Healthcare AI Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

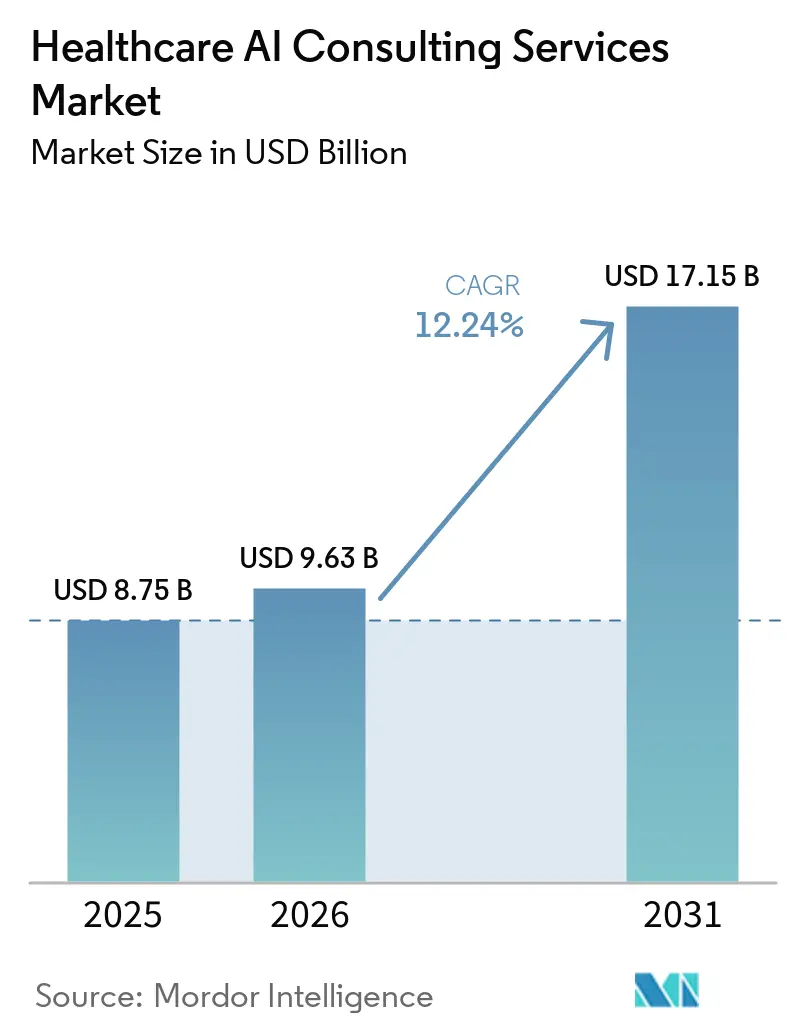

| Market Size (2026) | USD 9.63 Billion |

| Market Size (2031) | USD 17.15 Billion |

| Growth Rate (2026 - 2031) | 12.24% CAGR |

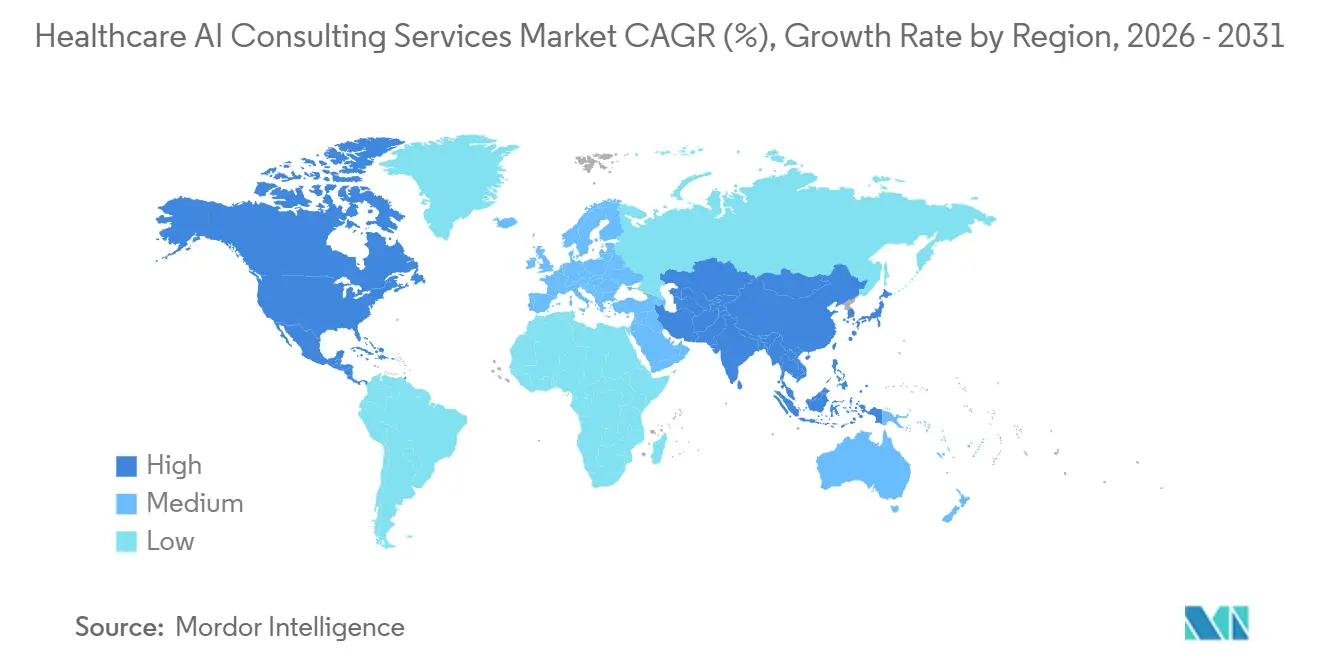

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

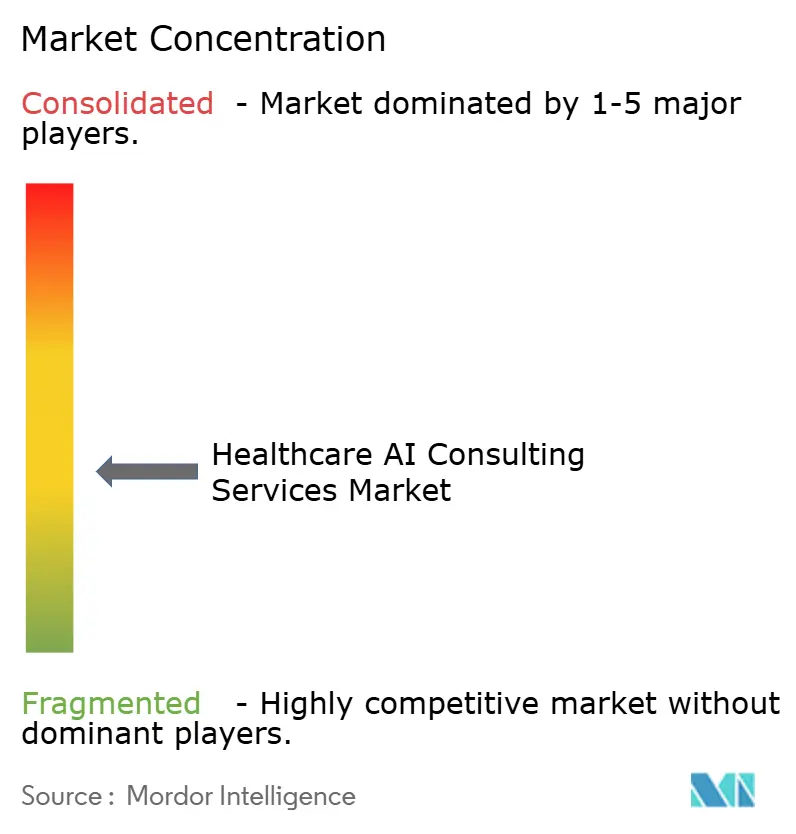

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare AI Consulting Services Market Analysis by Mordor Intelligence

The healthcare AI consulting services market is expected to increase from USD 8.75 billion in 2025 to USD 9.63 billion in 2026 and reach USD 17.15 billion by 2031, growing at a CAGR of 12.24% over 2026-2031. The healthcare AI consulting services market is being shaped by a clear shift from pilot programs to live deployment, which is increasing demand for architecture design, workflow integration, governance, and post-deployment optimization. The healthcare AI consulting services market is also gaining support from tighter regulatory oversight, because health systems and technology vendors now need outside help to map use cases, document model behavior, and maintain lifecycle controls in line with updated software and AI management frameworks. Another durable growth layer in the healthcare AI consulting services market is the rise of jurisdiction-specific model tuning and sovereign deployment requirements, especially in Europe and parts of Asia, where data localization rules limit the use of generic hosted models and extend consulting engagement cycles. Competitive conditions in the healthcare AI consulting services market are tightening as global firms deepen cloud alliances and package strategy, implementation, and governance into one delivery model, while engineering-led specialists continue to win selective mandates in the mid-market. This leaves the healthcare AI consulting services market with strong opportunity in sovereign AI infrastructure, regulated clinical deployment, payer operations automation, and recurring governance work that continues after the first implementation wave.

Key Report Takeaways

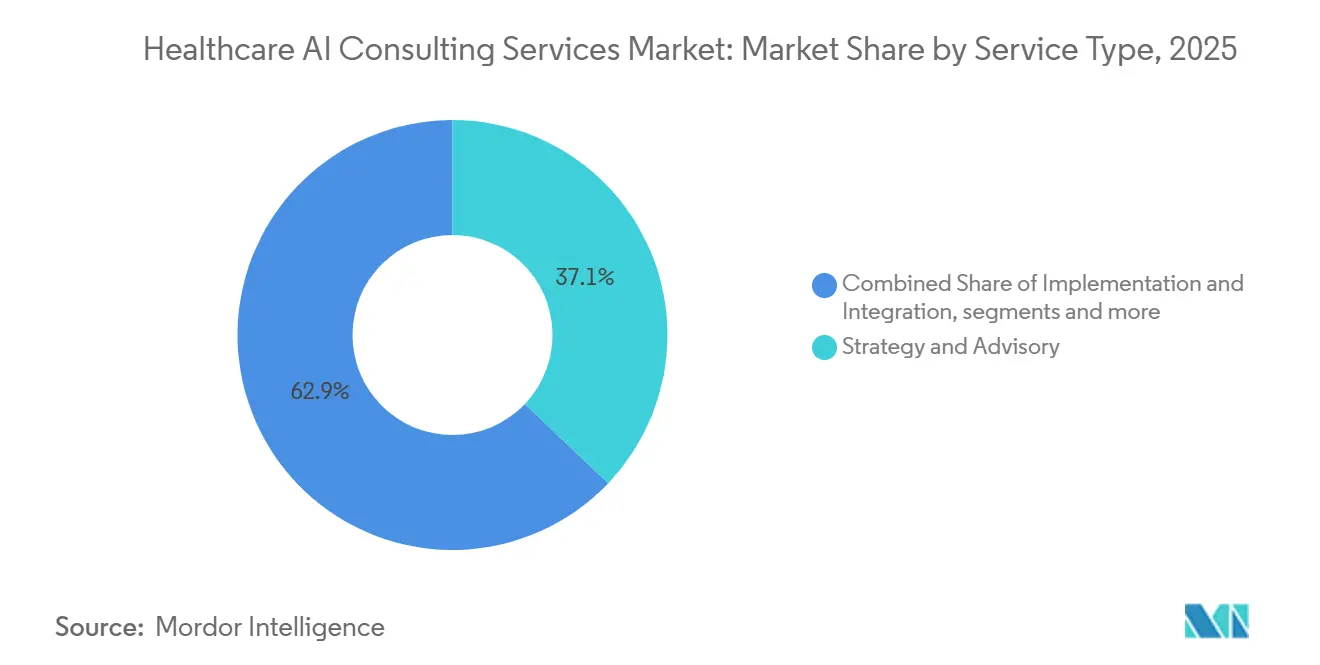

- By service type, implementation and integration held 37.14% of the healthcare AI consulting services market share in 2025, while AI model development and customization is projected to grow at a 12.77% CAGR through 2031.

- By deployment model, cloud-based AI solutions accounted for 55.46% of market revenue in 2025, and this same segment is expected to expand at a 12.68% CAGR through 2031.

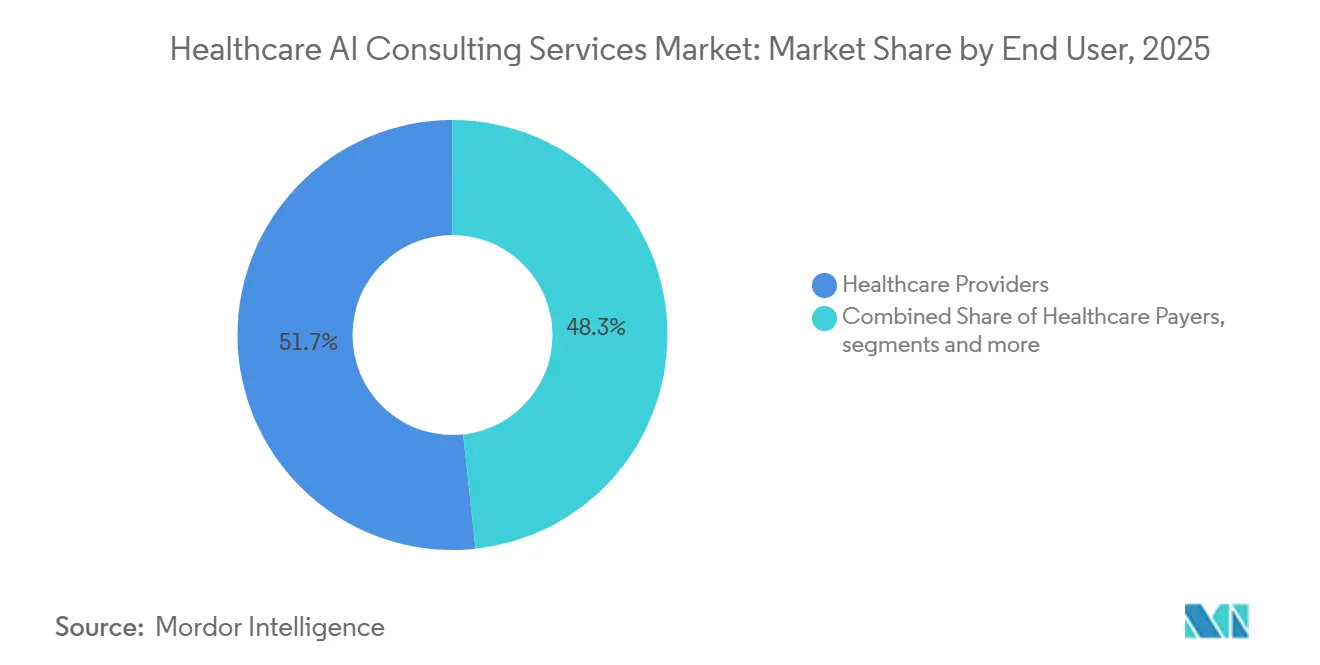

- By end user, healthcare providers captured 51.74% of market revenue in 2025, while healthcare payers recorded the highest projected CAGR at 13.60% through 2031.

- By application, clinical decision support and diagnostics accounted for 53.9% of the healthcare AI consulting services market size in 2025, while administrative and operational optimization is projected to advance at a 13.52% CAGR through 2031.

- By geography, North America held 53.13% of the healthcare AI consulting services market share in 2025, while Asia-Pacific is projected to grow at 13.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare AI Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of AI-Driven Clinical Decision Support Systems | +2.0% | Global, with North America and Asia-Pacific leading clinical deployment | Medium term (2-4 years) |

| Rising Healthcare-Cost Pressures Pushing Efficiency-Focused AI Consulting | +1.8% | Global, most acute in North America, Western Europe, and APAC | Short term (≤ 2 years) |

| Increasing Cloud Migration of Healthcare IT Infrastructure | +1.6% | Global, APAC highest growth velocity, North America most advanced maturity | Short term (≤ 2 years) |

| Shift Toward Outcome-Based Consulting Fee Models Enabling Risk-Sharing | +1.5% | North America leading adoption, spill-over to Western Europe | Medium term (2-4 years) |

| Emerging Demand for Foundation-Model Fine-Tuning to Meet Data-Sovereignty Rules | +1.5% | Europe, Asia-Pacific | Medium term (2-4 years) |

| Increasing Regulatory Focus on Responsible AI Governance in Healthcare | +1.4% | Global, North America and EU at forefront of formal frameworks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of AI-Driven Clinical Decision Support Systems

Hospitals and health systems are moving from limited pilots to live use of AI-driven clinical decision support, and that shift is creating steady demand for design, validation, integration, and optimization work in the healthcare AI consulting services market. The FDA’s reissued Clinical Decision Support Software guidance in January 2026 sharpened the boundary between non-device CDS functions and regulated software, which increases the need for outside advisory support on system design and compliance mapping in the United States.[1]Food and Drug Administration, “Clinical Decision Support Software Final Guidance,” FDA, fda.gov That same guidance also leaves room for faster deployment of AI-assisted recommendations when each function is carefully mapped against the statutory criteria, so consulting teams that can do this precisely are gaining importance. The work is no longer limited to model selection, because organizations also need help aligning model outputs with clinical workflow, escalation rules, documentation standards, and oversight controls. This expands the scope of the healthcare AI consulting services market from implementation alone to a broader mix of validation, monitoring, and governance support. It also raises the value of consultants that can translate regulatory language into practical operating rules for health systems and software vendors.

Rising Healthcare-Cost Pressures Pushing Efficiency-Focused AI Consulting

Healthcare cost pressure is acting as a direct catalyst for AI consulting demand rather than slowing spending in the healthcare AI consulting services market. Health systems are now asking for tightly scoped programs tied to measurable workflow gains, claims efficiency, and staff time savings instead of longer strategy-heavy engagements. This has made administrative and financial workflows one of the fastest entry points for consulting-led AI deployment, because leaders can track cycle time, rework, throughput, and denial outcomes with less ambiguity than many clinical use cases. Aetna’s second-generation Claims Assist Manager, launched in May 2026, reduced processing time for complex claims by more than 20%, which shows why payer and provider organizations are directing consulting budgets toward repeatable operational use cases.[2]CVS Health, “Aetna Reduces Claims Processing Time by More Than 20% With AI to Improve Care Experience,” CVS Health Investor Relations, investors.cvshealth.comThe healthcare AI consulting services market is therefore seeing stronger demand for short-cycle implementation, workflow redesign, and benefits tracking support. Firms that can prove rapid execution in revenue cycle and adjacent back-office areas are better positioned to win follow-on work across a broader enterprise estate.

Emerging Demand for Foundation-Model Fine-Tuning to Meet Data-Sovereignty Rules

Government-led data localization and sovereign hosting requirements are turning jurisdiction-specific model tuning into a core growth pocket in the healthcare AI consulting services market. France’s national AI and health data strategy for 2025 to 2028 explicitly supports sovereign AI systems that keep health data within French and European borders, which makes generic deployment models less workable for many hospitals and public institutions. The NITRD health workshop report from 2025 also highlighted federated learning as a practical approach for training and tuning models across institutions without centralizing patient data.[3]National Coordination Office for Networking and Information Technology Research and Development, “Foundation LLM Health Workshop Report,” NITRD, nitrd.gov Research published in late 2025 on personalized federated fine-tuning for healthcare showed stronger task performance than both purely local and centralized training methods on real-world medical imaging workloads. Corti’s launch of Europe’s first sovereign healthcare AI infrastructure in July 2025 showed that this requirement is already moving from policy discussion into live deployment practice. This makes the healthcare AI consulting services market more attractive for firms that can combine regulatory interpretation, deployment architecture, and clinical validation in one engagement.

Increasing Regulatory Focus on Responsible AI Governance in Healthcare

Responsible AI governance is becoming a separate buying category within the healthcare AI consulting services market as regulators define clearer compliance expectations across the model lifecycle. The FDA’s updated CDS guidance and the IMDRF technical framework issued in April 2026 both narrow the room for informal deployment practices by clarifying expectations around intended use, oversight, documentation, and lifecycle management. As a result, health systems and vendors increasingly need third-party support to set governance structures before wider rollouts take place. This is expanding consulting work into model inventory design, traceability processes, validation plans, audit trails, and change management controls. The healthcare AI consulting services market benefits because governance work often continues after the first deployment and becomes part of ongoing operating discipline. It also strengthens firms that can package legal, technical, and clinical oversight into one delivery team.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Security Concerns Under HIPAA/GDPR | -1.2% | North America, EU, spill-over globally | Short term (≤ 2 years) |

| Shortage of AI-Skilled Healthcare Workforce | -1.0% | Global, most acute in APAC and Latin America | Medium term (2-4 years) |

| Vendor-Liability Uncertainty in AI-Caused Misdiagnosis Litigation | -0.6% | North America primary, EU emerging | Medium term (2-4 years) |

| High Implementation and Integration Costs Across Legacy Healthcare Systems | -0.4% | Global, most severe in developing economies and smaller provider organizations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy and Security Concerns Under HIPAA/GDPR

Privacy and security issues slow projects in the healthcare AI consulting services market mainly by extending deployment timelines instead of stopping demand outright. AI tools that process protected health information require risk analysis, access control review, workflow documentation, and contract controls before they move into production, which adds sequencing pressure to already complex health system programs. This is more difficult for organizations operating across both U.S. and European jurisdictions, because logging, documentation, and governance needs cannot be treated as one common process when the underlying legal frameworks differ. The result is a larger compliance workload per engagement, but it also delays the proof points that many buyers want before approving broader rollout budgets. This creates a short-term drag on the healthcare AI consulting services market even while it expands the scope of individual consulting assignments. It also favors providers that can reduce friction by combining privacy, technical controls, and operating model support in one program.

Shortage of AI-Skilled Healthcare Workforce

The workforce constraint in the healthcare AI consulting services market is not only a technical staffing issue, because it also affects adoption quality, workflow redesign, and the speed of value capture after deployment. OECD data published in 2025 showed that demand for health professionals with AI-related skills remained only 0.2% to 0.3% of total new health profession job postings across OECD countries, which points to slow diffusion of AI capability into the clinical frontline. This means healthcare organizations can complete architecture work successfully yet still underperform at the user level if staff training, role design, and change support are weak. The healthcare AI consulting services market therefore depends on more than implementation, because adoption programs increasingly need education, governance, and workflow coaching as part of the same mandate. In many cases, the limiting factor is not the model itself but the ability of clinicians, administrators, and managers to trust and use it consistently. That gap can compress measurable return and slow the release of follow-on budgets even when the initial deployment is technically sound.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Implementation Dominates, but Customization Captures the Next Wave

Implementation and integration held 37.14% of revenue in 2025, which shows that the healthcare AI consulting services market is still centered on production deployment rather than early-stage ideation. Health systems are using consultants to connect AI models with live EHR environments, fit outputs into existing clinical pathways, and build monitoring processes that satisfy both IT and clinical governance needs. This makes implementation work larger in scope than simple technical activation, because it also includes workflow redesign, testing, and operational handoff. AI model development and customization is the fastest-growing service type and is projected to expand at a 12.77% CAGR from 2026 to 2031. That growth reflects rising demand for locally tuned models in regulated healthcare settings and for use cases that cannot rely on generic model behavior.

The healthcare AI consulting services market is also becoming more layered within this service split. Strategy and Advisory, Data and Governance Consulting, and Regulatory and Compliance Consulting hold smaller shares, but they are becoming recurring mandates as organizations move from first deployment to control, optimization, and audit readiness. This means implementation projects often create downstream demand for governance and compliance scopes rather than ending once a model is live.

By Deployment Model: Cloud Leads Across Both Share and Growth Metrics

Cloud-based AI solutions accounted for 55.46% of revenue in 2025, which makes cloud the leading infrastructure layer for the healthcare AI consulting services market. That position reflects the growing need to support enterprise-scale AI workloads, broader data access, and faster deployment cycles across providers, payers, and digital health platforms. Earlier cloud transitions in EHR environments, telehealth systems, and data-intensive workloads have already created a base of organizations that are technically ready for AI but still need outside help to operationalize it. Cloud-based AI solutions are also the fastest-growing deployment segment and are expected to be forecasted at 12.68% CAGR through 2031. This makes cloud consulting central to the next phase of the healthcare AI consulting services market, especially where orchestration, interoperability, monitoring, and security have to be handled together.

On-premise AI solutions still retain a meaningful role in organizations that face strict residency rules, highly controlled network environments, or internal preferences for direct infrastructure oversight. This is especially relevant in settings where sensitive workloads cannot be moved easily into shared hosted environments. Hybrid Solutions are therefore emerging as the practical middle path, because many health systems need flexibility across cloud, local processing, and application-specific environments.

By End User: Providers Anchor Demand While Payers Accelerate Fastest

Healthcare providers held 51.74% of market revenue in 2025, which gave them the leading position in the healthcare AI consulting services market. Their demand is broad, because it spans ambient documentation, clinical decision support, diagnostics, operational automation, and patient engagement. Provider organizations also face the greatest need to fit AI into live clinical and administrative workflows without disrupting care delivery. Healthcare payers are the fastest-growing end-user segment and are projected to expand at a 13.60% CAGR from 2026 to 2031. That faster rise reflects pressure around claims workflows, prior authorization, utilization management, and member service operations.

Life sciences and pharma companies remain active buyers for drug discovery support, trial optimization, and regulatory submission work. MedTech and device companies are also expanding advisory needs for embedded algorithms and for Predetermined Change Control Plan submissions under the FDA’s final guidance issued in December 2024. Government and public health agencies, along with healthcare IT and digital health companies, form smaller segments, but they are still important because public digital health programs and platform modernization efforts continue to create targeted consulting demand.

By Application: CDS Anchors Market, RCM Defines the Fastest Opportunity

Clinical decision support and diagnostics held 53.86% of revenue in 2025, making it the largest application area in the healthcare AI consulting services market. This leadership reflects sustained spending on ambient AI, imaging support, clinical recommendations, and treatment pathway tools across hospital systems. The consulting need here extends beyond implementation, because organizations must validate outputs, define oversight, and connect AI recommendations with physician workflow and documentation standards. Administrative and operational optimization is the fastest-growing application segment and is projected to grow at a 13.52% CAGR from 2026 to 2031. That pattern shows where organizations are seeing the clearest operational return from AI-assisted redesign.

The healthcare AI consulting services market is benefiting from the fact that revenue cycle and adjacent administrative workflows can often deliver measurable improvements sooner than many clinical deployments. Medical Imaging and Population Health and Predictive Analytics also remain important applications, with consulting work tied to governance, integration, and scaling across multiple settings. Drug Discovery and Development continues to generate steady demand from pharmaceutical and biotech clients that are applying AI to target identification, screening, and filing processes. The FDA’s 2025 guiding principles for good AI practice in drug development are helping shape a clearer compliance advisory path for this part of the market. As a result, the healthcare AI consulting services market is seeing a balanced mix of clinically oriented work and operationally focused mandates, with faster near-term expansion in functions where financial outcomes are easier to document.

Geography Analysis

North America accounted for 53.13% of global revenue in 2025, which kept it as the largest regional block in the healthcare AI consulting services market. The United States supports that position through mature digital infrastructure, high consulting spend per health system, and a regulatory environment that creates both compliance work and clearer buying triggers. The launch of Aetna’s second-generation Claims Assist Manager in May 2026 and the continued scaling of AI-enabled payer operations show how operational use cases are translating into real consulting demand in the region. Canada and Mexico also contribute through public digital health activity and commercial healthcare modernization programs. California’s AB-2575 adds another layer of importance because it introduces specific liability rules for AI-based clinical decision support and is likely to influence compliance planning beyond one state.

Europe remains the second-largest region in the healthcare AI consulting services market, led by Germany, the United Kingdom, and France. Germany’s environment is shaped by digital health reimbursement structures and by practical interpretation of the EU AI Act, with BfArM publishing guidance in 2025 on how AI-based medical products should be classified under the relevant European frameworks. France is also becoming more important as sovereign deployment rules and national health data strategy priorities raise demand for localized architecture, governance, and implementation support. The United Kingdom, Italy, and Spain remain active adoption markets, while the rest of Europe continues to build momentum through broader digital health programs.

Asia-Pacific is the fastest-growing region and is anticipated to expand at a 13.92% CAGR from 2026 to 2031, which gives it the strongest growth profile in the healthcare AI consulting services market. Growth across China, South Korea, and India is not uniform, because each market is being shaped by different combinations of reimbursement policy, digital health infrastructure, and public program design. South Korea’s 2026 mandate for AI cancer screening under national health insurance creates immediate implementation and compliance work, while India’s National Digital Health Mission continues to support interoperable data standards across a large and diverse care base. Middle East and Africa is being driven mainly by GCC smart health programs, and South America is progressing through private insurer adoption led by countries such as Brazil and Argentina. This means the healthcare AI consulting services market is broadening geographically, but the pace of consulting demand still depends heavily on policy execution, public digital infrastructure, and local system readiness.

Competitive Landscape

The healthcare AI consulting services market is moderately fragmented at the top, with the Big Four advisory firms, MBB strategy firms, and large IT services providers controlling much of the premium enterprise work. Even so, the healthcare AI consulting services market is not locked by a small group, because specialist healthcare firms and engineering-led boutiques continue to win targeted programs where domain knowledge or delivery speed matters more than global scale. Competition is shifting further in 2026 toward hyperscaler-linked delivery ecosystems. Accenture’s recognition as Google Cloud’s 2026 Global Services Partner of the Year for the fourth straight year reinforces how deeply cloud relationships now shape perceived consulting capability in the healthcare AI consulting services market.

Specialist healthcare consultancies still hold defensible positions in the healthcare AI consulting services market where payer data, real-world evidence, or workflow-specific expertise matter. Optum Advisory, IQVIA, and ZS Associates benefit from stronger healthcare domain alignment than many generalist providers, especially in payer and pharma work. Infosys strengthened its provider-facing capabilities through the completion of its Optimum Healthcare IT acquisition in May 2026. IBM also improved its data and agentic workflow position with the completion of its Confluent acquisition in March 2026, which matters for healthcare use cases where real-time data movement affects operational performance.

The healthcare AI consulting services market still offers white space in sovereign AI architecture, federated learning deployment, outcome-linked program design, and independent governance assurance. That leaves room for smaller engineering-first firms that can offer fixed-fee delivery and tighter execution in cost-sensitive accounts. Strategic moves across 2026 support this view, including Roche’s agreement to acquire PathAI to deepen AI-driven diagnostics capability and Cognizant’s decision to open TriZetto Unify to AI agents for payer-provider workflows. The healthcare AI consulting services market therefore rewards scale, but it still leaves enough room for specialist firms that can solve a narrow healthcare problem faster than broader platform-led competitors.

Healthcare AI Consulting Services Industry Leaders

Accenture

Deloitte

IBM

PwC

Cognizant

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Aetna (CVS Health) launched the second-generation Aetna Claims Assist Manager (CAM), an AI-powered agentic claims advisory platform that reduces processing time by over 20% for complex claims. The deployment consolidates eligibility, coverage, member, and provider data across AI agents, positioning Aetna as a benchmark for payer AI adoption in the RCM domain.

- May 2026: Roche entered a definitive merger agreement to acquire PathAI, a digital pathology and AI-powered diagnostics company, for USD 750 million upfront plus milestone payments up to USD 300 million. The deal builds on a partnership established in 2021 and advances Roche's AI-enabled companion diagnostic capabilities, with closing expected in H2 2026.

- May 2026: Infosys completed the acquisition of Optimum Healthcare IT, a Best-in-KLAS healthcare digital transformation and consulting firm. The combination targets AI-powered, large-scale cloud and data transformation for healthcare providers, strengthening Infosys's end-to-end healthcare services offering.

- May 2026: Cognizant opened its TriZetto Unify platform to AI agents for prior authorization, treating AI agents as first-tier consumers of payer-provider workflow automation. TriZetto platforms support over 200 million healthcare members and process over USD 500 billion in annual healthcare spend.

Global Healthcare AI Consulting Services Market Report Scope

According to the report’s scope, the healthcare AI consulting services market refers to the industry that provides advisory, strategy, implementation, integration, governance, and optimization services to healthcare organizations seeking to adopt artificial intelligence technologies. These services help healthcare providers, payers, pharmaceutical companies, and life sciences organizations leverage AI for clinical decision-making, operational efficiency, patient engagement, and data-driven healthcare transformation.

The healthcare AI consulting services market is segmented into service type, deployment model, end user, application, and geography. By service type, the market is segmented into strategy and advisory, implementation and integration, AI model development and customization, data and governance consulting, regulatory and compliance consulting, and others. By deployment model, the market is segmented into on-premise AI solutions, cloud-based AI solutions, and hybrid solutions. By end user, the market is segmented into healthcare providers, healthcare payers, life sciences and pharma companies, medtech and device companies, healthcare IT and digital health companies (incl. startups), and government and public health agencies. By application, the market is segmented into clinical decision support and diagnostics, medical imaging, population health and predictive analytics, drug discovery and development, administrative and operational optimization (incl. RCM), and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Strategy and Advisory |

| Implementation and Integration |

| AI Model Development and Customization |

| Data and Governance Consulting |

| Regulatory and Compliance Consulting |

| Others |

| On-Premise AI Solutions |

| Cloud-Based AI Solutions |

| Hybrid Solutions |

| Healthcare Providers |

| Healthcare Payers |

| Life Sciences and Pharma Companies |

| MedTech and Device Companies |

| Healthcare IT and Digital Health Companies (incl. startups) |

| Government and Public Health Agencies |

| Clinical Decision Support and Diagnostics |

| Medical Imaging |

| Population Health and Predictive Analytics |

| Drug Discovery and Development |

| Administrative and Operational Optimization (incl. RCM) |

| Others |

| Inpatient |

| Outpatient |

| Emergency and Urgent Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Service Type | Strategy and Advisory | |

| Implementation and Integration | ||

| AI Model Development and Customization | ||

| Data and Governance Consulting | ||

| Regulatory and Compliance Consulting | ||

| Others | ||

| By Deployment Model | On-Premise AI Solutions | |

| Cloud-Based AI Solutions | ||

| Hybrid Solutions | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Life Sciences and Pharma Companies | ||

| MedTech and Device Companies | ||

| Healthcare IT and Digital Health Companies (incl. startups) | ||

| Government and Public Health Agencies | ||

| By Application | Clinical Decision Support and Diagnostics | |

| Medical Imaging | ||

| Population Health and Predictive Analytics | ||

| Drug Discovery and Development | ||

| Administrative and Operational Optimization (incl. RCM) | ||

| Others | ||

| By Clinical Setting | Inpatient | |

| Outpatient | ||

| Emergency and Urgent Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of healthcare AI consulting services by 2031?

The healthcare AI consulting services market is projected to reach USD 17.15 billion by 2031 from USD 9.63 billion in 2026, which reflects sustained demand for deployment, governance, and optimization support.

Which service type currently leads spending?

Implementation and Integration led in 2025 with 37.14% of revenue, showing that buyers are still prioritizing production rollout and system integration over early-stage advisory alone.

Which application area is growing the fastest?

Administrative and Operational Optimization is the fastest-growing application area, with a projected 13.52% CAGR from 2026 to 2031, supported by strong demand in revenue cycle and related workflows.

Why is Asia-Pacific expanding faster than other regions?

Asia-Pacific is projected to grow at a 13.92% CAGR through 2031 because policy support, digital health infrastructure programs, and country-level implementation mandates are accelerating adoption.

Page last updated on: