AI Medical Diagnosis App Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

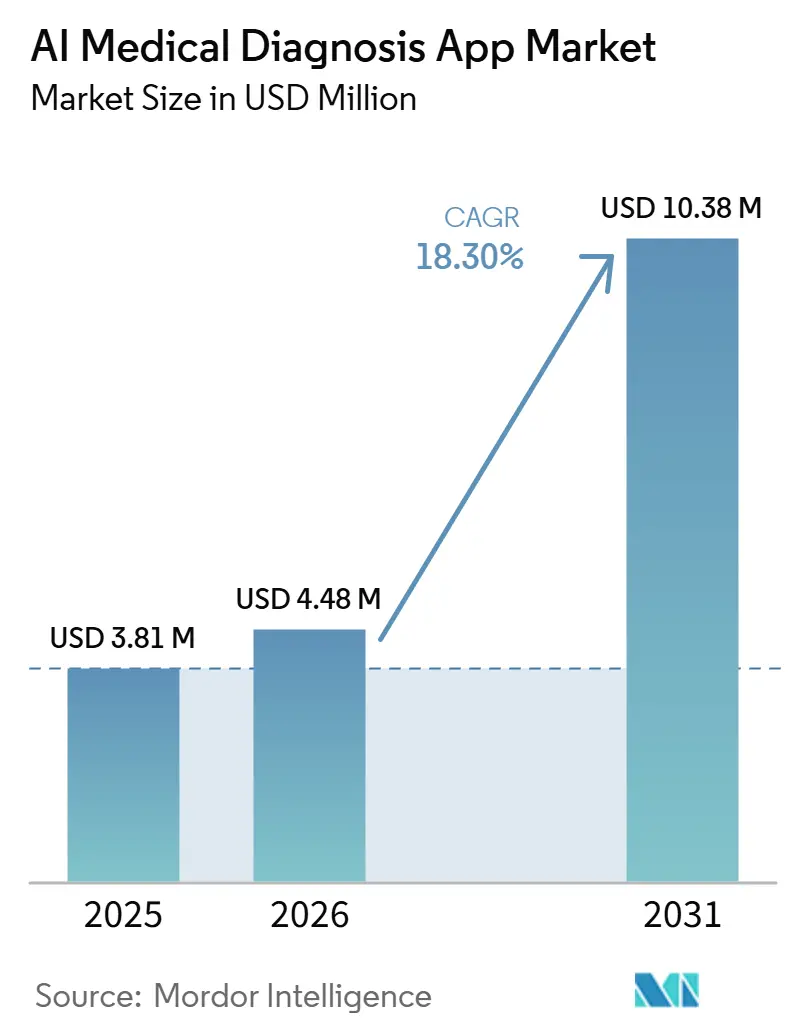

| Market Size (2026) | USD 4.48 Million |

| Market Size (2031) | USD 10.38 Million |

| Growth Rate (2026 - 2031) | 18.30% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Medical Diagnosis App Market Analysis by Mordor Intelligence

The AI Medical Diagnosis App Market size is expected to grow from USD 3.81 million in 2025 to USD 4.48 million in 2026 and is forecast to reach USD 10.38 million by 2031 at 18.30% CAGR over 2026-2031.

The AI medical diagnosis app market is expanding because health systems need faster diagnostic throughput, better screening coverage, and lower per-patient operating pressure without losing clinical accuracy. The AI medical diagnosis app market is also moving beyond single-use tools as vendors now combine imaging, laboratory data, genomics, and patient history into broader clinical software environments that are harder to replace once deployed. Regulatory pressure is shaping competition as vendors with stronger FDA, EU, and country-level compliance capabilities are better placed to win enterprise contracts across regions. Cloud and hybrid deployment models are gaining traction because providers want continuous model updates and lower upfront spending while still managing data governance requirements across jurisdictions. Competitive positioning in the AI medical diagnosis app market is therefore shifting toward vendors that can pair regulatory breadth, workflow integration, and real-world validation with a business model that scales across hospital networks and diagnostic platforms.

Key Report Takeaways

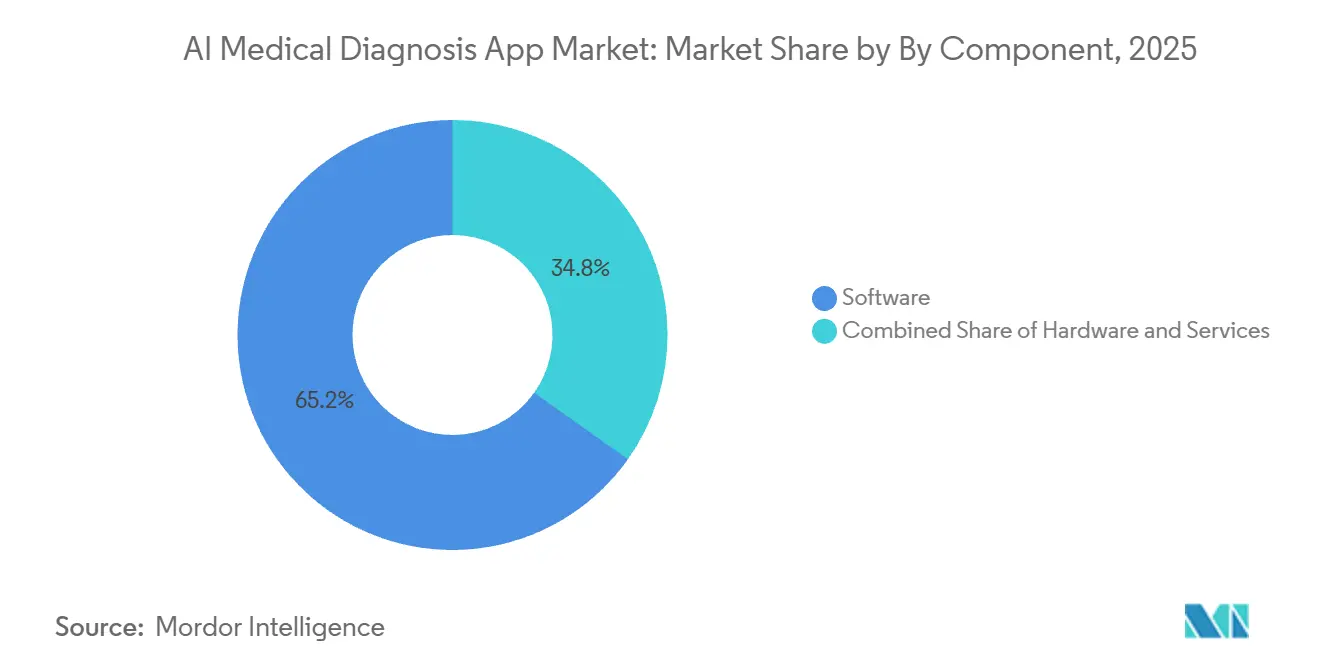

By component, software held 65.2% share in 2025, and software also records the fastest CAGR of 18.8% through 2031 in the AI medical diagnosis app market.

By application, in vivo diagnostics accounted for 63.8% share of the AI medical diagnosis app market size in 2025, while in vitro diagnostics is projected to expand at a 5.2% CAGR through 2031.

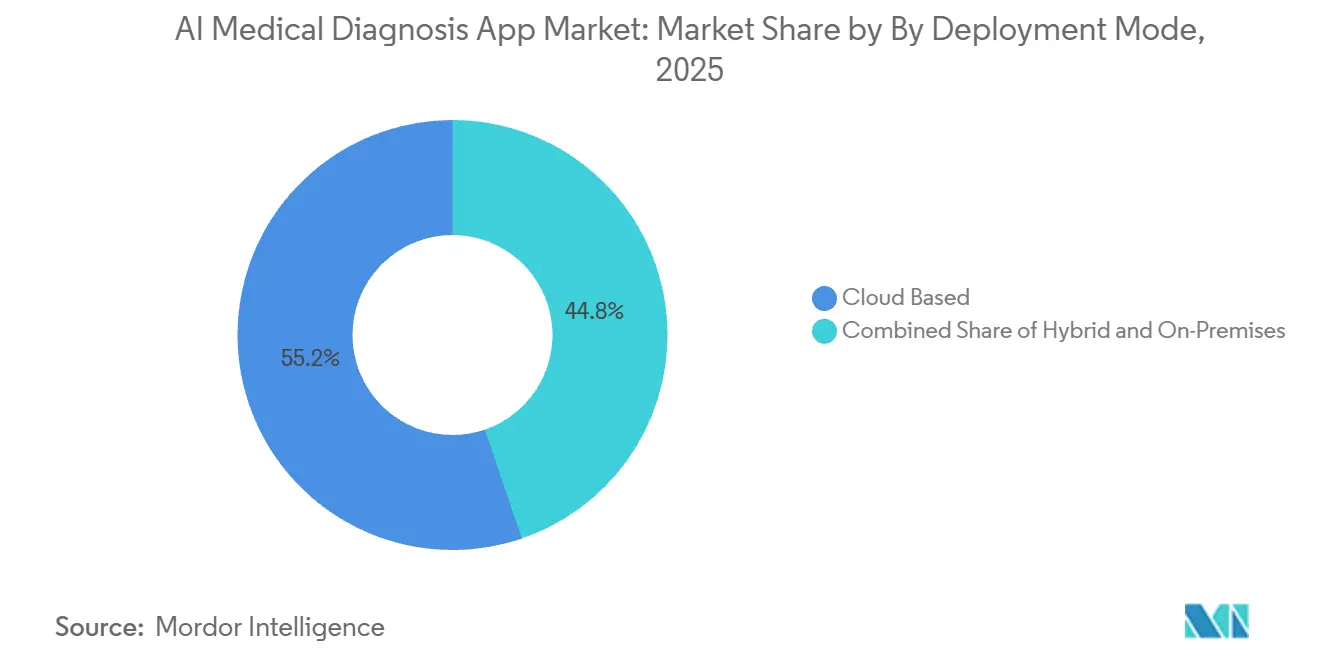

By deployment mode, cloud-based deployment held 55.2% share in 2025, and it also posts the highest CAGR of 18.9% through 2031 in the AI medical diagnosis app market.

By end user, hospitals represented 41.4% share in 2025, while diagnostic laboratories record the fastest projected CAGR at 18.5% through 2031 in the AI medical diagnosis app market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Medical Diagnosis App Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Faster Triage And Early Disease Detection | +3.5% | Global, with highest intensity in North America and Western Europe | Short term (≤ 2 years) |

| Expansion Of AI-Enabled Radiology And Pathology Workflow | +3.0% | North America, Europe, with spillover to Asia Pacific | Medium term (2-4 years) |

| Multi-Modal Clinical Data Convergence Improves Diagnostic Precision | +2.8% | North America, Europe, and early-stage Asia Pacific | Medium term (2-4 years) |

| Provider Push Toward Workflow Automation In Overloaded Systems | +2.5% | Global, with strong pressure in the UK, India, and Sub-Saharan Africa | Short term (≤ 2 years) to Medium term (2-4 years) |

| Integration With Wearables And Remote Monitoring Extends Diagnostic Reach | +2.0% | North America, Asia Pacific, and Western Europe | Medium term (2-4 years) to Long term (≥ 4 years) |

| Growing Investment In Clinical Validation And Interoperability | +1.5% | North America, the EU, and emerging Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Faster Triage and Early Disease Detection

The AI medical diagnosis app market is benefiting from hospital demand for faster reading, earlier flagging, and better front-end prioritization in overloaded imaging workflows. Aidoc received FDA Breakthrough Device Designation in June 2026 for First Read, an autonomous tool that generates preliminary chest radiograph reports, which shows that AI medical diagnosis app market adoption is moving beyond alerting into direct reporting support[1]Aidoc, “First Read and CARE Triage Updates,” Aidoc. . A 2026 study in BMC Medical Imaging found that an AI-integrated structured reporting tool for coronary CT angiography reduced reporting time by 40.2% and improved inter-reader agreement from 45.3% to 94.6%, which supports faster output without weakening consistency [2]BMC Medical Imaging, “AI-Integrated Structured Reporting Tool for Coronary CT Angiography.. Hospitals facing staffing shortages are therefore more willing to evaluate systems that shorten turnaround time and help clinicians focus on urgent cases first. This pattern is helping the AI medical diagnosis app market move toward use cases where time savings and operational relief are visible at the department level soon after deployment.

Expansion of AI-Enabled Radiology and Pathology Workflow

The AI medical diagnosis app market continues to build on radiology because imaging remains the most mature clinical area for regulatory clearances, deployment experience, and dataset availability. Siemens Healthineers and Mayo Clinic expanded their collaboration in February 2026 to develop AI-enabled MRI protocols for neurodegenerative disease, prostate cancer, and metastatic liver tumor management, which shows how vendors are embedding AI inside imaging workflows rather than selling it as a separate layer. GE HealthCare’s Photonova Spectra photon-counting CT received FDA 510(k) clearance in March 2026 and integrates NVIDIA accelerated computing that handles up to 50 times more data than conventional CT, which strengthens routine AI-based quantitative analysis in daily imaging practice. In pathology, vendors such as Paige and Ibex are pushing tissue AI into clinical workflows, which is expanding the AI medical diagnosis app market beyond radiology and into diagnostic processes with high review volume and clear automation needs. As AI becomes part of scanner protocols and diagnostic systems, buyers face deeper vendor dependence over multiyear equipment cycles, and that raises switching barriers in the AI medical diagnosis app market.

Multi-Modal Clinical Data Convergence Improves Diagnostic Precision

The AI medical diagnosis app market is shifting from single-modality tools toward platforms that combine imaging, laboratory results, genomics, text records, and time-series data in one clinical workflow. A 2026 Nature Medicine study evaluating Google DeepMind’s AMIE reported that multimodal conversational AI matched or exceeded specialist physicians in management reasoning across text, images, ECG tracings, and clinical documents, which supports broader platform design in the AI medical diagnosis app market. The CLIMB dataset included 4.5 million patient samples and showed up to 29% improvement in ultrasound analysis and 23% improvement in ECG analysis over single-task approaches, which gives procurement teams a clearer reason to prioritize vendors with broader data integration strategies. Google released MedGemma 1.5 in 2026 alongside MedASR, extending medical image interpretation and medical speech-to-text support across more modalities. HL7 FHIR and DICOM are becoming baseline requirements for deployment, so vendors with native standards support are better placed as the AI medical diagnosis app market moves toward multimodal clinical environments

Provider Push Toward Workflow Automation in Overloaded Systems

The AI medical diagnosis app market is gaining support from providers that need workflow automation across radiology, mammography, and laboratory operations where staff shortages have become persistent rather than temporary. GE HealthCare expanded its collaboration with RadNet’s DeepHealth subsidiary in April 2026 to advance AI-powered breast cancer screening and automated density classification, which targets one of the highest-volume imaging use cases in routine care. Siemens Healthineers adopted NVIDIA MONAI Deploy at RSNA 2025 to accelerate AI workflow integration into syngo Carbon and syngo.via, which points to growing demand for deployment frameworks that lower integration friction inside hospital systems. The Royal College of Radiologists reported in its 2026 census that AI remained underused for administrative tasks with strong workload reduction potential, which leaves room for the AI medical diagnosis app market to expand into scheduling, reporting support, and worklist management. The FDA’s June 2026 classification framework under 21 CFR 892.2055 gives hospitals clearer regulatory footing when evaluating radiological machine learning software, and that reduces one barrier to procurement in the AI medical diagnosis app market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithm Explainability And Liability Concerns Slow Clinical Adoption | -1.5% | Global, with the strongest effect in the US, the EU, and the UK | Short term (≤ 2 years) to Medium term (2-4 years) |

| High Integration Cost Across PACS, EHR, And Hospital Systems | -1.8% | Global, with disproportionate effect in markets with legacy infrastructure | Short term (≤ 2 years) |

| Data Privacy, Sovereignty, And Cross-Border Model Deployment Friction | -1.2% | The EU, the US, China, Asia Pacific, and global multi-jurisdictional deployments | Medium term (2-4 years) to Long term (≥ 4 years) |

| Regulatory Heterogeneity And Revalidation Burden For AI Models Across Markets | -1.0% | Global, with the highest burden for vendors pursuing FDA, CE, NMPA, and PMDA approvals | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Algorithm Explainability and Liability Concerns Slow Clinical Adoption

The AI medical diagnosis app market is advancing faster than the governance systems that decide accountability when an algorithm influences a clinical decision . A JAMA Network Open [3]Source: JAMA Network Open, “FDA-Authorized AI-Enabled Medical Devices Review,” JAMA Network Open. study reviewing FDA-authorized AI-enabled medical devices noted that all implantable AI devices in its sample cleared through the 510(k) pathway, which raises questions around the depth of clinical evidence and legal responsibility when errors occur. The EU AI Act classifies many medical diagnostic applications as high-risk systems, and the phased compliance burden will require stronger post-market monitoring, human oversight, and transparency processes from vendors. A 2026 review available through PMC also noted that continuous learning models create accountability gaps because post-deployment updates do not fit neatly into older surveillance structures. As a result, enterprise buying cycles in the AI medical diagnosis app market can lengthen when legal, ethics, and compliance teams want stronger proof of model behavior, update control, and failure response.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Leads in Revenue and Growth

Software held 65.2% of AI medical diagnosis app market share in 2025, and it is also projected to grow at an 18.8% CAGR through 2031. This lead reflects the economics of licensing and subscription models, where incremental distribution is easier than for hardware-heavy systems in the AI medical diagnosis app market. Google released MedGemma 1.5 in 2026[4]Google DeepMind, “MedGemma 1.5 and Health AI Research Updates,” Google DeepMind., and NVIDIA expanded medical imaging support through NIM microservices, which helps software vendors shorten the path from model development to deployable products. As a result, software remains the clearest scale engine inside the AI medical diagnosis app industry because it combines regulatory reuse, update flexibility, and recurring revenue potential.

Hardware still matters because AI-enabled scanners and accelerated edge systems raise the quality and speed of inference during routine use. GE HealthCare’s Photonova Spectra shows this role clearly because the system supports GPU-based reconstruction and high-volume data handling at the imaging layer. Services form the third component block, and this part of the AI medical diagnosis app market will stay relevant as providers need validation, implementation, monitoring, and compliance support after deployment. Regulatory demands in China and Europe are also increasing the need for lifecycle management and post-market oversight, which supports a steady services opportunity across the AI medical diagnosis app industry.

By Application: Imaging Holds the Base While In Vitro Uses Expand

In vivo diagnostics represented 63.8% share of the AI medical diagnosis app market size in 2025, which keeps imaging at the center of current commercial demand. Radiology reached adoption earlier than most specialties because it had clearer regulatory precedents, large labeled datasets, and stronger workflow fit for automation in the AI medical diagnosis app market. Qure.ai had 26 FDA-cleared indications across 9 products by February 2026, which shows how regulatory depth in imaging can support broad deployment across screening and hospital settings. This keeps in vivo diagnostics ahead on installed use, customer familiarity, and near-term revenue capture.

In vitro diagnostics is smaller today, but it is projected to grow at a 5.2% CAGR through 2031 as machine learning expands into immunoassay, molecular diagnostics, and digital pathology workflows. The draft notes that AI-enabled microfluidic platforms can support self-correcting lab-on-chip systems that compare outputs to training data in real time, which strengthens automation at the point of care. Roche’s planned acquisition of PathAI also shows that large diagnostics companies now view AI pathology and image management as core assets rather than optional extensions. Over time, the AI medical diagnosis app market should see a more balanced application mix as laboratory automation and pathology software move closer to imaging in commercial relevance.

By Deployment Mode: Cloud Stays Ahead While Hybrid Gains Strategic Weight

Cloud-based deployment accounted for 55.2% share of the AI medical diagnosis app market size in 2025, and it is also projected to grow at an 18.9% CAGR through 2031 M. Providers prefer this model because it reduces upfront infrastructure spending and allows vendors to deliver updates without repeated local installation work. This gives the AI medical diagnosis app market a clear subscription-oriented direction, especially in hospital groups that want faster implementation across multiple sites. Cloud leadership also fits the broader move toward enterprise AI platforms rather than isolated point solutions.

Hybrid deployment is gaining importance because many providers want cloud-based training and storage with local or edge inference for sensitive clinical decisions. The AI medical diagnosis app market is seeing more interest in this model as HIPAA, GDPR, the EU AI Act, and national privacy rules make cross-border data routing more difficult. On-premises systems remain relevant in markets with localization requirements and in institutions managing sensitive research data, even if their adoption pace is slower than the cloud. Vendors that can offer modular cloud-plus-edge options are therefore better positioned than pure-cloud vendors in the next phase of the AI medical diagnosis app market.

By End User: Hospitals Anchor Demand While Laboratories Accelerate

Hospitals held 41.4% share in 2025, which makes them the largest end-user group in the AI medical diagnosis app market. Their lead reflects their role as the main buyers of enterprise clinical platforms, imaging systems, and broader diagnostic infrastructure MO. Aidoc reported deployment across nearly 2,000 hospitals and analysis of more than 120 million patient cases by mid-2026, which illustrates the scale that hospital-based adoption can reach when one platform spans multiple diagnostic workflows. Hospitals will therefore remain central to large contract value, multi-department integration, and clinical validation in the AI medical diagnosis app market.

Diagnostic laboratories are the fastest-growing end-user group with an 18.5% CAGR through 2031, supported by AI use in molecular, genomic, and pathology workflows. This growth matters because laboratory settings can translate faster turnaround and lower error rates into measurable contract value with payers and provider networks. Diagnostic imaging centers also benefit from high-throughput use cases, while clinics and other healthcare providers remain a later opportunity as lighter triage and symptom-based tools mature. That mix gives the AI medical diagnosis app market both a stable hospital base and a faster-growth laboratory channel over the forecast period.

Geography Analysis

North America held 55.1% of AI medical diagnosis app market share in 2025, which keeps it as the largest regional block in the AI medical diagnosis app market. This position is supported by a strong FDA clearance environment, high IT readiness, and provider budgets that can absorb enterprise-scale software deployment. Aidoc received FDA Breakthrough Device Designation for First Read in June 2026, and that kind of regulatory acceleration supports faster commercialization for vendors addressing urgent clinical workflows. Private capital also remains active in the region, as Aidoc raised USD 150 million in April 2026, which signals continued investor confidence in near-term clinical AI monetization in the AI medical diagnosis app market.

Europe has a different profile because growth is tied closely to compliance readiness, hospital digitization, and system-level procurement rules in the AI medical diagnosis app market. The EU AI Act and GDPR create a stricter operating environment for health data and high-risk software, which tends to favor vendors with established filings and stronger documentation capacity. The UK’s NHS has also shown that AI can reduce mammography screening workloads, and this keeps imaging use cases prominent in regional procurement discussions. Germany remains important because of its medical technology base and hospital purchasing depth, while France, Italy, and Spain offer expansion potential as digitization programs support EHR and PACS modernization.

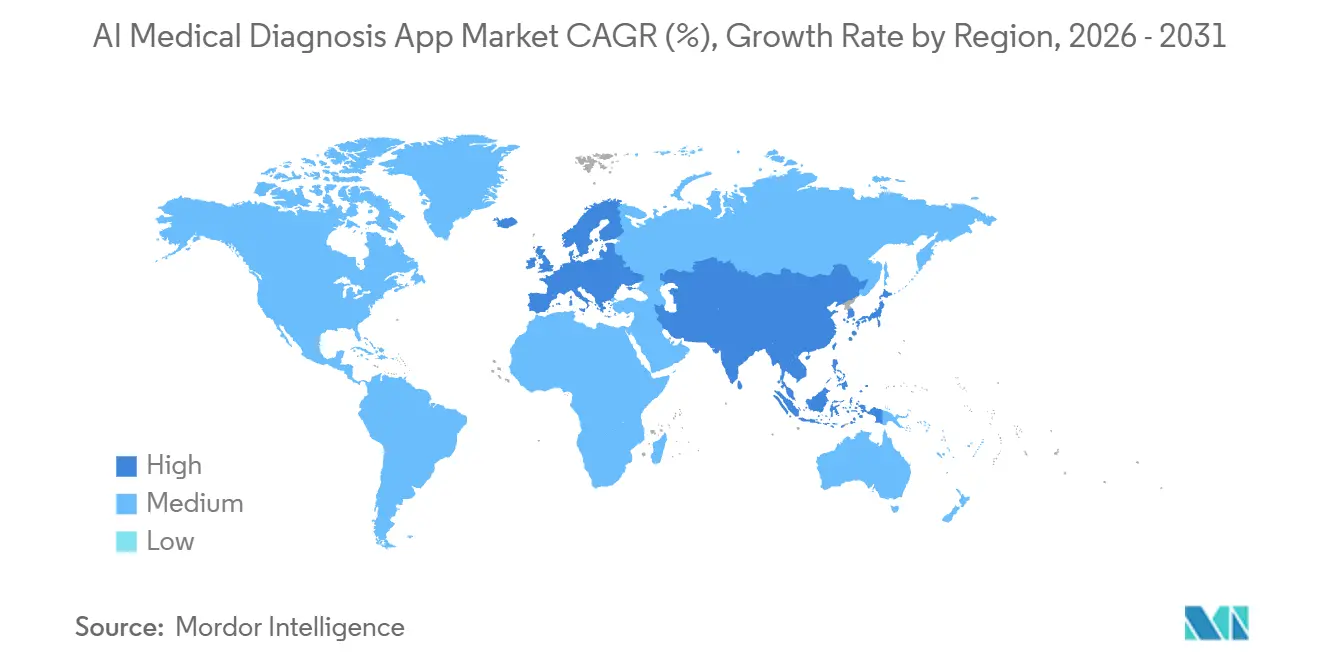

Asia Pacific is projected to record the fastest CAGR at 19.2% through 2031 in the AI medical diagnosis app market. The region is benefiting from policy support, domestic AI vendors, and large unmet diagnostic demand across both advanced and emerging healthcare systems. South Korea reported 157 medical AI approvals in 2025 and issued the first clearance of a generative AI medical device in April 2026, which shows an active regulatory environment for newer software categories. Japan is also updating SaMD guidance, while India and Southeast Asia are expanding deployment in under-resourced settings through models tied to portable imaging and public health programs. The Middle East and Africa are growing from a smaller base through smart hospital investment and public partnerships, while South America is being supported by hospital group consolidation and broader private insurance reach.

Competitive Landscape

The AI medical diagnosis app market is moderately concentrated at the platform level, but it remains fragmented across clinical specialties, imaging indications, and laboratory use cases. Alphabet, Microsoft, and NVIDIA mainly support the AI medical diagnosis app market as infrastructure providers through foundation models, compute, and acceleration hardware rather than as direct clinical application leaders. Domain-specific competitors such as Aidoc, Qure.ai, Lunit, Siemens Healthineers, GE HealthCare, Paige, and Ibex compete more directly on regulatory clearances, workflow depth, and clinical validation. This means share gains in the AI medical diagnosis app market depend less on general AI branding and more on evidence, interoperability, and embedded workflow value.

Aidoc and Qure.ai illustrate this pattern because both companies have built wide regulatory portfolios that create barriers for newer entrants. Aidoc had more than 31 FDA clearances and Qure.ai had 26 cleared indications across 9 products in the draft, which supports the importance of breadth in high-volume clinical pathways. Roche’s agreement in May 2026 to acquire PathAI for USD 750 million upfront plus up to USD 300 million in milestones shows that established diagnostics groups now prefer buying mature AI assets rather than building from scratch . The AI medical diagnosis app market is therefore seeing consolidation where larger diagnostic and medtech players use M&A to close capability gaps quickly.

Strategic partnerships also matter because they help vendors insert AI deeper into clinical systems that hospitals already use. Siemens Healthineers expanded its Mayo Clinic collaboration in February 2026, and GE HealthCare expanded its DeepHealth mammography collaboration in April 2026, which shows how established medtech firms are tying AI development to installed clinical workflows. NVIDIA’s MONAI Deploy and similar frameworks are also becoming competitive tools because they reduce deployment friction and support regulated update pathways. Newer challengers are attracting capital in oncology, pathology, and multi-cancer detection, but the AI medical diagnosis app market still rewards companies that can prove real-world performance at enterprise scale. As foundational models become easier to access, differentiation in the AI medical diagnosis app market will depend more on regulated workflows, installed partnerships, and clinical outcomes than on model novelty alone.

AI Medical Diagnosis App Industry Leaders

Ada Health GmbH

PathAI, Inc.

Aidoc Medical Ltd.

Qure.ai Technologies Private Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Aidoc received FDA Breakthrough Device Designation for First Read, an AI that analyses chest radiographs and autonomously generates preliminary radiology reports. The designation, Aidoc's second in under a year, following CARE Triage in September 2025, signals regulatory confidence in autonomous reporting AI and opens a new revenue category beyond triage notification tools.

- June 2026: GRAIL, Inc. completed a USD 110 million equity financing with Samsung affiliates, including Samsung C&T Corporation, at USD 70.1 per share. The investment supports GRAIL's international expansion of its multi-cancer early detection platform and marks Samsung's long-term commitment to oncology diagnostics.

- May 2026: Roche entered a definitive merger agreement to acquire PathAI for USD 750 million upfront and up to USD 300 million in milestone payments. The deal will integrate PathAI's Image Management System and AI pathology algorithms into Roche's Diagnostics division, accelerating companion diagnostic development and clinical therapy decision-making.

- April 2026: Aidoc raised USD 150 million in Series E funding led by Goldman Sachs Alternatives, with participation from General Catalyst, SoftBank Vision Fund 2, and NVentures, NVIDIA's venture arm. Total funding exceeds USD 500 million, proceeds fund expansion of the CARE clinical foundation model and the aiOS enterprise platform across nearly 2,000 hospitals.

Global AI Medical Diagnosis App Market Report Scope

| Software |

| Hardware |

| Services |

| In Vivo Diagnostics |

| In Vitro Diagnostics |

| Cloud Based |

| Hybrid |

| On Premises |

| Hospitals |

| Diagnostic Imaging Centers |

| Diagnostic Laboratories |

| Clinics and Other Healthcare Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| United States | |

| Canada | |

| Mexico | |

| Germany | |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Hardware | ||

| Services | ||

| By Application | In Vivo Diagnostics | |

| In Vitro Diagnostics | ||

| By Deployment Mode | Cloud Based | |

| Hybrid | ||

| On Premises | ||

| By Tend User | Hospitals | |

| Diagnostic Imaging Centers | ||

| Diagnostic Laboratories | ||

| Clinics and Other Healthcare Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| United States | ||

| Canada | ||

| Mexico | ||

| Germany | ||

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2026 value of the AI medical diagnosis app market?

The AI medical diagnosis app market stands at USD 4.5 billion in 2026 and is forecast to reach USD 10.4 billion by 2031 at an 18.3% CAGR.

Which component leads revenue in AI medical diagnosis apps?

Software leads with 65.2% share in 2025 and is also the fastest-growing component at an 18.8% CAGR through 2031.

Why are hospitals adopting AI medical diagnosis apps faster now?

Hospitals want faster triage, lower reporting burden, and smoother workflow automation, especially in imaging and high-volume diagnostic settings.

Which deployment model is growing the fastest?

Cloud-based deployment leads with 55.2% share in 2025 and also posts the fastest CAGR at 18.9% through 2031.

Which region is growing the fastest for AI medical diagnosis apps?

Asia Pacific records the fastest regional CAGR at 19.2% through 2031, supported by policy action, local vendors, and unmet diagnostic demand.

What is the main risk slowing commercial rollout?

Explainability, liability, privacy rules, and integration cost remain the main barriers because they can delay procurement and raise implementation complexity.

Page last updated on: