AI In Clinical Conversations Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

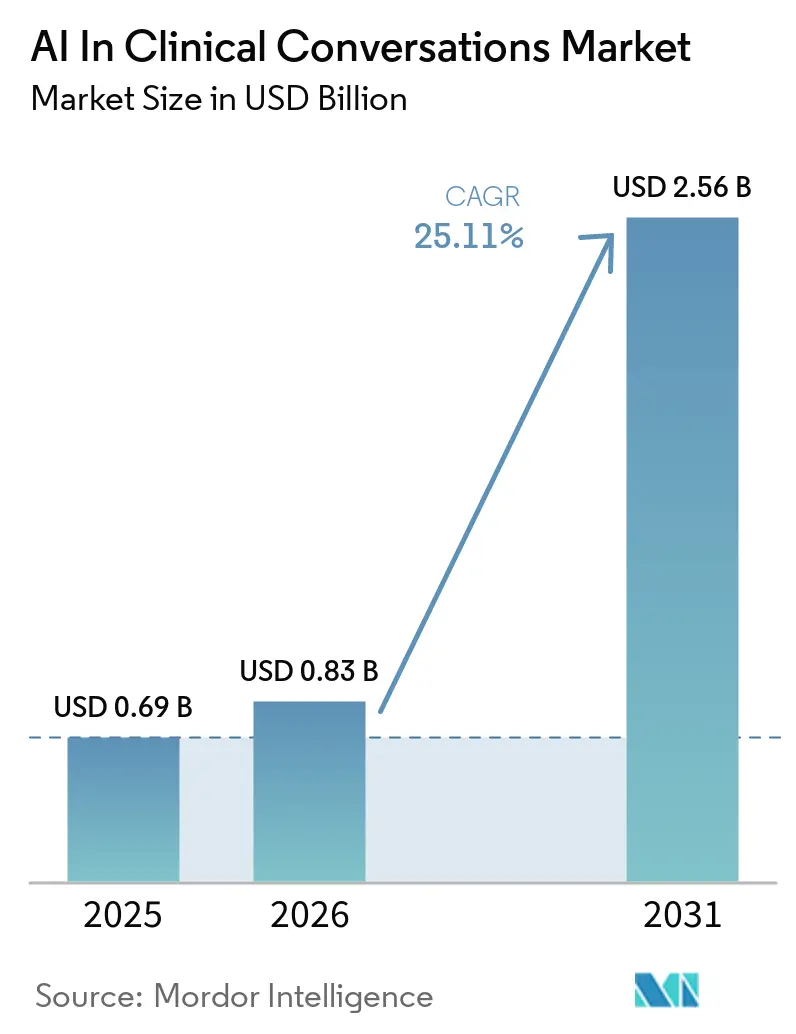

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 25.11% CAGR |

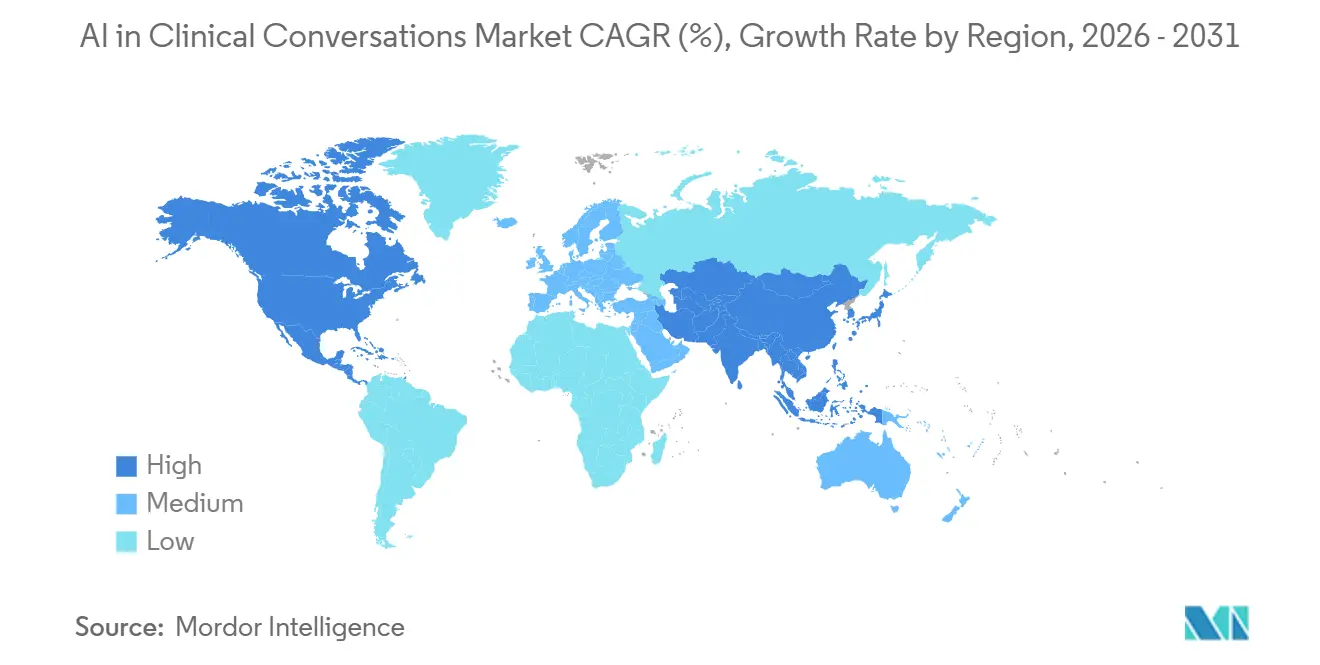

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

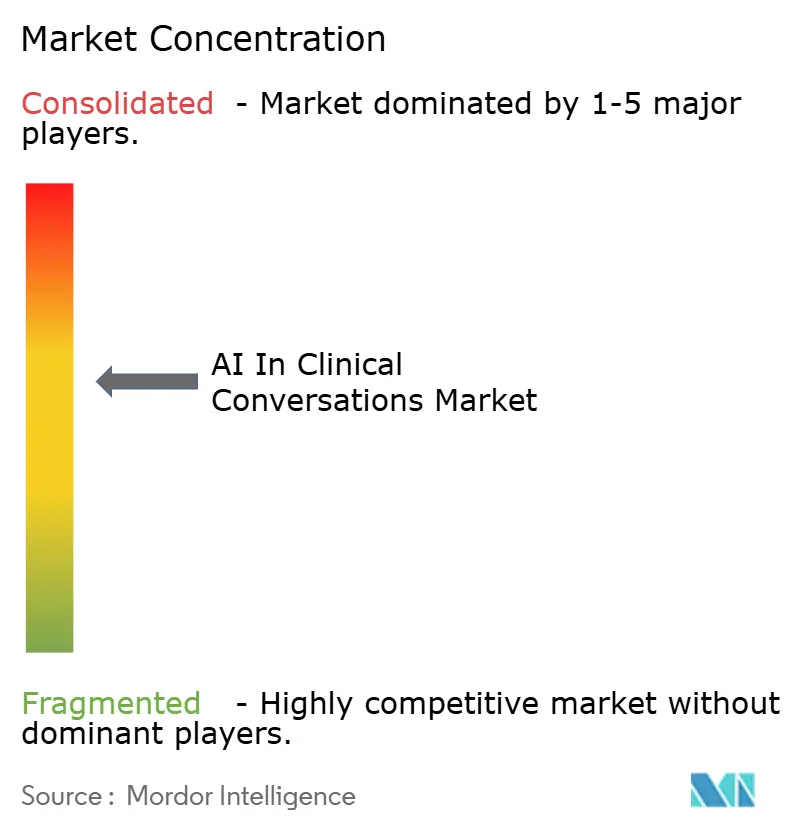

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Clinical Conversations Market Analysis by Mordor Intelligence

The AI in clinical conversations market size was USD 0.69 billion in 2025 and is projected to reach USD 2.56 billion by 2031, registering a 25.11% CAGR over 2026-2031. The growth path reflects how health systems convert ambient documentation into measurable gains in productivity and revenue cycle performance. Health providers in 2026 scale deployments where AI-generated notes reduce click burden and help clinicians complete documentation during the encounter, which improves on-time completion and reduces after-hours charting. Vendors shift from point tools to platforms that embed clinical documentation integrity and coding support inside end-to-end workflows. Native integrations with major electronic health record systems lower implementation friction and shorten time-to-value. Cloud-first stacks make it easier to distribute model updates and new features, which in turn supports faster expansion across clinical specialties and sites.

Key Report Takeaways

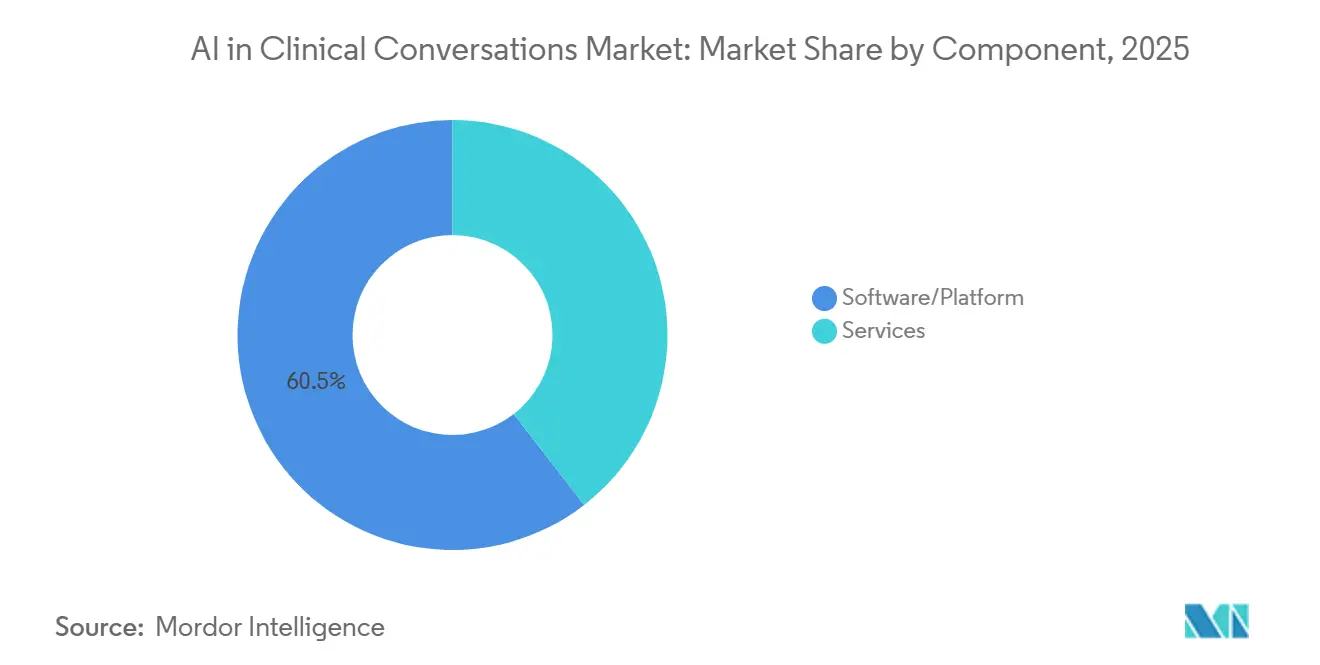

- By component, software/platform led with 60.54% revenue share in 2025 while software/platform is also projected to grow fastest at a 26.10% CAGR through 2031.

- By deployment mode, cloud-based accounted for 68.41% of 2025 revenue while cloud-based is also forecast to expand at a 27.12% CAGR to 2031.

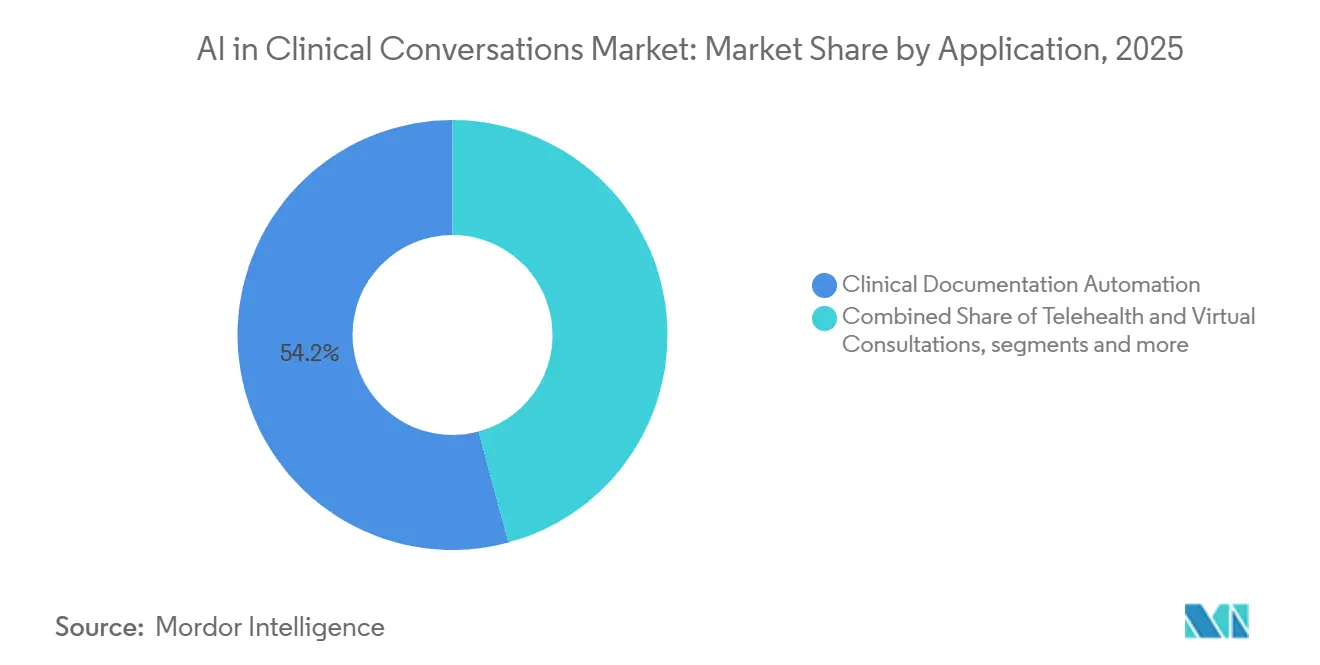

- By application, clinical documentation automation accounted for 54.24% of 2025 revenue while telehealth and virtual consultations are projected to grow fastest at a 27.34% CAGR through 2031.

- By end user, healthcare providers held 62.22% of 2025 revenue while healthcare payers are expected to grow at a 26.57% CAGR through 2031.

- By geography, North America held 45.67% of 2025 revenue while Asia-Pacific is expected to grow at a 27.23% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Clinical Conversations Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Clinician burnout relief and documentation time cuts enable rapid ROI | +5.2% | North America core, spillover to APAC and Europe | Short term (≤ 2 years) |

| Cloud-first EHR ecosystems accelerate ambient AI rollouts | +4.8% | Global, stronger in North America and Australia | Medium term (2-4 years) |

| Deep EHR integrations and vendor co-development shorten time-to-scale | +4.3% | North America, UK NHS, select APAC | Medium term (2-4 years) |

| North America's regulatory and funding tailwinds mature enterprise demand | +3.9% | North America, regulatory spillover to EU and APAC | Short to medium term (≤ 3 years) |

| Expansion from outpatient to inpatient or nursing or order workflows multiplies value | +4.1% | Global, early in North America and UK | Long term (≥ 4 years) |

| Point-of-care CDI or HCC capture turns ambient notes into revenue integrity wins | +2.9% | North America, value-based care markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Clinician Burnout Relief and Documentation Time Cuts Enable Rapid ROI

Clinician time savings translate into fewer after-hours tasks, steadier note completion, and better focus during patient encounters. Ambient systems that finalize notes during the visit reduce rework and improve provider satisfaction when embedded directly in established workflows. Early enterprise rollouts show improvements in on-time documentation and hours saved per day across large health systems. For example, a major health network using an ambient platform reported an increase in timely note completion to 87% with clinicians reporting daily time savings that compound across specialties, which illustrates how deployment at scale can improve consistency in clinical operations.[1]Commure, “Commure Ambient AI: Going Beyond the Note,” Commure, commure.comAs documentation shifts from memory-based typing to real-time capture, the likelihood of capturing complete clinical elements improves, which benefits coding quality and care team coordination. Health systems that standardize ambient documentation also create a foundation for expanding into adjacent workflows like clinical documentation integrity and structured data extraction.

Cloud-First EHR Ecosystems Accelerate Ambient AI Rollouts

Cloud-native services deliver consistent interfaces, rapid deployment options, and centralized security controls that suit regulated healthcare environments. One example is a cloud service that exposes unified software development kits across common programming languages, integrates with FHIR data stores, and can surface draft notes with suggested ICD-10 or CPT codes within seconds of document creation, which shortens the distance between clinical conversation and structured output. Organizations operating on the same cloud infrastructure can activate features with less middleware effort and benefit from synchronous model updates. Cloud EHR ecosystems can also distribute new automation to a large base of clinicians at once, as seen when practice networks adopt AI features inside their cloud-based clinical workflows. These advantages reduce cycle times for pilots and scale-up, which helps the AI in clinical conversations market sustain momentum across upgrades. The broader outcome is a shift from static installations to continuously improving services that reach clinicians with minimal disruption.

Deep EHR Integrations and Vendor Co-Development Shorten Time-To-Scale

Health systems emphasize integration depth because it determines whether AI fits into existing workflows without extra clicks or toggling. Enterprise buyers are awarding multi-year partnerships based on evidence from multi-specialty pilots, which shows that configuration, governance, and change management are as important as model accuracy. For instance, following extensive pilots across many specialties, a leading U.S. provider organization entered a multi-year agreement with a platform vendor whose roadmap includes features that read and write across EHR records to enrich note quality and streamline documentation steps.[2]Fernando Cowan, “Ambience Healthcare Review 2026 — Pros, Cons & Who It’s Best For,” DeepCura, deepcura.comNew features launched in 2026 apply context-awareness to the full longitudinal chart, which helps clinicians reconcile prior notes and diagnostics within the flow of documentation. Health systems that deployed AI assistants across hospitals and clinics highlighted the value of single-stack integrations for both inpatient and outpatient settings. On the payer and plan side, buyers reported five-day average deployment cycles with automated onboarding instead of months of consulting, which signals how templated integration playbooks can compress time-to-value in the AI in clinical conversations market.

North America's Regulatory and Funding Tailwinds Mature Enterprise Demand

Large enterprises in North America operate under established privacy and security requirements, which pushes vendors to align product design with auditability, access controls, and traceability. This regulatory context favors platforms that integrate AI functions within existing clinical systems, since unified logging and permissions reduce compliance complexity for health systems. Cloud providers building healthcare services have also emphasized features that support data governance, identity, and model management, which makes procurement and rollout more predictable for technology teams. As budget cycles in 2026 prioritize automation that lifts throughput and supports revenue integrity, executive sponsors are more willing to sign multi-year agreements tied to measurable operational outcomes. Vendor co-development efforts with large providers are expanding the scope from basic note creation to whole-workflow orchestration, which aligns adoption with enterprise goals across clinical and financial operations. The net effect for the AI in clinical conversations market is a pivot from pilots to enterprise programs with clear governance and defined adoption milestones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data privacy, consent, and security requirements increase deployment friction | -3.7% | EU and UK GDPR strict, California, global spillover | Short term (≤ 2 years) |

| EHR certification, change management, and workflow redesign add complexity | -2.8% | Global, acute in fragmented markets in EU and APAC emerging | Medium term (2-4 years) |

| Clinical liability and auditability demands raise bar for verifiable outputs | -1.9% | North America litigation-heavy, UK NHS governance focus | Short to medium term (≤ 3 years) |

| Audio quality, acoustics, and rural connectivity limit reliability in-field | -1.4% | Rural North America, India, Southeast Asia, Africa | Medium to long term (2-5 years) |

| Source: Mordor Intelligence | |||

Data Privacy, Consent, and Security Requirements Increase Deployment Friction

Compliance obligations differ by region and facility type, which increases the cost and time needed to standardize deployments. Enterprise buyers ask vendors to support granular consent, data minimization, and robust audit trails across all AI features. In Europe and the UK, strict consent standards and data localization expectations influence product design and rollout pacing. Providers and vendors must align on clear notices to patients when AI tools are used, with predictable escalation paths for human review of outputs. Cloud providers that offer healthcare services have emphasized unified SDKs, standardized security controls, and structured connectors to clinical data to streamline compliance, which helps reduce integration variability across environments. Organizational readiness remains a gating factor as legal, privacy, and clinical leadership teams collaborate on policies for responsible use within the AI in clinical conversations market.

EHR Certification, Change Management, and Workflow Redesign Add Complexity

Many health systems require clinical safety assessments, local risk documentation, and staff training before new tools go live. UK buyers, for instance, apply formal guidance for AI scribes that drives due diligence and safety casework during procurement and rollout, which extends timelines but ensures governance and patient protections.[3]Heidi Health, “New NHS Guidance on AI Scribes: What It Means for You,” Heidi Health, heidihealth.comSuccess depends on advanced integration that reduces clicks and streamlines tasks across a range of EHR environments. Vendors with broad integration engines that connect to dozens of medical record systems have shown how link methods across HL7, application programming interfaces, and front-end integration can carry implementations across heterogeneous estates, though each connection requires validation and maintenance. Health systems that awarded multi-year contracts after competitive pilots emphasize change management and clinician onboarding, since adoption depends on alignment with daily workflows as much as on raw transcription accuracy. Governance and safety work sit alongside new AI literacy efforts, as organizations train staff to understand failure modes, escalate issues, and calibrate appropriate use. These steps can increase time-to-deploy in the near term, yet they create stronger foundations for durable scaling in the AI in clinical conversations market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software/Platforms Embed Revenue Cycle Intelligence

Software/Platform solutions captured 60.54% of 2025 revenue and are projected to grow at a 26.10% CAGR through 2031 as buyers prefer configurable platforms over implementation-heavy services. The AI in clinical conversations market sees software vendors bundling clinical documentation integrity, coding assistance, and payer policy logic into unified offerings that address both clinical and financial objectives. Platform designs that surface documentation suggestions and code prompts within the EHR have expanded addressable value beyond basic note creation. Some products report material revenue lift per clinician from better coding completeness, which aligns financial benefits with daily workflows in documentation. Platform momentum is also visible in deployment speed, where health plans report five-day average onboarding cycles that compress what used to require months of consulting and custom work in the AI in clinical conversations market.

The evolution from passive to proactive systems continues as vendors combine ambient capture with agentic capabilities that can initiate EHR actions and suggest structured codes. One large U.S. network selected a combined ambient assistant and dictation solution for hospitals and clinics, which shows buyers prefer integrated toolchains over point tools when scaling across service lines. Vendors that emphasize whole-chart awareness and bidirectional EHR interactions differentiate on speed and accuracy of chart updates as well as on the completeness of captured clinical elements. As adoption grows, the AI in clinical conversations industry is seeing stronger demand for configurable templates, analytics, and controls that support compliance and operational reporting. The segment’s direction favors platforms with modular components that administrators can switch on and off as governance matures. In 2026, this platform shift underpins the software segment’s role as the core driver of the AI in clinical conversations market.

By Deployment Mode: Cloud Infrastructure Unlocks Real-Time Model Updates

Cloud-based deployment accounted for 68.41% of 2025 revenue and is projected to grow at a 27.12% CAGR through 2031 as health systems prioritize services that can scale without on-premises hardware refreshes. Cloud architectures centralize security, identity, and logging, which supports audit and compliance needs in regulated environments. One healthcare cloud service offers unified software development kits across languages and integrates with a healthcare data lake to pull clinical context during documentation, which helps deliver near real-time outputs including codes within seconds of generating a clinical document. These capabilities align with the operational goal of having ambient outputs appear in the right field at the right time with minimal middleware. The AI in clinical conversations market benefits when updates ship to thousands of clinicians at once, which cloud platforms can achieve by pushing new features and models across tenants without site-by-site patching.

The business case for cloud deployment also links to flexibility in scaling up new specialties and handling variable demand without capital outlays. Practice networks adopting cloud EHRs with AI features report faster access to automation layers that support clinical workflows, which reduces internal IT effort during rollouts. As health plans and revenue cycle firms expand transaction automation, several companies have raised capital to scale cloud-native systems that orchestrate operational workflows at high volume. Payment integrity providers and coding automation companies also describe expanding cloud operations to support payer and provider clients, which reinforces cloud’s role as the default deployment path in this segment of the AI in clinical conversations market.

By Application: Telehealth Consults Drive Fastest Adoption Velocity

Clinical Documentation Automation represented 54.24% of 2025 application revenue as the foundational entry point for many health systems. The AI in clinical conversations market built initial credibility on reducing documentation time and improving completeness, which laid the groundwork to expand into downstream processes. Telehealth and Virtual Consultations, the fastest-growing application at a 27.34% CAGR, benefit from greenfield workflows where voice capture and AI summarization can be embedded natively in the visit experience. Buyers prioritize ambient capture that produces structured notes and code suggestions as sessions conclude, which helps standardize outputs across high-volume virtual encounters. Platform vendors continue to add features for specialty templates and structured summaries that reduce rework when documentation moves to the chart. As models improve speech handling and medical terminology across accents and background conditions, telehealth workflows that rely on mixed audio environments see better output quality. The balance of 2026 adoption indicates many organizations will keep Clinical Documentation Automation as the anchor while adding telehealth-specific automation to expand the surface area of value in the AI in clinical conversations market.

Telehealth growth also links to enterprise preferences for integrated stacks that cover virtual and in-person visits. Buyers lean toward solutions that can operate across devices and settings with the same identity and logging controls, since unified governance simplifies audits and reduces training time. Vendors with agentic capabilities that draft notes and propose codes in real time also position well for virtual visit settings where clinicians expect outcomes during the session. These dynamics reinforce the rapid adoption of virtual consultation automation as a complement to documentation in brick-and-mortar clinics. Over 2026, advances in context awareness and bidirectional EHR connectivity will continue to lift the usefulness of ambient outputs in virtual sessions. This momentum supports sustained growth in telehealth applications within the AI in clinical conversations market.

By End User: Healthcare Payers Automate Prior Authorization at Scale

Healthcare Providers led 2025 with 62.22% of revenue as hospitals and physician groups targeted clinician time savings and revenue cycle accuracy. Early deployments focused on specialties with heavy documentation loads and clear coding pathways. The AI in clinical conversations market is now seeing the payer segment accelerate as plans adopt AI to triage reviews, structure unstructured documents, and standardize clinical criteria application. Health plan buyers report rapid deployment cycles and high user satisfaction for tools that reduce clinical review workloads and shorten determination timelines. As payers automate pre-claim and post-claim integrity checks, companies in payment integrity and revenue cycle automation have scaled cloud operations to support large volumes and deliver measurable reductions in manual effort.

Healthcare Payers also benefit from structured outputs that align with coding and policy criteria, which increases throughput while preserving auditability. Several operational AI companies have expanded to orchestrate multi-step processes that combine ambient extraction with rules-based and learning-based decision support across claims and authorizations. As these capabilities mature, providers and payers are converging on platforms that share a common substrate for documentation, coding, and policy logic. This convergence supports value on both sides of the transaction when definitions and mappings align. Across 2026, the AI in clinical conversations industry is expected to continue shifting into higher-stakes decisions under tighter controls, which further boosts interest among payer organizations seeking reliable automation. The combination of rapid onboarding and measurable workload reduction underpins the end-user trajectory in this segment of the AI in clinical conversations market.

Geography Analysis

North America held 45.67% of the AI in clinical conversations market size in 2025, supported by enterprise-scale deployments and strong integration with incumbent EHR ecosystems. Buyers in 2026 favor platforms embedded inside clinical systems to reduce workflow friction and to centralize logging and access controls. Cloud-native healthcare services that plug into clinical data stores and can surface timely documentation and coding outputs show clear appeal for large multi-site providers. Ambient products that improve on-time note completion and save hours per day are used as evidence of value during enterprise procurement decisions. As budgets prioritize operational gains and revenue capture, platforms that link ambient documentation with coding accuracy and billing completeness receive broader consideration. The region’s implementation capacity supports faster scale-up once pilots conclude, which helps the AI in clinical conversations market compound adoption momentum.

Asia-Pacific is the fastest growing region at a 27.23% CAGR through 2031, reflecting strong demand for tools that reduce documentation burdens in resource-constrained settings. Health systems in 2026 emphasize cloud EHRs, localization, and mobile-first workflows that embed AI capture into routine clinical encounters. Growth is supported by investments in digital health infrastructure and the need to stretch workforce capacity through automation. Vendors that support multilingual environments and device-agnostic capture position well for clinics that handle diverse patient populations. The region’s mix of public and private providers makes value articulation around time savings and throughput gains important, since many sites must serve more patients without large workforce additions. As models improve audio handling and medical terminology recognition in varied settings, organizations are more willing to deploy ambient tools in frontline care. The AI in clinical conversations market in Asia-Pacific is expected to continue outpacing other regions as best practices from early adopters spread across networks.

Europe’s adoption reflects formal digital health governance and a fragmented EHR landscape that demands strong integration strategies. National health systems and regional collaborations publish guidance that shapes procurement and safety evaluations for AI documentation tools, which brings clarity to buyers and vendors. In the UK, an AI scribe self-certification registry and related guidance help signal product maturity and compliance alignment to provider organizations reviewing options. Continental Europe continues to benefit from EHR platform partnerships that embed ambient features within hospital systems, as shown by collaborations to expand integrated ambient documentation across multiple countries. Vendors entering markets like Germany emphasize the ability to connect with diverse hospital information systems through multiple integration methods, which illustrates how product flexibility matters in fragmented environments. As these practices mature, the AI in clinical conversations market in Europe is expected to accelerate adoption within structured frameworks that balance innovation with patient safety.

Competitive Landscape

The AI in clinical conversations market remains moderately fragmented in 2026, although consolidation is underway as platform vendors broaden scope beyond transcription. Three clusters define competitive positioning. First, EHR-native incumbents and cloud providers integrate ambient services inside core clinical systems and data platforms to centralize security and accelerate adoption. Second, platform specialists provide cross-EHR deployments with agentic capabilities that draft notes, summarize charts, and propose codes in real time, which helps reduce friction across varied workflows. Third, niche leaders focus on high-documentation specialties such as oncology and demonstrate scale in capturing visits and standardizing outputs for specific clinical areas.

Competitive edges depend on integration depth, workflow fit, and proof of measurable outcomes. Vendors that interpret the full longitudinal chart and support bidirectional EHR interactions are positioned to reduce toggling and improve documentation completeness. Health systems that adopt combined ambient and dictation stacks across hospitals and clinics underscore the preference for unified solutions that can standardize outputs at enterprise scale. Cloud EHRs that roll out AI capabilities across large clinician networks illustrate how distribution advantages can influence vendor selection for buyers prioritizing speed and manageability. As buyers expand evaluation criteria from transcription accuracy to revenue cycle support and governance controls, platforms with configurable policy logic and enterprise-grade security gain traction in the AI in clinical conversations market.

Capital formation and M&A activity signal strategic bets on operating platforms and revenue cycle outcomes. Several operational and revenue cycle AI companies have raised new capital to scale automation that coordinates multi-step tasks across health systems. Payment integrity vendors also report momentum in pre-claim analytics and risk detection, expanding demand among payer clients who want to reduce manual reviews. In Europe, a primary care-focused vendor achieved strong national penetration and was acquired to expand a clinician-first documentation approach across new markets, which shows how regional champions can become platforms for broader continental growth. New entrants addressing financial operations have also secured funding to build automation layers for the healthcare revenue stack, which complements clinical documentation platforms in enterprise roadmaps. These shifts point to tighter linkages between documentation quality, coding completeness, and financial outcomes as deciding factors in vendor selection within the AI in clinical conversations market.

AI In Clinical Conversations Industry Leaders

Microsoft

Abridge

Suki AI

Augmedix

Ambience Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Abridge expanded clinical decision support capabilities through partnerships with Wolters Kluwer's UpToDate, NEJM Group, and the American Medical Association, integrating context-aware evidence-based recommendations directly within ambient documentation workflows to reduce cognitive load and improve clinician confidence. This signals market evolution from passive transcription toward active clinical intelligence.

- September 2025: Seattle Children’s Hospital deployed Abridge’s AI platform across the organization to streamline clinical documentation by automatically capturing and transcribing provider–patient conversations. The system generates structured draft clinical notes that are then seamlessly integrated into the hospital’s EHR system.

- July 2025: Regard enhanced its AI platform to integrate EHR chart data with physician–patient conversations, improving the accuracy of clinical documentation and enabling more proactive diagnosis support.

Global AI In Clinical Conversations Market Report Scope

As per the scope of the report, AI in clinical conversations refers to the use of natural‑language processing and machine‑learning systems that capture, interpret, and generate clinician–patient dialogue to automate documentation, surface insights, and support real‑time clinical decision‑making. It transforms spoken or written clinical exchanges into structured data, reduces administrative burden through ambient note‑taking, and enhances communication accuracy and workflow efficiency across care settings.

The AI in clinical conversations market is segmented by component, deployment mode, application, end user, and geography. By component, the market is segmented into software/platform and services. By deployment mode, the market is segmented into cloud-based, on-premises, and hybrid. By application, the market is segmented into clinical documentation automation, telehealth & virtual consultations, administrative & coding support, training & quality assurance, and others. By end-user, the market is segmented as healthcare providers, healthcare payers, and others. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| Software/Platform |

| Services |

| Cloud-based |

| On-Premises |

| Hybrid |

| Clinical Documentation Automation |

| Telehealth and Virtual Consultations |

| Administrative and Coding Support |

| Training and Quality Assurance |

| Others |

| Healthcare Providers |

| Healthcare Payers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software/Platform | |

| Services | ||

| By Deployment Mode | Cloud-based | |

| On-Premises | ||

| Hybrid | ||

| By Application | Clinical Documentation Automation | |

| Telehealth and Virtual Consultations | ||

| Administrative and Coding Support | ||

| Training and Quality Assurance | ||

| Others | ||

| By End User | Healthcare Providers | |

| Healthcare Payers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the AI in clinical conversations market growing through 2031

It is projected to expand at a 25.11% CAGR from 2026 to 2031, rising from USD 0.69 billion in 2025 to USD 2.56 billion by 2031.

Which component leads adoption in the AI in clinical conversations market

Software/Platform leads with 60.54% of 2025 revenue and also shows the fastest projected growth at 26.10% CAGR to 2031.

What deployment approach is winning in the AI in clinical conversations market

Cloud-based models dominate with 68.41% of 2025 revenue and the strongest growth outlook at a 27.12% CAGR, due to rapid rollout and centralized updates.

Which applications are scaling fastest for the AI in clinical conversations market

Clinical Documentation Automation holds the largest share at 54.24% in 2025, while Telehealth and Virtual Consultations is the fastest growing at a 27.34% CAGR.

Page last updated on: