AI In Medical Coding Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

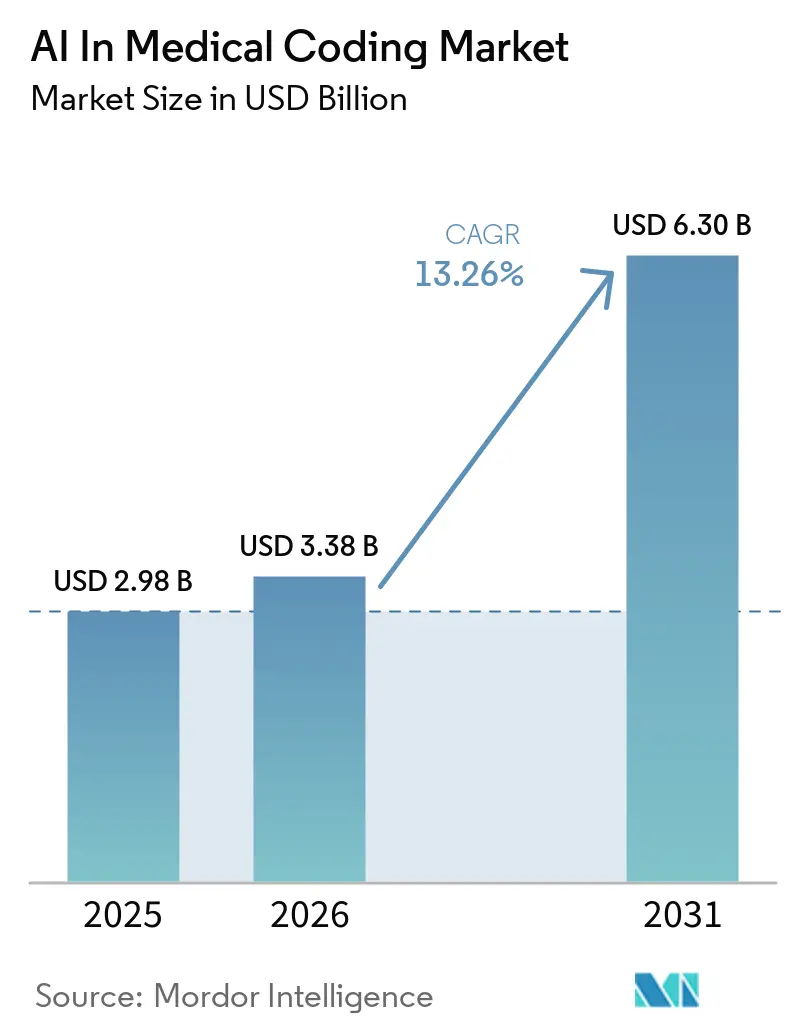

| Market Size (2026) | USD 3.38 Billion |

| Market Size (2031) | USD 6.30 Billion |

| Growth Rate (2026 - 2031) | 13.26% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

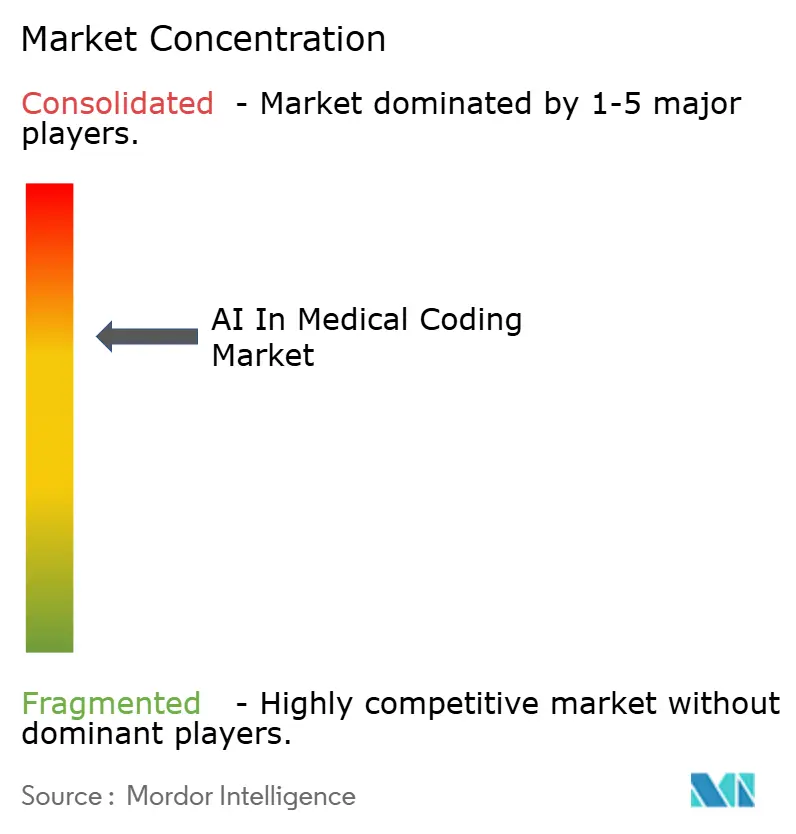

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI In Medical Coding Market Analysis by Mordor Intelligence

The AI in medical coding software market size is expected to grow from USD 2.98 billion in 2025 to USD 3.38 billion in 2026 and is forecast to reach USD 6.30 billion by 2031 at a 13.26% CAGR over 2026-2031. Heightened mainstream hospital adoption of computer-assisted coding (CAC) suites, rising reliance on cloud GPU inference, and tighter value-based-care reimbursement rules are reinforcing demand. North America currently dominates because 71% of U.S. hospitals deployed predictive AI in 2024, a five-point jump in a single year. ICD-11 migration is accelerating investment across Europe and Asia-Pacific, where 72 World Health Organization (WHO) member states were actively rolling out the new code set by 2024. Large language models (LLMs) fine-tuned on clinical corpora now achieve 68.1% top-1 accuracy for the 30 highest-volume diagnosis-related groups (DRGs), trimming manual abstraction costs by 70%. Cybersecurity concerns after the February 2024 Change Healthcare breach are prompting payers to diversify coding vendors and to explore on-premise GPU clusters despite capital-cost headwinds.

Key Report Takeaways

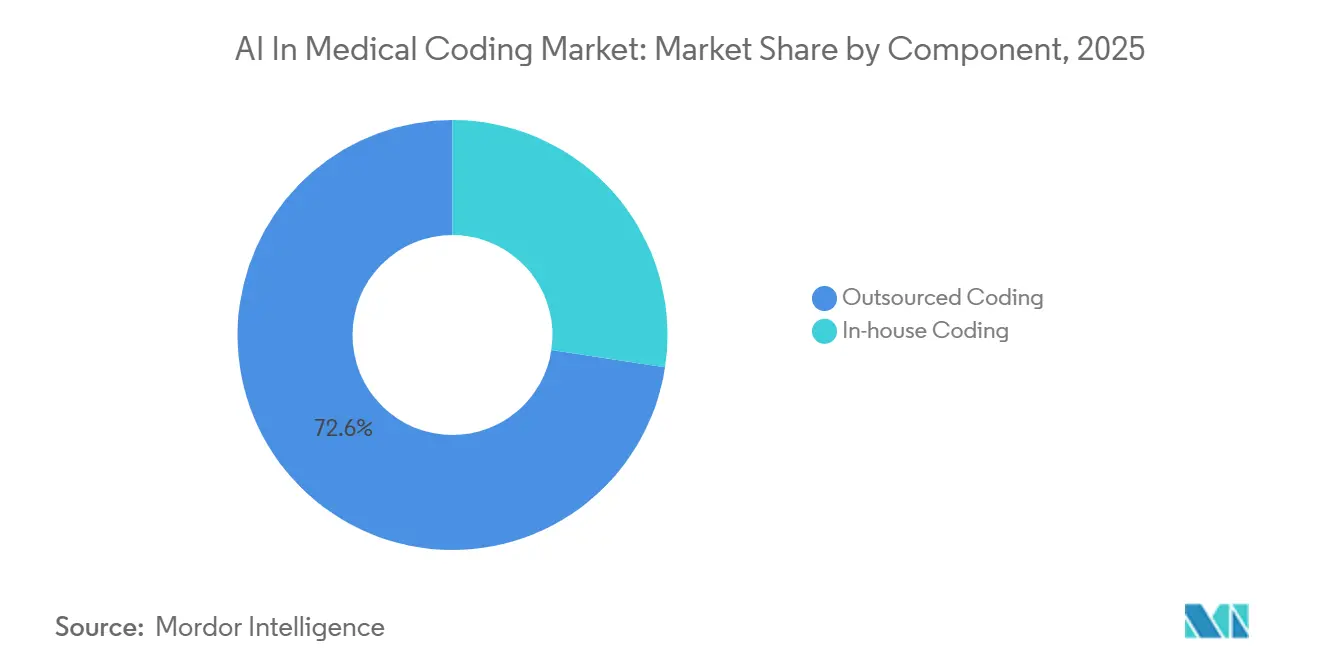

- By component, outsourced coding led with 72.60% of the AI in medical coding software market share in 2025 and is projected to expand at a 15.45% CAGR through 2031.

- By deployment mode, cloud solutions captured 53.90% of the AI in medical coding software market size in 2025 and are projected to expand at a 15.34% CAGR to 2031.

- By application, automated code assignment captured 46.09% in 2025, whereas fraud detection & compliance monitoring recorded the fastest trajectory at 16.15% CAGR to 2031.

- By end user, healthcare providers held 57.90% revenue in 2025, whereas payers recorded the fastest trajectory at 15.09% CAGR to 2031.

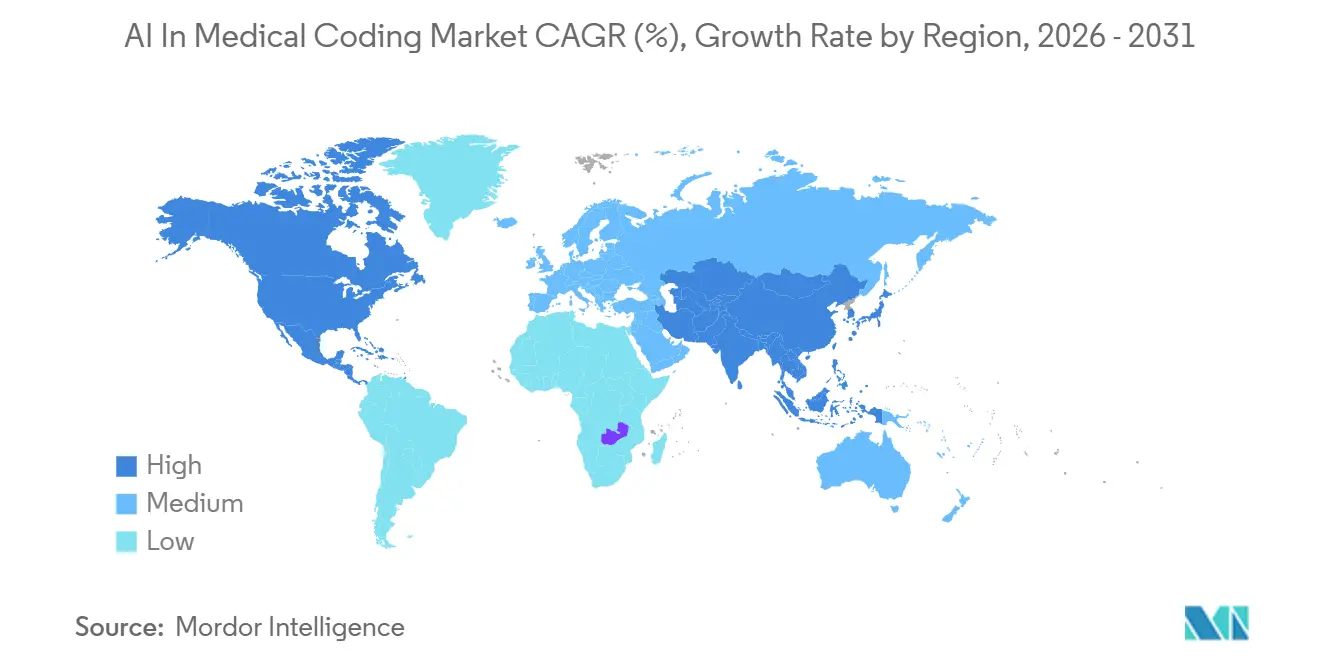

- By geography, North America retained a 51.42% share in 2025; Asia-Pacific is the quickest mover, growing at a 15.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI In Medical Coding Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream hospital adoption of CAC suites | +3.2% | North America, Europe | Short term (≤ 2 years) |

| ICD-11 migration pressures in Europe & APAC | +2.1% | Europe, Asia-Pacific, spill-over to MEA | Medium term (2-4 years) |

| Value-based-care reimbursement analytics | +2.8% | North America, Europe | Medium term (2-4 years) |

| GPT-4-level LLM fine-tuning on clinical data | +2.4% | Global | Short term (≤ 2 years) |

| Ambient scribe data flowing into coding | +2.0% | North America, Asia-Pacific | Short term (≤ 2 years) |

| National payer AI-audit incentives | +1.8% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream Hospital Adoption of Computer-Assisted Coding Suites

U.S. hospital billing-automation penetration jumped from 36% in 2023 to 61% in 2024 as CFOs aimed to recapture 30-40% margins previously ceded to offshore vendors. Ambient documentation systems used over 2.5 million times at Kaiser Permanente generated structured notes that flow directly into CAC engines, eliminating manual lag. Multi-facility health systems now consolidate coding in shared-services centers that run cloud-native AI platforms. Academic medical centers already code 60-70% of encounters autonomously, whereas rural sites still depend on assisted workflows. This gradient underscores why in-house coding is forecast to outgrow outsourcing through 2031.

ICD-11 Migration Pressures in Europe & APAC

Germany mandated ICD-11 for inpatient claims in January 2025, compelling hospitals to upgrade coding engines or risk withheld reimbursements [1]World Health Organization, “ICD-11 Implementation Status,” who.int. India embedded ICD-11 into its Ayushman Bharat Digital Mission in 2024, exposing a 500 million-patient pool to API-ready cloud solutions. ICD-11’s semantic foundation improves LLM mapping accuracy, reducing manual overrides by up to 40%. Legacy vendors hard-coded to ICD-10 are losing share to cloud entrants able to push code-set updates instantly. Asia-Pacific’s 15.63% CAGR reflects this leapfrog dynamic.

Value-Based-Care Reimbursement Analytics Integration

The CMS HCC V28 model took effect in 2024, heightening the revenue stakes tied to coding specificity [2]Centers for Medicare & Medicaid Services, “Risk Adjustment Data Validation Final Rule,” cms.gov. Medicare Advantage plans that under-code diagnoses forfeit millions in monthly capitations, while over-coding now triggers repayment extrapolations across entire contracts. AI platforms embed real-time gap analysis that lifts risk-adjustment factor (RAF) scores 8-12% without up-coding. Healthacre payers therefore represent the fastest-growing end-user cohort at 15.09% CAGR to 2031. The February 2024 Change Healthcare cyberattack, however, revealed concentration risk and opened the door for rivals offering decentralized audit tools.

GPT-4-Level LLM Fine-Tuning on Clinical Corpora

Fine-tuning on the MIMIC-IV dataset raised ICD-10 accuracy from 29.7% to 62.6%; GPT-4 derivatives now reach 68.1% top-1 DRG precision. Microsoft-Nuance DAX Copilot uses this capability to suggest codes during the encounter, dropping per-chart labor costs from USD 3-7 to USD 0.50-1.50. Oracle Health embedded parallel functionality in Cerner Millennium late in 2024 . Inference economics remain the constraint: each GPT-4 call costs USD 0.10-0.20, so smaller hospitals are trialing quantized Llama-3 models on local GPU stacks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Algorithmic bias scrutiny under EU AI Act | -1.5% | Europe, spill-over North America | Medium term (2-4 years) |

| Shortage of AI-literate HIM staff | -1.2% | Global, acute North America | Long term (≥ 4 years) |

| Proprietary EHR data-sharing lock-ins | - 0.9% | North America, Europe | Long term (≥ 4 years) |

| Rising GPU-cloud inference costs | - 0.7% | Global, acute APAC, MEA | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Algorithmic Bias Regulatory Scrutiny (EU AI Act)

Since August 2024, high-risk medical decision-support systems must pass third-party bias audits or face fines up to EUR 35 million or 7% of turnover. Vendors are adding explainability layers that delay go-lives 6-12 months. Germany’s BfArM issued draft guidance in 2025 requiring yearly audits, concentrating share with resource-rich incumbents able to absorb compliance costs.

Shortage of AI-Literate Health Information Management Staff

Thirty percent of AHIMA-certified coders plan retirement within five years, and only 23% feel ready to oversee AI workflows. Hospitals deploying autonomous coding still cite 15-20% error rates when reviewers lack prompt-engineering skill. India’s National Health Authority launched an AI-coder certification in 2025, creating offshore talent pipelines but not yet filling domestic gaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Margin-Reclaiming Shift Toward In-House Platforms

Outsourced coding captured 72.60% AI in the medical coding software market share in 2025 and is projected to expand at a 15.45% CAGR, as hospitals historically relied on offshore teams charging USD 2-4 per record. Further, the in-house option is also expanding because ambient data and GPT-4 engines now let large delivery systems achieve 70% autonomous coding at USD 0.50–1.50 per chart. CFOs calculate the break-even at 8,000-10,000 annual encounters, prompting multi-facility groups such as the Cleveland Clinic to insource during 2024-2025.

In contrast, specialty areas like oncology still depend on outsourced coders who manage nuanced staging rules. Outsourcing vendors are fighting back by purchasing AI start-ups. GeBBS acquired a Bengaluru LLM shop in 2025 to offer hybrid models where offshore staff validate machine suggestions. The HIM retirement wave projected through 2029 could swing momentum cyclically back toward external providers if health systems cannot replenish talent.

By Deployment Mode: Cloud Leads on GPU Economics

Cloud-based deployment type held 53.90% of the AI in medical coding software market size in 2025 thanks to amortized GPU inference and vendor preference for subscription revenue. Reserved-instance contracts that cap monthly spend at USD 3,000-5,000 make the model viable for mid-tier hospitals. On-prem solutions survive in academic centers obligated to meet strict data-sovereignty rules and in systems that already invested in local GPU clusters.

Hybrid strategies are emerging in Europe: ambient capture and language modeling stay in the vendor cloud, but final code generation happens on internal servers to satisfy GDPR. Even so, less than 10% of deployments followed this path by early 2026. Asia-Pacific’s double-digit CAGR indicates many hospitals will leapfrog directly to cloud coding, mirroring their earlier mobile banking adoption curve.

By Application: Risk Adjustment Coding Rises Fastest

Automated code assignment still accounts for the majority of revenue, yet risk-adjustment coding is posting the highest trajectory. AI audit suites that close hierarchical condition category (HCC) gaps are helping payers avoid seven-figure clawbacks under the 2024 RADV extrapolation protocols. Platforms that combine real-time CDI prompts with prospective RAF scoring gain rapid traction, especially in Medicare Advantage.

Fraud-detection modules rank next in growth as the Office of Inspector General identified USD 31.2 billion in improper fee-for-service payments for 2024, 40% tied to coding mistakes. Prior authorization and denial-management features round out the suite, though their adoption lags until interoperability bottlenecks ease. Europe’s tighter transparency rules slow the rollout of unsupervised anomaly-detection algorithms, trimming short-term revenue potential there.

By End User: Payers Overtake Providers in Growth Pace

Healthcare providers commanded 57.90% spender share in 2025, driven by the need to clear documentation backlogs that delay revenue cycles. Healthcare payers, however, show a 15.09% CAGR through 2031 as Medicare Advantage and commercial insurers fortify defenses against audit penalties. UnitedHealth, Humana, and Centene each rolled out GPT-4-assisted risk-adjustment suites across all 2025 plan years, aiming to catch under-coding in near real time.

Third-party medical-billing firms compete by bundling AI coding with eligibility verification and claims editing, yet margin pressure is forcing consolidation into larger revenue-cycle service groups. Government health agencies, while a small slice today, represent latent upside once funding for automation loosens in Medicaid and Veterans Affairs.

Geography Analysis

North America held 51.42% AI in medical coding software market share in 2025 on the back of 71% predictive-AI hospital penetration and strict CMS audit rules. Canada’s Ontario Health and British Columbia Health introduced pilot programs in 2025 targeting 20% administrative cost savings, while Mexico’s IMSS issued a cloud CAC tender covering 1,500 sites. The 21st Century Cures Act has begun loosening EHR data silos, though Epic and Oracle continue charging steep API fees.

Europe’s landscape is defined by ICD-11 migration and the EU AI Act [3]European Parliament, “Artificial Intelligence Act Text,” artificialintelligenceact.eu. Germany compelled hospitals to transmit ICD-11 codes from January 2025, and the U.K.’s National Health Service earmarked GBP 50 million for AI coding pilots across 30 trusts. Nordic countries, already digital frontrunners, are experimenting with edge deployments to comply with stringent data-localization laws. Southern Europe is catching up through the EU Digital Europe Programme grants that fund cloud-based solutions.

Asia-Pacific is projected to post the fastest 15.63% CAGR through 2031. India incorporated ICD-11 into its Ayushman Bharat Digital Mission, unlocking the world’s largest single-payer dataset after China. Australia mandated ICD-11 for public hospitals beginning July 2025, while China’s 14th Five-Year Plan designates AI coding as a smart-hospital pillar. South Korea’s National Health Insurance piloted coding bots in 2025 to mitigate chronic medical-records staffing shortages. Emerging Southeast Asian markets remain early-stage but benefit from rapid cloud-infrastructure build-outs.

Competitive Landscape

Market concentration is moderate. Microsoft-Nuance, 3M (spun off as Solventum in April 2024), and UnitedHealth’s Optum division collectively leverage entrenched EHR partnerships to retain a sizeable installed base. Microsoft-Nuance DAX Copilot went live at 200+ U.S. health systems by March 2024, evidencing the power of bundled ambient capture plus coding suggestion. Solventum’s 360 Encompass maintains traction among integrated delivery networks still wary of cloud dependencies.

Cloud-native challengers, notably EZDI, Dolbey, and Streamline Health, win accounts by offering open APIs that bypass Epic lock-ins. Funding rounds exceeding USD 50 million for scribe-centric players Abridge and Suki during 2024-2025 underscore investor appetite for front-end innovations that feed coding automation. Compliance costs tied to the EU AI Act favor large incumbents that can fund annual bias audits, potentially stalling disruptor expansion in Europe.

Technology differentiation turns on LLM fine-tuning accuracy, GPU inference optimization, and FHIR-based interoperability. Quantized 8-bit models running on NVIDIA H100 chips dropped unit compute costs 60%, a benefit quickly productized by newer vendors. Incumbents counter with integrated workforce-training services that address the looming HIM retirement cliff; GeBBS and EZDI both added certification academies in 2025 to strengthen client retention.

AI In Medical Coding Industry Leaders

Optum, Inc.

Oracle Corporation

Solventum

Nuance Communications, Inc. (Microsoft Corporation)

IBM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Oracle introduced an AI application suite automating prior authorization, coding, and claims, touting potential USD 200 billion annual U.S. administrative savings.

- August 2025: HandsOn Global Management took full control of Aidéo Technologies via preferred-stock issuance, expanding an autonomous-coding platform that uses NLP and real-time analytics across emergency medicine and radiology.

- June 2025: Ambience Healthcare unveiled an AI model that out-performed board-certified physicians by 27% on ICD-10 accuracy, validated by 18 clinical experts testing complex scenarios.

Global AI In Medical Coding Market Report Scope

According to the report’s scope, AI in medical coding includes artificial intelligence–driven solutions that automate the assignment of standardized medical codes to diagnoses, procedures, and clinical documentation. These solutions improve coding accuracy, reduce manual effort, accelerate billing cycles, ensure regulatory compliance, and enhance revenue cycle efficiency for healthcare providers.

The AI in medical coding market is segmented into component, deployment mode, application, end-user, and geography. By component, the market is segmented into in-house coding and outsourced coding. By deployment, the market is segmented into cloud-based, on-premise, and hybrid. By application, the market is segmented into automated code assignment, clinical documentation improvement (CDI), risk adjustment coding, fraud detection & compliance monitoring, and others. By end-user, the market is segmented into healthcare providers, healthcare payers, medical billing companies, and government firms. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| In-house Coding |

| Outsourced Coding |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Automated Code Assignment |

| Clinical Documentation Improvement (CDI) |

| Risk Adjustment Coding |

| Fraud Detection & Compliance Monitoring |

| Others |

| Healthcare Providers |

| Healthcare Payers |

| Medical Billing Companies |

| Government Firms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | In-house Coding | |

| Outsourced Coding | ||

| By Deployment Mode | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Application | Automated Code Assignment | |

| Clinical Documentation Improvement (CDI) | ||

| Risk Adjustment Coding | ||

| Fraud Detection & Compliance Monitoring | ||

| Others | ||

| By End-User | Healthcare Providers | |

| Healthcare Payers | ||

| Medical Billing Companies | ||

| Government Firms | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is AI in Medical Coding market growth outlook to 2031?

The AI in Medical Coding size is projected to reach USD 6.30 billion by 2031, expanding at a 13.26% CAGR over 2026-2031.

Which deployment model is most popular for AI coding platforms?

Cloud installations captured 70.13% of spending in 2025 because shared GPU infrastructure lowers upfront costs and accelerates updates.

Where is the fastest regional growth expected?

Asia-Pacific is projected to expand at a 15.63% CAGR through 2031 as India, Japan, and Australia mandate ICD-11 and fund smart-hospital initiatives.

How do ambient scribes complement coding automation?

Voice-based ambient tools convert conversations into structured notes that feed CAC engines, shortening claim cycles by 7-10 days and boosting DRG accuracy.

Page last updated on: