AI-Based Patient Recruitment And Retention Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

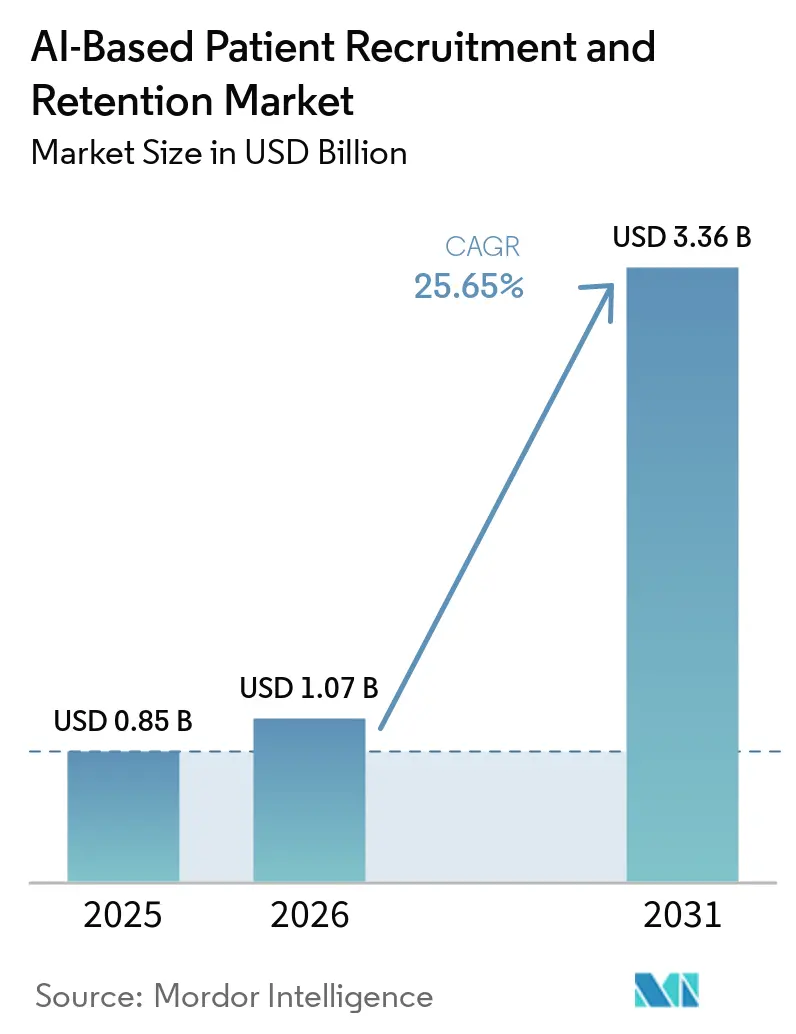

| Market Size (2026) | USD 1.07 Billion |

| Market Size (2031) | USD 3.36 Billion |

| Growth Rate (2026 - 2031) | 25.65% CAGR |

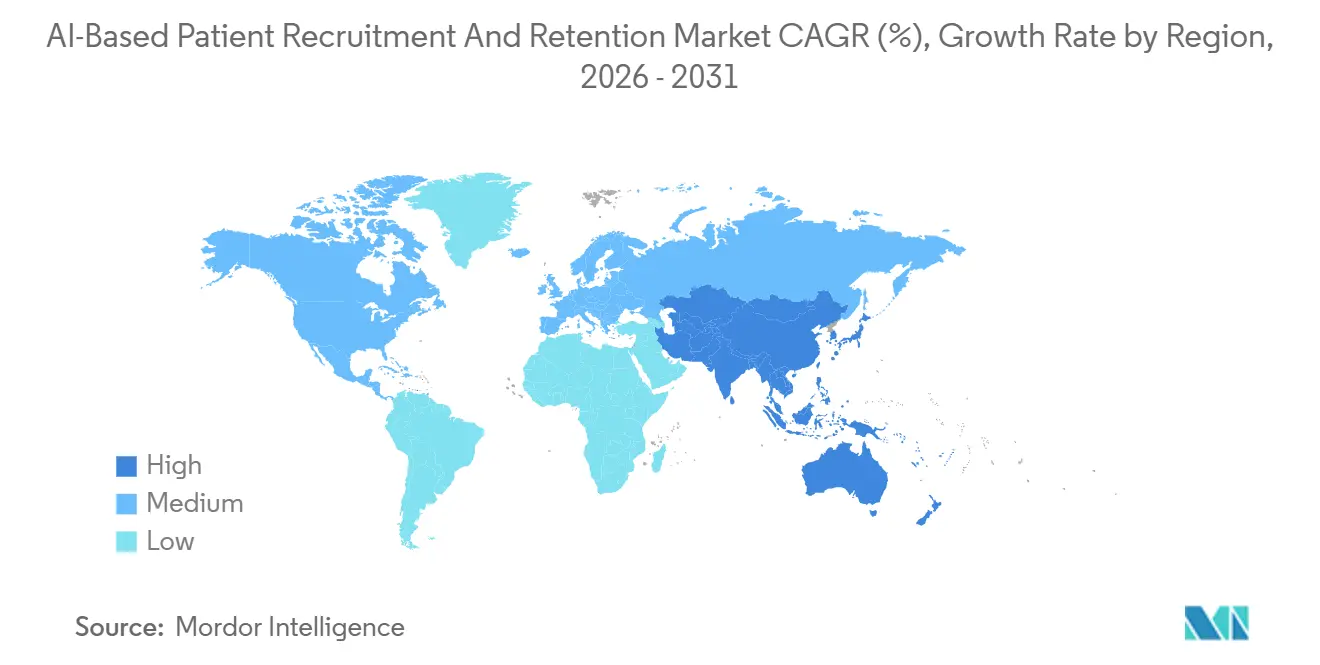

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

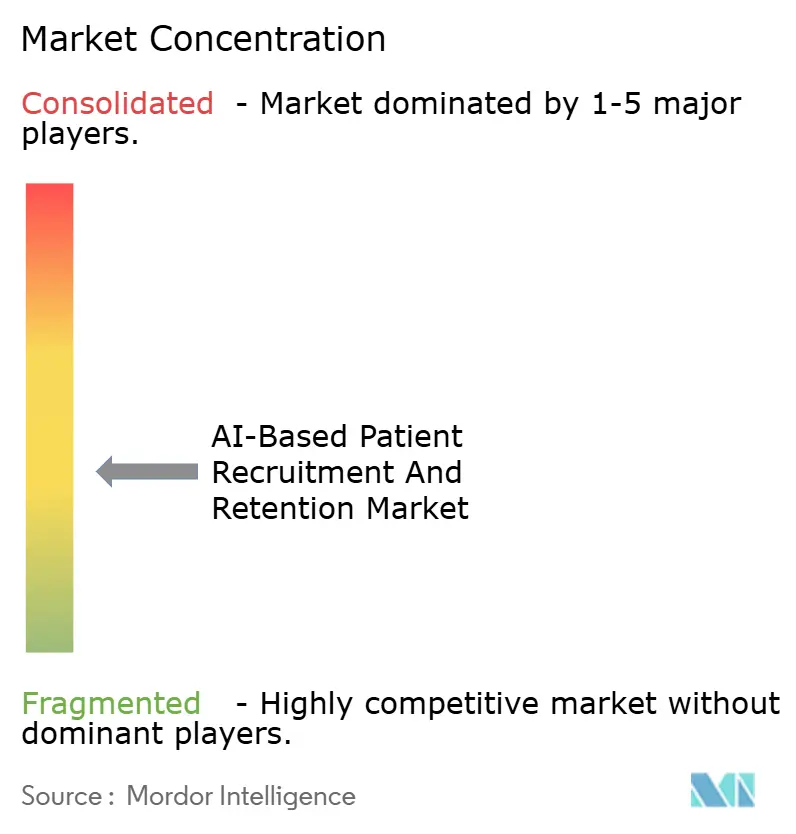

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI-Based Patient Recruitment And Retention Market Analysis by Mordor Intelligence

The AI-Based Patient Recruitment And Retention Market size is expected to grow from USD 0.85 billion in 2025 to USD 1.07 billion in 2026 and is forecast to reach USD 3.36 billion by 2031 at 25.65% CAGR over 2026-2031.

Regulatory approvals for decentralized designs, along with nationwide interoperability enabled by TEFCA, are expanding the pool of potential trial candidates across various therapeutic areas. Additionally, the decreasing costs of large language model prescreening are driving this growth. Sponsors leveraging electronic health records, claims data, and wearable technology can now identify eligible participants within days instead of months, significantly reducing protocol start-up timelines and minimizing screening failures. Strategic acquisitions, such as Tempus AI's purchase of Deep 6 AI, are consolidating data platforms, providing vendors with scale advantages in model training. Remote-first designs are also increasing access to late-phase oncology and rare-disease studies by enabling community clinics, which previously faced staffing challenges, to conduct intensive eligibility reviews more effectively.

Key Report Takeaways

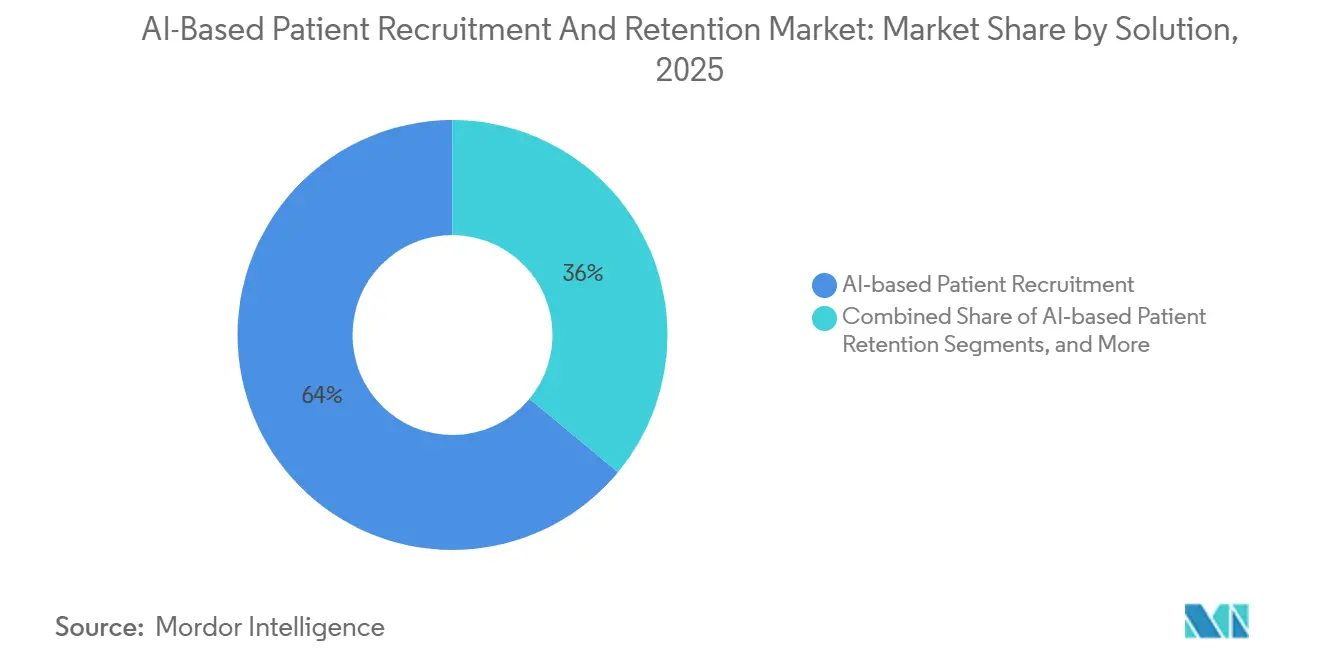

- By solution, AI-based patient recruitment led with 63.98% of the AI-based patient recruitment and retention market share in 2025, while AI-based patient retention tools are projected to advance at a 28.77% CAGR through 2031.

- By end user, pharma and biotech firms held 53.17% share of the AI-based patient recruitment and retention market size in 2025, whereas contract research organizations are projected to grow at a 27.16% CAGR through 2031.

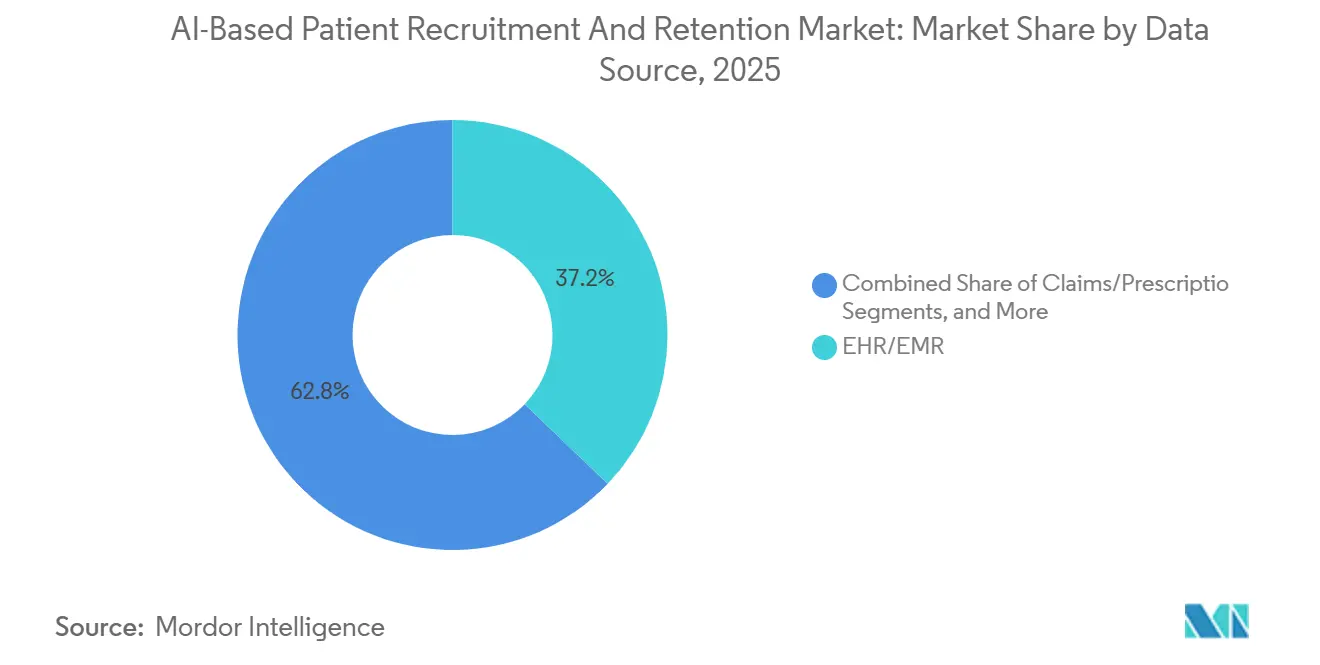

- By data source, electronic health records captured 37.17% of the AI-based patient recruitment and retention market size in 2025, and real-world data from wearables is projected to grow at a 28.33% CAGR to 2031.

- By trial phase, Phase III protocols commanded 42.18% share of the AI-based patient recruitment and retention market size in 2025, while Phase I adoption is projected to grow at a 27.91% CAGR.

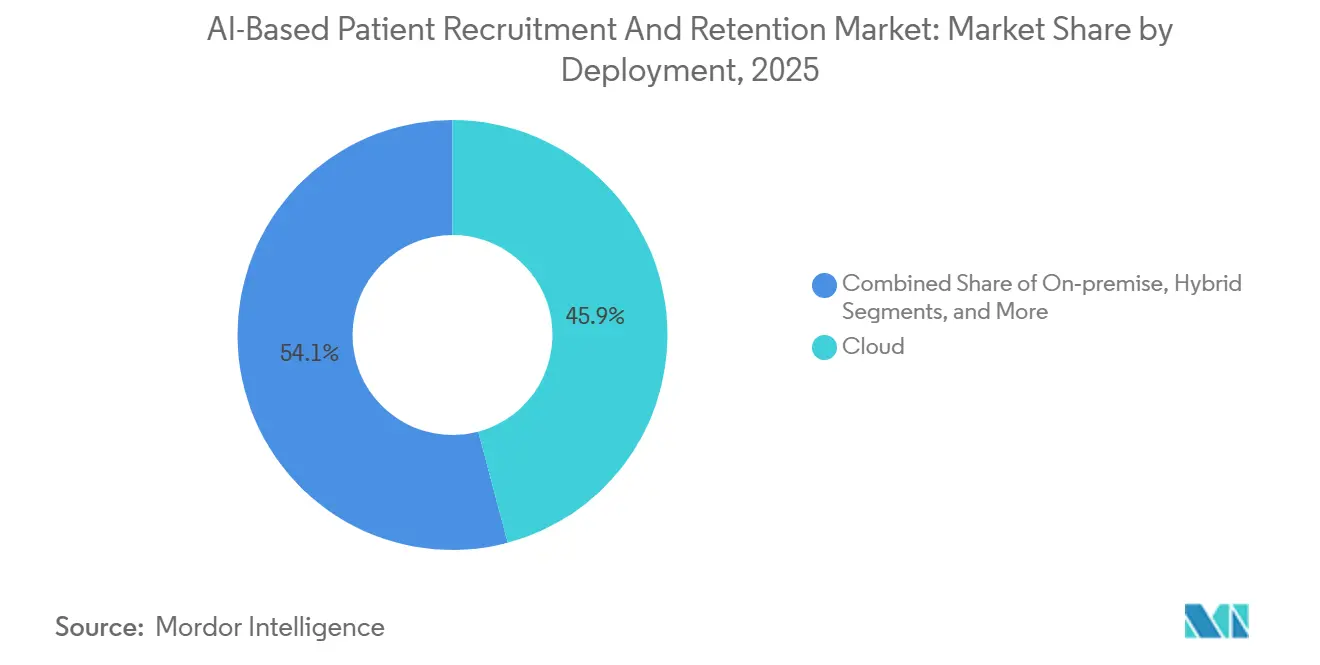

- By deployment, cloud-based tools accounted for 45.87% revenue in 2025, but on-premise installations are projected to rise at a 28.12% CAGR among academic centers.

- By geography, North America led with 45.12% share in 2025, and Asia-Pacific is the fastest-growing region at a 27.43% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI-Based Patient Recruitment And Retention Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Regulatory tailwinds for decentralized and hybrid trials enable digital recruitment and remote engagement | +4.5% | Global, early uptake in North America and EU | Medium term (2-4 years) |

| Diversity action plans drive inclusive enrollment and data-driven outreach to underrepresented groups | +3.8% | North America and EU, rising in APAC | Short term (≤ 2 years) |

| Interoperability mandates unlock EHR-driven patient-finding at scale | +5.2% | North America dominant, EU pilot regions | Medium term (2-4 years) |

| Rising protocol complexity and biomarker-driven eligibility intensify screening needs | +4.1% | Global oncology and rare-disease hubs | Long term (≥ 4 years) |

| Real-time claims alerts enable micro-cohort activation at care moments | +3.9% | North America and EU, emerging APAC cities | Medium term (2-4 years) |

| LLM-assisted prescreening of unstructured notes boosts match yield | +4.7% | Global, highest in U.S. academic centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Tailwinds For Decentralized And Hybrid Trials Enable Digital Recruitment And Remote Engagement

In January 2026, the FDA and the European Medicines Agency formally recognized the use of remote consent, telemedicine visits, and algorithmic eligibility checks, provided sponsors validate their models and maintain human oversight. This decision addresses concerns among sponsors regarding inconsistent review standards. The FDA's real-world evidence framework, introduced in December 2025, allows registry data to replace certain site visits, reducing the operational burden on traditional hubs.[1]U.S. Food and Drug Administration, “FDA Announces New Real-World Evidence Framework,” FDA Press Announcements, fda.gov In 2025, decentralized designs accounted for 28% of newly launched Phase III oncology protocols, a significant increase from 11% in 2022. The World Health Organization's GCP update in September 2024 standardized electronic consent and remote monitoring across its 194 member states.[2]World Health Organization, “Good Clinical Practice Update 2024,” who.int Source: ONC, “USCDI Version 7 Draft,” healthit.gov Sponsors using hybrid models report enrollment speeds that outperform traditional site-centric methods by up to 60%, particularly in geographically diverse areas such as Alzheimer’s disease.

Diversity Action Plans Drive Inclusive Enrollment And Data-Driven Outreach To Underrepresented Groups

The FDA's draft guidance from June 2024 requires late-stage trials to project enrollment demographics by race, ethnicity, age, and sex before IND approval. AI platforms are addressing this by stratifying EHR cohorts based on social health determinants and tailoring outreach to historically underrepresented groups.[3]U.S. Food and Drug Administration, “Decentralized Clinical Trials Guidance,” fda.gov In 2024, the World Health Organization introduced diversity benchmarks recommending that enrollment reflect disease epidemiology. A review of 47 oncology trials in 2025 showed that AI-driven outreach nearly doubled Black and Hispanic participation, increasing from 8% to 19%. Community organizations are collaborating to design consent materials, enhancing trust and improving response rates.[4]Rodriguez, M. et al., “Algorithmic Bias in AI Screening Tools,” Nature Medicine, nature.com Sponsors failing to meet diversity benchmarks have faced regulatory holds, elevating inclusive enrollment from a social objective to a compliance requirement.

Interoperability And Data Liquidity Unlock EHR-Driven Patient-Finding At Scale

By January 2026, TEFCA successfully connected 170 qualified health information networks, enabling federated queries across 500 million U.S. records without centralizing protected data. AI engines now deliver de-identified counts for complex phenotype queries within 48 hours. The latest USCDI version adds 23 new data elements, including social factors and genomic variants, which enhance the precision of algorithmic matches. Vendors like TriNetX have reduced site onboarding timelines from six months to six weeks by leveraging FHIR APIs. A 2025 study found that hospitals utilizing the full USCDI elements achieved a 42% improvement in AI-match accuracy compared to those relying on traditional data feeds.

Rising Protocol Complexity And Biomarker-Driven Eligibility Intensify Screening Needs

Current oncology protocols now include an average of 47 inclusion criteria, driven by companion diagnostics and multi-arm designs. Manual chart reviews often fail to identify rare biomarker combinations, slowing enrollment processes. In 2025, AI tools capable of analyzing unstructured pathology and imaging reports reduced screen-failure rates by 35% in cardiovascular trials. The FDA acknowledged computational prescreening as valid evidence in February 2025, provided validation is documented. By identifying mismatched referrals early, sponsors avoid unnecessary imaging costs ranging from USD 3,000 to 5,000 per candidate.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Heightened IRB and ethics scrutiny of AI recruiting | −1.8% | Global, strongest in EU and academic centers | Short term (≤ 2 years) |

| Data or algorithmic bias and model drift risk | −2.1% | Global, highest in diverse populations | Medium term (2-4 years) |

| Cross-border data flows and consent portability constraints | −1.5% | EU-U.S. corridors, emerging APAC routes | Long term (≥ 4 years) |

| Site IT heterogeneity and variable FHIR data quality hinder integrations | −1.9% | Global, acute in community hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI Recruiting Faces Increased Scrutiny from IRBs and Ethics Boards (Transparency, Consent, Bias)

Institutional review boards (IRBs) now require sponsors to disclose model training sources, feature weights, and decision thresholds before granting approvals. Columbia University’s 2024 framework emphasizes the inclusion of opt-out language and clear algorithm descriptions in patient outreach. In 2025, Advarra’s central IRB introduced model consent templates, which have extended AI study protocol timelines by an additional 8 to 12 weeks. A three-stage ethics audit proposed by Frontiers in Medicine has been widely adopted by academic centers, focusing on midpoint bias checks. However, smaller biotech companies face challenges with the extensive documentation requirements, slowing the adoption of AI in early-stage pipelines.

Data Or Algorithmic Bias And Model Drift Risk: False Matches And Inequities

A 2025 Nature Medicine paper showed screening tools trained on majority-white data missed 18% of eligible Black cardiovascular patients. False-positive alerts waste coordinator time and erode confidence. The open-source Bias Mitigation Fairness Toolkit offers re-weighting and post-processing methods, but adoption remains limited outside large hospitals. Regulators increasingly demand bias metrics; FDA diversity guidance now requests disparate impact ratios in enrollment reports. The EMA plans to add periodic re-validation requirements by late 2026, which may raise maintenance costs for vendors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution: Retention Tools Expand As Sponsors Focus On Dropout

In 2025, AI-based patient recruitment generated the majority of revenue, but increasing dropout costs are now redirecting budgets toward retention analytics. The market for AI-based patient recruitment and retention modules is expected to grow rapidly through 2031, driven by tools that can predict disengagement weeks before a missed visit. Medable’s Axon platform uses natural language processing on patient-reported outcomes to detect early warning signs, while Science 37 integrates data from wearables, adherence metrics, and daily surveys to create engagement scores. A study in 2025 demonstrated a 22% reduction in dropouts for cardiovascular trials due to AI-driven nudges, with the most significant impact on patients living more than 50 miles from study sites. Sponsors are increasingly attracted to integrated suites that combine recruitment and retention, offering the convenience of unified dashboards and single contracts.

By End User: CROs Embed AI To Win Master-Protocol Mandates

Contract research organizations (CROs) are embedding AI into design, site selection, and patient engagement to differentiate their services. Launched in 2026, IQVIA.ai coordinates 150 AI agents across protocol simulation, federated EHR queries, and engagement chatbots. This comprehensive capability positions CROs to secure master agreements in complex adaptive trials. While pharmaceutical and biotech companies remain the primary spenders, their internal teams increasingly demand CRO partners to provide validated AI solutions.

Site management organizations are also making significant investments. Elligo Health Research, for example, raised USD 135 million to enhance its model, which integrates AI prescreening with on-site staff for eligibility confirmation and consent acquisition. Meanwhile, patient foundations are leveraging their registry ownership to bypass traditional intermediaries.

By Data Source: Wearables And Real-World Data Accelerate Growth

Traditional electronic health records (EHRs) remain the primary data source, but their dominance is gradually declining. Wearables, combined with claims feeds, provide objective physiological insights alongside real-time care events, enabling sponsors to define specific micro-cohorts, such as those recently diagnosed with atrial fibrillation. The FDA’s clearance of atrial-fibrillation detection on wearable devices in 2024 has validated the use of continuous monitoring endpoints. Medidata’s Sensor Cloud now integrates data from multiple device manufacturers into its cohort queries, with sponsors reporting a 15-30% reduction in dropouts due to fewer in-person visits.

Claims data and pharmacy histories are critical for identifying subjects with prior medication experience, particularly in oncology populations resistant to treatments. With coverage extending to 330 million U.S. lives, Komodo Health’s Healthcare Map enables sponsors to match rare diseases, even with limited prevalence.

By Trial Phase: Early-Phase Complexity Drives AI Uptake

In 2025, Phase III protocols were the primary adopters of AI, benefiting from larger cohorts that justified the associated technology costs. However, first-in-human oncology studies and rare-disease trials are facing increasing biomarker complexities. Algorithms capable of interpreting pathology and genomic results have demonstrated significant time savings, with some studies reporting a 42% reduction in time-to-first-patient for oncology trials. Additionally, a 2025 analysis highlighted significant cost savings per Phase III cardiovascular study due to fewer screen failures. Phase IV safety programs are leveraging claims and pharmacy data to efficiently enroll post-marketing cohorts, reducing site visits when endpoints rely on routine care data.

By Deployment: On-Premise Gains Traction In Academic Systems

Cloud platforms continue to dominate due to their flexibility and managed security features. Sponsors managing multi-country programs benefit from avoiding the need to install servers in every jurisdiction. However, academic medical centers and hospitals with strict data-residency requirements are increasingly opting for on-premise solutions, despite their higher upfront costs. For example, Mount Sinai’s PRISM system operates entirely within hospital firewalls and has successfully matched thousands of patients without external data movement. Hybrid models that combine local data storage with cloud analytics are also gaining traction, particularly among integrated delivery networks overseeing multiple hospitals.

Geography Analysis

North America takes the lead in adoption, driven by interoperability mandates that ease data access. TEFCA's milestone in January 2026 connected 170 networks and 500 million patient records, facilitating near real-time eligibility checks across state lines. The FDA's real-world evidence framework reduces the need for physical site visits, encouraging sponsors to invest in digital recruitment platforms. Meanwhile, Canada benefits from province-wide EHR repositories that streamline trial enrollment nationwide. However, privacy laws require province-specific data-sharing agreements.

Asia-Pacific is experiencing the fastest growth. China's Clinical Trial Center registry includes 1,200 institutions. In India, the National Digital Health Mission links health IDs of 400 million citizens to trial matching engines. Leading hospital groups in Bangalore, Hyderabad, and Chennai are utilizing AI tools across 50 locations, accelerating enrollment cycles for both local and international studies. Japan and South Korea are advancing rapidly, supported by national EHR networks and agency roadmaps that promote AI in clinical development. However, data-localization laws create challenges for cross-border matching, prompting vendors to adopt federated analytics confined within national borders.

Europe benefits from collaborative principles established by the FDA and EMA, which define acceptable AI applications. However, GDPR consent rules and uncertainties surrounding Schrems II slow down widespread deployments across the region. To avoid cross-border data transfer issues, sponsors often limit AI matching to domestic data centers. While initiatives like the European Health Data Space pilot aim to enhance data liquidity, a fully connected landscape is unlikely before 2028. In South America, Brazil's ANVISA is driving decentralized trials, fostering experimentation, and the country's health-system datasets are supporting early AI initiatives.

Competitive Landscape

The AI-Based Patient Recruitment and Retention market remains fragmented. No single vendor accounts for more than 12% of the revenue, while the top 10 vendors collectively control approximately 55%, indicating moderate market concentration. Tempus AI’s 2025 acquisition of Deep 6 AI demonstrates vertical integration by combining a genomic analytics platform with an EHR-mining engine. TriNetX is testing a federated-learning model that trains algorithms without exporting data, a strategy likely to align with EU regulatory preferences. Smaller competitors, such as Mendel AI, utilize open-source language models to achieve similar accuracy at reduced costs.

Winning strategies in this market emphasize extensive data partnerships and compliance features that are easy to implement. Vendors providing built-in bias metrics address diversity requirements with minimal effort from sponsors. Real-time data updates command premium pricing, as sponsors prioritize avoiding outdated eligibility lists. Patient foundations and advocacy groups are becoming influential players by directly monetizing registries, compelling CROs to demonstrate value beyond basic matchmaking. Patent filings suggest ongoing advancements in federated analytics, bias detection, and low-code site integrations.

AI-Based Patient Recruitment And Retention Industry Leaders

IQVIA

Medidata Solutions, Inc.

Tempus AI, Inc.

Flatiron Health, Inc.

TriNetX, LLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: IQVIA launched IQVIA.ai, integrating more than 150 AI agents and 90 patents to cut Phase III enrollment timelines by as much as 50% .

- March 2026: Gainwell Technologies rolled out a Medicaid claims engine that flags new cardiovascular or diabetes events within 72 hours across 12 states.

- January 2026: The FDA and EMA released joint principles for AI-enabled trials that endorse remote consent, telemedicine visits, and algorithmic matching, provided validation is documented.

- January 2026: The Office of the National Coordinator for Health IT published USCDI version 7 draft, adding 23 new data elements, including genomics and patient-reported outcomes.

- December 2025: The FDA announced a real-world evidence framework that permits registry endpoints to substitute for site assessments in certain post-market studies.

Global AI-Based Patient Recruitment And Retention Market Report Scope

As per the scope of report, AI-based patient recruitment and retention is the use of artificial intelligence including machine learning (ML), natural language processing (NLP), and predictive analytics to automate, speed up, and improve how participants are identified, screened, enrolled, and kept in clinical trials.

The AI-based patient recruitment and retention market is segmented by solution, end-user, data source, trial type/phase, deployment, and geography. By solution, the market includes AI-driven patient recruitment, AI-driven patient retention, and integrated platforms. By end-user, the market is segmented into pharmaceutical/biotech sponsors, contract research organizations (CROs), sites/site management organizations (SMOs), and patient advocacy groups/registries. By data source, the market is categorized into electronic health records/electronic medical records (EHR/EMR), claims and prescriptions, real-world data and wearables, genomic data, and social and community data. By trial type/phase, the market is segmented into Phase I trials, Phase II trials, Phase III trials, and Phase IV trials. By deployment, the market includes cloud-based, on-premise solutions, and hybrid approaches. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| AI-based Patient Recruitment |

| AI-based Patient Retention |

| Integrated Platforms |

| Pharma/Biotech Sponsors |

| CROs |

| Sites/SMOs |

| Patient Advocacy/Registries |

| EHR/EMR |

| Claims/Prescription |

| Real-world/Wearables |

| Genomics |

| Social/Community |

| Phase I |

| Phase II |

| Phase III |

| Phase IV |

| Cloud |

| On-premise |

| Hybrid |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Solution | AI-based Patient Recruitment | |

| AI-based Patient Retention | ||

| Integrated Platforms | ||

| By End User | Pharma/Biotech Sponsors | |

| CROs | ||

| Sites/SMOs | ||

| Patient Advocacy/Registries | ||

| By Data Source | EHR/EMR | |

| Claims/Prescription | ||

| Real-world/Wearables | ||

| Genomics | ||

| Social/Community | ||

| By Trial Type/Phase | Phase I | |

| Phase II | ||

| Phase III | ||

| Phase IV | ||

| By Deployment | Cloud | |

| On-premise | ||

| Hybrid | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the AI-Based Patient Recruitment and Retention market today?

The AI-Based Patient Recruitment and Retention market size is USD 1.07 billion in 2026 and is projected to reach USD 3.36 billion by 2031.

What drives double-digit growth in AI recruitment tools?

Regulatory acceptance of decentralized trials, nationwide interoperability under TEFCA, and lower costs for large language model prescreening collectively lift demand.

Which region shows the fastest future expansion?

Asia-Pacific is forecast to grow at a 27.43% CAGR through 2031 as China and India scale national health data networks.

Why are sponsors investing in retention analytics?

A 15-30% drop in participant attrition can save up to USD 8 million per day in late-stage oncology programs, making AI-based retention tools attractive.

How concentrated is vendor competition?

The top 10 firms account for roughly 55% of global revenue, suggesting moderate consolidation without a dominant supplier.

Which data sources are gaining share beyond electronic health records?

Wearable streams and claims data are expanding fastest, helped by recent FDA clearances for continuous monitoring devices.

Page last updated on: