AI In Enterprise Healthcare Platforms Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

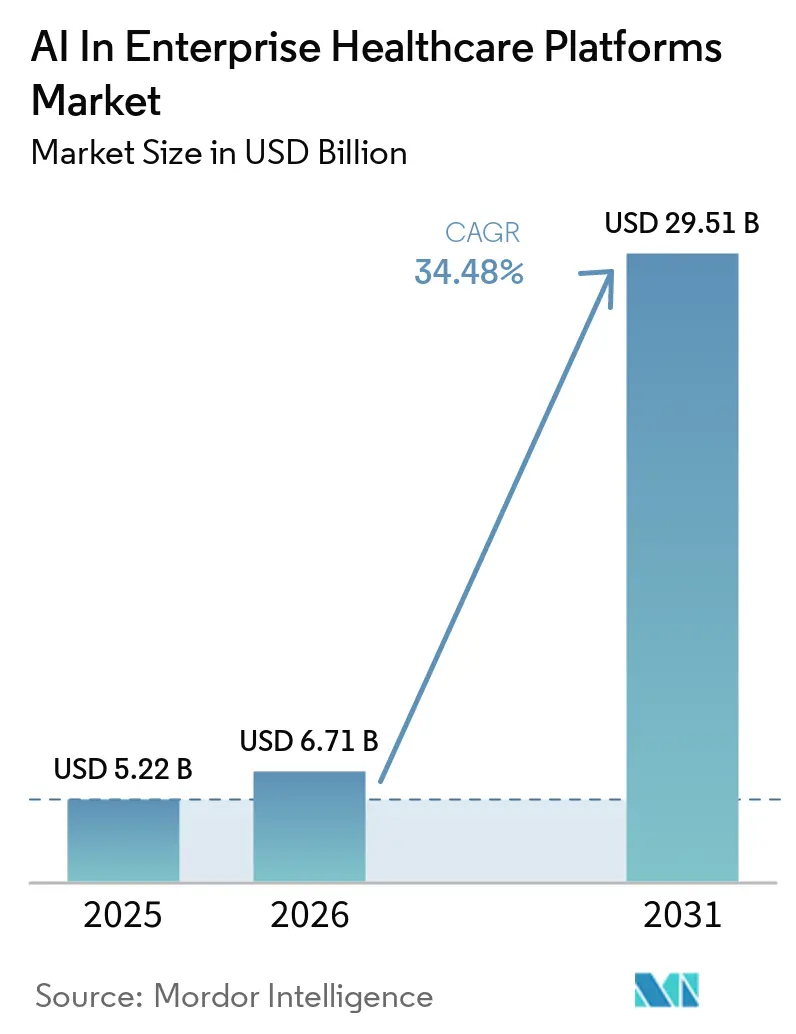

| Market Size (2026) | USD 6.71 Billion |

| Market Size (2031) | USD 29.51 Billion |

| Growth Rate (2026 - 2031) | 34.48% CAGR |

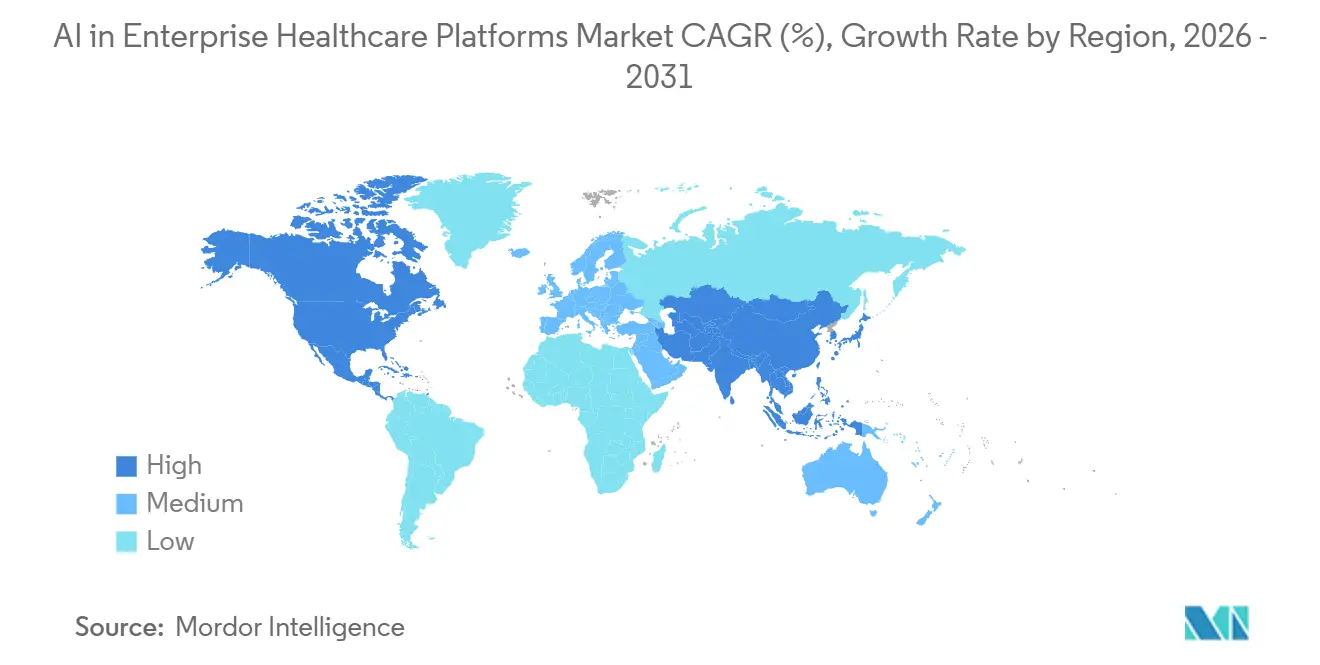

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Enterprise Healthcare Platforms Market Analysis by Mordor Intelligence

The AI in Enterprise Healthcare Platforms market size reached USD 5.22 billion in 2025 and is projected to reach USD 29.51 billion by 2031, advancing at a CAGR of 34.48% over 2026-2031. Health systems are shifting from point solutions to unified platforms to reduce integration debt, streamline governance, and remove workflow friction created by fragmented deployments. Regulatory clarity for AI-enabled devices has reduced uncertainty for product teams and clinical buyers, which supports faster deployment decisions at enterprise scale. EHR incumbents are accelerating embedded AI adoption through native capabilities that ride on their installed bases and access to longitudinal records, giving them a distribution advantage for ambient documentation and agentic assistants. Cloud-native data and AI services now provide the FHIR, governance, and inference primitives that make two to four-week deployments practical for best-in-class platforms, which encourages standardized adoption patterns across large provider and payer enterprises. Ambient and conversational AI remain top-of-mind for executives because they directly relieve clinician burden while forming a gateway to broader enterprise automation programs across care delivery and revenue cycle.

Key Report Takeaways

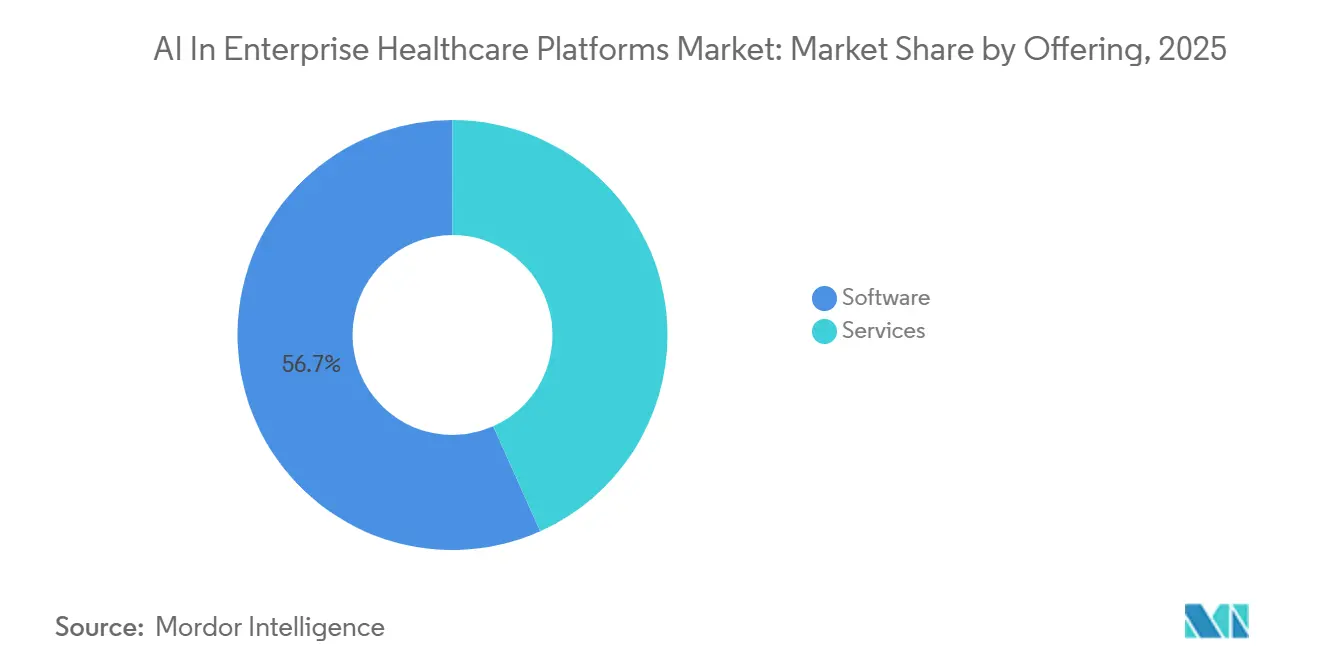

- By offering, software held 56.72% share in 2025 and is forecast to grow at 39.34% CAGR through 2031, while services expand to address governance and implementation needs.

- By application, medical imaging and diagnostics platforms led with 47.43% share in 2025, while revenue cycle and coding automation are projected to grow at 37.65% CAGR through 2031.

- By deployment, cloud led with 53.35% share in 2025, while hybrid/edge is set to expand at 39.67% CAGR on latency and data-residency needs.

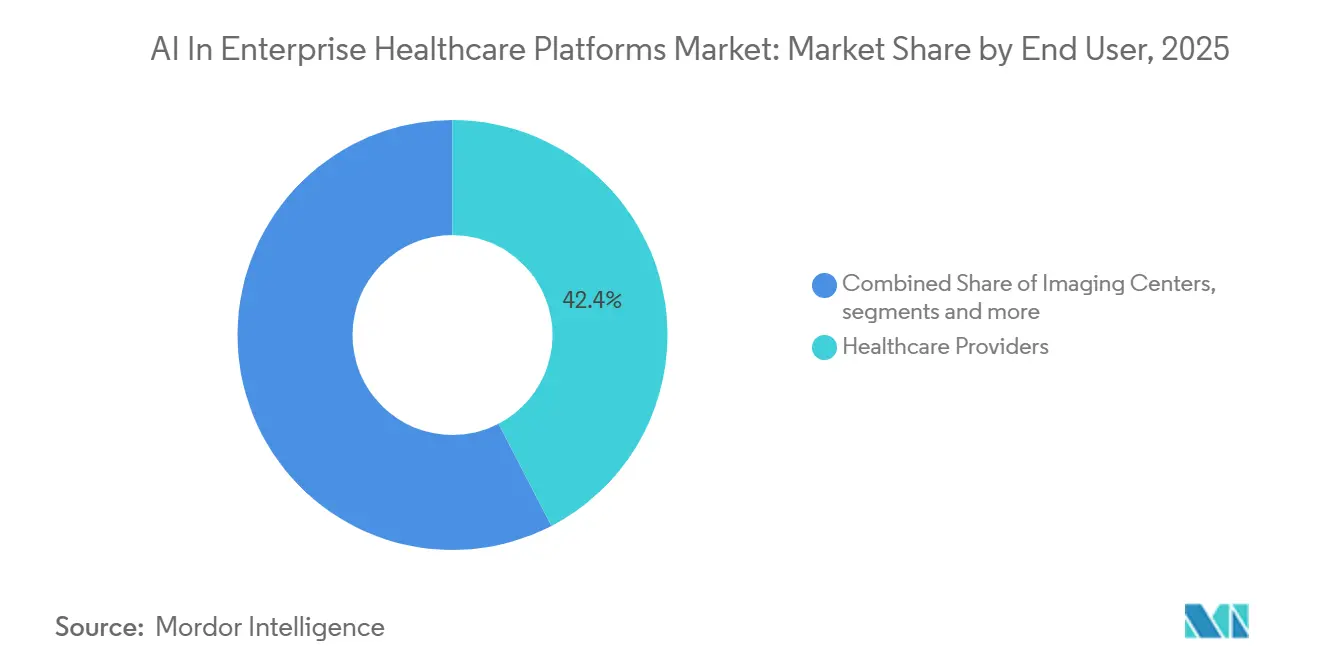

- By end user, healthcare providers accounted for 42.39% of spend in 2025, while healthcare payers are the fastest-growing at 36.88% CAGR through 2031.

- By AI technology, machine learning and deep learning held 48.27% share in 2025, while natural language processing and speech/ASR are advancing at 39.43% CAGR.

- By geography, North America led with 46.34% share in 2025, while Asia-Pacific is projected to record the fastest growth at 39.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Enterprise Healthcare Platforms Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud/SaaS shift enabling rapid AI deployment | +8.2% | Global, early in North America and Western Europe, accelerating in Asia-Pacific via sovereign cloud initiatives | Medium term (2-4 years) |

| Ambient clinical AI reduces documentation burden and unlocks ROI | +7.5% | North America leads with Epic hospital adoption, expanding in EU and APAC with multilingual models | Short term (≤ 2 years) |

| EHR incumbents’ distribution moats accelerate embedded AI uptake | +6.1% | North America primary, Europe via regional EHR vendors | Medium term (2-4 years) |

| Value-based and revenue-cycle pressures push automation platform buys | +5.8% | United States first, spreading to EU under cost containment reforms | Medium term (2-4 years) |

| AI governance and safety toolchains de-risk rollouts and unlock budgets | +3.2% | Global; EU AI Act and FDA guidance drive frameworks | Long term (≥ 4 years) |

| AI marketplaces and orchestration unify multi-vendor apps in workflows | +2.7% | North America and EU mature markets, emerging in Asia-Pacific IDNs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud/SaaS Shift Enabling Rapid AI Deployment at Enterprise Scale

Enterprise buyers in 2026 prioritize cloud-native platforms because they compress implementation timelines from many months to a few weeks while lowering total cost of ownership through managed services and pay-per-use inference economics. Cloud providers now offer native pipelines that convert legacy clinical documents into FHIR resources, with tools that remove a significant portion of historical mapping and data wrangling work that previously dominated health IT budgets. EHR suites that have been rebuilt on cloud infrastructure bring embedded agents for documentation, ordering, and coding, reducing the need to maintain separate inference stacks or integrate multiple point solutions across workflows. Wave-one deployments often focus on ambient documentation or imaging triage, which prove value quickly and then scale into more complex agentic orchestration across departments on the same operating layer for AI inside the AI in Enterprise Healthcare Platforms market. Integration of clinical assistants with productivity tools, such as calendaring and enterprise collaboration, supports unified agent experiences that draw context from clinical data and organizational workflows in a single pane of glass.[1]Microsoft, “A Year of DAX Copilot: Healthcare Innovation That Refocuses on the Clinician-Patient Connection,” Microsoft, blogs.microsoft.com

Ambient Clinical AI Reduces Documentation Burden and Unlocks ROI

Ambient clinical intelligence has moved from pilots to scaled rollouts because it reduces documentation time and improves note quality without harming accuracy, which places it at the top of many clinical AI roadmaps in 2026. Native EHR capabilities now support large sets of specialties and can align notes with coding and quality needs, which helps convert time savings into revenue capture and compliance benefits inside the AI in Enterprise Healthcare Platforms market. Ambient solutions combine ASR, specialty logic, and EHR context, while mapping content to the evidence captured in the encounter, which builds clinician trust and simplifies audit readiness.[2]Epic, “Epic AI Charting Rolls Out Alongside an Expanding Set of Built-in AI Capabilities,” Epic, epic.com Regulatory clarity for AI-enabled medical devices further reduces uncertainty for healthcare organizations as they deploy AI tools in production settings. Enterprise-grade platforms that pair multilingual ASR with governance and data security controls attract health systems looking to standardize ambient documentation at scale.

EHR Incumbents’ Distribution Moats Accelerate Embedded AI Uptake

EHR platforms are bundling native AI charting and coding assistants that work inside clinician workflows, reducing context switching and lowering the operational overhead of third-party tools. These vendors draw on longitudinal patient data within the EHR’s semantic model, which enhances agent performance on documentation and ordering tasks and shortens the path from pilot to enterprise-wide deployment for the AI in Enterprise Healthcare Platforms market. Expanding note-generation features from ambulatory to inpatient and emergency settings broadens the addressable base without separate vendor contracts or duplicative security reviews.[3]Oracle, “Oracle Health Clinical AI Agent Helps Emergency and Inpatient Doctors Spend More Time on Patient Care,” Oracle, oracle.comAs embedded AI becomes part of core EHR agreements, procurement friction drops because organizations do not need to evaluate multiple standalone products for overlapping functions. The combination of workflow integration, data leverage, and simplified procurement shapes buyer preferences toward platforms that can serve many use cases without vendor sprawl.

Value-Based and Revenue-Cycle Pressures Push Automation Platform Buys

Provider organizations under margin pressure in 2026 prefer automation platforms that tie clinical capture to revenue cycle needs, which supports a faster path to return on investment inside the AI in Enterprise Healthcare Platforms market. Policy shifts requiring standards-based prior authorization APIs create a forcing function for end-to-end automation that connects clinical documentation with utilization management and coding actions. Vendors that automate clinical appeals and contract analytics provide tangible impact on denials and time to cash, which aligns with CFO priorities for measurable working capital benefits. New contact center and point-of-care assistants can automate verification, scheduling, and documentation, which lowers administrative costs while improving patient access. As platforms link ambient documentation with automated orders and coding suggestions, revenue integrity improves because data capture aligns with billing, quality, and prior authorization requirements at the point of care.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Privacy/security and PHI governance slow scale-up | -4.5% | Global; heightened in EU and U.S., emerging in APAC | Short term (≤ 2 years) |

| Legacy integration and interoperability complexity | -3.8% | Global, with acute challenges where HL7 v2 persists and FHIR maturity varies | Medium term (2-4 years) |

| Reimbursement scrutiny on AI-assisted coding and prior authorization | -2.1% | United States focus, limited EU impact due to payer structures | Medium term (2-4 years) |

| Ethical and reputational pushback stalls platform deployments | -1.7% | Global; sensitive in academic medical centers and public health systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Privacy/Security and PHI Governance Slow Scale-Up

Healthcare organizations intensify controls on AI that touches PHI, which increases the time needed to finalize risk assessments, data minimization strategies, and audit procedures before production go-live. Enterprise buyers increasingly require evidence mapping and explainability to address clinical and legal concerns about how agentic systems produce outputs, which adds validation and documentation work to deployment plans in the AI in Enterprise Healthcare Platforms market. Healthcare AI that functions as a medical device continues to operate under lifecycle oversight and post-market monitoring expectations, which creates ongoing compliance responsibilities for both vendors and provider users. The EU AI Act’s high-risk classification for healthcare requires conformity, human oversight, technical documentation, and monitoring, which motivates organizations with international footprints to adopt governance programs that can serve multiple jurisdictions. These layered obligations raise the bar for vendors, especially smaller point-solution providers, and tilt buyer preferences to platforms that include governance-by-design for scaled use.

Legacy Integration and Interoperability Complexity

Modern AI expects FHIR APIs, event-driven architectures, and cloud services, but many clinical systems still rely on legacy integrations that are harder to standardize, which increases project scope and timeline.[4]Rhapsody Health Solutions Team, “Rhapsody Launches API Guardian to Power AI-Ready, Secure Data Exchange Across Healthcare,” Rhapsody, rhapsody.health Coexistence of HL7 v2 interfaces with FHIR-based services introduces bidirectional mapping work and version management, especially for labs, imaging, and billing systems that remain on older stacks. Health systems often operate hybrid models where on-premises EHR databases must connect securely to cloud inference services, which adds network, latency, and reliability considerations to design and testing inside the AI in Enterprise Healthcare Platforms market. API governance is becoming more central to multi-vendor environments as organizations standardize identity, authorization, and audit logging across FHIR and legacy protocols to support agentic workflows. Tooling that automates document-to-FHIR conversion, combined with managed FHIR services, reduces the lift of bringing historical records into AI-ready stores for downstream agents and assistants.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Platform consolidation drives software dominance and services expansion

Software commanded 56.72% share in 2025 and is projected to grow at 39.34% CAGR through 2031, driven by unified operating layers that embed inference, orchestration, and governance within core clinical and administrative workflows in the AI in Enterprise Healthcare Platforms market. EHR platforms now embed native charting and coding assistants that reduce the need for separate tools, which tightens workflow integration and accelerates deployment. Cloud-native EHR suites with agentic capabilities bundle AI into the core contract rather than as add-ons, which streamlines procurement and centralizes governance. Hyperscaler services that manage FHIR data stores, PHI governance, and model access provide the primitives to build agents across clinical and revenue cycle use cases inside the AI in Enterprise Healthcare Platforms market.

Services follow software growth as enterprises engage partners for AI readiness, FHIR migration, validation frameworks, and change management needed to scale deployments. Clinical and regulatory documentation for AI-enabled features requires lifecycle oversight that many organizations prefer to standardize with vendor support and internal governance teams. Cloud, EHR, and orchestration vendors also provide implementation accelerators and toolkits that reduce integration overhead for multi-entity provider systems. This pairing of embedded software and professional services sustains platform consolidation, replacing vendor sprawl with a smaller set of strategic relationships across the AI in Enterprise Healthcare Platforms market.

By Application: Imaging leads share, revenue cycle automation drives growth

Medical Imaging and Diagnostics Platforms held 47.43% share in 2025, supported by the breadth of authorized AI/ML-enabled devices and strong evidence for workflow gains in radiology. Improvements in multimodal models and clinical validation continue to increase confidence for image analysis and triage, which strengthens the case for department-wide scaling inside the AI in Enterprise Healthcare Platforms market. Integration of vision and language features with EHR context also helps move from narrow single-task algorithms to assistant-like workflows that connect findings with next-step actions. As general-purpose biomedical model platforms expand, imaging teams can adopt broader capabilities while maintaining explainability and audit trails.

Revenue Cycle and Coding Automation is the fastest-growing application at 37.65% CAGR, since organizations link clinical capture with coding, denials prevention, and prior authorization to improve cash flow and compliance in the AI in Enterprise Healthcare Platforms market. Embedded assistants that suggest codes, create orders, and structure documentation reduce downstream rework and denials, which aligns automation with measurable financial results. Contact center and point-of-care agents that handle verification, scheduling, and documentation lower administrative burden while improving throughput. As automated workflows expand, buyers favor platforms that connect documentation, coding, and authorization steps into a single governed path.

By Deployment: Cloud scale meets hybrid/edge latency demands

Cloud deployment commanded 53.35% share in 2025 because elasticity, managed FHIR services, and enterprise security attestations simplify rollout and scaling in the AI in Enterprise Healthcare Platforms market. Hyperscaler services integrate data pipelines, search, and model access that enterprises combine into clinical and business agents, accelerating the move from pilots to broad production. Cloud-native EHRs further compress time-to-value for note generation and order assistance by embedding agents and governance in the core platform. As platform capabilities expand, more organizations standardize on cloud-first approaches for AI orchestration across departments inside the AI in Enterprise Healthcare Platforms market.

Hybrid/Edge is the fastest-growing model at 39.67% CAGR because latency-sensitive uses like ambient documentation and intraoperative support require on-site compute while models and governance remain cloud-managed. Edge inference complements cloud training and lifecycle controls, which keeps protected data local when required and enables millisecond response for live clinical interactions. National data localization rules and sovereign cloud programs in multiple regions also motivate hybrid patterns with federated or partitioned data flows. Organizations continue to maintain some on-premises workloads for regulated or device-embedded functions, but the direction of travel favors cloud-plus-edge architectures inside the AI in Enterprise Healthcare Platforms market.

By End User: Healthcare Providers lead, healthcare payers accelerate under regulatory momentum

Healthcare Providers accounted for 42.39% of spend in 2025, reflecting broad deployment of ambient documentation, imaging, and operational assistants across integrated delivery networks and specialty clinics. Academic centers with advanced research programs partner with AI infrastructure providers to develop and validate foundational biomedical models, while community hospitals select turnkey platforms that minimize IT lift. Providers also favor embedded EHR features for charting and coding that operate in native workflows, which reduces training and change management friction inside the AI in Enterprise Healthcare Platforms market. As procurement teams consolidate vendors, platform breadth and governance capabilities become selection priorities.

Healthcare Payers are the fastest-growing end user at 36.88% CAGR as they modernize prior authorization, member engagement, and clinical-data intake with AI assistants and automation. Data-rich payers and life sciences firms adopt AI infrastructure for drug discovery and real-world evidence pipelines, which advances model development and supports precision interventions. Frontline payer operations add voice and chat agents for verification, scheduling, and benefits questions to improve member experience and lower costs inside the AI in Enterprise Healthcare Platforms market. The combination of policy momentum and maturing orchestration layers drives broader adoption across payer portfolios.

By AI Technology: Multimodal fusion displaces single-modality taxonomies

Machine Learning and Deep Learning held 48.27% share in 2025 because these approaches underpin imaging analysis, claims prediction, and care management risk models across the AI in Enterprise Healthcare Platforms market. Rapid progress in foundational architectures allows a single system to integrate vision, language, and structured prediction, which narrows the gap between discrete tools and unified assistants. As general-purpose biomedical model platforms mature, healthcare enterprises focus on orchestration layers, grounding, and explainability to deploy them safely at scale. This shift reduces the relevance of single-technology taxonomies compared with the orchestration layer that unifies agents and workflows in the AI in Enterprise Healthcare Platforms market.

Natural Language Processing and Speech/ASR is the fastest-growing technology at 39.43% CAGR due to the ambient documentation boom and the spread of conversational assistants into patient access and revenue cycle interactions. Multilingual ASR, speaker diarization, and noise robustness have matured for complex clinical environments, which supports broad rollouts in ambulatory and inpatient settings. EHR-native mobile and desktop integrations further simplify clinician adoption by keeping assistants inside existing workflows. As RAG becomes standard for clinical assistants, organizations ground outputs in guidelines, literature, and internal protocols to improve accuracy and trust across the AI in Enterprise Healthcare Platforms market.

Geography Analysis

North America led the AI in Enterprise Healthcare Platforms market with 46.34% share in 2025 as regulatory clarity, EHR incumbent distribution, and cloud maturity combined to drive enterprise-wide deployments. The FDA’s AI guidance and the rapid expansion of native AI charting inside major EHRs helped normalize AI use at scale in clinical settings. EHR platforms reported strong adoption of ambient documentation by mid-2025, which created an installed base for broader agentic workflows across specialties. Standards-based API requirements and payer modernization initiatives continue to push organizations to adopt FHIR-aligned automation flows in the AI in Enterprise Healthcare Platforms market.

Europe’s trajectory is shaped by the EU AI Act, which classifies healthcare as high-risk and establishes obligations for conformity assessment, human oversight, and post-market monitoring. Countries with strong digital health infrastructure and interoperability policies are adopting platform approaches that combine embedded EHR AI with curated marketplaces under unified governance. As vendors align with MDR and IVDR pathways and build evidence for safety and performance, adoption proceeds in a compliance-first fashion inside the AI in Enterprise Healthcare Platforms market. Cloud and edge combinations support data-residency rules while enabling advanced agentic capability at the point of care.

Asia-Pacific is projected to grow at 39.12% CAGR through 2031 as governments invest in AI and data infrastructure and as health systems expand digital capabilities across large populations. National strategies around AI adoption, localized language models, and sovereign cloud efforts support platform deployments that combine ambient documentation, imaging support, and patient access assistants. Multilingual capabilities and in-region cloud services help meet sovereignty and latency needs in the AI in Enterprise Healthcare Platforms market. As providers and payers align incentives for automation, APAC health systems move from pilots to scaled orchestrations that connect clinical, operational, and revenue workflows.

Competitive Landscape

The AI in Enterprise Healthcare Platforms market is characterized by competitive dynamics that are coalescing around two archetypes: EHR-embedded platforms with broad distribution scale, and best-of-breed AI specialists focused on deep, niche innovation. Platform vendors are expanding native charting, coding, and orchestration, which pressures standalone tools where the platform can match or exceed feature sets inside integrated workflows. EHR-native agents that extend from ambulatory to inpatient and emergency settings gain reach without separate integrations and contracts, which consolidates enterprise spend toward fewer platforms.

Hyperscalers are countering by positioning their AI services as the orchestration and governance substrate across multi-vendor ecosystems in the AI in Enterprise Healthcare Platforms market. Vendor marketplaces and third-party extensibility signal a platform-of-platforms direction that keeps choice for health systems while centralizing identity, audit, and PHI controls. Cloud-native healthcare data services that emphasize FHIR interoperability and enterprise-grade governance are now a cornerstone of hyperscaler strategies for healthcare.

AI infrastructure providers influence the pace of innovation by enabling foundation models and synthetic data pipelines for life sciences and provider research groups. Pharmaceutical and diagnostics leaders that build large hybrid-cloud AI factories gain the compute and tooling to develop models across R&D and clinical workflows, which raises the bar for specialized competitor. In parallel, new healthcare-focused AI assistants from hyperscalers target contact centers and point-of-care operations, opening white space not fully served by incumbent EHR vendors inside the AI in Enterprise Healthcare Platforms market.

AI In Enterprise Healthcare Platforms Industry Leaders

Epic Systems

Microsoft

Oracle

Koninklijke Philips N.V.

GE HealthCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Merck and Google Cloud announced a multi-year partnership valued at up to USD 1 billion to accelerate Merck's enterprise transformation into an AI-enabled entity, deploying an agentic platform across R&D, manufacturing, commercial, and corporate functions utilizing Google Cloud's Gemini Enterprise to digitize data and boost productivity for Merck's 75,000 employees.

- April 2026: Bunkerhill Health secured a CMS reimbursement pathway and FDA clearance for its AI algorithms evaluating coronary artery calcium and aortic valve calcium on contrast-enhanced chest CTs, with CMS establishing a new national billing code and associated payment under the Hospital Outpatient Prospective Payment System effective April 1, 2026, representing the first AI cardiovascular analysis to achieve dedicated reimbursement outside of traditional imaging pathways.

- April 2026: Autonomize AI introduced Version 3 of its Intelligence Platform, an AI operating layer for healthcare providing 160+ healthcare-native AI agents, over 50 pre-built system connectors, and a Command Center with real-time visibility into KPIs.

- April 2026: AWS launched Amazon Bio Discovery, an AI-powered application for drug development that provides access to biological foundation models and includes an AI agent for experiment design with integration to lab partners.

Global AI In Enterprise Healthcare Platforms Market Report Scope

According to the report’s scope, AI in enterprise healthcare platforms refers to the integration of machine‑learning, natural‑language processing, and automation tools within large‑scale hospital and health‑system software ecosystems to enhance clinical, operational, and financial performance. It enables intelligent workflows such as automated documentation, predictive analytics, population‑health insights, and real‑time decision support, improving efficiency, accuracy, and system‑wide coordination.

The AI in enterprise healthcare platforms market is segmented into offering, application, deployment, end user, AI technology, and geography. By offering, the market is segmented into Software and Services. By application, the market is segmented into medical imaging and diagnostics platforms, clinical documentation and ambient scribing, clinical decision support and care orchestration, revenue cycle and coding automation, patient engagement/CRM and contact center AI, cybersecurity/privacy and PHI redaction, and others. By deployment, the market is segmented into cloud, on-premises, and hybrid/edge. By end user, the market is segmented into healthcare providers, imaging centers, healthcare payers, and others. By AI technology, the market is segmented into machine learning and deep learning, natural language processing and speech/ASR, and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Software |

| Services |

| Medical Imaging and Diagnostics Platforms |

| Clinical Documentation and Ambient Scribing |

| Clinical Decision Support and Care Orchestration |

| Revenue Cycle and Coding Automation |

| Patient Engagement/CRM and Contact Center AI |

| Cybersecurity/Privacy and PHI Redaction |

| Others |

| Cloud |

| On-premises |

| Hybrid/Edge |

| Healthcare Providers |

| Imaging Centers |

| Healthcare Payers |

| Others |

| Machine Learning and Deep Learning |

| Natural Language Processing and Speech/ASR |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Offering | Software | |

| Services | ||

| By Application | Medical Imaging and Diagnostics Platforms | |

| Clinical Documentation and Ambient Scribing | ||

| Clinical Decision Support and Care Orchestration | ||

| Revenue Cycle and Coding Automation | ||

| Patient Engagement/CRM and Contact Center AI | ||

| Cybersecurity/Privacy and PHI Redaction | ||

| Others | ||

| By Deployment | Cloud | |

| On-premises | ||

| Hybrid/Edge | ||

| By End User | Healthcare Providers | |

| Imaging Centers | ||

| Healthcare Payers | ||

| Others | ||

| By AI Technology | Machine Learning and Deep Learning | |

| Natural Language Processing and Speech/ASR | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the AI in Enterprise Healthcare Platforms market growth outlook to 2031?

The AI in Enterprise Healthcare Platforms market size is projected to reach USD 29.51 billion by 2031, expanding at a 34.48% CAGR over 2026-2031.

Which segments lead adoption within the AI in Enterprise Healthcare Platforms market?

Software led with 56.72% share in 2025 and Medical Imaging and Diagnostics Platforms held 47.43% share, supported by regulatory maturity and strong workflow ROI.

What deployment model is scaling fastest in the AI in Enterprise Healthcare Platforms market?

Cloud accounted for 53.35% share in 2025, while Hybrid/Edge is the fastest-growing model at 39.67% CAGR due to latency and data-residency needs.

Which end users are driving demand in the AI in Enterprise Healthcare Platforms market?

Healthcare Providers led spending with 42.39% in 2025, and payers are the fastest-growing as they modernize prior authorization and member engagement with agentic workflows.

Page last updated on: