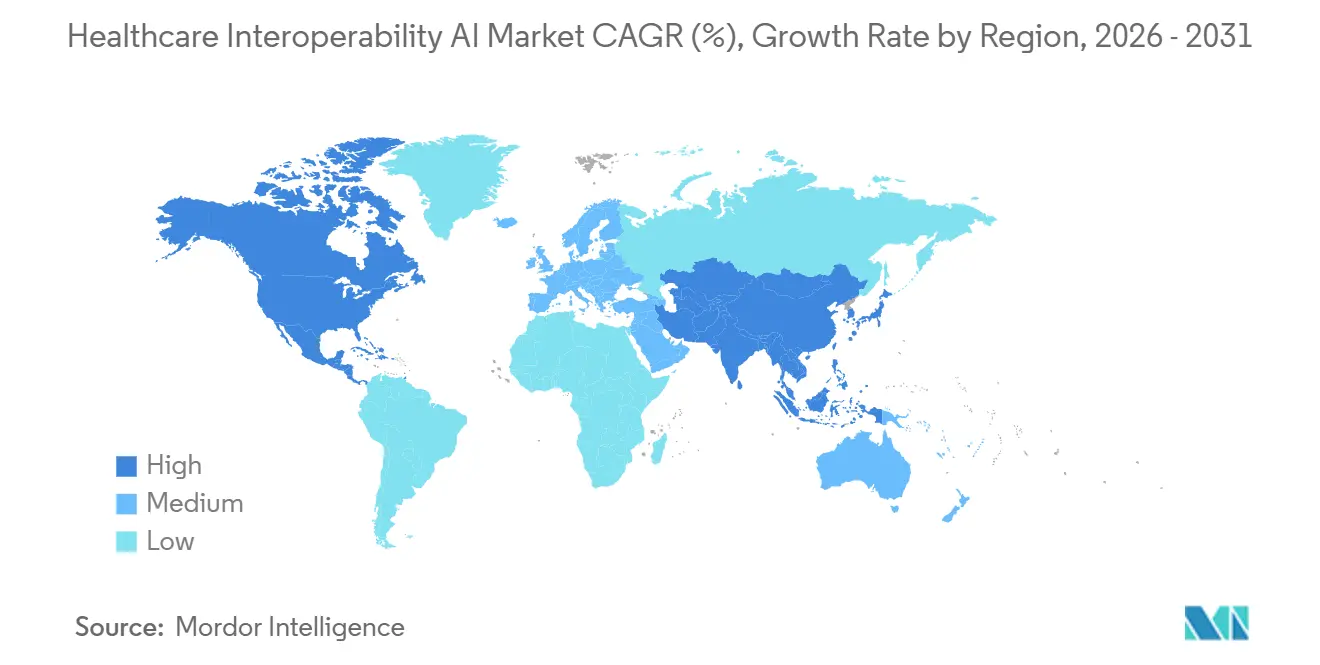

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

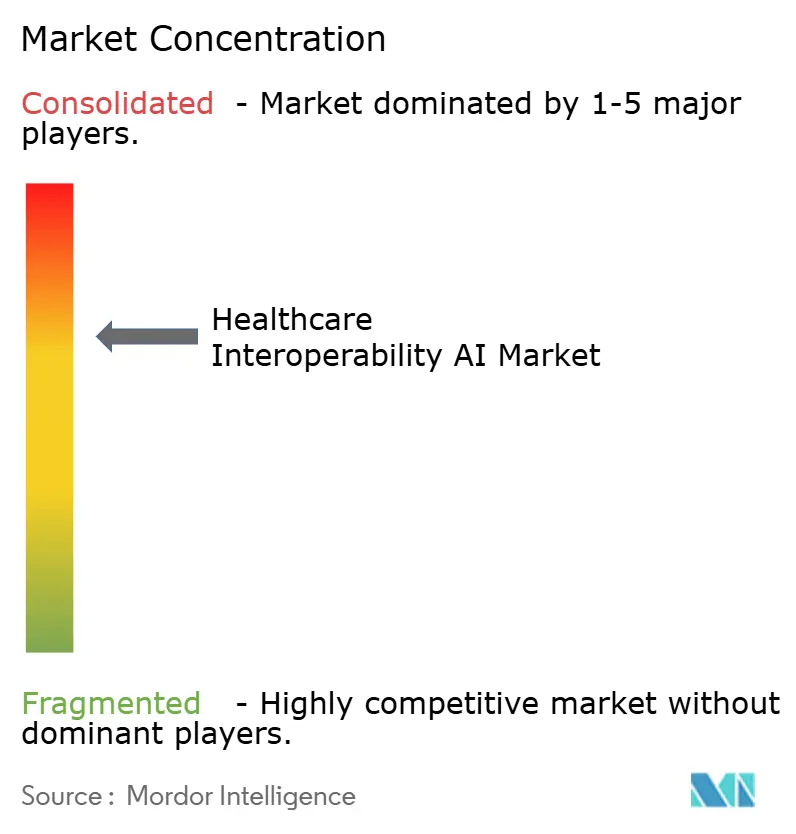

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Interoperability AI Market Analysis by Mordor Intelligence

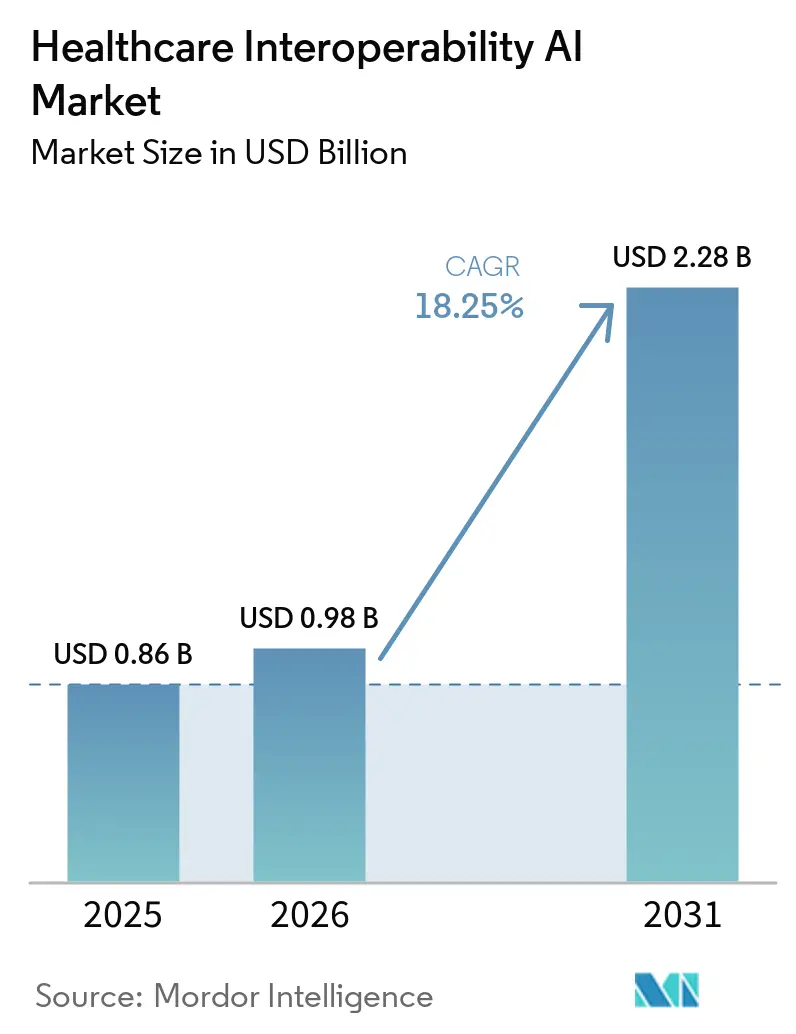

The Healthcare Interoperability AI Market size reached USD 0.86 billion in 2025 and is projected to reach USD 2.28 billion by 2031, at a CAGR of 18.25% from 2026 to 2031. The growth reflects synchronized regulatory pressure, maturing FHIR-native APIs, and growing automation in payer and provider workflows that now require AI-ready data flows at scale. Regulatory mandates in the United States and the European Union set firm timelines for API-based patient data access and standardized formats, shifting interoperability from optional innovation to operational infrastructure. Hyperscaler cloud platforms are embedding AI into ingestion and transformation pipelines that convert unstructured records into FHIR resources, which shortens integration cycles and supports real-time exchange. Payer–provider automation through ePA and clinical attachments depends on NLP and LLM-assisted extraction to pre-populate forms and speed determinations, which helps meet decision timelines and public reporting obligations. Emerging real-time patterns, including event-driven streaming via FHIR Subscriptions and cloud notifications, reduce data latency for clinical coordination and operational analytics.

Key Report Takeaways

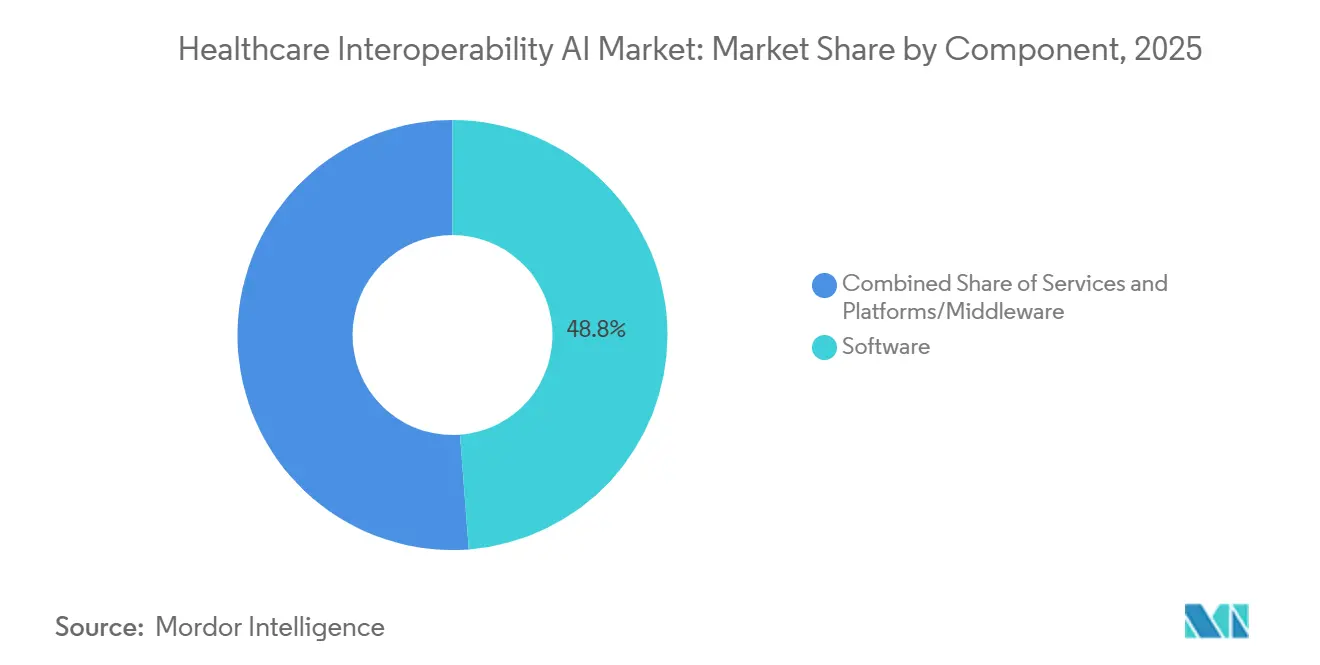

- By component, software led with 48.79% revenue share in 2025. platforms/middleware is projected to expand at a 20.46% CAGR through 2031.

- By application, data ingestion and normalization accounted for a 46.35% share in 2025. Clinical document understanding is forecast to grow at a 21.34% CAGR through 2031.

- By deployment, Cloud captured 56.73% share in 2025. Cloud deployments are projected to grow at a 22.41% CAGR through 2031.

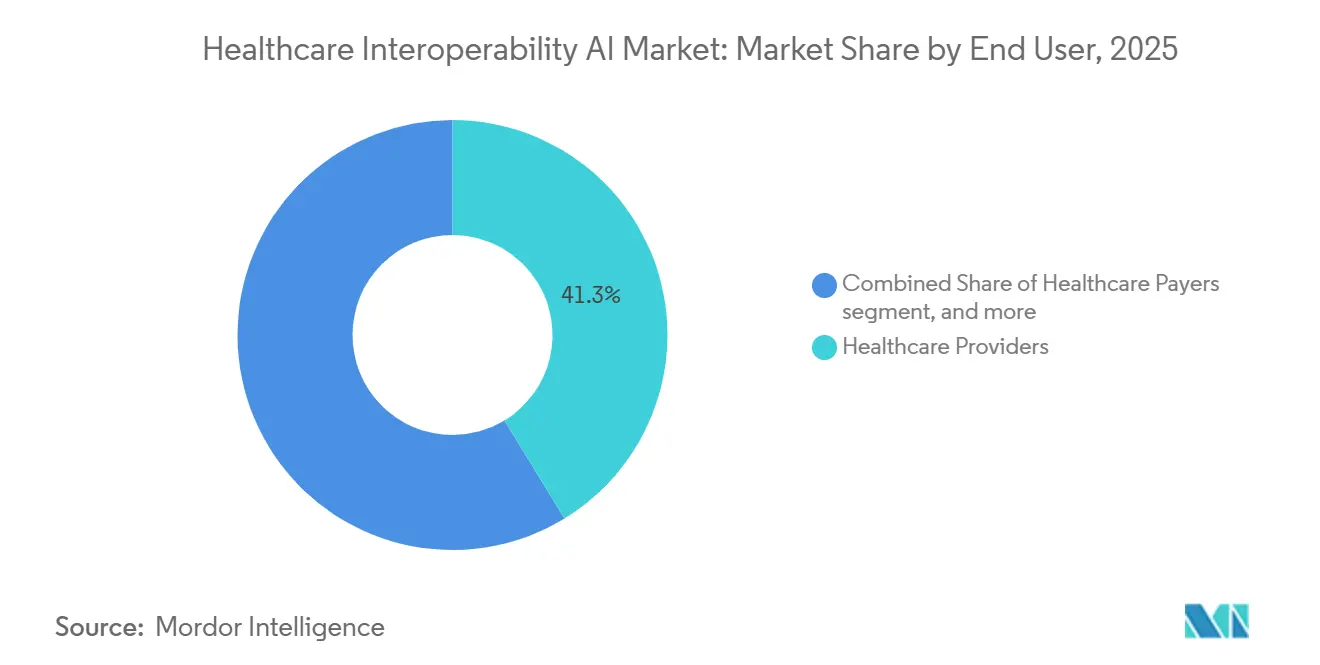

- By end user, healthcare providers represented 41.29% share in 2025. Healthcare payers are projected to post the fastest growth at a 21.14% CAGR through 2031.

- By interoperability level, foundational approaches held 47.17% share in 2025. Structural interoperability is projected to expand at a 20.26% CAGR through 2031, aligned to broader FHIR R4 adoption.

- By geography, North America held 48.62% share in 2025. Asia-Pacific is projected to be the fastest-growing region at a 22.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Interoperability AI Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory mandates accelerating FHIR-based exchange and API interoperability | +4.2% | Global, with North America (CMS-0057-F) and EU (EHDS Regulation) leading; spillover to APAC via national digital health programs | Short term (≤ 2 years) |

| Payer–provider automation mandates (ePA, attachments) scaling AI-mediated exchange | +3.8% | North America core, early adoption in EU via RWD/RWE programs, limited APAC penetration | Medium term (2-4 years) |

| Cloud-native health data platforms embed AI for unstructured-to-FHIR conversion | +3.5% | Global, hyperscaler dominance in North America and EU; APAC uptake in India and Australia | Short term (≤ 2 years) |

| RWD/RWE pipelines need automated normalization and terminology mapping | +2.9% | Global, driven by FDA and EMA guidance; APAC pharma R&D acceleration | Medium term (2-4 years) |

| LLM-assisted clinical document understanding reduces integration backlog | +2.7% | North America and EU early majority; APAC pilot phase | Short term (≤ 2 years) |

| Event-driven streaming (FHIR subscriptions, IoMT) enabling real-time harmonization | +1.1% | North America and EU; high IoMT penetration in selected APAC markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Mandates Accelerating FHIR-Based Exchange and API Interoperability

U.S. policy now compels payers to publish and operate four FHIR R4-based APIs by January 1, 2027, covering Patient Access, Provider Access, Payer-to-Payer, and Prior Authorization, with decision timelines set at 7 days standard and 72 hours expedited and with annual public reporting of prior authorization metrics starting in 2026.[1]Centers for Medicare & Medicaid Services, “Interoperability and Prior Authorization Final Rule (CMS-0057-F),” Federal Register, federalregister.govThese rules are built on HL7 FHIR R4 and associated implementation guides that standardize resource models, security, and bulk data access, which reduces integration variability and supports scalable exchange. In Europe, the European Health Data Space sets mandatory interoperability and security obligations by January 2026 for providers and vendors, requires primary-use data exchange of patient summaries and e-prescriptions by March 2029, and phases in imaging and lab data by March 2031 with significant administrative fines for non-compliance. DARWIN EU expanded its evidence-generation capacity through 2025, signaling stronger institutional support for multi-database RWD studies that depend on standardized exchange and curation. U.S. TEFCA governance, alongside Facilitated FHIR, sets neutral exchange conditions that help interoperability move from bilateral connections to network-scale data liquidity. These policies direct investment toward API-first architectures, structured data exchange, and consent-aware workflows that AI systems can use reliably across organizational boundaries.

Payer–Provider Automation Mandates (ePA, Attachments) Scaling AI-Mediated Exchange

Physicians reported high administrative burdens from prior authorization in 2024, including frequent requests and time lost to documentation, which heightened the need for automated evidence retrieval and form completion inside EHR workflows.[2]American Medical Association, “2024 Prior Authorization Physician Survey,” AMA, ama-assn.org The HL7 Da Vinci Implementation Guides operationalize ePA through CRD, DTR, and PAS, enabling real-time checks, structured documentation capture, and FHIR-based submission that can be augmented by AI to extract evidence from charts. Federal timelines and public reporting requirements incentivize automation that meets utilization management standards while providing auditable decisions. Early pilots show material cycle-time and approval-rate gains when structured data and NLP are used to pre-populate documented criteria at order time and during appeals. Attachments automation through Da Vinci CDex allows payers to request discrete clinical elements, which scales better than fax-based attachments and supports explainability for clinical reviewers. As regulators and plans scrutinize algorithmic decisions, systems that trace inputs, justifications, and timings will become requirements for sustained ePA performance.

Cloud-Native Health Data Platforms Embed AI for Unstructured-To-FHIR Conversion

Cloud platforms now combine HIPAA-eligible services, integrated medical NLP, and FHIR-native storage to transform unstructured documents into queryable resources at scale.[3]AWS News Team, “AWS HealthLake Data Transformation Agent,” AWS News Blog, aws.amazon.com AWS HealthLake’s data transformation agent accepts CCDA inputs, produces FHIR Bundles in seconds, supports human validation, and applies natural-language template customization to accelerate conversions from weeks to days. Google Cloud Healthcare API publishes event notifications for FHIR resource creation, updates, and deletions, which helps downstream services react in near real time with consistent security primitives. Azure Health Data Services routes health data events into serverless functions and event hubs, enabling operational automation with PHI-compliant controls and auditability. Vendors are also advancing multimodal health data assembly on a FHIR backbone to support analytics and model training with strong governance and lineage controls. These capabilities are shifting budgets away from brittle point-to-point interfaces toward centralized orchestration that can power analytics, operational workflows, and safety-critical applications in one environment.

RWD/RWE Pipelines Need Automated Normalization and Terminology Mapping

Regulators have clarified expectations for using EHR and claims data in submissions, which elevates the importance of data provenance, semantic mapping, and methodological transparency in real-world evidence packages. ICH E23 aims to harmonize principles for RWD quality, metadata, and FAIR practices, which sets a common direction for sponsors that must run consistent pipelines across regions.[4]International Council for Harmonisation, “ICH E23 Concept Paper: Considerations for the Use of Real-World Evidence,” ICH, ich.org Distributed research networks using common data models rely on consistent mappings across vocabularies to enable federated queries without data centralization. Model-agnostic validation frameworks are emerging to demonstrate that AI-extracted clinical variables meet quality thresholds through performance metrics, automated verification checks, and replication against trusted comparators. These guardrails are pushing the Healthcare Interoperability AI Market toward interoperable curation workflows that can be audited at variable and cohort levels. As a result, sponsors and health systems prioritize normalized, lineage-rich datasets that reduce downstream friction during regulatory and payer reviews.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy, consent, and cross-border data transfer constraints | -3.7% | Global, with EU (GDPR, EHDS) strictest; U.S. HIPAA baseline plus states; varied APAC rules | Short term (≤ 2 years) |

| Heterogeneous legacy systems and shortages of skilled integration talent | -2.8% | Global, acute in North America and EU; moderated in APAC with greenfield cloud adoption | Medium term (2-4 years) |

| Validation burden and explainability risks for AI-generated mappings | -1.4% | North America and EU lead with formal guidance; APAC frameworks emerging | Medium term (2-4 years) |

| Ecosystem lock-in and commercial disincentives to portability | -1.1% | Global, notable in large EHR vendor markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy, Consent, and Cross-Border Data Transfer Constraints

GDPR classifies health data as a special category that requires explicit consent and imposes steep administrative penalties for violations, which increases the cost and complexity of secondary-use pipelines and cross-border flows for AI model development. HIPAA sets U.S. baseline safeguards and breach notification rules, which shape how organizations design encryption, access controls, and risk assessments for PHI in cloud-native environments that run AI workloads. Proposed HIPAA Security Rule updates would formalize stronger requirements on encryption, multifactor authentication, asset inventories, and vulnerability scanning, which can accelerate modernization toward platforms that provide managed security controls. EHDS introduces secure processing environments for secondary-use data, while strict enforcement and reciprocity conditions can limit access for non-EU applicants, which pushes organizations toward in-region compute enclaves. Recorded breach volumes in recent years underscore the need for consent-aware data flows, robust encryption, and audit trails when deploying AI in production pipelines. These governance demands influence vendor selection and architecture patterns across the Healthcare Interoperability AI Market because compliance, consent, and cross-border transfer rules now define technical guardrails for sustained operations.

Heterogeneous Legacy Systems and Shortages of Skilled Integration Talent

Many providers still run older systems that were not built for OAuth 2.0, RESTful interfaces, or FHIR R4, which necessitates middleware translation from HL7v2, CCDA, and proprietary formats into standardized resources for downstream use. Point-to-point connections raise maintenance costs and introduce fragility when new endpoints and data types are added, which slows deployment of AI use cases that depend on reliable inputs . Health information leaders report persistent workforce gaps in technical roles, which constrains the speed of modernization and security hardening. Many teams must prioritize maintaining legacy integrations over new buildouts, which delays adoption of event-driven architectures and unified data layers for AI training and inference. These constraints increase reliance on cloud services and specialized middleware providers that can compress integration timelines with prebuilt connectors and managed services. As organizations tackle talent shortages and technical debt, the Healthcare Interoperability AI Market benefits from solutions that abstract legacy complexity and enforce governance in one place.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Platforms Orchestrate Multi-Vendor Data Flows

Software held 48.79% of Healthcare Interoperability AI market share in 2025, while Platforms/Middleware is projected to post the fastest 20.46% CAGR through 2031 as buyers consolidate point connections into orchestrated hubs for reliable real-time data access. This shift reflects the operational need to mediate HL7v2 feeds, bulk exports, and FHIR Subscriptions through consent-aware middleware that enforces a single governance layer across many endpoints. Platform growth is further supported by cloud-native data services that streamline CCDA-to-FHIR conversion, event routing, and validation logs into turnkey workflows, which lowers implementation time and cost for large-scale transformations. Ecosystem vendors publish hundreds of production APIs and notification hooks that third parties consume to build clinical and administrative automation, which increases network effects around high-volume platforms. The Healthcare Interoperability AI Market benefits from platforms that can scale ingestion while ensuring audit trails, access controls, and structured outputs that are ready for analytics and model training.

As endpoint complexity grows, orchestrators reduce maintenance overhead, simplify upgrades to new standards, and create predictable integration patterns that accelerate downstream AI use cases. Platforms combine FHIR-native data stores and managed event infrastructure so developers can subscribe to changes, retrieve context through APIs, and build decision support on top of complete patient and claims histories. High-volume exchange also requires consent-aware enforcement with consistent policy application, which middleware can centralize and document for audits and patient access rights. With regulatory timelines now fixed in major markets, demand has shifted from custom one-off interfaces to scalable platforms that spread operational investment across many use cases. Platform-led approaches also future-proof against new evidence needs and regulatory updates by decoupling data capture from application logic and by standardizing normalized outputs for analytics.

By Application: NLP-Driven Document Understanding Gains Urgency

Data Ingestion and Normalization accounted for 46.35% of the Healthcare Interoperability AI market size in 2025, reflecting the foundational need to standardize HL7v2 messages, CCDA files, and other formats into FHIR resources for routine analytics and reporting. Clinical Document Understanding is projected to grow the fastest at a 21.34% CAGR as LLM-enabled extraction turns unstructured notes and reports into structured data that can support ePA, quality measures, and RWD/RWE submissions. Attachment processing and payer workflows are also expanding as AI systems pre-populate evidence fields and track determinations against timelines and audit requirements. These applications rely on source-of-truth references and validation frameworks that confirm variable-level performance and cohort-level replication against established comparators. As event-driven exchange matures, real-time normalization and NLP extraction will feed downstream automation for care coordination and utilization management.

Within the Healthcare Interoperability AI industry, platforms with integrated medical NLP and configurable transformation templates shorten delivery cycles and adapt to local documentation nuances with less overhead. Clinical abstraction tools with read-only EHR connectivity help produce registry-ready outputs with embedded citations, which increases trust and speeds adoption in clinical quality programs. Coding accuracy and revenue improvements follow when human reviewers validate AI-extracted data in refined workflows, which contribute to measurable financial impact for provider organizations. With FDA guidance clarifying credibility expectations, demand is rising for systems that integrate explainability, dataset lineage, and fairness audits into operational pipelines. These capabilities underpin consistent automation across clinical documentation, payer attachments, and regulatory evidence capture.

By Deployment Mode: Cloud Dominance Accelerates via Hyperscaler Offerings

Cloud deployments captured 56.73% share of the Healthcare Interoperability AI market size in 2025 and are projected to post a 22.41% CAGR, supported by HIPAA-eligible services, managed event infrastructure, and rapid template-driven transformations for standardizing clinical data. Managed encryption, audit trails, and service catalog depth reduce the friction to ingest, normalize, and exchange data across large networks with strict governance and consent needs. Cloud-native platforms also publish event notifications to support real-time clinical and operational automation without heavy polling, which improves timeliness for downstream systems. These advantages drive consolidation into centralized platforms that unify ingestion, storage, and model training while enabling hybrid controls where data residency rules apply. Cloud services evolve quickly to align with new FHIR profiles and regulatory demands, which reduces cost of keeping current with mandated standards.

On-premises and hybrid patterns remain where data residency, sovereign controls, or specialized compliance regimes apply, but the overall trend favors migration to managed services that simplify upgrades and security hardening at scale. As organizations modernize to meet ePA timelines, structural interoperability goals, and TEFCA exchange requirements, cloud platforms become anchor points for API-first architectures that supervise both ingestion and event-driven distribution. Natural-language template customization further lowers the barrier to operationalize complex transformations for CCDA and other documents, which improves delivery predictability for large ingest programs. The Healthcare Interoperability AI Market therefore tracks toward cloud-native orchestration as buyers prioritize speed, governance, and extensibility over custom point solutions.

By End User: Payers Accelerate Under ePA Mandates

Healthcare Providers represented 41.29% of 2025 revenue, reflecting ongoing integration of EHRs, lab systems, and imaging archives with analytics and quality programs that rely on normalized FHIR resources. Healthcare Payers are projected to grow fastest at a 21.14% CAGR through 2031, driven by CMS timelines for Patient Access, Provider Access, Payer-to-Payer, and Prior Authorization APIs alongside reporting obligations for approval, denial, and timing metrics. Payers are adopting platforms that orchestrate data across many sources, apply coverage rules, and generate audit-ready trails for determinations, appeals, and compliance attestations. Provider organizations continue to scale NLP and LLM-based extraction to reduce documentation burden and to improve care coordination, coding accuracy, and clinical evidence assembly. These adoption patterns reinforce shared infrastructure where API access, event notifications, and consent-aware data routing support both administrative and clinical uses in one environment.

Life sciences teams depend on normalized, high-quality RWD for feasibility, submissions, and post-market analytics, which extends demand for standardized pipelines and governance controls across the research lifecycle. EMA’s DARWIN EU and other EU-level initiatives broaden access to multi-country data through governance-led frameworks that favor standardized exchange and controlled processing environments. With clearer expectations from regulators and payers, end users invest in architectures that extract structured data from narratives with evidence trails that meet audit requirements, which supports broader adoption across stakeholders in the Healthcare Interoperability AI Market. As payer ePA programs mature and provider automation deepens, shared technical investments accrue across care delivery, reimbursement, and evidence generation.

By Interoperability Level: Structural Standards Displace Foundational Connectivity

Foundational connectivity still dominates many settings and captured 47.17% in 2025 as legacy HL7v2 feeds, file drops, and direct messaging persist, especially in smaller practices and resource-constrained environments. Structural interoperability is projected to expand at a 20.26% CAGR as FHIR R4 becomes the reference model for APIs, event notifications, and bulk data exports that preserve meaning across exchanges. As vendors expose richer FHIR APIs and align to regulatory timelines, organizations standardize on resource models that simplify mappings, security models, and validation for clinical and administrative uses. These patterns enable semantic layers and common data models to operate more reliably across participants, which improves comparability and speeds federation in research and quality measurement.

Organizational interoperability grows in importance as TEFCA and similar frameworks define participation terms, consent handling, and nondiscrimination obligations, which provide the basis for predictable multi-party exchange. As consent policies become computable, consent-aware query enforcement can occur in near real time, which reduces manual effort while protecting patient rights. Together, these levels move data flows toward normalized, audit-ready exchange that AI systems can reuse across many applications in the Healthcare Interoperability AI Market.

Geography Analysis

North America accounted for 48.62% share of the Healthcare Interoperability AI market size in 2025, supported by firm CMS timelines for FHIR APIs and by adoption of TEFCA-based exchange models that favor standardized, consent-aware interoperability. Health systems, payers, and vendors are scaling event-driven architectures and automation that rely on AI to extract structured evidence and to power ePA, quality programs, and operations analytics. TEFCA implementation sets shared expectations for nondiscriminatory access, which improves cross-network exchange and expands the platform opportunity for API-first orchestration. Vendor investments in FHIR APIs, notifications, and workflow-enablement accelerate in this environment, which raises the baseline for real-time harmonization and for LLM-based extraction integrated into clinical systems. As a result, the Healthcare Interoperability AI Market in North America is characterized by policy-led adoption and rapid platform improvements that support both administrative and clinical exchange.

Europe is building a comprehensive framework under EHDS that sets deadlines for interoperable primary-use data exchange and a governance model for secondary-use access through secure processing environments, which supports AI development and evidence generation. DARWIN EU expands the supply of regulatory-grade RWD studies and elevates the importance of standardized data flows and common models to enable rapid, multi-country analyses. As EHDS deadlines approach, European providers and vendors must align systems to FHIR profiles and secure exchange requirements, which creates demand for platforms that standardize and automate transformations and events. These changes position the Healthcare Interoperability AI Market in Europe for higher baseline interoperability and broader secondary-use access that can be harnessed for analytics, surveillance, and AI model validation. Policy strength coexists with varied national implementations, which sustains near-term demand for orchestration layers that can align heterogeneous local systems into consistent flows.

Asia-Pacific is projected to be the fastest-growing region at a 22.27% CAGR as national health stacks and FHIR-centered programs expand access, standardize exchange, and embed AI in public health and chronic disease management workflows. Cloud-first deployments in several APAC markets avoid legacy constraints and favor managed services that deliver security, auditability, and rapid AI enablement for streaming data sources. Public-sector initiatives across the region are incorporating standards-based exchange that supports population-level analytics and cross-institutional coordination, which increases the role of event-driven architectures for critical use cases. The Healthcare Interoperability AI Market in APAC therefore benefits from greenfield design, regulatory support for modernization, and growing demand for consent-aware AI deployment that can scale across diverse health systems. As these programs mature, platform providers that combine standardized ingestion, real-time notifications, and strong governance will capture growth opportunities across this region.

Competitive Landscape

The Healthcare Interoperability AI Market features active participation from EHR vendors, hyperscalers, and specialized middleware providers that converge on FHIR-native exchange, event-driven patterns, and AI-augmented extraction. EHR incumbents continue to expand published FHIR APIs and network exchange participation while keeping control of clinical workflows and marketplaces that govern app distribution. Hyperscalers differentiate on integrated NLP, managed event infrastructure, and secure data stores that support rapid normalization and streaming without extensive custom development. Specialist vendors focus on bridging legacy protocols and ensuring consent-aware federation, which positions them as orchestration backbones for multi-system exchange.

Recent strategic moves underscore the platform race and regulatory alignment. Epic accelerated TEFCA enrollment to bring more hospitals into network-based exchange with broad access through FHIR APIs and vetted apps, which strengthens its platform position. AWS released a HealthLake data transformation agent that turns CCDA files into FHIR Bundles with natural-language customization, which compresses project timelines and supports auditability at ingest. Google Cloud and Microsoft advanced event frameworks to let downstream services react to FHIR changes in a secure, scalable manner, which reduces polling and latency across clinical and administrative workflows. These moves align with policy shifts that require standardized, timely exchange and with buyer priorities for explainable automation that meets audit and security requirements.

Oracle Health’s migration focus toward FHIR R4 and its cloud stack reinforces regulatory timelines and modern event models while shifting customers from legacy endpoints to current interfaces and governance patterns. Middleware providers integrate across EHRs and external data systems to normalize representations and enforce consent-aware policy, which reduces the technical debt of maintaining many bespoke connections. As ePA and structured attachments scale, vendors that combine high-quality NLP extraction, credible validation, and consistent event routing will stand out for reliability and compliance readiness across payers and providers. The overall competitive narrative is shaped by policy-led standardization, cloud-platform leverage, and demand for operational proof that AI-derived data meets regulatory and payer expectations at production scale.

Healthcare Interoperability AI Industry Leaders

Epic Systems

Oracle

Microsoft

Google Cloud

InterSystems

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: AWS announced the preview of its HealthLake data transformation agent for automated CCDA-to-FHIR conversion with AI-powered template customization, accelerating transformation and enabling rapid validation and ingest.

- February 2026: The Sequoia Project released state privacy and consent guidance to support automated, high-confidence enforcement of sensitive-health-data rules across state lines in computable consent engines.

- December 2025: Oracle Health confirmed deprecation of FHIR DSTU-2 in favor of FHIR R4 and expanded cloud-native features, guiding customers to current endpoints aligned to regulatory timelines.

Global Healthcare Interoperability AI Market Report Scope

As per the scope of this report, healthcare interoperability AI refers to the use of machine‑learning and automation technologies to enable seamless exchange, interpretation, and integration of clinical and administrative data across disparate healthcare systems. It helps standardize unstructured information, resolve data mismatches, and ensure real‑time, secure connectivity between EHRs, labs, imaging systems, payers, and other platforms, supporting coordinated care and more efficient enterprise workflows.

The healthcare interoperability AI market is segmented into component, application, deployment mode, end user, interoperability level, and geography. By component, the market is segmented into software, services, and platforms/middleware. By application, the market is segmented into data ingestion and normalization, clinical document understanding, patient matching and identity resolution, prior authorization and claims attachments automation, and others. By deployment mode, the market is segmented into cloud, on-premises, and hybrid. By end user, the market is segmented into healthcare providers, healthcare payers, life sciences/pharma companies, and others. By interoperability level, the market is segmented into foundational, structural, semantic, and organizational. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Platforms/Middleware |

| Data Ingestion and Normalization |

| Clinical Document Understanding |

| Patient Matching and Identity Resolution |

| Prior Authorization and Claims Attachments Automation |

| Others |

| Cloud |

| On-Premises |

| Hybrid |

| Healthcare Providers |

| Healthcare Payers |

| Life Sciences / Pharma Companies |

| Others |

| Foundational |

| Structural |

| Semantic |

| Organizational |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Platforms/Middleware | ||

| By Application | Data Ingestion and Normalization | |

| Clinical Document Understanding | ||

| Patient Matching and Identity Resolution | ||

| Prior Authorization and Claims Attachments Automation | ||

| Others | ||

| By Deployment Mode | Cloud | |

| On-Premises | ||

| Hybrid | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Life Sciences / Pharma Companies | ||

| Others | ||

| By Interoperability Level | Foundational | |

| Structural | ||

| Semantic | ||

| Organizational | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the Healthcare Interoperability AI Market growth outlook to 2031?

The Healthcare Interoperability AI Market is projected to grow from USD 0.86 billion in 2025 to USD 2.28 billion by 2031 at a 18.25% CAGR from 2026 to 2031.

Which deployment approach is expanding fastest in this space?

Cloud deployments are projected to grow the fastest with a 22.41% CAGR due to HIPAA-eligible services, integrated events, and rapid CCDA-to-FHIR transformation workflows.

Which applications are seeing the strongest momentum?

Clinical Document Understanding is the fastest-growing application as LLM-enabled extraction converts unstructured notes into FHIR resources for ePA, quality measures, and RWD/RWE, underpinned by credible validation frameworks.

What region holds the largest share today and which is growing fastest?

North America held the largest share in 2025, while Asia-Pacific is projected to be the fastest-growing region through 2031 due to national digital health programs and cloud-first deployments.

Page last updated on: